SPONSOR: New Age Metals Inc. The company owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces in the Inferred. Learn More.

———————

Supply And Demand Outlook Favors Palladium Vs. Platinum

- Palladium has outperformed platinum ever since the fundamentals of supply and demand have changed due to the diesel emissions scandal.

- The gap between platinum and palladium has shrunk in recent weeks, which would break the current trend of palladium outperforming platinum if it continues.

- Both the fundamental and technical pictures point to the trend staying in place relative to platinum and palladium despite the recent hiccup.

The biggest source of demand for platinum (PPLT) and palladium (PALL) is the automotive industry where emission standards are becoming increasingly stringent. These standards are driving demand for platinum and palladium due to their ability to help reduce harmful emissions. The result has been a sort of competition between the two of them.

However, the competition has become somewhat one-sided ever since the platinum market was rocked in 2015 by the emissions scandal or “Diesel Gate†involving Volkswagen (OTCPK:VWAGY). The reason is because platinum is heavily used in vehicles with diesel engines. On the other hand, palladium is associated with gasoline engines.

Cars powered by diesel engines have since fallen out of favor, and people are now turning towards cars powered by gasoline engines. This trend does not look to change anytime soon, but it’s set to continue for the foreseeable future. This is bullish for palladium and bearish for platinum. The result can be seen in the supply and demand equation for palladium and platinum.

The market for palladium has a deficit with a surplus for platinum

The emissions scandal has fundamentally altered the landscape for vehicles powered by diesel and gasoline engines and, by extension, platinum and palladium. The former is seeing demand decrease, and the latter is seeing demand increase as there is a shift away from diesel-powered cars towards gasoline-powered cars.

The two tables reveal that the platinum market has a surplus, with supply exceeding net demand. Except for industrial demand, every other segment, including autocatalyst, jewelry, and investment, is in decline. While supplies from mining have stayed roughly the same, platinum recycling is adding to the surplus of platinum in the market. The trend is clearly bearish for platinum.

| Platinum supply and demand (Unit: 1000 oz) | |||

| Supply | 2016 | 2017 | 2018 |

| South Africa | 4392 | 4449 | 4471 |

| Russia | 717 | 703 | 657 |

| Others | 988 | 953 | 980 |

| Total supply | 6097 | 6105 | 6108 |

| Demand | |||

| Autocatalyst | 3342 | 3218 | 3052 |

| Jewelry | 2412 | 2400 | 2363 |

| Industrial | 1806 | 2022 | 2321 |

| Investment | 620 | 361 | 89 |

| Total demand | 8180 | 8001 | 7825 |

| Recycling | -1934 | -2072 | -2215 |

| Net demand | 6246 | 5929 | 5610 |

| Surplus/deficit | -149 | 176 | 498 |

Source: Johnson Matthey

The opposite is true for palladium. Supply of palladium falls short of net demand and is driven primarily by the increased demand in the autocatalyst segment. Recycling has made more palladium available, but supplies have yet to eliminate the deficit in the market for palladium. Overall, the trend for palladium looks to be a lot better compared to platinum.

| Palladium supply and demand (Unit: 1000 oz) | |||

| Supply | 2016 | 2017 | 2018 |

| South Africa | 2570 | 2550 | 2590 |

| Russia | 2773 | 2406 | 2840 |

| Others | 1417 | 1405 | 1450 |

| Total supply | 6760 | 6361 | 6880 |

| Demand | |||

| Autocatalyst | 7951 | 8428 | 8655 |

| Jewelry | 191 | 173 | 166 |

| Industrial | 1875 | 1832 | 1855 |

| Investment | -646 | -386 | -555 |

| Total demand | 9371 | 10047 | 10121 |

| Recycling | -2491 | -2899 | -3212 |

| Net demand | 6880 | 7148 | 6909 |

| Surplus/deficit | -120 | -787 | -29 |

The forecast for 2019 calls for more of the same, assuming there are no unforeseen events that could disrupt the supply and demand equation. Platinum will have a surplus, and palladium, a deficit. The trend established in recent years as shown in the two tables is not expected to change. That is bullish for palladium, but bearish for platinum.

Divergence in prices for platinum and palladium

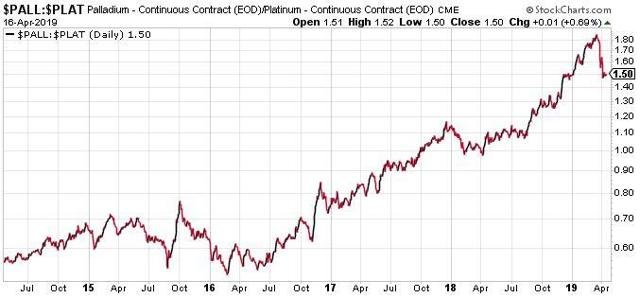

As a result of a favorable outlook, palladium prices have vastly outperformed platinum. While platinum used to command a much higher price than palladium, the roles have now been reversed, and palladium is now worth more. The chart below tracks the relationship between platinum and palladium prices.

Notice that at its peak in March, a troy ounce of palladium was worth almost two ounces of platinum. That ratio has now come down, and palladium is now worth 1.5 ounces of platinum. A significant change, but still far removed from the days when platinum was more expensive than palladium.

However, the fact remains that the gap between platinum and palladium has shrunk with platinum outperforming palladium during this time frame. The gap could continue to shrink, but it could also begin to widen as before. Which of the two is more likely to happen will depend on a few factors that should be taken into consideration.

Can platinum and palladium be substituted for one another in the manufacture of an autocatalyst?

The short answer is yes, but only to a certain extent. While platinum and palladium are more suitable and preferred in diesel and gasoline vehicles, respectively, it is not absolutely necessary. The more expensive palladium becomes relative to platinum, the more manufacturers may be inclined to look into replacing palladium with platinum in the manufacture of an autocatalyst. Not necessarily completely, but at least partially.

In theory, this should act as a cap on palladium relative to platinum. If the gap in prices between the two becomes too extreme, precious metal substitution could force the ratio between palladium and platinum to reverse and narrow. There would be less demand for palladium and demand for platinum would increase under these conditions. However, in practice, it is difficult to replace more expensive palladium with cheaper platinum.

The two precious metals are only needed in trace amounts, and the price difference would have to be very severe to make a noticeable difference in the final cost of a vehicle. It also takes a lot of time and expense to test that changes in precious metal composition in an autocatalyst meet desired specifications. In a nutshell, while it’s possible, it’s almost certainly not worth the trouble to replace platinum with palladium or vice versa.

Why gold prices affect platinum more than palladium

Unlike palladium, platinum prices are more prone to being influenced by the price of gold (GLD). The reason is because platinum is heavily used in jewelry, much more than palladium. Because of this, platinum is in direct competition with gold. In fact, people often have to decide which of the two, gold or platinum, they will select in a purchase.

People will more often than not pick gold, but they may be tempted to go for platinum if the former is much more expensive than the latter. Rising gold prices are, therefore, good for platinum because it makes platinum a more attractive substitute. But if gold prices fall, then there is less need for platinum because most people tend to prefer gold.

It’s, therefore, necessary that we look at gold when considering where platinum will go relative to palladium. The ratio between gold and platinum prices has changed recently as gold prices have gone down. A previous article discussing why gold is likely to face pressure can be found here.

The chart above tracks the relationship between platinum and gold prices. Notice that while an ounce of platinum was roughly equal to 60% of gold at its low, the ratio has gone up and is now at almost 70%. What this basically means is that platinum’s appeal as an alternative has declined versus gold. This should be seen as a negative for platinum demand, which could put downward pressure on the price of platinum.

Palladium looks to be priming itself for a big move

Palladium prices have been going sideways after a big drop from their recent highs. In fact, the chart pattern for palladium resembles that of a symmetrical triangle or a coil. If this technical analysis is correct, then a big move may be coming once consolidation is done. The triangle could resolve to the downside, but it’s more likely to continue the long-term trend, which is up.

Both the fundamental and technical pictures suggest that a move to the upside is the most probable outcome. In contrast, platinum is being held back by a number of issues as a previous article explains here. This would reverse the narrowing of the spread between platinum and palladium and, instead, widen the gap that exists.

The ratio between palladium and platinum has been stuck at around 1.5, as previous charts reveal. This ratio could decrease further, but the most likely path is for the ratio to resume its previous uptrend after the time it has spent consolidating. This would be consistent with the price of palladium outperforming that of platinum.

Palladium will outperform platinum

It’s important to mention that the long-term picture for platinum and palladium in terms of demand is not a good one. Recent research suggests that it will one day be possible to make an autocatalyst without the need for any precious metals such as platinum and palladium. If this happens, then both metals will be left without their biggest source of demand.

Furthermore, electrical vehicles are on the rise, and they do not emit the harmful emissions that platinum and palladium are tasked with reducing. The challenge for platinum and palladium will be to find new applications where they can be used. Otherwise, the future of platinum and palladium does not look all that bright.

Having said that, palladium is most likely to outperform platinum with both charts and supply and demand in its favor. There is still a shortage of palladium that the market will not be able to resolve in the short term. The supply deficit, combined with the recent consolidation in prices after a major correction, will most likely result in palladium rising again.

On the other hand, gold is under pressure, and it’s hard to see platinum doing well when gold is struggling. There is also a surplus of platinum that will not go away anytime soon. Therefore, barring a major supply disruption, such as a major strike that drastically reduces supplies, platinum is highly unlikely to do as well as palladium. Platinum may have outperformed palladium in recent weeks, but that should soon reverse.

Source: https://seekingalpha.com/article/4255191-supply-demand-outlook-favors-palladium-vs-platinum

Last modified: July 27, 2026