Posted by AGORACOM

at 9:37 AM on Tuesday, October 27th, 2020

Hole ND-10-03 intersected 4.53% Ni, within a larger interval averaging 1.02% Ni, 0.38% Cu over 4 metres.

The mineralization remains open along strike and to depth.

Claims previously owned by Canadian Arrow Mines Limited in 2010

TORONTO, ON / ACCESSWIRE / October 27, 2020 / Tartisan Nickel Corp. (CSE:TN)(OTC PINK:TTSRF)(FSE:A2D) (“Tartisan”, or the “Company”) is pleased to announce that the Company has acquired the Night Danger, Glatz nickel-copper claims located in the Turtle Pond Project area near Dryden, Ontario.

The Company has acquired a 100% interest in the Glatz, Night Danger Nickel-Copper Claims located approximately 70 kms from the Company’s flagship Kenbridge Nickel Deposit. The property is situated in an area of excellent infrastructure and consists of 16 claim units. The 16 claim unit property hosts the historical Glatz and Night Danger nickel-copper showings. Previous exploration efforts identified nickel-copper sulphide mineralization in twelve trenches along a 700 metre trend at the Glatz nickel copper showing. The zone, discovered in 1965 by local prospector A. Glatz, is up to 40 metres wide and is open along strike and at depth. Historical grab samples were reported to contain up to 1.95% Ni. In 2007, Canadian Arrow Mines Limited conducted a surface grab sampling program which produced the following results: 1.28% Ni, 0.26% Cu re Glatz Trench 3; 0.99% Ni, 0.18% Cu re Glatz Trench 3; 0.39% Ni, 4.06% Cu re Trench 4. The mineralization varies from disseminated sulphides to narrow semi-massive sulphide bands. Six short drill holes were completed at that time with hole GZ-09-02 encountering 0.34% Ni, 0.16% Cu and 0.02% Co over 5.9 m from 45.0-50.9 m.

Exploration diamond drilling work completed in 2009 and 2010 on the Night Danger nickel-copper showing reported a nine metre wide section of stringers and blebs of sulphide which assayed 0.57% Ni and 0.45% Cu at a drill depth of 79m in hole ND-09-1. Two sections within this interval assayed greater than 1% nickel. Drill hole ND-10-1 intersected 4.53% Ni over 0.7m at a drill depth of 57.5m (Source; MNDM assessment files and Canadian Arrow Mines Limited news release dated June 1, 2010).

Mark Appleby, President and CEO of Tartisan stated, “The Glatz and Night Danger nickel-copper showings display similar nickel and copper tenors as what we find near surface at our Kenbridge Nickel Deposit. Acquisition of these showings complements the company’s larger objective of developing the Kenbridge Nickel Deposit into an operating mine with a central milling facility.”

About Tartisan Nickel Corp.

Tartisan Nickel Corp. is a Canadian based mineral exploration and development company which owns; the Kenbridge Nickel Project in northwestern Ontario; the Sill Lake Silver property in Sault Ste. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel and Technologies Limited and Peruvian Metals Corp.

Tartisan Nickel Corp. common shares are listed on the Canadian Securities Exchange (CSE:TN; US-OTC:TTSRF; FSE:A2D). Currently, there are 101,603,550 shares outstanding (107,203,550 fully diluted).

For further information, please contact Mr. D. Mark Appleby, President & CEO and a Director of the Company, at 416-804-0280 ([email protected]). Additional information about Tartisan can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

Posted by AGORACOM

at 9:58 AM on Wednesday, October 7th, 2020

By Ellsworth Dickson

Nickel is a most useful base metal. Because rust never sleeps, some 75% of nickel produced is used to make stainless steel, most being what is known as Class 2 nickel. Class 1 nickel, or pure nickel, is used for making steel alloys, storage batteries for laptops and cell phones and, of increasing importance, electric vehicle (EV) batteries.

Nickel is part of the cathode in a Li-ion battery. It is these Li-ion batteries that are kick-starting a sea change in the nickel market.

Combining all uses, nickel demand grew 9.4% during 2018 and 2018 – outperforming all other major base metals – making it a US$20 billion per year industry. In 2018, Canadian exports of nickel-based products totaled $4.2 billion with Canada ranking fifth in the world for mine production.

Nickel prices are currently trading around US$14,000/tonne, or US$6.42/lb, up more than 30% from March lows and near its highest levels in November 2019.

And while stainless steel and other nickel usages continue to steadily grow as the world’s population increases, it is the EV market that is expected to see a huge growth in nickel demand, according to senior miner Glencore. For the first time, in 2017, sales of EVs passed the 1 million mark; however, this is just the beginning.

According to the International Energy Agency, (IEA), sales of electric cars topped 2.1 million globally in 2019, surpassing 2018 – already a another record year – to boost the stock to 7.2 million electric cars, 47% of which were in China. It’s hard to believe that in 2010, there were only 17,000 EVs on the road. Electric cars, which accounted for 2.6% of global car sales and about 1% of global car stock in 2019, registered a 40% year-on-year increase.

In their recent report, the IEA stated that nine countries had more than 100,000 electric cars on the road. At least 20 countries reached market shares above 1%. However, this growth has sometimes been disrupted by various events and circumstances that negatively affected EV sales.

Deloitte’s outlook shows EV sales reaching 21 million vehicles in 2030 as the cost of manufacturing batteries falls significantly and range anxiety becomes less of a concern. Another challenge for would-be EV buyers is availability of charging stations out of town and, in tow, lacking of charging stations in older apartment buildings.

This huge increase in EV sales will be even more jump-started with the introduction of electric pickup trucks, SUVs, delivery trucks and semi tractor trailers. This could cause a supply crunch for Class 1 nickel.

Interestingly, the IEA noted that electric two/three-wheelers will continue to represent the lion’s share of the total electric vehicle fleet, as this category is most suited to rapid transition to electric drive. The future electric two/three-wheeler fleet is concentrated in China, India and the ten countries of ASEAN.

Wood Mackenzie predicts an increase in nickel demand for EVs from 128 kt in 2019 to 265 kt in 2025 and 1.23 Mt in 2040, increasing nickel battery demand from 4% in 2018 to 31% by 2040.

It has been estimated that by 2025 the world need almost 1 million tonnes per year of new nickel supply. By 2030, 2.5 million tonnes, or double that of today, is required.

Wood Mackenzie is forecasting an average annual nickel deficit of 60,000 tonnes through to 2027 – a situation that bodes well for nickel explorers, developers and producers.

About one-half of the world’s nickel supply is suitable for use in batteries such as the nickel sulphide mines in Sudbury, Voisey’s Bay and Russia.

Those companies involved in discovering and mining nickel deposits are participating in a massive unstoppable global event with the electrification of the world’s vehicles – a good place to be.

Tartisan Nickel Corp. [TN-CSE; TTSRF-OTC; A2D-FSE] has favourably positioned itself to participate in the growing electric vehicle sector with its advanced-stage Kenbridge nickel-copper-cobalt project in northwestern Ontario.

While copper and cobalt are important for the EV battery and vehicle market, Elon Musk of Tesla Motors recently stated that nickel remains a key ingredient to its rapidly improving EV battery technology. Stainless steel production still accounts for the majority of nickel usage; however, commodity research firm Roskill has stated that the current EV nickel demand will grow from 4% to 15-20% of the market.

Longer term, California Governor Gavin Newsom just signed an executive order that will ban the sale of new gas-powered passengers cars starting in 2025.

Tartisan’s Kenbridge Project, located near Atikwa Lake in the Kenora-Fort Frances area, has undergone an updated mineral resource estimate.

The updated estimates were done for pit constrained and out-of-pit nickel, copper, and cobalt resources. Total Measured & Indicated Mineral Resources, based on a Net Smelter Return (NSR) cut-off value of CDN$15/tonne for pit constrained Mineral Resources and CDN$6/tonne NSR for out-of-pit Mineral Resources is 7.5 Mt at 0.58% nickel and 0.32% copper for a total of 95 Mlb of contained nickel. An additional 0.985 Mt at 1.0% nickel and 0.62% copper (22 Mlb contained nickel) were calculated as Inferred Resources. Pit constrained Measured & Indicated Resources total 5.27 Mt of 0.45% nickel, 0.26% copper and 0.009% cobalt at an NSR cut-off value of CDN$15/tonne. The out-of-pit Measured & Indicated Resources total 2.23 Mt of 0.86% nickel; 0.45% copper; and 0.006% cobalt. Inferred Mineral Resources out-of-pit total 0.985 Mt at 1.00% nickel, 0.62% copper and 0.003% cobalt, at an NSR cut-off value of CDN$60/tonne.

Mark Appleby, President and CEO, notes that the deposit is open to depth with the highest nickel grades having a strong down-plunge orientation such as hole KB07-180 that returned 2.95% nickel and 0.82% copper over 21.5 metres, including 7.2% nickel and 0.67% copper over 5.5 metres.

Highlights of an Updated PEA were: average nickel recovery life-of-mine was 86%; recovered nickel was 84.6 Mlb; NPV7.5% pre-tax was $253M; and IRR% pre-tax was 65%.

The Kenbridge property has good access to roads and power. It has a shaft to a depth of 622 metres, with level stations at 45-metre intervals below the shaft collar and two levels developed at 107 metres and 152 metres below the shaft collar.

Tartisan Nickel has planned a surface exploration and definition drilling plan, in addition to geotechnical, metallurgical and environmental work to advance the project in the upcoming 2020 winter season and into summer 2021.

The company also owns equity stakes in Eloro Resources Ltd. that is exploring the 99%-optioned ISKA ISKA Project, a gold-silver-zinc-lead target with a 3,500-metre underground drilling program underway in the Potosi district, Bolivia, and the low-sulphidation epithermal 82%-owned La Victoria gold-silver project in Peru.

Tartisan is a shareholder in Class 1 Nickel and Technologies that holds the past-producing Alexo-Kelex Dundonald nickel project near Timmins, Ontario in which Tartisan has a 0.5% NSR. The property hosts an estimated total NI 43-101 compliant Indicated Mineral Resources of 571.7k tonnes averaging 0.77% nickel plus Inferred Resources.

Being a prospect generator, Tartisan spun out the Alexco-Kelex Project to Class 1 Nickel as well as the La Victoria Project to Eloro.

Tartisan is a shareholder in Peruvian Metals Corp. that is operating a toll mill in Peru and announced an exploration and bulk sampling program on the high-grade gold-silver-copper Palta Dorada Project.

Tartisan also has a 100% interest in the Sill Lake silver-lead project near Sault Ste. Marie, Ontario.

Tartisan’s investment portfolio is in excess of $7 million which can provide funds for its activities and avoids share dilution through further share issuances. The company has 101.6 million shares outstanding.

Though its acquisitions and investments, Tartisan Nickel is poised to benefit from the burgeoning EV battery sector as well as its precious metal and base metal prospects.

Garibaldi Resources Corp. [GGI-TSXV; GGIFF-OTC; RQM-FSE] has been following up its 2017 magmatic nickel massive sulphide discovery in the Golden Triangle region of northwestern British Columbia.

Located on Nickel Mountain, the flagship E&L deposit hosts nickel, copper, cobalt, platinum, palladium gold and silver. The latest drill results from the 2020 program have extended the strike length of the mineralized E&L system from 200 metres to over 650 metres to the east, where the intrusion remains open.

The 100%-owned project is the Golden Triangle’s first magmatic nickel-copper-rich massive sulphide system in the heart of the prolific Eskay Camp. The 2017 discovery drill hole EL-17-14 intersected 8.3% nickel, 4.2% copper, 0.19% cobalt, 1.96 g/t platinum, 4.5 g/t palladium, 1.1 g/t gold and 11.1 g/t silver over 16.75 metres starting 100.4 metres downhole, within a broader 40.4-metre core length highlighted by 3.9% nickel and 2.4% copper.

In February, 2019, Garibaldi confirmed an even shallower new zone (Northeast Zone) with drill hole EL-18-33 that returned 7.7% nickel and 2.95% copper over 4.8 metres within a broader interval of 49 metres grading 1.34% nickel and 0.89% copper (core length) plus cobalt, platinum, palladium, gold and silver credits.

Diamond drilling continues to build out on the persistent widespread nickel-copper mineralization, which includes massive sulphides featuring top-tier nickel-copper grades in addition to palladium, platinum, cobalt, gold, silver and strategic PGE (platinum group element) rare metals, including rhodium.

Hole EL-20-88, collared 350 metres east of pivotal hole EL-19-80, intersected 142.79 metres of mineralized taxitic gabbro and olivine pyroxenite along trend of the E&L system. This large step-out hole exhibited an E&L geochemical signature which expanded the strike length of the E&L gabbroic intrusion to over 650 metres within a 2-km structural corridor that remains untested and open.

Hole El-20-89 has produced the widest mineralized intercept so far from 71.34 metres to 223 metres returning nickel-copper mineralization over 151.6 metres grading 0.56% nickel and 0.61% copper. This intersect included 80.53 metres of 0.88% nickel and 0.85% copper, which expanded the northeastern massive sulphide zone six metres south, the LDZ 15 metres north and the Second Chamber 45 metres west.

Semi-massive veins along the contact edge with sediments assayed 0.33 metres (100.54 to 100.87 m) of 6.87% nickel and 1.69% copper, and 0.15 metres (147.48 to 147.63 m) of 3.04% nickel and 1.62% copper.

Garibaldi has drilled 10 additional holes at the E&L project on Nickel Mountain and is up to hole 94 so far this season. With new geochemical and geophysical targets located at depth, the immediate goal of the drill program is to follow the steeply-plunging E&L gabbro to the east. The conductors detected off hole will be drill tested for mineralization.

Garibaldi owns 100% of more than 200 km2 in Eskay Camp, including newly discovered high-grade gold quartz vein system at Casper, located 15 km north of Nickel Mountain. Assays are pending. The company also has four projects in Mexico.

Garibaldi’s nickel discovery is a unique development in the Golden Triangle with excellent potential for significant expansion at a time of increasing nickel demand from the electric vehicle market.

Just 12 km north of the E&L nickel deposit is Garibaldi’s 100%-owned Casper high-grade gold quartz vein discovery. The Casper gold vein is a strategic low elevation target (420 metres) within a km of road access and hydroelectric power.

Field crews collected 165 samples within 250 metres north of and 250 metres south of the northwest-southeast-striking Casper vein. High-grade grab samples at Casper were reported up to 249 g/t gold and assays for 86 Casper channel samples have been released with up to 92 g/t gold and 5.69 g/t gold over 52 metres.

Mechanical trenching at the Casper gold quartz vein has further uncovered the high-grade vein over more than 120 metres, from the initial 43 metres of hand trenching exposing the discovery.

The quartz vein remains open with mineralized rock samples extending along trend for 330 metres within a 500-metre gold-in-soil and MMI (mobile metal ion) geochemical anomaly.

The latest assays from 61 channel sample assays returned gold grades ranging from 0.676 g/t gold up to 93.29 g/t gold from a channel sample that contained visible gold.

The company has 116 million shares outstanding.

Sama Resources Inc. [SME-TSXV; SAMMF-OTC.PK] is a Canada-based mineral exploration and development company with projects in West Africa, in particular, the Samapleu nickel-copper-cobalt-platinum group metals project in Côte d’Ivoire (Ivory Coast).

Sama’s projects are located approximately 600 km northwest of Abidjan in Côte d’Ivoire and adjacent to the Guinean border in West Africa.

In 2010, Sama discovered nickel-copper-PGE mineralization, including veins and lenses of high grades material near surface at numerous locations within the then discovered Yacouba intrusive complex.

In October, 2017, Sama announced that it had entered into a binding term sheet in view of forming a strategic partnership with HPX TechCo Inc., a private mineral exploration company in which mining entrepreneur Robert Friedland is a significant stakeholder, in order to develop the Samapleu Project. HPX is spending $18 million on the project.

Since March 2010, Sama has performed surface IP and Mag surveys as well as Airborne Mag-Radiometric and HTEM surveys and 388 boreholes for a total of 54,000 metres of drilling. Mineral resources assessments have been completed at one site, the Samapleu deposit, aiming for a modest scale Ni-Cu open pit mining and processing operation, while continuing to explore newly discovered prospective ground. Sama’s objective is to delineate massive sulphide reservoirs that could be the source of these high-grade nickel–copper-cobalt-palladium lenses. The newly discovered Yacouba complex can be compared to other world class bases metals camps like Jinchuan in China and Voisey’s Bay in Canada, etc.

Highlights of a Preliminary Economic Assessment at Samapleu, include average annual production of 3,900 tonnes of carbonyl nickel powder, 8,400 tonnes of carbonyl iron powder and 14,100 tonnes of copper concentrate over a 20-year mine life. Capital costs are estimated to be $282 million, including a contingency of $37 million with operational costs of $23.96/tonne milled.

Pre-tax Net Present Value (8% discount rate) is $615 million and an Internal Rate of Return of 32.5%. After-tax NPV (8% discount rate) of $391 million and an after-tax IRR of 27.2%.

Geophysical activities have resumed with downhole electromagnetic surveys planned in four deep drill holes at the Yepleu target zone and in one deep drill hole at the Bounta target zone. The holes at Yepleu and Bounta were drilled in the early months of 2020, with both zones part of the large Yacouba Ultramafic-Mafic intrusive complex discovered by Sama in 2010.

Future production will be managed by a JV controlled 66⅔% by Sama Nickel Corp. a wholly-owned subsidiary of Sama Resources, and 33⅓% by SODEMI. Sama Resources has $2.5 million in its treasury and holds $12.4 million in securities with no debt. The company has 216,466,410 shares outstanding.

The Samapleu nickel-copper-cobalt-platinum group metals project is located in mining-friendly West Africa, home to a number of successful mining operations. The polymetallic project hosts a suite of metals – nickel-copper-cobalt-platinum group metals – all of which are currently in demand.

Posted by AGORACOM-JC

at 2:11 PM on Friday, September 25th, 2020

The Liberal Government announced new measures towards climate, clean energy and transport in yesterday’s throne speech. This will no doubt help accelerate the transition toward electric mobility while ensuring a cleaner, healthier economy. Here are 6 small cap companies that stand to benefit from these initiatives (in alphabetical order).

Gratomic Inc. (GRAT :TSXV) is gearing up to bring its high grade, environmentally sustainable graphite to the North American EV market. In a race that started in 2012, Gratomic is the only one of several graphite companies that has successfully brought its asset through to the final construction phase.

The Company is now ready to introduce its graphite to battery producers for use in advanced anode technology. Being of such naturally high purity, Gratomic’s vein graphite is ideal for use in this application, requiring simpler, less expensive and more efficient processing methods, resulting in a final product with naturally lower contents of deleterious elements.

In addition to its high purity levels, the Company’s Aukam graphite is a much cleaner alternative to this market’s current supply options as a sustainably sourced resource as per the Company’s September 3rd Press Release. The Company intends to establish a new benchmark for recording and guaranteeing the product’s carbon footprint, based on latest generation blockchain technology.

Gratomic is preparing the high grade Aukam Graphite mine for commercial production. The company anticipates commencement of production in Q4 of 2020 while producing 20,000 tonnes of high purity vein graphite annually to support a burgeoning market.

HPQ Silicon Resources (HPQ:TSXV) is a Canadian producer of Silicon Solutions that is building a line of specialty silicon products needed for electric batteries. More than just lip service, HPQ has already announced NDA’s with 2 undisclosed companies in the space and has hinted at other NDA’s that are so tight they could not even be announced.

Over the past 5 years, HPQ has teamed up with 2 world renowned technology partners, including PyroGenesis Canada (PYR:TSXV) to manufacture high purity silicon cleaner, cheaper and better than anyone in the world – because you can’t dig it out of the ground like other battery metals such as graphite, cobalt and nickel. Now HPQ is on the verge of sending samples of its industry leading silicon to NDA and other potential partners as early as December.

However, despite providing shareholders with a great return during this period, HPQ’s silicon plan was still met by skepticism amongst investors who found it easier to understand traditional battery metal stories …. This all changed on September 23rd 2020, when this headline emerged from Tesla’s “Battery Day”

Lomiko Metals (LMR: TSXV) discovered high-grade graphite at La Loutre property in Quebec and is working toward a Pre Economic Assessment to increase current resource to 10m/t of 10% Cg.

“Initial indications are that La Loutre Graphite Property is high-quality and high-grade and thus worthy of development.” stated A. Paul Gill, CEO. “The only operating graphite mine in North America which is the Imerys Graphite & Carbon at Lac-des-Îles, is 30 miles northwest of La Loutre and has operated for 30 years.

Lomiko is in an ideal position to participate in the Electrical Vehicle market with the potential to become a North American supplier of graphite materials.

New Age Metals Inc. (NAM: TSXV) is a green metals company focused on PGM and Lithium. The company’s Lithium division is the largest mineral claim holder in the Winnipeg River Pegmatite Field, where the Company is exploring for hard rock lithium and various rare elements such as tantalum and rubidium. Manitoba is THE untapped frontier for ‘Hard Rock’ Lithium.

The Company’s philosophy is to be a project generator with the objective of optioning its Lithium projects with major and junior mining companies through to production.

St-Georges Eco-Mining (SX:CSE) is developing new technologies to solve some of the most common environmental problems in the mining industry. The company is focused on value-adding the recovery of battery-grade nickel, ferronickel for alloying in the stainless steel industry and recovery of valuable elements such as cobalt. St-Georges is working on processing nickel and minimizing tailings with solutions to energy challenges.

The company is also working on lithium extraction technologies with non-conventional resources, such as clays, and working on ways to concentrate and reduce the environmental impact while unlocking the valuable content of the material.

More than just lip service, the Company’s lithium extraction technology has already delivered its first License agreement with Iconic Minerals in exchange for:

$100,000 cash

5,000,000 shares in 3 stages

A perpetual net revenue interest royalty (NRI) of 5% on all minerals produced on sites licensed with SX technologies in the state of Nevada

Tartisan Nickel (TN:CSE) – 95 Million Pounds Of Contained Nickel

Nickel is the new gold, a critical element for the growing electric vehicle market, Tartisan just announced a re-estimation of the Mineral Resource Estimate at the Kenbridge Nickel-Copper-Cobalt Project. Kenbridge holds mineral resources of 7.5 Mt of 0.58% Ni and 0.32% Cu for a total of 95 Mlb of contained nickel. Class 1 nickel sulphide deposits are emerging as a key supplier of Nickel to the growing electric vehicle market.

CEO Mr. Mark Appleby stated, “The Updated Mineral Resource Estimate was necessary to determine if Kenbridge mineralization is potentially extractable under current metal prices and exchange rates. This is a major milestone achieved by the Company as the market conditions for Class 1 nickel sulphide deposits improve. The differences between the previous P&E Mineral Resource Estimate (2008) and the current P&E Updated Mineral Resource Estimate are attributed to changes in metal prices and recalculation of NSR values.

Posted by AGORACOM

at 9:17 AM on Thursday, September 24th, 2020

TORONTO, ON / September 24, 2020 / Tartisan Nickel Corp. (CSE:TN; OTC PINK:TTSRF; FSE:A2D) (“Tartisan”, or the “Company”) is pleased to update shareholders on the Company’s operations in the Republic of Peru. The Don Pancho polymetallic Silver-Lead-Zinc project (“Don Pancho”) located in the department of Lima, Peru, 110 kilometres north-northeast of Lima, comprising of two concessions totalling 849 hectares. The project is located in a prolific polymetallic mineral belt in central Peru with several operating mines in the area, including Minas de Buenaventura’s silver-lead-zinc-manganese (Ag-Pb-Zn-Mn) Uchucchacua mine located 66 kilometres north of Don Pancho which produced more than 15 million ounces of silver in 2018.

Previous exploration on the property includes an extensive surface mapping and sampling program, geophysics, and a small diamond drilling program conducted by a private Peruvian company in 2014. Mapping and sampling by the previous operators defined two main mineralized zones. The main zone called “Yanapallaca” is an extensive NNW-SSE-trending breccia zone covering a surface area of over 800 metres in length and up to 200 metres in width. Numerous small old workings and three underground drifts exist within this zone. One of the adits crosscut a two metre wide massive sulphide vein grading 106 g/t Ag, 3.26% Pb, 17.56% Zn and 2.58% Mn. Other untested mineralized structures located within this zone that are exposed on surface include chip over 1 metre returning 406 g/t Ag and 27.05% Pb.

The second mineralized zone called “La Cruz” is located several hundreds of metres NE of Yanapallaca shows two mineralized trends. Sampling across the main N-S trend returned 96.6 g/t Ag, 5.53% Pb and 0.88% Zn over 1.50 metres with a crosscutting WNW-ESE structure grading 360 g/t Ag and 12.66% Pb over a 1 metre width. Very little work has been conducted by the previous operators on this prospective area.

Tartisan is pleased to announce the appointment of Carlos Agreda Minaya as the General Manager for Tartisan’s Peruvian subsidiary, Minera Tartisan Peru S.A.C. Mr. Agreda is an experienced manager with a MBA from Peru’s highly reputable ESAN program. Mr. Agreda has extensive experience in permitting, accounting and mineral processing. Mr. Agreda is very knowledgeable of the Company’s Don Pancho property and has submitted the necessary permits to start an underground bulk sampling program. Mr. Agreda is also the General Manager of Peruvian Metals Corp., a Canadian junior explorer in Peru with a processing plant located in Northern Peru where mineral from the Don Pancho will be processed.

Jeffrey Reeder, P.Geo, a qualified person as defined in National Instrument 43-101, has prepared, supervised the preparation of, or approved the scientific and technical disclosure contained in this news release.

About Tartisan Nickel Corp.

Tartisan Nickel Corp. is a Canadian based mineral exploration and development company which owns; the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Silver-Lead-Zinc Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel & Technologies Limited and Peruvian Metals Corp.

Tartisan Nickel Corp. common shares are listed on the Canadian Securities Exchange (CSE:TN; US-OTC:TTSRF; FSE:A2D). Currently, there are 101,603,550 shares outstanding (107,203,550 fully diluted).

For further information, please contact Mr. Mark Appleby, President & CEO and a Director of Tartisan Nickel Corp. at 416-804-0280 ([email protected]). Additional information about Tartisan Nickel Corp. can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

This news release may contain forward-looking statements including but not limited to comments regarding the timing and content of upcoming work programs, geological interpretations, receipt of property titles, potential mineral recovery processes, etc. Forward-looking statements address future events and conditions and therefore, involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements.

The Canadian Securities Exchange (operated by CNSX Markets Inc.) has neither approved nor disapproved of the contents of this press release.

Posted by AGORACOM

at 10:23 AM on Wednesday, September 23rd, 2020

Tartisan Nickel Corp. owns the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel & Technologies Limited and Peruvian Metals Corp. Click Here For More Info

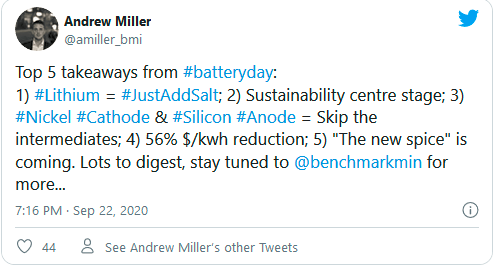

Calling traditional metal refining processes “legacy” and “insanely complicated”, Elon Musk said today his company has re-thought and simplified how lithium and nickel will be processed for his future batteries.

Musk made the comments during a live simulcast presentation of Battery Day held in a parking lot in Fremont, California, near his manufacturing facilities. Musk shared part of the presentation with Drew Baglino, SVP of Powertrain and Energy Engineering at Tesla.

Musk called the traditional cathode process of processing nickel “a big target” due to its high cost

“It’s insanely complicated,” said Musk. “These things just grow up as legacy. We looked at the entire value chain and asked how can we make this as simple as possible.”

Bagnilo and Musk said many steps in the traditional refining method could be skipped resulting in 66% less investment, 76% less processing cost and 0% waste water.

The CEO of FPX Nickel, Martin Turenne, concurred with Musk: mineral processing can be made cleaner and more economical.

“The current methods of processing [nickel] are generally well established, and they’re done for a reason, because they work and because alternatives would be costly or they’re at an unproven stage,” said Turenne in an interview with Kitco after he watched Tesla’s Battery Day presentation.

At his own FPX, Turenne believes his nickel is in a form that would be suitable for batteries with the potential to skip the smelting step.

Musk and Bragnila imagine Tesla factories processing raw nickel powder for processing.

“Raw materials from a mine go to the plant and out comes a battery,” said Bragnila. “We are just consuming the raw nickel powder. It dramalitcally simplifies the raw nickel refining part of the whole process. We can eliminate billions in battery grade nickel intermediate production. It is not needed at all.”

What struck Turenne during the presentation is the forecast level of demand.

“At three terawatt-hours of battery cells per annum by 2030, that would entail approximately annual consumption of 2 million tonnes of nickel. That’s almost the entire scale of the current global nickel output,” said Turenne.

Posted by AGORACOM

at 8:10 AM on Tuesday, September 22nd, 2020

Tartisan Nickel Corp. owns the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel & Technologies Limited and Peruvian Metals Corp.

The federal government is planning investments in the electric vehicle industry to create a domestic supply chain for electric vehicle batteries that could supply the North American market. (Jonathan Hayward/The Canadian Press)

The Liberal government will use the speech from the throne to lay out a plan to create tens of thousands of jobs by connecting Canada’s resource sector with its manufacturing base to produce batteries for electric cars, Radio-Canada has learned.

“We recognize we have a unique opportunity to take advantage of our skilled labour force and we know we have a long and proud history of manufacturing vehicles, planes, ships and trains, and we also have an abundant amount of natural resources,” Innovation, Science and Industry Minister Navdeep Bains told Radio-Canada.

“We could be a world leader in [electric vehicle] battery manufacturing if we leverage our natural resources like lithium, cobalt … nickel, aluminum — the key ingredients that are required in batteries. Then we want to make sure that we manufacture them here and … use them in our trains, our buses, our ships and our planes.”

Bains said the green technology sector is expected to be worth trillions of dollars in the coming years and Canada could take advantage of that market by positioning itself as the chief North American supplier of batteries for electric vehicles.

“Not only do we want to be in a position to be building [electric vehicle] batteries here in Canada for the North American market, we want to be a global leader to take advantage of global opportunities,” he said.

CBC News has confirmed a report which first appeared in the Toronto Star — that the federal government is willing to put up to $500 million, with some money coming from the Ontario government, toward turning Ford’s Oakville plant over to the production of electric vehicles, an investment that could keep the plant open for years to come.

The paper reported that the mass production of electric vehicles and batteries is at the heart of talks between Ford Motor Co. and the union representing its employees.

When asked about the deal yesterday Ontario Premier Doug Ford said negotiations are still ongoing.

“What I can tell you is how important the auto industry is, one of the most important industries in Ontario,” he said during his daily briefing.

“This is good if we move forward. The parts are very important. We would like to manufacture the batteries here rather than bringing the batteries in from out of country. We have the capabilities and the raw materials here. Why can’t we produce the batteries? That’s my big ask to Ford.”

Adding value through manufacturing

Bains also said his government is looking at putting money into high-speed internet access — something he said the country needs more of now, with more and more Canadians working from home.

He also said the federal government is looking at investments in the agriculture sector to help make Canada “a world leader in plant proteins.”

Bains did not say if the agriculture and internet proposals will be a part of the throne speech.

“The bottom line is that we want to take advantage of what we have in Canada,” he said. “And what we have is an incredibly skilled labour workforce, we have natural resources and we have the ability to add value through our manufacturing processing initiatives.”

Posted by AGORACOM-JC

at 8:27 AM on Tuesday, September 15th, 2020

Announced that Tartisan has staked an additional ten single-cell mining claims contiguous to the Kenbridge Nickel Deposit patented and unpatented mining claim group, as well as an additional ten single-cell mining claims in a new area some 2.14 km to the northwest

The newly acquired claims bring the total claim count to 43 single-cell mining claims adjoining the Kenbridge patented mining claim group

TORONTO, ON / September 15, 2020 / Tartisan Nickel Corp. (CSE:TN)(OTC PINK:TTSRF)(FSE:A2D) (“Tartisan”, or the “Company”) is pleased to announce that Tartisan has staked an additional ten single-cell mining claims contiguous to the Kenbridge Nickel Deposit patented and unpatented mining claim group, as well as an additional ten single-cell mining claims in a new area some 2.14 km to the northwest. The newly acquired claims bring the total claim count to 43 single-cell mining claims adjoining the Kenbridge patented mining claim group. Each single-cell mining claim covers an area of approximately 20.92 ha. for a total area of 899.56 ha. The Kenbridge Nickel Project has now a combined total of 2,287.41 ha. of patented and unpatented mining claims.

The new lands were staked to cover multi-faceted anomalies that were discovered from analysis of spectral data and synthetic aperture data from the Aster Funds Ltd surveys carried out over the Kenbridge Nickel Property and environs.

The Aster Funds Ltd spectral analysis survey generated sixteen different elements, six of which are directly related to the mineral suite at the Kenbridge Nickel Deposit. Five areas with six out of six indicator elements as well as a favourable structural setting were determined, four of which were inside the patented ground and previously staked single-cell mining claims. One such six out of six anomaly was discovered just off the property to the south, also in the structural corridor in which the Kenbridge Nickel Deposit is situated. This newly discovered area was covered by the new claim staking.

In addition, the spectral analysis and synthetic aperture radar surveys outlined other anomalies, further afield. One such area is to the northwest, where a six/six anomaly and large five/six margin may highlight a parallel structure. This anomaly sits on top of a large magnetic anomaly in Ontario Geological Survey data. As well, a five/six anomaly in a large four/six margin was seen on the eastern side of the existing Kenbridge Property, and may represent another mineralized corridor, in as much as two of the minerals were talc and pyrrhotite, which represent mineralization and the host tectonic structure of the Kenbridge Nickel Deposit.

CEO Mr. Mark Appleby said, “The Kenbridge Nickel Deposit sits in a mineralized zone that has a strike length of approximately 250 m, as indicated by drill data. The mineralization has been investigated in detail on two underground levels and with drilling to a depth of 823 m. It makes sense that there may be other similar tectonic structures to the Kenbridge Deposit and the new staking covers two of these potential areas. The Company will follow up on these anomalies on the ground as well as the very prospective targets the surveys found inside the Kenbridge Property boundaries”.

Tartisan Nickel Corp. plans surface exploration and a definition plan for the Kenbridge Project for the autumn of 2020 and winter of 2021.

About Tartisan Nickel Corp.

Tartisan Nickel Corp. is a Canadian based mineral exploration and development company which owns; the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel & Technologies Limited and Peruvian Metals Corp.

Tartisan Nickel Corp. common shares are listed on the Canadian Securities Exchange (CSE:TN; US-OTC:TTSRF; FSE:A2D). Currently, there are 101,603,550 shares outstanding (103,303,550 fully diluted).

For further information, please contact Mr. Mark Appleby, President & CEO and a Director of Tartisan Nickel Corp. at 416-804-0280 ([email protected]). Additional information about Tartisan Nickel Corp. can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

Jim Steel MBA P.Geo. is the Qualified Person under NI 43-101 and has read and approved the technical content of this News Release.

This news release may contain forward-looking statements including but not limited to comments regarding the timing and content of upcoming work programs, geological interpretations, receipt of property titles, potential mineral recovery processes, etc. Forward-looking statements address future events and conditions and therefore, involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements.

The Canadian Securities Exchange (operated by CNSX Markets Inc.) has neither approved nor disapproved of the contents of this press release.

Posted by AGORACOM

at 11:07 AM on Tuesday, September 1st, 2020

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

The deepest hole extends to 838.4 metres, intersecting mineralization grading 4.25% nickel and 1.38% copper over 10.7 metres

The deposit remains open at depth

Tartisan completed a Spectral Analysis Survey that identified the Kenbridge Deposit, and has shown a possible extension and three additional trends

Owns 17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property and are drilling their Iska Iska Pollymetallic project in Bolivia

Tartisan currently owns close to 4 million ELO shares

Tartisan owns close to 1,700,000 shares in Class 1 Nickel (CSE:NICO)

Tartisan vended the Alexo- Kelex asset to Class 1 Nickel, who recently listed on CSE

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is equipped with a 623m deep shaft and has never been mined

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits

Plans for Kenbridge include updating PEA, advancing the project through to feasibility and exploring the open mineralization at depth

Recent News

Company has completed a Spectral Analysis Survey

Survey covered the patented and single-cell mining claims that make up the historic land position which contains the Kenbridge Deposit and the surrounding area, identifying several new exploration targets not only for nickel, copper, cobalt, but also for potential gold occurrences

Analysis Survey shows the distribution and intensity of up to 304 minerals, with the first pass showing up to 16 minerals

Each mineral can be classified into an exploration relevance for base metals, precious metals and industrial metals

Tartisan CEO Mark Appleby said, “the survey picked out the Kenbridge Deposit, and has shown the possible extension to the Kenbridge Deposit and three additional trends that relate directly to underlying geology and structure implicit in the Kenbridge Deposit. Of significant interest, the survey found two gold trends as well, which include the Violet and Nina historic gold occurrences. One of the occurrences is almost 54 hectares in size and covers almost all of three of our staked claims on the border of the Kenbridge property.”

DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM

at 10:06 AM on Thursday, August 27th, 2020

SEOUL (Reuters) – Tesla Inc (TSLA.O) CEO Elon Musk has suggested the U.S. electric carmaker may be able to mass produce batteries with 50% more energy density in three to four years, which could even enable electric airplanes.

SEOUL (Reuters) – Tesla Inc (TSLA.O) CEO Elon Musk has suggested the U.S. electric carmaker may be able to mass produce batteries with 50% more energy density in three to four years, which could even enable electric airplanes.

His comments came as speculation is growing about announcements at Tesla’s anticipated “Battery Day” event where it is expected to reveal how it has improved its battery performance.

“400 Wh/kg *with* high cycle life, produced in volume (not just a lab) is not far. Probably 3 to 4 years,” Musk tweeted on Monday in response to a Twitter thread by Sam Korus, an analyst at ARK Investment Management LLC, about why Musk keeps hinting at a Tesla electric plane.

Researchers have said the energy density of Panasonic’s (6752.T) “2170” batteries used in Tesla’s Model 3 is around 260 Wh/kg, meaning a 50% jump from the current energy density which is key to achieving a longer driving range.

Musk said last year that for electric flight to work, the energy density of batteries needed to improve to over 400 Wh/kg, a threshold which may be achieved in five years.

The electric car manufacturer also showed an image where a number of dots are clustered in line formations, sparking speculation among media and fans about what it will reveal at the event. (here)

South Korean battery expert Park Chul-wan said the image may hint at “silicon nanowire anode,” a breakthrough technology which can potentially increase both battery energy density and battery life sharply.

Panasonic Corp (6752.T) earlier told Reuters that it plans to boost the energy density of the original “2170” battery cells it supplies to Tesla by 20% in five years.

Tesla is also working with China’s Contemporary Amperex Technology Ltd (CATL) (300750.SZ) to introduce a new low-cost, long-life battery in its Model 3 sedan in China later this year or early next year, with the batteries designed to last for a million miles of use, Reuters reported in May.

Tesla has said its Battery Day will take place on the same day as its 2020 annual meeting of shareholders on Sept. 22.

A very “limited number of stockholders” will be able to attend both of the events due to pandemic-related restrictions, Tesla said, and a lottery will be held to select attendees.

Posted by AGORACOM

at 9:29 AM on Tuesday, August 25th, 2020

“I’d just like to re-emphasize, any mining companies out there, please mine more nickel,” said Musk

Nickel is arguably the single most important metal component in EV batteries.

In the popular imagination, lithium is the element that powers EVs. However, as Elon Musk has pointed out, the term “lithium-ion batteries” is something of a misnomer, because they don’t really contain that much lithium. “Although [they’re] called lithium-ion, the actual percentage of lithium in a lithium-ion cell is approximately 2%,” Musk explained at Tesla’s 2016 shareholder meeting. “Technically, our cells should be called nickel-graphite, because the primary constituent in the cell as a whole is nickel.”

More recently, Musk reiterated the importance of nickel, and made what sounded to some like an urgent plea for more of the stuff. “I’d just like to re-emphasise, any mining companies out there, please mine more nickel,” said Musk during Tesla’s latest quarterly conference call. “Wherever you are in the world, please mine more nickel and…go for efficiency, obviously environmentally-friendly nickel mining at high volume. Tesla will give you a giant contract for a long period of time, if you mine nickel efficiently and in an environmentally sensitive way.”

However, meeting the expected surge in demand for element #28 may not be so easy, because of various supply-side issues. In a recent interview with Kitco News, Michael Beck, Managing Director at Regent Advisors, said he sees something of a “perfect storm” brewing in the nickel trade.

A Tesla Model 3 contains around 30 kilograms of nickel, Beck told Kitco’s Michael McCrae. “Nickel is probably the single most important metal component in battery fabrication. It’s where all of the energy is stored, and increasingly battery chemistries are being refined to allow the inclusion of as much nickel as possible. The more nickel, the higher the energy density of the battery.”

The spotlight on nickel is a recent development. Nickel prices collapsed in 2007, and there’s been little development of new capacity since then, says Beck. “In this intervening almost 12 years there was no material investment in new nickel capacity. The last 12 years has been a drawdown of excess inventory, and that’s coming to an end. The ramp-up of demand is just beginning.”

The long lead time for bringing new nickel mines into production is another constraining factor. “It takes 7 to 10 years to bring on new nickel projects,” says Beck. “So, you have the makings of a perfect storm. You have a baked-in structural deficit for the next 12 years…you have inventories in the next 18 months going down to almost zero. You also have this new demand source that never existed for nickel.”

Above: Ken Hoffman, senior expert at McKinsey, weighs in on Tesla’s need for nickel in order to expedite the EV revolution (YouTube: Kitco NEWS)

All that would seem to add up to an investment opportunity for somebody. “In the universe of metals, [nickel is] our favorite,” says Beck. “We think in the next two to three years you’re going to see a major up-tick of the nickel price…as shortages emerge, and that’s what’s going to be required to get new investment in the sector.”

So, what companies are poised to take advantage of the coming nickel rush? “Maybe the most interesting in the larger cap of established players is Norilsk,” says Beck. “They’re the number-two nickel producer, and they’re based in Russia. That’s probably the single best large-cap way to get exposure to nickel. It’s a major producer of the metal, and when nickel goes up, their share price goes up accordingly. At the smaller cap end of the spectrum, there are a bunch of smallish nickel explorers and emerging developers.”

Over the next few years, Beck believes that nickel shortages will emerge, and most companies with nickel exposure will benefit. However, there’s another factor in play. Tesla and other EV-makers are naturally eager to get their raw materials from sustainable sources. The industry has invested much effort and cash in cleaning up its supply chain for cobalt. Elon’s recent plea for nickel specified that it needed to be mined in an environmentally sensitive way. (Norilsk, by the way, has recently been involved in not one but two oil spills in Russia’s Arctic region.)

Vancouver-based Giga Metals quickly responded to Elon’s appeal, saying that it has a source of environmentally-responsible nickel in development. As Matthew Hall reports in Mining Technology, Giga Metals owns a property called Turnagain in north-central British Columbia, which it says is one of the largest undeveloped sulphide nickel projects in the world, and also contains cobalt.

Canada has plenty of nickel mines, but Giga Metals has a unique vision for the Turnagain mine. “Our goal is to be the world’s first carbon-neutral mine,” said Giga Metals President Martin Vydra. “We plan to use power from BC Hydro’s clean energy grid, which will involve more capital expenditure than the alternatives, but is the right thing to do.”

Above: Tesla’s Model 3 (Source: EVANNEX; Photo by Casey Murphy)

“If you want environmentally-responsible nickel, I really think you have to look at sulphide deposits in first-world jurisdictions such as Canada and Australia,” said Giga Metals CEO Mark Jarvis. “Canada has several very large, low-grade, open-pittable sulphide nickel deposits waiting to be developed, including Canada Nickel’s Crawford deposit, Waterton’s Dumont deposit and our own Turnagain deposit. Canada has some of the toughest environmental regulations in the world, so if you buy your nickel from Canada, you can be assured that this part of your supply chain is ethically sourced.”

.png)

.png)