Posted by AGORACOM-JC

at 4:04 PM on Monday, November 4th, 2019

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is

equipped with a 623m deep shaft and has never been mined.

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits.

Plans for Kenbridge include updating PEA,

advancing the project through to feasibility and exploring the open

mineralization at depth

FULL DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in All Recent Posts, Tartisan Nickel | Comments Off on CLIENT FEATURE: Tartisan Nickel $TN.ca Kenbridge Property Hosts M&I Resource of 7.14 Million Tonnes of 0.62% Nickel + 0.33% Copper $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 2:45 PM on Monday, November 4th, 2019

SPONSOR:ThreeD Capital Inc. (IDK:CSE)

Led by legendary financier, Sheldon Inwentash, ThreeD is a

Canadian-based venture capital firm that only invests in best of breed

small-cap companies which are both defensible and mass scalable. More

than just lip service, Inwentash has financed many of Canada’s biggest

small-cap exits. Click Here For More Information.

I’ve been an entrepreneur in this wild cryptocurrency industry for

over 5 years. My focus has been on leading a team of core developers to

build an open decentralized protocol that solves real problems for real

users. I’m not alone in this endeavour. There are at least a few dozen

of my peers leading projects with broadly similar goals.

To the outside world, we’re all crypto geeks building alternatives to

Bitcoin. That said, there are nuances in the designs and goals of

various projects that form the basis of some early investments theses

that leading funds have adopted to guide their selection criteria when

looking at digital assets.

Without getting into all the specifics, for the purposes of this

article, I want to focus only on the specific digital asset classes that

are native to their own networks or blockchains, rather than tokens

built into “dApps†or other similar models.

The reason this is important is because there are an increasing

number of funds, both institutional and not, that are looking at digital

assets as the next asset class to include in their diversified

portfolios that include everything from public equities, to real estate,

to gold, to bonds and other instruments. Who knows, maybe the next time

you check your pension, your favourite digital asset could be in it.

As such, it’s helpful to have a standard way to think about

the differences and similarities among digital assets, such that they

can be categorized for investment decisions.

To the outside looking in, this industry can be extremely opaque to

understand and evaluate. How value will be created, on what time horizon

and how does one form opinions on the quality of the project they’re

looking at. While there is infinite nuance between projects, protocols,

dApps, etc., most digital assets fall within common buckets, that have

formed the informal standard crypto theses. This mental model is helpful

for any observer, technologist or fund that has been researching or

thinking about allocating capital or time into this industry. It also

might help us understand new opportunities for value that fall outside

of these established categories (more on this later).

In speaking to a prominent investor in the cryptocurrency industry recently, he summarized this very simply:

“I understand and believe in Bitcoin and Ethereum. Everything else is just playing copy-cat and trying to play the same game.â€

In a broad sense, this is generally how the industry has evolved.

Bitcoin became dominant, and then many built alternatives (“altâ€-coins)

broadly solving for a similar goal, and then Ethereum introduced a new

type of protocol that was quickly followed by its own inspired

alternatives – something that Chris Burniske of Placeholder Ventures

refers to as “Ethereum Killersâ€.

The funds investing in this industry have had to build their theses

around this reality. As such, you’ll often find funds with a deep

conviction for Bitcoin and Ethereum, and then, to a lesser extent, a

series of “hedges†into alternatives that could grow in relevance and in

some cases potentially overtake the projects that first inspired them.

Many of these alternatives have taken different technical approaches,

but in general seek to solve the same problem and target the same

‘blockchain-converted’ developer or investor audience.

These investment themes behind Bitcoin and Ethereum are similar in

that they are both digital assets, but they’re different in the problems

they seek to solve.

Bitcoin established a category of digital assets that Multicoin Capital likes to refer to as “Global, State-free Moneyâ€.

This theme focuses on a growing need for a global form of money that is

independent of institutional trust and provides a digital alternative

to gold. The need for such an asset is to address the >500m people in

the world who live in countries with greater than 10% inflation, and to

provide a place for people to store their wealth that is safe from

seizure and “portable†across geographic boundaries.

Although it’s unclear how to measure the size of that addressable

market, the thesis implies a multi-trillion-dollar opportunity in this

category.

Ethereum, on the other hand, professed to be building a “world

computer†or in other contexts, the basis for a “decentralized

internetâ€. This category of digital assets known as “decentralized

internet†projects is what primarily caused the run up of the ICO

markets in 2017-2018. Believers in this thesis argue that the causes of

many of the inequities online today stem from the overly “centralizedâ€

nature of the internet’s infrastructure, such that incentives lead

towards monopolization of online services – think Facebook and Google.

As such, there is a massive interest in owning a piece of the “fuelâ€

that will power the renewed internet infrastructure of the future.

On top of this thesis are companies building utopia as they see it.

These ideas range from a system of finance that is open and alternative

to banking, a system of identity independent of governments, to other

lofty and worthy ideas that would find their homes in the “decentralized

internet†category.

Within these two broad categories, there are nuances and further

sub-categories, but at the highest level, this is a helpful frame to

better understand where a particular project fits, and what alternatives

it should be compared against. This framing should also help to better

understand why Bitcoin and Ethereum are fundamentally not competing

technologies, but why EOS, Tron, and Cardano have yet to prove why

they’re contenders to supplant Ethereum, their category king. As with

categories in other online industries, we’ll likely see a market where

75% of the value is dominated by the category leader, and the rest

spread among its competitors.

With 25-30+ launched or soon-to-be live networks looking to compete

in Ethereum’s category, its quickly become saturated. At the current

state of adoption in our industry, we’re nearing an oversupply of novel

technical solutions and a real need for actual usage. Networks have

collapsed into mirror-like narratives (build a dApp here!), use cases

(build DeFi here!), and are all seemingly speaking to the same audience.

So when looking at how this market might evolve, the real

breakthroughs will likely lie with projects that have a disproportionate

chance of dominating these two categories or projects that define a

brand new category with massive market potential. More on this next

week.

Posted by AGORACOM-JC

at 12:37 PM on Monday, November 4th, 2019

SPONSOR: Betteru Education Corp.

aims to provide access to quality education from around the world. The

Company plans to bridge the prevailing gap in the education and job

industry and enhance the lives of its prospective learners by developing

an integrated ecosystem. Click here for more information.

BTRU: TSX-V

EdTech startups can address shortage of machine learning experts in India

Edtech startup: Enhanced outreach of technology is resulting in industries and end users taking a leap of faith into the world of new concepts.

Machine learning (ML) is one such domain that has around 10x jobs at present as compared to the situation, five years ago.

EdTech startup: Enhanced

outreach of technology is resulting in industries and end users taking a

leap of faith into the world of new concepts. Several industries have

polished their approach in designing an outcome for the new generation

to mould something new and relevant, according to the trends of the

future. Machine learning (ML) is one such domain that has around 10x jobs at present as compared to the situation, five years ago.

This situation has shaped up due to various contributing factors

including huge popularity of machine learning. Fortune 500 companies are

integrating machine learning and artificial intelligence into their

processes and Indian firms are following suit. Machine learning is

responsible for shaping the business landscape. Business analytics and

intelligence teams are able to analyse terabytes of data in seconds

using different methods like recognition, diagnosis, regression,

prediction and many more.

Machine learning focuses on the development of algorithms which helps

those machines teach themselves grow, develop and respond to new data.

The reason machine learning has become hugely popular is because it has

helped all the companies (from various industrial sectors) get exact and

real time insights and mitigate the strategy level risks, if any.

While on the one hand, we are amazed by these developments; there is a

concern on the other hand too. Yes, machine learning is the most

in-demand skill right now but is our talent pool really equipped with

the required skills. The answer is “Noâ€. Demand for machine learning

experts will continue to increase in the coming years and will probably

outpace the current supply of talent pool in the next three-four years.

According to the LinkedIn economic graph, the jobs in ML have been a

turning point in the technological trends as compared to the other

umbrella domains. The number of jobs which were five years ago is now

9.8 times, thus, helping to provide an asset to the industry.

Educational institutions have always provided the industry with the

required set of skills but with an increased demand in such a short

time, they have been unable to come up with a solution on such a short

notice. In order to cater to the current industry trends, EdTech startups have come with excellent “Industry-Vetted Course Curriculumâ€.

EdTech startups create a perfect amalgamation

EdTech startups don’t focus on just teaching theoretical concepts but

rather provide an online learning which is no less than the offline

classroom approach. There are online videos which can be accessed

anytime and from anywhere. Since the videos are self-paced, it is made

sure that they cater to the speed of every individual.

EdTech startups create a perfect amalgamation by getting industrial

experts on board and creating a course curriculum as per the exact needs

of the ML industry. In order to make sure that the student doesn’t

deviate and follows the curriculum, virtual / physical assistance is

provided which analyse the performance of each and every student on a

daily basis and customised approach is recommended.

They are deploying algorithms to bring a personalised touch for every

student, thus ensuring a better application-based learning. We have

experienced and welcomed this new way of mobile teaching which takes

care of every individual student’s needs, comforts and results at the

same time.

EdTech companies have come up with the content which not only

satisfies the need of the industry but can also be imparted to anyone in

due amount of time; thus, fulfilling the requirement of the ML domain.

Several factors which have enabled these startups develop skilled ML

experts are: self-paced learning; industry-vetted content; regular

industrial interaction through bootcamps and webinars; individual

learning and development system; real-time actionable insights; and

industrial projects which can be deployed in companies.

Machine learning is one of the most promising technologies of the

last decade and it is the perfect time to realise we have a companion

since “Machines also Learnâ€.

Posted by AGORACOM-JC

at 4:00 PM on Thursday, October 31st, 2019

SPONSOR: NORTHBUD (NBUD:CSE)

Sustainable low cost, high quality cannabinoid production and

procurement focusing on both bio-pharmaceutical development and

Cannabinoid Infused Products. Learn More.

NBUD: CSE —————————–

Edible CBD Products Offer Consumers a New Health Trend

North American consumer spending on cannabis-infused foods and drinks reached USD 1.5 Billion in 2018, according to data compiled by Arcview Market Research and BDS Analytics,

By 2022, the two firms suggest that edible sales are on track to reach USD 4.1 Billion

NEW YORK, Oct. 31, 2019 – Consumer trends constantly require industries to adapt in order to thrive among the competition. Specifically, the food and beverage industry is one of the fastest evolving markets because of constant changes in consumer demands. Nowadays, the increasing demand for healthier and more organic options is prompting manufacturers to produce alternatives to sugar-packed drinks and fatty snacks. Instead, consumers are looking for products that are processed with healthier sustainable ingredients, proteins, vitamins, and antioxidants. Notably, many consumers have turned to the beverage industry for functional drinks such as kombucha. A functional drink is a type of beverage that typically conveys a health benefit such as being packed with performance-enhancing agents like nootropics and amino acids. Consequently, the growing demand in the functional beverage market sparked interest within the CBD market. CBD is a derivative of the hemp plant, which falls under the cannabis family.

Typically, cannabis is associated with its marijuana component, which

causes psychoactive effects because of its heavy THC concentrate.

However, hemp does not cause psychoactive effects because the main

compound is CBD. THC and CBD are widely different in their biological

makeup, but because they derive from the cannabis plant, regulators

deemed both compounds to be unsafe for consumers. However, extensive

research has uncovered that CBD provides therapeutic and health

benefits, which then led to the rapid emergence of CBD-based products.

As such, North American consumer spending on cannabis-infused foods and

drinks reached USD 1.5 Billion in 2018, according to data

compiled by Arcview Market Research and BDS Analytics, By 2022, the two

firms suggest that edible sales are on track to reach USD 4.1 Billion.

Typically, most people consume CBD to simply relax. However, clinical

trials have proven that CBD can also provide medical benefits.

Specifically, patients suffering from chronic ailments such as severe

pain, cancer, arthritis, and epilepsy can consume CBD drinks to subdue

the symptoms. And while CBD is quickly permeating throughout global

regions, the North American market is the primary driver because of

legality stance. Canada moved to legalize cannabis entirely

back in late 2018, which prompted a spur of recreational demand. On the

other hand, the U.S. passed the Farm Bill in 2018, which legalized

hemp-derived CBD products. Shortly after, stores across the nation began

to commercialize CBD goods.

Now, consumers can easily purchase products such as tinctures,

topicals, oils, and edibles at their local convenience stores or online

e-commerce platforms. However, the CBD beverage market is one of the

most popular segments because consumers can easily purchase a CBD-based

tincture and add droplets of CBD into their beverage. Generally, CBD can

be found within beverages such as soda, juice, coffee, wine, water, and

even alcohol. However, consumers can also add CBD-based powders into

their beverages and some producers have even mentioned that powders are

much better in terms of solubility. Overall, the cannabis-infused

beverage industry is quickly gaining traction, however, some beverage

producers are still evaluating the industry.

Nonetheless, a handful of corporations such as the alcohol industry,

have already dove into the marketplace and are already marking their

presence. “Everyone in the industry recognizes that CBD-infused

beverages are going to be one of the largest category opportunities in

all of CBD,” said Ben Witte, the Founder and Chief

Executive Officer of Recess, a company producing CBD-infused sparkling

water. “As a result of that, a lot of the suppliers in the supply chain

have innovated to create a format that is soluble in beverages.”

Posted by AGORACOM-JC

at 12:07 PM on Thursday, October 31st, 2019

Company has notified BWA Group plc (London, England) (NEX:BWAP) of its intention to convert GBP300,000 ($511,000) of Convertible Loan notes “CLN” into 60,000,000 ordinary shares in BWA Group plc.

Shares will be admitted to trading on the NEX Exchange Growth Market in London, effective November 6, 2019

Montreal – October 31, 2019 –St-Georges Eco-Mining Corp. (CSE:SX) (OTC:SXOOF) (FSE: 85G1) is pleased to inform its shareholders that the Company has notified BWA Group plc (London, England) (NEX:BWAP) of its intention to convert GBP300,000 ($511,000) of Convertible Loan notes “CLN” into 60,000,000 ordinary shares in BWA Group plc.

The Company has been notified by

BWA Group plc that the shares will be admitted to trading on the NEX

Exchange Growth Market in London, effective November 6, 2019. Following

the allotment of these ordinary shares, St-Georges will hold 60,000,000

ordinary shares of BWA Group plc, representing 23.75% of this

corporation’s enlarged issued share capital.

The Company received GBP2,451,409

($4,183,000) of convertible loan notes on September 30, 2019 in relation

to sale of its subsidiary Kings of the North to BWA Group plc. After

the conversion, St-Georges has GBP2,151,409 worth of loan notes

outstanding at an approximate value of $3,671,427.

ON BEHALF OF THE BOARD OF DIRECTORS

“Mark Billings”

MARK BILLINGS

Chairman

About St-Georges

St-Georges is developing new

technologies to solve some of the most common environmental problems in

the mining industry. The Company controls directly or indirectly,

through rights of first refusal, all of the active mineral tenures in

Iceland. It also explores for nickel on the Julie Nickel Project &

for industrial minerals on Quebec’s North Shore and for lithium and rare

metals in Northern Quebec and in the Abitibi region. Headquartered in

Montreal, St-Georges’ stock is listed on the CSE under the symbol SX, on

the US OTC under the Symbol SXOOF and on the Frankfurt Stock Exchange

under the symbol 85G1.

The

Canadian Securities Exchange (CSE) has not reviewed and does not accept

responsibility for the adequacy or the accuracy of the contents of this

release.

Posted by AGORACOM-JC

at 10:24 AM on Thursday, October 31st, 2019

SPONSOR:ThreeD Capital Inc. (IDK:CSE)

Led by legendary financier, Sheldon Inwentash, ThreeD is a

Canadian-based venture capital firm that only invests in best of breed

small-cap companies which are both defensible and mass scalable. More

than just lip service, Inwentash has financed many of Canada’s biggest

small-cap exits. Click Here For More Information.

IDK: CSE

Bitcoin And Crypto Is Heading For An Epic Social Media Showdown

While the social media monetary situation is not this clear cut, both

Dorsey and Zuckerberg have emerged as champions of two similar but

opposing ideas; the internet needs its own currency, one sees it as

centralised, through Facebook, the other sees it as decentralised,

through bitcoin.

“I believe that this is something that needs to get built,”

Zuckerberg told U.S. senators last week, defending Facebook’s

involvement in the controversial libra project and arguing libra could

bring financial maturity to millions, if not billions, of people around

the world.

Zuckerberg also warned the U.S. could fall behind other countries if

lawmakers moved to block the development of libra and similar digital

money projects.

Posted by AGORACOM-JC

at 9:08 AM on Thursday, October 31st, 2019

Announced its collaboration with Professor Lionel ROUÉ of the Institut National de Recherche Scientifique (INRS)

Aimed at evaluating the electrochemical performances of different materials produced by the HPQ PUREVAP™Quartz Reduction Reactor for Li-ion batteries

MONTREAL, Oct. 31, 2019 — HPQ Silicon Resources Inc. – TSX-V: HPQ; OTCPink: URAGF; FWB: UGE (“HPQ†or “the Companyâ€) is pleased to announce its collaboration with Professor Lionel ROUÉ of the Institut National de Recherche Scientifique (INRS) within the scope of projects aimed at evaluating the electrochemical performances of different materials produced by the HPQ PUREVAP™Quartz Reduction Reactor (“QRR”) for Li-ion batteries.

Professor Lionel ROUÉ of the INRS-EMT has developed a scientific

program focused on the study of new electrode materials for various

applications of industrial interest (batteries, aluminium production,

etc.). In recent years, a significant part of its research activities

has been devoted to the study of Si anodes for Li-ion batteries and the

development of in-situ characterization methods applied to batteries.

He is the author of more than 150 publications, including twenty

articles and 2 patents on Si-based anodes for Li-ion batteries. He was

awarded the Energia Prize by the Quebec Association for the Mastery of

Energy for his work in this field.

EVALUATING WORLDWIDE BATTERY MARKET POTENTIAL OF MATERIALS PRODUCED BY PUREVAP™

The first goal of the association is determining the commercial potential of materials produced by the PUREVAPTM

QRR as anode material for the Li-ion battery market and ascertaining

whether their usage within Li-ion batteries could lead to a significant

increase in their energy density, which is crucial for some

applications, especially electric vehicles.

In the second phase, the electrochemical performance of PUREVAPTM silicon based porous silicon wafers made using Apollon Solar’s patented process will be tested.

“Silicon’s potential to meet energy storage demand is generating massive investments. Collaborating

with a world-class university center, HPQ will be able to validate the

potential of silicon materials produced from the PUREVAP™QRR as high-capacity anode materials for Li-ion batteries†said Bernard Tourillon, President & CEO of HPQ Silicon Resources Inc. Mr. Tourillon added: “HPQ, working with PyroGenesis, Apollon and the INRS Energy Materials Telecommunications (EMT) Research Centre, fully intends to use its Gen3 PUREVAP™ QRR to produce and market Silicon materials for batteriesâ€.

GLOBAL ENERGY STORAGE MARKET READY TO EXPLODE

A recent report

projects that energy storage deployments are estimated to grow 1,300%

from a 12 Gigawatt-hour market in 2018 to a 158 Gigawatt-hour market in

2024. An estimated US$71 billion in investments will be made into

storage systems where batteries will make up the lion’s share of capital

deployment. Research suggests

that replacing graphite materials with Silicon anodes in Li-Ion

Batteries promises an almost tenfold (10x) increase in the specific

capacity of the anode, inducing a 20-40% gain in the energy density of

Li-ion batteries.

About Silicon

Silicon (Si) is one of today’s strategic materials needed to fulfil

the renewable energy revolution presently under way. Silicon does not

exist in its pure state; it must be extracted from quartz, one of the

most abundant minerals of the earth’s crust and other expensive raw

materials in a carbothermic process.

About HPQ Silicon

HPQ Silicon Resources Inc. is a TSX-V listed company developing, in

collaboration with industry leader PyroGenesis (TSX-V: PYR) the

innovative PUREVAPTM “Quartz Reduction Reactors†(QRR), a truly

2.0 Carbothermic process (patent pending), which will permit the

transformation and purification of quartz (SiO2) into Metallurgical

Grade Silicon (Mg-Si) at prices that will propagate its significant

renewable energy potential.

HPQ is also working with industry leader Apollon Solar to develop: Porous silicon wafers manufacturing using PUREVAP™

Silicon (PVAP Si) that can be used as anode for all-solid-state and

Li-ion batteries; and a metallurgical pathway of producing Solar Grade

Silicon Metal (SoG Si) that will take full advantage of the PUREVAPTM QRR

one-step production of high purity silicon (Si) and significantly

reduce the Capex and Opex associated with the transformation of quartz

(SiO2) into SoG-Si.

HPQ focus is becoming the lowest cost producer of Silicon (Si), High

Purity Silicon (Si), Porous Silicon Wafers and Solar Grade Silicon Metal

(SoG-Si). The pilot plant equipment that will validate the commercial

potential of the process is on schedule to start in 2019.

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

Disclaimers:

The Corporation’s interest in developing the PUREVAP™ QRR and any

projected capital or operating cost savings associated with its

development should not be construed as being related to the establishing

the economic viability or technical feasibility of the Company’s

Roncevaux Quartz Project, Matapedia Area, in the Gaspe Region, Province

of Quebec.

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward-looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Company’s current expectation and assumptions and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Company with respect to future events and are subject to certain risks

and uncertainties and other risks detailed from time-to-time in the

Company’s on-going filings with the security’s regulatory authorities,

which filings can be found at www.sedar.com. Actual results, events, and

performance may differ materially. Readers are cautioned not to place

undue reliance on these forward-looking statements. The Company

undertakes no obligation to publicly update or revise any

forward-looking statements either as a result of new information, future

events or otherwise, except as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

For further information contact Bernard J. Tourillon, Chairman, President and CEO Tel (514) 907-1011 Patrick Levasseur, Vice-President and COO Tel: (514) 262-9239 http://www.hpqsilicon.com Email: [email protected]

Posted by AGORACOM-JC

at 11:03 AM on Wednesday, October 30th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

TN: CSE —————————-

A nickel for your thoughts – The price of nickel has run up to a five-year high of late

The price of nickel has run up to a five-year high of late, defying softness in the rest of the base metal complex.

The reasons are both simple and complicated. The price of nickel

doubled in two years, from US$4 per lb. in August 2017 to US$8 per lb. a

few weeks ago. The reasons:

· Robust demand. Nickel is primarily used to make stainless steel. And despite slowing growth, stainless steel demand keeps marching up.

In the first half of 2019, for instance, Chinese stainless steel

production was up 8.5% yearover-year. (As the chart suggests, forecasts

predict softening of demand in the current quarter.)

· China makes most of the world’s stainless steel. And China gets the

nickel for that steel from its own mines as well as mines in Indonesia

and the Philippines, many of which produce a lowgrade, high-impurity ore

called nickel pig iron (NPI). NPI production has

ballooned over the last decade, enough that as of 2020 the world will

get more of its nickel from NPI than from conventional nickel ores.

However, this reliance on NPI brings with it a few problems.

· Indonesia will implement a ban on nickel ore exports at the start of 2020.

This has been in the works for some time but until a few months ago the

ban was not scheduled to take effect until 2022. Indonesia produces

roughly ~12% of global supply, so this ban is significant. The idea is

to push the development of domestic smelters, which would keep more of

the resource upside in country versus exporting raw ore. This is in the

works – the country already has 11 nickel smelters and 25 more are

planned or under construction – so Indonesian nickel supplies should

slide in the near term but recover within about three years. However,

the smelters in China that relied on Indonesia’s nickel pig iron (NPI)

ore will have to find feed elsewhere; the main candidate is the

Philippines, where ore is generally lower grade. The only other option

is to upgrade to processing Class I ores. Either move would increase

costs overall, which supports a higher nickel price.

· Batteries. Eighty percent of the world’s nickel

goes into stainless steel, so steel certainly drives the market. But

many of the batteries that power laptops, electric vehicles, phones, and

even power grids require nickel. This has transformed nickel from a one

trick pony to a two trick market – and if electric cars take off then

nickel’s battery market will take off right alongside. Right now

batteries consume 5% of global nickel but demand is rising rapidly and

is expected to reach 8% by 2020. Vice President of market analysis and

economics for BHP, Dr Huw McKay, says he sees a future where batteries

and stainless steel become “equally important†nickel consumers. Global

nickel demand currently sits around 2 million tonnes per annum; it is

expected to grow to 6 million tonnes per annum by 2035 with batteries

accounting for almost half of demand growth.

· In addition, batteries cannot use nickel from NPI, as impurities are too high, so the battery factor has divided the nickel market into two parts

– high purity Class I nickel and lower purity Class II. All of this has

two important effects: it is bringing energy metal investors into the

nickel space and it is underlining that NPI, which has been the dominant

source of nickel growth for the last 10-plus years, will not solve the

nickel supply gap going forward.

· To address that second point and boost production of Class I

nickel, China is developing several mines tapping into nickel laterite

deposits. Nickel laterite is easy to mine but very difficult to process,

requiring high pressure acid leaching (HPAL). Most analysts are

highly skeptical that China’s planned HPAL facilities will come online

anywhere near their projected timelines or budgets, as these facilities are notoriously difficult and expensive.

· Because NPI has ballooned so in the last decade, explorers and developers have not looked for conventional nickel deposits. There

is a true lack of development-stage nickel projects with conventional

sulphide deposits that could be built to fill supply gaps.

· Current mine-specific supply issues. The biggest

producer of NPI in the Philippines just ran out of ore. The Ramu project

in Papua New Guinea is temporarily suspended, which removes 35,000

tonnes of annual nickel supply.

· Stockpiles are falling – and fast. Nickel stockpiles have been declining for five years.

This is what happens when a market is persistently undersupplied. But

as you can see, the decline accelerated in the last two years…and

stockpiles dropped off a cliff a few weeks ago.

The cliff is likely the result of panic buying and/or stockpiling ahead of the Indonesian ban.

I told you it was complicated!

Complicated is normal for nickel, which has a long track record of

extreme price moves. In 2008 a supply shortage drove the price as high

as US$22 per lb. before steel mills found substitutes, 7 including

manganese, and within 18 months the price was back at US$4.50 per lb.

(The Great Financial Crisis likely exacerbated the price decline.)

The Bear Case

The key question on this side is: to what extent is speculation driving nickel?

If speculators are pushing the price up, entering the space now is

risky because (1) speculative tides turn fast and (2) that turn would

likely transpire in the next 6 to 9 months. Indonesia’s ban comes into

effect in January 1 so over the next six months the impacts start to

play out.

It’s clear that stockpile drawdowns are at least in part because

smelters and speculators have been stockpiling metal privately. That

metal will be used or sold to ease any nickel price jumps.

If increased physical metal availability coincides with the absence of speculative upside pressure…nickel could turn down fast.

On top of all that, there are reasons to believe (1) stainless steel

demand will weaken to end this year, (2) EV demand is taking longer to

ramp than expected, (3) scrap usage is increasing, and (4) rising

backwardation alongside falling physical premiums is a sign that actual

demand is lower than perceived.

The fourth point above needs some explaining. In a tight market,

limited stockpiles lead to backwardation – people paying more for metal

today than in the future. Backwardation should only happen when the

current physical market is very tight. If that’s the case, there should

also be high physical premiums, which are extra amounts paid for actual

metal now (rather than paper metal).

What weird about nickel is that premiums are down sharply, from $200

per tonne a few months ago to negative $50 per tonne today. It’s the

first-time premiums have ever gone negative in China and something that

is very rare across the metals complex. European nickel briquette

premiums are also down 80% in recent months.

The dark blue line below shows physical premiums. The light blue line

shows the difference between current and three-month nickel prices; a

positive Cash-3M is backwardation.

<

This suggests:

· The physical market is not that tight

· Speculation in the paper market is driving the price

· Speculation is not simply investors; nickel users and producers are

also playing games (stockpiling) to boost the price. When they stop,

the price will lose ground rapidly.

The Bottom Line

Nickel may or may not continue its bull run from here. The fact the

physical premiums are so low when prices have gained so much and the

paper market is in backwardation is definitely concerning, enough that I

am not ready to enter the space right now. The fact that nickel spot

price recently stepped back almost 10% reinforces my outlook.

However, in the medium and long term this is a market that has good

opportunity. Stainless steel demand growth is reliable. The battery

space will need more and more Class I nickel with each year. The

pipeline of new projects is very limited, especially if you (like me)

see China struggling with its nickel laterite output mines and HPAL

facilities.

I might be wrong and my hesitation on entering now may mean missing

out on near term upside, but such decisions are common in this sector!

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in Tartisan Nickel | Comments Off on Tartisan #Nickel $TN.ca – A nickel for your thoughts – The price of nickel has run up to a five-year high of late $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 10:29 AM on Wednesday, October 30th, 2019

SPONSOR:ThreeD Capital Inc. (IDK:CSE)

Led by legendary financier, Sheldon Inwentash, ThreeD is a

Canadian-based venture capital firm that only invests in best of breed

small-cap companies which are both defensible and mass scalable. More

than just lip service, Inwentash has financed many of Canada’s biggest

small-cap exits. Click Here For More Information.

IDK: CSE

Twitter’s Dorsey puts another bet on crypto

Bitcoin proponent Twitter CEO Jack Dorsey continues to bet on crypto by investing in CoinList, a two-year-old venture that helps startups raise money through token sales.

The company says it connects investors with thoroughly vetted

blockchain-related companies in compliance with crypto regulations.

CoinList has supported more than $800M of token offerings since August 2017.

Dorsey participated in a recent $10M funding round, the Wall Street Journal reports.

The new capital will help with its plans to offer new services

including a new exchange, CoinList Trade, and a crypto wallet.

Posted by AGORACOM-JC

at 9:00 AM on Wednesday, October 30th, 2019

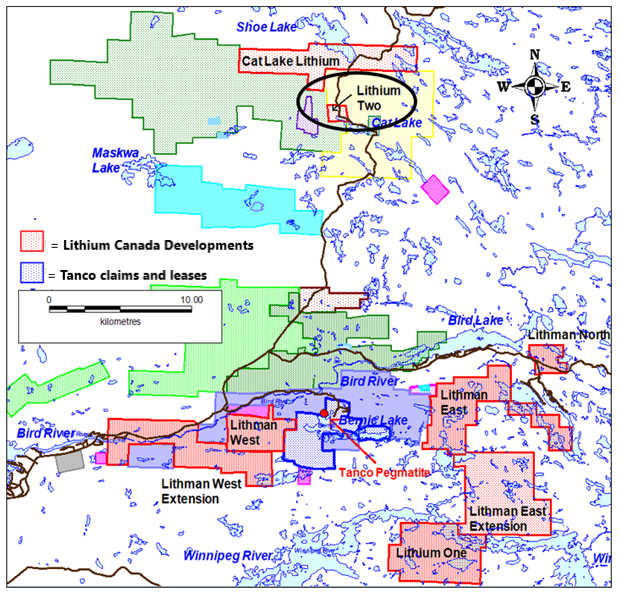

A drill permit has been issued by the Manitoba government for a drill program on the company’s Lithium Two Project.

NAM has 100% ownership of eight pegmatite hosted Lithium and Rare Element Projects in the Winnipeg River Pegmatite Field, located in southeast (SE) Manitoba.

Exploration in SE Manitoba is focused on Lithium-bearing pegmatites.

Archaeological Assessment in progress on Lithium One as part of the drill permit process.

The eight projects are strategically situated within the Winnipeg River Pegmatite Field, which hosts the world-class Tanco Pegmatite that has been mined for Tantalum, Cesium and Spodumene (one of the primary Lithium minerals) in varying capacities, since 1969.

NAM management is finalizing a plan for a 1,500-metre drill program on Lithium Two.

October 30th, 2019 – Rockport, Canada – New Age Metals Inc. (NAM) (TSX.V: NAM; OTCQB: NMTLF; FSE: P7J) New Age Metals is pleased to announce that a drill permit has been issued to the company’s wholly owned subsidiary, Lithium Canada Development by the Manitoba government for the company’s Lithium Two Project located in the Cat Lake area of southeast (SE) Manitoba.

The Winnipeg River Pegmatite Field

The

Winnipeg River-Cat Lake Pegmatite Field in SE Manitoba is host to

numerous pegmatite deposits and contains the world-class Tanco

Pegmatite. The Tanco pegmatite has been mined since 1969 in

varying capacities for spodumene (Li rich mineral), Tantalum and Cesium.

The pegmatite field contains at least 10 pegmatite groups and hosts

hundreds of pegmatite bodies. Many of the pegmatites are lithium

bearing.

The Tanco Mine, which was owned by the

Cabot Corporation, was recently sold to Sinomine Rare Metals Resources

Co. Ltd. (Sinomine) at a purchase price of $130 million ($US). Sinomine

is a joint stock public company based in China, principally engaged in

the provision of geological exploration, mining investment and base

metal chemical manufacturing. This transaction certainly adds new

interest in the region as to the potential of the pegmatite field and

lithium and/or rare element potential in the area. This sale should

advance the Lithium production potential of the area as Lithium Ore feed

may be required in the event that Sinomine commences lithium

production.

Lithium Two Project

The Lithium Two Project is located

approximately 20 kilometres north of the Tanco Mine and is an active

area for Lithium exploration. Several companies are active in the

immediate region, exploring for Lithium.

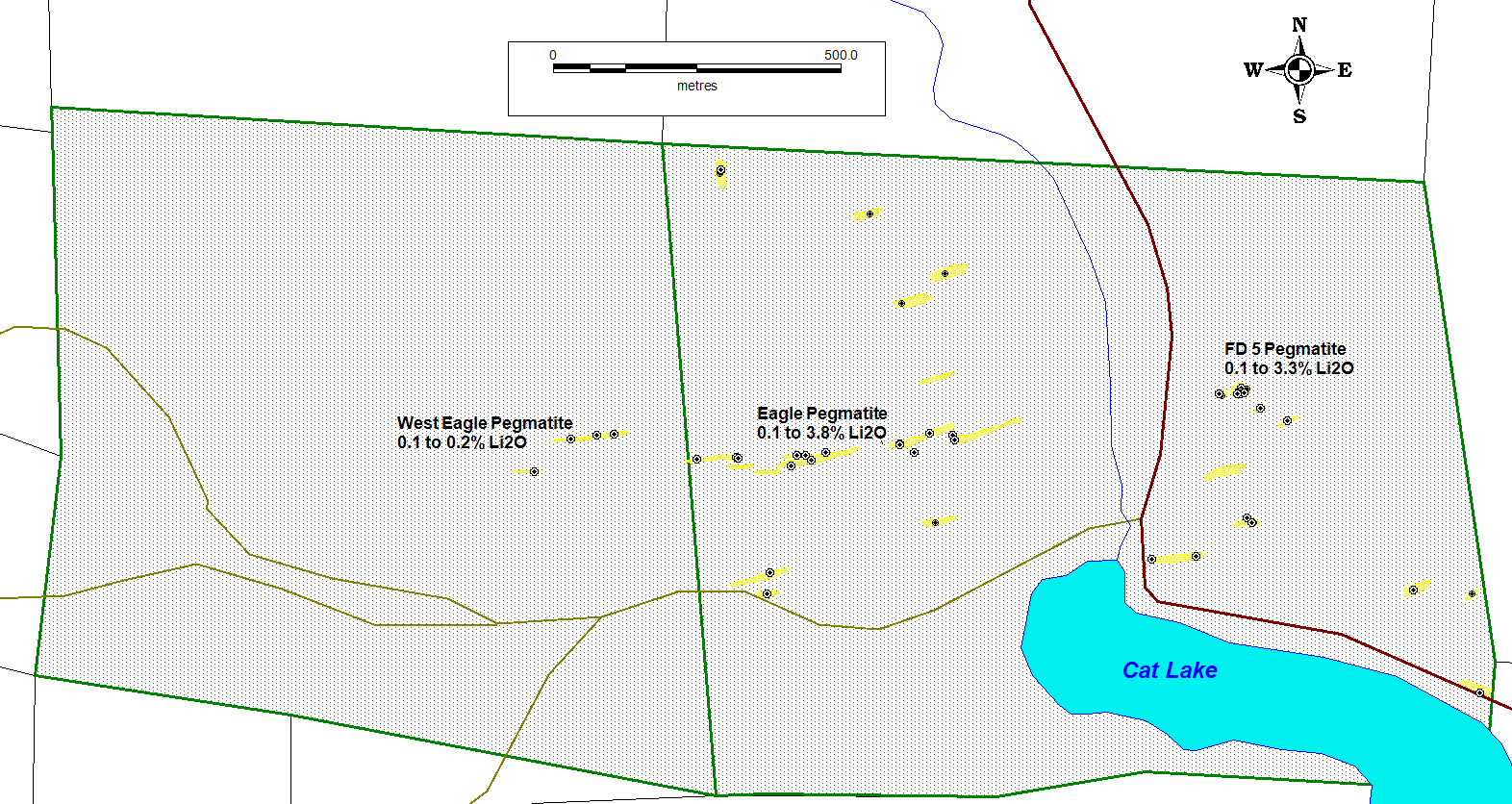

Surface exploration was carried out on the Lithium Two Project during the summer of 2018 (see News Release October 30th, 2018).

The exploration work was designed to examine the known surface

pegmatites to aid in the determination of drill targets. The field

program also focussed on more detailed structural geological mapping and

mapping of the westward extent of the Eagle Pegmatite. The Lithium Two

Project has several historically known Spodumene bearing pegmatites (see

Figure 2).

Click Image To View Full Size

Figure 1: Manitoba Lithium and Rare Element Projects 2019

The Eagle Pegmatite was drilled in 1947

with a historic (non 43-101 compliant) tonnage estimate of 544,460

tonnes with a grade of 1.4% Li2O to the 61-metre level. These historical

estimates do not use categories that conform to current CIM Definition

Standards on Mineral Resources and Mineral Reserves as outlined in

National Instrument 43-101, Standards of Disclosure for Mineral Projects

(“NI 43-101”) and have not been redefined to conform to current CIM

Definition Standards. A qualified person has not done sufficient work to

classify the historical estimates as current mineral resources and the

Company is not treating the historical estimates as current mineral

resources. Investors are cautioned that the historical estimates do not

mean or imply that economic deposits exist on the properties. The

Company has not undertaken any independent investigation of the

historical estimates or other information contained in this press

release nor has it independently analyzed the results of the previous

exploration work in order to verify the accuracy of the information. The

Company believes that these historical estimates and other information

contained in this news release are relevant to continuing exploration on

the properties as it identifies significant mineralization that will be

the target of future exploration and development.

The Eagle Pegmatite was historically reported to remain open to depth.

The FD5 Pegmatite, located east of the Eagle Pegmatite has never been

drilled. Historic assessment reports revealed a Spodumene bearing

pegmatite drilled in the late 1940’s, located approximately 500 metres

southeast of the Eagle Pegmatite but is not exposed on surface. No

assays were provided in the report at the time. This pegmatite, as well as the Eagle and FD5, will be tested during an upcoming recommended drill program.

Click Image To View Full Size

Figure 2: 2018 Lithium Assays at the Lithium Two Project, SE Manitoba

The Eagle Pegmatite has been mapped on surface for over 850 metres and has surface assays of 0.1 to 3.8% Li2O.

The FD5 pegmatite had surface assays from 0.1 to 3.3% Li2O. In

geological terms, the pegmatites encountered on the Lithium Two Project

are LCT Type (Lithium-Cesium-Tantalum) Pegmatites and are in the

Albite-Spodumene Subgroup. Spodumene is expressed in the pegmatites as

small green blades up to 3 centimetres in length. The Eagle Pegmatite is

a west-northwest to west-striking, vertically dipping, lenticular

pegmatite dyke intruded into mafic volcanics. The widths of the

pegmatite have been measured to be between 2 to 10 metres. The Eagle

Pegmatite system appears to be a swarm of closely spaced pegmatite

bodies.

Phase 1 Drill Program Planning in Progress

A drill program of 1,500 metres is planned

to test three spodumene bearing pegmatite targets. A drill permit has

recently been issued by the Manitoba government.

Lithium One Drill Program

Recently,

NAM engaged White Spruce Archaeology as part of its Exploration

Agreement with the Sagkeeng First Nation to conduct an archaeological

assessment on the proposed drill sites for Lithium One as part of the

drill permitting process. The assessment was completed in October

and the report is pending. A 1,500 metre drill program is planned to

test targets on the Silverleaf pegmatite ( News Release Sept 27, 1018) situated in the Lithium One project area.

NAM/AAZ Property Option Update

JV partner Azincourt Energy (AAZ) and NAM

are in discussions regarding AAZ’s compliance for its contractual

obligations as part of the option agreement with NAM. NAM and AAZ are in

continuing talks regarding a revision to the existing option agreement

or termination.

OPT-IN LIST

If you have not done so already, we encourage you to sign up on our website (www.newagemetals.com) to receive our updated news.

ABOUT NAM’S PGM DIVISION

NAM’s flagship project is its 100% owned River Valley PGM Project (NAM Website – River Valley Project)

in the Sudbury Mining District of Northern Ontario (100 km east of

Sudbury, Ontario). Recently the company announced the results of the

first PEA (see News Release – June 27th, 2019)

completed on the River Valley Project. The PEA has been developed by

various independent consultants – P&E Mining Consultants Inc.

(P&E) was responsible for the open pit mining, surface

infrastructure, tailings facility, and project economics; DRA Americas

Inc. (“DRA”) was responsible for all metallurgical test work and

processing aspects of the Project; and WSP Canada Inc. (“WSP”) was

responsible for the Mineral Resource Estimate. The

PEA is a preliminary report but it has demonstrated that there are

positive economics for a large-scale mining open pit operation, with 14

years of Palladium and Platinum production.

The

Genesis project is a PGM-Cu-Ni property located in the northeastern

Chugach Mountains, 75 paved road miles north of the all-season port city

of Valdez, Alaska. The project is within 3 km of the all-season

paved Richardson Highway and a high capacity electric power line. The

project is covered by 4,144 hectares of State of Alaska mining claims

owned 100% by New Age Metals. Past exploration has revealed the presence

of chromite-associated platinum and palladium mineralization and

stratabound Ni-Cu-PGM mineralization within magmatic layers of the

Tonsina Ultramafic Complex. Pyrrhotite, pentlandite, and chalcopyrite

occur in disseminations and net textured segregations associated with

platinum and palladium sulfides. There has been limited exploration over

the Genesis project and there has been no past exploration drilling on

the project. NAM management is actively seeking an option/joint-venture partner for this road accessible PGM and Multiple Element Project.

QUALIFIED PERSON

The contents contained herein that

relate to exploration results or geological aspects is based on

information compiled, reviewed or prepared by Carey Galeschuk, P. Geo., a

consulting geoscientist for New Age Metals. Mr. Galeschuk is the

Qualified Person as defined by National Instrument 43-101 and has

reviewed and approved the technical content of this news release.

On behalf of the Board of Directors

“Harry Barr”

Harry G. Barr

Chairman and CEO

Neither the TSX Venture Exchange nor its

Regulation Services Provider (as that term is defined in the policies

of the TSX Venture Exchange) accepts responsibility for the adequacy or

accuracy of this release.

Cautionary Note Regarding Forward

Looking Statements: This release contains forward-looking statements

that involve risks and uncertainties. These statements may differ

materially from actual future events or results and are based on current

expectations or beliefs. For this purpose, statements of historical

fact may be deemed to be forward-looking statements. In addition,

forward-looking statements include statements in which the Company uses

words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”,

“confident”, “intend”, “strategy”, “plan”, “will”, “estimate”,

“project”, “goal”, “target”, “prospects”, “optimistic” or similar

expressions. These statements by their nature involve risks and

uncertainties, and actual results may differ materially depending on a

variety of important factors, including, among others, the Company’s

ability and continuation of efforts to timely and completely make

available adequate current public information, additional or different

regulatory and legal requirements and restrictions that may be imposed,

and other factors as may be discussed in the documents filed by the

Company on SEDAR (www.sedar.com), including the most recent reports that

identify important risk factors that could cause actual results to

differ from those contained in the forward-looking statements. The

Company does not undertake any obligation to review or confirm analysts’

expectations or estimates or to release publicly any revisions to any

forward-looking statements to reflect events or circumstances after the

date hereof or to reflect the occurrence of unanticipated events.

Investors should not place undue reliance on forward-looking statements.