Posted by AGORACOM-JC

at 5:26 PM on Monday, December 23rd, 2019

Announce that it has acquired 3,000,000 units of St-Georges Eco-Mining Corp. at a price of $0.10 per Unit

In consideration, the Company has issued an aggregate of 5,000,000 common shares of the Company at a deemed price of $0.05 per common share and made a cash payment in the amount of $50,000.

TORONTO, Dec. 23, 2019 – ThreeD Capital Inc. (the “Companyâ€) (CSE:IDK), a Canadian-based venture capital firm focused on investments in promising, early stage companies and ICOs with disruptive capabilities, is pleased to announce that it has acquired 3,000,000 units (the “Unitsâ€) of St-Georges Eco-Mining Corp. (“St-Georgesâ€) at a price of $0.10 per Unit. In consideration, the Company has issued an aggregate of 5,000,000 common shares of the Company at a deemed price of $0.05 per common share (the “Offeringâ€) and made a cash payment in the amount of $50,000. Each Unit of St-Georges consists of one common share (the “Shareâ€) of St-Georges and one share purchase warrant (the “Warrantâ€) of St-Georges, with each Warrant being exercisable to acquire one additional Share at an exercise price of C$0.185 for a period of 9 months following the date of issuance.

“ThreeD is very pleased to deepen its relationship with St-Georges,â€

said ThreeD Capital’s Founder, Chairman and CEO Sheldon Inwentash.

“We are pleased to have the continuous support of ThreeD in our

financing efforts. The company has been a supportive partner helping us

expand our different business silos and making valuable introductions,â€

commented Mark Billings, Chairman of St-Georges.

All securities issued and issuable in connection with the Offering

are subject to a statutory hold period expiring on April 24, 2020.

About ThreeD Capital Inc.

ThreeD is a publicly-traded Canadian-based venture capital firm

focused on opportunistic investments in companies in the Junior

Resources, Artificial Intelligence and Blockchain sectors. ThreeD seeks

to invest in early stage, promising companies and ICOs where it may be

the lead investor and can additionally provide investees with advisory

services, mentoring and access to the Company’s ecosystem.

Posted by AGORACOM-JC

at 3:32 PM on Monday, December 23rd, 2019

SPONSOR:ThreeD Capital Inc. (IDK:CSE)

Led by legendary financier, Sheldon Inwentash, ThreeD is a

Canadian-based venture capital firm that only invests in best of breed

small-cap companies which are both defensible and mass scalable. More

than just lip service, Inwentash has financed many of Canada’s biggest

small-cap exits. Click Here For More Information.

Institutional Investment in Crypto: Top 10 Takeaways of 2019

By: Scott Army

This post is part of CoinDesk’s 2019 Year in Review, a collection

of 100+ op-eds, interviews and takes on the state of blockchain and the

world. Scott Army is the founder and CEO of digital asset manager

Vision Hill Group. The following is a summary of the report: “An Institutional Take on the 2019/2020 Digital Asset Marketâ€.

No. 1: There’s bitcoin, and then there’s everything else.

The industry is currently segmented into two main categories: Bitcoin

and everything else. “Everything else†includes: Web3 innovation,

Decentralized Finance (“DeFiâ€), Decentralized Autonomous Organizations,

smart contract platforms, security tokens, digital identity, data

privacy, gaming, enterprise blockchain or distributed ledger technology,

and much more.

Non-crypto natives are seldom aware that there are multiple

blockchains. Bitcoin, by virtue of it being the first blockchain network

brought into the mainstream and by being the largest digital asset by

market capitalization, is often the first stop for many newcomers and

likely will continue to be for the foreseeable future.

No. 2: Bitcoin is perhaps market beta, for now.

In traditional equity markets, beta is defined as a measure of

volatility, or unsystematic risk an individual stock possesses relative

to the systematic risk of the market as a whole. The difficulty in

defining “market beta†in a space like digital assets is that there is

no consensus for a market proxy like the S&P 500 or Dow Jones.

Since the space is still very early in its development, and bitcoin has

dominant market share (~68 percent at the time of writing), bitcoin is

often viewed as the obvious choice for beta, despite the drawbacks of defining “market beta†as a single asset with idiosyncratic tendencies.

Bitcoin’s size and its institutionalization (futures, options,

custody, and clear regulatory status as a commodity), have enabled it to

be an attractive first step for allocators looking to get exposure

(both long and short) to the digital asset market, suggesting that

bitcoin is perhaps positioned to be digital asset market beta, for now.

No. 3: Despite slow conversion, substantial progress was made on growing institutional investor interest in 2019.

Education, education, education. Blockchain technology and digital

assets represent an extraordinarily complex asset class – one that

requires a non-trivial time commitment to undergo a proper learning

curve. While handfuls of institutions have already started to invest in

the space, a very small amount of institutional capital has actually

made it in (relative to the broader institutional landscape), gauged by

the size of the asset class and the public market trading volumes. This

has led many to repeatedly ask: “when will the herd actually come?â€

The reality is that institutional investors are still learning –

slowly getting comfortable – and this process will continue to take

time. Despite educational progress through 2019, some institutions are

wondering if it’s too early to be investing in this space, and whether

they can potentially get involved in investing in digital assets in the

future and still generate positive returns, but in ways that are

de-risked relative to today.

Despite a few other challenges imposed on larger institutional

allocators with respect to investing in digital assets, true believers

inside these large organizations are emerging, and the processes for

forming a digital asset strategy are either getting started or already

underway.

No. 4: Long simplicity, short complexity

Another trend we observed emerge this year was a shift away from

complexity and toward simplicity. We saw significant growth in simple,

passive, low-cost structures to capture beta. With the lowest-friction

investor adoption focused on the largest liquid asset in the space –

bitcoin – the proliferation of single asset vehicles has increased.

These private vehicles are a result of delayed approval of an official

bitcoin ETF by the SEC.

In addition to the Grayscale Bitcoin Trust, other bitcoin-focused products this year include the launch of Bakkt, the launch of Galaxy Digital’s two new bitcoin funds, Fidelity’s bitcoin product rollout, TD Ameritrade’s bitcoin trading service on Nasdaq via its brokerage platform, 3iQ’s recent favorable ruling for a bitcoin fund and Stone Ridge Asset Management’s recent SEC approval for its NYDIG Bitcoin Strategy Fund, based on cash-settled bitcoin futures.

We also observed a growing institutional appetite for simpler hedge

fund and venture fund structures. For the last several years, many

fundamental-focused crypto-native hedge funds operated hybrid structures

with the use of side-pockets that enabled a barbell strategy approach

to investing in both the public and private digital asset markets.

These hedge funds tend to have longer lock-up periods – typically two or

three years – and low liquidity. While this may be attractive from an

opportunistic perspective, the reality is it’s quite complicated from an

institutional perspective for reporting purposes.

No. 5: Active management’s been challenged, but differentiated sources of alpha are emerging.

For the year-to-date period ended Q3 2019,

active managers were collectively up 30 percent on an absolute return

basis according to our tracking of approximately 50

institutional-quality funds, compared to bitcoin being up 122 percent

over the same time period.

Bitcoin’s performance this year, particularly in Q2 2019, has made it

clear that its parabolic ascents challenge the ability of active

managers to outperform bitcoin during the windows they occur. Active

managers generally need to justify the fees they charge investors by

outperforming their benchmark(s), which are often beta proxies, yet at

the same time they need to avoid imprudent risk behavior that can

potentially have swift and sizable negative effects on their

portfolios.

Interestingly, active management performance from the beginning of

2018 consistently outperformed passively holding bitcoin (with the

exception of “opportunistic†managers who also take advantage of yield

and staking opportunities, as of May 2019). This is largely due to

various risk management techniques used to mitigate the negative

performance drawdowns experienced throughout the extended market

sell-off in 2018.

Source: Vision Hill Group

Although 2019 has challenged the large-scale success of these alpha

strategies, they are nonetheless in the process of proving themselves

out through various market cycles, and we expect this to be a growing

theme in 2020.

No. 6: Token value accrual: Transitioning from subjective to objective

At the end of Q3 2019, according to dapp.com,

there were 1,721 decentralized applications built on top of ethereum,

with 604 of them actively used – more than any other blockchain.

Ethereum also had 1.8 million total unique users, with just under

400,000 of them active – also more than any other blockchain. Yet,

despite all this growing network activity, the value of ETH has remained

largely flat throughout most of 2019 and is on track to end the year

down approximately 10 percent at the time of writing (by comparison, BTC

has nearly doubled in value over the same period). This begs the

question: is ETH adequately capturing the economic value of the ethereum

network’s activity, and DeFi in particular?

A new fundamental metric was introduced earlier this year by Chris Burniske

– the Network Value to Token Value (“NVTVâ€) ratio – to ascertain

whether the value of all assets anchored into a platform can be greater

than the value of the base platform’s asset.

The ETH NVTV ratio has steadily declined

throughout the last few years. There are likely to be several reasons

for this, but I think one theory summarizes it best: most applications

and tokens built and issued atop ethereum may be parasitic. ETH token

holders are paying for the security of all these applications and

tokens, via the inflation rate that is currently given to the miners –

dilution for ETH holders, but not for holders of ethereum-based tokens.

This is not a bullish or bearish statement on ETH; rather it is an

observation of early signs of network stack value capture in the space.

No. 7: Money or not, software-powered collateral economies are here

Another trend we observed this year is a larger migration away from

“cryptocurrencies†in an ideological currency (e.g., money/payment and a

means of exchange) sense, and toward digital assets for financial

applications and economic utility. A form of economic utility that took

the stage this year is the notion of software-powered collateral

economies. People generally want to hold assets with disinflationary or

deflationary supply curves, because part of their promise is that they

should store value well. Smart contracts enable us to program the

characteristics of any asset, thus it is not irrational to assume that

it’s only a matter of time until traditional collateral assets get

digitized and put to economic use on blockchain networks.

The benefit of digital collateral is that it can be liquid and

economically productive in its nature while at the same time serving its

primary purpose (to collateralize another asset), yet without

possessing the risks of traditional rehypothecation. If assets can be

allocated for multiple purposes simultaneously, with the risks

appropriately managed, we should see more liquidity, lower cost of

borrowing, and more effective allocation of capital in ways the

traditional world may not be able to compete with.

No. 8: Network lifecycles: An established supply side meets a quiet but emerging demand side.

Supply side services in digital asset networks are services provided

by a third party to a decentralized network in exchange for compensation

allocated by that network. Examples include mining, staking,

validation, bonding, curation, node operation and more, done to help

bootstrap and grow these networks. Incentivizing the supply side is

important in digital assets to facilitate their growth early in their

lifecycles, from initial fundraising and distribution through the

bootstrapping phase to eventual mainnet launches.

While there has been significant growth of this supply side of

the equation in 2019 from funds, companies, and developers, the open

question is how and when demand for these services will pick up. Our

view is that as developer infrastructure continues to mature and

activity begins to move “up the stack†toward the application layer,

more obvious manifestations of product-market fit are likely to emerge

with cleaner and simpler interfaces that will attract high volumes of

users in the process. In essence, it is important to build the necessary

infrastructure first (the supply side) to enable buy-in from the end

users of those services (the demand side).

No. 9: We are in the late innings of the smart contract wars.

While ethereum leads the space on adoption and moves closer to

executing on its scalability initiatives, dozens of smart contract

competitors fundraised in the market throughout 2018 and 2019 in an

attempt to dethrone ethereum. A handful have formally launched their

chains and operate in mainnet as of the end of 2019, while many others

remain in testnet or have stalled in development.

What’s been particularly interesting to observe is the accelerative

pace of innovation – not just technologically, but economically

(incentive mechanisms) and socially (community building) as well. We

expect many more smart contract competitors operating privately as of Q4

2019 to launch their mainnets in 2020. Thus, given the incoming

magnitude of publicly observable experimentations throughout 2020, if a

smart contract platform does not launch in 2020, it is likely to become

disadvantageously positioned relative to the rest of the landscape as it

relates to capturing substantial developer mindshare and future users

and creating defensible network effects.

No. 10: Product-market fit is coming, if not already here

We don’t think human and financial capital would have continued

pouring into the digital asset space in such great magnitude over the

last several years if there wasn’t a focus on solving at least one very

clear problem. The questionable sustainability of modern monetary theory

is one of them, and Ray Dalio of Bridgerwater Associates has been quite vocal

about it. Big Tech centralization is another. There are also growing

global concerns related to data privacy and identity. And let’s not

forget cybersecurity. The list goes on. We are at the tip of the iceberg

as it relates to the products and applications blockchain technology

enables, and mainstream users will come with growing manifestations of

product-market fit. As more time and attention gets spent on diagnosing

problems and working on solutions, the industry will begin to achieve

its full potential. Facebook’s Libra and Twitter’s Bluesky initiative

confirm that as an industry we are heading in the right direction.

A 2020 look ahead

We see 2020 shaping up to be one of the brightest years on record for

the digital asset industry. To be clear, this is not a price forecast;

if we exclusively measured the health of the industry from a fundamental

progress perspective, by various accounts and measures we should have

been in a raging bull market for the last two years, and that has not

been the case. Rather, we expect 2020 to be a year of accelerated

industry maturation.

Source: Vision Hill Group

Digital assets are still an emerging asset class with many quickly

evolving narratives, trends, and investment strategies. It is important

to note, that not all strategies are suitable for all investors. The

size of allocations to each category will and should vary depending on

the specific allocator’s type, risk tolerance, return expectations,

liquidity needs, time horizon and other factors. What is encouraging is

that as the asset class continues to grow and mature, the opacity slowly

dissipates and clearly defined frameworks for evaluation will continue

to emerge. This will hopefully lead to more informed investment

decisions across the space. The future is bright for 2020 and beyond.

Posted by AGORACOM-JC

at 2:13 PM on Monday, December 23rd, 2019

SPONSOR: CardioComm Solutions (EKG: TSX-V)

– The heartbeat of cardiovascular medicine and telemedicine. Patented

systems enable medical professionals, patients, and other healthcare

professionals, clinics, hospitals and call centres to access and manage

patient information in a secure and reliable environment.

mHealth Market is Expected to Expand at a CAGR of 22.1% During 2017 to 2025

According to experts from TMR, the global mHelath market stood at US$23.9 bn in 2017

This revenue is expected to gain an impressive value of US$118.4bn by the end of 2025

Experts project this growth to occur with a meteoric CAGR of 22.1% during the forecast period from 2017 to 2025

The globalmHelath market bears

a highly fragmented vendor landscape, says Transparency Market Research

(TMR) in a recently published report. This is solely because of the

existence of large, medium, and small-scale players in the market. Withings, FitBit, Apple Inc., Jawbone, and Dexcom are the dominant players working in the global mHelath market.

Out of the various strategic alliances

adopted by players in the global mHelath market to hold a sizeable

stakes, capitalizing on the emerging opportunities and acquiring latest

technologies and tools has gained maximum popularity. The level of

competition among leading vendors is getting escalated with rising use

of technologies and smart devices such as wearables. The global mHelath

market is expected to grow steadily due to the presence of highly

established players who are concentrating on improving their product

quality, facilitating product differentiation, and enhancing

geographical reach. These companies are also attempting to introduce

advanced and new products into the industry on a daily basis.

According to experts from TMR, the

global mHelath market stood at US$23.9 bn in 2017. This revenue is

expected to gain an impressive value of US$118.4bn by the end of 2025.

Experts project this growth to occur with a meteoric CAGR of 22.1%

during the forecast period from 2017 to 2025.

Among various products in the global

mHelath market, connected medical devices hold substantial share, which

is expected to boost the global mHelath market during the forecast

period. This is because of rising focus towards fitness and increasing

use of heart rate monitors among people. Region wise, North America is

expected to lead the global mHelath market in the coming years. This is

attributed to a strong technological infrastructure along with high

healthcare expenditure in the region.

Integration of Wireless Technologies to Fuel mHealth Market’s Growth

Health-related technologies and mobile

applications are often known as mHealth, which helps in managing

patients’ experiences. Such health mobile technologies and apps utilize

advanced data analytics to help medical professionals in providing their

patients best care at low cost. These health mobile applications

facilitate easy and better health management through simple apps such as

diet, exercise trackers, and calorie-counting. Such USPs are driving

the global mHelath market. Along with this, rising penetration of

internet connections and smartphones, and rapid technological

advancements in healthcare industry are the factors majorly fueling

growth in the global mHelath market.

Furthermore, mHelath ensures continuous

communication between medical professionals and patients, thereby allow

physicians to monitor, and diagnose patients without seeing them in

person. Such benefits are also boosting the global mHelath market. Apart

from these, rapid adoption of connected devices for monitoring various

chronic diseases, and increasing demand for cost-effective medical

services are also propelling expansion in the global mHelath market.

Low Physician Density May Hinder mHealth Market’s Growth

Growing reluctance of physicians to move

over conventional methods, lack of regulations, concerns about data

security, and low density of skilled professionals are some of the major

challenges in the global mHealth market. Nonetheless, persistent demand

and rising prevalence of various lifestyle disorders is believed to

help industry players overcome these challenges in the near future.

About Us

Transparency Market Research is a

next-generation market intelligence provider, offering fact-based

solutions to business leaders, consultants, and strategy professionals.

Our reports are single-point solutions

for businesses to grow, evolve, and mature. Our real-time data

collection methods along with ability to track more than one million

high growth niche products are aligned with your aims. The detailed and

proprietary statistical models used by our analysts offer insights for

making right decision in the shortest span of time. For organizations

that require specific but comprehensive information we offer customized

solutions through adhoc reports. These requests are delivered with the

perfect combination of right sense of fact-oriented problem solving

methodologies and leveraging existing data repositories.

TMR believes that unison of solutions

for clients-specific problems with right methodology of research is the

key to help enterprises reach right decision.

Tags: EKG, mhealth, small cap stocks, stocks, tsx, tsx-v Posted in CardioComm Solutions | Comments Off on #Mhealth Market is Expected to Expand at a CAGR of 22.1% – SPONSOR: CardioComm Solutions $EKG.ca – $ATE.ca $TLT.ca $OGI.ca $ACST.ca $IPA.ca

Posted by AGORACOM-JC

at 10:47 AM on Monday, December 23rd, 2019

Spyder has two current Development Permits in Calgary, Alberta to build cannabis retail stores and has received the building permit for one of the two locations

The second building permit has been submitted and awaiting approval

Vaughan, Ontario–(December 23, 2019) – Spyder Cannabis Inc. (TSXV: SPDR) (“Spyder Cannabis” or the “Company“), an established Canadian cannabis accessory and an alternative to smoking retailer, provides an update to the corporate business development. Founded in 2014 Spyder is an established chain of three high-end alternative to smoking stores and two cannabis accessory stores in Ontario, with locations in Woodbridge, Scarborough, Burlington, Niagara Falls and Pickering. The Spyder brand is defined by its high-quality proprietary line of e-juice, liquids and exclusive retail deals, dispensed in uniquely designed stores creating the optimal customer experience. Spyder is building off this leading retail, distribution and branding platform by pursuing expansion into the legal cannabis market.

Spyder has two current Development Permits in Calgary, Alberta to

build cannabis retail stores and has received the building permit for

one of the two locations. The second building permit has been submitted

and awaiting approval.

Two weeks ago the government of Ontario announced it will abandon the

current lottery system for cannabis retail and move towards an open

licensing system beginning January 6, 2020. Store authorizations will be

issued starting in April, at the rate of 20 per month. Spyder will be

submitting applications on January 6, 2020 for some of the stores

currently operating. These stores are already built out and Spyder does

not expect major renovations will be required to conform to the Ontario

specifications for licenced stores.

Spyder is currently pursuing other locations in Ontario for aggressive expansion of its scalable retail platform.

The Company’s common shares will resume trading on the TSXV at market open on December 24, 2019

FOR ADDITIONAL INFORMATION, PLEASE CONTACT:

For more information, please contact:

Spyder Cannabis Inc. Dan Pelchovitz President & Chief Executive Officer Contact: Investor Relations Phone: 1-888-504-SPDR (1-888-504-7737) Email: [email protected]

Cautionary Statements

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

Certain statements contained in this press release constitute

forward-looking information. These statements relate to future events or

future performance. The use of any of the words “could”, “intend”,

“expect”, “believe”, “will”, “projected”, “estimated” and similar

expressions and statements relating to matters that are not historical

facts are intended to identify forward-looking information and are based

on the Company’s current belief or assumptions as to the outcome and

timing of such future events. Actual future results may differ

materially. In particular, this release contains forward-looking

information relating to the satisfaction of the closing conditions

contemplated under the Agreement. Various assumptions or factors are

typically applied in drawing conclusions or making the forecasts or

projections set out in forward-looking information. Those assumptions

and factors are based on information currently available to the Company.

Risk factors that could cause actual results or outcomes to differ

materially from the results expressed or implied by forward-looking

information include, among other things: the TSX Venture Exchange

declining to accept the transaction, the landlord not consenting to the

Lease Assignment, changes in tax laws, general economic and business

conditions; and changes in the regulatory regulation. The Company

cautions the reader that the above list of risk factors is not

exhaustive. The forward-looking information contained in this release is

made as of the date hereof and the Company is not obligated to update

or revise any forward-looking information, whether as a result of new

information, future events or otherwise, except as required by

applicable securities laws. Because of the risks, uncertainties and

assumptions contained herein, investors should not place undue reliance

on forward-looking information. The foregoing statements expressly

qualify any forward-looking information contained herein.

Posted by AGORACOM-JC

at 10:30 AM on Monday, December 23rd, 2019

SPONSOR: BetterU Education Corp.

aims to provide access to quality education from around the world.

The company plans to bridge the prevailing gap in the education and job

industry and enhance the lives of its prospective learners by developing

an integrated ecosystem. Click here for more information.

How Education Technology Has Evolved In 2010s

EdTech (or Education Technology) industry in India, according to a KPMG report, was worth about $247million and could reach $1.96 billion by 2021.

New Delhi:

When Byju Raveendran set up his company, Think & Learn, in 2011,

offering online lessons before launching his main app in 2015, he

wouldn’t have imagined that the decade would end with him becoming a

billionaire. Mr Byju, who developed an education app (Byju’s app )

that’s grown to a valuation of almost $6 billion in about seven years, joined the rarefied club after his company scored $150 million

(roughly Rs. 1,000 crores) in funding in in July this year. That deal,

according to Bloomberg, conferred a value of $5.7 billion (roughly Rs.

39,000 crores) on the company in which the founder owns more than 21

percent.

The business signed up more than 35 million of whom about 2.4 million

pay an annual fee of 10,000 to 12,000 rupees, helping it became

profitable in the year ending March 2019.

EdTech (or Education Technology) industry in India, according to a

2016 KPMG report, was worth about $247million and could reach $1.96

billion by 2021.

A survey done by Gradeup indicated that 70% of students would shift

to online learning if given access to live online classes. Of these,

over 80% cited ‘access to expert faculty’ as the primary reason.

‘A decade ago, EdTech industry did not even exist’

Beas Dev Ralhan, Co-Founder and CEO, Next Edcuation India, says the

industry is engaging latest technologies such as experiential learning

tools, Artificial Intelligence (AI) and Gamification of Learning which

are revolutionising the preparation strategies of students currently and

will continue to do so.

Mr Ralhan says the educational landscape of India has been

transformed by a series of developments in new-age pedagogies and their

popularity is expected to continue in the coming years.

“Conventional methods of education have mostly lost their appeal

among students who are now exploring new strategies to learn and prepare

for exams,” he added.

The increased mobile penetration in the country especially in rural

areas was a major breakthrough for the development of this industry.

“A decade ago, EdTech industry did not even exist. Getting

accessible, affordable and a quality education for students preparing

for competitive exams, especially, in Tier 2,3 cities was a big

challenge. This was the opportunity that Ed-tech industry resolved to

address. This also coincided with the increased mobile penetration in

the country especially in rural areas,” says Shobhit Bhatnagar, CEO and

Co-Founder, Gradeup.

‘Interactive and result-oriented’

Once the issue of accessibility was solved, the startups, which boomed in last one decade, concentrated on the delivery side.

“The preparation had to be effective and result-oriented, for which,

EdTech players introduced live online courses from some of India’s best

teachers through their platform. Classes are interactive, engaging and

allowed students the freedom and privacy to learn at their convenience

from the best. With a structured methodology and day-wise study plan,”

Mr Bhatnagar details how the industry evolved.

Shweta Sastri, Managing Director, Canadian International School,

Bangalore, says the penetration of internet-based smartphones and

gadgets is taking quality learning to students across geographies in

India.

The teacher connect

According to Ms Sastri, by using the internet or software tools,

students can create online groups that connect them in real time with

students and teachers.

“They can receive feedback from their teachers and share questions

and concerns about their lessons. Hence teachers need to integrate

technology seamlessly into the curriculum instead of viewing it as an

add-on,” she adds.

“Technology has become a crucial aspect of enabling learning and

empowering teachers with the usage of multiple tools to improve teaching

methodology. With the use of technology, learning and teaching not only

become more interactive and exciting, but also become personalized to

suit the needs of every individual student,” she said.

Classroom experience

The smart boards are gradually replacing the black-boards in the

classrooms wherein the teacher can bring the world inside a classroom,

which broadens the horizons of teaching and learning, says Niru Agarwal,

Trustee, Greenwood High International School.

“Through technology”, Ms Agarwal says “the teacher and students are

always connected which enhances their preparation strategies. Media

presentations are designed in a student-friendly manner, and which can

also be shared easily. Calendar applications help in creating a schedule

for the student, thereby making their goals achievable”.

“Experiential learning tools are being implemented in India in the

form of virtual labs and virtual and augmented reality tools. Virtual

and augmented reality creates immersive, real-life experiences in the

classroom through graphical simulations. On the other hand, virtual

labs help them conduct simulated experiments based on real-world

phenomena via a computer interface,” says Mr Ralhan.

The outcome

According to Zishaan Hayath, CEO and Founder, Toppr , efficient use

of tech in education has led to a reduction in the need for a human

advisor, improving affordability for the student.

“There are about 350 million school-going students in India, one of

the largest population in the world. Stronger implementation of AI and

ML have helped bring out truly adaptive and personalized platforms

addressing real learning needs. The main purpose of these assistive

technologies is to provide a more accessible and on-demand experience

for students that need immediate assistance with certain issues. Tech

tools and software have also allowed to streamline the educational

experience, improve accessibility and offer new resources to students,”

he adds.

However, psychologists and educationists are arguing the

implementation of large scale technological solutions in school

education needs detailed studies on how it’s affecting the cognitive

abilities of a student in the era of “digital natives”.

“In the era of ‘digital natives’, the role of technology in teaching

cannot be overlooked,” says Muhsina Lubaiba, a psychologist who works

among school children.

“As Prensky says,.. rapid dissemination of digital technology…

changed the way students think and process information, making it

difficult for them to excel academically using the outdated teaching

methods of the day. In other words, children raised in a digital,

media-saturated world, require a media-rich learning environment to hold

their attention,” she quoted Marc Prensky, the writer of the book

‘Digital Natives, Digital Immigrants’.

She also said the quality and efficiency of the educational apps available today is debatable.

“I’m of the opinion that, even if genuine and expert evaluated apps

are used by children, it is by no means a substitute for the classroom

teaching. The issue here is that the teachers need to be updated and

should find ways to engage these digital natives using technology, but

their role cannot be completely neglected,” she said.

Posted by AGORACOM-JC

at 8:36 AM on Monday, December 23rd, 2019

Closed a non-brokered private placement of 3,000,000 units at $0.07 per Unit for gross proceeds of $210,000

“Manufacturing Silicon (Si) samples for emerging Li-ion batteries opportunities identified during the latter part of 2019 required additional investments. This financing gives us the flexibility needed to accelerate our battery related R&D efforts in early 2020,†said Bernard Tourillon, President & CEO of HPQ Silicon.

“Manufacturing Silicon (Si) samples for emerging Li-ion batteries

opportunities identified during the latter part of 2019 required

additional investments. This financing gives us the flexibility needed

to accelerate our battery related R&D efforts in early 2020,†said Bernard Tourillon, President & CEO of HPQ Silicon. “Being

able to attract this level of unsolicited investor interest, during the

worst period of the year to raise hard cash funding, gives us great

confidence about 2020 as we strive to deliver the critical Silicon

material required by the surging Li-ion battery market in 2020 and

beyond.â€

Placement Terms: Each Unit is comprised of one (1) common share and

one (1) common share purchase warrant (“Warrant”) of the Company. Each

Warrant will entitle the Subscribers to purchase one common share of the

capital stock of the Company at an exercise price of $ 0.10 for a

period of 36 months from the date of closing of the placement. Each

share issued pursuant to the placement will have a mandatory four (4)

month and one (1) day holding period from the date of closing of the

placement. The Placement is subject to standard regulatory approvals.

In connection with the placement the Company will pay cash finder’s

fee of $15,358 to StephenAvenue Securities Inc. (“StephenAvenueâ€) of

Toronto, Ontario. The Company will also issue 219,400 warrants to

StephenAvenue. Any share purchased through the exercise of the warrants

has the mandatory four (4) month and one (1) day holding period from

the date of closing of the placement and each warrant gives

StephenAvenue the right to purchase one (1) common share at $0.10 for 36

months following the closing of the Placement.

Mrs. Noëlle Drapeau, HPQ Corporate Secretary and a Director has

subscribed for 100,000 Units. Following the completion of the Private

Placement, Mrs. Drapeau will beneficially own or exercise control or

direction over, directly or indirectly, 1,778,416 Common Shares,

representing approximately 0.77% of the issued and outstanding Common

Shares of the Company.

The participation of Mrs. Drapeau in the Private Placement

constitutes a “related party transaction” within the meaning of

Multilateral Instrument 61-101 Protection of Minority Security Holders

in Special Transactions (“MI 61-101”) and Policy 5.9 – Protection of

Minority Security Holders in Special Transactions of the Exchange. In

connection with this related party transaction, the Company is relying

on the formal valuation and minority approval exemptions of respectively

subsection 5.5(a) and 5.7(1)(a) of MI 61-101 as the fair market value

of the portion of the Private Placement subscribed by Mrs. Drapeau does

not exceed 25% of the Company’s market capitalization. The Board of

directors of the Company has approved the Private Placement, including

the participation of Mrs. Drapeau therein, with Mrs. Drapeau abstaining

with respect to his participation.

About Silicon

Silicon (Si) is one of today’s strategic materials needed to fulfil

the renewable energy revolution presently under way. Silicon does not

exist in its pure state; it must be extracted from quartz, one of the

most abundant minerals of the earth’s crust and other expensive raw

materials in a carbothermic process.

About HPQ Silicon

HPQ Silicon Resources Inc. (TSX-V: HPQ) is developing, with PyroGenesis Canada Inc.(TSX-V: PYR), a high-tech company that designs, develops, manufactures and commercializes plasma base processes, the innovative PUREVAPTM “Quartz Reduction Reactors†(QRR),

a truly 2.0 Carbothermic process (patent pending), which will permit

the One Step transformation of Quartz (SiO2) into High Purity Silicon

(Si) at prices that will propagate its considerable renewable energy

potential. The Gen3 PUREVAPTM QRR pilot plant that will validate the commercial potential of the process is scheduled to start during Q1 2020.

HPQ, working with PyroGenesis, is also developing a process that can take the High Purity Silicon (Si) made by the PUREVAPTM

and manufacture Nano-Structure Silicon powders for Next Gen Li-ion

batteries. Starting in Q1 2020, the plan is to validate our game

changing manufacturing approach using a modified Gen2 PUREVAPTM reactor to produce Nanoscale Structure Silicon (Si) powders samples for industry participants and research institutions’.

Concurrently, HPQ is also working with industry leader Apollon Solar to develop a manufacturing capability that uses the High Purity Silicon (Si) made with the PUREVAP™

to make Porous silicon wafers needed for solid-state Li-ion batteries.

The first Silicon wafer should be ready to be ship for testing to a

battery manufacture (under NDA) during Q1 2020.

Finally, with Apollon Solar, we are also looking into developing a

metallurgical pathway of producing Solar Grade Silicon Metal (SoG Si)

that will take full advantage of the PUREVAPTM QRR one-step production of Silicon (Si) material of 4N+ purity with low boron count (< 1 ppm).

All in all, HPQ focus is becoming the lowest cost producer of Silicon

(Si), High Purity Silicon (Si), Nano-Structure Silicon powders for Next

Gen Li-ion batteries, Porous Silicon Wafers for Solid states Li-ion

batteries, Porous Silicon Powders for Li-ion batteries and Solar Grade

Silicon Metal (SoG-Si).

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

Disclaimers: The Corporation’s interest in

developing the PUREVAP™ QRR and any projected capital or operating cost

savings associated with its development should not be construed as being

related to the establishing the economic viability or technical

feasibility of the Company’s Roncevaux Quartz Project, Matapedia Area,

in the Gaspe Region, Province of Quebec.

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward-looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Company’s current expectation and assumptions and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Company with respect to future events and are subject to certain risks

and uncertainties and other risks detailed from time-to-time in the

Company’s on-going filings with the security’s regulatory authorities,

which filings can be found at www.sedar.com. Actual results, events, and

performance may differ materially. Readers are cautioned not to place

undue reliance on these forward-looking statements. The Company

undertakes no obligation to publicly update or revise any

forward-looking statements either as a result of new information, future

events or otherwise, except as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services Provider

(as that term is defined in the policies of the TSX Venture Exchange)

accepts responsibility for the adequacy or accuracy of this release.

For further information contact Bernard J. Tourillon, Chairman, President and CEO Tel (514) 907-1011 Patrick Levasseur, Vice-President and COO Tel: (514) 262-9239 Email: [email protected]

Posted by AGORACOM-JC

at 4:51 PM on Friday, December 20th, 2019

SPONSOR: New Age Metals Inc.

The company owns one of North America’s largest primary platinum

group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral

Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an

additional 1,059,000 PdEq Ounces Inferred. Learn More.

Platinum Group Metals Shine

An incredible year in the palladium market continues to the end.

It could be an excellent time to start thinking about renaming the

Platinum Group Metals. After all, since 2016, the price action in

rhodium and palladium has left the namesake head of the group in the

dust. Platinum has been a laggard. The old title as “rich man’s gold” is as inappropriate from an investment perspective today as it is from a social one.

Meanwhile, the price action in platinum in 2019 was not that bad. The

platinum futures market looks like it will post a double-digit

percentage gain compared to its closing price at the end of 2018. If the

price action in the other members of the precious metals sector,

including gold, palladium, and rhodium, are harbingers of the future for

platinum, 2020 could turn out to be an exciting year for devotees of

the metal that has not lived up to its reputation as a rare precious and

industrial metal.

Meanwhile, the precious metals sector of the commodities market is

barreling into 2020 after a bullish run in 2019. The Aberdeen Standard

Physical Precious Metals Basket Shares ETF (NYSEARCA:GLTR)

holds long positions in gold, silver, platinum, and palladium bullion. A

diversified approach to the sector could be an excellent way to spread

risk going into the new decade that is just around the corner.

Rhodium is the star

In 2016, the price of rhodium fell to a low at $575 per ounce.

Rhodium is a byproduct of South African platinum output. The weakness in

the platinum price, which fell to the lowest level since 2003 in 2018

when the price reached $755.70 per ounce, caused a decline in south

African platinum production. Less platinum mining caused a deficit in

the rhodium market, which does not trade on the futures exchange. In the

physical market, the price of rhodium took off like a rocket ship.

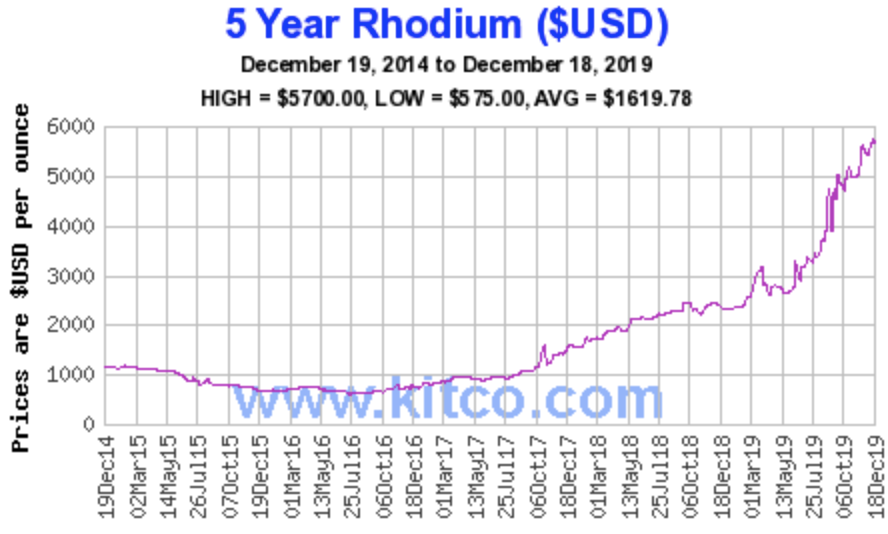

Source: Kitco

As the chart highlights, rhodium was trading at a midpoint value of

$5,840 per ounce on December 19, over ten times higher than the price in

2016. The deficit in the rhodium market could continue to push the

price higher in 2020, and a test of the all-time high at just over

$10,000 per ounce could be in the cards for the platinum group metal.

Rhodium has been the best performing PGM over the past years. In 2019

alone, the price more than doubled, moving from below the $2,500 level

at the end of 2018 to almost $6,000 per ounce on December 17.

An incredible year in the palladium market continues to the end

While rhodium is the metal with the most impressive percentage gain

since the 2016 low, the price action in palladium pushed the price of

the metal to a series of new all-time highs throughout 2019.

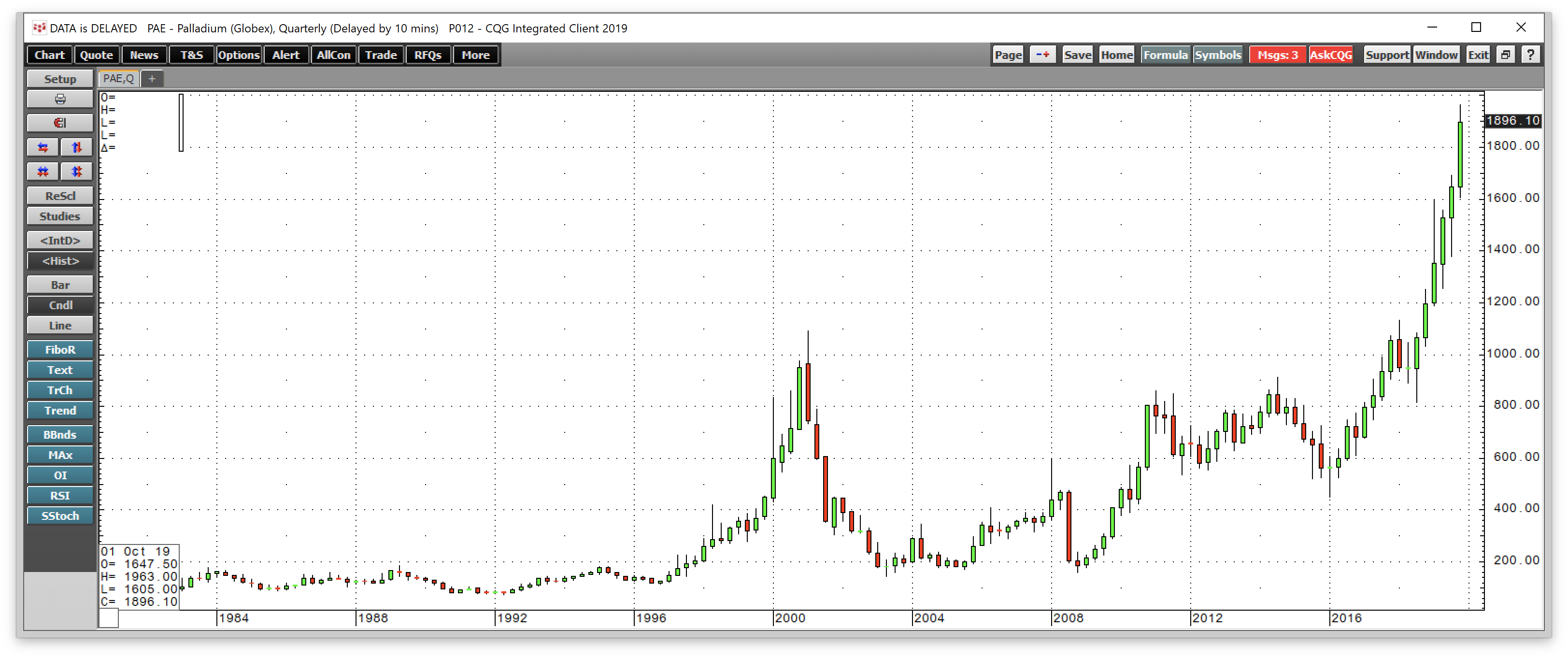

Source: CQG

The quarterly chart of nearby NYMEX palladium futures illustrates

that, before 2017, the all-time peak came in 2001 at $1,090 per ounce.

Palladium blew through that high like a hot knife goes through butter

and has posted gains in the past seven consecutive quarters. The price

was approaching the $2,000 per ounce level as of last week when it hit a

high at $1,974.60 on the active month March futures contract on

December 17.

The ascent of palladium is a function of the rising demand for catalytic converters for gasoline-powered automobiles. The “phase one”

trade deal between the US and China could stabilize the Chinese economy

lifting requirements for new cars and palladium-based catalytic

converters in the world’s most populous nation. On the supply side of

the fundamental equation for palladium, supplies come from South Africa

and Russia. In Russia, platinum group metals are a byproduct of nickel

output.

Platinum shows some signs of life

The price action in platinum has lagged rhodium and palladium over

the past years, and 2019 has been no exception. However, platinum looks

set to post a gain for the year that is coming to an end.

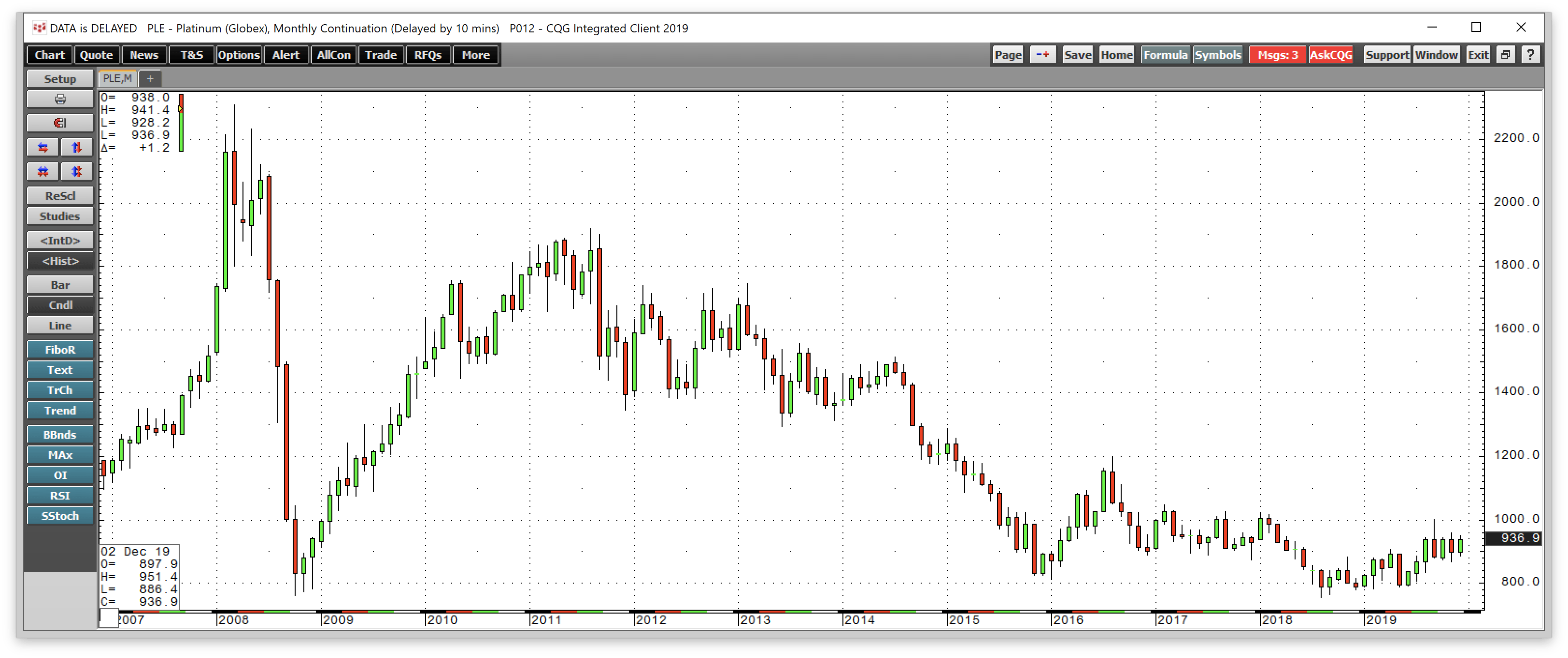

Source: CQG

The monthly chart shows that platinum closed 2018 at $788.50 and was

trading around the $937 level on December 19. Platinum looks set to

deliver a double-digit percentage gain as it was 18.8% higher than the

2018 closing price. However, its performance pales in comparison to the

palladium and rhodium markets.

Source: CQG

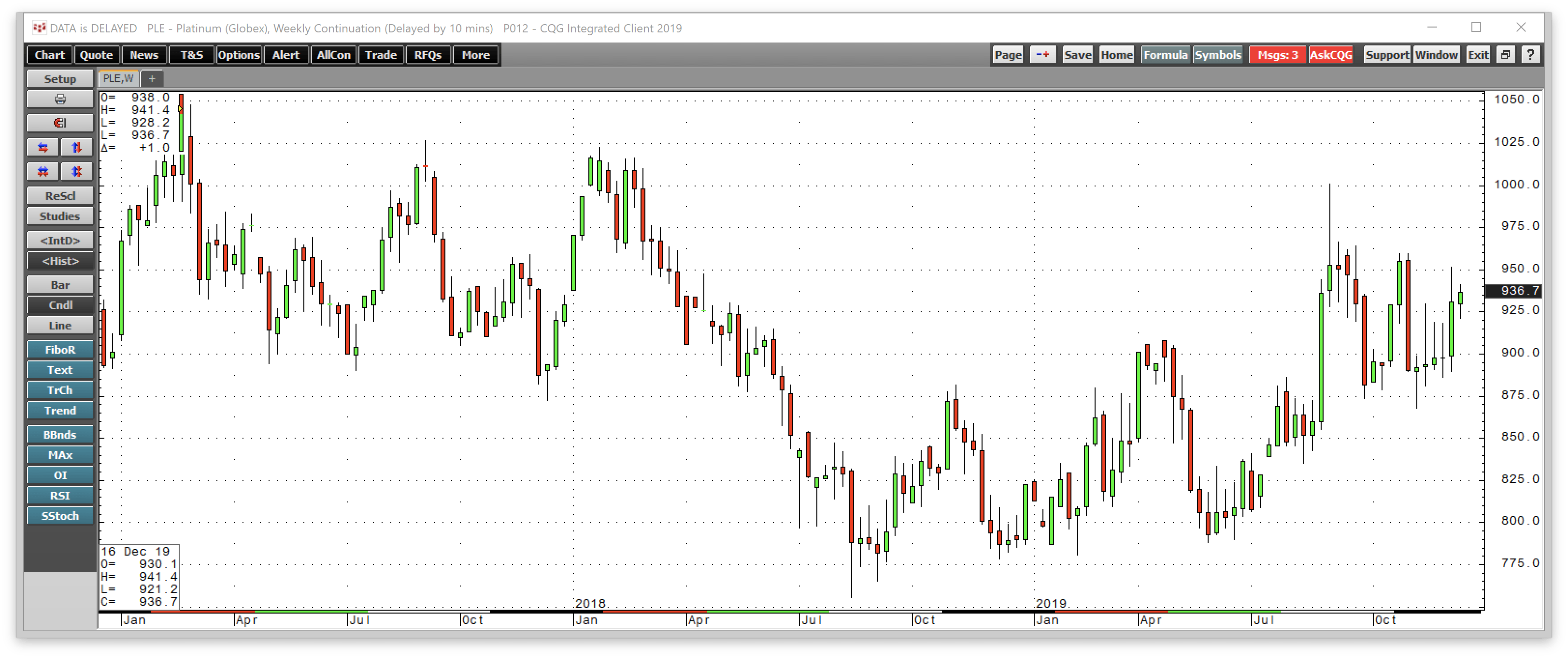

The weekly chart displays that platinum has made higher lows and

higher highs throughout 2019. The price range in the platinum market has

been from $787.30 and $1,000.80 on the continuous futures contract. At

$937 on December 19, the price of platinum around $43 above its midpoint

for the year. While platinum is not breaking any records, the price

action is going into 2020 in a bullish trend.

Industrial and precious metal

Platinum group metals have a myriad of industrial applications. Aside

from automobile catalytic converters, the dense metals with high

resistance to heat are required in oil and petrochemical refining,

fiberglass manufacturing, medical devices, and a host of other

applications. Of the three metals, platinum is the densest, with the

highest boiling and melting point. Therefore, platinum can serve as a

substitute for rhodium and palladium in industry.

Platinum also has a history as a financial asset and a store of

value. Since the 1970s, platinum had mostly traded at a premium to gold

as it is over ten times rarer than the yellow metal when it comes to

annual output.

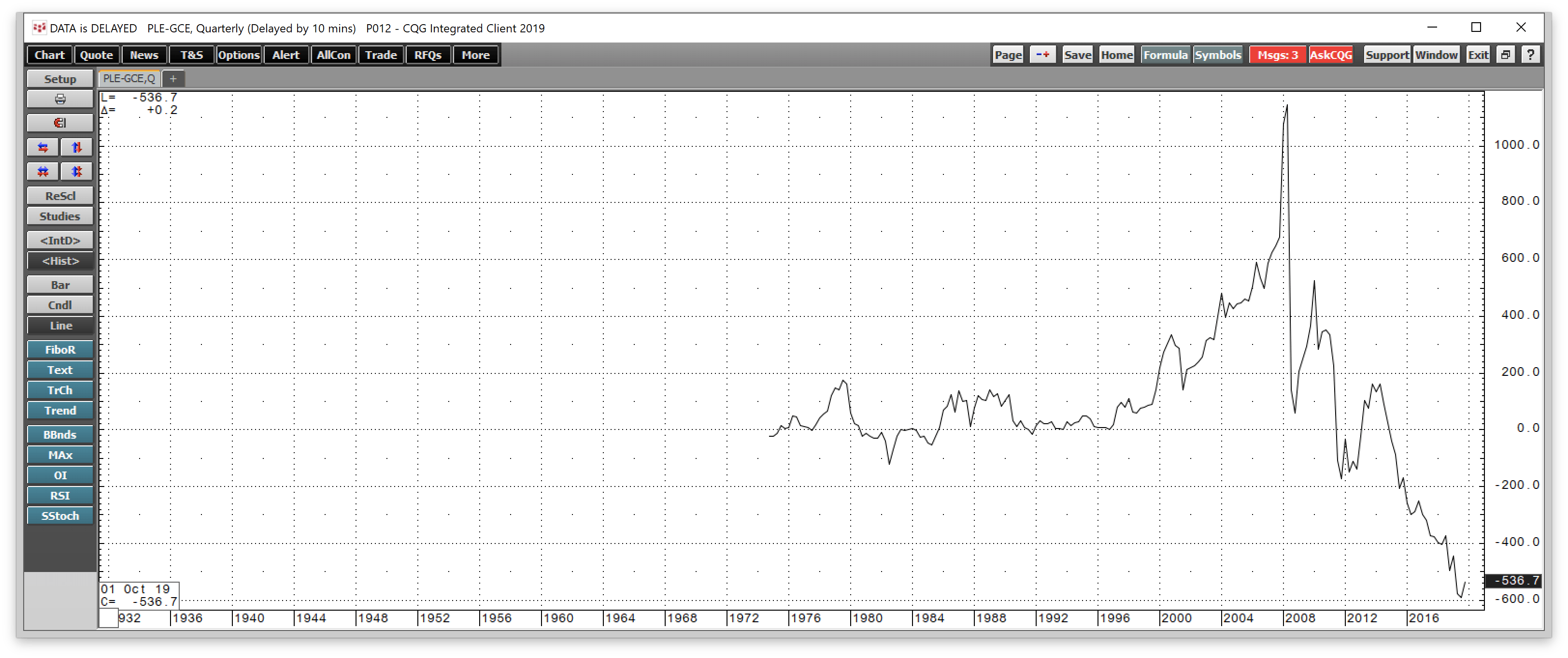

Source: CQG

The quarterly chart shows that platinum traded to an over $1,140

premium to gold in 2008, but it slipped to a discount in 2014 and never

looked back. After falling to a low at a $600 discount to gold in 2019,

platinum was still over $537 below the yellow metal on December 19.

Platinum moved almost 19% higher in 2019, gold broke out to the upside in June but slightly lagged platinum so far in 2019.

The GLTR ETF holds long positions in two of the three platinum group metals

Precious metals are going into the new decade on a bullish note after

posting across the board gains in 2019. The low level of global

interest rates could cause a continuation of bullish price action in

2020.

An ETF product that offers a diversified approach to a precious

metals investment is the Aberdeen Standard Physical Precious Metals

Basket Shares ETF. The fund summary for GLTR states:

“The investment seeks to reflect the performance of the price of

physical gold, silver, platinum and palladium in the proportions held by

the Trust, less the expenses of the Trust’s operations. The Shares are

designed for investors who want a cost-effective and convenient way to

invest in a basket of Bullion with minimal credit risk.“

Source: Yahoo Finance

The most recent top holdings of GLTR include:

Source: Yahoo Finance

GLTR has net assets of $463.08 million and trades an average of

22,754 shares each day. The ETF product charges an expense ratio of

0.60%.

Platinum continues to offer the most compelling value proposition in

the precious metals sector at around the $930 per ounce level. However,

the trend in all of the precious metals will enter 2020 in bullish mode.

The Hecht Commodity Report

is one of the most comprehensive commodities reports available today

from the #2 ranked author in both commodities and precious metals. My

weekly report covers the market movements of 20 different commodities

and provides bullish, bearish and neutral calls; directional trading

recommendations, and actionable ideas for traders. I just reworked the

report to make it very actionable!

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I

wrote this article myself, and it expresses my own opinions. I am not

receiving compensation for it (other than from Seeking Alpha). I have no

business relationship with any company whose stock is mentioned in this

article.

Posted by AGORACOM-JC

at 3:02 PM on Friday, December 20th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

BGL Metals Insider Says Nickel Forecasted to Shine

While stainless steel has historically been the primary end market for nickel, increased adoption of electrification in vehicle production is shifting demand for the material with advancements in battery technology

This structural shift is expected to change the supply and demand dynamics within the nickel market

CHICAGO and CLEVELAND, Dec. 18, 2019 –Â Technological advancements in the transportation industry are setting the stage for a surge in nickel demand, according to the Metals Insider, an industry report released by Brown Gibbons Lang & Company (BGL). While stainless steel has historically been the primary end market for nickel, increased adoption of electrification in vehicle production is shifting demand for the material with advancements in battery technology. This structural shift is expected to change the supply and demand dynamics within the nickel market.

Technological advancements in the transportation industry are setting

the stage for a surge in nickel demand, according to the Metals Insider,

an industry report released by Brown Gibbons Lang & Company (BGL).

While stainless steel has historically been the primary end market for

nickel, increased adoption of electrification in vehicle production is

shifting demand for the material with advancements in battery

technology.

Industry participants cite battery demand as a transformational

development for the nickel industry, with vehicle electrification and

global tightening of emissions standards key drivers underpinning market

growth:

Market forecasts quantify the shift to electric mobility, which

predict a nearly five-fold increase in electric vehicle (EV) models by

2030, when one in five passenger cars sold globally will be battery

electric vehicles. Government initiatives are driving EV growth, notably

stringent enforcement of emissions standards supported by targeted bans

on internal combustion engine vehicle sales.

Nickel consumption in EV batteries could expand ten-fold by 2025,

with battery demand projected to more than triple to an estimated 15

percent market share– up from 4 percent today.

Major nickel producers are validating the demand shift and investing

to support double-digit volume growth, with nickel integral to

strategic business models. Manufacturing capacity, raw materials

availability, and advancements in new battery technologies are critical

variables that will impact the supply outlook.

The nickel market is expected to undergo a structural shift across

the value chain that will impact supply demand dynamics for stainless

steel and nickel producers, distributors, manufacturers, and the major

end markets they serve, with the oil & gas, aerospace, and food

industries among the large consumers of the nickel- bearing material.

About Brown Gibbons Lang & Company Brown

Gibbons Lang & Company is a leading independent investment bank and

financial advisory firm focused on the global middle market. The firm

advises private and public corporations and private equity groups

on mergers and acquisitions, divestitures, capital markets, financial

restructurings, valuations and opinions, and other strategic

matters. BGL has investment banking offices in Chicago, Cleveland, and Philadelphia, and real estate offices in Chicago, Cleveland, Denver, San Antonio, and San Diego.

The firm is also a founding member of Global M&A Partners, enabling

BGL to service clients in more than 30 countries around the world.

Securities transactions are conducted through Brown, Gibbons, Lang &

Company Securities, Inc., an affiliate of Brown Gibbons Lang &

Company LLC and a registered broker-dealer and member of FINRA and SIPC. For more information, please visit www.bglco.com.

Posted by AGORACOM-JC

at 2:28 PM on Friday, December 20th, 2019

Spyder Cannabis Announces MOU with HighBreed Growth has Expired

Previously announced Memorandum of Understanding with HighBreed Growth Corp. has expired pursuant to its terms

Under the MOU signed on September 5, 2019, the parties intended to complete a business combination that would result in a reverse take-over of Spyder Cannabis by HGBGC

Company’s common shares will resume trading on the TSXV at market open on December 24, 2019

Vaughan, Ontario–(December 20, 2019) – Spyder Cannabis Inc. (TSXV: SPDR) (“Spyder Cannabis” or the “Company“), an established Canadian cannabis accessory and vape retailer, announces its previously announced Memorandum of Understanding (the “MOU“) with HighBreed Growth Corp. (“HBGC“) has expired pursuant to its terms. Under the MOU signed on September 5, 2019, the parties intended to complete a business combination that would result in a reverse take-over of Spyder Cannabis by HGBGC. Given that the transaction will no longer proceed, the Company does not, at the present time, intend to proceed with a delisting from the TSX Venture Exchange (the “TSXV“).

The Company’s common shares will resume trading on the TSXV at market open on December 24, 2019

About Spyder

Founded in 2014 Spyder is an established chain of three high-end vape

stores in Ontario, with stores located in Woodbridge, Scarborough and

Burlington. The Spyder brand is defined by its high-quality proprietary

line of e-juice, liquids and exclusive retail deals, dispensed in

uniquely designed stores creating the optimal customer experience.

Spyder is building off this leading retail, distribution and branding

eCig and vapes company and is pursuing expansion into the legal cannabis

market. Spyder has developed a scalable retail model with aggressive

expansion plan to create a significant retail footprint with targeted

and

FOR ADDITIONAL INFORMATION, PLEASE CONTACT:

For more information, please contact:

Spyder Cannabis Inc. Dan Pelchovitz President & Chief Executive Officer Contact: Investor Relations Phone: 1-888-504-SPDR (1-888-504-7737) Email: [email protected]

Cautionary Statements

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

Certain statements contained in this press release constitute

forward-looking information. These statements relate to future events or

future performance. The use of any of the words “could”, “intend”,

“expect”, “believe”, “will”, “projected”, “estimated” and similar

expressions and statements relating to matters that are not historical

facts are intended to identify forward-looking information and are based

on the Company’s current belief or assumptions as to the outcome and

timing of such future events. Actual future results may differ

materially. In particular, this release contains forward-looking

information relating to the satisfaction of the closing conditions

contemplated under the Agreement. Various assumptions or factors are

typically applied in drawing conclusions or making the forecasts or

projections set out in forward-looking information. Those assumptions

and factors are based on information currently available to the Company.

Risk factors that could cause actual results or outcomes to differ

materially from the results expressed or implied by forward-looking

information include, among other things: the TSX Venture Exchange

declining to accept the transaction, the landlord not consenting to the

Lease Assginment, changes in tax laws, general economic and business

conditions; and changes in the regulatory regulation. The Company

cautions the reader that the above list of risk factors is not

exhaustive. The forward-looking information contained in this release is

made as of the date hereof and the Company is not obligated to update

or revise any forward-looking information, whether as a result of new

information, future events or otherwise, except as required by

applicable securities laws. Because of the risks, uncertainties and

assumptions contained herein, investors should not place undue reliance

on forward-looking information. The foregoing statements expressly

qualify any forward-looking information contained herein.

Posted by AGORACOM-JC

at 12:00 PM on Friday, December 20th, 2019

SPONSOR:ThreeD Capital Inc. (IDK:CSE)

Led by legendary financier, Sheldon Inwentash, ThreeD is a

Canadian-based venture capital firm that only invests in best of breed

small-cap companies which are both defensible and mass scalable. More

than just lip service, Inwentash has financed many of Canada’s biggest

small-cap exits. Click Here For More Information.

How To Keep Your Crypto Safe Against Exchange Hackers

Exchange hacks appear to be one of the critical problems without any kind of a solution in sight.

This year alone, there have been several high-profile attacks.

Despite all the developments and innovations in the cryptocurrency

space over recent years, exchange hacks appear to be one of the

critical problems without any kind of a solution in sight. These days,

cryptocurrencies are far more distributed across hundreds of exchanges

than they were back in 2014 when Mt.Gox was hit, derailing the price of Bitcoin overnight. Nevertheless, exchanges remain prime targets for hackers.

This year alone, there have been several high-profile attacks.

Cryptopia was one of the first, subject two separate incidents that

ultimately crippled the New Zealand-based exchange, causing it to close

its doors for good.

After that, Singaporean DragonEx and

Korean Bithumb were both targeted, before trading behemoth Binance was

hit in May this year. Although the company was quick to reassure users

that their account balances were protected by its insurance fund, the

attack left a smear on Binance’s previously unblemished record of

security.

The latest exchange to fall prey to hackers is Upbit, which lost $50 million worth of ETH in late November.

So, what are crypto users to do, to

keep their funds safe? In light of the ongoing hacking issues, many

exchanges are now starting to sell themselves on their enhanced security

measures.

Going the Extra Mile to Prevent Attacks

For a while, two-factor

authentication was the established means of ensuring user account.

However, many exchanges are now taking additional measures, such as IP

binding. This means that you can restrict access to your exchange

accounts to only a single IP address. If someone attempts to log in from

another machine than your own, you’ll be notified.

Singaporean exchange ecxx

is one example of an exchange following this practice, along with other

measures to help keep your funds safe from theft. The exchange keeps

user funds in cold wallets, requiring multiple signatures from the

company to access.

Earlier this year, QuadrigaCX users found their funds had gone missing after the exchange founder died abroad

as the only person holding the private keys to access his company’s

wallet. Multi-signature wallets are a way of protecting against this

risk.

Furthermore, ecxx has integrated with MyInfo,

the government of Singapore’s user portal. It enables Singaporean

citizens and residents to interact with government agencies and private

companies online. The integration offers local users in Singapore a

trusted means of logging on to the ecxx platform with their existing

MyInfo credentials.

For institutions, ecxx has also partnered with Ledger,

one of the global leaders in digital asset cold storage. Professional

traders and investors can choose to have their funds stored in a Ledger

Vault, meaning that ecxx doesn’t take custody of funds at all.

Decentralized Exchanges – a Non-Custodial Solution

Another option for exchanging tokens

without incurring the security risks of hacking is to use a

decentralized exchange (DEX.) A DEX generally doesn’t take custody of

your accounts, meaning that you’re solely responsible for fund

security.

At this point in the evolution of

cryptocurrency, users have their pick of DEXs, with various different

models for enabling trading. However, a critical challenge of

peer-to-peer DEXs is that many are underused, meaning they suffer from

low liquidity. Unless you’re trading Bitcoin

or one of the major alts, you may find your trade left hanging while

the matching engine searches for a counterpart with whom to trade.

Therefore, it makes sense to find a DEX with high liquidity.

IDEX

is one of the more popular DEXs, meaning that liquidity is less of a

challenge. Users manage their funds via the platform’s Ethereum-based

smart contract. Users can access the smart contract via four methods – a

Metamask wallet, a Ledger Nano S cold storage wallet, a Keystore file,

or a manual private key entry.

Another safe option is to use a

liquidity protocol, which is a kind of DEX using a third token to enable

swaps between a wide variety of tokens. Bancor and Uniswap are both examples of liquidity protocols.

Wallets

If you do prefer to stick with

centralized exchanges, then conventional wisdom says that you should

only keep your funds in your exchange account when you’re actively

trading. Therefore, if you’re planning on keeping your investments in crypto, get yourself a wallet. Hot storage wallets such as Atomic or Edge are very easy to get started using only a smartphone app.

An even safer option for long-term

HODLers is to use a cold storage wallet such as a Ledger Nano S or

Trezor. Just make sure you have a safe method of storing your recovery

seed.