Posted by AGORACOM

at 9:18 AM on Tuesday, May 12th, 2020

Cardston, Alberta–(Newsfile Corp. – May 12, 2020) – American Creek Resources Ltd. (TSXV: AMK) (“the Corporation”) (“American Creek”) today announced that it has executed an agreement with Tudor Gold Corp. (“Tudor”) whereby Tudor is buying out the Corporation’s 40% interest in the Electrum Project Joint Venture located near Stewart, British Columbia.

Tudor will pay American Creek $250,000 cash and issue 1,400,000 Tudor shares upon the transaction closing. The shares are subject to a standard four month hold period and a voluntary eight month hold as well.

This transaction is subject to approval by the TSX Venture Exchange.

Darren Blaney, American Creek CEO stated: “We think this transaction makes sense for American Creek and its shareholders as we are trading a minority interest in the Electrum property for non-dilutive operating cash as well as a substantial share position in Tudor which gives us more exposure to the upcoming Treaty Creek developments which we believe will be very significant.”

About American Creek

American Creek holds a strong portfolio of gold and silver properties in British Columbia.

Three of those properties are located in the prolific “Golden Triangle”; the Treaty Creek and Electrum joint venture projects with Tudor (Walter Storm) as well as the 100% owned past producing Dunwell Mine.

The Corporation also holds the Gold Hill, Austruck-Bonanza, Ample Goldmax, Silver Side, and Glitter King properties located in other prospective areas of the province.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com

Posted by AGORACOM

at 11:05 AM on Monday, May 11th, 2020

The length of the northeast axis of the Goldstorm System is over 850 meters

The Southeast axis is at least 600m

The system remains open in both dimensions, as well as to depth.

The strongest mineralization encountered to date is from two consecutive 150m step-out holes at the northeast end of the drill grid: GS-19-42 yielded0.849 g/t Au Eq over 780 m with the 300 Horizon averaging 1.275 g/t Au Eq over 370.5m and GS-19-47 yielded 0.697 g/t Au Eq over 1,081.5m with the 300 Horizon averaging 0.867 g/t Au Eq over 301.5m.

Program focused on expanding the mineralized area from these two very encouraging step-out holes.

Furthermore, we plan to continue advancing along the NE axis with yet another 150 meter step out hole. The best results from the southeast dimension came from GS-19-52 which yielded 0.783 g/t Au Eq over 601.5m with 1.062 g/t Au Eq over 336.0m within the 300 Horizon.“

Cardston, Alberta–(Newsfile Corp. – May 11, 2020) – American Creek Resources Ltd. (TSXV: AMK) (“the Corporation”) is pleased to report that its JV partner Tudor Gold Corp has begun this season’s diamond drill hole program at its flagship property, Treaty Creek, located in the heart of the Golden Triangle of Northwestern British Columbia. Diamond drilling has begun with two drill rigs on the Goldstorm Zone which is on-trend from Seabridges’ KMS Project located just five kilometers to the southwest. These first two drills have begun drilling the initial holes of the 20,000 meter exploration program.

Tudor Gold’s Vice President of Project Development, Ken Konkin, P.Geo., states: “We are very proud of the hard work and dedication that our crews exhibited during the weeks prior to the start of drilling. Due to their diligence in preparing the camp we have been able to start our drill program a month earlier than last year’s program. The priority is to continue to expand the Goldstorm System to the southeast and to the northeast.”

“The current known length of the northeast axis of the Goldstorm System is over 850 meters, and the southeast axis is at least 600 m; the system remains open in both dimensions, as well as to depth. The strongest mineralization encountered to date is from two consecutive 150m step-out holes at the northeast end of the drill grid: GS-19-42 yielded0.849 g/t Au Eq over 780 m with the 300 Horizon averaging 1.275 g/t Au Eq over 370.5m and GS-19-47 yielded 0.697 g/t Au Eq over 1,081.5m with the 300 Horizon averaging 0.867 g/t Au Eq over 301.5m. Our program will be focused on expanding the mineralized area from these two very encouraging step-out holes. Furthermore, we plan to continue advancing along the NE axis with yet another 150 meter step out hole. The best results from the southeast dimension came from GS-19-52 which yielded 0.783 g/t Au Eq over 601.5m with 1.062 g/t Au Eq over 336.0m within the 300 Horizon.“

(The above results were from Tudors news release dated March 3rd, 2020,, in which the following metal prices were used to calculate the Au Eq metal content: Gold $1322/oz, Ag: $15.91/oz, Cu: $2.86/lb. Calculations used the formula Au Eq g/t = (Au g/t) + (Ag g/t x 0.012) + (Cu% x 1.4835). All metals are reported in USD and calculations do not consider metal recoveries. True widths have not been determined as the mineralized body remains open in all directions. Further drilling is required to determine the mineralized body orientation and true widths.)

Tudor Gold and its associated service companies have taken extreme measures to maintain the highest professional standards while working under COVID-19 health and safety protocols. Only essential personnel are permitted to enter the camp and staging areas. An on-site certified paramedic conducts strict daily monitoring of temperatures and general health conditions of personnel and service providers who are working at the project site and the staging area.

Walter Storm, Tudor President and CEO, stated: “I am very pleased with the safe start-up of the 2020 exploration program thanks to the hard work and dedication of our crews. The Company’s intent is to advance the Treaty Creek Project with full recognition and confidence in the recommended COVID-19 safety protocols. The goal for this year is to complete enough drilling that we can begin to delineate a first resource estimation at Treaty Creek.”

Darren Blaney, American Creek President and CEO stated: “2019 was a very successful year at Treaty Creek and this year looks to be far better with an extension of the drilling season and a drill program that is over twice as big as last years. With the recent announcement of working towards a resource calculation along with baseline studies and metallurgical work for an initial economic assessment, Mr Storm was right in calling this a transformational year at Treaty Creek.”

Qualified Person

The Qualified Person for this news release for the purposes of National Instrument 43-101 is the Company‘s Vice President of Project Development, Ken Konkin, P.Geo. He has read and approved the scientific and technical information that forms the basis for the disclosure contained in this news release.

Treaty Creek JV Partnership

The Treaty Creek Project is a Joint Venture with Tudor Gold owning 3/5th and acting as operator. American Creek and Teuton Resources each have a 1/5th interest in the project creating a 3:1 ownership relationship between Tudor Gold and American Creek. American Creek and Teuton are both fully carried until such time as a Production Notice is issued, at which time they are required to contribute their respective 20% share of development costs. Until such time, Tudor is required to fund all exploration and development costs while both American Creek and Teuton have “free rides”.

Treaty Creek Background

The Treaty Creek Project lies in the same hydrothermal system as Pretium’s Brucejack mine and Seabridge’s KSM deposits with far better logistics.

American Creek is a Canadian junior mineral exploration company with a strong portfolio of gold and silver properties in British Columbia. Three of those properties are located in the prolific “Golden Triangle”; the Treaty Creek and Electrum joint venture projects with Tudor Gold/Walter Storm as well as the 100% owned past producing Dunwell Mine.

The Corporation also holds the Gold Hill, Austruck-Bonanza, Ample Goldmax, Silver Side, and Glitter King properties located in other prospective areas of the province.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com

Posted by AGORACOM

at 9:54 AM on Tuesday, April 28th, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged 0.683 g/t Au over 780m in a vertical intercept. 2020 drilling plans 18,000 to 20,000 metres from 7-10 drill platforms with four diamond drill rigs. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits and is fully funded for exploration in 2020. Click Here For More Info

COVID-19: The Pin that Punctured the Credit Balloon

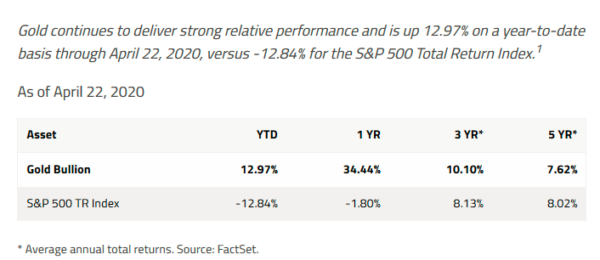

Gold is on the cusp of breaking out to all-time highs in U.S. dollars and has already done so in virtually every other currency. Gold mining stocks continue to lag the metal and, in our opinion, represent a compelling investment opportunity at this moment. The COVID-19 pandemic panic was merely the black swan that punctured a financial market asset bubble that took almost a decade to inflate.

Think of the pandemic as the pin that punctured the credit balloon. In a few months, the pandemic will ease (hopefully) with the formulation of a COVID-19 vaccine, widespread testing and other responses that will surely come from the healthcare industry. However, the fiscal and monetary policy damage committed by all governments to save the world has created a debt hangover that will linger for years. Economic growth will rebound but only to subpar levels once extreme health-related restrictions are lifted and “stimulus†kicks in.

The requisites for robust economic growth most likely to misfire are investment confidence and bank lending. Both have been severely compromised. Whether this landscape evolves into a long stretch of deflation or combusts into untamed inflation remains to be seen. What seems quite apparent is that traditional Keynesian stimulus measures are in their endgame. They will most likely deliver only steadily diminishing returns. Starkly opposite economic outcomes are possible from this policy morass; both would be positive for gold but negative for real returns on fixed income or equities.

Q1 Marks a Pivotal Turning Point for All Asset Classes

As of this writing, gold is trading about 10% less than its all-time high of US$1,900 attained nine years ago (September 2011). In effect, it has gone nowhere for a decade despite a tectonic shift in the investment and economic outlook. A lengthy correction lasting until 2016 and subsequent churning resulted in the establishment of a powerful multi-year basing structure. From this base and with strong macroeconomic tailwinds, we believe new highs well above $1,900 can be achieved over the next four years.

Despite enthusiastic advocacy and much chatter from investment luminaries, including Ray Dalio, Jeff Gundlach, Seth Klarman and others, gold remains severely and inappropriately underrepresented in the portfolios of fiduciaries, endowments and family offices. Flows into channels such as gold-backed exchange traded funds (“ETFsâ€) have been strong relative to previous low levels, but must still be considered a trickle in terms of what could still come.

Figure 1. Gold-Backed ETFs Reach Record Levels Global gold-backed ETFs added 298 tonnes and net inflows of US$23 billion in Q1 2020 — the highest quarterly amount ever in absolute U.S. dollar terms and the largest tonnage additions since 2016. Source: World Gold Council. Data as of 3/31/2020.

In our opinion, the first quarter of 2020 will mark a pivotal, secular turning point for all major asset classes including equities, bonds, gold and currencies. A return to the pre-2020 financial market normalcy and investment complacency is unlikely. In our view, consensus hopes remain high that the credit smash is only a temporary repercussion of the health scare. We disagree and suggest the effects will be long lasting.

Despite the solid price gains achieved by gold in the past two years, there is much more upside to come as investors gradually give up on repeated equity market bottom fishing and the hope of a return to financial market normalcy. A full reversal to the previous complacency cannot take place following a brief crash. The mood change will more likely become pervasive after grueling stretches of disappointing returns from previously successful investment strategies.

Unprecedented Central Bank Monetary Expansion

In our view, the decade preceding 2020 was characterized by the systematic stifling of price discovery for interest rates and the appropriate dependent valuations for financial assets. Such distortion was made possible only by unprecedented central bank balance sheet expansion that encouraged, abetted and rewarded risk taking in the form of ever greater leverage.

The prolonged somnolence of gold was among the most egregious price distortions of the previous decade and this suppressed interest in the metal as a risk mitigator and portfolio diversifier. Disinterest was fed in large part by the nearly universal expectation that the past would always be prologue and that highly leveraged financial and economic structures would perpetually result in outsized returns. In our view, the greatest change stemming from the credit bust will be a mood shift or paradigm change in the opposite direction.

At gold’s previous peak in 2011, the combined balance sheets of the U.S. Federal Reserve (“U.S. Fedâ€) and the European Central Bank (“ECBâ€) totaled approximately US$5.5 trillion. Today, that number is more than $11.4 trillion and rapidly moving higher. The USD gold price is still lower than nine years ago. In our view, gold price is still well below where it should be and will likely trade higher in the new macro landscape.

Figure 2. Pandemic Policy Response Pushes Global Balance Sheets to Record Levels Source: Bloomberg. Data as of 3/31/2020.

Gold Mining Stocks are Inexpensive

If gold is not correctly priced for what has transpired and what lies ahead, gold mining stocks are even more inappropriately priced. Based on current metal prices, most companies are generating positive earnings and cash flow and in many cases, free cash flow that can be applied to higher dividend payouts. Compared to other sectors of the economy, the gold mining industry stands almost alone in looking forward to strong 2020 earnings and a positive outlook for 2021.

2020 free cash flow yields for large-cap producers range from 3%-7% and 6%-25% for intermediate producers based on conventional sell-side research. The stats are similar or better for 2021 based on spot gold prices. As Figure 3. shows, mining stocks are inexpensive in absolute terms and have never been so cheap relative to the gold price.

Figure 3. Gold Equities Are Undervalued Relative to Bullion Ratio of XAU Index to Spot Gold (12/23/1983-3/31/2020) Data as of 3/31/2020. Source: Bloomberg. 12/23/1983 represents the inception of the XAU.

Since 2008, the relative valuation of gold equities to gold bullion has fallen 75% from the prior 25-year average. The ratio of the XAU Index to spot gold averaged 0.2497x for a quarter century through 2008. As of 3/31/2020, the ratio was 0.0501x.

It is undoubtedly true that the industry will suffer health-related mine shutdowns and other shortfalls this year. Much of the disruption potential has already been broadcast and priced into the market. Some downside news may still have yet to surface. However, most miners are not financially levered and should be able to survive a few quarters of lower or no production. Unlike the airline, leisure, retail and manufacturing sectors, gold not produced today should grow in value and be produced at higher prices and lower costs next year and those beyond. It is not the same story for many other sectors of the economy. Based on fundamentals, gold stocks are inexpensive. By contrast, several other sectors of the economy could face long stretches of poor earnings, bad news flow and financial woes.

The gold mining sector registered a decline of approximately 20% in Q1 (as measured by GDX2) as shares did get battered by indiscriminate liquidations during March. However, as of this writing, two weeks after the close of the quarter, most shares trade near to where they stood at the beginning of the year, and have certainly registered outstanding performance in relative terms. It is remarkable that the largest sector ETF, GDX, suffered outflows of $381 million3 during the quarter at what could be the threshold of an upside breakout. In a favorable cycle for the gold price, mining stocks have historically delivered outperformance 3 to 5 times that of the metal itself.

Gold mining shares continue to be viewed by investors with deep skepticism as reflected by valuation and flows. When we scan Figure 4, it appears to us that the sector is on the verge of an upside breakout from a multi-year base should our assessment of the macroeconomic environment prove correct.

Figure 4. NYSE Arca Gold BUGS Index (HUI4) Source: Bloomberg. Data as of 4/20/2020.

Monetary and Fiscal Policy Going Ballistic

There is no need to belabor the obvious. However, the consequences of these actions have yet to be priced into the financial markets or gold. The risk parity trade has fallen short, partly because bonds were caught up in the indiscriminate liquidations of Q1. Looking forward, bonds may no longer be able to play the safe haven role they traditionally filled to balance equity risk. The vacuum could be filled in part by increased gold exposure for all classes of investors. Sovereign credit liquidity injections are likely to remain significant and permanent. The bond market has become socialized. Owning Treasury bonds of any duration could become akin to parking Treasury bills, with little upside and considerable risk of impairment through inflation. Gold is the antidote to the fixed-income investor’s dilemma.

Gold is extremely under-owned, under-represented, and poorly thought of in the circles of conventional investment thinking. It is still considered to be a fringe asset. Just ask Goldman Sachs which recently advised its clients:

“We concluded then (2010) that gold does not have a role as a strategic asset class in clients’ already well-diversified portfolios. We have updated the research and the evidence is even more compelling today than it was then.” (4/5/2020; Goldman Sachs Investment Strategy Group)

We remind the reader that Goldman is the same firm that in December 2019 declared the U.S. economy to be “recession proof†and then in March 2020 cautioned that stocks had substantial further downside:

“Overall, the changes underlying the Great Moderation appear intact, and we see the economy as structurally less recession prone today.†(12/31/2019; Goldman economists Jan Hatzius and David Mericle)

“Goldman Sachs on Friday dramatically cut its U.S. economic forecast, saying it now expects GDP to decline by 25% in the second quarter of 2020 because of the coronavirus panic.†(3/20/2020; Business Insider)

“What is your estimate for the S&P 500 by yearend 2020? David Kostin, “3400.†(1/2020; GS Podcast, David Kostin Goldman, U.S. chief equity strategist and Jake Siewert)

“Kostin thinks the market goes lower. ‘In the near term, we expect the S&P 500 will fall towards a low of 2000.’†(3/22/2020; Yahoo Finance)

Goldman’s commentary is, in our opinion, a reasonable proxy for conventional wisdom. One could easily find other embarrassing examples of mainstream thinking ignorant of the best-performing asset class (by far) versus equities and bonds since 2000.

Contrarians and value investors, take note! The secular gold bull that began in 2000 and corrected for a few years has returned to life with renewed vigor. Pullbacks — price declines during this uptrend — should be bought. The setup for gold and gold mining shares ticks every box for highly rewarding investment returns.

Figure 5. Gold Has Outperformed Stocks, Bonds and USD over the Past 20 Years Returns for Period from 12/31/1999-4/13/2020 Source: Bloomberg. Period from 12/31/1999-4/20/2020. Gold is measured by GOLDS Comdty; US Agg Bond Index is measured by the Bloomberg Barclays US Agg Total Return Value Unhedged USD (LBUSTRUU Index); S&P 500 TR is measured by the SPX; and the U.S. Dollar is measured by DXY Curncy. Past performance is no guarantee of future results.

Figure 6. Gold Provides Portfolio Diversification Gold provides diversification in a portfolio, and has low correlation with other asset classes. The period measured is April 1, 2015 to April 1, 2020. * Source: World Gold Council. Period from April 1, 2015 to April 1, 2020, based on monthly returns. Gold is measured by the LBMA Gold Price; stocks by the S&P 500 Index; commodities by the Bloomberg Commodity Index; Bonds by the BarCap Treasuries and Corporates.

1

The S&P 500 or Standard & Poor’s 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. You cannot invest directly in an index. TR, “Total Return”, represents the index with dividend income reinvested.

2

VanEck Vectors Gold Miners ETF (GDX) seeks to replicate the NYSE Arca Gold Miners Index (GDMNTR), which is intended to track the overall performance of companies involved in the gold mining industry.

3

Source: ETFtrends.com.

4

The NYSE Arca Gold BUGS Index (HUI) is a modified equal dollar weighted index of companies involved in gold mining.

Source: Bloomberg. Data as of 3/31/2020.

Source: Bloomberg. Data as of 3/31/2020. Data as of 3/31/2020. Source: Bloomberg. 12/23/1983 represents the inception of the XAU.

Data as of 3/31/2020. Source: Bloomberg. 12/23/1983 represents the inception of the XAU.

Source: Bloomberg. Data as of 4/20/2020.

Source: Bloomberg. Data as of 4/20/2020.

{kind=link}