Posted by Brittany McNabb

at 12:14 AM on Thursday, December 21st, 2023

HPQ Silicon Anode Battery Tech Wins 3rd Party Validation With €90,000 Grant By French Bank of Public Investments. Plans To Seek Additional Grant Up to €2M

In the realm of electric vehicle (EV) batteries, the anode serves as a critical component, acting as a storage vessel for lithium ions. Graphite anodes, the current market dominators, have reached their peak energy density. This limitation prompts a shift toward Silicon-based anodes, offering up to 10 times the energy density.

Major players like Porsche, Mercedes, and GM are embracing this technology, recognizing its potential to revolutionize EV performance.

However, Silicon anodes face challenges in degradation during charging cycles.

ENTER HPQ SILICON INC. (TSX-V: HPQ) (OTCQB: HPQFF)

HPQ Silicon is a technology company specializing in green engineering for silicon manufacturing. Positioned strategically to become a key supplier for Silicon materials in battery anodes, HPQ Silicon’s efforts align with the US and Canadian governments’ initiatives to establish domestic battery manufacturing ecosystems.

Novacium, HPQ’s France-based affiliate, has acquired patents enhancing anode material performance, particularly in silicon-based Li-ion batteries. With the pressing demand for domestic battery material suppliers, HPQ Silicon’s advancements in engineered SiOx materials position it as a crucial player in meeting the evolving needs of the electric vehicle industry while addressing supply chain vulnerabilities.

GRANT PROVIDES MORE THAN FUNDING – IT PROVIDES 3RD PARTY VALIDATION

In a groundbreaking leap toward transforming the landscape of battery technologies, HPQ Silicon Inc.’s affiliate, Novacium SAS, has been awarded a prestigious €90,000 French Tech Emergence Grant. This grant, administered by the French Bank of Public Investments, reflects not only Novacium’s prowess in “deep tech” projects but also its dedication to advancing the realm of highly engineered SiOx-based anode materials for batteries.

BERNARD TOURILLON CEO OF HPQ SILICON

“Today’s news, which can be considered a big milestone, validates our strategic partnership with Novacium and strengthens our collective position in the global market for reliable, sustainable and innovatively engineered SiOx battery materials.”

SIOX-BASED ANODE MATERIALS FOR BATTERIES

Novacium’s innovative project focuses on revolutionizing the entire value chain of SiOx-based anode materials for batteries, addressing critical challenges in the lithium battery industry. The ongoing SiOx battery tests, anticipated to yield promising results, position Novacium to seek additional deep-tech financing, potentially up to €2 million, propelling their project to a pre-commercial stage.

RIGOROUS SELECTION PROCESS PASSED BEFORE GRANT BY FRENCH BANK OF PUBLIC INVESTMENTS

The grant approval follows a rigorous selection process by the French Bank of Public Investments, validating Novacium’s deep-tech characteristics and its project’s innovativeness and industrial impact in both France, as well as, on a global scale.

Mr. Jed Kraiem, COO of Novacium, notes that the recent recognition from the French government underscores the significant industrial impact of their work, reinforcing the value proposition of their groundbreaking project.

MARKET SIZE FOR ENGINEERED SIOX ANODE MATERIALS IS EXPANDING

As the market for engineered SiOx anode materials expands, Novacium emerges as a key player, with projections indicating a potential demand of 300,000 tons by 2030, valued at an estimated US$15 billion.

A PIVOTAL MOMENT IN THE TRAJECTORY OF SIOX BASED BATTERY MATERIAL

Novacium’s recent achievement and the substantial grant from BPI underscore a pivotal moment in the trajectory of SiOx-based battery materials. With ongoing tests poised to reveal transformative results, Novacium’s commitment to shaping the future of battery technologies is undeniable.

Sit back, relax and watch this powerful interview with Bernard Tourillon, President and CEO of HPQ Silicon Inc. and NOVACIUM SAS.

Posted by AGORACOM-JC

at 9:00 AM on Wednesday, March 27th, 2019

SPONSOR: HPQ-Silicon Resources Inc. (HPQ:TSX-V) A leader in High Purity Quartz Exploration in Quebec and vertically integrated producer of Silicon Metal, Solar Grade Silicon Metal and polysilicon. Learn More.

HPQ: TSX-V

————————-

New Wind and Solar Power Is Cheaper Than Existing Coal in Much of the U.S., Analysis Finds

Coal-fired power plants in the Southeast and Ohio Valley

stand out. In all, 74% of coal plants cost more to run than building new

wind or solar, analysts found.

Not a single coal-fired power plant along the Ohio River will be able to compete on price with new wind and solar power by 2025, according to a new report by energy analysts.

The same is true for every coal plant in a swath of the South that includes the Carolinas, Georgia, Alabama and Mississippi

Nearly three-fourths of the country’s coal-fired power plants already cost more to operate than if wind and solar capacity were built in the same areas to replace them, a new analysis says. Credit: Robert Nickelsberg/Getty Images

Not a single coal-fired power plant along the Ohio River will be able

to compete on price with new wind and solar power by 2025, according to

a new report by energy analysts.

The same is true for every coal plant in a swath of the South that

includes the Carolinas, Georgia, Alabama and Mississippi. They’re part

of the 86 percent of coal plants nationwide that are projected to be on

the losing end of this cost comparison, the analysis found.

The findings are part of a report

issued Monday by Energy Innovation and Vibrant Clean Energy that shows

where the shifting economics of electricity generation may force

utilities and regulators to ask difficult questions about what to do

with assets that are losing their value.

The report takes a point that has been well-established by other

studies—that coal power, in addition to contributing to air pollution

and climate change,

is often a money-loser—and shows how it applies at the state level and

plant level when compared with local wind and solar power capacity.

“My big takeaway is the breadth and universality of this trend across

the continental U.S. and the speed with which things are changing,”

said Mike O’Boyle, a co-author of the report and director of energy

policy for Energy Innovation, a research firm focused on clean energy.

The report is not saying that all of those coal plants could or

should be immediately replaced by renewable sources. That kind of

transition requires careful planning to make sure that the electricity

system has the resources it needs. It also doesn’t consider the role of

competition from natural gas.

The key point is a simpler one: Building new wind and solar power

capacity locally, defined as within 35 miles for the report, is often

less expensive than people in those markets realize, and this is

indicative of a price trend that is making coal less competitive.

This shift shows how market forces are helping the country move away

from fossil fuels. At the same time, coal interests have been trying to

obscure or cast doubt on this trend, while seeking more government

subsidies to slow their industry’s decline.

Coal Concerns in the Solar-Rich Southeast

Nearly three-fourths of the country’s coal-fired power plants already

cost more to operate than if wind and solar power were built in the

same areas to replace them, the report says.

By 2025, with the costs of building wind and solar power expected to

continue to decline, the analysts project that 86 percent of coal-fired

power plants will be more expensive than local renewable energy.

Notably, the 2025 wind and solar estimates assume that expiring federal

tax credits will not be extended, so any price advantage is without

federal credits.

In parts of the country where power plants compete on open markets,

such as most of Texas, companies may be more quick to shut down

money-losing plants because plant owners are the ones bearing the

losses.

It’s different in places where plants are fully regulated, as plant owners can pass extra costs on to consumers.

The Southeast, which is almost entirely regulated markets, has some

of the costliest coal plants and is rich with solar resources.

“Consumer advocates and regulators there should be asking harder

questions about integrating renewables,” said Eric Gimon, an energy

analyst and co-author of the report.

In North Carolina, for example, a state second only to Indiana in

total coal plant capacity, every one of those coal-fired power plants is

“substantially at risk,” meaning the existing plants have operational

costs that are at least 25 percent more than what it would cost to build

wind or solar capacity, the report says.

The state’s largest utility, Duke Energy, has invested in solar. The

report shows that there is room for more of this development, and that

the state remains heavily dependent on coal power that is not

cost-competitive.

Political Opposition in the Ohio Valley

In the Ohio Valley, some of the sunniest parts of Ohio

are near the river in the southern and southwest parts of the state,

areas that now have almost no solar power development. American Electric

Power, a Columbus-based utility, has proposed solar arrays

there, but the plans are running into fierce opposition before state

regulators and it is far from clear that the projects will get approved.

The Ohio Valley is a hub for coal-fired power, with plants that were

built because of proximity to coal mines and the ability to deliver coal

on river barges. And yet, the report shows that most of those plants

cost more to operate than building new wind and solar capacity.

One of the exceptions is the Gavin Power Plant, the largest in Ohio

and one of the largest in the country at 2,600 megawatts, which is

operating at a large enough scale to remain competitive. But by 2025,

even Gavin won’t be able to keep up with the declining costs of wind and

solar, according to the report. This doesn’t mean the plant will be

unprofitable, but it signals a shift in the market that will put

increasing pressure on the plant.

Some Utilities Are Factoring in Climate Impact

Colorado and the St. Louis metro area are two of the few places were

coal plants would retain a cost advantage over new renewable energy in

2025, according to the analysis. The authors say that is because of a

lack of available land to build cost-effective wind or solar within 35

miles and because the plants are close to coal mines, which reduces fuel

costs.

But a purely cost-based analysis leaves out other reasons to shut

down coal plants and build wind and solar, as shown by the largest

utility in Colorado, Xcel Energy, which is doing just that.

The company’s executives said they were responding to reports about

the acceleration of climate change. They have found that they can build

new wind and solar capacity for little or no extra cost, which is a less

precise comparison than in the new report.

And, they are preparing for the possibility that Colorado will pass a

law requiring utilities to shift to 100 percent renewable energy, which

is a priority of new Democratic Gov. Jared Polis.

Distance can also make a difference in cost calculations. If new

resources are built far from the ones they are replacing, grid operators

and utilities need to make sure they have enough power line capacity to

transport the electricity. Also, there are local economic

considerations. Utilities sometimes put new projects in the same metro

areas as ones that are closing to help the local community. This has

been part of Excel’s planning process in Pueblo, Colorado, where it is

closing a coal plant and developing new solar.

Natural Gas Competition Also Plays a Role

The report’s findings about the declining viability of coal plants

are in line with previous studies, including one from March 2018 from

BloombergNEF with the headline “Half of U.S. Coal Fleet on Shaky

Economic Footing.”

But there is a key difference. The BloombergNEF report looked at the

finances of coal plants in the context of competition from all fuels,

including natural gas.

William Nelson, a co-author of the BloombergNEF report, says he is

leery of comparing the costs of building new wind and solar to the costs

of operating existing coal plants because a coal plant is capable of

running around the clock, which makes it a different type of resource

than wind and solar unless there is large-scale battery storage.

And, he thinks that natural gas prices are an essential part of the

conversation in places such as the Ohio Valley, where gas is plentiful

and inexpensive.

Gimon of Energy Innovation says he agrees that the role of natural

gas in the market is an important element, but he says the report

intentionally narrowed the focus to look at the deteriorating finances

of coal and the improving competitiveness of wind and solar, rather than

at the electricity market as a whole.

Daniel Cohan, a Rice University engineering professor who is not

involved in the new report, says “gas is more of a gamble” for power

plant owners than wind or solar because of uncertainty about future gas

prices.

He thinks there is more certainty that wind and solar will continue

to get less expensive and that their prices can serve as a useful

comparison for coal.

The decreasing costs of wind and solar will lead to a growing gap

compared to the costs of operating coal plants, one that coal plant

owners and regulators would be wise to prepare for, Gimon said.

“You really can’t hang tight,” he said. “It’s just going to get worse.”

Tags: Hpq, Solar Posted in HPQ-Silicon Resources Inc. | Comments Off on $HPQ.ca Silicon Resources Inc. – New Wind and Solar Power Is Cheaper Than Existing Coal in Much of the U.S., Analysis Finds

Posted by AGORACOM-JC

at 11:15 AM on Tuesday, March 5th, 2019

Announced the receipt of a progress report from PyroGenesis Canada Inc (TSX Venture: PYR) describing continuous development testing of the pilot plant design and reactor related subsystems of the Silicon Melt Drainage (Tapping) part of the process. Â

Work of the Gen2 PUREVAP™ Commercial Scalability Proof of Concept platform is undertaken in order to minimize the risk of design failure during the pilot plant trials schedule to start mid-2019.

MONTREAL, March 05, 2019 – HPQ Silicon Resources Inc. (HPQ) (TSX VENTURE:HPQ) (FRANKFURT:UGE) (OTC PINK:URAGF) is pleased to announce the receipt of a progress report from PyroGenesis Canada Inc (“PyroGenesisâ€) (TSX Venture: PYR) describing continuous development testing of the pilot plant design and reactor related subsystems of the Silicon Melt Drainage (Tapping) part of the process.  This work of the Gen2 PUREVAP™ Commercial Scalability Proof of Concept platform is undertaken in order to minimize the risk of design failure during the pilot plant trials schedule to start mid-2019.

DRAINAGE OF LIQUID SILICON MELT AT THE BOTTOM OF REACTOR (TAPPING) CRITICAL TO PROCESS

Drainage of silicon (tapping) is one of the most important aspects of

the process. Efforts have been made by PyroGenesis to optimize the

design of the melt drainage subsystems of the pilot plant. In order to

test design efficiency and to generate computational studies to predict

the tapping behaviour of liquid silicon in the Gen3 pilot plant, a few

silicon melting and tapping tests using GEN2 reactor have been conducted

to date.

SIMULATED TAPPING DONE USING GEN2

To simulate the tapping process of the pilot plant unit, the Gen2

reactor was ramped up to operating parameters with a standard mixture of

quartz and carbon introduced at the beginning. Once the reactor

reached operating temperature as-received Si is introduced in the

reactor for effective melting. Once the whole Si mass melted, the tap

hole was opened to drain the liquid metal and the data from the test was

then used to generate computational studies.

Mr. Bernard Tourillon, President and CEO of HPQ Silicon Resources Inc stated: “We are very happy to show our first ever public picture of the Gen2 in action. What these tests demonstrate is the incredible versatility of our Gen2 PUREVAPTM QRR platform, highlighting the advancement being made on the project and toward de-risking the mid-2019, Gen3 commercial scalability testing phaseâ€.

Pierre Carabin, Eng., M. Eng., Chief Technology Officer and Chief

Strategist of PyroGenesis has reviewed and approved the technical

content of this press release.

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

About HPQ Silicon

HPQ Silicon Resources Inc. is a TSX-V listed resource company focuses

on becoming a vertically integrated and diversified High Purity, Solar

Grade Silicon Metal (SoG Si) producer and a manufacturer of multi and

monocrystalline solar cells of the P and N types, required for

production of high performance photovoltaic conversion.

HPQ’s goal is to develop, in collaboration with industry leaders,

PyroGenesis (TSX-V: PYR) and Apollon Solar, that are experts in their

fields of interest, the innovative PUREVAPTM “Quartz Reduction Reactors

(QRR)â€, a truly 2.0 Carbothermic process (patent pending), which will

permit the transformation and purification of quartz (SiO2) into high

purity silicon metal (Si) in one step and reduce by a factor of at least

two-thirds (2/3) the costs associated with the transformation of quartz

(SiO2) into SoG Si. The pilot plant equipment that will validate the

commercial potential of the process is on schedule to start mid-2019.

Disclaimers:

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward-looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Company’s current expectation and assumptions, and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Company with respect to future events and are subject to certain risks

and uncertainties and other risks detailed from time-to-time in the

Company’s on-going filings with the securities regulatory authorities,

which filings can be found at www.sedar.com.

Actual results, events, and performance may differ materially. Readers

are cautioned not to place undue reliance on these forward-looking

statements. The Company undertakes no obligation to publicly update or

revise any forward-looking statements either as a result of new

information, future events or otherwise, except as required by

applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

For further information contact Bernard J. Tourillon, Chairman, President and CEO Tel (514) 907-1011 Patrick Levasseur, Vice-President and COO Tel: (514) 262-9239 www.HPQSilicon.com

Posted by AGORACOM-JC

at 11:39 AM on Wednesday, February 27th, 2019

Announcement today is as a result of a step by step study which was performed to investigate the effect production yield has on the purity of silicon end-product.

Theoretical calculations which were obtained in the previous phase were also validated

In conclusion, it was found that higher production yields actually enhance end-product purity, which confirms our previous calculations.

MONTREAL, Feb. 27, 2019 – PyroGenesis Canada Inc. (http://pyrogenesis.com) (TSX-V: PYR), (the “Company”, the “Corporation†or “PyroGenesis”) a Company that that designs, develops, manufactures and commercializes plasma atomized metal powder, plasma waste-to-energy systems and plasma torch products, announces today its latest testing results for PUREVAP™ Gen2, and provides a general update on its PUREVAP™ Project with HPQ Silicon Resources Inc (“HPQâ€).

This announcement today is as a result of a step by step study which

was performed to investigate the effect production yield has on the

purity of silicon end-product. Theoretical calculations which were

obtained in the previous phase were also validated. In conclusion, it

was found that higher production yields actually enhance end-product

purity, which confirms our previous calculations. Specifically, the

results of this extrapolation calculation indicate that a higher

production yield will enhance the final silicon purity, reaching 99.993%

(+4N) at 90% production yield.

Mr. P. Peter Pascali, President and CEO of PyroGenesis, provides this

update on PUREVAP™ in the following Q&A format. The questions, for

the most part, are derived from inquiries received from investors, and

analysts:

Q. For those that are new to the story, could you please provide an overview of the project and technology?

A. Most certainly.

HPQ is the owner of quartz properties. Quartz can be processed,

through multiple steps, into a high purity silicon metal which is an

important element in solar panels. It helps convert solar energy into

useful electricity. Many in the solar panel industry consider the cost

of converting quartz into solar grade silicon metal to be a limiting

factor in the growth of the solar panel industry.

PyroGenesis was first engaged by HPQ to demonstrate, on a laboratory

scale, that its proprietary PUREVAPTM process could produce high purity

silicon metal from quartz in just one step.

This could be significant to the solar panel industry since the

industry is highly dependent on high purity silicon metal in its solar

panels. Any reduction in the cost of high purity silicon metal would

benefit the industry as a whole, and if significant, could be game

changing.

The primary goal of the PUREVAP™ process is to reduce (i) capital

costs, and (ii) operating costs in the production of high purity silicon

metal. A side benefit of the PUREVAP™ process is that, at the same

time, it can replace polluting conventional processes, with a cheaper

and environmentally friendly alternative by reducing the carbon

footprint of current silicon metal production methods.

Specifically, PUREVAP™â€™s current targets are as follows:

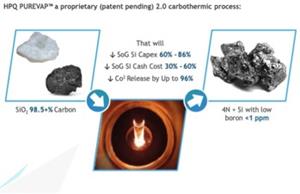

Reduce CAPEX to transform quartz to solar grade silicon by between 60% (China) and 86% (“Rest of the World†or “ROWâ€);

Reduce OPEX to transform quartz to solar grade silicon by between 30% (China) and 60% (ROW);

Reduce carbon footprint to transform quartz to solar grade silicon by up to 96%;

Investigate new opportunities for high value niche applications that could also benefit from cheap high purity silicon.

Q. Where do we stand with the technology?

A. Let us first review the question in the context of what we have achieved to date:

We started this project in early 2016, a little over 2 years ago. By

June 2016, we had already demonstrated PUREVAP™â€™s ability to transform

quartz into high purity silicon metal exceeding 99.9+%, or 3N (3N

reflects 99.9% or 3 Nines). Before moving on let me put 3N in the

context of what we are trying to achieve:

Purity

Grade

Applications

Market Size

98.5-99.5% (1N-2N)

Metallurgical Grade

Feedstream to electronic and solar grade Silicon production

Additive for aluminum alloys

Feedstream to making fumed silica, silanes and silicone

> 2.2M T/yr

99.9 – 99.99% (3N-4N)

High Purity & Special Grade

Powders for batteries

SiAl targets for the glass industry

Industrial quality Si3N4

> 220 kT/yr

> 99.999% (5N+)

Solar Grade

Solar cells

> 400 kT/yr

Table 1

The potential uses of high purity silicon metal is depicted on Table 1

above. This market is typically divided into three broad grades:

Metallurgical Grade (1N-2N), High Purity & Special Grade (3N-4N),

and Solar grade (5N+).

One can see that 3N silicon metal addresses a significant market. As

we are developing a process to produce solar grade silicon metal, we

have discovered a way to produce 3N. To do so on a commercial basis

opens up another revenue stream, and effectively reduces project risk.

Once we demonstrated the ability to transform quartz into high purity

silicon metal, we next needed to demonstrate scalability. This we did

by the beginning of 2017. By this time, we had demonstrated scalability

of the process by increasing production from 1.1g to 8.8g of material.

Later in 2017, by Q3, we estimated that silicon production yield played

an important role on the final purity of the metal produced; PyroGenesis

theoretical calculations, assuming a 100% production yield, concluded

that the purity of the silicon produced, under various operational

conditions could, at commercial scale, range from 3N (99.984 % Si) to 4N

(99.996 % Si) for low purity feedstock, and to 4N+ (99.998 % Si) when

using high purity feedstock. Recent Gen2 tests reported not only confirm

these results, but exceed them and, as such, our baseline has now moved

from 3N+ to 4N+ which, it and itself, is quite noteworthy.

Q. What is the next step?

A. The next step will be the pilot plant where we

expect to produce silicon metal based on the results developed during

the GEN1 and GEN2 lab phase tests.

We are currently designing and building a 50 tonnes per year (TPY)

pilot plant to produce larger quantities of 4N+ silicon, which will then

be upgraded to solar grade silicon, with the ultimate goal of producing

test solar cells. We expect the pilot plant to be completed within the

next two quarters.

Q. Ok, but 4N is still not solar grade. How do you think you can achieve solar grade?

A. This is the interesting part, and one I don’t

think the market fully understands. We are still targeting 6N as our

ultimate goal however, in the interim, HPQ has identified a faster route

to market by the addition of Apollon Solar (“Apollonâ€). Apollon is a

private French company with longstanding expertise in Silicon

Purification and Crystallisation, Solar Silicon, Photovoltaic Cells and

Photovoltaic Modules. Simply put, Apollon is one of the world’s leaders

in renewable energies, and has an expertise in purifying/upgrading high

purity silicon metal even further to obtain solar grade silicon. Of

note, they also have an expertise in producing solar cells. This is a

huge addition to the PUREVAP™ process because it essentially means that

on the way to target 6N, we can use a lower level of purity which could

be further upgraded with Apollon’s expertise, thereby further reducing

overall project risk. In short, the time to market has been

significantly reduced with the addition of Apollon.

Q. What does this mean for PyroGenesis?

A. We are not a charity. We deploy assets for the

benefit of our shareholders, for whom there are many advantages with our

contractual relationship with HPQ. First, we are currently under

contract with HPQ to deliver and operate the pilot plant. Second, we are

entitled to a 10% royalty on all future silicon metal sales. Third, we

have a right of first refusal on the next phases of the project, the

first of which would be a commercial plant at 5,000 TPY (which is

expected to be ordered shortly after the pilot phase). Finally, we

retain the right to use the technology for other applications other than

the conversion of quartz to silicon, opening up new markets and

opportunities for PyroGenesis.

In short, this project is very meaningful to PyroGenesis and its shareholders.

Q. What are the next milestones?

A. These latest results were what we needed before

going flat out with the completion of the installation and commissioning

of the pilot system, which will be the next real milestone. It is

expected that the output from this system will be upgraded by Apollon to

solar grade material which will then be used to produce test solar

cells. We expect to produce our first solar cells made using PUREVAP™

sometime late 2019/early 2020. Shortly after that, a full commercial

plant will be commissioned.

Q. Are there any risks?

A. There are always risks with R&D, as you know,

and there is never a guarantee of success. However, if you ask me

generally about the risk of this project, I can tell you with 100%

certainty that the risks have been significantly reduced in our favor

since we started. We have considerably de-risked the project by doing

extensive tests on GEN1 and further validating our scale-up assumptions

with GEN2. We have gained invaluable experience with GEN2 which we have

implemented in the design of the pilot plant.

Of note, something else the market has not fully understood is that

along the way, we believe we have identified possible commercial uses

for the 3N+ material itself which, as I noted earlier, opens up new

commercial applications, and further reduces project risk.

Q. Do you still feel this technology will work?

A. I have said this before and I will say it again,

PyroGenesis does not have time or money to waste on projects that do not

have future potential. Each and every day PyroGenesis has to decide

where to allocate its resources, the most important of which is its

time. Plasma expertise, such as ours, does not grow on trees and we must

be very discerning as to where we dedicate this valuable resource. Do

we dedicate it to Additive Manufacturing (powders for 3D printers),

DROSRITETM, other development projects…or HPQ? The profit from the HPQ

relationship does not, in and of itself, justify dedicating such scarce

resources to the project. However, the royalty from the success of the

project, does.

So, to answer your question, yes, we are fully committed to its

technology, and believe more than ever before that it will be game

changing in its own right.

Talk is cheap, but as you can see, we currently hold over 21M common

shares plus over 17M warrants in HPQ. You can’t get more committed than

this.

Q. What would you advise investors?

A. Do your due diligence. Invest with full understanding, and…follow the money.

PyroGenesis Canada Inc., a TSX Venture 50® high-tech company, is the world leader in the design, development, manufacture and commercialization of advanced plasma processes and products. We provide engineering and manufacturing expertise, cutting-edge contract research, as well as turnkey process equipment packages to the defense, metallurgical, mining, advanced materials (including 3D printing), oil & gas, and environmental industries. With a team of experienced engineers, scientists and technicians working out of our Montreal office and our 3,800 m2 manufacturing facility, PyroGenesis maintains its competitive advantage by remaining at the forefront of technology development and commercialization. Our core competencies allow PyroGenesis to lead the way in providing innovative plasma torches, plasma waste processes, high-temperature metallurgical processes, and engineering services to the global marketplace. Our operations are ISO 9001:2015 certified, and have been since 1997. PyroGenesis is a publicly-traded Canadian Corporation on the TSX Venture Exchange (Ticker Symbol: PYR) and on the OTCQB Marketplace. For more information, please visit www.pyrogenesis.com.

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward- looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Corporation’s current expectation and assumptions and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Corporation with respect to future events and are subject to certain

risks and uncertainties and other risks detailed from time-to-time in

the Corporation’s ongoing filings with the securities regulatory

authorities, which filings can be found at www.sedar.com, or at www.otcmarkets.com. Actual

results, events, and performance may differ materially. Readers are

cautioned not to place undue reliance on these forward-looking

statements. The Corporation undertakes no obligation to publicly update

or revise any forward- looking statements either as a result of new

information, future events or otherwise, except as required by

applicable securities laws. Neither the TSX Venture Exchange, its

Regulation Services Provider (as that term is defined in the policies of

the TSX Venture Exchange) nor the OTCQB accepts responsibility for the

adequacy or accuracy of this press release.

Solar shines brightest for renewables-keen investors

Institutional investors surveyed by the Octopus Group have ranked grid-scale solar power as their top deployment target, amid plans to inject US$210 billion in the broader renewable sector within five years.

A poll of 100 names published by the firm on Monday found 43% of those managing a portfolio of renewables were invested in solar, ahead of firms invested in onshore and offshore wind (28% each), hydropower (27%) and waste-to-energy and biomass (an aggregate 24%).

Institutional investors ranked uncertainty with energy prices as a top obstacle (Source: Karnakata Tata)

Institutional investors surveyed by the Octopus Group have ranked

grid-scale solar power as their top deployment target, amid plans to

inject US$210 billion in the broader renewable sector within five years.

A poll of 100 names published by the firm on Monday found 43% of

those managing a portfolio of renewables were invested in solar, ahead

of firms invested in onshore and offshore wind (28% each), hydropower

(27%) and waste-to-energy and biomass (an aggregate 24%).

Of the respondents – a mix including pension funds, insurers and

banks with US$6.8 trillion in combined assets under management –

Australians (63%) were keenest on solar, followed by EMEA (58%), Asian

(45%) and UK firms (29%).

The industry was the most sought-after also among firms currently not

invested in renewables, although some appeared sceptical. Some 58% of

those managing a renewables-free portfolio claimed to be considering

solar plays, while 21% were not contemplating it and another 21% felt

unsure.

Five years to unlock US$210 billion

Even as they singled out grid-scale solar as their top target, the

polled investors promised to scale up allocations to all forms of

renewables, with US$210 billion set to be deployed within five years.

Private banks appeared the most ambitious, sharing plans for renewables

to represent 9.7% of their portfolios over the period. They were

followed by strategic investors (8.9%) and pension funds (7.8%), while

high-net-worth individuals and family offices (5.5%) and insurers (4.7%)

were the most reluctant.

The Octopus survey evidenced the renewables momentum won’t be

challenge-free, though. Energy price uncertainty, liquidity challenges

and skills shortages ranked as the top concerns for the polled

investors, although costs and regulatory barriers were also seen as

obstacles.

Europe before its subsidy-free hour

The Solar Finance and Investment conference held in London in late

January identified investors as the key enablers of subsidy-free solar

in Europe. Corporate PPAs and other emerging arrangements are easing –

although not fully dispelling – investors’ unease around merchant risks

and potentially low returns, it was argued.

The Octopus poll placed the continent as the most in-demand

destination for renewables investors. Of the top 10 countries and

region, only Australia (seventh) and Japan (10th) were non-European.

The survey produced a finding likely to be welcomed by subsidy-free

players. Almost one-in-two institutional investors piling into clean

energy worldwide was driven by stable cash flows (a driver for 48%) and

attractive risk-adjusted returns (40%); only diversification and ESG

considerations placed higher.

Posted by AGORACOM-JC

at 9:25 AM on Thursday, January 24th, 2019

MONTREAL, Jan. 24, 2019 — HPQ Silicon Resources Inc. (HPQ) (TSX-V “HPQâ€) is pleased to provide investors this corporate overview of the milestones attained since our 2014 entry in the Quartz exploration business and our 2015 decision to become a vertically integrated producer of Solar Grade Silicon Metal through the development of the PUREVAP™ Quartz Reduction Reactor (QRR). Shareholders and prospective investors are encouraged to review the following information in its entirety to understand the progress made and plans being implemented to transform HPQ into the lowest cost and greenest producer of Solar Grade Silicon Metal, as we commence 2019 with the final assembly of the PUREVAP™ Pilot Plant, “Gen 3†and it’s mid 2019 start-up.

Mr. Bernard J. Tourillon, President and CEO of HPQ-Silicon provides

his responses in the following Q&A format. The questions, for the

most part, are derived from inquiries received from investors,

investment professionals and industry participants. A table summarizing

the Purevap™ milestones appears on page 2 of this summary:

Q. To start,could you please briefly describe the focus and objectives of HPQ going forward?

A. Most certainly. Following the successful closing

of our $ 5,250,000 Financing in August 2018 and the December 2018

completion of our Beauce Gold Field assets spinout, HPQ is now entirely

focused on becoming a vertically integrated producer of solar grade

silicon metal. In 2019, we intend to:

Use our 50 tpa (tonnes per year) Pilot Plant, developed by our

partners PyroGenesis Canada Inc. (“PyroGenesis†or “PYRâ€), to

demonstrate the commercial potential of the PUREVAPTM “Quartz Reduction Reactors†(QRR)

process (patent pending), and its ability to convert Quartz (Silicon

Dioxide or SiO2) into High Purity Silicon Metal of 99.9% to 99.99% Si,

(referred to as 3N and 4N, respectively) in just one step;

Use the material produced by the Pilot Plant to finalize the best metallurgical pathway (UMG) to upgrade “HPQ PUREVAP™ Siâ€

(Silicon Metal) to Solar Grade Silicon Metal (SoG Si), through

collaboration with PYR and Apollon Solar (“Apollonâ€), and in doing so

becoming the world’s leading Low Cost, Low Carbon Footprint producer of

SoG Si;

HPQ expects to confirm that PUREVAPTM and UMG processes will:

Reduce CAPEX to transform Quartz to SoG Si by between 60% (China) and 86% (“Rest of the World†or “ROWâ€) 1;

Reduce OPEX to transform Quartz to SoG Si by between 30% (China) and 60% (ROW)1;

Reduce the Carbon Footprint to transform Quartz to SoG Si by up to 96%2;

Investigate new opportunities for high value niche applications that need the High Purity Silicon Metal that our PUREVAPTM QRR produces in one step.

Q. Could you please briefly describe what started HPQ

interest in becoming a vertically Integrated Producer of Solar Grade

Silicon metal?

A. Well, the short answer is: “Necessity is the

Mother of Inventionâ€. The long answer is that in 2014 HPQ had a number

of gold properties that contained extensive quartz veins with which gold

is typically associated. Quartz (Silicon Dioxide or SiO2) is the key

ingredient required for making Silicon Metal (Si).

Silicon Metal (Si), is one of today’s key strategic metals, like

Lithium and Cobalt, that is needed to fulfil the renewable energy

revolution presently under way.

By early 2015, HPQ management came to the realization that in order

for HPQ to succeed in the Quartz business, HPQ needed to transform its

low value quartz resources into a higher value material, Silicon Metal,

and ultimately Solar Grade Silicon Metal (SoG Si), which is a higher

purity form of Silicon Metal that allows the transformation of the sun’s

energy into electricity in photovoltaic (PV) modules.

In short, we needed to find a pathway to become a vertically

integrated producer of Si, and preferably SoG Si. That is when we

discovered PyroGenesis.

Q. Ok, its one thing to say “HPQ wants to become a

vertically integrated producer of Solar Grade Silicon metal†but

implementing is another. Could you please describe what makes the HPQ

plan unique?

A. Certainly. From the start we knew that HPQ could

not afford the time or money required to assemble a world-class

technical team with Silicon Metal (Si) or Solar Grade Silicon Metal (SoG

Si) expertise. To reach our goal, our choices were either a)

collaborate with a university, knowing that it would take years just to

pass the proof of concept phase, or b) outsource our R&D with a

technological partner that possesses proven expertise with high

temperatures processes, and a track record of successfully taking new

concepts, from the lab to commercialization phase.

During 2015, HPQ concluded that to convert our Quartz into Si, and

possibly SoG Si, we needed to convince PyroGenesis Canada Inc

(“PyroGenesisâ€), with their vast expertise on high temperature plasma

base processes, to partner with us.

PyroGenesis has an impressive track record of successfully taking new

concepts from the lab to commercialization, including but not limited

to, the following:

The US Navy, developing the PAWDS™ technology from lab scale to

finally being specified in the design of the new US Aircraft Carriers,

Plasma atomization for 3D printing;

More recently with the deployment of their DROSRITE™ technology.

PyroGenesis expertise is of such high level that:

In addition to the US Navy, during the last 2 months, PyroGenesis

has concluded exclusive partnerships with two multi-billion

conglomerates to commercialize specific applications they have

developed, from lab to commercial scale, on a global basis.

In 2015, HPQ’s Board of Directors accepted a testing proposal from

PyroGenesis regarding laboratory scale, proof of concept, metallurgical

testing of the PUREVAPTM QRR. The proposed program was to

validate its capacity to produce high purity silicon metal from HPQ

quartz in just one step (September 30, 2015 release).

In June 2016, the first successful lab scale tests were completed and

by test #6, results confirmed the game changing potential of the PUREVAPTM QRR process.

HPQ immediately approached PyroGenesis regarding additional testing

and the development of a pathway to building a pilot plant that could

validate the commercial scalability of the process as quickly as

possible. As they say, the rest is history.

Q. What motivated HPQ to move so fast to validate the commercial scalability of the PUREVAPTM QRR process?

A. The decision was simple; the first bench test

showed all equipment and data analyzers worked. By test #6, not only

did the system operate as designed, but also the PUREVAPTM QRR

process was already reaching its first major milestones, the ability to

transform quartz into high purity Silicon Metal (Si) exceeding 99.9+% Si

“3N†(June 29, 2016 release).

HPQ and PyroGenesis came to an agreement whereby HPQ would invest

100% of project costs for 90% of the revenues to be generated by

PUREVAPTM QRR and, with that, HPQ obtained the participation of a world

class technical team to work on our project of becoming a vertically

Integrated producer of Solar Grade Silicon Metal (SoG Si).

Fundamentally, the agreement allows both Parties to reap the rewards of

the new process to make High Purity Silicon Metal (Si) and eventually

SoG Si using HPQ Quartz and the PyroGenesis PUREVAPTM QRR.

On August 2, 2016, PyroGenesis and HPQ announced the terms under which HPQ would invest the funds and own the PUREVAPTM QRR’s

Intellectual Property3 (August 2, 2016 release), with PyroGenesis

taking responsibility for the bench testing, process design,

fabrication, assembly, and cold commissioning of the Pilot Plant.

Q. In your press releases you refer to Gen 1 and Gen 2 can you please describe Gen 1 and the testing milestones?

A. As we outlined above, the project started in 2015

with PyroGenesis’ technical team designing and building a laboratory

scale proof of concept PUREVAPTM QRR, the Gen1 reactor.

The Gen1 PUREVAPTM QRR laboratory scale equipment completed

15 tests between March 29th and July 22th 2016 under the scope of the

“Phase 1 – Proof of Concept Metallurgical Tests Programâ€. These tests

confirmed that the PUREVAP™ QRR concept of combining different

known steps into a one step process works at lab scale. With this

milestone achieved, we then agreed to expand our collaboration to go all

the way to Pilot Plant.

In September 2016, while initial Pilot Plant design was underway, HPQ

also ordered a new series of lab scale R&D tests using the Gen1 PUREVAPTM QRR

to provide invaluable input toward the design of the pilot plant, as

well as, determine the most efficient way of scaling up the PUREVAPTM QRR process to commercial scale production.

In November 2016, another key milestones was reached as Gen1 testing

results demonstrated that the PUREVAP™ QRR was capable of using SiO2

feed material below minimum industry specifications to produce Silicon

Metal (Si) of greater purity than what could be achieved by traditional,

status quo processes used to make Metallurgical Grade (98.5% to 99.5% Si) Silicon Metal4 today.

By the end of January 2017, in tests using a modified and expanded

Gen1 PUREVAP™ QRR reactor, the yield increased from less than 0.1 g to

8.8 g (test #32), an increase of approximately 9,000% (roughly one

hundred-fold), thereby confirming the potential scalability of the

process.

Ongoing work to the end of Q2 2017 validated our systematic and

methodical approach to the project and allowed PyroGenesis to advance

the detailed engineering and design of the pilot plant.

By the end of Q2 2017, it was clear that the Gen1 PUREVAP™ QRR had

reached its maximum usefulness so the decision was made to build a Gen2

PUREVAP™ QRR, pushing the design envelope of the lab scale system to a

point that will allow it to be operated in a semi-batch mode to increase

Silicon Metal (Si) yields. This would provide further insight into

process improvements needed for the Pilot Plant, thereby saving millions

of dollars in future development work.

Q. Now during 2017 you announced an agreement with

Apollon Solar, can you diverge a bit and tell us how that came about,

and the impact?

A. In 2017, we attracted the attention of Apollon

Solar SAS, (“Apollonâ€). This is significant because Apollon is a private

French company with longstanding expertise in Silicon Purification and

Crystallisation, Solar Silicon, Photovoltaic Cells and Photovoltaic

Modules. The team at Apollon has become one of the world leaders in the

development of processes to refine Solar Grade Silicon Metal “SoG Si

UMGâ€. They achieved, an independently confirmed, world record

conversion efficiency of 21.1% with a monocrystalline ingot, for a solar

cell made with 100% “SoG Si UMGâ€.

Apollon first completed a technological audit of the Gen1 PUREVAP™

QRR results to evaluate the potential of the innovative PUREVAP™ QRR

process. They concluded that successful commercial scaling-up of the

PUREVAP™ process could lead to the production of solar quality silicon

at a significantly lower cost compared to those of competing process

technologies (examples include Siemens chemical process, Elkem Solar,

Silicor Materials, etc.).

As a result, in December 2017, HPQ and Apollon announced the signing

of a consultancy agreement whereby Apollon agreed to transfer knowledge

it has acquired in solar silicon over the last 20 years for the benefit

of HPQ and PyroGenesis.

Q. That’s all very exciting, now can you discuss Gen 2 and the commercial scalability of the PUREVAPTM QRR process?

A. The Gen2 PUREVAP™ QRR incorporates important

process modifications identified during Gen1 testing and is designed to

be a scale replica of the planned larger pilot plant (Gen3 PUREVAP™

QRR). In Q2 of 2017 we set about constructing the newly redesigned

reactor while awaiting the final report from the Gen1 work. In Q4, as

Gen2 was being finalized, HPQ received a final report on the Gen1

PUREVAP™ QRR testing and we learned that:

The highest silicon tested for bulk purity was produced in test #75 and measured 99.92% Silicon Metal (Si)5.

Si yield could be increased by increasing production yield, which had been constrained around an average of about 3% in Gen1.

Theoretical calculations indicated that purity of the Si produced

under various conditions could range from 3N (99.984 % Si) to 4N (99.996

% Si) with the addition of volatilization agents for low purity

feedstock, to over 4N (99.998 % Si) when using high purity feedstock5.

These results were incorporated into Gen2 and, by November 2017, the

Gen2 PUREVAP™ QRR was operational, allowing the de-facto start of the

pilot plant testing and commissioning, thereby reducing the risk profile

of the project and allowing additional process modifications and

further proof of commercial scalability work to be done in parallel with

major plant fabrication, to keep advancing work.

JANUARY 2018

PyroGenesis confirmed that the Gen2 PUREVAP™ QRR was operating as

designed and yielding results that were in line with expectations. By

this time, we had also arranged monthly meetings with Apollon and

PyroGenesis to benefit from the backend expertise of Apollon in our

ongoing test work as we continued to plan for the Gen3 Pilot Plant

design.

Gen2 PUREVAP™ demonstrated it could be operate and perform under the

conditions demanded for optimum operational parameters to produce the

purities required in one step. Again, this was another major milestone

because, to our knowledge, there is no other process that does this in

the world.

With the main design and equipment performance characteristics reached, significantly increasing the Yield6 and the Production Yield7 of the Gen2 PUREVAP™ became the next key objectives in contributing to final purity.

FEBRUARY 2018

By mid February 2018, the Gen2 PUREVAP™ was proving to be an

invaluable bench test platform and the results were used to scale back

on the size of the planned Pilot Plant from 200 tonnes per year to 50

tonnes per year. This had a massive benefit on our planned costs,

timing, and on locating the Pilot Plant test site – right inside the

PyroGenesis testing facility, another huge cost saver.

By the end of February 2018, the Gen2 reactor was operating within

the 90th percentile of its achievable production yield. By mid April

2018, as a direct result of continuous process improvements done by

PyroGenesis, Gen2 PUREVAP™ test #14 attained Yield and Production Yield

numbers that surpassed theoretical expectations. The total mass of

Silicon Metal (Si) produced (yield) during test 14 was 101.45 gr; and

conversion of material, referred to as Production Yield, of 34.3%, the

highest to date.

APRIL 2018

PyroGenesis completed a scheduled audit of the Gen2 PUREVAP™

equipment for wear and tear following test#14. The audit was needed to

help identify critical operational parameters for the PUREVAP™ Pilot

Plant and allowed the evaluation of additional design modifications that

could be implemented for further tests using the Gen2 PUREVAP™.

JULY 2018

By the end of July 2018, the Gen2 PUREVAP™ equipment had been

refurbished, re-assembled and modified to incorporate the latest design

modifications and was ready to start a new series of at least 8

additional tests focused on:

Continuing to optimize conditions for the Gen2 PUREVAP™ and the planned Gen3 PUREVAP™ Pilot Plant operation;

Increasing the Yield and the Production Yield;

Testing the Purity range of the Silicon Metal (Si) from low purity

feed stock (98.84% SiO2) and ultra high purity feed stock (> 99.9%

SiO2), analyzed using ICP-OES8;

Q. It sounds like Gen2 is giving great results and

contributing to the Pilot Plant final parameters. You mentioned CO2

(“Greenhouse Gas†or “GHGâ€) reductions as another positive feature of

the PUREVAP™ process can you elaborate on that?

A. Yes we are very excited about this aspect of the project. First, readers must understand that: “It’s

not because photovoltaic solar panels do not emit CO2 (GHG) while

producing electricity that solar energy is not a significant source of

GHGâ€.9 In fact solar power has its greenhouse gas issues that lurk

behind the scenes. Seventy percent (70%) of the GHG generated when

building a new solar farm10 comes from the production of the Solar Grade

Silicon Metal (SoG Si) needed for the fabrication of the solar panels.

Manufacturing SoG Si in China, the world’s largest producer,

generates an astounding 141 kg of CO2 per kg of SoG Si produced. In

Germany that ratio is reduced to 87.7 kg CO2 per kg of SoG Si produced.

What we see is that solar power is not that panacea of low carbon if one

looks at the entire process from start to finish.

96% REDUCTION IN CARBON FOOTPRINT – OPPORTUNITY TO RESOLVE SOLAR PARADOX

In August 2018, PyroGenesis prepared a report11 that found that the

PUREVAPtm QRR process operated in Quebec should only produce 5.4 kg CO2

per kg of SoG Si produced, a 96% reduction in the carbon footprint

compared to existing processes. This is why we are so excited about this

“green†opportunity revolutionizing the solar energy industry.

Q. Technically it sounds like great progress is being made, how is HPQ set financially today?

Thanks to these new financings HPQ, in collaboration with its

technical partners, will now be able to dedicate its efforts and

energies toward the fulfilment of the ambitious commercial validation of

the PUREVAPtmQRR process and the production of Solar Grade Silicon Metal (SoG Si) at the Pilot Plant level.

Q. Sounds like you have the financing under control. You

mentioned at the onset that HPQ and partners are targeting a Pilot

Plant, with bench test work well in hand and financing complete, can you

give a status update of the Pilot Plant that you are now referring to

as Gen3?

As of the date of this corporate update, the Gen2 PUREVAP™

equipment is still being used by PyroGenesis to test different

operational conditions in order to gain more information about future

Gen3 PUREVAP™ operation and testing is also ongoing to find new ways of increasing the Yield and the Production Yield of the Gen2 PUREVAP™.

Finally, a new progress report on the test results completed in 2018 with the Gen2 Purevap should be ready soon.

Q. How transferable are the results obtained from Gen2 to the pilot plant?

A. We believe they are very transferable. In fact,

we expect the results to be even better at larger scale. By increasing

the scale, we are increasing the production rate. As you can imagine, we

are already extremely excited about the results we have had with Gen2,

and at a larger scale, the production rate is automatically higher

which, as we have already proven with Gen1, should lead to a higher

conversion yield and better purity.

Q. HPQ has started talking about using a metallurgical process to transform the Si produced via the PUREVAPTM QRR to produce SoG Si. Is this just a semantic change or is HPQ changing its objectives?

A. It is more semantic than anything else; the

project is advancing towards meeting our stated objectives when we

started it in 2015:

“The “PUREVAP ™ Quartz Reduction Reactor is a proprietary process

that uses a plasma arc within a vacuum furnace. This unique technology

should allow HPQ (Uragold then) to convert its (…) Quartz Projects into

the highest purity, lowest cost supplier of Solar Grade Silicon Metal

(…) to the solar industry.

But this may be a good opportunity to explain in detail what makes the PUREVAPtm QRR such a game changing technology and why we have started to refer to it as a “Second Generation (2.0) Carbothermic processâ€.

Presently, using the status quo to produce Solar Grade Silicon Metal

(SoG Si), you first need to transform Quartz (Silicon Dioxide or SiO2)

into Metallurgical Grade Silicon Metal (MG Si) and then the MG Si needs

to be further purified produce SoG Si.

PRESENT LEGACY CARBOTHERMIC PROCESS

The first step in making SoG Si involves mixing Pure Quartz (99.5%+

SiO2), Low Ash Carbon and Wood Chips and heating the mixture to very

high temperatures in an electric arc furnace to create the Carbothermic

process required to reduce the SiO2 to Metallurgical Grade Silicon Metal

(MG Si).

The traditional smelter process to make MG Si requires six (6) tonnes

of raw material to produce one (1) Tonne of Silicon Metal (Si).

By its design, the impurities contained in the raw material end up

being concentrated in the final product, that is why traditional

smelters need (99.5%+ SiO2) to produce 98.0% Si.

The maximum purity that can be attained in traditional smelters is

around the 99.5% Si threshold, but that requires additional post

treatments. On average these postproduction processes can increase the

purity of the MG Si by a factor ranging from ½ N to 1 N.

For Silicon Metal (Si) to be used in the Solar and High Tech

Industries, higher purity levels than what can be attained by standard

carbothermic reduction are required. Presently, less then twenty

percent (20%) of MG SI produced by smelter meets the demanding feedstock

purity specs required for the different additional purifications steps.

CHEMICAL DISTILLATIONS PROCESS (Siemens)

Chemical distillations process (Siemens process) to purify MG Si to

purity required for Solar Grade applications or electronic applications

has become the gold standard, with over 95% of the world SoG Si produced

through chemical distillations, even with it negative environmental

footprint.

Producing SoG Si (Polysilicon) via chemical distillations requires

between 72,000 KWh/T up to 120,000 kWh/t and as the term clearly

indicates chemical distillation implies that further refinement involves

the use of harsh chemicals like hydrochloric acid, and the final

products include liquid silicon tetrachloride and polysilicon. Each ton

of polysilicon is manufactured at the cost of three to four tons of

these hazardous by-products. When silicon tetrachloride is exposed to

water it releases hydrochloric acid, which causes acidification of soil

as well as the emission of toxic fumes.12

For many years, companies have been searching and investing funds

looking for a metallurgical alternative to Chemical distillations

process to transform MG Si into SoG Si.

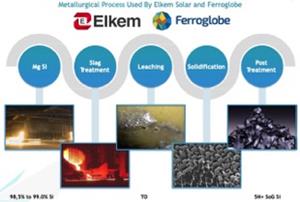

Two groups, Elkem and Ferroglobe have been able to demonstrate, at

commercial scale, the technical viability of using metallurgical process

to further purify what is essentially 2N MG Si (99.0% Si) into a 5N+

SoG Si (UMG) that can be used to produce solar cells that deliver

efficiencies and yield ratios which compare very favourably with

photovoltaic industry benchmarks.13

The main advantage of a metallurgical process is the low operational

cost, (for each individual step and total) combined with lower energy

consumption for producing the UMG SoG Si (35,000 kWh/t versus a minimum

of 72,000 KWh/t).

The biggest drawback of this process and the reason why, until now,

it has not become the industry standard is that the CAPEX cost

associated with every operational step (Slag Treatment, Leaching,

Solidification and Post Treatment) are high, due to size and capacity

needed to purify what is essentially 2N MG Si (99.0% Si) into a 5N+ SoG

Si (UMG).

The fact that the operational cost saving are marginal on relative

term while the CAPEX (Cost per kg of annual capacity matrix) associated

with a complete metallurgical process to make UMG SoG Si is equivalent

to the CAPEX (Cost per kg of annual capacity matrix) of building a

chemical distillation process (Siemens) plant, is the only reason why

metallurgical processes to make UMG SoG Si have not become mainstream in

the industry.

Q. Now that is all very interesting, but if big companies

like Elkem and Ferroglobe have not been able to make metallurgical

processes work, why should we believe that HPQ with it’s PUREVAPTM QRR can?

A. It really comes down to big corporate culture.

Our approach to the problem is disruptive; we are not looking at

tweaking existing process to transform Quartz (Silicon Dioxide or SiO2)

to Metallurgical Grade Silicon Metal (MG Si) or developing a new process

that will be more efficient at removing the impurities from MG Si to

produce Solar Grade Silicon Metal (SoG Si). We are looking for a new

pathway of reducing Quartz (Silicon Dioxide or SiO2) to Solar Grade

Silicon Metal (SoG Si) by developing the PUREVAP™ QRR a “Second Generation (2.0) Carbothermic processâ€.

Imagine a young engineer walking into a meeting and telling his

bosses that the billions of dollars invested in the technology assets of

the company should be scrapped for a brand new concept. Those bosses

grew up, as it were, on the existing technology. There is no way that

is going to happen, so big corporations spend all their effort tweaking

the existing process.

It takes an upstart that is unencumbered with this corporate culture

to bring about change. Examples include Microsoft with IBM, Tesla and

GM, as simple examples of this concept.

This is what we are working on accomplishing and we believe that the PUREVAPtm QRR is that game changing disruptive technology for Solar Grade Silicon Metal.

Q. Ok, its one thing to say: the PUREVAPTM QRR is a game changing disruptive technology, but why and more important when will HPQ be in a position to demonstratethat the project is truly advancing toward that tipping point?

A. We, HPQ and technical partners PyroGenesis and Apollon Solar, have identified the following reasons why the PUREVAPtm QRR process will become the game-changing technology that could revolutionize the solar energy industry:

Using metallurgical process to purify 2N MG Si (99.0% Si) into a 5N+ SoG Si (UMG) is technically feasible;

The costs (CAPEX and OPEX) of removing, with metallurgical

processes, multiple N of impurities from MG Si to produce 5N+ SoG Si

(UMG) are prohibitive and make these process not financially feasible at

present;

Increasing by one (1) or better yet two (2) N the purity of the

Silicon Metal (Si) produced during the carbothermic phase of converting

Quartz (Silicon Dioxide or SiO2) to Si, for the same (CAPEX and OPEX)

costs as traditional smelters incur to produce 2N MG Si (99.0% Si),

should generate significant reductions of (CAPEX and OPEX) costs to make

UMG SoG Si;

This is what our Gen1 PUREVAPtm QRR results indicated should happen at commercial scale, and that is what the Gen3 PUREVAPtm QRR was built to demonstrate at commercial scale.

So, during 2019, as the Gen3 PUREVAPtm QRR pilot plant

confirms the key working hypothesis of the November 2017 Gen1 based

theoretical calculations is working at commercial scale, is when we expect to start receiving inquires from players in Silicon Metal and Solar Grade Silicon Metal industries.

If we can demonstrate a capacity to produce, in one step, a Silicon

Metal (Si) with a purity that range from 3N+ to 4N+ from low purity

Quartz (Silicon Dioxide or SiO2) feedstock, interest may also come from

Solar players, since we would be starting to validate our claim that our

PUREVAPtm QRR and UMG process will be the cheapest and greenest way to produce SoG SI in the world.

This does not mean that they are not looking at what we are doing,

“au contraireâ€â€¦ But presently, we are attracting mostly interest from

industry participants that have invested significant funds developing

Quartz resources looking for ways of increasing the economic model of

their projects.

Finally, shareholders and prospective investors would be wrong to

assume that nothing will happen until then. As stated above, the Gen2

PUREVAP™ equipment is still being used to test different operational

conditions in order to gain more information about future Gen3 PUREVAP™

operations and testing, to find new ways of increasing the Yield and the

Production Yield of the Gen2 PUREVAP™.

A new progress report on the test results completed in 2018 with the Gen2 Purevap should be ready soon.

Q. With Solar Energy Prices now at Parity with Natural Gas and Coal, is there still a need for a new process like thePUREVAPTM (QRR)?

A. Yes, actually more than ever, as the size and

speed of future investment in renewables energy is dependent on an

ever-declining cost per watt model going forward, while the GHG concerns

are becoming more challenging to governments and industry.

Over the last 40 years, solar energy innovations, financed mostly by

government incentives, have allowed solar energy prices to reach parity

with most fossil fuels today14. While this type of approach has

generated phenomenal success regarding the cost per watt matrix, this

approach is also responsible for phenomenal long term and short term

market dislocation.

One of the most important dislocations is related to the costs (CAPEX

and OPEX) of making Solar Grade Silicon Metal (SoG Si). Process

improvements for making SoG Si have plateaued while returns for

producing SoG Si are vanishing for investors, making financing of new

high purity silicon capacity using old processes to turn MG Si into SoG

Si difficult. HPQ solves this problem.

As figures 5 and 6 demonstrates, without new processes (like the

PUREVAPTM QRR) that can bring about a new leg down in the cost (CAPEX

and OPEX) of making SoG Si, this situation will either lead to

production bottlenecks and potential shortage of SoG Si to meet demand.

As with all commodities, this will result in a surge in the price of

silicon, causing an unexpected increase in the price of solar energy.

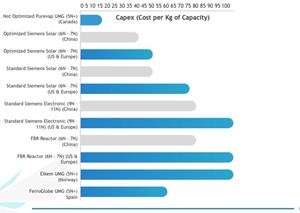

CAPEX reduction as it pertains to the cost of making SoG Si have

plateaued around the US $35 Cost per Kg of annual Capacity in China and

US$ 50 Cost per Kg of annual Capacity in the Rest of the World.

Figure 5 clearly demonstrates the disruptive Capex potential (US$) of the PUREVAPTM QRR process.

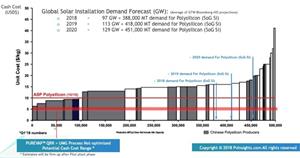

Figure 6 for its part demonstrates that, even in 2018, the cost curve

for SoG SI suggests that reductions in the OPEX costs had now plateaued

and that a longâ€term SoG Si price below USD 14/Kg is simply not

feasible. It is clear that to break this plateau, new processes like

the PUREVAPTM QRR will need to reach commercial viability.

Q. According to a specialized publication15, Solar Grade Silicon Metal (SoG Si) consumption should decline to 3g/W by 2022, from 4g/W in 2018, how will this new reality affect HPQ Business Model?

A. My answer may sound counter intuitive, but HPQ sees this as a

positive factor for our PUREVAPTM QRR + UMG project going forward. The

effect of the decline will negatively impact mainly the highest cost

producer, but a new process that can cut CAPEX and OPEX costs as much as

our PUREVAPTM QRR + UMG project appears to be on the threshold of

doing, will definitively benefit the entire industry and future

consumers, possibly leading to the breakout needed to catapult solar

energy ahead of carbon based energy for future generations.

What is important to realize is that demand for SoG Si is a

combination of demand for each new GW of solar energy for the consumer

and the SoG Si consumption needed to produce that new GW.

What is also shown in Figure 6 is the demand need for increased

amounts of SoG Si required to meet the demand growth for solar energy:

2018 was projected at 97 GW @ 4.0 g per W; ≈ 388,000 MT of SoG Si demand;

2019 was projected at 113 GW @ 3.7 g per W; ≈ 418,000 MT of SoG Si demand;

2020 was projected at 129 GW @ 3.5 g per W; ≈ 451,000 MT of SoG Si demand.

Future demand projections for solar energy is such that even at 3.5 g

thresholds, demand for SoG Si in 2020 should exceed the 451,000 MT

mark, and that can be directly related to the fact that Solar Energy

demand grows from its present two percent (2%) market share of the

global electricity generation capacity to the ten percent (10%)

threshold anticipated by 203016.

This translates into a demand in US$ for SoG Si that will grow from US$ 7.1 B in 2018 to over the US$ 11.8 B mark by 202817.

Q. An often-asked question is, how comfortable are you with the patent application?

A. The short answer is: very comfortable. PyroGenesis is leading the

patent application, which is progressing as expected. Given PyroGenesis

vast experience in obtaining patents and their $1,950,000 investment in

HPQ at a premium in August, this question should be put to rest once

and for all.

Q. Some investors/shareholders are skeptical about the whole process. Do you have any comments?

A. Well, they should meet the engineers! Now there is a skeptical

bunch and that is natural with any new process as groundbreaking as

this. Every step of the way has brought its share of challenges but has

also brought about many more positive surprises and developments. This

is the immense competitive advantage HPQ has as a result of bringing

together the engineering brainpower of PyroGenesis and Apollon Solar.

Seriously, we are talking about a process that potentially could be game

changing by several magnitudes. Who wouldn’t be skeptical? You would

have to be a fool not to be. Adding to this is the fact that the

results to date are beyond our expectations, which, in a weird way,

fuels the “too good to be true†skepticism, no? On the other hand, how

many chances do you get to invest into such potential, at 6 cents a

share and market cap of CAD$13 million, when our strategic partner and

the Government have invested CAD$5,250,00 at a Company valuation of

CAD$26 million? Food for thought!

Q. What about the quartz properties? The last we heard about

quartz exploration was in Q4 2017 when you announced a drilling

campaign on the Ronceveaux?

A. We are still fully invested in our 100% owned Martinville and

Ronceveaux quartz properties. However we decided to hold off on quartz

exploration to allocate exploration funds for geophysics and geology

work on the Beauce Gold property.

Now that the spin-off of Beauce Gold Fields is done, we intend to go

back to Martinville and Ronceveaux properties to bulk sample quartz as

test feed for the Gen3 PUREVAP reactor. For the next twelve (12) to

twenty-four (24) mounts our need in Quartz as feedstock is limited to

about 150 MT for 2019-2020.

Q. Ok so you have talk a lot about your plans for the solar

market but in your first answer you mentioned silicon for batteries,

what is that about?

A. From phones to electric cars, batteries play important role for

just about everyone on earth, and Si usage in the batteries space is

increasing. The most promising new type of battery being developed

presently is Lithium Silicon Anode Batteries (Li-Si

Batteries). Researchers have found that by replacing the graphite with

silicon in a standard lithium battery, your drastically improve

performance. Anyone who owns a mobile phone or for that matter, an

electric car, wishes that the battery would charge faster and last

longer.

For everybody involved in this project it has given an appreciation

of silicon metal, and some surprises have included opportunities that

may have an impact on the lithium ion battery industry. We will not

retire the Gen2 reactor as we did Gen1 but we will use it to pursue some

of the interesting ‘accidental outcomes’ from our efforts to develop a

new pathway to make clean energy cleaner and more cost efficient.

Q. Conclusion?

A. There is no other way to say it, our belief that PUREVAP™ process

is going to become a game-changing event that has the potential to

revolutionize the solar energy industry has not waned one bit since we

made our first bold statements in 2015. The project is advancing, the

success we have attained in less than 3 years is spectacular and the

de-risking that has occurred with every successful phase is significant.

In short, all three partners are happy with the progress to date and

stand firmly behind the project. We are more convinced than ever that

we will be successful in having a commercially viable process at the end

of the 2019. Investors need to remember that we are just at the start

of this process and that we have more exciting developments moving

forward then what we have already accomplished to this point. The future

of HPQ is very bright – no pun intended.

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

About HPQ Silicon

HPQ Silicon Resources Inc. is a TSX-V listed resource company

planning to become a vertically integrated and diversified High Purity,

Solar Grade Silicon Metal (SoG Si) producer and a manufacturer of multi

and monocrystalline solar cells of the P and N types, required for

production of high performance photovoltaic conversion.

HPQ’s goal is to develop, in collaboration with industry leaders,

PyroGenesis (TSX-V: PYR) and Apollon Solar, that are experts in their

fields of interest, the innovative PUREVAPTM “Quartz Reduction Reactors

(QRR)â€, a truly 2.0 Carbothermic process (patent pending), which will

permit the transformation and purification of quartz (SiO2) into high

purity silicon metal (Si) in one step and reduce by a factor of at least