On Friday December 4th, Seabridge Gold (SEA) announced its intentions to purchase the Snowfield deposit from Pretium Resources (PVG), details here. As a result, we experienced a high volume of emails and calls as to how this may affect Treaty Creek. In our opinion, we think it’s a positive move for all three projects located in the Sulphurets Hydrothermal System. Our analysis of the transaction and the associated benefits is as follows:

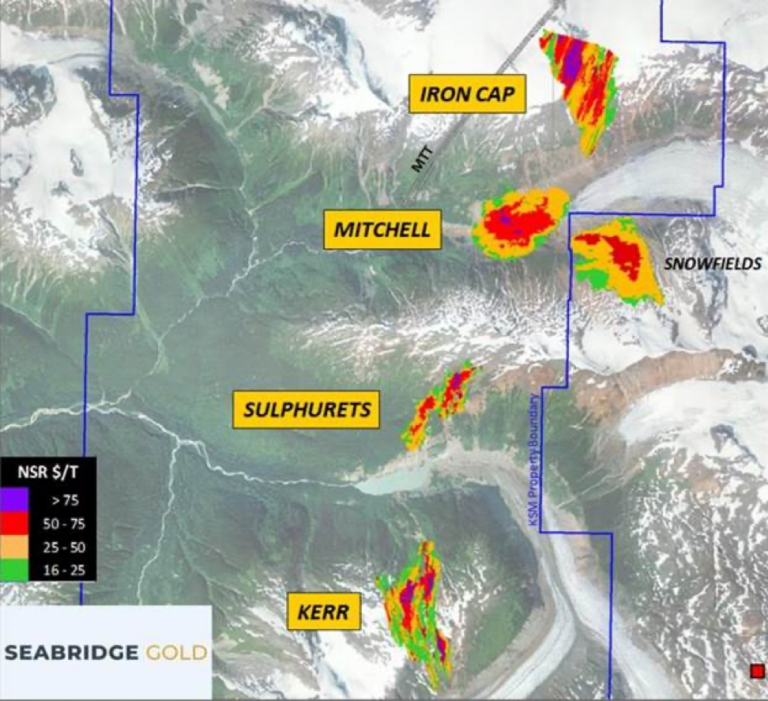

Below is an image created by Seabridge showing the KSM and Snowfield deposits and the relative gold grades/value of those deposits. Technically, the Snowfield is the top part of the Mitchell deposit, which it sits beside.

|

| On its own, the Snowfield added no present value to Pretium in the near term for a few reasons: The Snowfield has a very low-grade halo that on its own, at present gold values, isn’t profitable to produce. It has a higher-grade core but that core isn’t large enough to justify the costs to get it out at today’s gold price. Logistics. Because the Snowfield is located upslope above the Mitchell deposit in the Mitchell valley, mine construction would have been very difficult due to the terrain combined with the proximity to the Mitchell deposit located below owned by Seabridge. Access. Even if the gold grades were higher and there was room to develop the Snowfield on its own, there appears to be no feasible way to get the ore to market except through the proposed Mitchell Teigen Tunnels (MTT) which (if built) would be owned by Seabridge. The above, and perhaps some other reasons as well, is why the Snowfield deposit has been sitting there with no progression for many years, which in its present state added zero value to Pretium. It could be argued that a sale worth $3 USD per ounce in the ground is a lot better than $0 per ounce while it sits dormant. We think this was a great deal for PVG as they get: $100m up front in working capital $20m down the road A Net Smelter Royalty (NSR) of 1.5% down the road |

|

By combining the Snowfield with the KSM, SEA removed the “higher grade core isn’t big enough on its own” problem, the “no room” problem, and the “access” problem. We think this was a great deal for SEA as it helps them accomplish their goals:

- Improve their ounces/share ratio

- Improve the NPV and IRR on the KSM

- Allow them to defer underground operations until later in the production schedule

- Pay down the Cap-X for the KSM quicker

We think this a great deal for Treaty Creek (TC) shareholders (TUD, AMK, TUO) because anything that improves Seabridge’s chances of going into production is potentially beneficial to us:

- The only route for the KSM to go into production is through the use of the MTT which closely follows both the Kyba Line and the Sulphurets Thrust Fault through most of TC (this is the most heavily mineralized trend though TC including the Perfect Storm (PSZ), the Goldstorm (GS), and orpiment (GS2) zones as seen on the image above.

- If SEA is able to find a route through TC without disturbing potential deposits then it will build important infrastructure (bridge, roads, power, etc.) right onto TC.

- If SEA isn’t able to find a route through TC without disturbing potential deposits then SEA potentially will form an agreement with TC owners (benefiting TC shareholders) followed by building important infrastructure right onto TC.

- A second mine, especially one of this magnitude, going into production within the Sulphurets Hydrothermal System will undoubtedly capture the attention of investors and mining companies and shine a spotlight on the third project advancing in the same system; Treaty Creek.

The $3 USD per ounce paid for the Snowfield was a good deal for both companies and has no real bearing on potential insitu gold deposits and associated valuations at TC. It’s all a question of grade, logistics, and potential buyers. The Snowfield has low grade, horrible logistics (to be developed on its own) and potential for only one buyer (SEA). TC sits “on the right side of the mountain” only 20km away down a valley from the highway and the cheapest power in the world. The Goldstorm zone also has its highest gold grades right at surface (300 zone) over a very extended area opposed to dipping steeply into the ground. The logistics, and therefor potential Cap-X and Op-X, are completely different at TC vs both the Snowfield and the KSM.

In conclusion, we believe that the Snowfield purchase by Seabridge will positively impact every company located within the Sulphurets Hydrothermal System. We view this as another very positive development in the rapid progression of Treaty Creek’s development.

-Kelvin Burton

Last modified: July 13, 2026

as AI-Powered, Privacy‑First Ad Platform Reaches 500M+ Monthly Users")