Posted by AGORACOM-JC

at 10:05 AM on Wednesday, July 31st, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

Crypto Markets See Second Day of Green, Bitcoin Above $9,700

crypto markets are seeing widespread green, with Bitcoin (BTC) breaking back above $9,700 and many large market cap altcoins seeing solid gains of between 3 and 9% on the day.

Wednesday, July 31 — crypto markets are seeing widespread green, with Bitcoin (BTC) breaking back above $9,700 and many large market cap altcoins seeing solid gains of between 3 and 9% on the day.

Despite trading in a lower price range since dropping back to a four-figure price point in a recent corrections, BTC is today up a solid 2.4%, bringing it to $9,717 by press time.

This mild uptick nonetheless stops short of bringing the coin back

into the green on its 7-day chart, where Bitcoin is still reporting a

fractional 0.7% loss. On the month, losses are starker, topping 8%.

Yesterday, Peter Tchir — a former Executive Director at German multinational investment bank Deutsche Bank — argued

that Bitcoin is an indicator of hidden geopolitical tensions, pointing

to the coin’s momentous performance this May at a time of fraught trade

talks between the United States and China.

Also this week, erstwhile Bitcoin bear and CNBC host Joe Kernen predicted that the top coin could hit $55,000 — a 500%+ price surge — by the time of its next halving in May 2020.

Top altcoin Ether (ETH) — which celebrated its fourth birthday

yesterday — has posted a 1.9% to trade around $212 by press time. In

corrections earlier this week, the coin had circled perilously close to

the round $200 mark, but has since recovered ground and is just slightly

in the red, at 2.2%, on its 7-day chart. On the month, however, Ether

is down over 18%.

XRP is

reporting a 2.7% gain on the day, while among the remaining top ten

coins several alts are seeing stronger upward momentum: Bitcoin Cash (BCH) is posting a 7.5% gain on the day, Litecoin (LTC) is up 3.6% and Binance Coin (BNB) is up 4.1%.

In the context of top twenty coins, Tezos (XTZ) is outstripping all

other assets, seeing a 24% gain on the day following news of the token’s

listing on major United States crypto exchange Coinbase. At press time, XTZ is trading at $1.24

Still among the top twenty, strong gains are being reported by Chainlink (LINK) — up over 9% — as well as by NEO (NEO), IOTA (MIOTA) and Cosmos (ATOM), all of which are up by 4-5%.

Total market capitalization for all cryptocurrencies is at $261,434,827,781 at press time, according to Coin360 data.

Dominating the crypto headlines this week is the hearing devoted to

examining regulatory frameworks for cryptocurrencies and blockchain held

at the United States Senate Banking Committee. Cointelegraph reported live on the most important developments during the hearing as it unfolded.

Yesterday’s Committee hearing notably follows upon earlier hearings in mid-July that had examined the regulatory hurdles surrounding Facebook’s Libra.

Posted by AGORACOM-JC

at 3:36 PM on Tuesday, July 30th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

Branson-backed cryptocurrency firm launches a super-fast exchange to take on Coinbase

Blockchain’s exchange is the result of work led by a team of former trading industry executives.

The exchange can execute orders in a matter of “microseconds,†according to CEO Peter Smith.

The firm has raised $70 million from investors including Richard Branson, Alphabet and Lakestar.

Blockchain CEO Peter Smith.

Krisztian Bocsi | Bloomberg via Getty Images

Blockchain, one of the world’s largest cryptocurrency wallet

platforms, says it’s launched a digital currency exchange aimed at

delivering “lightning-fast†trades.

The company’s exchange, called The PIT, is the result of a

behind-the-scenes effort led by a team of former executives from the New

York Stock Exchange, TD Ameritrade, Google and Goldman Sachs.

According to Blockchain CEO Peter Smith, the new exchange’s matching

engine Mercury can execute buy or sell orders in “40 to 50

microseconds,†an “order of magnitude faster than other market playersâ€

like Coinbase and Binance.

Founded in 2011, Blockchain initially started out with what’s known

as a block explorer — kind of like an internet browser for

cryptocurrency data — and then built digital wallets for users to store

and exchange their crypto. It derives its name from the eponymous

blockchain network that records bitcoin transactions.

Having enjoyed popularity with bitcoin enthusiasts — Blockchain

claims to account for about 25% of daily activity on the bitcoin network

— the company is hoping its exchange platform will help lure in the

uninitiated.

“There’s a huge audience of people who have not yet placed their

first bitcoin trade,†Nicole Sherrod, head of trading products at

Blockchain, told CNBC in an interview. Sherrod previously led the active

trading product team at online stock broker TD Ameritrade before

joining Blockchain.

Sherrod said the new trading platform would give investors a degree of liquidity not seen in competitor exchanges.

“In volatile markets in particular, speed is of utmost importance,â€

she said. “I would not feel comfortable delivering a platform to retail

investors that puts them in a position where they couldn’t get in and

out of a trade with lightning-fast speed.â€

Blockchain CEO Peter Smith says the cryptocurrency firm’s new exchange can executive order in a matter of “microseconds.â€

Blockchain

Cryptocurrencies have gained a reputation for their volatile price

swings. Bitcoin in late 2017 skyrocketed to a near-$20,000 record high,

before plummeting the following year to as low as $3,122. The world’s

best-known digital currency has been on the rise this year, however,

last trading at $9,502.

Bitcoin’s rise in 2019 was attributed in part to Facebook’s plans to

create a cryptocurrency, with analysts saying it brings some much-needed

credibility to cryptocurrencies. Facebook’s Libra project has been

panned by regulators, however, concerned by the risks it may pose to

consumers.

One big hurdle for the industry to overcome is bringing institutional

investors with deep pockets on board. That may be slowly starting to

happen, with financial services giant Fidelity signaling it’s warming to the space. Sherrod said that Blockchain’s crypto exchange is providing liquidity through “institutional-level market makers.â€

Blockchain said its exchange will be available in more than 200

countries, starting with 26 trading pairs. Users will be able to link

their bank account with Blockchain and use U.S. dollars, euros and

sterling to trade cryptocurrencies.

The company has raised over $70 million from investors including

British billionaire Richard Branson, Alphabet venture arm GV and early

Spotify backer Lakestar. It has also accrued over 40 million users,

Blockchain said, who will be able to transfer crypto from their wallets

to the exchange.

Posted by AGORACOM-JC

at 11:49 AM on Monday, July 29th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

——————

Blockchain is finally becoming the next-gen database of choice

Image Credit: TimeStopper/Getty

In short, a blockchain is a server that can’t crash and a database that can’t be corrupted — all in one easy to deploy package.

When I think of why we need a blockchain, I think of one guy. There was a dev we had hired to build a few important parts of our product for us. A few years previously, in another life, he had been hosting his own servers and one of them crashed. He was telling me this with tears in his eyes: The database, a massive mess full of customer data, point-of-sale info, and inventory information had gone up in smoke. The backups were hosed, as well. And there was no way to rewind the data.

He spent almost 24 hours in an air-conditioned server room, a monitor

attached to the rack and a keyboard on his knees, trying to resurrect

it. He was partially successful, but the real question was whether the

data was accurate. Whether the transactions all matched up, whether he

would keep his job in the morning.

Everything turned out fine and, since then, it has gotten a lot

easier to do his job. Cloud replaced servers while also being cheaper

and more reliable. His lingering fear never went away though. Things are

better, but he can’t be 100% sure things will never go sideways again.

He believes, though, that there’s a stronger safety net available now

than we’ve had before: blockchain.

Benefits like disaster recovery,

security, availability, and automation are all baked into blockchain.

The serverless architecture of public blockchains makes them powerful

proofs of how blockchain can deliver on enterprise-grade reliability for

business databases. The costs are also not much higher: Blockchain’s

ability to instantly replicate may even allow you to safely get away

with the same (or even less) redundancy compared to a traditional

database. Perhaps the biggest advantage? Smart contracts

will regulate changes, so a new hire can’t throw a wrench into

everything — the blockchain will protect you from changes that could

compromise data or stability.

In short, a blockchain is a server that can’t crash and a database that can’t be corrupted — all in one easy to deploy package.

To be clear, blockchain isn’t perfectly suited to solve certain data

problems, the same way that email isn’t suited for instant messaging.

Big data analytics is crazy expensive to replicate, and unless you are

directly monetizing the data (like selling ads), it is not worth the

cost to shoehorn blockchain into an analytical workload. Blockchains are

best for core business transactional data, like your account balance.

They are absolutely mission-critical when it comes to account data and

ownership records, the loss of which would be an existential threat to a

company. A company like Walmart can probably survive the loss of all

website traffic data, but it would be very much at risk if it lost its

inventory ledger.

Business continuity is a major concern for enterprise players as

customers demand nothing less than always-on availability. As businesses

grow though, the pains of migrating databases and updating systems can

lead to massive fumbles. According to Boston Computing Network’s

research, 60 percent of companies that lose their data will shut down

within six months of the disaster. There exists an entire industry of

SysOps, DevOps, and others who monitor code pushes and database

migrations, giving humans plenty of chances to foul up a launch.

So blockchain represents a big opportunity for businesses to move quickly while keeping their operations secure.

Today, it isn’t just about the speed of transactions, it’s also about

verifying and securing those transactions. That’s what has always been

missing in system management and is something that anyone from our

beleaguered dev to the teams that run databases for Twitter, Facebook,

and LinkedIn are learning.

Blockchain tech is the evolution of the database. Smart contracts

enforce business rules, while databases are backed up and verified

continuously. All of the infrastructure and computational needs are

calculated before deployment, and embedded rules ensure compliance from

day one onward.

In fact, it looks a lot like the next generation of what APIs look

like. You’re encapsulating processes, tying them together with requests

for data, and expecting results. Right now, the business logic is

processed on central servers of some kind. What’s innovative with

blockchain is that you can take that logic, wrapped as a smart contract,

and run it on your own. It still adheres to the rules set by the people

who created it, and it must interact as expected.

Now, imagine databases on blockchain using these same robust rules.

Robust databases that are unkillable. You don’t have to worry about your

main server going down. Replication is built-in. Immutable laws exist

that you can’t lose or change. If you’re on a public blockchain, this is

as robust as possible, and you don’t have to pay for any servers. With a

public blockchain, your data is stored cryptographically by the

blockchain’s miners all around the world. If you’re on a private

blockchain, you may run several replicated systems. Or, you can own all

the nodes. You can also use blockchain on cloud platforms like Amazon

Web Services and Microsoft Azure. The key is that blockchain is built to

be replicated, again and again. Traditional databases must be migrated

in specific, expensive ways under certain conditions to guard against

data loss.

Ultimately, this is where blockchain really proves its worth:

combining the basic elements of security, robustness, replication, and

business logic all in its “DNA.†Smart contracts are safe, distributed,

and secure. Your entire dataset is more secure this way, too. This is

why blockchain promises to be the next-generation database.

Posted by AGORACOM-JC

at 10:18 AM on Friday, July 26th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

In First, SEC Clears Blockchain Gaming Startup to Sell Ethereum Tokens

U.S. Securities and Exchange Commission has issued a no-action letter to Pocketful of Quarters (PoQ), a gaming startup looking to issue tokens on the ethereum blockchain.

PoQ may legally sell its Quarters tokens to consumers without registering them as securities, the SEC Division of Corporation Finance wrote in its second no-action letter to a company seeking to launch a token sale.

The U.S. Securities and Exchange Commission has issued a no-action

letter to Pocketful of Quarters (PoQ), a gaming startup looking to issue

tokens on the ethereum blockchain.

PoQ may legally sell its Quarters tokens to consumers without

registering them as securities, the SEC Division of Corporation Finance wrote in its second no-action letter to a company seeking to launch a token sale. (The first was granted in April to TurnKey Jet, a business-travel startup.)

Quarters are built according to the ERC-20 standard – the first such token to receive U.S. regulatory approval.

In the July 25 letter, Jonathan Ingram, chief legal officer for the SEC’s FinHub wing, wrote:

“Based on the facts presented, the Division will not recommend

enforcement action to the Commission if, in reliance on your opinion as

counsel that the Quarters are not securities, PoQ offers and sells the

Quarters without registration under Section 5 of the Securities Act and

does not register Quarters as a class of equity securities under Section

12(g) of the Exchange Act.â€

“The thing that’s notable here, this is the first ERC-20 public

blockchain token [approved for a sale],†said Lewis Cohen of DLX Law,

which worked with PoQ to secure the letter.

The token is a stablecoin, with PoQ setting the price of the Quarters

as the only seller, PoQ CEO George Weiksner said. This is part of the

company’s compliance requirement with the SEC. (A smart contract

prevents tokens from being sent to unapproved accounts, thereby

restricting secondary trading.)

PoQ also raised money through a registered securities sale using an

investment token, which will remain separate from the Quarters sale.

The two-token system is meant to ensure that users conduct

transactions with Quarters, rather than hold them in the hopes of

securing a return, Weiksner explained.

He said he hopes Quarters will improve the gaming experience for

players who are tired of spending large sums for different platforms,

adding:

“It’s a way to make games better.â€

“The most important thing for teenage boys is playing video games and

this might be the first financial product that they have and it’ll be a

crypto wallet,†said Michael Weiksner, the company’s principal (and

George’s father).

PoQ is working with Apple and Google to sell Quarters tokens in the

App and Google Play stores, respectively, the elder Weiksner said.

Launch conditions

The no-action letter requires a PoQ to follow a number of

commitments, including ensuring that players can’t sell, buy or exchange

tokens with each other. Rather, only developer or “influencer†accounts

will be able to transact with players.

“Players can never buy or sell or exchange to anyone except for

approved developers, and that’s a key component of our … [compliance]

strategy,†Michael Weiksner said.

“Accounts are born as regular accounts but they’re restricted, so

they can’t exchange,†he said. “The default accounts are restricted and

only approved accounts can accept Quarters.â€

At present, only PoQ can approve accounts, and there are no concrete

plans to grant other entities the ability to do so, he said. PoQ is

still looking into whether that’s possible.

Developers and influencers will have to pass know-your-customer (KYC)

and anti-money laundering (AML) processes before they can get an

approved account.

According to the letter, Pocketful of Quarters has fully developed its platform and can go live before any tokens are sold.

Moreover, the Quarters tokens “will be immediately usable for their

intended purpose†with PoQ’s gaming platform when the sale begins, and

“only developers and influences with approved accounts will be capable

of exchanging Quarters for [ether] at pre-determined exchange rates by

transferring their Quarters to the Quarters Smart Contract.â€

The SEC’s Ingram warned that “any different facts or conditions might require the Division to reach a different conclusion.â€

“Further, this response expresses the Division’s position on

enforcement action only and does not express any legal conclusion on the

question presented or on the applicability of any other laws, including

the Bank Secrecy Act and anti-money laundering and related frameworks,â€

he wrote.

Reaching this point took PoQ and DLX the better part of a year, Michael Weiksner said.

Cohen told CoinDesk, “we have long championed the importance of

working with, rather than against, regulators, and we believe the

outcome today of this … letter, the first-ever ERC-20 that can be sold

without being a securities offering, I think it’s an incredibly

important point.â€

He concluded:

“It required a lot of patience, and it shows that not every ERC-20

token is a securities offering and it is a positive event in working

with regulators.â€

Posted by AGORACOM-JC

at 10:26 AM on Thursday, July 25th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

The Future Of Banking: Is It All Bitcoin And Blockchain?

At the beginning of July, news broke of Deutsche Bank staff being

sent home as 18,000 job cuts began unraveling before our very eyes. This

news was brought to life with an iconic image of two suited men

carrying their possessions past the doors of a Deutsche Bank branch in

London along with a bag branded “Bitcoins.”

Unfortunately, that image turned out only to be an incredible piece

of timing and coincidence as the men were not now out-of-work bankers

hoofing it from their formal institutional workplace brandishing the

‘future of money,’ on their bags, instead they were tailors walking past

at the right time.

Still, that near-perfect latent image of the finance’s future did

spark a few questions in my mind, and the minds of others. Just how far

are we from a future predicated on Bitcoin and blockchain in banking?

The beginning of the end for banks

To answer this question, I had to look at what is happening in the

world of banking that has led to job cuts and the concerns for the

traditional way of doing things in finance. Living in the United

Kingdom, London is a historical hotspot for banking and the seat of

power for some of the world’s biggest banks.

However, beyond the high-rise glass structures in the city center,

there are signs – usually in the tube stations and bus stops – of a new

way of managing and controlling your money on a day to day basis. No, it

is not Bitcoin – yet – it is the challenger banks.

Challenger banks, as defined,

are: “Small, recently-created retail banks in the United Kingdom that

compete directly with the longer-established banks in the country,

sometimes by specializing in areas underserved by the “big four” banks.”

These banks, also called App-banks, are usually highly customer

focused and made to be as user-friendly and as easy to operate on a day

to day basis as they can. In comparison with traditional banks,

challenger banks try and play to general user frustrations from your big

institutional banks. Sound familiar?

Challenging the legacy

I spoke with Anne Boden, a banking doyen with 30 years experience in

some of the most important financial institutions in the world, and now

the founder and CEO of Starling Bank – one such challenger bank in the UK.

Talking to her about the future of banking was fascinating for

although Boden is aware of Bitcoin, blockchain, and its potential it has

in the banking sector, she believes its time is still far on the

horizon.

In her recently released book, “The Money Revolution” Boden

states: “[Blockchain] is easily the most revolutionary money change on

the horizon and may make a huge difference across the fintech sector.”

BERLIN, GERMANY – NOVEMBER 30: CEO of Starling Bank Anne Boden speaks

on stage during TechCrunch Disrupt Berlin 2018 at Treptow Arena on

November 30, 2018 in Berlin, Germany. (Photo by Noam Galai/Getty Images

for TechCrunch)

Getty Images for TechCrunch

Her thoughts on how traditional banks will need to change and evolve

because of several different factors could easily be viewed in the same

way, but with blockchain and cryptocurrency-tinted glasses

“I spent 30-odd years in traditional banking, I worked for all the

big banks, I worked for Lloyds Bank, Standard Chartered, UBS, Zurich,

and RBS. Then I went into AIG, post-financial crisis, to do the

turn-around and I came to the conclusion that it was easier to start a

new bank than to fix the old,” Boden told me.

Indeed, the banking legacy and way of doing things has become so

stagnant that the wants of the banks and the needs of the customers

almost do not line up anymore – especially on a day to day basis.

Challenger banks are this fresh start customers have been baying for,

but in comparison, cryptocurrencies and blockchain could be an entirely

fresh system.

“In this era, it is people like Atom, Monzo, and Starling that have

come to market, and the ones that have been successful are the ones that

have built their own technology,” Boden added. “All these organizations

have been called challenger banks, but you can only really disrupt when

you have a current account – because people are using that every day –

and when you have your own technology.”

Again, Boden is not necessarily referring to that technology as being

blockchain; however, one can see how blockchain is a prime example of

disruptive technology for the banking sector. The world is changing, and

the way people do everything is different, and this is also down to

technology.

“Customers have changed. Customers are buying music differently; they

are shopping on Amazon; they are doing things very differently,” said

Boden. “Technology has changed. Everyone is wandering around with their

smartphones, these phones have better penetration than the laptop, and

then all the time the regulations are changing as well, and that is a

perfect storm to bring something like Starling to the market.”

Starling is one of several challenger banks that are succeeding at

disrupting the banking hegemony with their customer focus, their

everyday usability, and their own technologies. Their success is indeed a

challenge to institutional financial systems, but because this is a

fast-moving space, there are already challengers to the challenger

banks.

A new weapon in the arsenal

Challenger banks, App-banks, mobile payment companies, merchant

services aggregator, peer-to-peer payments companies, are all financial

services that are looking to take a piece of the pie that traditional

banks have held for so long – and it is not just a UK phenomenon.

Circle, Square, and even Revolut,

which is coming to the USA are also disruptive forces in the financial

space, but what they all have in common is a cryptocurrency offering.

Cryptocurrency may be a long way off from being as popular as the Pound

or the Dollar in regards to payments, but some of these companies are

still offering the chance to use this alternative payment method, should

you be so inclined.

This took me to the offices of two other App-banks in the UK, Wirex, and Zeux.

Both companies operate as an alternative banking solution, allowing for

payments and money transfers, but they also each have cryptocurrency

offerings as well.

These offerings are of course not going to be nearly as popular as

the general fiat services of Starling, for example, but they are not

supposed to be – as yet.

“App-banks, or digital banks, are making things more convenient for

everyday customers to manage their banking, “Frank Zhou, CEO of Zeux,

told me. “There are a lot of needs in the early adopter space who are

interested in cryptocurrency, from trading, investing, using it for

payments. Those types of customers are easier to reach as they follow

the newest developments and are willing to give it a try,”

Pavel Matveev, one of the founders at Wirex, explained that the use

of cryptocurrencies need not only be for experimenting though. There are

tangible use-cases within the payment sphere already.

“While App-based and digital banks offer a more convenient means of

managing money, they are still largely based on conventional payment

infrastructure. This means that cross-border payments still take 3-5

days to settle and command relatively high fees,” said Matveev

“Decentralised digital currencies have the potential to revolutionize

many aspects of the payments industry due to their transparency,

mobility, and ease-of-use,” added Dmitry Lazarichev, also of Wirex.

“One of the most significant areas is international remittance.

Cross-border crypto transactions are significantly faster than

conventional methods of transferring money abroad and require very

little in the way of fees and charges.”

Different offerings

What Matveev and Lazarichev, as well as Zhou, had to say about

including cryptocurrencies into the new era of banking, reminded me of

Boden’s view for the future of the industry. The hopes of the two

crypto-offering App-banks is that they can fill small niches for people

with this new technology, and for Boden, the view is that traditional

banks will face stiff competition in these small niches of finance

services.

“What is going to happen is other things happening in the environment

will catch up with the banking industry, they will surprise the banking

industry,” said Boden “The combination of 5G internet of things,

self-driving cars, AI and machine learning will change the profile of

how payments are made.”

“So I think that the nature of payments will change and you will get

new entrants providing some of those new payment mechanisms, and I think

in that environment the incumbent banks will find it harder to compete.

Some will survive and mutate to something relevant, and many of them

will die.”

If cryptocurrency is to become one of those new payment mechanisms,

getting an early foot in the door is vital, but even more important is

offering a service that is usable. Zeux may see this as using

cryptocurrency for general payments, while Wirex could believe

remittances are key for the digital currencies; neither is more right

than the other and perhaps that is the point – there will be a bevy of

offerings in the future.

“Like previous studies of mass adoption, it happens when the majority

can use it as easily as they would use it normally. For example, from

cash to PIN card, Pin card to contactless cards, contactless to mobile

payment. An easy-to-use experience is key to bringing adoption,” said

Zhou.

“I think the market is ready for crypto mass adoption. But, there

needs to be a solution before the mass demand surfaces. Once all the

customers know they can spend their cryptos easily everywhere in any

shops, it increases their willingness to accept cryptos as payment in

the first place. Mass adoption only happens after the solution appears,

not before.”

A changing future

The banking world has, for almost the last century, continued in

pretty much the same way with little to no threat from alternatives.

That is all changing. People would like to believe that the power of

blockchain in the financial system, and the option of cryptocurrencies,

are about to shake up the entire banking space, but they would be

wrong.

There is little doubt that banking will start to incorporate

blockchain, as Boden explains: “I think that blockchain is likely to be

used in certain aspects of the banking business, so probably for trade

finance where you have lots of parties collaborating on a transaction,

but I think you will see blockchain implementation in niche areas of the

business, you won’t see it as a wholesale change for the banking

platform.”

However, for an entire, legacy-based industry of such a traditional

magnitude to overhaul its entire system for a nascent technology is

foolhardy.

In saying that, cryptocurrencies will start to gain more mass appeal.

This does not mean these two sides of the same industry will be what

changes the face of banking. Still, the face of banking is changing, and

that is why traditional banks that are oblivious to this are starting

to show cracks.

Everyday usage of money and payments is already on the march, and

because of the needs of customers, there is an emerging market of

challenger banks, app-banks, financial institutions and payment

facilitators in the wings. Some are already offering blockchain and

crypto services, some may do so down the line, but to say that the only

way to the future of banking is with blockchain and crypto is

short-sighted – there are much bigger demands and many more niches to be

filled.

Posted by AGORACOM-JC

at 10:57 AM on Monday, July 22nd, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

Understanding blockchain technology and its implications on the future of transactions

Blockchain technology will disrupt the way we write and enforce contracts, execute transactions and maintain records.

Since blockchain technology is at the heart of Bitcoin and other virtual currencies, it can at the very least be expected to power even more consequential mediums of exchange in the future.

Shaan Ray Jul 22, 2019 Blockchain technology is transformative, and several commentators expect that it will have a massive economic impact similar to the one the Internet has had in the past few decades.

Blockchain could be the future of the financial industry.

Since blockchain technology is at the heart of Bitcoin

and other virtual currencies, it can at the very least be expected to

power even more consequential mediums of exchange in the future.

However, virtual currencies are merely the first use case of blockchain

technology.

Blockchain fundamentals

The blockchain is an open and distributed ledger. It uses an

append-only data structure, meaning new transactions and data can be

added on to a blockchain, but past data cannot be erased.

This results in a verifiable and permanent record of data and

transactions between two or more parties. This has the potential to

increase transparency and accountability, and positively enhance our

social and economic systems. A blockchain is built by running software

and linking several nodes together.

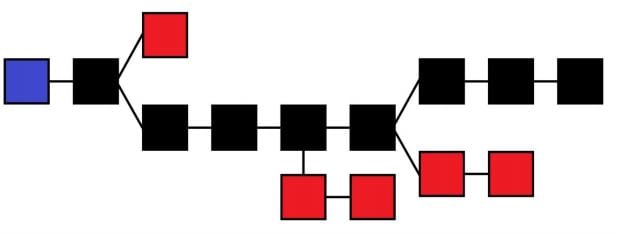

The main chain (black) consists of the longest series of blocks from the genesis block (blue) to the current block. Orphan blocks (red) exist outside of the main chain.

A blockchain is not one global entity — there are several

blockchains. Imagine a network of connected computers inside a highly

secure office, which are connected to each other, but not to the

internet. A blockchain is similar to this: it can have numerous

connected nodes, but remain totally separate and unique from other

blockchains.

Institutions and banks can build internal blockchains with their own

features for various organizational purposes. A consensus mechanism and a

reward system are required to maintain the integrity and functionality

of a blockchain.

In the Bitcoin blockchain, consensus is achieved by ‘mining’, and the

reward system is a protocol awarding a miner some amount of Bitcoin

upon successfully mining a block. Mining is undertaken by powerful

computers solving complex mathematical puzzles. Once a transaction is

verified and accepted as true by the entire network, miners start

working on the next block. Thus, a blockchain keeps growing (linking

each new block to the one before it).

Implications for transactions

Blockchain technology will disrupt the way we write and enforce

contracts, execute transactions and maintain records. Keeping records of

transactions is a core function of all businesses. These records are

meant to track past performance and help with forecasting and planning

for the future.

Most organizations’ records take a lot of time and effort to create,

and often the creation and storage processes are prone to errors.

Currently, transactions can be executed immediately, but settlement can

take anywhere from several hours to several days. For example, someone

selling stock in a corporation on a stock exchange can sell immediately,

but settlement can take a few days.

Similarly, a deal to purchase a house or car can be negotiated and

signed quickly, but the registration process (verifying and registering

the change in property ownership) often takes days and may involve

lawyers and government employees. In each of these examples, each party

maintains its own ledger, and cannot access the ledgers of the other

parties involved. On the blockchain, the process of transaction

verification and recording is immediate and permanent.

The ledger is distributed across several nodes, meaning the data is

replicated and stored instantaneously on each node across the system.

When a transaction is recorded in the blockchain, details of the

transaction such as price, asset, and ownership, are recorded, verified

and settled within seconds across all nodes. A verified change

registered on any one ledger is also simultaneously registered on all

other copies of the ledger. Since each transaction is transparently and

permanently recorded across all ledgers, open for anyone to see, there

is no need for third-party verification.

From virtual currencies to enterprise

Use The blockchain underlying Bitcoin is currently the largest and best-known blockchain. Ethereum is a separate blockchain:

while it supports the Ether currency, it also acts as a distributed

computing platform that features smart contract functionality.

Therefore, despite having a virtual currency element, it has many more

uses than Bitcoin. For example, companies in various industries raising

funds through ICOs use Ethereum for their projects.

The Hyperledger Project, by the Linux Foundation, aims to bring

together a number of independent efforts to develop open protocols and

standards in blockchain technology for enterprise use.

Here for the long term

Blockchain technology will disrupt the way we write Blockchain

technology, but is still in an early, formative stage, and

cryptocurrencies are only its first major use case.

Beyond cryptocurrency, blockchain technology will change how we

transact, and how we record and verify transactions. This will

revolutionise contracts and reduce friction in the exchange of assets.

Over the next few decades, blockchain technology will percolate

through our organizations and institutions, and shape how we transact

with one another. Just as the Internet continues to power emergent

technologies, we can expect to see new use cases of blockchain

technology across all industries.

Shaan Ray (MBA) is the head of Denver Hill, a group that uses

emerging technologies like blockchain, artificial intelligence, additive

manufacturing and the industrial internet to create new products and

processes.

Posted by AGORACOM-JC

at 9:45 PM on Sunday, July 21st, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

As Facebook Struggles For Blockchain Support, A Truly Decentralized Challenger Emerges

So, what is Celo? In a similar fashion to Libra, Celo is at its core a stablecoin platform

This means that the key value proposition of the assets running on top of the platform is that they are immune to the wide swings in volatility that have plagued leading crypto assets in recent years

Creates an opportunity for companies and projects like Celo, which are building pure blockchain-based financial services aimed at linking the nearly 2 billion people in the world that do not have access to bank accounts or the ability to verify their identity

As Facebook Blockchain Lead David Marcus tries to simultaneously use his testimony in front of U.S. lawmakers to restore trust in the company, and convince them that Facebook will not always be the driving force of its Libra project, it is easy to see why some of its key blockchain competitors are enthusiastic about the company’s entrance in the space.

The prevailing belief is that at some point the inherent contractions

in Facebook’s blockchain strategy and the Libra project are going to

become too much to overcome. Of course, this assumes that the project

launches at all, which is not certain given the regulatory scrutiny it

faces around the world.

This creates an opportunity for companies and projects like Celo,

which are building pure blockchain-based financial services aimed at

linking the nearly 2 billion people in the world that do not have access to bank accounts or the ability to verify their identity.

To the point, it is interesting that some of Libra’s first members,

including venerated venture capital firm Andreessen Horowitz and

crypto-unicorn Coinbase, have invested in Celo. Some of Celo’s other high-profile investors include LinkedIn founder Reid Hoffman and Twitter/Square CEO Jack Dorsey.

Understanding Celo

So, what is Celo? In a similar fashion to Libra, Celo is at its core a

stablecoin platform. This means that the key value proposition of the

assets running on top of the platform is that they are immune to the

wide swings in volatility that have plagued leading crypto assets in

recent years. Many are designed to mirror the price movements of

traditional currency, and most have names that reflect their fiat

brethren, such as the Gemini Dollar. This is a critical need for the

industry, as no asset will be able to serve as a currency if it does not

maintain a consistent price.

A man walks past signs advertising money transfer services and loans

outside a business in Mexico City, Tuesday, April 5, 2016. (AP

Photo/Rebecca Blackwell)

ASSOCIATED PRESS

However, rather than being a centralized issuer that supports the

price pegs with fiat held in banks, Celo has built a full-stack platform

(meaning it developed the underlying blockchain and applications that

run on top), that can offer an unlimited number of stablecoins all

backed by cryptoassets held in reserve.

Furthermore, Celo is what is known as an algorithmic-based stablecoin

provider. This distinction means that rather than being a centralized

entity that controls issuances and redemptions, the company employs a

smart-contract based stability protocol that automatically expands or

contracts the supply of its collateral reserves in a fashion similar to

how the Federal Reserve adjusts the U.S. monetary supply. In this vein,

Celo co-founder Rene Reinsberg told me that the company actually

“Maintains overcollaterization via a multi-asset crypto reserve composed

of Celo’s native asset, Celo Gold, and a basket of other crypto assets,

such as bitcoin.†This overcollateralization is important, and common

in crypto lending and stablecoin platforms, because it serves as a

buffer against potential volatility.

Additionally, a key differentiator for Celo from similar projects is

that for the first time its blockchain platform allows users to

send/receive money to a person’s phone number, IP address, email, as

well as other identifiers. This feature will be critical to the

long-term success for the network because it eliminates the need for

counterparties in a transaction to share their public keys with each

other prior to a transaction.

And now today, Celo is open-sourcing its entire codebase and design

after two years of development. Additionally, the company is launching

the first prototype of its platform, named the Alfajores Testnet, and

Celo Wallet, an Android app that will allow users to manage their

accounts and send/receive payments on the testnet.

This announcement and product is intended to be just the first of

what will be a wide range of financial services applications designed to

connect the world.

A Bright Outlook But Significant Question Remain

With all of that said, the company’s near and long-term success will

depend on its ability to navigate and address some key hurdles. Three in

particular immediately come to mind:

Stability of the Network. There are currently no

algorithmic/smart-contract based stablecoins in circulation today that

have seen widespread adoption. There are multiple reasons for this.

First, it is simpler to issue stablecoins on a 1:1 basis for fiat kept

in reserves. Second, it is nearly-impossible to design a complex system

that can account for and overcome any threat or challenge. It is likely

that at some point the future the network’s governance structure will be

challenged or that a critical flaw will be discovered in the underlying

code. The platform’s ability to rebound from these challenges without

compromising its decentralized nature will be a key determinant of its

future.

Ability to Adapt to Highly Volatile Fiat. A key

differentiator between Celo and other stablecoin issuers is that anyone

that participates in its governance function can propose a new currency.

The intention is that the platform will support a wide range of global,

national, and local currencies. Given that it is first targeting users

in the developing world, where the currencies are notoriously volatile,

there is a chance that the system could be strained as it seeks to

maintain constant pegs across the network. It is worth noting that the

company has given great thought and care to ensure that it is anti-fragile, and part of this strategy involves using a diverse basket of collateral to support all assets on the network.

Regulation. If the Libra hearings in front of Congress

proved nothing else, lawmakers are very concerned about crypto being

misappropriated for illicit uses. All issuers will need to comply with

existing AML/KYC laws. I asked Rene about this challenge and whether or

not their ability to comply will be hindered by the firms ability to

onboard users with little more than a phone number or some other

numerical identifier. His response was, “Yes, we’ve had conversations

with regulators both in the US and around the world. We think regulation

is critical for this space, particularly when it comes to protecting

consumers. We will absolutely comply with US laws and laws around the

world. We’re looking forward to sharing more on this at a later stage,

closer to mainnet launchâ€

Conclusion

There is a saying “nothing worth having comes easyâ€, and that

certainly applies to Celo and its diligent approach to development.

Additionally, the irony of its launch’s juxtaposition with the Libra

hearings underscores the need for a decentralized approach to connecting

the world.

Posted by AGORACOM-JC

at 9:49 AM on Monday, July 15th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

Bitcoin’s Price Could Rise If Facebook’s Crypto Survives Congress Hearings

Facebook’s fiat and government bond backed cryptocurrency Libra is widely considered a net positive for bitcoin, an anti-establishment asset.

Bitcoin has come under pressure ahead of the U.S. governmental hearings on Facebook’s Libra cryptocurrency on July 16 and 17.

The price of a single bitcoin, which stood near $13,000 five days

ago, fell below $10,000 earlier today and tested the 50-day moving

average at $9,900 for the first time since February 18.

Facebook’s head of Calibra – one of the entities set up to govern and develop the crypto project – David Marcus is scheduled testify to lawmakers on the Senate Banking Committee on Tuesday and the House Financial Services Committee on Wednesday.

The upcoming scrutiny of Libra may be weighing over bitcoin. After

all, past data shows BTC tends to drop ahead of congressional hearings

related to cryptocurrencies and rise on favorable outcomes.

Last year, for instance, BTC fell from $6,820 to $6,070 in five days

to July 12, before rallying to $7,400 on July 18 when the House

Committee on Financial Services gathered for a hearing on “crypto as a new form of moneyâ€.

More importantly, the cryptocurrency remained bid in the following

days and rose to a high of $8,500 on July 24 (according to Bitstamp

data) because the hearing didn’t take an overly negative tone.

On similar lines, BTC dropped from $12,000 to $6,000 in the 10 days leading up to a congressional hearing

on Feb. 6, 2018, where the Securities Exchange Commission (SEC)

chairman and the head of the Commodity Futures Trading Commission

testified before the Senate Banking Committee. That hearing was also

surprisingly positive and BTC rose back to levels above $11,700 by Feb.

20.

Going further back, the price action seen ahead of bitcoin’s first

congressional hearing on Nov. 18, 2013, was slightly different in the

sense that the cryptocurrency was solidly bid, rising from $85 to $650

in six weeks leading up to the event.

Again the hearing on the growing popularity of virtual currencies

wasn’t anti-crypto, allowing BTC to extend the rally to highs above

$1,150 on Nov. 30.

Will BTC rise this time round?

Facebook’s fiat and government bond backed cryptocurrency Libra is

widely considered a net positive for bitcoin, an anti-establishment

asset.

This is evident from the fact that BTC rallied from $9,000 to $13,800

in the eight days following Facebook’s unveiling of Libra’s white paper

on June 18.

So, it is hardly surprising that the leading cryptocurrency is

feeling the pull of gravity ahead of the congressional hearings on Libra

and will likely take a hit if the U.S. lawmakers throw a spanner in the

works for Facebook.

It is worth noting that the likes of the Federal Reserve President

Jerome Powell have already called for a halt to Facebook’s project until

concerns from privacy to money laundering are addressed. President

Trump also criticized the project in tweets last week.

BTC, however, may rise well past $13,800 and possibly hit record

highs before the end of the third quarter if the hearings are more

optimistic.

A far as the technical charts are concerned, the short-term outlook

will remain bullish as long as prices hold above $9,614 (July 2 low).

As of writing, BTC is changing hands at $10,300 on Bitstamp, representing 4.86 percent drop on a 24-hour basis.

Daily and 3-day charts

A UTC close below $9,614 would invalidate the bullish higher-lows pattern and confirm a bullish-to-bearish trend change.

That looks likely with the three-day chart reporting a bearish

divergence of the relative strength index (RSI). The indicator has also

dived out of the ascending trendline, signaling the end of the rally

from December lows.

Further, the previous three-candle closed well below the 10-candle

moving average, a level which acted as strong support throughout the

rise from $3,500 to $13,880, as discussed on Friday.

Weekly chart

The long upper wicks attached to two out of the last three candles

indicates bullish exhaustion and so does the bearish divergence of the

RSI.

All-in-all, the charts are biased for a drop to $9,097 (May 30 high),

unless the congressional hearings are more positive than expected. In

that case, prices may rise above $13,800, signaling a continuation of

the rally.

Hourly chart

BTC has recovered from lows near $9,850 to $10,300. The bearish

lower-highs pattern, however, is still intact. Prices may rise to

$11,200 in the next 24 hours if the cryptocurrency invalidates the

bearish lower highs pattern with a move above $10,732.

Disclosure: The author holds no cryptocurrency assets at the time of writing.

The leader in blockchain news, CoinDesk is a media outlet that strives for the highest journalistic standards and abides by a strict set of editorial policies.

CoinDesk is an independent operating subsidiary of Digital Currency

Group, which invests in cryptocurrencies and blockchain startups.

This article is intended as a news item to inform our readers

of various events and developments that affect, or that might in the

future affect, the value of the cryptocurrency described above. The

information contained herein is not intended to provide, and it does not

provide, sufficient information to form the basis for an investment

decision, and you should not rely on this information for that purpose.

The information presented herein is accurate only as of its date, and it

was not prepared by a research analyst or other investment

professional. You should seek additional information regarding the

merits and risks of investing in any cryptocurrency before deciding to

purchase or sell any such instruments.

Posted by AGORACOM-JC

at 2:00 PM on Thursday, July 11th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

‘Google Coin’ Within 2 Years as FANGs Will Go Crypto, Say Winklevoss

Speaking about Facebook Libra, the twins, who co-founded cryptocurrency trading platform Gemini, said it was only a matter of time before other tech giants followed suit.Â

Speaking about Facebook Libra, the twins, who co-founded cryptocurrency trading platform Gemini, said it was only a matter of time before other tech giants followed suit.

FANG refers to the unofficial “Big Four†of the internet: Facebook, Amazon, Netflix and Google.

“Our prediction is every FANG company will have some sort of

cryptocurrency project within the next two years,†Tyler told the

network.

Libra as a payment protocol has not yet launched, but regulators have voiced alarm, particularly in the United States, where several sources have demanded developers halt the project.

Concerns stem from Libra’s potential to bypass the banking system,

something cryptocurrency proponents conversely argue makes the banking establishment overly nervous about losing revenue.

On Thursday, Bitcoin (BTC) itself shed over 10% of its value after a senior U.S. lawmaker delivered fresh concerns about Libra.

For the Winklevosses, however, front-door approaches to regulators is key in getting any disruptive finance offering to market.

Though many say it is not a cryptocurrency at all, the twins even

suggested they would facilitate trading of Libra on Gemini, should it be

open and not subject to prohibitive restrictions.

“We’ll evaluate Libra in earnest, and it might actually be an asset

that is one day listed if it’s an open protocol; that’s possible,†Tyler

continued.

Earlier this week, Tom Lee,

a serial Bitcoin advocate, delivered a similar forecast regarding tech

giants’ future involvement in the digital currency industry.

“The fact that Facebook and likely other FANG companies are going to

create their own digital currencies is validating the idea that digital

money is here to stay,†he told CNBC.

Posted by AGORACOM-JC

at 10:22 AM on Wednesday, July 10th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

————-

Is Blockchain the New Technology of Trust?

Blockchain continues to be a hot topic across the global start-up ecosystem.

And more entrepreneurs are placing huge bets on this technology. Y

Nidhi Singh Former Correspondent, Entrepreneur Asia-Pacific

Blockchain continues to be a hot topic across the global start-up

ecosystem. And more entrepreneurs are placing huge bets on this

technology. Yet the adoption remains sluggish despite the growing

investment by start-ups and potential investors. Main reasons for this

are fears over security and regulatory uncertainty. Will mass

implementation of blockchain technology remain a distant fantasy?

US-based

rating agency Moody’s Investor Service warns about the risks associated

with the technology. “New risks with blockchain technology in

securitizations may emerge as well as the reinforcement of some already

existing ones. Risks include counterparty concentration, IT and

operational risks, inappropriate blockchain governance and legal and

regulatory issues,†its report says. Another study by auditing firm

PricewaterhouseCoopers (PwC) states that trust is one of the biggest

blockers to the blockchain’s adoption. Concern about trust among

respondents in the survey was highest in Singapore (37 per cent) after

Hong Kong (35 per cent).

Riding the Wave

Despite issues, companies, especially those in Asia Pacific, are not

shying away from the technology. Singapore-based LALA World Chief

ExecutiveOfficer and Founder Sankal Shangari believes blockchain

technology is not only bringing in a difference at the consumer level

but also posing a threat to the established system of governance, which

is obtrusive of financial freedom.

“A lot of myths are floating around the technology. It was dubbed as a

dubious technology, which may look promising, but was porous and could

be compromised. The reality is far from it, the technology is secure and

reliable than any of the other techniques available. But at the same

time, it is complex and in a nascent stage just like the web was in the

early 1990s and that is what helps the naysayers in spreading heresy

about it. The need is to understand its applicability to a particular

problem and the impact it has in solving it,†says Shangari.

LALA ID, a product of LALA World, is a comprehensive solution that

protects the personal information of users through the immutable

blockchain technology. Additionally, the start-up offers features like

crypto payments through its application. “The world is going gung-ho

about the possibilities of the said technology, which is gradually

growing as an infrastructural pillar of economic functionalities,

receiving the attention it deserves,†stresses Shangari.

Varied Uses

Mike Davie’s Quadrant Protocol leverages blockchain and smart

contracts to track the data’s journey along the data chain—from the

originating device to the data scientists that add value to the data—and

provide automatic compensation every time the data is purchased. This

helps create a more sustainable data economy. The start-up serves as the

blueprint that provides an organized system for the utilization of

decentralized data.

“Data quality is vital to the success of artificial intelligence.

Algorithms will believe whatever the data tells them to believe, so

using poor quality data can result in unintended consequences. Data

consumers, therefore, need to know where the data is coming from and be

able to trust the source. At the same time, the original providers of

the data are rarely compensated fairly. Data consumers like data

scientists or AI practitioners can be assured of the quality and

provenance of the data being purchased, while providers are compensated

fairly. All compensation is paid in Quadrant Protocol tokens, which are

recorded on the blockchain,†says Davie.

The company’s primary focus is on location data, which is an

essential tool in understanding the behaviour of potential customers.

The platform processes over 50 billion records a month, enabling

organisations in every industry to obtain data they can use to make

business and policy decisions. It is powered by a protocol that uses

blockchain technology to authenticate and map this data.

Insurtech company Hearti is serving insurers with their proprietary

artificial intelligence (AI) and blockchain platform. Keith Lim, Chief

Executive Officer, Hearti, believes blockchain’s immutable nature can

foster trust in the insurance agreements between consumers, insurers and

partners.

“Smart contracts are executed based on events that trigger conditions

within the agreement (for eg. to pay out claims in the event of a

flight delay). When claims data is shared securely on the blockchain,

duplicate claims and fraud can be tracked and detected. Such uses of

blockchain create huge value for our company’s proposition and put it at

the forefront of the industry,†says Lim.

Founded in June 2015, Hearti Lab was born out of the realization that

there was a void in the corporate and personal insurance sector: the

lack of a low-cost, full-featured AI platform for insurance management.

To achieve its vision of developing an integrated insurance platform,

the start-up has developed two complementary platforms: BENEFIT.X and

SURETY.AI.

In Tech We Trust

For Joseph Lee, Chief Technology Officer, BridgeX Network, blockchain

is the “new technology of trustâ€. BridgeX Network is a financial

ecosystem framework, built on a proprietary technology core that bridges

the worlds of cryptocurrencies and fiat.

“We are using blockchain technologies to create a platform to allow

lenders and borrowers to transact directly in a secure environment. The

terms are specified in the blockchain and will be executed automatically

without bias. The costs saved from eliminating intermediaries are

passed to participants on the platform,†says Lee. “Perhaps due to the

newness of the technology, there may still be a trust deficit with the

public. But we strongly believe in it.â€