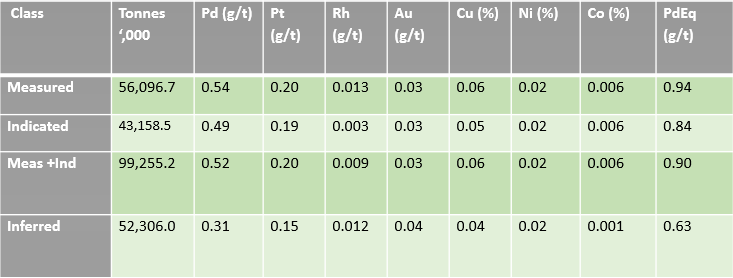

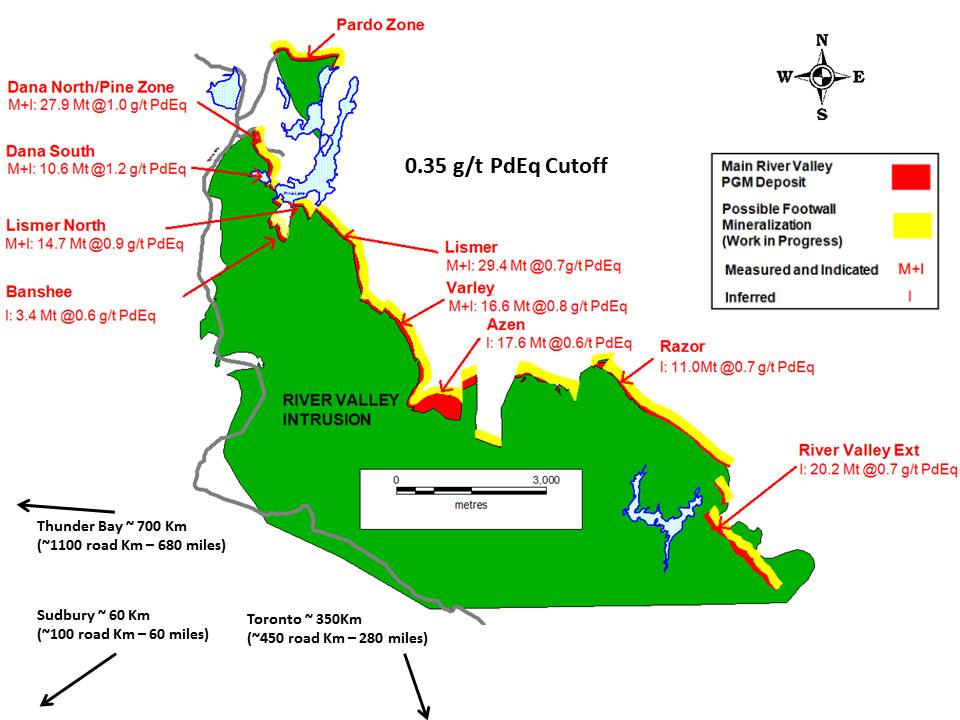

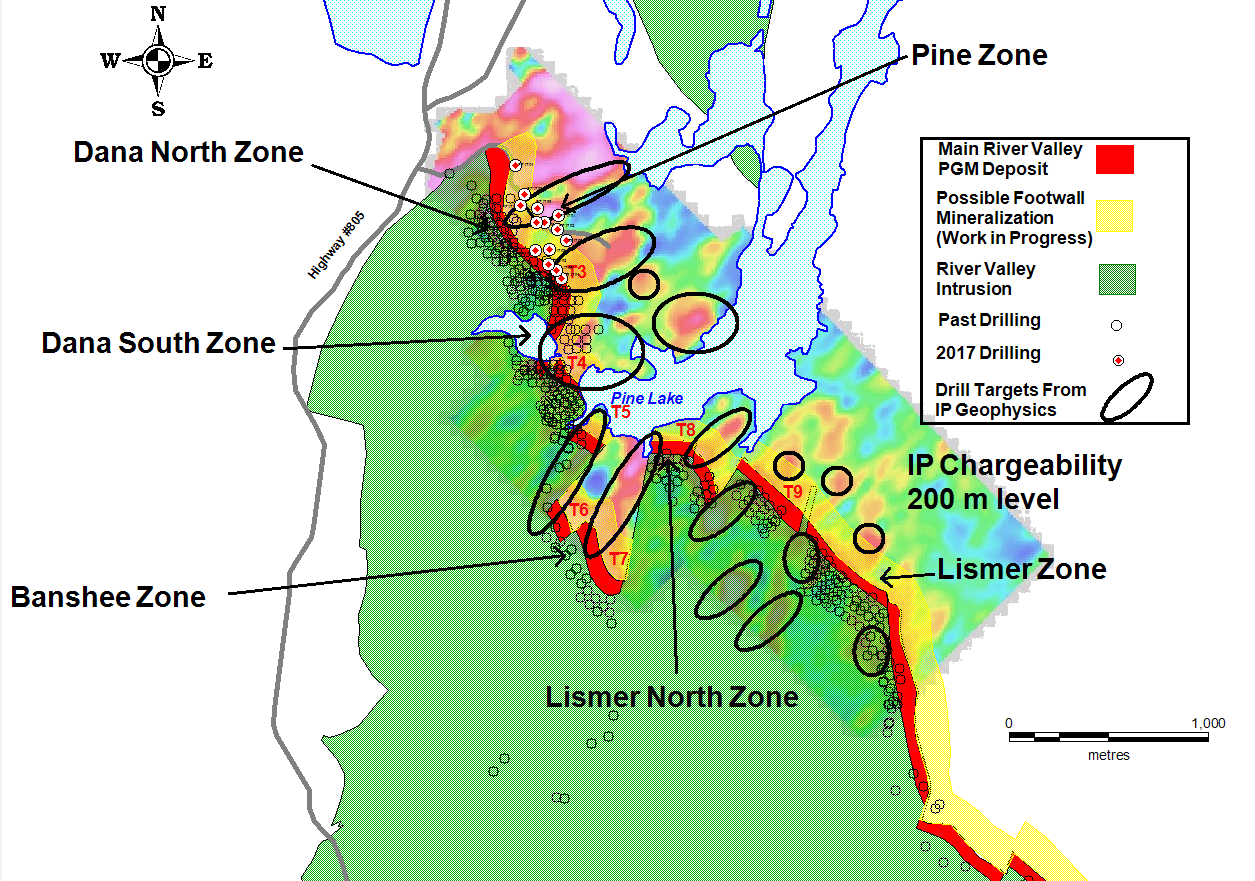

SPONSOR: New Age Metals Inc. (TSX-V: NAM) The company’s new Lithium Division has already made significant acquisitions in Canada and the USA. The company also owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Learn More.

———————

Huge demand for copper, cobalt, lithium and nickel in the offing as EV uptake increases

Purkiss’s presentation also emphasises an increasing amount of nickel content in lithium nickel manganese cobalt oxide (NMC) batteries, adding that nickel input primarily sourced from sulphides is a declining supply source.

By: Tracy Hancock

Creamer Media Senior Deputy Editor Contract Publishing and Sales

Investors focused on the mining sector may not fully appreciate how quickly the electric vehicle (EV) is being adopted globally, in light of the world pursuing a low-carbon emissions future, says battery metals investment vehicle Cobalt 27 Capital chairperson and CEO Anthony Milewski, who warns of a potential deficit in the supply of the metals critical to achieving this future.

Global management consultancy firm McKinsey & Company says 2017 marked the first time EV sales passed the one- million mark, noting in May 2018 that, by 2020, EV producers could be moving 4.5- million units, about 5% of the overall global light-vehicle market.

Also presenting at this year’s Mining Indaba was nickel-focused development vehicle Consolidated Nickel Mines (CNM) CEO Simon Purkiss, who provided an update on the restarting of the company’s Munali nickel mine, in southern Zambia.

Purkiss points to EV growth being an important factor in nickel’s demand-side development, noting a rapid increase in EV uptake, with financial services company Credit Suisse predicting EV growth to 3.1- million units by 2021 and 14.2-million units by 2025.

CNM identified Munali, where operations stopped in November 2011, owing to low nickel prices and poor operational performance by the previous owners, as key to its consolidation of nickel prospects in Southern Africa. Purkiss told delegates that financing of the restart was complete and, with the mine ramping up and the process plant being commissioned, first concentrates were expected in February and were on track to being transported to one of the nickel and copper smelters in the Southern Africa Development Community region in the first quarter of this year.

Purkiss says project economics were improved by changing the mining method, revising the metallurgical process and optimising the labour structure. Munali will produce low-cost nickel concentrate at $9 200/t of nickel, while, in the long term, CNM expects lower-cost nickel sulphate production of $5 000/t.

The company predicts global nickel stocks will decline until a trigger point is reached, at which time restocking will take place. Subsequently, says Purkiss, nickel prices will start rising, probably rapidly, and nickel pig iron production will restart, but only to fill Chinese stainless-steel demand, which will still be limited.

Purkiss’s presentation also emphasises an increasing amount of nickel content in lithium nickel manganese cobalt oxide (NMC) batteries, adding that nickel input primarily sourced from sulphides is a declining supply source.

Supporting his statement, a report on the lithium-ion battery market by Dublin-based market researcher Research & Markets foresees the market for NMC growing at a higher compound annual growth rate over 2018 to 2024.

EVs require high capacity and high power that can only be provided by using the NMC battery type, says the researcher. “The use of new electrolytes and additives support the charging of a cell up to 4.4 V/cell. The NMC cell is growing in its range as the three components involved are easy to blend together and can be made useful for a range of applications, from the automotive industry to energy storage systems.â€

The lithium-ion battery market is estimated to grow exponentially from $37.4-billion in 2018 to $92.2-billion by 2024. Research & Markets attributes the growth of the market not only to increased demand for plug-in vehicles but also to the growing need for automation and battery-operated materials- handling equipment, the increasing demand for smart devices and other industrial goods, and the high requirement of lithium-ion batteries for various industrial applications.

“However, factors such as safety issues related to storage and the transport of spent batteries hinder the market growth,†adds Research and Markets.

Nonetheless, Milewski is adamant that the level of activity in the EV battery metals space is only the ‘tip of the iceberg’, with the broader uptake of EVs yet to be fully realised.

He says demand for cobalt really depends on EV penetration. A material increase in the production of cobalt, a by-product of copper and nickel mining, is foreseen once demand for the metal more than doubles when EVs account for 15% of the world’s car sales.

“Cobalt 27, which owns the world’s largest private stockpile of physical cobalt, is positioned to take advantage of the early stages of the battery metals upcycle, where large- scale base metals producers are actively seeking to leverage by-product metals, such as cobalt, to fund mine expansion and repay debt using alternative, nondilutive sources of capital,†he tells Mining Weekly.

Officially, 105 000 t of cobalt is supplied globally, but Milewski says the unofficial figure is closer to between 115 000 t and 125 000 t of cobalt. This discrepancy, he says, is due to production being skewed by supply from undocumented artisanal mining in the Democratic Republic of Congo (DRC), where as much as 70% to 75% of the world’s cobalt is produced.

The balance of the globe’s cobalt supply is derived as a by-product of nickel mining in Australia, Canada, Cuba and Russia, along with the only existing cobalt mine in the world, in Morocco. Owned by private-equity industrial and financial group Omnium Nord Africain subsidiary Compagnie de Tifnout Tiranimine, the Bouazar cobalt deposit, about 34 km from Taznakht, in the Ouarzazate governorate, is said to produce 2 000 t/y of cobalt.

“With 98% of global cobalt supply a relatively small by-product of nickel and copper mining, one of Cobalt 27’s core principles is to invest in geopolitically stable jurisdictions outside the DRC. We believe the primary issue facing cobalt supply is the major concentration of cobalt reserves and production in the DRC, and the underlying human rights, environmental issues and political uncertainty associated with the country,†he adds.

The ethical sourcing of cobalt from the DRC continues to challenge the sector’s supply chain, with Milewski highlighting the significant challenges faced by industry participants in their attempts to promote the adoption of solutions that may be highly impractical in terms of the DRC business environment. Although, he adds, not all artisanal mining is bad, addressing the operations that are unethical will take years and large amounts of money.

A second challenge artisanal mining poses to the growth of the EV market involves the environmentally unfriendly mining methods practised, contradicting the intentions of early EV adopters: people concerned about the environment. However, other metals, such as lithium, whose mining process is highly reliant on water, also face challenges. “Each commodity has its own set of particular challenges,†adds Milewski.

Supply and Demand

As the electrification story unfolds, in 2025 and beyond, this sector could account for between 13% and 15% of the current copper market. “This is a massive demand, relative to the size of the copper market. Electrification is the much bigger story, as batteries will make energy much more accessible, but the type of battery used is dependent on the application and metals available to specific countries,†notes Milewski.

Market research specialist BMI Research last year forecast global copper output to climb from 23.4-million tonnes in 2018 to 29.9-million tonnes by 2027, averaging yearly growth of 2.7%. The global refined copper balance was also forecast to register a deficit of 251 000 t in 2018 and remain undersupplied through 2023.

In terms of nickel, BMI Research expects global yearly production to reach 2.9-million tonnes by 2027, according to its ‘Strategic Metals and Rare Earths Market Outlook – Q32018’ report.

Milewski says the size of the copper and nickel markets will continue to dwarf that of cobalt, predicting greater focus on investment and development around these metals.

However, he sees a lag in satisfying the need for these “future metals†and building the mines required to fulfil that need.

The issue is not whether there are enough of these metals in the ground, but whether funding is being made available to miners for the development of the operations necessary to meet future demand. Other than diversified miner Rio Tinto or Australian mining giant BHP, “I can’t think of any other mining company that has developed a mine recently for over $2-billionâ€, states Milewski.

Noting that capital markets are generally efficient, he says directors can make their mining projects look as attractive as possible, but “if the markets are closed, they are closedâ€. Higher commodity prices could, however, spur investment in the cobalt, copper, lithium and nickel markets, Milewski adds.

Sadly, with two-thirds of the world’s cobalt originating from copper mining in the DRC, where cobalt was declared a strategic metal last year, a supply surge from the country has resulted in a price slump. Subsequently, some major miners, such as Glencore, have implemented cost-cutting procedures to compensate for the two-year low. At its Mutanda mine, Glencore has retrenched workers and decided against renewing contracts with external contractors.

In February, diversified natural resources producer Eurasian Resources Group (ERG) also stopped production at a copper and cobalt mine in the DRC, as it considers future investment in new production methods.

The suspension at ERG’s Boss Mining comes at a time of strained relations between the DRC and investors after the nation last year introduced a 10% levy on cobalt exports, owing to cobalt’s strategic metal status.

Future metals have the attention of investors, as they primarily impact the low-carbon future and awareness is growing among mining companies of the benefit of aligning with the delivery of a low-carbon emissions future, with Glencore, for example, over the last year having adjusted its marketing message, says Milewski.

“Where mining companies are able to raise money presently is in this space,†he explains, adding that Rio Tinto is also looking into low-carbon-emission-metals- related projects.

Copper, cobalt, lithium and nickel are the core metals that will be impacted on by the pursuit of the world’s low-carbon-emissions future and whether other metals will join the story, only time will tell. Besides these mainstream metals, Milewski highlights interest in graphene, vanadium and certain zinc chemistries. “These metals are sitting on the sidelines and only time will tell if the technology will develop to grow their demand,†he concludes.

Even with South Africa’s electricity supply woes, automotive company Jaguar Land Rover South Africa forecast in January that South Africa could have 145 000 EVs on its roads, expecting yearly sales of new EVs to reach 43 000 units in the next six years.

The company based its prediction on the uptake of EVs locally matching the global average, which it says will account for up to 11% of all new-car sales in 2025.

“Actual EV car sales have far outpaced expectations and are going to have a tremendous impact on the demand for materials such as copper, cobalt, lithium and nickel,†says Milewski. Having recently spoken at the Investing in African Mining Indaba conference, which was held at the Cape Town International Convention Centre, in South Africa’s Western Cape, from February 4 to 7, Milewski highlights that most conversations at the event were around these metals.

Source: http://www.miningweekly.com/article/huge-demand-for-copper-cobalt-lithium-and-nickel-in-the-offing-as-ev-uptake-increases-2019-03-15/rep_id:3650