Origins and Evolution

Tartisan Nickel Corp., a Canadian-based mineral exploration and development company, has emerged as a pivotal player in the clean energy revolution. The company’s journey began with a vision to explore and develop mineral-rich properties that hold significant value for the burgeoning electric vehicle (EV) market. From its inception, Tartisan Nickel has focused on acquiring and advancing projects with the potential to supply the critical minerals essential for green technologies.

Strategic Acquisitions and Project Development

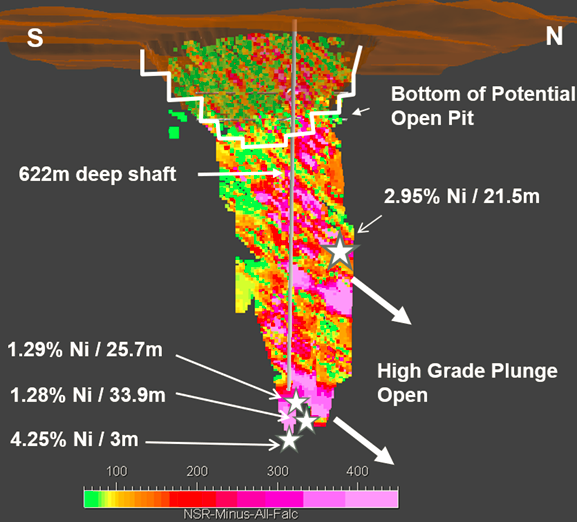

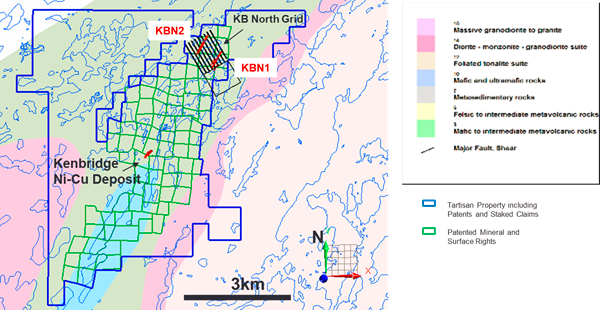

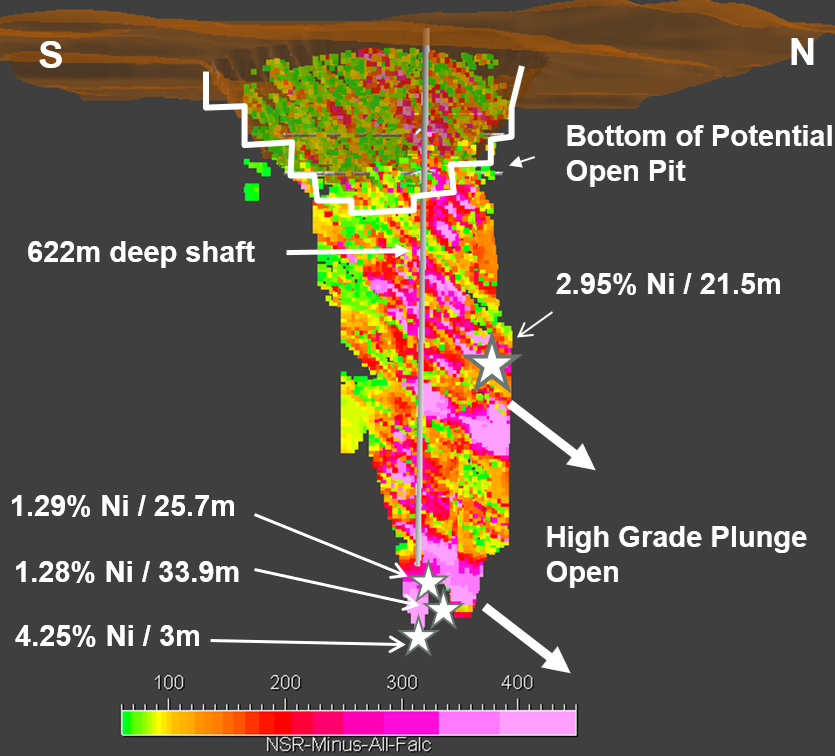

One of Tartisan Nickel’s cornerstone assets is the Kenbridge Nickel Project located in northwestern Ontario. This project, which includes a 622-meter-deep shaft and extensive mineralization, stands as a testament to Tartisan’s strategic vision. By acquiring additional contiguous claims and expanding its property size to cover 4,273 hectares, the company has positioned itself to meet the growing demand for high-purity Class 1 nickel, a crucial component in EV batteries.

The Role of Nickel in the EV Revolution

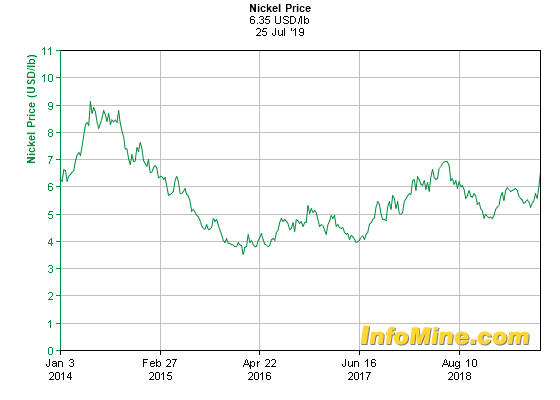

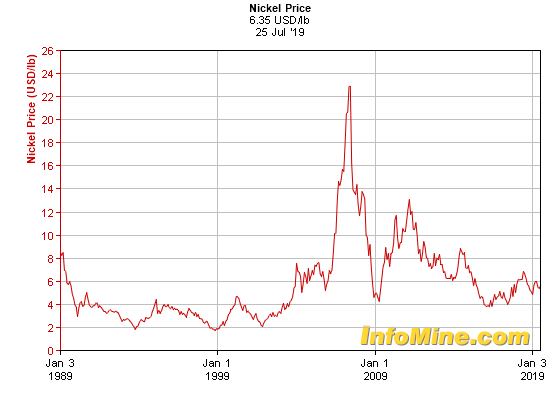

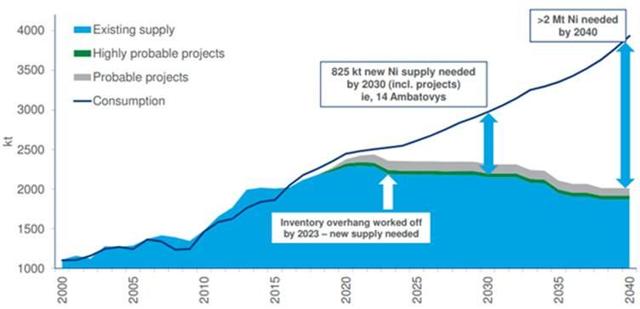

Nickel is indispensable in the manufacture of lithium-ion batteries, which power the majority of electric vehicles. High-purity Class 1 nickel, in particular, is essential for enhancing battery energy density and extending vehicle range. As the EV market continues to expand, the demand for nickel is projected to surge. According to industry forecasts, the global nickel mining market is expected to reach $94 billion by 2033, driven by the escalating demand for EVs and clean energy solutions.

Strong Financials and Resource Potential Bolster Kenbridge Nickel Project

Tartisan Nickel Corp.’s Kenbridge Nickel Project boasts an impressive resource estimate of 7.5 million tonnes grading 0.58% nickel and 0.32% copper, with a contained metal content of 95 million pounds of nickel and 47 million pounds of copper. The Preliminary Economic Assessment (PEA) highlights a robust after-tax NPV of $109 million and an IRR of 20%, supported by a 9-year mine life and low initial capital costs. This positions Tartisan as a key supplier of critical minerals for the EV market.

Environmental and Community Commitment

Tartisan Nickel is not just about mining; it is about sustainable development. The company has partnered with Aspen Biological Ltd. to conduct comprehensive baseline environmental studies. These studies, including aquatic and terrestrial fieldwork, are designed to support provincial and federal reviews, approvals, and permitting for advanced exploration and eventual mine development. Tartisan’s commitment to environmental stewardship ensures that its operations are conducted responsibly, with minimal impact on surrounding ecosystems.

Additionally, Tartisan Nickel is dedicated to fostering positive relationships with Indigenous communities. By engaging in meaningful consultations and incorporating traditional knowledge into its project planning, the company ensures that its operations respect and benefit local communities.

Driving the Clean Energy Transition

As the world moves towards cleaner energy sources, Tartisan Nickel is poised to play a critical role. The company’s high-grade nickel deposits are vital for the production of the lithium-ion batteries that power electric vehicles. By securing a reliable supply of this essential mineral, Tartisan Nickel is helping to drive the global transition to clean energy.

Recent Achievements and Future Prospects

Tartisan Nickel’s recent acquisition of additional claims for the Kenbridge Nickel Project marks a significant milestone in its growth trajectory. The company is advancing its baseline studies and preparing for future exploration activities. These efforts are aimed at unlocking the full potential of the Kenbridge Nickel Deposit and positioning Tartisan Nickel as a leading supplier of critical minerals for the EV industry.

Moreover, Tartisan’s diversified portfolio includes the Sill Lake Silver Property in Sault Ste. Marie, Ontario, and the Don Pancho Manganese-Zinc-Lead Silver Property in Peru. These projects complement the company’s nickel assets and underscore its commitment to supplying a range of critical minerals required for various green technologies.

Conclusion

Tartisan Nickel Corp. has evolved from a visionary mineral exploration company into a key player in the clean energy revolution. By focusing on the development of high-purity nickel resources, Tartisan Nickel is ensuring that it remains at the forefront of the EV market’s growth. The company’s strategic acquisitions, commitment to environmental sustainability, and engagement with Indigenous communities highlight its holistic approach to mining. As global demand for nickel and other critical minerals continues to rise, Tartisan Nickel is well-positioned to contribute to the world’s transition to a greener future.

YOUR NEXT STEPS

Visit $TN HUB On AGORACOM: https://agoracom.com/ir/TartisanNickel

Visit $TN 5 Minute Research Profile On AGORACOM: https://agoracom.com/ir/TartisanNickel/profile

Visit $TN Official Verified Discussion Forum On AGORACOM: https://agoracom.com/ir/TartisanNickel/forums/discussion

DISCLAIMER AND DISCLOSURE

This record is published on behalf of the featured company or companies mentioned (Collectively “Clients”), which are paid clients of Agora Internet Relations Corp or AGORACOM Investor Relations Corp. (Collectively “AGORACOM”)

AGORACOM.com is a platform. AGORACOM is an online marketing agency that is compensated by public companies to provide online marketing, branding and awareness through Advertising in the form of content on AGORACOM.com, its related websites (smallcapepicenter.com; smallcappodcast.com; smallcapagora.com) and all of their social media sites (Collectively “AGORACOM Network”) . As such please assume any of the companies mentioned above have paid for the creation, publication and dissemination of this article / post.

You understand that AGORACOM receives either monetary or securities compensation for our services, including creating, publishing and distributing content on behalf of Clients, which includes but is not limited to articles, press releases, videos, interview transcripts, industry bulletins, reports, GIFs, JPEGs, (Collectively “Records”) and other records by or on behalf of clients. Although AGORACOM compensation is not tied to the sale or appreciation of any securities, we stand to benefit from any volume or stock appreciation of our Clients. In exchange for publishing services rendered by AGORACOM on behalf of Clients, AGORACOM receives annual cash and/or securities compensation of typically up to $125,000.

Facts relied upon by AGORACOM are generally provided by clients or gathered by AGORACOM from other public sources including press releases, SEDAR and/or EDGAR filings, website, powerpoint presentations. These facts may be in error and if so, Records created by AGORACOM may be materially different. In our video interviews or video content, opinions are those of our guests or interviewees and do not necessarily reflect the opinion of AGORACOM.

From time to time, reference may be made in our marketing materials to prior Records we have published. These references may be selective, may reference only a portion of an article or recommendation, and are likely not to be current. As markets change continuously, previously published information and data may not be current and should not be relied upon.

NO INVESTMENT ADVICE

This record, and any record we publish by or on behalf of our clients, should not be construed as an offer or solicitation to buy or sell products or securities.

You understand and agree that no content in this record or published by AGORACOM constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable or advisable for any specific person and that no such content is tailored to any specific person’s needs. We will never advise you personally concerning the nature, potential, advisability, value or suitability of any particular security, portfolio of securities, transaction, investment strategy, or other matter.

Neither the writer of this record nor AGORACOM is an investment advisor. Both are neither licensed to provide nor are making any buy or sell recommendations. For more information about this or any other company, please review their public documents to conduct your own due diligence.

If you have any questions, please direct them to [email protected]

For our full website disclaimer, please visit https://agoracom.com/terms-and-conditions