Posted by AGORACOM

at 9:59 AM on Thursday, November 5th, 2020

Class 1 Nickel posts a two-million-tonne-plus resource at Alexo-Dundonald Project

Tartisan owns close to 1,700,000 shares of Class 1 Nickel (NICO:CSE) through vending of Tartisan’s Alexo-Kelex nickel asset in 2018

Crushed ore at the Alexo Mine site near Timmins in 2005.

A new nickel sulphide player has fully emerged in the Timmins camp seeking to revive a well-known piece of mining ground.

Class 1 Nickel and Technologies released a very promising new mineral resource estimate for its Alexo-Dundonald Nickel Project, 45 kilometres northeast of the city.

The Toronto-based company reported an updated estimated indicated mineral resource of 1.25 million tonnes with an average grade of 0.99 per cent of nickel, and a total estimated inferred mineral resource of 1.01 million tonnes with an average grade of 1.08 per cent.

The indicated resource count has jumped 119 per cent since the last mineral estimate in June. The inferred resource ballooned by 1,400 per cent.

The company thinks it has a turn-key project on its hands that can be fast-tracked into nickel and cobalt production with little capital expenditure.

With nickel, cobalt, copper, and platinum group elements in the ground, the company has eyes on supplying battery-grade material for the electric vehicle and stainless steel markets. Nickel sulphide is used in electric vehicle battery cathodes.

Class 1, which went public over the summer on the Canadian Securities Exchange, had been quietly assembling a 20-square-kilometre package of properties that hosted two former small-scale nickel mines along some promising exploration ground that follows a large ‘Z’-shaped group of komatiite rocks, known to contain nickel sulphide.

The project property includes two former one-pit and underground mines – the Alexo and Kelex – that ceased operations in 2005 due to low nickel prices, plus the nearby Dundonald property which contains nickel-bearing zones.

Alexo and Kelex were mined for nickel and copper three separate times around the time of the First World War, during the Great Depression and the Second World War, and lastly between 2004 and 2005.

Class 1 said much of the property has never been probed by drilling and modern geophysics. The last drilling program at Alexo-Kelex was done in 2011, and at Dundonald in 2005.

The company’s exploration program of geophysics has been focused on expanding the resource left behind at Alexo and Kelex, and probe the Dundonald property on the way to planning a drill program and eventually releasing a preliminary economic assessment report for a possible mine.

Management is currently out raising $3 million in flow-through shares for exploration.

Posted by AGORACOM

at 9:37 AM on Tuesday, October 27th, 2020

Hole ND-10-03 intersected 4.53% Ni, within a larger interval averaging 1.02% Ni, 0.38% Cu over 4 metres.

The mineralization remains open along strike and to depth.

Claims previously owned by Canadian Arrow Mines Limited in 2010

TORONTO, ON / ACCESSWIRE / October 27, 2020 / Tartisan Nickel Corp. (CSE:TN)(OTC PINK:TTSRF)(FSE:A2D) (“Tartisan”, or the “Company”) is pleased to announce that the Company has acquired the Night Danger, Glatz nickel-copper claims located in the Turtle Pond Project area near Dryden, Ontario.

The Company has acquired a 100% interest in the Glatz, Night Danger Nickel-Copper Claims located approximately 70 kms from the Company’s flagship Kenbridge Nickel Deposit. The property is situated in an area of excellent infrastructure and consists of 16 claim units. The 16 claim unit property hosts the historical Glatz and Night Danger nickel-copper showings. Previous exploration efforts identified nickel-copper sulphide mineralization in twelve trenches along a 700 metre trend at the Glatz nickel copper showing. The zone, discovered in 1965 by local prospector A. Glatz, is up to 40 metres wide and is open along strike and at depth. Historical grab samples were reported to contain up to 1.95% Ni. In 2007, Canadian Arrow Mines Limited conducted a surface grab sampling program which produced the following results: 1.28% Ni, 0.26% Cu re Glatz Trench 3; 0.99% Ni, 0.18% Cu re Glatz Trench 3; 0.39% Ni, 4.06% Cu re Trench 4. The mineralization varies from disseminated sulphides to narrow semi-massive sulphide bands. Six short drill holes were completed at that time with hole GZ-09-02 encountering 0.34% Ni, 0.16% Cu and 0.02% Co over 5.9 m from 45.0-50.9 m.

Exploration diamond drilling work completed in 2009 and 2010 on the Night Danger nickel-copper showing reported a nine metre wide section of stringers and blebs of sulphide which assayed 0.57% Ni and 0.45% Cu at a drill depth of 79m in hole ND-09-1. Two sections within this interval assayed greater than 1% nickel. Drill hole ND-10-1 intersected 4.53% Ni over 0.7m at a drill depth of 57.5m (Source; MNDM assessment files and Canadian Arrow Mines Limited news release dated June 1, 2010).

Mark Appleby, President and CEO of Tartisan stated, “The Glatz and Night Danger nickel-copper showings display similar nickel and copper tenors as what we find near surface at our Kenbridge Nickel Deposit. Acquisition of these showings complements the company’s larger objective of developing the Kenbridge Nickel Deposit into an operating mine with a central milling facility.”

About Tartisan Nickel Corp.

Tartisan Nickel Corp. is a Canadian based mineral exploration and development company which owns; the Kenbridge Nickel Project in northwestern Ontario; the Sill Lake Silver property in Sault Ste. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel and Technologies Limited and Peruvian Metals Corp.

Tartisan Nickel Corp. common shares are listed on the Canadian Securities Exchange (CSE:TN; US-OTC:TTSRF; FSE:A2D). Currently, there are 101,603,550 shares outstanding (107,203,550 fully diluted).

For further information, please contact Mr. D. Mark Appleby, President & CEO and a Director of the Company, at 416-804-0280 ([email protected]). Additional information about Tartisan can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

Posted by AGORACOM

at 9:58 AM on Wednesday, October 7th, 2020

By Ellsworth Dickson

Nickel is a most useful base metal. Because rust never sleeps, some 75% of nickel produced is used to make stainless steel, most being what is known as Class 2 nickel. Class 1 nickel, or pure nickel, is used for making steel alloys, storage batteries for laptops and cell phones and, of increasing importance, electric vehicle (EV) batteries.

Nickel is part of the cathode in a Li-ion battery. It is these Li-ion batteries that are kick-starting a sea change in the nickel market.

Combining all uses, nickel demand grew 9.4% during 2018 and 2018 – outperforming all other major base metals – making it a US$20 billion per year industry. In 2018, Canadian exports of nickel-based products totaled $4.2 billion with Canada ranking fifth in the world for mine production.

Nickel prices are currently trading around US$14,000/tonne, or US$6.42/lb, up more than 30% from March lows and near its highest levels in November 2019.

And while stainless steel and other nickel usages continue to steadily grow as the world’s population increases, it is the EV market that is expected to see a huge growth in nickel demand, according to senior miner Glencore. For the first time, in 2017, sales of EVs passed the 1 million mark; however, this is just the beginning.

According to the International Energy Agency, (IEA), sales of electric cars topped 2.1 million globally in 2019, surpassing 2018 – already a another record year – to boost the stock to 7.2 million electric cars, 47% of which were in China. It’s hard to believe that in 2010, there were only 17,000 EVs on the road. Electric cars, which accounted for 2.6% of global car sales and about 1% of global car stock in 2019, registered a 40% year-on-year increase.

In their recent report, the IEA stated that nine countries had more than 100,000 electric cars on the road. At least 20 countries reached market shares above 1%. However, this growth has sometimes been disrupted by various events and circumstances that negatively affected EV sales.

Deloitte’s outlook shows EV sales reaching 21 million vehicles in 2030 as the cost of manufacturing batteries falls significantly and range anxiety becomes less of a concern. Another challenge for would-be EV buyers is availability of charging stations out of town and, in tow, lacking of charging stations in older apartment buildings.

This huge increase in EV sales will be even more jump-started with the introduction of electric pickup trucks, SUVs, delivery trucks and semi tractor trailers. This could cause a supply crunch for Class 1 nickel.

Interestingly, the IEA noted that electric two/three-wheelers will continue to represent the lion’s share of the total electric vehicle fleet, as this category is most suited to rapid transition to electric drive. The future electric two/three-wheeler fleet is concentrated in China, India and the ten countries of ASEAN.

Wood Mackenzie predicts an increase in nickel demand for EVs from 128 kt in 2019 to 265 kt in 2025 and 1.23 Mt in 2040, increasing nickel battery demand from 4% in 2018 to 31% by 2040.

It has been estimated that by 2025 the world need almost 1 million tonnes per year of new nickel supply. By 2030, 2.5 million tonnes, or double that of today, is required.

Wood Mackenzie is forecasting an average annual nickel deficit of 60,000 tonnes through to 2027 – a situation that bodes well for nickel explorers, developers and producers.

About one-half of the world’s nickel supply is suitable for use in batteries such as the nickel sulphide mines in Sudbury, Voisey’s Bay and Russia.

Those companies involved in discovering and mining nickel deposits are participating in a massive unstoppable global event with the electrification of the world’s vehicles – a good place to be.

Tartisan Nickel Corp. [TN-CSE; TTSRF-OTC; A2D-FSE] has favourably positioned itself to participate in the growing electric vehicle sector with its advanced-stage Kenbridge nickel-copper-cobalt project in northwestern Ontario.

While copper and cobalt are important for the EV battery and vehicle market, Elon Musk of Tesla Motors recently stated that nickel remains a key ingredient to its rapidly improving EV battery technology. Stainless steel production still accounts for the majority of nickel usage; however, commodity research firm Roskill has stated that the current EV nickel demand will grow from 4% to 15-20% of the market.

Longer term, California Governor Gavin Newsom just signed an executive order that will ban the sale of new gas-powered passengers cars starting in 2025.

Tartisan’s Kenbridge Project, located near Atikwa Lake in the Kenora-Fort Frances area, has undergone an updated mineral resource estimate.

The updated estimates were done for pit constrained and out-of-pit nickel, copper, and cobalt resources. Total Measured & Indicated Mineral Resources, based on a Net Smelter Return (NSR) cut-off value of CDN$15/tonne for pit constrained Mineral Resources and CDN$6/tonne NSR for out-of-pit Mineral Resources is 7.5 Mt at 0.58% nickel and 0.32% copper for a total of 95 Mlb of contained nickel. An additional 0.985 Mt at 1.0% nickel and 0.62% copper (22 Mlb contained nickel) were calculated as Inferred Resources. Pit constrained Measured & Indicated Resources total 5.27 Mt of 0.45% nickel, 0.26% copper and 0.009% cobalt at an NSR cut-off value of CDN$15/tonne. The out-of-pit Measured & Indicated Resources total 2.23 Mt of 0.86% nickel; 0.45% copper; and 0.006% cobalt. Inferred Mineral Resources out-of-pit total 0.985 Mt at 1.00% nickel, 0.62% copper and 0.003% cobalt, at an NSR cut-off value of CDN$60/tonne.

Mark Appleby, President and CEO, notes that the deposit is open to depth with the highest nickel grades having a strong down-plunge orientation such as hole KB07-180 that returned 2.95% nickel and 0.82% copper over 21.5 metres, including 7.2% nickel and 0.67% copper over 5.5 metres.

Highlights of an Updated PEA were: average nickel recovery life-of-mine was 86%; recovered nickel was 84.6 Mlb; NPV7.5% pre-tax was $253M; and IRR% pre-tax was 65%.

The Kenbridge property has good access to roads and power. It has a shaft to a depth of 622 metres, with level stations at 45-metre intervals below the shaft collar and two levels developed at 107 metres and 152 metres below the shaft collar.

Tartisan Nickel has planned a surface exploration and definition drilling plan, in addition to geotechnical, metallurgical and environmental work to advance the project in the upcoming 2020 winter season and into summer 2021.

The company also owns equity stakes in Eloro Resources Ltd. that is exploring the 99%-optioned ISKA ISKA Project, a gold-silver-zinc-lead target with a 3,500-metre underground drilling program underway in the Potosi district, Bolivia, and the low-sulphidation epithermal 82%-owned La Victoria gold-silver project in Peru.

Tartisan is a shareholder in Class 1 Nickel and Technologies that holds the past-producing Alexo-Kelex Dundonald nickel project near Timmins, Ontario in which Tartisan has a 0.5% NSR. The property hosts an estimated total NI 43-101 compliant Indicated Mineral Resources of 571.7k tonnes averaging 0.77% nickel plus Inferred Resources.

Being a prospect generator, Tartisan spun out the Alexco-Kelex Project to Class 1 Nickel as well as the La Victoria Project to Eloro.

Tartisan is a shareholder in Peruvian Metals Corp. that is operating a toll mill in Peru and announced an exploration and bulk sampling program on the high-grade gold-silver-copper Palta Dorada Project.

Tartisan also has a 100% interest in the Sill Lake silver-lead project near Sault Ste. Marie, Ontario.

Tartisan’s investment portfolio is in excess of $7 million which can provide funds for its activities and avoids share dilution through further share issuances. The company has 101.6 million shares outstanding.

Though its acquisitions and investments, Tartisan Nickel is poised to benefit from the burgeoning EV battery sector as well as its precious metal and base metal prospects.

Garibaldi Resources Corp. [GGI-TSXV; GGIFF-OTC; RQM-FSE] has been following up its 2017 magmatic nickel massive sulphide discovery in the Golden Triangle region of northwestern British Columbia.

Located on Nickel Mountain, the flagship E&L deposit hosts nickel, copper, cobalt, platinum, palladium gold and silver. The latest drill results from the 2020 program have extended the strike length of the mineralized E&L system from 200 metres to over 650 metres to the east, where the intrusion remains open.

The 100%-owned project is the Golden Triangle’s first magmatic nickel-copper-rich massive sulphide system in the heart of the prolific Eskay Camp. The 2017 discovery drill hole EL-17-14 intersected 8.3% nickel, 4.2% copper, 0.19% cobalt, 1.96 g/t platinum, 4.5 g/t palladium, 1.1 g/t gold and 11.1 g/t silver over 16.75 metres starting 100.4 metres downhole, within a broader 40.4-metre core length highlighted by 3.9% nickel and 2.4% copper.

In February, 2019, Garibaldi confirmed an even shallower new zone (Northeast Zone) with drill hole EL-18-33 that returned 7.7% nickel and 2.95% copper over 4.8 metres within a broader interval of 49 metres grading 1.34% nickel and 0.89% copper (core length) plus cobalt, platinum, palladium, gold and silver credits.

Diamond drilling continues to build out on the persistent widespread nickel-copper mineralization, which includes massive sulphides featuring top-tier nickel-copper grades in addition to palladium, platinum, cobalt, gold, silver and strategic PGE (platinum group element) rare metals, including rhodium.

Hole EL-20-88, collared 350 metres east of pivotal hole EL-19-80, intersected 142.79 metres of mineralized taxitic gabbro and olivine pyroxenite along trend of the E&L system. This large step-out hole exhibited an E&L geochemical signature which expanded the strike length of the E&L gabbroic intrusion to over 650 metres within a 2-km structural corridor that remains untested and open.

Hole El-20-89 has produced the widest mineralized intercept so far from 71.34 metres to 223 metres returning nickel-copper mineralization over 151.6 metres grading 0.56% nickel and 0.61% copper. This intersect included 80.53 metres of 0.88% nickel and 0.85% copper, which expanded the northeastern massive sulphide zone six metres south, the LDZ 15 metres north and the Second Chamber 45 metres west.

Semi-massive veins along the contact edge with sediments assayed 0.33 metres (100.54 to 100.87 m) of 6.87% nickel and 1.69% copper, and 0.15 metres (147.48 to 147.63 m) of 3.04% nickel and 1.62% copper.

Garibaldi has drilled 10 additional holes at the E&L project on Nickel Mountain and is up to hole 94 so far this season. With new geochemical and geophysical targets located at depth, the immediate goal of the drill program is to follow the steeply-plunging E&L gabbro to the east. The conductors detected off hole will be drill tested for mineralization.

Garibaldi owns 100% of more than 200 km2 in Eskay Camp, including newly discovered high-grade gold quartz vein system at Casper, located 15 km north of Nickel Mountain. Assays are pending. The company also has four projects in Mexico.

Garibaldi’s nickel discovery is a unique development in the Golden Triangle with excellent potential for significant expansion at a time of increasing nickel demand from the electric vehicle market.

Just 12 km north of the E&L nickel deposit is Garibaldi’s 100%-owned Casper high-grade gold quartz vein discovery. The Casper gold vein is a strategic low elevation target (420 metres) within a km of road access and hydroelectric power.

Field crews collected 165 samples within 250 metres north of and 250 metres south of the northwest-southeast-striking Casper vein. High-grade grab samples at Casper were reported up to 249 g/t gold and assays for 86 Casper channel samples have been released with up to 92 g/t gold and 5.69 g/t gold over 52 metres.

Mechanical trenching at the Casper gold quartz vein has further uncovered the high-grade vein over more than 120 metres, from the initial 43 metres of hand trenching exposing the discovery.

The quartz vein remains open with mineralized rock samples extending along trend for 330 metres within a 500-metre gold-in-soil and MMI (mobile metal ion) geochemical anomaly.

The latest assays from 61 channel sample assays returned gold grades ranging from 0.676 g/t gold up to 93.29 g/t gold from a channel sample that contained visible gold.

The company has 116 million shares outstanding.

Sama Resources Inc. [SME-TSXV; SAMMF-OTC.PK] is a Canada-based mineral exploration and development company with projects in West Africa, in particular, the Samapleu nickel-copper-cobalt-platinum group metals project in Côte d’Ivoire (Ivory Coast).

Sama’s projects are located approximately 600 km northwest of Abidjan in Côte d’Ivoire and adjacent to the Guinean border in West Africa.

In 2010, Sama discovered nickel-copper-PGE mineralization, including veins and lenses of high grades material near surface at numerous locations within the then discovered Yacouba intrusive complex.

In October, 2017, Sama announced that it had entered into a binding term sheet in view of forming a strategic partnership with HPX TechCo Inc., a private mineral exploration company in which mining entrepreneur Robert Friedland is a significant stakeholder, in order to develop the Samapleu Project. HPX is spending $18 million on the project.

Since March 2010, Sama has performed surface IP and Mag surveys as well as Airborne Mag-Radiometric and HTEM surveys and 388 boreholes for a total of 54,000 metres of drilling. Mineral resources assessments have been completed at one site, the Samapleu deposit, aiming for a modest scale Ni-Cu open pit mining and processing operation, while continuing to explore newly discovered prospective ground. Sama’s objective is to delineate massive sulphide reservoirs that could be the source of these high-grade nickel–copper-cobalt-palladium lenses. The newly discovered Yacouba complex can be compared to other world class bases metals camps like Jinchuan in China and Voisey’s Bay in Canada, etc.

Highlights of a Preliminary Economic Assessment at Samapleu, include average annual production of 3,900 tonnes of carbonyl nickel powder, 8,400 tonnes of carbonyl iron powder and 14,100 tonnes of copper concentrate over a 20-year mine life. Capital costs are estimated to be $282 million, including a contingency of $37 million with operational costs of $23.96/tonne milled.

Pre-tax Net Present Value (8% discount rate) is $615 million and an Internal Rate of Return of 32.5%. After-tax NPV (8% discount rate) of $391 million and an after-tax IRR of 27.2%.

Geophysical activities have resumed with downhole electromagnetic surveys planned in four deep drill holes at the Yepleu target zone and in one deep drill hole at the Bounta target zone. The holes at Yepleu and Bounta were drilled in the early months of 2020, with both zones part of the large Yacouba Ultramafic-Mafic intrusive complex discovered by Sama in 2010.

Future production will be managed by a JV controlled 66⅔% by Sama Nickel Corp. a wholly-owned subsidiary of Sama Resources, and 33⅓% by SODEMI. Sama Resources has $2.5 million in its treasury and holds $12.4 million in securities with no debt. The company has 216,466,410 shares outstanding.

The Samapleu nickel-copper-cobalt-platinum group metals project is located in mining-friendly West Africa, home to a number of successful mining operations. The polymetallic project hosts a suite of metals – nickel-copper-cobalt-platinum group metals – all of which are currently in demand.

Posted by AGORACOM

at 9:09 AM on Tuesday, October 6th, 2020

Volatility in the gold market continues.

I’m not sure when it will end.

With the gold market moving mostly sideways, base metals have been on my mind as of late.

Copper, zinc and nickel are all seeing nice strength in their price.

Will it continue?

That’s a great question.

One of the biggest lessons I have learned over the last few years is that markets are complex and, therefore, impossible to predict with any consistency.

As such, I don’t let my view on the metal price dictate how I invest my money in the junior resource sector.

Remember, junior resource companies are speculations on management’s ability to pick the right projects, form action plans to add value and, of course, raise the money needed to execute on their action plan.

Without successful execution, it doesn’t matter how high the metal price goes, there is a high probability of losing money.

With that said, I do like to understand the metals markets as best I can and form a view of where the market is and where it is going.

Let’s take a closer look at the nickel market.

The Musk Effect

“In the short-term, the market is a voting machine and in the long-term, it’s a weighing machine.” ~ Rick Rule

Sentiment or narrative can be a major driver of a market in the short term, however, in the long term, the fundamentals of a company or a metals market need to be solid for gains to be sustained and perpetuated.

The cream always rises to the top.

In my view, the current nickel market is driven more by sentiment than its underlying fundamentals and, therefore, I’m skeptical of whether the nickel price can continue on its trajectory upwards.

Nickel’s bullish sentiment, I believe, has been derived from the comments made by Elon Musk, Billionaire Founder of Tesla, earlier this year.

Musk made a reference to nickel during one of Tesla’s post-earnings conference calls saying,

“Well, I’d just like to re-emphasize, any mining companies out there, please mine more nickel. Okay. Wherever you are in the world, please mine more nickel and don’t wait for nickel to go back to some long — some high point that you experienced some five years ago, whatever. Go for efficiency, obviously environmentally friendly nickel mining at high volume. Tesla will give you a giant contract for a long period of time, if you mine nickel efficiently and in an environmentally sensitive way. So hopefully this message goes out to all mining companies. Please get nickel.”

In my view, these comments set off two narratives;

The first, and arguably the most potent, is Musk’s request for efficient and environmentally sensitive nickel mining.

The second is Musk’s general request for more nickel to be produced.

Environmentally Sensitive Nickel Mining

A big question for me is whether Musk really understands what he is asking for when he says,

“Tesla will give you a giant contract for a long period of time, if you mine nickel efficiently and in an environmentally sensitive way.”

Efficient and environmentally sensitive mining, I find that very vague.

Does it mean he is making a distinction between nickel sulphide and laterite mining?

Or, does it mean, nickel mining operations that derive their power from renewable sources?

Or, is it nickel mining operations that are carbon neutral?

If this narrative is driving the market, more questions need to be asked.

Class #1 Nickel – Sulphide Versus Laterite

For those who don’t know, nickel sulphide mines produce nickel concentrates that are sold to smelters, which then convert the concentrate into the chemical nickel sulphate which is used by battery manufacturers.

In the case of nickel laterite mines, the ore is mined and then processed through a high pressure acid leach (HPAL) circuit, which is then further processed to produce nickel sulphate.

To add, the HPAL process is more complex, requiring more steps to get to the end product and, generally speaking, has a higher carbon foot print due to emissions from the process.

It, therefore, could be the distinction that Musk is trying to make with his comments.

It’s hard to tell.

Renewable Energy Source

No matter how you slice it, most of the energy generated worldwide is still derived from fossil fuels.

Therefore, even if the mining operation is fully electrical, to be deemed environmentally sensitive, you must determine how the electricity was produced.

Was it via nuclear power or renewables?

In fact, you really have to go a step further and realize that the dams for the hydro power, the construction and materials used in nuclear power plants, the solar panels and the wind turbines were all made with metals and/or concrete, which were mined and by equipment that was most likely fueled by fossil fuels.

My point?

Stating a nickel mine has to produce its nickel in an environmentally sensitive way needs to be further defined before it’s a realistic narrative driving the nickel market.

With this said, at the moment, I’m only aware of one junior nickel company that can actually say that it has the potential to be carbon neutral.

That company is FPX Nickel Corp. (FPX:TSXV).

This isn’t meant to be an advertisement for FPX, but the reality is, it’s the only junior nickel company that I can see could even come close to fitting Musk’s criteria.

Remember from my update on FPX earlier this year, I mentioned that UBC and Trent University were collaborating on a research program which is investigating carbon capture and storage at mining sites.

FPX’s Decar Nickel District is at the centre of this research as the study looks to maximize the reaction between carbon dioxide and magnesium silicate mine tailings.

The Decar mine waste is high in Brucite, which makes it a prime candidate for carbon sequestration.

It’s, therefore, possible that a future mine at Decar could be carbon neutral.

Class #1 Nickel

On to the 2nd narrative – Class #1 nickel supply.

I’m bullish on nickel; my bullishness is supported by the overall fundamentals of the market and the potential for the increase in Class #1 nickel demand.

For those who don’t know, 2/3s of nickel demand is from stainless steel.

Therefore, undoubtedly, if you’re bullish on nickel, you’re bullish on stainless steel.

While stainless steel represents the backbone of the nickel market, however, it’s battery demand that holds the potential to really disrupt the nickel market in the future.

Currently, battery manufacturers make up less than 5% of the global 2 Mt nickel market.

Roughly half of the 2Mt market is derived from Class #1 nickel and this is where it gets really interesting.

In 2018, Glencore commissioned CRU to model the metal requirements of a 30% adoption rate of EVs in the global vehicle market.

The results revealed the following:

As you can see, a 30% adoption rate would result in roughly 1.1 Mt of Class #1 nickel demand.

This is interesting because, as I mentioned, the current Class #1 nickel demand worldwide is roughly 1 Mt.

Given the long duration and expense of exploration and development, which is at least 10 years from discovery to construction, it begs the question, where will the nickel come from?

This is a great question and really speaks to the amount of disruption that could occur.

The next most obvious question, therefore, is what are the odds of the EV adoption rate hitting 30% within the next 10 years?

For me, it will be determined by the following points:

In the short term, what is the affect of a 2nd wave of Covid-19 in the last QTR of 2020?

There are a lot of unanswered questions regarding the last quarter of the year, especially when it comes to a 2nd wave of Covid-19. Further lockdowns would be devastating to the economy.

What is the health of the global economy?

High unemployment and a stagnant economy could stall adoption of EVs for as long as the recession or depression lasts.

Will governments around the world give further incentives to purchase EVs?

Especially in the case of poor global economics, I believe governments will have to continue, if not increase, subsidies for EV adoption. For example, we have seen in China, when the subsidy is removed, people stop buying them.

EV infrastructure spending

Large scale EV adoption will require more EV infrastructure to be built, at home, at work and in the public realm – malls, restaurants, highways, etc.

If left to the free market, I would say we are still a ways away from adopting EVs into our everyday life.

But we don’t live in a free market.

Governments around the world are becoming larger and larger parts of the economy and, therefore, destroy any of the logic or economic factors that usually control markets.

I can’t say with any certainty what will or won’t happen, but what I can say is that if the government decides that the push is toward renewable energy and EV adoption, that is where the money will flow.

For instance, it’s rumoured that the Canadian government will soon unveil their version of “The Green New Deal.”

If true, I would guess that it’s very likely we would see some incentive for EV adoption.

The Canadian market is small and, therefore, I don’t foresee it actually making a discernible difference to the EV market on a whole, but if this is indicative of a broader trend, things might actually fall in place.

Future Role of Nickel Laterites

As I outlined earlier, nickel laterites can be processed into Class #1 nickel with the help of the HPAL process.

Back in 2018, Tsinghan, a Chinese company, made the headlines within the nickel space as they toted the ability to construct a 50,000 tonne per year HPAL plant in Indonesia in just over a year, for $700ishM.

Tsinghan has a great reputation in the market for the pioneering of the NPI processing, which revolutionized the nickel market in the early 2000s.

This proclamation was, therefore, taken literally.

The nickel price sunk, as the market determined that the affect of an increase in demand to Class #1 market over time would be quelled if Tsinghan had this ability to construct a HPAL plant of this size, on the tight construction schedule and for under a billion dollars.

In the 2 years since, Tsinghan has experienced many of the historical delays associated with building a HPAL plant.

They have delayed construction and added upfront capital expenditures to continue to move forward with development.

With that said, in my view, I do believe that Tsinghan will be successful in constructing the plant.

Also, I think that as long as the Class #1 nickel market doesn’t require a certain environmental standard in the future, HPAL processing of nickel laterites will help quell some of the disruption caused by the potential surge in Class #1 nickel demand, albeit at a nickel price higher than US$10/lbs.

Nickel Market Fundamentals

Supply and demand fundamentals must be solid for any market to be strong over the long-term.

As I said, in my view, the current uptick in the nickel price is mainly driven by sentiment rather than underlying supply and demand fundamentals.

With that said, I think that there are many points to be bullish about.

Nickel Inventory

Over the last 5 years, the LME nickel inventories have been trending in the right direction.

As you can see from the graph, the inventory levels have steadily fallen since 2017, with a dramatic draw down in 2019.

The dramatic draw, however, was met with almost as dramatic a spike in the 10 months since, and now sits above the 200kt level.

The LME warehouses an inventory of Class #1 and is a key factor in gauging the health of the nickel market.

If we were to begin to see inventories drawn down once again, it would be very bullish for the nickel price, with the proviso that the reason for its depletion could be linked to a sustained source of demand or a permanent loss of supply.

As it stands right now, in a post pandemic world, nickel market analysts are calling for a surplus of supply to end 2020.

This is in sharp contrast to the pre-pandemic nickel market, where analysts were calling for a supply deficit.

NorNickel Corp Presentation – May 2020

Nickel Sulphide Supply

What I find most interesting about nickel sulphides is that not only are their production figures predicted to curtail over the coming years, but the amount of projects awaiting development is low.

Why is this?

In my mind, there are 2 reasons:

First, a bear market in the nickel price, which pre-dates 2016, has stunted exploration.

Second is the fact that exploring for these deep deposits is very costly. Drilling for a deposit at depths greater than 500m adds up quickly. Plus, if you add in the costs associated with tough terrain and weather, you have the perfect storm for short and costly drill seasons.

NOTE: A high percentage of nickel sulphide exploration is concentrated in cold climates – Russia, Finland, Greenland and Canada. Why? Most of the discoverable nickel sulphide deposits found around the equator or in hotter and wetter climates have mostly been converted, by nature, into nickel laterite deposits. Thus, nickel laterite deposits account for up to 70% of the known crustal nickel deposits on the earth.

Constrained nickel sulphide supply has the potential to be very bullish for the nickel price moving forward, however, it will have to be mixed with strong demand to be fully realized.

Nickel Demand

In my view, nickel demand is the key to understanding where the nickel price is headed in the future.

As I outlined earlier in the article, increased demand for Class #1 nickel from battery manufacturers and/or speciality steel makers has the potential to dramatically disrupt the nickel market.

Demand in the range of 500kt to 1Mt of Class #1 nickel per year by 2030 would very quickly reveal the short fall in supply from the nickel sulphide producers, and require much higher nickel prices to allow HPAL processing to economically participate in actively supplying the market.

Concluding Remarks

Generally speaking, I’m very bullish on the long-term potential for higher nickel prices.

With that said, I remain skeptical of the short-term longevity of the current run in the nickel price.

The global economy remains in disarray and, although governments have pledged unlimited amounts of QE to stimulate inflation, I’m still left with many questions about the remaining 3.5 months in 2020.

How will the U.S. election result affect both the U.S. and world economy?

Does a Trump re-election mean the broader stock market can continue upward?

Does a Biden win result in more socialist government policy? If so, what is the fall-out for the American economy?

Will there be a 2nd wave of Covid-19? If so, will governments revert back to complete lockdowns of their economies?

Is the U.S. headed to war with China? The world’s two largest economies remain at odds, with potential conflicts on a range of topics such as, the South China Sea, Covid-19, and human rights violations.

In my view, the next 3.5 months should provide us with a few of the answers to these questions, which will allow us to see more clearly into where things are headed in 2021.

In the end, the fact remains that markets are impossible to predict with any consistency.

Instead, I believe it’s pertinent to remain focused on the reasons why we are speculating in the junior companies.

Understand why a company is undervalued and how they will unlock that value through the execution of their action plans.

Posted by AGORACOM

at 9:17 AM on Thursday, September 24th, 2020

TORONTO, ON / September 24, 2020 / Tartisan Nickel Corp. (CSE:TN; OTC PINK:TTSRF; FSE:A2D) (“Tartisan”, or the “Company”) is pleased to update shareholders on the Company’s operations in the Republic of Peru. The Don Pancho polymetallic Silver-Lead-Zinc project (“Don Pancho”) located in the department of Lima, Peru, 110 kilometres north-northeast of Lima, comprising of two concessions totalling 849 hectares. The project is located in a prolific polymetallic mineral belt in central Peru with several operating mines in the area, including Minas de Buenaventura’s silver-lead-zinc-manganese (Ag-Pb-Zn-Mn) Uchucchacua mine located 66 kilometres north of Don Pancho which produced more than 15 million ounces of silver in 2018.

Previous exploration on the property includes an extensive surface mapping and sampling program, geophysics, and a small diamond drilling program conducted by a private Peruvian company in 2014. Mapping and sampling by the previous operators defined two main mineralized zones. The main zone called “Yanapallaca” is an extensive NNW-SSE-trending breccia zone covering a surface area of over 800 metres in length and up to 200 metres in width. Numerous small old workings and three underground drifts exist within this zone. One of the adits crosscut a two metre wide massive sulphide vein grading 106 g/t Ag, 3.26% Pb, 17.56% Zn and 2.58% Mn. Other untested mineralized structures located within this zone that are exposed on surface include chip over 1 metre returning 406 g/t Ag and 27.05% Pb.

The second mineralized zone called “La Cruz” is located several hundreds of metres NE of Yanapallaca shows two mineralized trends. Sampling across the main N-S trend returned 96.6 g/t Ag, 5.53% Pb and 0.88% Zn over 1.50 metres with a crosscutting WNW-ESE structure grading 360 g/t Ag and 12.66% Pb over a 1 metre width. Very little work has been conducted by the previous operators on this prospective area.

Tartisan is pleased to announce the appointment of Carlos Agreda Minaya as the General Manager for Tartisan’s Peruvian subsidiary, Minera Tartisan Peru S.A.C. Mr. Agreda is an experienced manager with a MBA from Peru’s highly reputable ESAN program. Mr. Agreda has extensive experience in permitting, accounting and mineral processing. Mr. Agreda is very knowledgeable of the Company’s Don Pancho property and has submitted the necessary permits to start an underground bulk sampling program. Mr. Agreda is also the General Manager of Peruvian Metals Corp., a Canadian junior explorer in Peru with a processing plant located in Northern Peru where mineral from the Don Pancho will be processed.

Jeffrey Reeder, P.Geo, a qualified person as defined in National Instrument 43-101, has prepared, supervised the preparation of, or approved the scientific and technical disclosure contained in this news release.

About Tartisan Nickel Corp.

Tartisan Nickel Corp. is a Canadian based mineral exploration and development company which owns; the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Silver-Lead-Zinc Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel & Technologies Limited and Peruvian Metals Corp.

Tartisan Nickel Corp. common shares are listed on the Canadian Securities Exchange (CSE:TN; US-OTC:TTSRF; FSE:A2D). Currently, there are 101,603,550 shares outstanding (107,203,550 fully diluted).

For further information, please contact Mr. Mark Appleby, President & CEO and a Director of Tartisan Nickel Corp. at 416-804-0280 ([email protected]). Additional information about Tartisan Nickel Corp. can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

This news release may contain forward-looking statements including but not limited to comments regarding the timing and content of upcoming work programs, geological interpretations, receipt of property titles, potential mineral recovery processes, etc. Forward-looking statements address future events and conditions and therefore, involve inherent risks and uncertainties. Actual results may differ materially from those currently anticipated in such statements.

The Canadian Securities Exchange (operated by CNSX Markets Inc.) has neither approved nor disapproved of the contents of this press release.

Posted by AGORACOM

at 10:23 AM on Wednesday, September 23rd, 2020

Tartisan Nickel Corp. owns the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel & Technologies Limited and Peruvian Metals Corp. Click Here For More Info

Calling traditional metal refining processes “legacy” and “insanely complicated”, Elon Musk said today his company has re-thought and simplified how lithium and nickel will be processed for his future batteries.

Musk made the comments during a live simulcast presentation of Battery Day held in a parking lot in Fremont, California, near his manufacturing facilities. Musk shared part of the presentation with Drew Baglino, SVP of Powertrain and Energy Engineering at Tesla.

Musk called the traditional cathode process of processing nickel “a big target” due to its high cost

“It’s insanely complicated,” said Musk. “These things just grow up as legacy. We looked at the entire value chain and asked how can we make this as simple as possible.”

Bagnilo and Musk said many steps in the traditional refining method could be skipped resulting in 66% less investment, 76% less processing cost and 0% waste water.

The CEO of FPX Nickel, Martin Turenne, concurred with Musk: mineral processing can be made cleaner and more economical.

“The current methods of processing [nickel] are generally well established, and they’re done for a reason, because they work and because alternatives would be costly or they’re at an unproven stage,” said Turenne in an interview with Kitco after he watched Tesla’s Battery Day presentation.

At his own FPX, Turenne believes his nickel is in a form that would be suitable for batteries with the potential to skip the smelting step.

Musk and Bragnila imagine Tesla factories processing raw nickel powder for processing.

“Raw materials from a mine go to the plant and out comes a battery,” said Bragnila. “We are just consuming the raw nickel powder. It dramalitcally simplifies the raw nickel refining part of the whole process. We can eliminate billions in battery grade nickel intermediate production. It is not needed at all.”

What struck Turenne during the presentation is the forecast level of demand.

“At three terawatt-hours of battery cells per annum by 2030, that would entail approximately annual consumption of 2 million tonnes of nickel. That’s almost the entire scale of the current global nickel output,” said Turenne.

Posted by AGORACOM

at 8:10 AM on Tuesday, September 22nd, 2020

Tartisan Nickel Corp. owns the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel & Technologies Limited and Peruvian Metals Corp.

The federal government is planning investments in the electric vehicle industry to create a domestic supply chain for electric vehicle batteries that could supply the North American market. (Jonathan Hayward/The Canadian Press)

The Liberal government will use the speech from the throne to lay out a plan to create tens of thousands of jobs by connecting Canada’s resource sector with its manufacturing base to produce batteries for electric cars, Radio-Canada has learned.

“We recognize we have a unique opportunity to take advantage of our skilled labour force and we know we have a long and proud history of manufacturing vehicles, planes, ships and trains, and we also have an abundant amount of natural resources,” Innovation, Science and Industry Minister Navdeep Bains told Radio-Canada.

“We could be a world leader in [electric vehicle] battery manufacturing if we leverage our natural resources like lithium, cobalt … nickel, aluminum — the key ingredients that are required in batteries. Then we want to make sure that we manufacture them here and … use them in our trains, our buses, our ships and our planes.”

Bains said the green technology sector is expected to be worth trillions of dollars in the coming years and Canada could take advantage of that market by positioning itself as the chief North American supplier of batteries for electric vehicles.

“Not only do we want to be in a position to be building [electric vehicle] batteries here in Canada for the North American market, we want to be a global leader to take advantage of global opportunities,” he said.

CBC News has confirmed a report which first appeared in the Toronto Star — that the federal government is willing to put up to $500 million, with some money coming from the Ontario government, toward turning Ford’s Oakville plant over to the production of electric vehicles, an investment that could keep the plant open for years to come.

The paper reported that the mass production of electric vehicles and batteries is at the heart of talks between Ford Motor Co. and the union representing its employees.

When asked about the deal yesterday Ontario Premier Doug Ford said negotiations are still ongoing.

“What I can tell you is how important the auto industry is, one of the most important industries in Ontario,” he said during his daily briefing.

“This is good if we move forward. The parts are very important. We would like to manufacture the batteries here rather than bringing the batteries in from out of country. We have the capabilities and the raw materials here. Why can’t we produce the batteries? That’s my big ask to Ford.”

Adding value through manufacturing

Bains also said his government is looking at putting money into high-speed internet access — something he said the country needs more of now, with more and more Canadians working from home.

He also said the federal government is looking at investments in the agriculture sector to help make Canada “a world leader in plant proteins.”

Bains did not say if the agriculture and internet proposals will be a part of the throne speech.

“The bottom line is that we want to take advantage of what we have in Canada,” he said. “And what we have is an incredibly skilled labour workforce, we have natural resources and we have the ability to add value through our manufacturing processing initiatives.”

Posted by AGORACOM

at 8:24 AM on Monday, September 21st, 2020

TORONTO, ON / ACCESSWIRE / September 21, 2020 / Tartisan Nickel Corp. (CSE:TN)(OTC PINK:TTSRF)(FSE:A2D) (“Tartisan”, or the “Company”) is pleased to announce that the Company has appointed Thomas Larsen, Dean MacEachern and Ronald Wortel as advisors to the Company. The Board of Directors welcomes them on behalf of all shareholders.

THOMAS LARSEN, CEO ELORO RESOURCES LTD.

Thomas Larsen is an executive in the resources sector with over 40 years of experience in the investment industry, specializing in corporate finance and management of junior resource companies, raising in excess of $150 million. Mr. Larsen is currently the Chief Executive Officer of Eloro Resources Ltd. and Cartier Iron Corporation. Additionally, Mr. Larsen previously held the position of President and Chief Executive Officer of Champion Iron Limited.

DEAN MACEACHERN, B.SC. (HONS), P.GEO.

Mr. MacEachern has thirty years of exploration experience, seventeen of which were with Falconbridge Limited (now Glencore), where he was involved with significant nickel, copper and zinc discoveries in the Sudbury and Timmins mining camps. He coordinated numerous base and precious metals exploration programs at several of the world’s major operating nickel copper zinc and PGM mining camps, including the Sudbury, Thompson and Abitibi Nickel Camps, the Kidd Creek VMS Camp in Canada and, the Bushveld PGM Camp in South Africa. He has been involved in developing projects with junior exploration companies in Canada, South America, and Europe for base and precious metal. Mr. MacEachern was the former President & CEO of Canadian Arrow Mines Limited.

RONALD WORTEL, B.A.SC. P.ENG., MBA

Mr. Wortel is a finance executive with over 20 years of experience in resource project analysis, transaction due diligence and financing. Starting in 1997, Mr. Wortel provided equity research coverage on the mining equity sector for sell side investment banks: National Bank, Dundee Capital and Northern Securities. Initially he covered the major gold companies and transitioned to the junior resource sector with an emphasis on near term production stories. In 2006, he joined Pathway Asset Management, a resource fund providing flow through funding to exploration companies. Here Mr. Wortel reviewed hundreds of gold and other resource projects as the fund placed over $1 billion into the sector.

CEO Mr. Mark Appleby said, “I am delighted to welcome these three gentlemen with their combined 90 years of experience and expertise in various disciplines. Their counsel should prove to be a valuable asset to the Company”.

About Tartisan Nickel Corp.

Tartisan Nickel Corp. is a Canadian based mineral exploration and development company which owns; the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru. The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel & Technologies Limited and Peruvian Metals Corp.

Tartisan Nickel Corp. common shares are listed on the Canadian Securities Exchange (CSE:TN)(OTC PINK:TTSRF)(FSE:A2D). Currently, there are 101,603,550 shares outstanding (fully-diluted 107,203,550).

For further information, please contact Mr. Mark Appleby, President & CEO and a Director of Tartisan Nickel Corp. at 416-804-0280 ([email protected]). Additional information about Tartisan Nickel Corp. can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

Posted by AGORACOM

at 8:27 AM on Thursday, September 17th, 2020

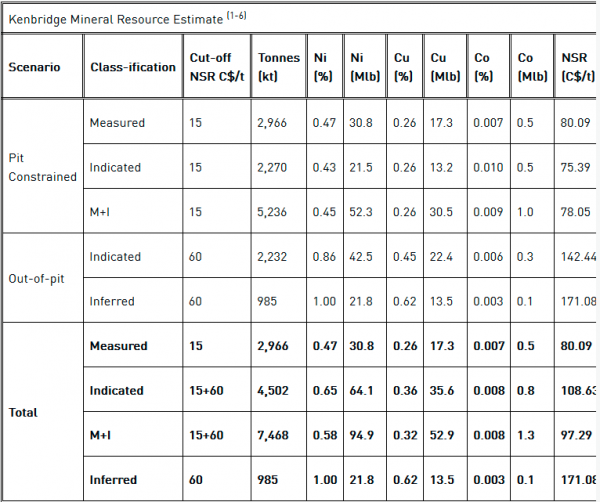

TORONTO, ON / ACCESSWIRE / September 17, 2020 / Tartisan Nickel Corp. (CSE:TN)(OTC:TTSRF)(FSE:A2D) (“Tartisan”, or the “Company”) is pleased to announce that P&E Mining Consultants Inc. has completed a review and re-estimation of the historic NI 43-101 compliant Technical Report and Updated Mineral Resource Estimate of the Kenbridge Nickel-Copper-Cobalt Project, Atikwa Lake Area, NW Ontario.

Updated estimates were done for pit constrained and out-of-pit nickel, copper, and cobalt Mineral Resources. Total Measured & Indicated Mineral Resources based on a Net Smelter Return (NSR) cut-off value of CDN$15 per tonne for pit constrained Mineral Resources and CDN$60 per tonne NSR for out-of-pit Mineral Resources is 7.5 Mt at 0.58% Ni and 0.32% Cu for a total of 95 Mlb of contained nickel. An additional 0.985 Mt at 1.0% Ni and 0.62% Cu (22 Mlb contained nickel) were calculated as Inferred Mineral Resources. The pit constrained Measured & Indicated Mineral Resources total 5.27 Mt of 0.45% nickel; 0.26% copper; and 0.009% cobalt at an NSR cut-off value of CDN$15/tonne. The out-of-pit Measured & Indicated Mineral Resources total 2.23 Mt of 0.86% nickel; 0.45% copper; and 0.006% cobalt. Inferred Mineral Resources out-of-pit total 0.985 Mt at 1.00% nickel; 0.62% copper; and 0.003% cobalt, at an NSR cut-off value of CDN$60/tonne. Details of the Mineral Resource Estimate are shown in Table 1.

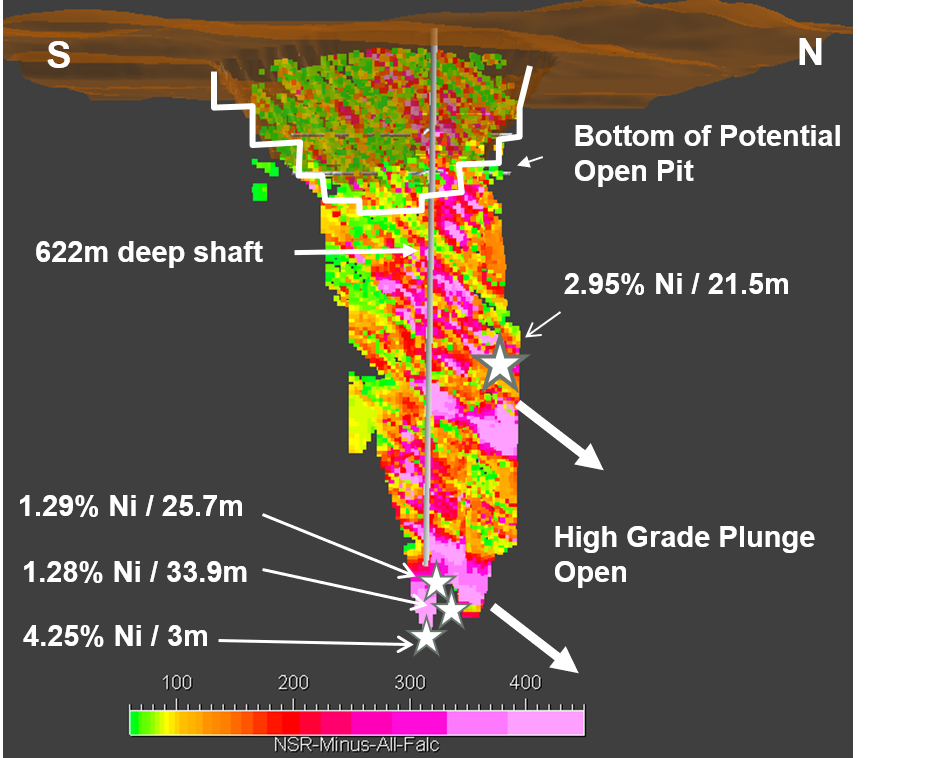

The Kenbridge Property is located in the Kenora – Fort Frances, Ontario area with good access to roads and power. It has a shaft to a depth of 2,042 ft (622 m), with level stations at 150 ft. (45 m) intervals below the shaft collar and two levels developed at 350 ft (107 m) and 500 ft (152 m) below the shaft collar.

Visual inspection of the NSR Block Model for the Kenbridge Deposit shows the highest nickel grades (>2.0%) appear to have a strong down-plunge orientation as illustrated in Figure 1.

A historical Preliminary Economic Assessment (PEA) for the Kenbridge Deposit was completed by Buck et al. in 2008 for Canadian Arrow Mines Limited (now a 100% wholly owned subsidiary of Tartisan Nickel Corp). The PEA was updated by WMT Associates Ltd. in a Canadian Arrow Mines Limited news release dated January 21, 2008, and subsequently updated again in a news release dated September 4, 2008. The Updated PEA was completed by WMT Associates Limited, based on an updated NI 43-101 Mineral Resource Estimate by P&E Mining Consultants Inc. (Canadian Arrow Mines Limited news release dated August 19, 2008) and improved metallurgical recoveries (Canadian Arrow Mines Limited news release dated June 26, 2008). Highlights of the Updated PEA were: average Ni recovery life of mine was 86%; recovered Ni was 84.6 Mlb; NPV 7.5% pre-tax was $253M; and IRR% pre-tax was 65%. The cost, value and financial assumptions used in the Updated PEA were unchanged from the original January 2008 PEA (Buck et al., 2008), including average life of mine, US$10/lb nickel and US$2.50/lb copper prices, and a CD$1.00:US$0.90 exchange rate. Although this PEA is deemed to be historical by the Company, it is thought to be important.

Table 1.

Kenbridge Mineral Resource Estimate (1-6)

Note: Ni =Nickel Cu = Copper, Co = Cobalt, NSR = Net Smelter Return.

1. Mineral Resources, which are not Mineral Reserves, do not have demonstrated economic viability.

2. The estimate of Mineral Resources may be materially affected by environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant issues.

3. The Inferred Mineral Resource in this estimate has a lower level of confidence than that applied to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of the Inferred Mineral Resource could be upgraded to an Indicated Mineral Resource with continued exploration.

4. The Mineral Resources in this report were estimated using the Canadian Institute of Mining, Metallurgy and Petroleum (“CIM”), CIM Standards on Mineral Resources and Reserves, Definitions and Guidelines prepared by the CIM Standing Committee on Reserve Definitions and adopted by the CIM Council.

5. The Mineral Resource Estimate was based on US$ metal prices of $7.42/lb nickel, $3/lb copper and $25/lb cobalt.

6. The out-of-pit Mineral Resource grade blocks were quantified above the $60/t NSR cut-off, below the constraining pit shell and within the constraining mineralized wireframes. Additionally, only groups of blocks that exhibited continuity and reasonable potential stope geometry were included. All orphaned blocks and narrow strings of blocks were excluded. The longhole stoping with backfill mining method was assumed for the out of pit Mineral Resource Estimate calculation.

Figure 1. Kenbridge Deposit 3D view illustrating calculated NSR blocks and drill hole intersections of significance.

CEO Mr. Mark Appleby stated, “The Updated Mineral Resource Estimate was necessary to determine if Kenbridge mineralization is potentially extractable under current metal prices and exchange rates. This is a major milestone achieved by the Company as the market conditions for Class 1 nickel sulphide deposits improve. The differences between the previous P&E Mineral Resource Estimate (2008) and the current P&E Updated Mineral Resource Estimate are attributed to changes in metal prices and recalculation of NSR values. The Kenbridge Deposit shows there is great potential to expand the Mineral Resource down-plunge of high-grade intersections such as hole KB07-180 (2.95% Ni, 0.82% Cu/21.5m including 7.2% Ni, 0.67% Cu/5.5m) and also at depth. The deepest hole (end of hole K2010 = 880 m below surface) intersected mineralization grading 4.25% nickel and 1.38% copper over 10.7 ft (3.3 m), indicating that the Deposit remains open at depth. Tartisan plans to expand on these intersections, upgrade the Indicated and Inferred Mineral Resources and test high potential nickel exploration targets, such as the Kenbridge North Target. Additionally, given the market interest in Class 1 nickel deposits, we will look to update the historic Preliminary Economic Assessment completed in 2008 based on this very positive Mineral Resource update.”

The Company plans an aggressive surface exploration and definition drilling plan, in addition to geotechnical, metallurgical and environmental work to advance the Kenbridge Nickel-Copper-Cobalt Project in the upcoming 2020 winter season and into the summer of 2021.

The effective date of the 2020 Updated Mineral Resource Estimate is September 2nd, 2020 and the Technical Report relating to the Updated Mineral Resource has now been filed on SEDAR.

Qualified Person

The technical information in this news release has been prepared in accordance with Canadian regulatory requirements as set out in NI 43-101 and reviewed and approved by Eugene Puritch, P.Eng., FEC, CET, a Qualified Person as defined by NI 43-101.

About Tartisan Nickel Corp.

Tartisan Nickel Corp. is a Canadian based mineral exploration and development company which owns; the Kenbridge Nickel Project in northwestern Ontario, the Sill Lake Silver Property in Sault St. Marie, Ontario as well as the Don Pancho Manganese-Zinc-Lead-Silver Project in Peru.

The Company has an equity stake in; Eloro Resources Limited, Class 1 Nickel and Technologies Limited and Peruvian Metals Corp.

Tartisan Nickel Corp. common shares are listed on the Canadian Securities Exchange (CSE:TN; US-OTC:TTSRF; FSE: A2D). Currently, there are 101,603,550 shares outstanding (103,303 ,550 fully diluted).

For further information, please contact Mr. D. Mark Appleby, President & CEO and a Director of the Company, at 416-804-0280 ([email protected]). Additional information about Tartisan can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

.jpg;w=960)

.png)

.png)