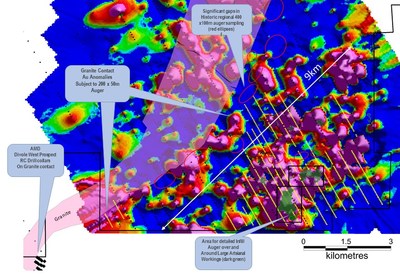

- Candente owns Cañariaco Norte, a large, economic, copper ore body in Peru

- 100% owned feasibility-stage porphyry copper deposit; a single, contiguous, open-pit mineable deposit of:

- 7.5B pounds Measured and Indicated and can be mined for 22 years once in production.

- Once in production Canariaco is in the lowest quartile of production costs for projects waiting to be developed.

- Operating costs of US$0.988 per pound of copper

- Capable of generating annual production of 262,000,000lbs of copper, 39,000 oz gold & 911,000 oz silver over initial mine life of 22 yrs(@ 95,000 tpd).

- The transition to an electrified clean energy economy is going to result in a monumental draw on metals and minerals from the earth’s crust

- The new energy transition hardware requires earthly resources — metals and minerals — which are suddenly escalating in price

Prices of copper, nickel, cobalt, platinum and rare earth elements are all inflating as electric vehicles and the wider electrification trend starts pulling on constrained resources. Photo by Getty Images/Bloomberg/Reuters

Like many in the energy business, I marvel at how fast the cost of producing renewable power, LED light bulbs and lithium-ion batteries has fallen over the past decade. Depending on what’s being measured, some costs are down by more than 90 per cent.

Should we assume these downward-trending cost curves are sustainable? And will this type of cost reduction be applicable to other emerging clean energy devices?

Based on advances in technology and more efficient manufacturing processes, the short answer is a qualified yes. Yet, we shouldn’t be blinded by the glow of the new economy — things like data science, process engineering, robotics and advanced materials — which, to date, have been the principal drivers for achieving these cost reductions.

Much of the new energy transition hardware requires earthly resources — metals and minerals — which are suddenly escalating in price

From the shadows, we are now seeing that the old economy isn’t so old after all. Much of the new energy transition hardware requires earthly resources — metals and minerals — which are suddenly escalating in price.

Prices of copper, nickel, cobalt, platinum and rare earth elements are all inflating as electric vehicles and the wider electrification trend starts pulling on constrained resources. For example, nickel prices just closed shy of a five-year high, copper is up 30 per cent from pre-COVID levels, and cobalt has jumped 25 per cent in value in 2021 alone.

I should note that the solar industry’s achievements are often quoted as a template to how fast clean energy costs can come down. But let’s be careful. Made from silicon, the most plentiful element in the earth’s crust (think sand), solar panels don’t have a resource constraint problem. Many of the vital metals and minerals needed to electrify transport and other industrial segments of our economy don’t enjoy t

There are now dozens of electric vehicle manufacturers at various stages of development around the world. Tesla Inc. is the leader, of course. Volkswagen AG is going all-in, and General Motors Co. is expected to accelerate from a trot to a gallop by mid-decade. Upstart companies are collectively raising billions of dollars to roll out new models. Expectations for EV sales are at high voltage, and now those expectations are zapping the resource sector. No wonder some investment analysts speak about a forthcoming “commodity supercycle.”

Consider the scale of what’s happening.

Tesla sold just shy of 500,000 vehicles last year. It’s an impressive number, but — in a world of a billion-plus cars — it’s still de minimis. At Tesla’s current rate of sales, it would take over 2,000 years to replace the world’s fleet of combustion-engine vehicles. We have barely dented the market for EVs.

The assumption that costs for new energy technologies will fall smoothly and forever needs a serious rethink

Now let’s look at what it takes to power one of them. A typical 75-kilowatt-hour electric car battery is 5,000 times the capacity of the one in your mobile phone. And that’s for a medium-sized sedan such as Tesla’s Model 3, not the super-sized pickup truck or SUV that most people are aspiring to develop.

From a money lens, the demand for natural resources is getting to be much more than a dent. Mining.com’s EV Metal Index for November 2020 show that sales of lithium, graphite, cobalt and nickel just for making EV batteries have risen rapidly to US$325 million per month. A mere four years ago, that number was a tenth of that. And we are going to sell how many EVs by 2030?

The point is, we don’t need a spreadsheet to realize that the transition to an electrified clean energy economy is going to result in a monumental draw on metals and minerals from the earth’s crust. And it’s going to cost a lot more money. In the past few months, rising commodity prices are a wake-up call to that reality. In the old economy, an inflection of demand that pulls on constrained resources leads to price spikes.

At a minimum, the assumption that costs for new energy technologies will fall smoothly and forever needs a serious rethink, especially for metal-intense segments of the business. At worst, commodity price inflation that passes through to end customers will restrain adoption of new-age products.

Sure, the challenges can be overcome. When commodity prices rise, more resource projects are permitted, financed and built, often in unsavory places.

We’ve seen it before. The world grew its oil production from nothing to an unfathomable 100 million barrels a day. But it took 150 years and hundreds of trillions of dollars. Along the way, there were plenty of commodity supercycles, not to mention geopolitical issues, which is a whole other supercharged issue when it comes to rare and geographically concentrated minerals.

And the challenges can be overcome by technology, too. For example, a new generation of solid-state batteries will ease the pressure on some metals, though the timeline for those is a decade out.

The resource world doesn’t move nearly as fast as technology, which is why commodity value is now chasing technology value. And the larger lesson is that the new economy can’t go anywhere without the old.

SOURCE: https://financialpost.com/commodities/energy/another-commodity-supercycle-is-coming-this-time-driven-by-renewable-energy-and-evs