Posted by AGORACOM-JC

at 10:18 AM on Friday, July 26th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

In First, SEC Clears Blockchain Gaming Startup to Sell Ethereum Tokens

U.S. Securities and Exchange Commission has issued a no-action letter to Pocketful of Quarters (PoQ), a gaming startup looking to issue tokens on the ethereum blockchain.

PoQ may legally sell its Quarters tokens to consumers without registering them as securities, the SEC Division of Corporation Finance wrote in its second no-action letter to a company seeking to launch a token sale.

The U.S. Securities and Exchange Commission has issued a no-action

letter to Pocketful of Quarters (PoQ), a gaming startup looking to issue

tokens on the ethereum blockchain.

PoQ may legally sell its Quarters tokens to consumers without

registering them as securities, the SEC Division of Corporation Finance wrote in its second no-action letter to a company seeking to launch a token sale. (The first was granted in April to TurnKey Jet, a business-travel startup.)

Quarters are built according to the ERC-20 standard – the first such token to receive U.S. regulatory approval.

In the July 25 letter, Jonathan Ingram, chief legal officer for the SEC’s FinHub wing, wrote:

“Based on the facts presented, the Division will not recommend

enforcement action to the Commission if, in reliance on your opinion as

counsel that the Quarters are not securities, PoQ offers and sells the

Quarters without registration under Section 5 of the Securities Act and

does not register Quarters as a class of equity securities under Section

12(g) of the Exchange Act.â€

“The thing that’s notable here, this is the first ERC-20 public

blockchain token [approved for a sale],†said Lewis Cohen of DLX Law,

which worked with PoQ to secure the letter.

The token is a stablecoin, with PoQ setting the price of the Quarters

as the only seller, PoQ CEO George Weiksner said. This is part of the

company’s compliance requirement with the SEC. (A smart contract

prevents tokens from being sent to unapproved accounts, thereby

restricting secondary trading.)

PoQ also raised money through a registered securities sale using an

investment token, which will remain separate from the Quarters sale.

The two-token system is meant to ensure that users conduct

transactions with Quarters, rather than hold them in the hopes of

securing a return, Weiksner explained.

He said he hopes Quarters will improve the gaming experience for

players who are tired of spending large sums for different platforms,

adding:

“It’s a way to make games better.â€

“The most important thing for teenage boys is playing video games and

this might be the first financial product that they have and it’ll be a

crypto wallet,†said Michael Weiksner, the company’s principal (and

George’s father).

PoQ is working with Apple and Google to sell Quarters tokens in the

App and Google Play stores, respectively, the elder Weiksner said.

Launch conditions

The no-action letter requires a PoQ to follow a number of

commitments, including ensuring that players can’t sell, buy or exchange

tokens with each other. Rather, only developer or “influencer†accounts

will be able to transact with players.

“Players can never buy or sell or exchange to anyone except for

approved developers, and that’s a key component of our … [compliance]

strategy,†Michael Weiksner said.

“Accounts are born as regular accounts but they’re restricted, so

they can’t exchange,†he said. “The default accounts are restricted and

only approved accounts can accept Quarters.â€

At present, only PoQ can approve accounts, and there are no concrete

plans to grant other entities the ability to do so, he said. PoQ is

still looking into whether that’s possible.

Developers and influencers will have to pass know-your-customer (KYC)

and anti-money laundering (AML) processes before they can get an

approved account.

According to the letter, Pocketful of Quarters has fully developed its platform and can go live before any tokens are sold.

Moreover, the Quarters tokens “will be immediately usable for their

intended purpose†with PoQ’s gaming platform when the sale begins, and

“only developers and influences with approved accounts will be capable

of exchanging Quarters for [ether] at pre-determined exchange rates by

transferring their Quarters to the Quarters Smart Contract.â€

The SEC’s Ingram warned that “any different facts or conditions might require the Division to reach a different conclusion.â€

“Further, this response expresses the Division’s position on

enforcement action only and does not express any legal conclusion on the

question presented or on the applicability of any other laws, including

the Bank Secrecy Act and anti-money laundering and related frameworks,â€

he wrote.

Reaching this point took PoQ and DLX the better part of a year, Michael Weiksner said.

Cohen told CoinDesk, “we have long championed the importance of

working with, rather than against, regulators, and we believe the

outcome today of this … letter, the first-ever ERC-20 that can be sold

without being a securities offering, I think it’s an incredibly

important point.â€

He concluded:

“It required a lot of patience, and it shows that not every ERC-20

token is a securities offering and it is a positive event in working

with regulators.â€

Posted by AGORACOM-JC

at 10:26 AM on Thursday, July 25th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

The Future Of Banking: Is It All Bitcoin And Blockchain?

At the beginning of July, news broke of Deutsche Bank staff being

sent home as 18,000 job cuts began unraveling before our very eyes. This

news was brought to life with an iconic image of two suited men

carrying their possessions past the doors of a Deutsche Bank branch in

London along with a bag branded “Bitcoins.”

Unfortunately, that image turned out only to be an incredible piece

of timing and coincidence as the men were not now out-of-work bankers

hoofing it from their formal institutional workplace brandishing the

‘future of money,’ on their bags, instead they were tailors walking past

at the right time.

Still, that near-perfect latent image of the finance’s future did

spark a few questions in my mind, and the minds of others. Just how far

are we from a future predicated on Bitcoin and blockchain in banking?

The beginning of the end for banks

To answer this question, I had to look at what is happening in the

world of banking that has led to job cuts and the concerns for the

traditional way of doing things in finance. Living in the United

Kingdom, London is a historical hotspot for banking and the seat of

power for some of the world’s biggest banks.

However, beyond the high-rise glass structures in the city center,

there are signs – usually in the tube stations and bus stops – of a new

way of managing and controlling your money on a day to day basis. No, it

is not Bitcoin – yet – it is the challenger banks.

Challenger banks, as defined,

are: “Small, recently-created retail banks in the United Kingdom that

compete directly with the longer-established banks in the country,

sometimes by specializing in areas underserved by the “big four” banks.”

These banks, also called App-banks, are usually highly customer

focused and made to be as user-friendly and as easy to operate on a day

to day basis as they can. In comparison with traditional banks,

challenger banks try and play to general user frustrations from your big

institutional banks. Sound familiar?

Challenging the legacy

I spoke with Anne Boden, a banking doyen with 30 years experience in

some of the most important financial institutions in the world, and now

the founder and CEO of Starling Bank – one such challenger bank in the UK.

Talking to her about the future of banking was fascinating for

although Boden is aware of Bitcoin, blockchain, and its potential it has

in the banking sector, she believes its time is still far on the

horizon.

In her recently released book, “The Money Revolution” Boden

states: “[Blockchain] is easily the most revolutionary money change on

the horizon and may make a huge difference across the fintech sector.”

BERLIN, GERMANY – NOVEMBER 30: CEO of Starling Bank Anne Boden speaks

on stage during TechCrunch Disrupt Berlin 2018 at Treptow Arena on

November 30, 2018 in Berlin, Germany. (Photo by Noam Galai/Getty Images

for TechCrunch)

Getty Images for TechCrunch

Her thoughts on how traditional banks will need to change and evolve

because of several different factors could easily be viewed in the same

way, but with blockchain and cryptocurrency-tinted glasses

“I spent 30-odd years in traditional banking, I worked for all the

big banks, I worked for Lloyds Bank, Standard Chartered, UBS, Zurich,

and RBS. Then I went into AIG, post-financial crisis, to do the

turn-around and I came to the conclusion that it was easier to start a

new bank than to fix the old,” Boden told me.

Indeed, the banking legacy and way of doing things has become so

stagnant that the wants of the banks and the needs of the customers

almost do not line up anymore – especially on a day to day basis.

Challenger banks are this fresh start customers have been baying for,

but in comparison, cryptocurrencies and blockchain could be an entirely

fresh system.

“In this era, it is people like Atom, Monzo, and Starling that have

come to market, and the ones that have been successful are the ones that

have built their own technology,” Boden added. “All these organizations

have been called challenger banks, but you can only really disrupt when

you have a current account – because people are using that every day –

and when you have your own technology.”

Again, Boden is not necessarily referring to that technology as being

blockchain; however, one can see how blockchain is a prime example of

disruptive technology for the banking sector. The world is changing, and

the way people do everything is different, and this is also down to

technology.

“Customers have changed. Customers are buying music differently; they

are shopping on Amazon; they are doing things very differently,” said

Boden. “Technology has changed. Everyone is wandering around with their

smartphones, these phones have better penetration than the laptop, and

then all the time the regulations are changing as well, and that is a

perfect storm to bring something like Starling to the market.”

Starling is one of several challenger banks that are succeeding at

disrupting the banking hegemony with their customer focus, their

everyday usability, and their own technologies. Their success is indeed a

challenge to institutional financial systems, but because this is a

fast-moving space, there are already challengers to the challenger

banks.

A new weapon in the arsenal

Challenger banks, App-banks, mobile payment companies, merchant

services aggregator, peer-to-peer payments companies, are all financial

services that are looking to take a piece of the pie that traditional

banks have held for so long – and it is not just a UK phenomenon.

Circle, Square, and even Revolut,

which is coming to the USA are also disruptive forces in the financial

space, but what they all have in common is a cryptocurrency offering.

Cryptocurrency may be a long way off from being as popular as the Pound

or the Dollar in regards to payments, but some of these companies are

still offering the chance to use this alternative payment method, should

you be so inclined.

This took me to the offices of two other App-banks in the UK, Wirex, and Zeux.

Both companies operate as an alternative banking solution, allowing for

payments and money transfers, but they also each have cryptocurrency

offerings as well.

These offerings are of course not going to be nearly as popular as

the general fiat services of Starling, for example, but they are not

supposed to be – as yet.

“App-banks, or digital banks, are making things more convenient for

everyday customers to manage their banking, “Frank Zhou, CEO of Zeux,

told me. “There are a lot of needs in the early adopter space who are

interested in cryptocurrency, from trading, investing, using it for

payments. Those types of customers are easier to reach as they follow

the newest developments and are willing to give it a try,”

Pavel Matveev, one of the founders at Wirex, explained that the use

of cryptocurrencies need not only be for experimenting though. There are

tangible use-cases within the payment sphere already.

“While App-based and digital banks offer a more convenient means of

managing money, they are still largely based on conventional payment

infrastructure. This means that cross-border payments still take 3-5

days to settle and command relatively high fees,” said Matveev

“Decentralised digital currencies have the potential to revolutionize

many aspects of the payments industry due to their transparency,

mobility, and ease-of-use,” added Dmitry Lazarichev, also of Wirex.

“One of the most significant areas is international remittance.

Cross-border crypto transactions are significantly faster than

conventional methods of transferring money abroad and require very

little in the way of fees and charges.”

Different offerings

What Matveev and Lazarichev, as well as Zhou, had to say about

including cryptocurrencies into the new era of banking, reminded me of

Boden’s view for the future of the industry. The hopes of the two

crypto-offering App-banks is that they can fill small niches for people

with this new technology, and for Boden, the view is that traditional

banks will face stiff competition in these small niches of finance

services.

“What is going to happen is other things happening in the environment

will catch up with the banking industry, they will surprise the banking

industry,” said Boden “The combination of 5G internet of things,

self-driving cars, AI and machine learning will change the profile of

how payments are made.”

“So I think that the nature of payments will change and you will get

new entrants providing some of those new payment mechanisms, and I think

in that environment the incumbent banks will find it harder to compete.

Some will survive and mutate to something relevant, and many of them

will die.”

If cryptocurrency is to become one of those new payment mechanisms,

getting an early foot in the door is vital, but even more important is

offering a service that is usable. Zeux may see this as using

cryptocurrency for general payments, while Wirex could believe

remittances are key for the digital currencies; neither is more right

than the other and perhaps that is the point – there will be a bevy of

offerings in the future.

“Like previous studies of mass adoption, it happens when the majority

can use it as easily as they would use it normally. For example, from

cash to PIN card, Pin card to contactless cards, contactless to mobile

payment. An easy-to-use experience is key to bringing adoption,” said

Zhou.

“I think the market is ready for crypto mass adoption. But, there

needs to be a solution before the mass demand surfaces. Once all the

customers know they can spend their cryptos easily everywhere in any

shops, it increases their willingness to accept cryptos as payment in

the first place. Mass adoption only happens after the solution appears,

not before.”

A changing future

The banking world has, for almost the last century, continued in

pretty much the same way with little to no threat from alternatives.

That is all changing. People would like to believe that the power of

blockchain in the financial system, and the option of cryptocurrencies,

are about to shake up the entire banking space, but they would be

wrong.

There is little doubt that banking will start to incorporate

blockchain, as Boden explains: “I think that blockchain is likely to be

used in certain aspects of the banking business, so probably for trade

finance where you have lots of parties collaborating on a transaction,

but I think you will see blockchain implementation in niche areas of the

business, you won’t see it as a wholesale change for the banking

platform.”

However, for an entire, legacy-based industry of such a traditional

magnitude to overhaul its entire system for a nascent technology is

foolhardy.

In saying that, cryptocurrencies will start to gain more mass appeal.

This does not mean these two sides of the same industry will be what

changes the face of banking. Still, the face of banking is changing, and

that is why traditional banks that are oblivious to this are starting

to show cracks.

Everyday usage of money and payments is already on the march, and

because of the needs of customers, there is an emerging market of

challenger banks, app-banks, financial institutions and payment

facilitators in the wings. Some are already offering blockchain and

crypto services, some may do so down the line, but to say that the only

way to the future of banking is with blockchain and crypto is

short-sighted – there are much bigger demands and many more niches to be

filled.

Posted by AGORACOM-JC

at 9:45 PM on Sunday, July 21st, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

As Facebook Struggles For Blockchain Support, A Truly Decentralized Challenger Emerges

So, what is Celo? In a similar fashion to Libra, Celo is at its core a stablecoin platform

This means that the key value proposition of the assets running on top of the platform is that they are immune to the wide swings in volatility that have plagued leading crypto assets in recent years

Creates an opportunity for companies and projects like Celo, which are building pure blockchain-based financial services aimed at linking the nearly 2 billion people in the world that do not have access to bank accounts or the ability to verify their identity

As Facebook Blockchain Lead David Marcus tries to simultaneously use his testimony in front of U.S. lawmakers to restore trust in the company, and convince them that Facebook will not always be the driving force of its Libra project, it is easy to see why some of its key blockchain competitors are enthusiastic about the company’s entrance in the space.

The prevailing belief is that at some point the inherent contractions

in Facebook’s blockchain strategy and the Libra project are going to

become too much to overcome. Of course, this assumes that the project

launches at all, which is not certain given the regulatory scrutiny it

faces around the world.

This creates an opportunity for companies and projects like Celo,

which are building pure blockchain-based financial services aimed at

linking the nearly 2 billion people in the world that do not have access to bank accounts or the ability to verify their identity.

To the point, it is interesting that some of Libra’s first members,

including venerated venture capital firm Andreessen Horowitz and

crypto-unicorn Coinbase, have invested in Celo. Some of Celo’s other high-profile investors include LinkedIn founder Reid Hoffman and Twitter/Square CEO Jack Dorsey.

Understanding Celo

So, what is Celo? In a similar fashion to Libra, Celo is at its core a

stablecoin platform. This means that the key value proposition of the

assets running on top of the platform is that they are immune to the

wide swings in volatility that have plagued leading crypto assets in

recent years. Many are designed to mirror the price movements of

traditional currency, and most have names that reflect their fiat

brethren, such as the Gemini Dollar. This is a critical need for the

industry, as no asset will be able to serve as a currency if it does not

maintain a consistent price.

A man walks past signs advertising money transfer services and loans

outside a business in Mexico City, Tuesday, April 5, 2016. (AP

Photo/Rebecca Blackwell)

ASSOCIATED PRESS

However, rather than being a centralized issuer that supports the

price pegs with fiat held in banks, Celo has built a full-stack platform

(meaning it developed the underlying blockchain and applications that

run on top), that can offer an unlimited number of stablecoins all

backed by cryptoassets held in reserve.

Furthermore, Celo is what is known as an algorithmic-based stablecoin

provider. This distinction means that rather than being a centralized

entity that controls issuances and redemptions, the company employs a

smart-contract based stability protocol that automatically expands or

contracts the supply of its collateral reserves in a fashion similar to

how the Federal Reserve adjusts the U.S. monetary supply. In this vein,

Celo co-founder Rene Reinsberg told me that the company actually

“Maintains overcollaterization via a multi-asset crypto reserve composed

of Celo’s native asset, Celo Gold, and a basket of other crypto assets,

such as bitcoin.†This overcollateralization is important, and common

in crypto lending and stablecoin platforms, because it serves as a

buffer against potential volatility.

Additionally, a key differentiator for Celo from similar projects is

that for the first time its blockchain platform allows users to

send/receive money to a person’s phone number, IP address, email, as

well as other identifiers. This feature will be critical to the

long-term success for the network because it eliminates the need for

counterparties in a transaction to share their public keys with each

other prior to a transaction.

And now today, Celo is open-sourcing its entire codebase and design

after two years of development. Additionally, the company is launching

the first prototype of its platform, named the Alfajores Testnet, and

Celo Wallet, an Android app that will allow users to manage their

accounts and send/receive payments on the testnet.

This announcement and product is intended to be just the first of

what will be a wide range of financial services applications designed to

connect the world.

A Bright Outlook But Significant Question Remain

With all of that said, the company’s near and long-term success will

depend on its ability to navigate and address some key hurdles. Three in

particular immediately come to mind:

Stability of the Network. There are currently no

algorithmic/smart-contract based stablecoins in circulation today that

have seen widespread adoption. There are multiple reasons for this.

First, it is simpler to issue stablecoins on a 1:1 basis for fiat kept

in reserves. Second, it is nearly-impossible to design a complex system

that can account for and overcome any threat or challenge. It is likely

that at some point the future the network’s governance structure will be

challenged or that a critical flaw will be discovered in the underlying

code. The platform’s ability to rebound from these challenges without

compromising its decentralized nature will be a key determinant of its

future.

Ability to Adapt to Highly Volatile Fiat. A key

differentiator between Celo and other stablecoin issuers is that anyone

that participates in its governance function can propose a new currency.

The intention is that the platform will support a wide range of global,

national, and local currencies. Given that it is first targeting users

in the developing world, where the currencies are notoriously volatile,

there is a chance that the system could be strained as it seeks to

maintain constant pegs across the network. It is worth noting that the

company has given great thought and care to ensure that it is anti-fragile, and part of this strategy involves using a diverse basket of collateral to support all assets on the network.

Regulation. If the Libra hearings in front of Congress

proved nothing else, lawmakers are very concerned about crypto being

misappropriated for illicit uses. All issuers will need to comply with

existing AML/KYC laws. I asked Rene about this challenge and whether or

not their ability to comply will be hindered by the firms ability to

onboard users with little more than a phone number or some other

numerical identifier. His response was, “Yes, we’ve had conversations

with regulators both in the US and around the world. We think regulation

is critical for this space, particularly when it comes to protecting

consumers. We will absolutely comply with US laws and laws around the

world. We’re looking forward to sharing more on this at a later stage,

closer to mainnet launchâ€

Conclusion

There is a saying “nothing worth having comes easyâ€, and that

certainly applies to Celo and its diligent approach to development.

Additionally, the irony of its launch’s juxtaposition with the Libra

hearings underscores the need for a decentralized approach to connecting

the world.

Posted by AGORACOM-JC

at 2:00 PM on Thursday, July 11th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

‘Google Coin’ Within 2 Years as FANGs Will Go Crypto, Say Winklevoss

Speaking about Facebook Libra, the twins, who co-founded cryptocurrency trading platform Gemini, said it was only a matter of time before other tech giants followed suit.Â

Speaking about Facebook Libra, the twins, who co-founded cryptocurrency trading platform Gemini, said it was only a matter of time before other tech giants followed suit.

FANG refers to the unofficial “Big Four†of the internet: Facebook, Amazon, Netflix and Google.

“Our prediction is every FANG company will have some sort of

cryptocurrency project within the next two years,†Tyler told the

network.

Libra as a payment protocol has not yet launched, but regulators have voiced alarm, particularly in the United States, where several sources have demanded developers halt the project.

Concerns stem from Libra’s potential to bypass the banking system,

something cryptocurrency proponents conversely argue makes the banking establishment overly nervous about losing revenue.

On Thursday, Bitcoin (BTC) itself shed over 10% of its value after a senior U.S. lawmaker delivered fresh concerns about Libra.

For the Winklevosses, however, front-door approaches to regulators is key in getting any disruptive finance offering to market.

Though many say it is not a cryptocurrency at all, the twins even

suggested they would facilitate trading of Libra on Gemini, should it be

open and not subject to prohibitive restrictions.

“We’ll evaluate Libra in earnest, and it might actually be an asset

that is one day listed if it’s an open protocol; that’s possible,†Tyler

continued.

Earlier this week, Tom Lee,

a serial Bitcoin advocate, delivered a similar forecast regarding tech

giants’ future involvement in the digital currency industry.

“The fact that Facebook and likely other FANG companies are going to

create their own digital currencies is validating the idea that digital

money is here to stay,†he told CNBC.

Posted by AGORACOM-JC

at 12:00 PM on Tuesday, July 9th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

Major Improvements Are Coming To Blockchain In 2020

Everyone in the enterprise world already has a blockchain strategy.

If they don’t have one now, they risk the chance of staying behind or simply missing an opportunity.

Everyone in the enterprise world already has a blockchain strategy.

If they don’t have one now, they risk the chance of staying behind or

simply missing an opportunity. For the last few years, the benefits and

correlated risks of fully adopting blockchain technology have been

estimated, analyzed, and discussed at large. One thing is clear –

despite the potential for a big upside, embracing a newly developed

technology presents numerous risks that shouldn’t be underestimated.

Blindly introducing new technology stack into an already working

production environment means exposing that environment to potentially

dangerous security breaches, hacks and data loss.

So, where we are now? Most blockchain protocols claim some level or

maturity … but are they, in fact, sufficiently mature? Are they ready

for full on-premise deployment in large-scale enterprises? Will CIOs and

other business executives enjoy the same comfort as that of the tooling

they already have? Let’s review what it takes to move a blockchain

protocol from open source to enterprise.

It’s no surprise that the largest cloud providers are also the largest drivers of the Blockchain as a Service (BaaS) model. Let’s call them Tier 1 BaaS

providers. They have already established themselves as market leaders

with large customer bases. Offering various cloud services and expanding

to blockchain seemed to be a logical and evolutional step.

Microsoft Azure

Microsoft is one of the largest players in the BaaS space. So far, it

has focused primarily on Ethereum but also offers services for running

R3’s Corda and Hyperledger Fabric networks. It has dedicated many

resources to building the Azure Blockchain Workbench and Azure Blockchain Service. Microsoft’s team is also a key founder and an active participant in the Ethereum Enterprise Alliance

(EEA) and Token Taxonomy Initiative (TTI). In addition, it has recently

joined the Hyperledger family, for which it will contribute to the code

and promise be an active member.

Amazon Web Services (AWS)

AWS and Microsoft Azure have almost equally split control of the

managed blockchain space, though your niche will determine which of

these services you use. If you are into financial services, you would

probably use Azure, but if you are into healthcare, insurance, or other

verticals, your choice is probably AWS. Recently, AWS has made publicly

available its Managed Blockchain

offering. It supports only Hyperledger Fabric for now but there are

plans to integrate Ethereum too. AWS has also invested in the

development of Amazon Quantum Ledger Database (QLDB), which is an append-only database with a cryptographically verifiable transaction log.

IBM Cloud

IBM is one of the primary maintainers of Hyperledger Fabric’s source

code and, thus, is heavily involved in providing cloud services and

product updates for it. Lately, IBM has opened its IBM Blockchain 2.0 to

be multi-cloud, which means you can run your Fabric network across

various cloud providers.

Oracle Blockchain

The Oracle blockchain platform

has based its solution only on Hyperledger Fabric, which is not ideal

but offers some neat services like enhance node provisioning, blockchain

explorer and improved security.

VMWare

VMWare clearly saw the issues that affect the current blockchain infrastructure. It is working to resolve these issues with Concord, a highly scalable and energy-efficient distributed trust infrastructure for consensus and smart contract execution.

VMWare Blockchain

VMWare

Apart from the major cloud providers, in 2018 we saw the birth of

Blockchain as a Service companies that base their products on top of

existing cloud computing platforms; let’s call them Tier 2 BaaS.

They are usually smaller, more agile startups that can push new

offerings almost every month. This makes them very good choices for a

faster go-to-market strategy. Their solutions are wide and colorful, and

they usually cover different blockchain protocols. They remain unable

to address most enterprise needs yet, but they will stay on the right

track and be an attractive option as long as the establishment doesn’t

disrupt them. The names that stand out in this category are Kaleido and Blockdaemon.

What are the enterprise needs from a blockchain perspective? Where do

we want to see improvements so that we can fully use the benefits of

decentralized ledger technology? Let’s separate the main requirements

into four categories: platform; interfaces; infrastructure and network;

and security and analytics.

Platform

Operational resilience – ability to maintain uptime and connectivity

even when some components fail, including several layers of protection

and failover strategy against data loss and corruption.

Pluggable consensus – ability to switch the consensus mechanism

depending on the requirements without rebuilding the whole network.

Broader off-chain data storage capabilities – support for encrypted data storage.

Adaptors to allow for SQL-based ledger queries, which will make the

broader developer community more comfortable working with blockchain.

Interfaces

Enterprise integrations – pre-built modules and onramps for existing enterprise systems.

Robust Oracles – ability to get real-time external data into smart contracts.Watch out for Chainlink.

Integration with GraphQL, a

Facebook-developed language that provides a powerful API to get only the

dataset you need in a single request, seamlessly combining data

sources.

Identity federation – ability to authenticate with existing identity

providers, which will facilitate faster adoption on the consortium

level.

Built-in privacy and permissioning features – for transactions, accounts, wallets, smart contracts and network participants.

Infrastructure and Network

Ability to maintain peak performance at the network level – managing

and operating hundreds of thousands of nodes while maintaining low

latency and facilitating hundreds of thousands of transactions with

guaranteed finality.

Ability to scale and reduce network size on demand – auto-scale a network by adding/removing more validators or orderers.

DevOps tools to make integration with existing IT systems easier and to make CI/CD build processes faster and seamless.

Support for cross-network interoperability and cross-blockchain atomic swaps.

Governance framework with an established and pre-determined

transparent structure, rules of participation, a funding model, and

financial incentives.

Enhanced Security and Analytics

Detailed privacy controls over data, smart contract execution, and transaction visibility.

Improved network monitoring with enhanced contextual meaning of the transactions, ability to troubleshoot on-chain events.

SLA monitoring with backward compatibility of upgrades.

Warehousing transaction history data, combining them with other

off-chain data sources and making them available for BI reporting tools

and other interactive dashboards.

As discussed, the blockchain technology stack has a long way to go

before it will be mature enough for mainstream enterprise adoption. This

is a completely normal process, as software developers and business

leaders transition their mindsets from the currently siloed and

centralized infrastructure to the distributed ledger networks. Luckily,

we are at the forefront of this technological revolution and have the

chance to contribute to what, one day, will be the norm.

Posted by AGORACOM-JC

at 9:00 PM on Sunday, July 7th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

—————-

Crypto Conference Shows Bitcoin Getting Whole Lot More Fun Again

People want to see high volatility, exchange founder says

As little as six months ago, Bitcoin was moribund, with prices

languishing at a fifth of their record high, disappointing a mass of

cryptocurrency enthusiasts who had grown use to extreme — and often

upwards — moves in the virtual currency.

But this week’s Asia Blockchain Summit in Taipei highlighted how

volatility is back, reviving the excitement around crypto trading.

“Bitcoin is fun, but it’s a hell of a lot more fun at 100 times

leverage,†said Arthur Hayes, the founder and chief executive officer of

the exchange BitMEX. “That’s what people want to see in crypto, they

want that high volatility,†he said. “At the end of the day, we’re all

in the entertainment business of traders.â€

The Taipei conference was the

second annual iteration of an Asia forum that brings investors together

with start-ups, financial services providers, academics and others to

engage on the blockchain technology that powers digital coins.

A person in a Bitcoin costume wanders through the Asia Blockchain Summit in Taipei on July 3.

Photographer: Joanna Ossinger/Bloomberg

“We’re surfing a wave here that’s very linked to the price of Bitcoin

and probably has taken a couple months to filter through,†said

attendee Vincent Alibert of ZVChain, a business-to-business blockchain

project, in an interview. “We don’t see any more of these revolutionary

ICO pitches,†he said, referring to initial coin offerings, which have

generally lost favor after many tokens lost more than 90% of their value.

A Bitcoin – or rather, someone dressed as one – wandered around the

venue. The chairs in the conference hall had covers from crypto.com:

“Get 8% p.a. on your Crypto,†they declared. Much of the conference was

spent on Facebook Inc.’s plans to launch the new Libra cryptocurrency,

which proponents say will spark more mainstream interest in virtual

currencies.

“It’ll definitely bring more people into the space,†said Charlie Lee, the creator of Litecoin, speaking on a panel.

Tron, which bills itself as the largest decentralized ecosystem in

the world, displayed a giant poster near the registration area about CEO

Justin Sun winning the annual charity lunch with Berkshire Hathaway’s

Warren Buffett. The successful bid of $4,567,888 featured prominently.

Posted by AGORACOM-JC

at 10:04 AM on Thursday, July 4th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

—————-

4 crypto trends for the next 5 years

Not long ago, only a handful of accountants dealt in cryptocurrency.

Now, just a few years later, every major financial news outlet dedicates

a portion of its coverage to crypto. Times have changed quickly, so

what will the crypto accounting industry look like in five years and

beyond?

Consider the following four trends in crypto accounting and how they will affect CPAs.

1. Increased automation

As cryptocurrencies further infiltrate the public consciousness,

traditional accounting services will automate more of their work to keep

up with the increased workload. Spreadsheets work well enough for fiat

transactions, but in the volatile crypto environment, static tools can’t

effectively serve anyone with a serious investment in alternative

currencies.

Average consumers today can do their taxes online

through services like TurboTax and H&R Block. Businesses and complex

individual situations require personalized care, but standard programs

can handle the load for most people. Tax programs don’t need to offer

advanced functionality just yet — a few equations on the back end do a

fine job.

But cryptocurrencies make things more complicated.

Accountants need automated tools to track increased crypto complexity,

like cost basis. Without smarter software, experts in the financial

services industry won’t be able to keep up with higher sophistication at

scale. Tax software providers will eventually offer new and highly

automated services for crypto investors, and consumers will pay for

those services using their crypto investments.

AI accountants

Accounting experts will use smarter tools to help their corporate

clients and major investors make better decisions. But the public won’t

need real accountants for their simple crypto investments; they’ll

simply turn to artificial intelligence tools that minimize human

interaction in most accounting scenarios.

The future will see

consumers interact with intelligent AI, machine learning, and bots

capable of natural language processing. Challenging concepts like crypto

cost basis, which can confuse even the sharpest accountants, pose

little threat to intelligent software. Accountants will still have a

place in the world, but their duties will evolve drastically as crypto

demands bring widespread change in the financial industry.

Not

everyone will feel comfortable doing taxes through AI. Accountants will

need to lean on automated tools of their own to keep pace, but

enterprise clients, heavy investors, and people suspicious of advanced

tech will continue to prefer the human touch. With more money going

toward nicer tools and less money going toward human intermediaries,

accountants must specialize and adapt to stay relevant.

3. Knowledge enrichment

Schools and universities will soon offer programs and specialty courses

to educate future accountants, bookkeepers, and CPAs on the intricacies

of crypto. Few schools today offer such services, but the more prominent

cryptocurrencies become, the greater the need will be for new

accountants to understand the rules of digital currency.

Some businesses already offer services to certify accountants

as crypto tax experts, but schools will remain the top trainers in the

accounting world. By educating students before they begin their careers,

universities can prepare graduates to operate effectively in an

industry with broad new responsibilities and expectations. Businesses

and crypto organizations will need new accountants who understand their

evolving needs.

For accountants already out of school, options

for continuing education will evolve from useful to essential. More

crypto trading means more crypto investors and crypto companies. Those

entities need experts who understand the cryptocurrency landscape. If

experienced accountants fail to adapt, fresh faces will gladly take the

business.

4. Updated regulatory standards

Where crypto regulation used to be nonexistent, legislators have

actually made some limited progress. The SEC now has more oversight to

shut down illicit initial coin offerings (ICOs), and the IRS clarified

that cryptocurrencies are property, not currency — at least for now.

But

the more that crypto changes, the more regulations will change with it.

Every business that deals with cryptocurrency will encounter newer,

more robust laws in the years to come. Soon every company and project

that deals with crypto will need an accountant (or accounting service)

with crypto experience to help navigate the unknown.

As new laws

get passed, businesses will invest more heavily in smarter crypto

accounting solutions. Artificial intelligence and machine learning will

do the heavy lifting while human accountants interpret that data to help

executives make smarter business decisions. More technology startups

will emerge to cater to this growing audience. Before long, crypto

accounting will become an industry unto itself.

These changes may seem like far-off concerns for another year, but crypto accounting — like cryptocurrencies themselves — moves quickly. Expectations and the tools to meet them become more complex and sophisticated each day. Accountants must stay vigilant to keep up with the times, or they risk losing ground to a new generation of crypto-savvy competitors. Â

Posted by AGORACOM-JC

at 9:53 AM on Wednesday, July 3rd, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

—————-

After Experimenting With Bitcoin and Ethereum, DocuSign Is Accelerating its Blockchain Ambitions

Business team two executive shaking hands after a meeting and conference to sign agreement and become partner in the office, results of their successful teamwork, contract between their firms.

Since its founding in 2003, firms of all sizes and industries have relied on the company to streamline the contract process through its best-in class security, identity authentication, user interface, and integration with leading business suites.

Famed cryptographer Nick Szabo may have coined the term “smart

contract†back in 1994, but DocuSign can make a compelling case for

being its true inventor. Since its founding in 2003, firms of all sizes

and industries have relied on the company to streamline the contract

process through its best-in class security, identity authentication,

user interface, and integration with leading business suites. Today

DocuSign has 500 thousand paying customers, and it earned over $700 million in revenue last year.

However, the company is not resting on its laurels and instead is

seeking ways to improve its service offerings, with much of this

experimentation incorporating blockchain technology. Over the last few

years this testing has included trials, demos, and partnerships on both Bitcoin and Ethereum. The company also joined the Accord Project,

an open-source software initiative that was established to develop a

technology stack for smart agreements. Furthermore, last week the

company invested in a $5.5 million Series A round

for smart contract provider Clause alongside Galaxy Digital with the

goal of making contracts on their DocuSign Agreement Cloud

“self-executing†and “self-aware†in an ongoing fashion, rather than

just one moment in time.

Given the core facets of DocuSign’s business and its research into

blockchain technology and smart contracts, the San Francisco-based

company is in an unrivaled position to assess their utility and

applicability to the needs of today’s businesses. Still, the road to

blockchain adoption has not been a straight line, and the company’s

plans face many of the same hurdles that other potential adopters are

trying to clear. To better understand DocuSign’s future direction, I had

an opportunity to speak with Ron Hirson, DocuSign Chief Product

Officer, who shed additional light on these endeavors, provided context

for the company’s investment in Clause, and offered expectations for how

blockchain will impact the company moving forward.

DocuSign’s Blockchain Strategy Began in 2015

When individuals think of major enterprise users of blockchain, the

first companies that come to mind often include blue-bloods such as

Facebook, IBM, and JP Morgan. However, DocuSign has been experimenting

with the technology since 2015, when it built a “smart-contract meets smart-asset meets smart-payment†demo with Visa on top of the Bitcoin blockchain.

According to Ron, the collaboration aimed to determine whether they

could utilize Bitcoin so that a user could “buy a car while sitting in

the carâ€, and have it start provided that the buyer’s insurance was up

to date.

Initial Forays Offered a Glimpse of Blockchain’s Potential, but Also Challenges

However, as exciting as these experiments were, neither went

mainstream for reasons that will ring familiar to active followers of

the enterprise blockchain space. According to Ron, the POC with Visa was

primarily an opportunity to learn, and the Bitcoin blockchain was

chosen because it was by far the most prominent platform in 2015

(remember Ethereum did not officially launch until July 30, 2015), even

if it was not tailor-made for this use case. Even then Bitcoin’s

limitations in functionality, data storage, and throughput were well

known to industry observers.

It is perhaps for these reasons that the company joined the EEA in

2018 and built its second project on top of Ethereum. However, despite

more functionality, the pilot did not gain widespread adoption because

customers already felt comfortable with DocuSign serving as a store of

record. Ron made it very clear in his conversations to me that most

customers did not see a need for an independent audit trail. He also

noted that education was not a problem, as he and the company “pitched

this broadly, stood on stage, screamed from the mountaintops, about that

we have this capability, and the uptake from customers who are

interested in it is fairly low because they don’t see the need.â€

Speaking more broadly about DocuSign’s global customer base and

blockchain’s shortcomings to this point, Ron underscored the massive

challenge facing technologists and blockchain enthusiasts. He provided a

hypothetical about a client trying to meet its sales goal before the

end of a quarter. Putting himself in the customer’s shoes he said “I

can’t rely on an open source system that may or may be available, may or

may not have the latency that I need, and oh my gosh it is way too

expensive to store all these files. Plus, there is no compelling UI for

me to engage in these kinds of systems.â€

Undaunted and Moving Ahead With a Clearer Vision

In spite of this feedback, Ron and the rest of the company believe in

the potential that blockchain technology has for its product lines, and

it is continuing to drive forward. However, from these initial

experiments, it became clear to the team at DocuSign that for blockchain

technology to transform their business and deliver client value, the

benefits from the technology must move far beyond “nice to haveâ€. In a

sense, the company would need to find a value proposition that was

unavailable before the invention of blockchain technology.

Rationale for the Clause Investment

It is for this reason that as reported last week it invested in smart-contract technology provider Clause.

The startup has built a promising business by leveraging its platform

to enable users to add smart clauses to documents that automate business

processes, workflows, and digital transactions. What this means in

layman’s terms is that contacts that utilize Clause’s technology can run

in the background until a specified date, time, or event and execute

when a certain condition is met. In my conversations with Ron, he

highlighted a demo that the company unveiled at its annual Momentum 2019

conference last month, whereby this new platform could be utilized to authenticate new drivers for a ride-sharing platform on an ongoing and persistent basis.

This speaks to the true potential of this collaboration. DocuSign is

in many ways the epicenter of complex business processes that take place

behind the scenes when a contract is signed. By incorporating these

“smart clauses†into future contracts a lot of this work can become

automated, removing middlemen such as title or escrow agents, offering a

more streamlined and efficient process for all involve parties to an

agreement all the way through to payment.

An Auspicious Start, but Many Challenges Ahead

It is clear that DocuSign is setting its sights much higher this

time. However, much still needs to be developed regarding this

partnership, including which platforms it will run on, the first use

cases, and an initial set of customers. Within this context it is

important to note that Clause’s code can run on top of any blockchain or

non-blockchain platform. Additionally, the collaborators will still

need to find solutions for the scalability, accessibility, and security

problems noted above, not to mention solving these challenges with the

elegant user interfaces that its customers have come to expect. Being

able to work on top of multiple blockchains should help.

Additionally, the partners will need to find and utilize oracles that

never go down and cannot be hacked or manipulated. For readers

unfamiliar with the term, oracles are data feeds that smart contracts

rely on to determine when a condition is met that would cause the

contract to self-execute. Today, there is no foolproof way to prove the

fidelity of an oracle, and it is a long-standing problem that

blockchains cannot differentiate between good and bad data being fed

into the system. For a partnership like this to truly succeed they will

need to find a solution, which is something that the partners dutifully

acknowledge.

Solving these challenges will require heavy lifting, and in

recognition of the size of this undertaking DocuSign has a product

manager and entire engineering team focused on the technology.

Therefore, it seems unlikely that lack of resources will be an issue,

boding well for the future. After all, the prize is big enough to

justify the cost, because if the collaborators succeed, this partnership

has the potential to impact every industry under the sun.

Posted by AGORACOM-JC

at 10:27 AM on Wednesday, June 26th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

The radical idea hiding inside Facebook’s digital currency proposal

A major goal of the Libra Association, the nonprofit Facebook has created to manage the project’s development, is to use Libra to revolutionize the concept of digital identity.

Relevant passage lives near the bottom of a document meant to explain the role of the Libra Association:

“An additional goal of the association is to develop and promote an open identity standard.

Last week, after months of hype and speculation, Facebook finally revealed its plan to launch a blockchain system, called Libra. Since the launch, most of the attention has focused on Libra coin, the cryptocurrency that will run on the new blockchain.

But tucked away in one of the documents Facebook published is

something that may turn out to be just as important as the coin—if not

more so. A major goal of the Libra Association, the nonprofit Facebook

has created to manage the project’s development, is to use Libra to

revolutionize the concept of digital identity.

The relevant passage lives near the bottom of a document

meant to explain the role of the Libra Association: “An additional goal

of the association is to develop and promote an open identity standard.

We believe that decentralized and portable digital identity is a

prerequisite to financial inclusion and competition.â€

But what is a “decentralized and portable digital identity� In

theory, it provides a way to avoid having to trust a single,

centralized authority to verify and take care of our identifying

credentials. For internet users, it would mean that instead of relying

on Facebook or Google’s own log-in tool to provide our credentials to

other websites, we could own and control them ourselves. In theory, this

could better protect that information from hackers and identity

thieves, since it wouldn’t live on company servers.

The concept (sometimes called “self-sovereign identityâ€)

is something of a holy grail in the world of internet technology, and

developers have been pursuing it for years. Big companies including

Microsoft and IBM have been working on decentralized identity

applications for a while now, and so have a number of startups.

But it’s more than just an internet thing. For the roughly one billion

people around the world without any kind of identifying credentials at

all, such technology could make it possible to access financial services

that they cannot today, starting with things like bank accounts and

loans.

Helping some of those people must be part of what Facebook meant when it said in the Libra white paper

that the new system is intended to “serve as an efficient medium of

exchange for billions of people around the world†and “improve access to

financial services.†In some cases the currency itself might be able to

do that, but in others it’s likely that users will need some form of

identification to access a particular service. That’s probably why

Libra’s developers call an open, portable identity standard a

“prerequisite to financial inclusion.â€

But such a digital identity could go beyond finance, too.

Sharing many kinds of sensitive data using a blockchain—for instance,

health information—might require some form of automated ID check.

Facebook itself already has experience with digital identities.

Facebook Connect lets users log in to third party sites using their

Facebook-verified credentials (you might be using it to access

technologyreview.com right now). But Facebook Connect is risky because

it relies on a central authority, argues Christopher Allen, cochair of the credentials community group

of the World Wide Web Consortium, the most important international

standards body for the web. Trusting one entity with this responsibility

is dangerous because the site could go down or the business could fail.

And Facebook can revoke accounts at will.

But it’s hard to say how decentralized Libra’s new identity

system would be, because Facebook hasn’t revealed anything about what

it’s planning.

For example, there’s the possibility that the digital identity

will only work inside the Libra network, which requires permission to

participate in. Unlike systems like Bitcoin and Ethereum, for which

anyone with the right hardware and an internet connection can join and

help validate transactions, Libra requires its validators to be

identified and approved. Nearly 30 companies have already signed up to

run network “nodes,†and Libra’s developers want to up that to 100 by

the time the platform is supposed to launch for real next year.

Facebook’s main message with the launch of Libra and the Libra

Association appears to be a response to past criticisms of how it

handled personal data. The company appears to be saying “Hey, look,

we’re trying to be more open. We don’t want to be this honey pot of

everyone’s information,†says Wayne Vaughan, co-founder of the Decentralized Identity Foundation,

a consortium of companies all working on aspects of blockchain-based

identity. But if whatever identity standard they might come up with only

works for 100 companies, says Vaughan, “that’s not decentralizedâ€â€”it’s

just a standard for 100 companies. Facebook did not respond to a request

for comment.

Either way, it’s not clear how Facebook and the Libra

Association would overcome some big technical challenges that have held

back blockchain-based identity systems. For one, blockchains are still

hard to use for many people. A problem that is particularly difficult

for identity applications is that if you lose or forget your private

keys, which aren’t easy to manage in the first place, it’s hard to

restore them, says Allen.

Another technical challenge pertains to privacy. How will the

personal identification data be kept separate from financial

transactions? This piece is particularly concerning for privacy

advocates in the context of Libra, given Facebook’s less-than-stellar

track record. And an aversion to financial surveillance fuels much of

the cryptocurrency movement.

“Where you spend your money and who you spend it with and how

much you spend is some of the most private information for people,†says

Vaughan.

On the whole, says Allen, though the technology of

decentralized identity has advanced to the point of several serious

pilot tests, it’s “not anywhere near ready†for adoption by billions of

people around the world. And given what the company has revealed so far,

“I don’t see how Facebook can do it,†he says.

Posted by AGORACOM-JC

at 4:36 PM on Tuesday, June 25th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

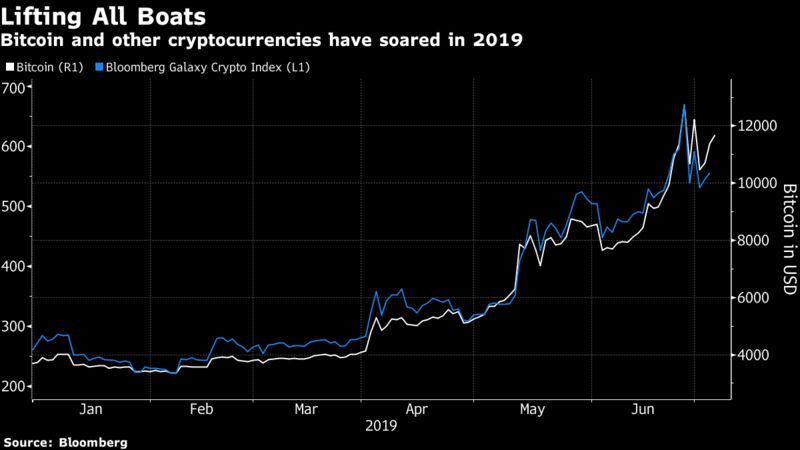

What Bitcoin Breaking $11,000 Means for the Crypto Market’s Future

Bitcoin, which collapsed to a low of $3,100 in December, smashed through the $11,000 mark on Sunday after breaking through the critical $10,000 level.

Both levels were considered highly unlikely only a few weeks ago.

Bitcoin,

which collapsed to a low of $3,100 in December, smashed through the

$11,000 mark on Sunday after breaking through the critical $10,000

level. Both levels were considered highly unlikely only a few weeks ago.

At a price just under $11,000 on Monday evening, the world’s largest

digital coin by market capitalization recovered over half its historic

increase during the peak of the crypto frenzy when it neared $20,000

before crashing almost 75%.

Bitcoin’s continued rise, which is also fueling rallies in Asian

cryptocurrency stocks, illustrates the currency’s resilience in the face

of major skepticism and also cryptocurrency’s widening acceptance by

major established companies such as Facebook Inc. (FB), investment behemoth Fidelity, and others, as outlined in a detailed Bloomberg report.

Crypto Money Has Been ‘Waiting on the Sidelines’

“The bounce back of Bitcoin has been fairly extraordinary,†said

George McDonaugh, chief executive and co-founder of London-based

blockchain and cryptocurrency investment firm KR1 Plc, to Bloomberg just

after the virtual currency breached the key $10,000 level on Friday. It

was the first time that Bitcoin had reached that level in roughly 15

months. “Money didn’t leave the asset behind, it just sat on the

sidelines waiting to get back in.â€

This in part due to renewed mainstream interest in cryptocurrencies

and the distributed ledger technology that it runs on. Facebook’s Libra

is perhaps the highest profile crypto project, as the social media

pioneer partners with companies such as Visa Inc. (V) and Uber Technologies Inc. (UBER) to build the system.

Asian Crypto-Stocks Gain Momentum Alongside Bitcoin Rally

The crypto rally coincided with a rally in related stocks in Asia on

Monday, per another Bloomberg report. In Tokyo, GMO Internet Inc. jumped

7%, while Metaphs Inc. climbed 11%, Remixpoint Inc. 6.2%, and Ceres

Inc. increased 4.4%. In South Korea, Vidente Co. increased 5.4%, and

Woori Technology Investment Co. jumped 4.6%.

Supun Walpola, an analyst with LightStream, attributes gains in Asian

crypto-stocks to Bitcoin’s resurgence. “Going long on stocks that have

exposure to cryptocurrency is something that we have seen in the past

during a Bitcoin/cryptocurrency bull run — especially with those who

want to avoid the volatility of crypto but at the same time want to have

some exposure into these markets,†he said, adding that the increase in

stock prices for these crypto companies typically increase more than

the actual benefit that these firms would get during a crypto surge.

This has “always resulted in immediate corrections,†Walpola wrote in an

email to Bloomberg.

That said, investors should check themselves before investing in

crypto stocks despite their relatively lower risk, given “such

strategies have often gone wrong when crypto markets turn red — which

could happen just about at any time,†said the analyst.

While Bitcoin has eased back below $11,000 it is still dramatically

higher than the $10,000 support level. Bitcoin’s 2019 rebound – and that

of other cryptocurrencies – will be tested by the latest calls by Treasury Secretary

Steven Mnuchin for new global regulatory standards to bring

cryptocurrency “out of the shadows” and to prevent illicit financing by

criminals, terrorists and rogue nations. Crypto bulls say these rules

would hobble the young industry, as outlined in another Bloomberg report.

Looking Ahead

Despite the growing demand for cryptocurrencies and signs that the

long “crypto winter†is over, various headwinds threaten to pull Bitcoin

back below $10,000, likely resulting in a downfall for the rest of the

nascent industry. These risks position the digital coin for continued

volatility as demonstrated in May. Alongside other downside drivers, the

fact that bitcoins are used mostly for speculation, not commerce, has

also been a main concern cited by bears.