Posted by AGORACOM-JC

at 4:10 PM on Thursday, November 7th, 2019

The headline pretty much says it all. Though HPQ has stated the

discussions are preliminary, this doesn’t hide the fact that HPQ has

moved incredibly fast from deciding to use its world-changing silicon

manufacturing process to enter the battery market.

It was only back on August 19th when Company CEO, Bernard Tourillon,

stated HPQ would “start meeting with end users” but few would have

expected NDA based discussions with a Li-ion battery manufacturer so

soon. Ironically, Tourillon says he expected something like this

“sooner” … now that is confidence.

In a small cap market full of companies claiming the holy grail of

supplying the battery market, it wasn’t hard to understand why investors

may have dismissed the Company’s OCT 31 statement that “HPQ fully

intends to use its Gen3 to produce and market silicon materials for

batteries”.

With discussions under NDA now started with a battery manufacturer,

HPQ has now set itself far apart from the pack and has earned the right

to be taken very seriously. Investors who have been waiting for ANY

company to move from theoretical to the actual boardroom, HPQ offers a

very compelling story.

Grab your favourite beverage and watch this interview with CEO Bernard Tourillon.

Posted by AGORACOM-JC

at 9:08 AM on Thursday, November 7th, 2019

HPQ and its partner Apollon Solar SAS have signed a non-disclosure agreement with a manufacturer of Li-ion batteries for the purposes of exchanging technical information and sending testing materials

For industry competitive reasons, the name of the battery manufacturer will remain confidential.

MONTREAL, Nov. 07, 2019 — HPQ Silicon Resources Inc. – TSX-V: HPQ; OTCPink: URAGF; FWB: UGE (“HPQ†or “the Companyâ€) is pleased to announce that HPQ and its partner Apollon Solar SAS, acting as one party, have signed a non-disclosure agreement (“NDAâ€) with a manufacturer of Li-ion batteries for the purposes of exchanging technical information and sending testing materials. For industry competitive reasons, the name of the battery manufacturer will remain confidential.

MEETINGS WITH INDUSTRY PARTICIPANTS LEAD TO NDA WITH BATTERY MANUFACTURER

In its’ press release dated August 19, 2019, HPQ announced it would

be meeting with industry participants and end users in H2 2019 about our

unique capacity to produce high purity Silicon (Si) in one step. The

NDA is a result of the manufacturer showing an interest in evaluating

porous silicon wafers made using Silicon (Si) produced by HPQ PUREVAP™Quartz Reduction Reactor

(“QRR”) and Apollon Solar patented process. Specifically, the cased use

is to explore using our porous silicon wafers as the anode for their

next generation Li-ion Si batteries.

“We are very happy to be in discussions with an innovative Li-ion

battery manufacturer and look forward to now having more substantive

technical discussions. More than four years of great technical work

culminated in the assembly of a world-class technical team in 2019 to

demonstrate the potential of silicon materials produced from the

PUREVAP™QRR as high-capacity anode materials for Li-ion batteries†said Bernard Tourillon, President and CEO HPQ Silicon. “Silicon’s potential to meet energy storage demand is undeniable and generating massive investments, as

well as, serious industry interest, so our timing could not be better.

Suffice it to say, we are very pleased to have attracted such early

interest. However, I must caution investors that although this agreement

does signal the interest in our products, we are still at the very

preliminary stages and there is no guarantee that anything, of any

commercial value, will materialize from these efforts. It does however

demonstrate the potential for new and exciting advances by HPQ and

partners in the silicon energy space.â€

GLOBAL ENERGY STORAGE MARKET READY TO EXPLODE

A recent report

projects that energy storage deployments are estimated to grow 1,300%

from a 12 Gigawatt-hour market in 2018 to a 158 Gigawatt-hour market in

2024. Meanwhile, at current growth rates of 2% per year, global energy consumption

will be an estimated 125,000 Terawatt-hours, which is 800,000 times

more than the estimated storage capacity. An estimated US$71 billion in

investments will be made into storage systems where batteries will make

up the lion’s share of capital deployment. Research suggests

that replacing graphite materials with Silicon anodes in Li-Ion

Batteries promises an almost tenfold (10x) increase in the specific

capacity of the anode, inducing a 20-40% gain in the energy density of

Li-ion batteries.

About Silicon

Silicon (Si) is one of today’s strategic materials needed to fulfil

the renewable energy revolution presently under way. Silicon does not

exist in its pure state; it must be extracted from quartz, one of the

most abundant minerals of the earth’s crust and other expensive raw

materials in a carbothermic process.

About HPQ Silicon

HPQ Silicon Resources Inc. is a TSX-V listed company developing, in

collaboration with industry leader PyroGenesis (TSX-V: PYR) the

innovative PUREVAPTM “Quartz Reduction Reactors†(QRR), a truly

2.0 Carbothermic process (patent pending), which will permit the

transformation and purification of quartz (SiO2) into Metallurgical

Grade Silicon (Mg-Si) at prices that will propagate its significant

renewable energy potential.

HPQ is also working with industry leader Apollon Solar to develop: Porous silicon wafers manufacturing using PUREVAP™

Silicon (PVAP Si) that can be used as anode for all-solid-state and

Li-ion batteries; and a metallurgical pathway of producing Solar Grade

Silicon Metal (SoG Si) that will take full advantage of the PUREVAPTM QRR

one-step production of high purity silicon (Si) and significantly

reduce the Capex and Opex associated with the transformation of quartz

(SiO2) into SoG-Si.

HPQ focus is becoming the lowest cost producer of Silicon (Si), High

Purity Silicon (Si), Porous Silicon Wafers and Solar Grade Silicon Metal

(SoG-Si). The pilot plant equipment that will validate the commercial

potential of the process is on schedule to start in 2019.

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

Disclaimers:

The Corporation’s interest in developing the PUREVAP™ QRR and any

projected capital or operating cost savings associated with its

development should not be construed as being related to the establishing

the economic viability or technical feasibility of the Company’s

Roncevaux Quartz Project, Matapedia Area, in the Gaspe Region, Province

of Quebec.

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward-looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Company’s current expectation and assumptions and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Company with respect to future events and are subject to certain risks

and uncertainties and other risks detailed from time-to-time in the

Company’s on-going filings with the security’s regulatory authorities,

which filings can be found at www.sedar.com. Actual results, events, and

performance may differ materially. Readers are cautioned not to place

undue reliance on these forward-looking statements. The Company

undertakes no obligation to publicly update or revise any

forward-looking statements either as a result of new information, future

events or otherwise, except as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

For further information contact Bernard J. Tourillon, Chairman, President and CEO Tel (514) 907-1011 Patrick Levasseur, Vice-President and COO Tel: (514) 262-9239 http://www.hpqsilicon.com Email: [email protected]

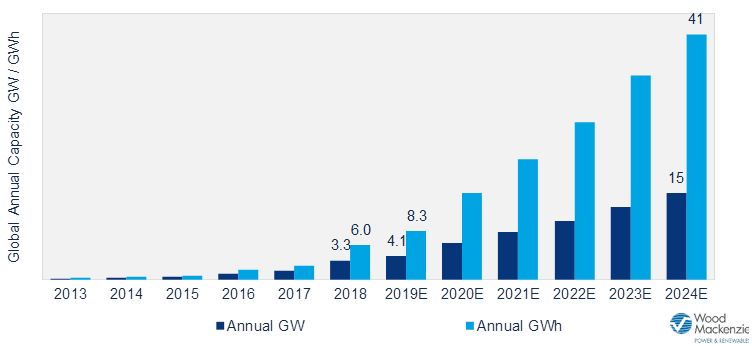

Global Energy Storage to Hit 158 Gigawatt-Hours by 2024, Led by US and China

Wood Mackenzie Power & Renewables projects a thirteenfold

increase in grid-scale storage over the next six years. Here’s a

market-by-market breakdown.

Report projects that energy storage deployments will grow thirteenfold over the next six years, from a 12 gigawatt-hour market in 2018 to a 158 gigawatt-hour market in 2024.Â

Equates to $71 billion in investment into storage systems excluding pumped hydro, with $14 billion of that coming in 2024 alone.

For the energy storage industry, the past five years have been

something of a stage rehearsal for a market explosion to come, led by

the U.S. and China, but expanding to cover markets across the globe.

That’s the picture painted by Wood Mackenzie Power & Renewable’s latest report, Global Energy Storage Outlook 2019: 2018 Year in Review and Outlook to 2024.

Tuesday’s report projects that energy storage deployments will grow

thirteenfold over the next six years, from a 12 gigawatt-hour market in

2018 to a 158 gigawatt-hour market in 2024.

That equates to $71 billion in investment into storage systems

excluding pumped hydro, with $14 billion of that coming in 2024 alone.

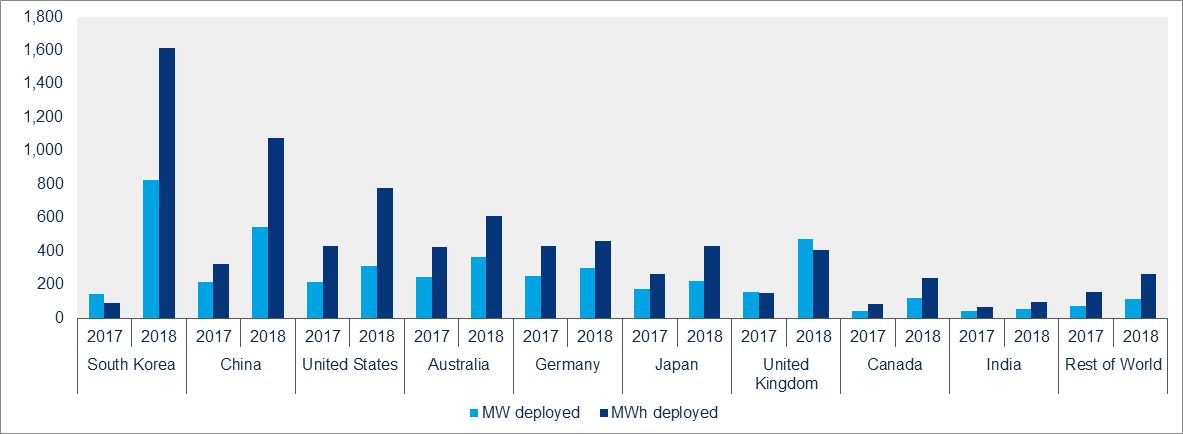

This growth will be concentrated in the United States and China, which

will account for 54 percent of global deployments by 2024, followed

by Japan, Australia and South Korea in a second tier of growth markets,

and Germany, Canada, India and the U.K. rounding out the list.

Each of these markets is taking its own approach to integrating

energy storage into its grid operations and market structures, from the

state-by-state development in the U.S. to China’s five-year plan. But

they share a commitment to relatively aggressive renewables growth

targets, along with the attendant challenges of integrating an

increasing share of intermittent wind and solar power into the grid.

And much like the renewables that are driving their growth, the

batteries that make up the lion’s share of new storage systems being

deployed are falling in price.

That’s positioning them for a much broader integration into grid

operations beyond renewables integration, Ravi Manghani, WoodMac’s head

of storage research, noted in a Tuesday interview: “Over the last five

years, the world began to experiment with storage; in the next five,

storage will become a key grid asset.â€

Last year saw global energy storage deployments grow 147 percent

year-over-year to reach 3.3 gigawatts, or 6 gigawatt-hours, the report

states. That’s nearly double the average 74 percent compound annual

growth rate for the industry from 2013 to 2018. In fact, last year’s

deployments made up more than half of the total amount of storage

deployed in the past five years, “indicating an inflection in storage

demand,†Manghani said.

This inflection point is measured not only in terms of project

volume, but in the variety of regulatory and market structures allowing

these projects to be financed and built, he noted. The past half-decade

of energy storage growth has been driven by a relatively limited and

isolated set of revenue streams, as well as government incentives

designed to jump-start development in advance of the market structures

to unlock the value of storage, he said.

From 2019 to 2024, WoodMac projects a more mature but still

early-stage compound annual growth rate of 38 percent for key storage

markets, but with a far broader set of money-making opportunities for

the systems being installed. This will include a shift

from short-duration systems providing high-value, but limited-size

markets such as frequency regulation, to long-duration systems that can

start to displace diesel, oil and natural-gas peaker plants.

A market-by-market breakdown

We’ve already covered WoodMac’s growth projections for the U.S. energy storage market,

the world’s biggest at present, and still expected to retain that

position by 2024, if only just ahead of China. The U.S. deployed a

record 311 megawatts and 777 megawatt-hours of energy storage in 2018,

but that market is expected to double in 2019 and triple in 2020,

according to last month’s Energy Storage Monitor from WoodMac and the Energy Storage Association.

This growth will continue to be driven by key markets like

California, the country’s leader in behind-the-meter batteries, and

other states with gigawatt-scale energy storage deployment mandates such

as New York and Massachusetts. But it will also be driven by utilities

adopting storage for capacity or as part of large-scale solar projects,

as with recent large-scale contracts in Hawaii, Texas, Minnesota and

Colorado.

And of course, Federal Energy Regulatory Commission Order 841, which

orders the country’s regional wholesale market operators to open up

energy, capacity and ancillary services markets to energy storage, will

create new market opportunities.

Turning to Asia, “we’ve seen China wake up in terms of energy

storage, and slightly ahead of schedule,†Manghani said. China saw a 40

percent year-over-year energy storage market growth in 2018, driven by

more than 300 megawatts, or nearly 500 megawatt-hours, of utility-scale

deployment.

In November 2017, China’s government announced a 10-year plan for developing its own grid-scale energy storage industry.

This was partly a means of supporting and building upon its already

massive dominance in battery manufacturing for electric vehicles, but

it’s also a response to China’s mounting grid challenges — namely,

integrating the massive amounts of wind and solar power being built in

remote western regions to the country’s urban east.

And when China decides to build grid batteries, it builds them at

scale. “The majority of the deployments are currently pilot-scale

projects — but when China does pilot-scale projects, we’re talking about

tens of megawatt-hours,†Manghani said. Last year saw one

101-megawatt/202-megawatt-hour energy storage project come online in

Jiangsu, and another 240-megawatt/720 megawatt-hour project approved in

Gansu to reduce renewables curtailment.

In the next five years, several more large-scale energy storage

projects to support grid reliability and flexibility are expected to

come online. About 65 percent of China’s 2018 installed capacity was

developed by the State Grid Corporation of China for ancillary services

purposes, indicating the importance of central planning for growth.

South Korea represents a similar story of how government planning can

drive massive energy storage market growth, with a new policy to allow

storage-backed wind and solar projects to earn renewable energy

certificates worth five times their capacity value driving a massive

boom in 2018. From less than 10 megawatt-hours deployed in 2017, South

Korea’s utility-scale and commercial-industrial behind-the-meter

deployments boomed to 1,100 megawatt-hours in 2018, with nearly $400

million in energy storage investments and a pipeline of projects that’s

already overshot its goal of 800 megawatt-hours by 2020.

Australia, by contrast, has been driven by solar-plus-storage projects on the residential side of the market,

due to its competitive energy markets and the increasingly attractive

economics of self-generated solar power. Australia led the world in

residential storage in 2018 with 150 megawatts, or 300 megawatt-hours,

of systems deployed. Japan ranked a close second in residential storage,

taking a slight lead over Germany in terms of 2018 deployments,

although Germany still retains the lead in total number of systems

deployed, at about 860 megawatt-hours.

At the same time, policy shifts can have an impact on global energy

storage markets. The U.K. installed its own record-setting 408

megawatts/325 megawatt-hours of utility-scale storage in 2018. But as

these figures indicate, this boom was largely in the form of

shorter-duration battery systems, which could see their value decrease

significantly under changes to the U.K.’s capacity market mechanism to

de-rate shorter-duration systems in favor of multi-hour storage.

At the same time, a November European court ruling against the U.K.’s

capacity market mechanism — along with the broader uncertainty over how

the country’s departure from the EU under Brexit could affect its

energy future — has created challenges for the market.

Likewise, in Canada, last year’s efforts to incorporate energy

storage into wholesale markets in Ontario and Alberta have been

counterbalanced somewhat by the new Ontario government’s decision to

cancel hundreds of renewable energy projects.

Posted by AGORACOM-JC

at 9:08 AM on Thursday, October 31st, 2019

Announced its collaboration with Professor Lionel ROUÉ of the Institut National de Recherche Scientifique (INRS)

Aimed at evaluating the electrochemical performances of different materials produced by the HPQ PUREVAP™Quartz Reduction Reactor for Li-ion batteries

MONTREAL, Oct. 31, 2019 — HPQ Silicon Resources Inc. – TSX-V: HPQ; OTCPink: URAGF; FWB: UGE (“HPQ†or “the Companyâ€) is pleased to announce its collaboration with Professor Lionel ROUÉ of the Institut National de Recherche Scientifique (INRS) within the scope of projects aimed at evaluating the electrochemical performances of different materials produced by the HPQ PUREVAP™Quartz Reduction Reactor (“QRR”) for Li-ion batteries.

Professor Lionel ROUÉ of the INRS-EMT has developed a scientific

program focused on the study of new electrode materials for various

applications of industrial interest (batteries, aluminium production,

etc.). In recent years, a significant part of its research activities

has been devoted to the study of Si anodes for Li-ion batteries and the

development of in-situ characterization methods applied to batteries.

He is the author of more than 150 publications, including twenty

articles and 2 patents on Si-based anodes for Li-ion batteries. He was

awarded the Energia Prize by the Quebec Association for the Mastery of

Energy for his work in this field.

EVALUATING WORLDWIDE BATTERY MARKET POTENTIAL OF MATERIALS PRODUCED BY PUREVAP™

The first goal of the association is determining the commercial potential of materials produced by the PUREVAPTM

QRR as anode material for the Li-ion battery market and ascertaining

whether their usage within Li-ion batteries could lead to a significant

increase in their energy density, which is crucial for some

applications, especially electric vehicles.

In the second phase, the electrochemical performance of PUREVAPTM silicon based porous silicon wafers made using Apollon Solar’s patented process will be tested.

“Silicon’s potential to meet energy storage demand is generating massive investments. Collaborating

with a world-class university center, HPQ will be able to validate the

potential of silicon materials produced from the PUREVAP™QRR as high-capacity anode materials for Li-ion batteries†said Bernard Tourillon, President & CEO of HPQ Silicon Resources Inc. Mr. Tourillon added: “HPQ, working with PyroGenesis, Apollon and the INRS Energy Materials Telecommunications (EMT) Research Centre, fully intends to use its Gen3 PUREVAP™ QRR to produce and market Silicon materials for batteriesâ€.

GLOBAL ENERGY STORAGE MARKET READY TO EXPLODE

A recent report

projects that energy storage deployments are estimated to grow 1,300%

from a 12 Gigawatt-hour market in 2018 to a 158 Gigawatt-hour market in

2024. An estimated US$71 billion in investments will be made into

storage systems where batteries will make up the lion’s share of capital

deployment. Research suggests

that replacing graphite materials with Silicon anodes in Li-Ion

Batteries promises an almost tenfold (10x) increase in the specific

capacity of the anode, inducing a 20-40% gain in the energy density of

Li-ion batteries.

About Silicon

Silicon (Si) is one of today’s strategic materials needed to fulfil

the renewable energy revolution presently under way. Silicon does not

exist in its pure state; it must be extracted from quartz, one of the

most abundant minerals of the earth’s crust and other expensive raw

materials in a carbothermic process.

About HPQ Silicon

HPQ Silicon Resources Inc. is a TSX-V listed company developing, in

collaboration with industry leader PyroGenesis (TSX-V: PYR) the

innovative PUREVAPTM “Quartz Reduction Reactors†(QRR), a truly

2.0 Carbothermic process (patent pending), which will permit the

transformation and purification of quartz (SiO2) into Metallurgical

Grade Silicon (Mg-Si) at prices that will propagate its significant

renewable energy potential.

HPQ is also working with industry leader Apollon Solar to develop: Porous silicon wafers manufacturing using PUREVAP™

Silicon (PVAP Si) that can be used as anode for all-solid-state and

Li-ion batteries; and a metallurgical pathway of producing Solar Grade

Silicon Metal (SoG Si) that will take full advantage of the PUREVAPTM QRR

one-step production of high purity silicon (Si) and significantly

reduce the Capex and Opex associated with the transformation of quartz

(SiO2) into SoG-Si.

HPQ focus is becoming the lowest cost producer of Silicon (Si), High

Purity Silicon (Si), Porous Silicon Wafers and Solar Grade Silicon Metal

(SoG-Si). The pilot plant equipment that will validate the commercial

potential of the process is on schedule to start in 2019.

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

Disclaimers:

The Corporation’s interest in developing the PUREVAP™ QRR and any

projected capital or operating cost savings associated with its

development should not be construed as being related to the establishing

the economic viability or technical feasibility of the Company’s

Roncevaux Quartz Project, Matapedia Area, in the Gaspe Region, Province

of Quebec.

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward-looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Company’s current expectation and assumptions and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Company with respect to future events and are subject to certain risks

and uncertainties and other risks detailed from time-to-time in the

Company’s on-going filings with the security’s regulatory authorities,

which filings can be found at www.sedar.com. Actual results, events, and

performance may differ materially. Readers are cautioned not to place

undue reliance on these forward-looking statements. The Company

undertakes no obligation to publicly update or revise any

forward-looking statements either as a result of new information, future

events or otherwise, except as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

For further information contact Bernard J. Tourillon, Chairman, President and CEO Tel (514) 907-1011 Patrick Levasseur, Vice-President and COO Tel: (514) 262-9239 http://www.hpqsilicon.com Email: [email protected]

Posted by AGORACOM-JC

at 5:45 PM on Friday, October 18th, 2019

HPQ Silicon makes its strongest case ever for the lead it has taken in the commercialization of its’

Solar grade silicon;

Silicon wafers for Li-ion batteries

High purity silicon for high value niche applications;

Metallurgical grade silicon at prices the industry has never seen before;

More than just lip service that we have typically come to expect from 98% of small cap companies, the Company’s pilot plant is about to go live and produce test samples of silicon wafers for batteries and is supported by not 1 but 2 (TWO) world class technology partners that validate both the HPQ process and commercialization plan.

This is a powerful presentation that is worthy of your time to watch and learn about the rise of HPQ Silicon.

Posted by AGORACOM-JC

at 4:01 PM on Wednesday, September 25th, 2019

When the lithium craze hit the markets a few years back, dozens of companies dreamed of cashing in on the impending battery craze for electric vehicles.

While 99% of companies focused on lithium or graphite, HPQ focused on creating the world’s cheapest and lowest emission Silicon for multiple applications, including solar.

Along the way, HPQ picked up 2 world class technology partners and the Quebec government as an investor.

Today, the company is on the verge of producing Silicon from its 50 ton pilot plant for multiple applications.

Serendipitously, experts now agree that Silicon is the superior material for electric battery anodes versus graphite.

If

that wasn’t enough, the Company’s solar partner happens to hold the

world wide patent on manufacturing porus silicon wafers, which is

exactly what is needed for battery anodes.

Today, while most other companies working on Li-Ion Silicon

are still stuck in R&D, HPQ has rocketed ahead to its

commercialization stage and has the electric vehicle battery market

watching with great anticipation.

Watch this

incredible video with HPQ Silicon CEO, Bernard Tourillon, who has

brilliantly architected the company’s development from concept to

commercialization.

Posted by AGORACOM-JC

at 8:36 AM on Wednesday, September 25th, 2019

Announced the extension and the expansion of scope of the December 2017 collaboration agreement with Apollon Solar SAS,

The agreement now includes evaluating manufacturing porous Silicon wafers for solid-state Li-Ion batteries using Apollon patented process and Silicon (Si) produced by HPQ PUREVAP™Quartz Reduction Reactor

MONTREAL, Sept. 25, 2019 — HPQ Silicon Resources Inc. - TSX-V: HPQ; OTCPink: URAGF; FWB: UGE (“HPQ†or “the Companyâ€) is pleased to announce the extension and the expansion of scope of the December 2017 collaboration agreement with Apollon Solar SAS, (“Apollon”). The agreement now includes evaluating manufacturing porous Silicon wafers for solid-state Li-Ion batteries using Apollon patented process and Silicon (Si) produced by HPQ PUREVAP™Quartz Reduction Reactor (“QRR”) (“PVAP Siâ€).

APOLLON PATENTED LOW-COST APPROACH TO MAKING POROUS SILICON WAFERS

In 2012, Apollon, working in collaboration with France CNRS (“Centre

National de la Recherche Scientifiqueâ€), developed and obtained a

worldwide patent for a unique low-cost process that uses standard

metallurgical Silicon (2N to 4N+ Si) to produce square porous Silicon

Wafers with a thickness of up to 2 cm.

“The HPQ PUREVAP™ QRR’s proprietary capacity of controlling the

purity of the Silicon (Si) produced should allow our unique and patented

process to optimize the porous structure of the wafers between

Microporous (pore size <5nm), Mesoporous (pore size 5nm – 50nm) and

Macroporous (pore size >50nm) as per end-users requirements, simply

by adapting process parameters†stated Mr. Jed Kraiem Ph.D, General Manager of Apollon Solar.

Working with Apollon, HPQ intends to develop the manufacturing of porous silicon wafers using PUREVAP™ Si that can be used as anodes for solid-state Li-ion batteries.

“Combining Apollon’s patented low cost approach to make porous Si

wafers and the HPQ PUREVAP™ Gen3 Pilot Plant’s ability to produce Si

will allow us to start the commercialisation of our porous Si wafers for

solid state Li-Ion batteries earlier then most competitors, who are

still only earlier stages R&D plays†said Bernard Tourillon, President & CEO of HPQ Silicon Resources Inc. Mr. Tourillon added: “Production of the first porous Silicon test wafers could start as early as Q4 2019.â€

GLOBAL ENERGY STORAGE MARKET READY TO EXPLODE

A recent report

projects that energy storage deployments are estimated to grow 1,300%

from a 12 Gigawatt-hour market in 2018 to a 158 Gigawatt-hour market in

2024. An estimated US$71 billion in investments will be made into

storage systems where batteries will make up the lion’s share of capital

deployment. Research suggests

that replacing graphite materials with Silicon anodes in Li-Ion

Batteries promises an almost tenfold (10x) increase in the charging

capacity of batteries.

“Silicon potential to meet energy storage demand is generating massive investments.

HPQ, working with Apollon, fully intends to use its first mover

advantage in low cost porous Silicon (Si) wafer manufacturing using

metallurgically produced PUREVAP™ Silicon (2N to 4N+ Si) to attract

investors and commercial interest†said Mr. Tourillon.

About Silicon

Silicon (Si) is one of today’s strategic materials needed to fulfil

the renewable energy revolution presently under way. Silicon does not

exist in its pure state; it must be extracted from quartz, one of the

most abundant minerals of the earth’s crust and other expensive raw

materials in a carbothermic process.

About HPQ Silicon

HPQ Silicon Resources Inc. is a TSX-V listed company developing, in

collaboration with industry leader PyroGenesis (TSX-V: PYR) the

innovative PUREVAPTM “Quartz Reduction Reactors†(QRR), a truly

2.0 Carbothermic process (patent pending), which will permit the

transformation and purification of quartz (SiO2) into Metallurgical

Grade Silicon (Mg-Si) at prices that will propagate its significant

renewable energy potential.

HPQ is also working with industry leader Apollon Solar to develop:

Porous silicon wafers manufacturing using PUREVAP™ Silicon (PVAP Si) that can be used as anode for solid-state Li-ion batteries; and

A metallurgical pathway of producing Solar Grade Silicon Metal (SoG Si) that will take full advantage of the PUREVAPTM QRR

one-step production of high purity silicon (Si) and significantly

reduce the Capex and Opex associated with the transformation of quartz

(SiO2) into SoG-Si.

HPQ focus is becoming the lowest cost producer of Silicon (Si), High

Purity Silicon (Si), Porous Silicon Wafers and Solar Grade Silicon Metal

(SoG-Si). The pilot plant equipment that will validate the commercial

potential of the process is on schedule to start in 2019.

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

Disclaimers:

The Corporation’s interest in developing the PUREVAP™ QRR and any

projected capital or operating cost savings associated with its

development should not be construed as being related to the establishing

the economic viability or technical feasibility of the Company’s

Roncevaux Quartz Project, Matapedia Area, in the Gaspe Region, Province

of Quebec.

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward-looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Company’s current expectation and assumptions, and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Company with respect to future events and are subject to certain risks

and uncertainties and other risks detailed from time-to-time in the

Company’s on-going filings with the securities regulatory authorities,

which filings can be found at www.sedar.com. Actual results, events, and

performance may differ materially. Readers are cautioned not to place

undue reliance on these forward-looking statements. The Company

undertakes no obligation to publicly update or revise any

forward-looking statements either as a result of new information, future

events or otherwise, except as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

For further information contact Bernard J. Tourillon, Chairman, President and CEO Tel (514) 907-1011 Patrick Levasseur, Vice-President and COO Tel: (514) 262-9239 http://www.hpqsilicon.com Email: [email protected]

The industry has been growing exponentially thanks to plain old solar panels.

In the U.S., of all new power capacity added to the grid in 2018, about 30% was from solar.

Elon Musk may have promised the world Tesla solar roof tiles in 2016, but turns out the solar industry may not need the upgrade.

The industry has been growing exponentially thanks to plain old solar

panels. You can see the evidence both on people’s rooftops and in the

desert, where utility-scale solar plants are increasingly popping up.

Here in the U.S., of all new power capacity added to the grid in 2018, about 30% was from solar.

But the picture is not all rosy. Solar power is intermittent. The sun

isn’t always shining, and the price of storage solutions like lithium

ion batteries is still relatively high.

These are real problems that the industry needs to tackle if solar is

going to reach its potential. However, if the recent past is any

indication, solar power is going to help lead the transition to a

carbon-free future, and it might do it faster than we all expected.

Watch the video to learn more.

Developing, in collaboration with industry leader PyroGenesis (TSX-V: PYR) the innovative PUREVAPTM “Quartz Reduction Reactorsâ€, will permit the transformation and purification of quartz (SiO2) into Metallurgical Grade Silicon (Mg-Si) at prices that will propagate its significant renewable energy potential.

Also working with industry leader Apollon Solar to develop a metallurgical pathway of producing Solar Grade Silicon Metal (SoG Si) that will take full advantage of the PUREVAPTM QRR one-step production of high purity silicon (Si) and significantly reduce the Capex and Opex associated with the transformation of quartz (SiO2) into SoG-Si.

Focused on becoming the lowest cost producer of Silicon (Si), High Purity Silicon (Si) and Solar Grade Silicon Metal (SoG-Si). The pilot plant equipment that will validate the commercial potential of the process is on schedule to start in 2019.

Niagara Falls in Ontario, Canada, was chosen as the locale for the North American reveal of the Porsche Taycan

fully electric sedan for good reason: the ginormous hydro-electric

power plant that resides there. It didn’t hurt that the Taycan looked

imposing in the foreground of the press snaps either. It’ll likely

garner attention wherever it goes, especially from whomever it quietly

zooms past thanks to the eye-catching, futuristic design and some

serious power-train engineering.

In terms of size, the Taycan is smaller than the Panamera,

about the same size as a BMW 5 Series or a Mercedes-Benz E-Class, or

even the car that it’ll henceforth be benchmarked against: the Tesla

Model S. I got a test-ride in a Taycan around a Formula E track.

Despite being thrashed around by a professional racing driver, I felt

that the backseat was plush and spacious enough for my 6-foot-2 frame.

The car was also fast as hell.

The 750 hp Taycan Turbo S surges from zero to 60 mph in 2.8 seconds using launch control. Photo: Courtesy of Porsche AG.

Underneath the floor is a skateboard containing a 93 kWh lithium-ion

battery pack, which pushes energy to a pair of synchronous electric

motors, one for each axle. The front axle receives a single-speed motor

while the rear contains a two-speed transmission. For the quizzical, the

first gear is for acceleration, and the shift point is around 62 miles

an hour. While it’s pretty unusual for an EV to include a transmission,

the point here is pure power and time will tell whether this will

practically benefit drivers.

Onto the name. The base Taycan will be called the Turbo and some

engineering tinkering will eke out more power for the Turbo S. As there

is no combustion engine to which a turbo can physically be affixed, it’s

silly to keep the conventional names, but Porsche

is doing so because it believes customers can better equate the

products to competitor vehicles. (Later next year, there will be a wagon

variant, too.)

Both the Turbo and the Turbo S generate 616 hp, but an “overboostâ€

function affords the Turbo bursts up to 670 hp while the Turbo S pushes

750 ponies to the wheels. The torque is 626 and 774 ft lbs,

respectively, which is good enough to propel the 5,121-pound beast from a

standstill to 60 mph in 3.0 seconds for the Turbo and in 2.6 seconds

for the Turbo S. While those numbers are more blunted than a Tesla Model

S, Porsche would prefer you focus on the fact that the engineers were

more concerned with making an all-around dynamic car with repeatable

performance rather than a drag strip winner.

The Taycan Turbo runs with 670 horses and 626 ft lbs of torque. Photo: Courtesy of Porsche AG.

Porsche hopes for a range of 280 miles, though no official EPA

numbers have arrived. It’ll likely clock in around 240 miles, and that’s

a little bit of a bummer because the Model S can go about 50 percent

further (370 miles) on a battery that’s only about 8 percent bigger.

Perhaps to offset this, Porsche’s imbued the Taycan with 800-volt

charging systems, a giant nose-thumb to the norm of 400-volt systems in

most other EVs. Still, the battery can only take about 270 kWh at its

peak, though Porsche believes to achieve 400-500 kWh as advancements in

technology develop. For now, with optimal temperature and conditions,

the Taycan can go from five percent charge to 80 percent in roughly 20

minutes.

The Taycan’s high-tech interior. Photo: Courtesy of Porsche AG.

The Turbo starts at $153,510 (though the launch edition includes a

glass roof and better charger) and the Turbo S will begin at $187,610.

After launch, they’ll drop down to $150,900 and $185,000, respectively.

Are they worth the money? Check back with us later this month after our

first-drive review.