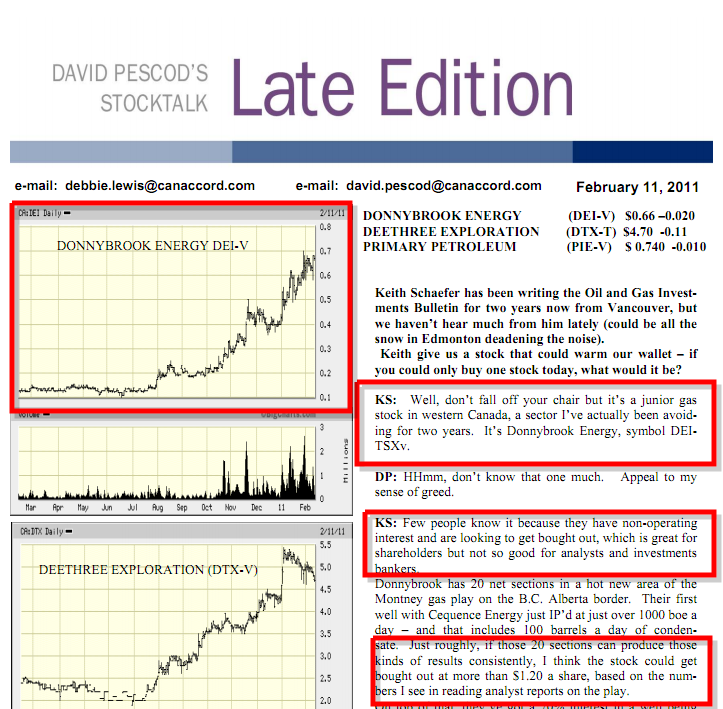

Canadian Small Cap Consolidation Continues - Image Courtesy Of FlashDBA.com

Pursuant to my theme that a Canadian small-cap catharsis is underway … and long overdue … take a look at the huge headline below.

Hats off to the management teams of all 3 companies for this great move.

Pace Oil & Gas, AvenEx Energy and Charger Energy to Combine and Form Intermediate Dividend Paying Corporation

Conversion of natural gas volumes to barrels of oil equivalent (boe) are at 6:1.

CALGARY, ALBERTA–(Marketwire – Dec. 20, 2012) –

NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR DISSEMINATION IN THE UNITED STATES. ANY FAILURE TO COMPLY WITH THIS RESTRICTION MAY CONSTITUTE A VIOLATION OF U.S. SECURITIES LAWS.

Pace Oil & Gas Ltd. (“Pace”) (TSX:PCE), AvenEx Energy Corp. (“AvenEx”) (TSX:AVF) and Charger Energy Corp. (“Charger”) (TSX VENTURE:CHX) announce that they have entered into an agreement (the “Arrangement Agreement”) providing for the combination of Pace, AvenEx and Charger to form a dividend paying corporation to be named “Spyglass Resources Corp.” (“Spyglass”). Spyglass will have a balanced commodity profile and sustainable business model underpinned by 18,000 boe/d of stable, low decline oil and gas production and will be led by an experienced management team.

The merger will be completed through an amalgamation of the three parties (the “Merger”) on the basis of 1.30 Spyglass shares for each outstanding common share of Pace (the “Pace Shares”), 1.00 Spyglass share for each outstanding common share of AvenEx (the “AvenEx Shares”) and 0.18 Spyglass shares for each outstanding Class A share of Charger (the “Charger Shares”). The exchange ratios represent a value of $4.32 for each Pace Share, $3.32 for each AvenEx Share and $0.60 for each Charger Share based on the closing price for AvenEx on December 19, 2012.

In conjunction with the Merger, AvenEx has reached a binding agreement for the sale of its Elbow River Marketing business (the “Elbow River Sale”) for aggregate cash proceeds of $80 million, subject to regulatory approvals, customary closing conditions and adjustments. The Elbow River Sale is expected to close by mid-February 2013.

Spyglass will have approximately 129 million common shares outstanding upon completion of the Merger and, subject to receipt of the final approval of the TSX, will be listed on the TSX under the symbol “SGL”. Spyglass will be managed by the current Charger team, led by Tom Buchanan as CEO (former President and CEO of Provident Energy Trust) and Dan O’Byrne as President (former COO of Provident Energy Trust). The Board of Directors of Spyglass will consist of 8 members with nominees from each party including Randy Findlay as Chair, Dennis Balderston, Tom Buchanan, Gary Dundas, Mike Shaikh, Jeff Smith, Fred Woods and John Wright.

“We are very pleased to introduce a new dividend-paying intermediate oil and gas producer to the Canadian market,” said Tom Buchanan, Chairman and CEO of Charger. “The combined asset base features mature, low decline properties and a balanced commodity profile coupled with the light oil development opportunities needed to sustain the model. The management team has previously operated the majority of the assets that are being contributed to Spyglass and has a proven track record in respect of the execution, financial and operational discipline that is required to sustain a cash-distributing entity.”

Dividend Policy

Upon closing, Spyglass will implement a monthly dividend of $0.03 per share with a dividend payout of 35% to 40% of cash flow (approximately $46 million annual dividend) and a target all-in payout ratio (including $80 to $90 million of sustaining capital expenditures) of approximately 100% of cash flow. The dividend policy will be reviewed monthly and is based on a number of factors including current and future commodity prices, foreign exchange rates, an active commodity price hedging program, status of current operations and future investment opportunities. Each dividend declaration will be confirmed by Spyglass in a monthly news release. Spyglass will consider implementing a dividend reinvestment plan (DRIP) following completion of the Merger.

Key Attributes and Sustainability Criteria of Spyglass

Each of Pace, AvenEx and Charger believe that the Merger will create immediate and long term shareholder value through the introduction of an income and growth company of scale with a low decline, balanced commodity profile and a sustainable dividend. The business model is supported by the following key attributes: (more…)