Posted by AGORACOM-JC

at 11:38 AM on Thursday, December 12th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

Nickel prices hit 2-week high

Nickel prices hit their highest in nearly two weeks on Thursday, as investors who bet on falling prices had to buy in at a strong support level.

By Mai Nguyen

SINGAPORE, Dec 12 (Reuters) – Nickel prices hit their highest in

nearly two weeks on Thursday, as investors who bet on falling prices had

to buy in at a strong support level.

Nickel prices have fallen in the past weeks to touch a five-month low

of $12,900 a tonne on the London Metal Exchange (LME) on Tuesday, as

the market viewed prices more expensive than supply and demand

fundamentals indicated.

“$13,000 was a critical number to defend,†said a trader.

Three-month nickel on the LME on Thursday climbed as much as 0.9% to $13,980 a tonne, its highest since Nov. 29.

The most-traded nickel contract on the Shanghai Futures Exchange

(ShFE) jumped as high as 3.5% to 110,570 yuan ($15,708.42) a tonne,

nearing a two-week high, before ending at 110,190 yuan a tonne, up 3.1%

from the previous close.

Other nickel industry players said that a royalty hike in top nickel

ore producer Indonesia contributed to a bullish view on prices, but they

expressed uncertainty over how long the upward trend could last.

FUNDAMENTALS

* SPREAD: The LME cash nickel contract was last at a $65 a tonne

discount to the three-month contract, suggesting sufficient nearby

supplies.

* NICKEL STOCKS: LME on-warrant nickel inventories, or those

available to the market, rose to a 2-1/2-month high at 67,248 tonnes.

MNISTX-TOTAL

* ALUMINIUM STOCKS & SPREAD: LME headline aluminium stocks

MALSTX-TOTAL jumped to their highest since April 2018 at 1.33 million

tonnes, and the spread between the cash and three-month contract flipped

to a discount of $8.75 a tonne after mostly holding in the premium zone

for around a month. CMAL0-3

* OTHER PRICES: LME zinc advanced 1.3% to $2,250 a tonne at 0712 GMT,

while copper fell 0.3% to $6,139 a tonne and aluminium rose 0.3% to

$1,766 a tonne. ShFE copper rallied 0.5% to 49,030 yuan a tonne and zinc

jumped 1.1% while aluminium fell 0.3%.

Posted by AGORACOM-JC

at 10:30 AM on Tuesday, December 10th, 2019

Tartisan Nickel Corp. has begun

An Investor Awareness Initiative with particular focus on Tartisan’s

flagship asset – The Kenbridge Nickel Deposit in Kenora, Ontario.

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

Advanced stage deposit remains open

in three directions, is equipped with a 623m deep shaft and has

never been mined.

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits.

Plans for Kenbridge include updating PEA, advancing the project through to feasibility and exploring the open mineralization at depth

FULL DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM-JC

at 12:56 PM on Wednesday, November 27th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

China to dominate battery metal demand

Demand trends for EV battery metals over the coming years have revealed that China will remain the key driver of direct metals demand

Direct demand for nickel, cobalt and lithium will remain the strongest in China across both the core and bearish case scenarios over the coming years.

By: Molly Hancock

Fitch Solutions’ demand trends for EV battery metals over the coming

years have revealed that China will remain the key driver of direct

metals demand.

The analysis estimates that the indirect growth for cobalt, nickel

and lithium will be the strongest across the EU under the bullish

scenario, which is underpinned by favourable policy assumptions.

However, indirect growth for these three metals will lag behind

across all scenarios in the United States, due to more restrictive EV

policy assumptions based on poor support at the federal level.

Fitch Solutions has divided the geographic demands for battery metals

into direct demand, which refers to demand from any country/region

where battery manufacturing takes place domestically and indirect

demand, which refers to demand from country/regions where EV sales make

stoke demand for batteries containing key metals that are produced.

The direct demand for nickel, cobalt and lithium will remain the

strongest in China across both the core and bearish case scenarios over

the coming years.

The Chinese Government has set ambitious EV targets and we retain a

positive outlook for China’s EV market as intensifying competition from

major vehicle brands will drive down costs and improve choice.

Despite recent subsidy cuts announced in July 2019, price reductions

among automakers and the rolling out of EV sales targets for vehicle

manufacturers will continue to position the Chinese EV market as the

most dynamic in the world.

While the demand growth for nickel, cobalt and lithium will spike in

2023-2025, Chinese carmakers’ strategies relating to EV production

targets generally end in 2025, and EV sales growth and subsequent metals

demand growth will begin to slow from 2025 onwards.

Fitch Solutions also revealed that due to the still-prevalent use of

iron-heavy LFP batteries in China, a bullish case for EV sales and

metals demand would lead to cumulative demand of 415,000 tonnes of iron

from the country over 2019-2028 compared to just 145,000 tonnes in its

bear case scenario.

Under Fitch Solutions’ bullish scenario, the EU will witness the

fastest average growth in indirect demand for cobalt (25.8 per cent

y-o-y), nickel (31 per cent y-o-y) and lithium (27.9 per cent y-o-y) up

to 2028, ahead of China and the US.

According to Fitch Solutions, the reason for this is that EU EV sales

team from a lower base in comparison to the US and China and as such

the potential for growth is higher.

For example, according to Fitch Solutions’ Autos team estimates, EV

sales will amount to over 370,000 units in 2019, compared to 458,000 in

the US and 1.252 million in China.

Within its bullish, base and bearish case scenarios, Fitch Solutions

forecast that the US indirect demand for cobalt, nickel and lithium to

average slower annual growth than in China and the EU over 2019-2028, as

a lack of supportive federal policy will pose obstacles to mass EV

adoption in the country.

In February 2019, the Trump administration announced new standards

that freeze emissions and fuel-efficiency requirements at the 2021

level, loosening previous higher targets and in contrasts to much

stricter regulations implemented by California and adopted by 12 other

states.

Its bullish case for the country assumes that future US government

policy will take a favourable turn towards the EV market, in order to

keep pace with rapidly developing EV segments in China and Europe.

The ongoing use of NCA batteries (containing nickel, cobalt and

aluminium) by Tesla in the US market means that indirect aluminium

demand will remain sustained in this market.

Cumulative indirect aluminium demand from the US EV market in our

bullish scenario will amount to 9800 tonnes over 2019-2028, compared

with to 3300 tonnes in China and 1300 tonnes in the EU.

Posted by AGORACOM-JC

at 3:33 PM on Monday, November 25th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

Nickel prices seen driven by Indonesia export ban, auto industry demand — Fitch Solutions

NICKEL prices are expected to gradually increase between 2020 and 2022 due to tight supply as a result of the export ban imposed by Indonesia, the mineral’s top producer, and the growing demand from the automotive industry, Fitch Solutions Macro Research said.

“While prices could still head lower in the coming weeks, we believe that they will rebound from spot levels as we move into 2020 and remain elevated throughout next year, buoyed by a tight fundamental picture,†Fitch Solutions said in its Commodity Price Forecast published on Nov. 22.

In 2020, it projects average nickel prices of $15,000 per ton,

upgrading a previous estimate of $14,500. This is expected to increase

to $15,500 in 2021 and 2022, then easing to $15,250 in 2023.

Fitch noted that the increase in price will be influenced by Indonesia’s nickel export ban starting January.

“In the longer term, we believe that prices will continue heading

higher up until 2022 as the market will remain in deficit or balanced,â€

it said, and added that the ban could also limit refining activity in

China next year. Chinese refining output is now expected to grow an

average of 2.5% year-on-year, down from 3% projected for 2019.

However, supply concerns due to the ban have started to dissolve due

to a realization that the Philippines could fill part of the gap as

suspended mines resume their operations.

The United States Geological Survey noted in a report published

February that Indonesia produced 560,000 tons of nickel last year,

making it the top producer, followed by the Philippines with 340,000

tons.

The Philippine Mines and Geosciences Bureau (MGB) said that in the

first half of the year, nickel ore production increased 3% to 11.306

million dry metric tons (DMT).

Nickel prices will also be influenced by demand from the automotive

industry, a major user of stainless steel, which is the main application

for nickel. Automotive demand will come into greater prominence amid an

expected slowdown in the Chinese construction industry.

“Vehicle production will continue to record positive average annual

growth of 1.0% over 2020-2028, lending some support to nickel demand.

Other major nickel-consuming markets such as South Korea and India will

also provide an upside to demand due to strong average vehicle

production growth of 9.1% and 11.4%, respectively, over the next 10

years,†Fitch Solutions said.

The booming electric vehicle market will also drive demand for

nickel, with most of the demand coming from China for the production of

lithium-ion batteries. China is expected to expand the minimum range of

vehicles eligible for subsidies to 150 kilometers (km) from 100 km. This

will increase demand for nickel since longer-range electric vehicles

need higher nickel content in their batteries.

“We forecast China to witness average EV sales growth of 10.9%

year-on-year over 2019-2028, which will drive global electric vehicle

sales growth and lead to an additional nickel demand during the period,â€

Fitch Solutions said. — Vincent Mariel P. Galang

Posted by AGORACOM-JC

at 10:14 AM on Monday, November 18th, 2019

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is

equipped with a 623m deep shaft and has never been mined.

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits.

Plans for Kenbridge include updating PEA,

advancing the project through to feasibility and exploring the open

mineralization at depth

FULL DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM-JC

at 5:57 PM on Tuesday, November 5th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

TN: CSE —————————-

Nickel Is Hot Right Now – The Nickel Boom May Have Just Begun

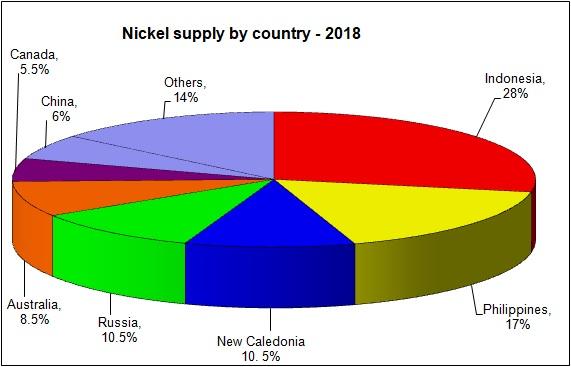

Indonesia announced they will ban nickel ore exports beginning 2020.

Indonesia currently accounts for about 27-28% of global nickel ore supply.

Other sources of nickel supply appear somewhat constrained, while demand for nickel looks strong, especially boosted by EVs.

Indonesia has declared that they will ban nickel ore exports as of January 1st, 2020

(previously scheduled for 2022). However, on Monday, September 2, 2019,

Indonesia’s Energy and Mineral Resources Ministry confirmed plans to move the ban up and place it ahead of schedule. Indonesia currently accounts for about 27-28% of global nickel ore supply. Nickel prices surged higher on the news.

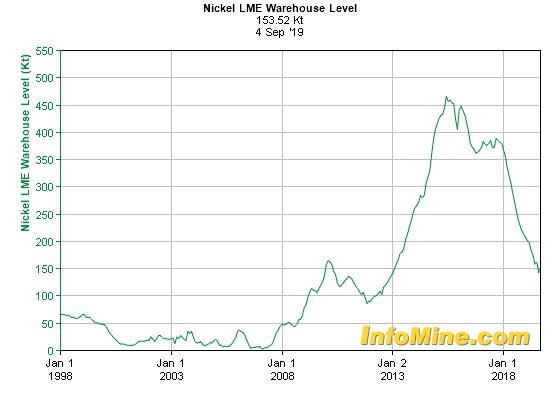

The 2007/08 nickel spike coincided with record low LME nickel

inventory levels (see chart below) and a China construction boom. Today,

LME nickel inventory is at 153,000 tonnes and has been falling steadily

for some time now. The Indonesia export ban could easily send nickel

inventories back below 50,000 tonnes in 2020 and cause another huge

nickel price spike.

Indonesia’s Coal and Minerals Director General Bambang Gatot Ariyono stated:

“The government decided, after weighing all the pros and cons, that we

want to expedite smelter building. So we took the initiative to stop

exports of nickel ores of all quality.â€

Indonesia will soon have 36 smelters, and if exports were to

continue, there would have been only enough reserves for seven to eight

years. These smelters can process low-grade nickel ores and they can be

used for batteries to help Indonesia meet its electric-vehicle goals.

Bambang continued: “We already exported 38 million

tons up until July this year. At this rate, we would need to think

about our reserves especially if we keep issuing exports permits.â€

Put simply, Indonesia has long wanted to encourage investments within

Indonesia that can value-add to their nickel ore. The end game would be

for Indonesia to be able to produce their own finished nickel,

stainless steel, and lithium-ion batteries (NMC batteries require plenty

of nickel).

“Indonesia currently has 13 operating nickel smelters with input

capacity of 24.52 million tonnes. Government data showed that 22 more

nickel miners are currently under development with additional capacity

of 46.33 million tonnes. Lengkey said the installed capacity will not be

enough to process the country’s ore output.”

Nickel supply by country

Source: Own chart with data sourced from Investing News

Other sources of nickel supply

The Philippines is the number two global nickel supplier. No doubt Philippine nickel miners will tryto boost

ore production next year when the Indonesia export ban kicks in. The

Philippines has 29 nickel mines and two nickel processing plants.

However, strict environmental law changes in the Philippines in recent

years have reduced their nickel supply. Also, it is said that many

Chinese buyers prefer higher-grade ores from Indonesia. Current

Philippine nickel ore production has dropped to about 340,000

tonnes in 2018 due to the closure of 23 mines as the government seeks

to curb environmental damage from mines in the Philippines.

Perhaps the boost will come from New Caledonia, Russia, Australia,

Canada, China and some contributions from the new Indonesian smelters.

But will this be enough?

Overall, it appears for now that very large new sources of nickel

supply appear somewhat constrained, especially given the Philippines

recent focus on environmental protection and nickel mine closures.

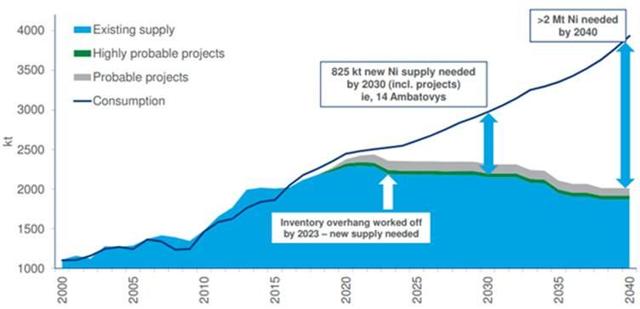

Nickel demand looks set to increase boosted by electric vehicles

All experts agree that demand for nickel sulphate is set to go

through the roof as electric vehicles [EVs] take off. Fastmarkets stated last year:

“Demand for nickel in the EV space is expected to total 36,000 tonnes in 2018… That figure is expected to surge to 350,000-500,000 tonnes by 2025.â€

That’s more than a tenfold increase, in just 7 years. Wow!

The best source of nickel sulphate will come from the nickel sulphide miners.

No doubt new sources of nickel will start to fill the supply gap that

Indonesia will leave, but this takes time. Indonesia will also step up

their processing of ores, but this will take several years to raise

capital and then build out the processing plants. Many companies that

halted nickel sales due to the recent bear market years for base metals

will start to come back online, as will new nickel projects assuming the

nickel price stays strong. Will we see nickel over USD 10/lb in 2020?

Yes, I would say this is very possible, as with most severe supply

disruptions, the industry usually takes a couple of years to catch up.

The chart below shows nickel is forecast to be in deficit after ~2020-2022 (and this was before factoring in the Indonesia ban).

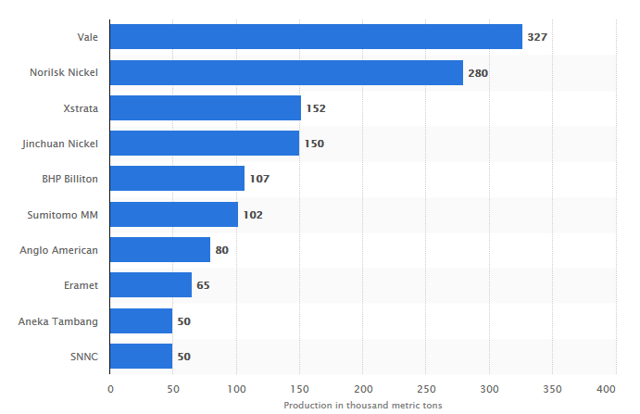

The top global nickel producers by nickel production volume are Vale [BZ: VALE3](NYSE:VALE), Norilsk Nickel [LSX: MNOD] (OTCPK:NILSY), Jinchuan International Group Resources [HK:2362], Glencore (OTCPK:GLCNF)[LSX:GLEN], and BHP Group [ASX:BHP] (NYSE:BHP). Good smaller producers include Independence Group [ASX:IGO] (OTC:IIDDY) and Western Areas [ASX:WSA](OTCPK:WNARF). Some top nickel developers with very large resources include RNC Minerals [TSX:RNX] (OTCQX:RNKLF), Ardea Resources [ASX:ARL] (OTCPK:ARRRF), and Australian Mines [ASX:AUZ].

Rather than repeat information from my other recent nickel articles

here, I refer to the further reading section below that gives plenty of

company information.

Forecast leading companies based on finished nickel production worldwide in 2020 (in 1,000 metric tons)

A China or global slowdown could reduce demand for nickel. China and

the stainless steel industry are by far the largest consumers of

nickel.

Nickel prices falling. Indonesia may reverse their decision, or

other countries may bring on excess new supply. Also, the new Indonesian

smelters once running will be a new source of nickel supply from

Indonesian nickel ore. Noting Indonesia already has 13 operating

smelters.

This article is for the purpose of alerting Trend Investing members

that the nickel boom may have just begun. Certainly all the signs are

there.

The further reading section above gives plenty of good information on

the better nickel plays. My standout nickel miner continues to be

Norilsk Nickel due to their massive (sulphide) resources, very low cost

of production when taking into account by-products (palladium, copper),

low valuation (2020 PE of 8.3),

and high dividend yield (2020 estimate 10.9%). Vale offers some

attraction right now after recent price falls, but is mostly an iron ore

miner. My top nickel developers are RNC Minerals, Ardea Resources, and

Australian Mines.

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in Tartisan Nickel | Comments Off on Tartisan #Nickel $TN.ca – Nickel Is Hot Right Now – The Nickel Boom May Have Just Begun $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 4:04 PM on Monday, November 4th, 2019

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is

equipped with a 623m deep shaft and has never been mined.

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits.

Plans for Kenbridge include updating PEA,

advancing the project through to feasibility and exploring the open

mineralization at depth

FULL DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in All Recent Posts, Tartisan Nickel | Comments Off on CLIENT FEATURE: Tartisan Nickel $TN.ca Kenbridge Property Hosts M&I Resource of 7.14 Million Tonnes of 0.62% Nickel + 0.33% Copper $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 11:03 AM on Wednesday, October 30th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

TN: CSE —————————-

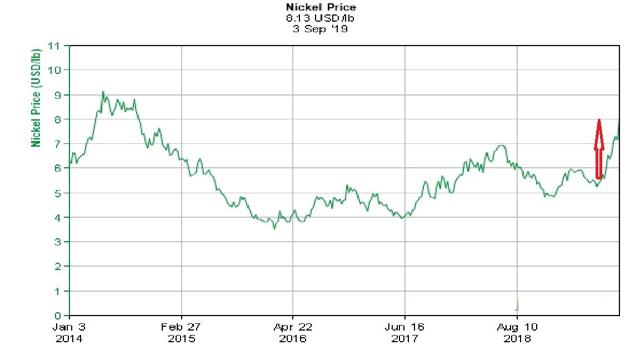

A nickel for your thoughts – The price of nickel has run up to a five-year high of late

The price of nickel has run up to a five-year high of late, defying softness in the rest of the base metal complex.

The reasons are both simple and complicated. The price of nickel

doubled in two years, from US$4 per lb. in August 2017 to US$8 per lb. a

few weeks ago. The reasons:

· Robust demand. Nickel is primarily used to make stainless steel. And despite slowing growth, stainless steel demand keeps marching up.

In the first half of 2019, for instance, Chinese stainless steel

production was up 8.5% yearover-year. (As the chart suggests, forecasts

predict softening of demand in the current quarter.)

· China makes most of the world’s stainless steel. And China gets the

nickel for that steel from its own mines as well as mines in Indonesia

and the Philippines, many of which produce a lowgrade, high-impurity ore

called nickel pig iron (NPI). NPI production has

ballooned over the last decade, enough that as of 2020 the world will

get more of its nickel from NPI than from conventional nickel ores.

However, this reliance on NPI brings with it a few problems.

· Indonesia will implement a ban on nickel ore exports at the start of 2020.

This has been in the works for some time but until a few months ago the

ban was not scheduled to take effect until 2022. Indonesia produces

roughly ~12% of global supply, so this ban is significant. The idea is

to push the development of domestic smelters, which would keep more of

the resource upside in country versus exporting raw ore. This is in the

works – the country already has 11 nickel smelters and 25 more are

planned or under construction – so Indonesian nickel supplies should

slide in the near term but recover within about three years. However,

the smelters in China that relied on Indonesia’s nickel pig iron (NPI)

ore will have to find feed elsewhere; the main candidate is the

Philippines, where ore is generally lower grade. The only other option

is to upgrade to processing Class I ores. Either move would increase

costs overall, which supports a higher nickel price.

· Batteries. Eighty percent of the world’s nickel

goes into stainless steel, so steel certainly drives the market. But

many of the batteries that power laptops, electric vehicles, phones, and

even power grids require nickel. This has transformed nickel from a one

trick pony to a two trick market – and if electric cars take off then

nickel’s battery market will take off right alongside. Right now

batteries consume 5% of global nickel but demand is rising rapidly and

is expected to reach 8% by 2020. Vice President of market analysis and

economics for BHP, Dr Huw McKay, says he sees a future where batteries

and stainless steel become “equally important†nickel consumers. Global

nickel demand currently sits around 2 million tonnes per annum; it is

expected to grow to 6 million tonnes per annum by 2035 with batteries

accounting for almost half of demand growth.

· In addition, batteries cannot use nickel from NPI, as impurities are too high, so the battery factor has divided the nickel market into two parts

– high purity Class I nickel and lower purity Class II. All of this has

two important effects: it is bringing energy metal investors into the

nickel space and it is underlining that NPI, which has been the dominant

source of nickel growth for the last 10-plus years, will not solve the

nickel supply gap going forward.

· To address that second point and boost production of Class I

nickel, China is developing several mines tapping into nickel laterite

deposits. Nickel laterite is easy to mine but very difficult to process,

requiring high pressure acid leaching (HPAL). Most analysts are

highly skeptical that China’s planned HPAL facilities will come online

anywhere near their projected timelines or budgets, as these facilities are notoriously difficult and expensive.

· Because NPI has ballooned so in the last decade, explorers and developers have not looked for conventional nickel deposits. There

is a true lack of development-stage nickel projects with conventional

sulphide deposits that could be built to fill supply gaps.

· Current mine-specific supply issues. The biggest

producer of NPI in the Philippines just ran out of ore. The Ramu project

in Papua New Guinea is temporarily suspended, which removes 35,000

tonnes of annual nickel supply.

· Stockpiles are falling – and fast. Nickel stockpiles have been declining for five years.

This is what happens when a market is persistently undersupplied. But

as you can see, the decline accelerated in the last two years…and

stockpiles dropped off a cliff a few weeks ago.

The cliff is likely the result of panic buying and/or stockpiling ahead of the Indonesian ban.

I told you it was complicated!

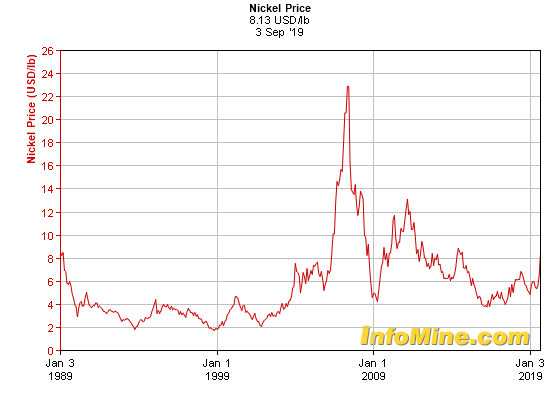

Complicated is normal for nickel, which has a long track record of

extreme price moves. In 2008 a supply shortage drove the price as high

as US$22 per lb. before steel mills found substitutes, 7 including

manganese, and within 18 months the price was back at US$4.50 per lb.

(The Great Financial Crisis likely exacerbated the price decline.)

The Bear Case

The key question on this side is: to what extent is speculation driving nickel?

If speculators are pushing the price up, entering the space now is

risky because (1) speculative tides turn fast and (2) that turn would

likely transpire in the next 6 to 9 months. Indonesia’s ban comes into

effect in January 1 so over the next six months the impacts start to

play out.

It’s clear that stockpile drawdowns are at least in part because

smelters and speculators have been stockpiling metal privately. That

metal will be used or sold to ease any nickel price jumps.

If increased physical metal availability coincides with the absence of speculative upside pressure…nickel could turn down fast.

On top of all that, there are reasons to believe (1) stainless steel

demand will weaken to end this year, (2) EV demand is taking longer to

ramp than expected, (3) scrap usage is increasing, and (4) rising

backwardation alongside falling physical premiums is a sign that actual

demand is lower than perceived.

The fourth point above needs some explaining. In a tight market,

limited stockpiles lead to backwardation – people paying more for metal

today than in the future. Backwardation should only happen when the

current physical market is very tight. If that’s the case, there should

also be high physical premiums, which are extra amounts paid for actual

metal now (rather than paper metal).

What weird about nickel is that premiums are down sharply, from $200

per tonne a few months ago to negative $50 per tonne today. It’s the

first-time premiums have ever gone negative in China and something that

is very rare across the metals complex. European nickel briquette

premiums are also down 80% in recent months.

The dark blue line below shows physical premiums. The light blue line

shows the difference between current and three-month nickel prices; a

positive Cash-3M is backwardation.

<

This suggests:

· The physical market is not that tight

· Speculation in the paper market is driving the price

· Speculation is not simply investors; nickel users and producers are

also playing games (stockpiling) to boost the price. When they stop,

the price will lose ground rapidly.

The Bottom Line

Nickel may or may not continue its bull run from here. The fact the

physical premiums are so low when prices have gained so much and the

paper market is in backwardation is definitely concerning, enough that I

am not ready to enter the space right now. The fact that nickel spot

price recently stepped back almost 10% reinforces my outlook.

However, in the medium and long term this is a market that has good

opportunity. Stainless steel demand growth is reliable. The battery

space will need more and more Class I nickel with each year. The

pipeline of new projects is very limited, especially if you (like me)

see China struggling with its nickel laterite output mines and HPAL

facilities.

I might be wrong and my hesitation on entering now may mean missing

out on near term upside, but such decisions are common in this sector!

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in Tartisan Nickel | Comments Off on Tartisan #Nickel $TN.ca – A nickel for your thoughts – The price of nickel has run up to a five-year high of late $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 10:48 AM on Wednesday, October 16th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)Â Kenbridge Property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has interests in Peru, including a 20 percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property. Click her for more information

TN: CSE —————————-

Nickel and palladium surge on the back of supply constraints

Nickel price has recently surged reaching US$18,000/t

This is mostly due to the Indonesian nickel ore export ban to commence January 2020, as well as the Philippines indefinitely suspending nickel mining in southern Philippines (27% of overall Philippine nickel ore exports are from this area).

The past few years have generally been tough for the miners,

especially for investors that joined the electric vehicle (EV) metal

miners boom at its first peak (January 2018). However, all is not lost.

For nimble investors, there are some great gains to be made when metal

prices spike, but you need to be not too late to the party. Right nowtwo metals are rising fast

on supply constraints and strong demand. Furthermore, they should

continue to do well for some time. In many cases, the associated miners

have been slow to reflect the gains as investor sentiment has been

weighed down by the trade war. This leaves some incredible buys for those willing to invest.

Those two metals are nickel and palladium.

Nickel

As we can see below the nickel price has recently surged reaching US$18,000/t. This is mostly due to the Indonesian nickel ore export ban to commence January 2020, as well as the Philippines indefinitely suspending nickel mining in southern Philippines (27% of overall Philippine nickel ore exports are from this area).

Nickel supply reductions from the two largest nickel producing

countries (Indonesia and Philippines represent 45% of global nickel

supply) and an EV led demand surge are combining to cause nickel

deficits and a nickel price spike, as shown below.

Add in resilient nickel demand and soon a surge in EV related demand and you have the recipe for a nickel boom.

Nickel 5 year price chart

EV related demand for class 1 nickel is set to surge more than

tenfold from end 2018 to 2025, or increase from 36,000 tonnes in 2018 to

350,000-500,000 tonnes by 2025. In a 2 million tonne total nickel

market, a 500,000 tonne increase represents a 25% increase just from the

EV boom.

LME nickel inventory levels fell last week the most in 40 years

Just last week LME inventory levels fell the most in 40 years, as

China’s Tsingshan Holding Group Co. bought 25,000 tonnes of LME nickel.

Apparently a further 75,000 tons of metal are scheduled to be delivered

out soon. That could send LME nickel below 50,000 tonnes and panic the

market causing nickel prices to surge even higher.

Palladium

Palladium metal prices have doubled the past year and a half on the

back of strong demand for palladium used in catalytic converters. The

price is now over US$1,700/oz, significantly higher than gold at

US$1,492/oz.

Palladium 5 year price chart

Europe is reducing emissions targets in 2020, 2025, and 2030 and

other countries will follow. This means more palladium will be needed in

catalytic converters. As reported

by Reuters, Morgan Stanley recently stated that starting 2020 in China

each vehicle will need to contain around 30% more palladium, platinum

and rhodium. Some analysts are already forecasting US$2,000/oz palladium.

The only caveat here is if we see very rapid electric vehicle take up

and hence less internal combustion engine (ICE) vehicles then demand

could stall or even reverse. However, this should still be several years

away given the electric car market share globally is still only at

2.3%. Hybrid EVs use both palladium and nickel. Note also that platinum

can be used to substitute for palladium but it is not so easy and the

cycle to replace can be costly and take ~2 years.

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in Tartisan Nickel | Comments Off on Tartisan #Nickel $TN.ca – Nickel and palladium surge on the back of supply constraints $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 8:36 AM on Wednesday, October 9th, 2019

Company has engaged Aster Funds Ltd, Toronto, Ontario, to conduct a satellite-based long wave infrared thermal mineral scan and a synthetic aperture radar survey of the Sill Lake Pb-Ag property, Vankoughnet Twp. Ontario.

Aster Funds Ltd provides spectral analysis surveys and synthetic aperture radar surveys to exploration companies

TORONTO, ON / October 9, 2019 / Tartisan Nickel Corp. (CSE:TN)(OTCPINK:TTSRF)(FSE:A2D) (“Tartisan”, or the “Company”) is pleased to announce that the Company has engaged Aster Funds Ltd, Toronto, Ontario, to conduct a satellite-based long wave infrared thermal mineral scan and a synthetic aperture radar survey of the Sill Lake Pb-Ag property, Vankoughnet Twp. Ontario.

Aster Funds Ltd provides spectral analysis surveys and synthetic

aperture radar surveys to exploration companies principally active in

Canada, Latin America, and Australia. The spectral analysis survey

provides a property-wide distribution of up to 16 mineral and rock

species consistent with the Sill Lake deposit model, while the synthetic

aperture radar survey provides a distribution of surface and shallow

buried conductors similar to what an airborne electromagnetic survey

would generate.

Tartisan Nickel CEO Mr. Mark Appleby said, “we are going to test Sill

Lake with the Aster Funds Ltd technology, which should give us some

very good insights into the extent of mineralization on the property.

This would focus detailed exploration on targets that would deliver

shareholder value in a discovery or definition context.”

Tartisan Nickel Corp. common shares are listed on the Canadian

Securities Exchange (CSE:TN, US-OTC-TTSRF, FSE A2D). Currently, there

are 100,403,550 shares outstanding (103,103,550 fully diluted).

For further information, please contact Mr. D. Mark Appleby,

President & CEO and a Director of the Company, at 416-804-0280 ([email protected]). Additional information about Tartisan can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

Jim Steel MBA P.Geo. is the Qualified Person under NI 43-101 and has

read and approved the technical content of this News Release.

This news release may contain forward-looking statements

including but not limited to comments regarding the timing and content

of upcoming work programs, geological interpretations, receipt of

property titles, potential mineral recovery processes, etc.

Forward-looking statements address future events and conditions and

therefore, involve inherent risks and uncertainties. Actual results may

differ materially from those currently anticipated in such statements.

The Canadian Securities Exchange (operated by CNSX Markets Inc.)

has neither approved nor disapproved of the contents of this press

release.

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in Tartisan Nickel | Comments Off on Tartisan Nickel Corp $TN.ca Engages Aster Funds Ltd for a Spectral Analysis Survey of the Sill Lake Lead-Silver Project $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca