Posted by AGORACOM-JC

at 2:39 PM on Monday, December 9th, 2019

SPONSOR: New Age Metals Inc.

The company owns one of North America’s largest primary platinum

group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral

Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an

additional 1,059,000 PdEq Ounces in the Inferred. Learn More.

Palladium eyes $1,900 in record surge, gold firms on trade doubts

Palladium soared to a record just shy of the $1,900 mark on Monday

Gold edged higher as uncertainty over U.S.-China trade talks took center stage ahead of a Dec. 15 deadline for fresh U.S. tariffs.

Autocatalyst metal palladium climbed to an all-time high of $1,898.50 an ounce and was last up 0.19% at $1,881.43.

“Palladium has a very strong fundamental backdrop with supply set to

stay quite scarce and demand growth set to increase,†said Daniel Ghali,

commodity strategist at TD Securities.

Palladium has risen nearly 50% in 2019 on a sustained supply squeeze,

and has constantly been breaking records, despite a weakening global

auto sector. Increasingly stringent emissions regulations globally are

raising the palladium in autocatalysts for gasoline-powered cars and

2020 could see the most number of regulations, Ghali added.

“There is a widespread expectation that (palladium) spot prices are

headed towards $2,000 and the market does currently appear to be in a

one-way street,†INTL FCStone analyst Rhona O’Connell said in a note.

“Even with the (auto) sector under pressure, palladium will be in

deficit for the foreseeable future and the funds are chasing it higher.â€

“The tariff deadline of Dec. 15 is certainly top of everyone’s mind

… The situation is still uncertain, helping gold stay firm,†TD

Securities’ Ghali said. China said on Monday it hoped to make a trade

deal with the United States as soon as possible, as Washington’s next

round of tariffs against Chinese goods is scheduled to take effect on

Dec. 15. Also supporting bullion, equity markets were further pressured

after China’s exports shrank in November.

Markets now await the U.S. Federal Reserve’s two-day meeting starting

on Tuesday for cues on its monetary policy. The central bank is

expected to highlight the economy’s resilience and keep interest rates

on hold in the range of 1.50% to 1.75%.

U.S. investment bank Goldman Sachs said investment demand for gold

would be supported by recession fears and political uncertainty,

forecasting prices at $1,600 an ounce over a three- and 12-month period.

Platinum and silver were up 0.2% at $897.36 and $16.60 an ounce, respectively.

Posted by AGORACOM-JC

at 12:42 PM on Thursday, December 5th, 2019

SPONSOR: New Age Metals Inc.

The company owns one of North America’s largest primary platinum

group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral

Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an

additional 1,059,000 PdEq Ounces in the Inferred. Learn More.

Palladium zooms past $1,860/oz

Palladium was up 0.3% at $1,845.80 an ounce, after hitting a new high of $1,861.71 earlier in the session.

The metal has been breaking records daily since Nov. 25.

“Palladium positioning is slightly counter-intuitive to the price

action, implicitly confirming heavy OTC interest from the long side,â€

INTL FCStone analyst Rhona O’Connell said in a note. “After weak longs

were shaken out in early November another push to the upside is now

approaching resistance from the uptrend.â€

Concerns that supply of the metal used in car exhaust systems could

run out has helped to lift prices by more than 47% this year alone,

despite a weakening auto sector.

Silver shed 0.4% to $16.95 an ounce and platinum gained 0.4% to $903.51.

Posted by AGORACOM-JC

at 2:55 PM on Tuesday, November 26th, 2019

SPONSOR: New Age Metals Inc. The company owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces in the Inferred. Learn More.

Investor demand to create deficit in platinum market in 2019 – WPIC

In its Platinum Quarterly report for the third quarter, the WPIC

updated its supply and demand forecast for the year and released its

initial estimates for 2020

Because of strong demand for exchange-traded products the platinum’s

expected surplus of 345,000 ounces is projected to fall into a 30,000

ounce deficit

(Kitco News) –

Unprecedented investment demand has helped to transform the platinum

market, shifting what was expected to be a surplus market into a small

deficit, according to the latest data from the World Platinum Investment

Council (WPIC).

In its Platinum Quarterly report for the third quarter, the WPIC

updated its supply and demand forecast for the year and released its

initial estimates for 2020. Because of strong demand for exchange-traded

products the platinum’s expected surplus of 345,000 ounces is projected

to fall into a 30,000 ounce deficit.

“The substantial 12% increase in total demand is driven by record ETF

buying, which more than offsets expected demand decreases in the

automotive (-5%), jewelry (-6%) and industrial (-1%) segments and total

supply growth of 2% for full-year 2019,†the WPIC said in a press

release.

According to the report, funds investment demand has driven

platinum-backed ETF holding to one million ounces so far this year; “the

highest seen since physically backed platinum ETFs were launched in

2007,†the report said.

“This ETF buying by large institutional investors, who typically take

2 to 3 year views and positions, reflect the value opportunity they

see; driven by future demand growth potential and constrained supply,”

the WPIC said.

Looking ahead, the council said that they are forecasting a surplus

of 670,000 ounces next year, reflecting a 1% increase in supply and a

10% decrease in demand.

However, Trevor Raymond, director of research with the council, said

that the estimates are fairly conservative and it wouldn’t take much to

push the market back into neutral territory. Raymond added that he

expects investor demand to remain strong.

“You only need two or three funds to increase their platinum holding

to see a repeat of this year,†he said. “The fact that investment demand

has turned the market around so quickly should not be ignored.â€

Along with investment demand, Raymond said that their estimates also

don’t include substitute projections and rising diesel vehicle demand.

With palladium expected to see its ninth consecutive year of supply

deficits, Raymond said that substitution remains an important topic

within the PGM market. He added that he suspects that auto companies are

already using cheaper platinum instead of palladium.

“I think we will start to see signs of substitution within the next 12 to 18 months,†he said.

Raymond added that a bottoming in the European diesel auto market would also be a positive sign for platinum.

“Every 4% increase in market share in the European auto market equals

roughly 100,000 ounces of platinum,†he said. “Auto companies

substituting 4% of the palladium for platinum would equal about 400,000

ounces. If a few factors come together next year the market can easily

become balanced again.â€

As for platinum jewelry demand, which has declined 6% so far this

year, Raymond said that stable higher prices could ignite renewed

interest, especially in China and India, as those markets continue to

deal with near-record high gold prices.

Posted by AGORACOM-JC

at 12:06 PM on Friday, November 22nd, 2019

SPONSOR: New Age Metals Inc.

The company’s Lithium Division has already made significant

acquisitions in Canada and the USA. The company also owns one of North

America’s largest primary platinum group metals deposit in Sudbury,

Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq

Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces

in the Inferred. Learn More.

What role are lithium-ion batteries playing in energy transition?

Lithium-ion batteries have been essential to the mainstream adoption of electric vehicles as part of a larger energy transition.

This has led to an unprecedented surge in the market for lithium-ion

batteries and an even larger spike in supply. Prices have fallen

recently, but demand is expected to continue rising.

Lithium-ion batteries also have potential applications in

utility-scale renewable energy, although they face competition from

newly developed technologies in that arena.

The energy transition has encouraged industries to move from fossil

fuel to renewable energy sources. In doing so, companies have faced

challenges in determining how to store significant amounts of energy for

extended periods of time. This need is especially acute in the electric

car market, which has turned to lithium batteries for energy storage. Demand for lithium

is projected to grow by as much as 20% in 2019 compared to the previous

year, according to Chilean producer SQM, largely because of increasing

investment in and mainstream adoption of electric vehicles.

More traditional technologies, like internal combustion engines, use

energy almost as soon as it is created. Comparatively, electric vehicles

need to store electrical energy for long periods of time before using

the supplies. Lithium-ion batteries, specifically those using the

compound lithium hydroxide,

store energy while taking up less space than other battery

technologies, and their adoption by the mass market has encouraged

innovation in the technologies underpinning the batteries. The impact

and success of lithium-ion battery technology and its potential in the

global energy transition to renewable energy has been recognized on an

outsized scale — the technology’s creators won the Nobel Prize for chemistry in 2019.

Tesla,

the electric car manufacturer owned by Elon Musk, has become a major

player in the American lithium business. Tesla acquired lithium deposits

across the American West while building huge “gigafactories†to mass

produce the batteries. The company’s plans call for the first of these

factories in Nevada to process 25,000 metric tons of lithium hydroxide

per year, and it has a larger footprint than any other building in the

country. Electric vehicle sales

worldwide surged 75% year over year in the first quarter of 2019, even

as the overall global automobile market contracted; regardless of

opinions over the energy transition’s evolution, all of these cars need

batteries.

Although electric vehicles have been the most significant application

of lithium-ion batteries to date in the energy transition, lithium

could also make renewable energy sources more viable for utilities.

Whereas traditional fossil fuel power plants constantly produce energy,

renewables like solar and wind can only produce energy while the sun is

shining or the wind is blowing. To ensure that the power grid works

constantly, regardless of external variables, transitioning to renewable

energy would require the utility-scale use of energy storage. S&P

Global Market Intelligence analysis shows that lithium-ion batteries are

seen as the technology to compete with in this market.

Potential alternatives to lithium-ion batteries include batteries

made from different chemical compounds. Lithium has faced some

technological challenges in its adoption at the grand scale necessary

for utilities, which resulted in multiple fires in Arizona that led a member of the state’s public utilities commission to call for different technology solutions.

The increasing demand for lithium-ion batteries and the importance

they may hold for the transition to renewable energy has sparked

geopolitical competition to secure a stable supply of batteries. Chinese

firms have invested billions of dollars in lithium deposits across Australia and South America in recent years as part of the country’s plan to quadruple electric vehicle production between 2019 and 2025. In response, European companies

have sought to expand their own investments in lithium so that their

supply of batteries does not rely on foreign supply chains. Companies

investing in European lithium processing have also voiced concerns about

the potential environmental impact

of processing the lithium into batteries in China and then shipping

them across the world for use in Europe. As similar tensions arise

between China and the U.S., lithium has become another flash point in the countries’ trade battles.

Market demand has contributed to a surge in the lithium mining and production businesses. Budgets for mining industry lithium exploration

grew nearly sevenfold worldwide between 2015 and 2018, according to

S&P Global Market Intelligence. The jump in demand for lithium-ion

batteries led to a spike in prices in the early 2010s, and acquisitions

of lithium deposits and mines rose sharply. Since then, the supply of

lithium has risen more quickly than demand, so prices have fallen and

deal-making has slowed.

Although lithium prices across autumn 2019 were on the lower side and

some projects have been delayed or cut back, many market participants

still expect the sector to grow significantly. Lithium production is expected to triple to 1.5 million metric tons worldwide by 2025. S&P Global Platts has reported on fears that even this increase in supply might not be enough to keep up with demand, especially if expected electric vehicle adoption rates continue.

Posted by AGORACOM-JC

at 11:59 AM on Thursday, November 21st, 2019

SPONSOR: New Age Metals Inc.

The company’s Lithium Division has already made significant

acquisitions in Canada and the USA. The company also owns one of North

America’s largest primary platinum group metals deposit in Sudbury,

Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq

Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces

in the Inferred. Learn More.

Lithium: The New Oil

Lithium prices will likely increase in the next few years.

As electric cars replace gasoline powered ones, lithium will gain a strategic value not unlike that of crude oil today.

And, Bolivia, the poorest country in South America, has the resources to become the ‘Saudi Arabia’ of lithium.

The Coup in Bolivia Could Boost Lithium Prices and Energy Resource Geopolitical Dynamics

Lithium prices will likely increase in the next few years. As

electric cars replace gasoline powered ones, lithium will gain a

strategic value not unlike that of crude oil today. And, Bolivia, the

poorest country in South America, has the resources to become the ‘Saudi

Arabia’ of lithium. The resignation of Evo Morales has tightened the

market, indefinitely putting a halt to important lithium mining

projects, which should sustain prices in the medium term. Notably, the

coup and its possible – if not probable – links to lithium mining have

stressed how all South American leaders (just as those of the Persian

Gulf in relation to oil) will have to decide how manage the largest

lithium reserves in the world.

Lithium: The New Oil

To an even more anxious extent than drivers looking for gas stations

during the 1973 OPEC oil embargo, nothing characterizes 21stcentury

‘homo-sapiens’ lifestyle quite like the (insert gadget of

choice)-battery-socket triangle. If social scientists, media gurus and

advertising copywriters have noticed this trend, investors should have

perceived by now that much monetary value lurks behind the gesture of

‘plugging-in’. The whole world needs to ‘plug-in’ angst, and the angst

to recharge batteries will only intensify as car manufacturers are

shifting away from the internal combustion engine in favor of electric

motors at a faster pace than anyone had imagined even five years ago.

Whoever has the most reliable, enduring, lightest and most powerful

battery will build the best vehicles. Batteries, in an imminent future,

will even generate enough power (and be light enough) to propel

airplanes.A cell phone, a notebook, a tablet, work because of the

energy contained and released through lithium-ion batteries. But, the

appeal of electric cars, (or even hybrid cars), is driving the appetite.

Such vehicles are, quite literally, battery packs on wheels. And the

batteries alone make up some 42% of the sticker price. (Source:

Investopedia).

Many see ‘electric power’ as the way to end dependence on oil from

the Middle East. However, such independence is the stuff of geopolitical

fantasies: the rising demand for battery generated electric power has

already shifted the geopolitical balance away from the sands of Saudi

Arabia and closer to those of South America, which holds the richest

lithium deposits in the world; especially, Argentina, Chile and Bolivia

together hold some 80% of the world’s lithium (the Salar de Uuuni,

a salt flat covering 10,000 square kilometers at 3,600 meters above sea

level). being the largest known deposit). It is located near Potosi,

perhaps the most important mining center of South America during the

Spanish colonial era. The salt flat, which is also rich in magnesium,

potassium and sodium, contains some 47% of the known world’s lithium

reserves. At a price ranging between $8,000-10,000 per metric ton, the

potential is clear.

Indeed, the batteries that have hooked the whole world are the

lithium-ion (Li-ion) kind. And they are found in anything from

smartphones to tablets, to electric cars and modern airliners.

Lithium is a low-density metal, typically found in salt form, noted

for its ability to keep its level of charge (in case of inactivity). It

is an abundant alkaline mineral, but nowhere is it abundant (and easy to

extract) as it is in vast majority of the kind that’s most suitable to

make rechargeable batteries. However, one of lithium’s main advantages

as a resource is that, unlike oil, just about everyone has some. It’s

found everywhere; and therefore, it’s unlikely that conflicts will break

out because of it. Should a geopolitical dispute develop over lithium,

it will have more to do with the know-how to advance related battery

technology than Nevertheless, because of its sheer size, all major

industrial powers, starting from the United States, are coveting South

American lithium. Those who will, write rules of the contest to build

the best lithium battery, therefore, will not focus on the geographic

control of the resource. Rather, they will focus on the ability to

combine the expertise, technology and resource together in order to

transform the resource directly into batteries. More than

power-relations, the winners of this game will excel at diplomacy.

Battery dominance will be a factor of scientific competence, mining and

geopolitics.

Who Wants South American lithium?

All industrial powers want South American lithium, though, clearly

the United States, Japan, Germany, South Korea and, of course, China

have the most interest. But, it’s China, which has been investing most

heavily in the research. And therein rests the core of the problem.

Because the real ‘resource’ is the manipulation and technology around

lithium, ambitious governments, focused on lifting standards of living,

have imposed conditions on would-be extractors. They must invest in the

mining as well as the technology. And that’s the key to understand what

happened to President Evo Morales of Bolivia – and the key to

understanding how the race for lithium, the ‘21stcentury oil’, will have

to be played. Indeed, as commercial lithium mining operations in the

Salar de Ayuni began in 2016, President Morales quickly became

dissatisfied with the notion of perpetuating the exporting model that

has kept so many countries behind: that is the export of natural

resources and the import of expensive finished goods.

Morales wanted to establish an in-house battery production process in

order to export finished batteries. And Morales reached such an

agreement in January 2019 with Germany’s ACI System(ACISA).

Among others, ACISA supplies batteries to Tesla Motors. Germany, which

is one of the remaining industrial powers, needs to secure batteries for

its large auto manufacturing groups, which have quickly developed

electric vehicle lineups, after a few years of trailing behind the

Japanese and Americans. But last November 4, the Bolivian government

canceled the agreement after protests from Potosi locals, expressing

anger over the terms of the deal and the environmental consequences

deriving from the magnesium tailings from the lithium extraction.

Morales, for his part, probably expected more investment in the human

resources through the installation of educational facilities, chemistry

faculties, or at least scholarships to train the local people in the

relevant skills. Morales, in turn, wanted to sign a $2.3 billion

agreement – this time with China – turning Beijing into its strategic

partner for lithium extraction and battery technology. Morales thought

China to offer the best solution to achieve a complete battery

production supply chain. The Bolivian government was even rumored to

attempt a nationalization of the project, but a week after the

cancellation, President Evo Morales ‘resigned’ (or was the victim of a

coup).

Is there a coincidence between the cancellation and the resignation?

Perhaps, but the resulting political turmoil has effectively cut out

Bolivia and its massive lithium resources from the market. Even China,

which had designs with a project of its own in the Salar de Uyuni, will

not have a chance to pursue any mining, given the political and social

instability – even if the new people in charge will seek re-alignment

with the West (i.e. USA, Europe) instead of China and Russia.

Posted by AGORACOM-JC

at 3:30 PM on Friday, November 15th, 2019

SPONSOR: New Age Metals Inc.

The company’s Lithium Division has already made significant

acquisitions in Canada and the USA. The company also owns one of North

America’s largest primary platinum group metals deposit in Sudbury,

Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq

Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces

in the Inferred. Learn More.

Europe EVs now use 57% more lithium carbonate equivalent

Changing mix of EV sales is most noticeable in Europe where the average battery in new passenger EVs sold in September contained 15.8kg of LCE

Constitutes a 57% surge compared to last year, thanks in no small part to the popularity of the Tesla Model 3 on the continent

Electric car pioneer Tesla is already producing units on a trial basis at its giant Shanghai gigafactory despite only breaking ground this year, but thanks to changes to the Chinese EV subsidy program, demand for locally-made Teslas may fall short of expectations.

On Monday, China’s automobile manufacturing industry body said fewer

new energy vehicles, or NEVs as they are termed domestically, could be

sold this year than in 2018 (last year sales boomed by more than 60%).

Sales of NEVs – which apart from battery-powered vehicles also

include hybrids and fuel cell cars – fell by more than 45% in October

from the same month last year, adding to the woes of an industry coping

with 16 straight months of declining overall sales.

Changes to China’s EV incentive program favour hybrids so lithium loads may start to tend downwards in that country too

Adamas Intelligence tracks the battery capacity (and the metals used in them)

of electric vehicles sold around the world and the slowdown in the EV

market, where lithium-ion batteries dominate, has already showed up in

raw material deployment data.

In September 2019, the average new passenger EV including plug-in and

conventional hybrids sold globally contained 12.2 kilograms of lithium

carbonate equivalent (LCE), a modest increase of 4% over 2018, according

to the latest Adamas report.

The Toronto-based research company’s data shows China still

outstripped global growth in September with a 7% increase in LCE on a

per-EV basis, reaching a sales-weighted average of just shy of 20kg

thanks to the prevalence of full electric models in the country.

That’s in stark contrast to Japan, where hybrids represent more than

90% of EV sales and average batteries contain only 1.1kg of LCE. Changes

to China’s EV incentive program favour hybrids so lithium loads may

start to tend downwards in that country too.

The changing mix of EV sales is most noticeable in Europe where the

average battery in new passenger EVs sold in September contained 15.8kg

of LCE.

That constitutes a 57% surge compared to last year, thanks in no

small part to the popularity of the Tesla Model 3 on the continent.

Teslas have always had bigger batteries than competitor cars to help

with fast-charging and range.

In the US the trend is in the opposite direction – with passenger EVs

leaving showrooms containing on average 15.2kg of LCE, 12% less than in

September 2018.

Posted by AGORACOM-JC

at 12:59 PM on Thursday, November 14th, 2019

SPONSOR: New Age Metals Inc.

The company’s Lithium Division has already made significant

acquisitions in Canada and the USA. The company also owns one of North

America’s largest primary platinum group metals deposit in Sudbury,

Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq

Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces

in the Inferred. Learn More.

Sales Revenue of Palladium to Soar in the Near Future Owing to Growing Consumer Adoption

Global market for palladium is likely to experience

significant growth with declining demand for metals and increasing

demand for recycling metals, leading to palladium demand outstripping

the supply.

In addition, changing prospects of investments in palladium have also contributed to the growth of the market

Palladium

is a lustrous silvery-white rare metal used in a diverse range of

applications. The metal with other elements such as osmium, iridium,

ruthenium, rhodium, and platinum are referred to as Platinum Group

Metals (PGM). Palladium is majorly consumed in the automotive industry

as catalytic converters, manufacturing of electronics and jewelry, as

well as chemical and dental applications. Palladium is sourced from two

major sources, viz., mine production and recycling.

The global market for palladium is likely to experience significant

growth with declining demand for metals and increasing demand for

recycling metals, leading to palladium demand outstripping the supply.

In addition, changing prospects of investments in palladium have also

contributed to the growth of the market. Several new palladium

exchange-traded funds by companies such as Absa Capital in South

Africa are expected to create a significant boost for the palladium

market.

Growing demand for palladium in catalytic converters in the

automotive industry in vehicles exhausts are one of the major growth

factors driving the palladium market. Demand for the metal from other

sectors such as jewelry and industrial are also anticipated to

contribute to the growth of the market. However, rising prices of

palladium owing to supply issues in South Africa and declining state

stockpiles in Russia are expected to hamper the growth of the market.

North America was the largest consumer for palladium, followed by China

owing to the presence of the vast automotive industry in the region.

Future market growth is expected to be from Asia Pacific with the

growing industrial activities in emerging economies such as India. These

factors are expected to provide new opportunities for the growth of the

market.

Posted by AGORACOM-JC

at 3:54 PM on Tuesday, November 12th, 2019

SPONSOR: New Age Metals Inc.

The company’s Lithium Division has already made significant

acquisitions in Canada and the USA. The company also owns one of North

America’s largest primary platinum group metals deposit in Sudbury,

Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq

Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces

in the Inferred. Learn More.

Palladium Prices Soar to Record High

Global Precious Monthly Metals Index (MMI)Â jumped six points this month, rising for a November MMI reading of 113.

As noted here many times before, platinum had historically traded at a premium to palladium.

That relationship, however, flipped as of September 2017, and has remained flipped ever since.

The palladium-platinum spread widened this month, even as platinum made gains.

The spread rose to $850/mt this month, up from $763/mt last month.

Looking Ahead

Gold and silver enjoyed a strong run-up during the summer season, but what is ahead for the precious metals?

“Having risen into the summer, gold and

silver prices have plateaued in Q3 even as some ETFs have seen strong

inflows due to accommodative monetary policies, such as falling Fed

rates and safe haven buying in the face of geopolitical uncertainty,â€

MetalMiner’s Stuart Burns explained. “But jewelry demand is down,

central bank buying of gold is lower than the same time last year and a

strong dollar set up a number of headwinds that have seen prices unwind

as news comes out about a possible winding back of tariffs between the

US and China.â€

As for platinum, prices did not tick up as much as one might have expected given trends in the automotive industry.

“Likewise, platinum prices have failed to

make any headway in Q3 despite a strong showing from other PGMs, such as

palladium and rhodium, both of which continue to benefit from the

switch to petrol internal combustion engines among European carmakers,â€

Burns added.

“Gold, silver and palladium prices are expected to ease further in

the run up to the year-end while other PGMs will be swayed more by car

production and dollar strength. Much will depend on a successful outcome

to the encouraging progress on trade talks, which could see investors

take a more bullish attitude on risk to industrial metals and weaken

demand for safe-haven investment metals.â€

Actual Metal Prices and Trends

The U.S. silver ingot/bar price rose 5.0% month over month to $18.08/ounce as of Nov. 1.

U.S. platinum bars rose 6.3% to $930/ounce. U.S. palladium bars jumped 8.7% to $1,780/ounce.

Chinese gold bullion rose 1.7% to $48.79/gram. U.S. gold bullion increased 2.3% to $1,512.70/ounce.

Posted by AGORACOM-JC

at 11:49 AM on Wednesday, November 6th, 2019

SPONSOR: New Age Metals Inc.

The company’s Lithium Division has already made significant

acquisitions in Canada and the USA. The company also owns one of North

America’s largest primary platinum group metals deposit in Sudbury,

Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq

Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces

in the Inferred. Learn More.

Palladium soaring: the quiet precious metal

Traditionally, gold, silver and platinum have received all the attention.

But like a spurned sibling that everyone ignored, the palladium spot price has broken free and there’s been no looking back just yet.

In notes to our clients we’ve talked a couple of times about gold,

and touched on silver and platinum which are all members of the precious

metals family. The potential for gains in all three of the metals has

been sizeable in the last few months. There has been some notable

pullbacks and profit-taking of late, particularly in gold stocks,

however there is a member of the family we have yet to discuss in any

depth. Palladium.

Traditionally, gold, silver and platinum have received all the

attention. But like a spurned sibling that everyone ignored, the

palladium spot price has broken free and there’s been no looking back

just yet.

Palladium Price $US/ounce

Source: Macrotrends

Much lesser known than the other three major precious metals,

palladium has in a very short period of time become the most expensive,

overtaking gold. Similar to platinum, not much is known about the metal –

what it is used for, how it is mined, and more importantly, how or why

has it become so darn expensive?

The majority of palladium ends up in car exhaust systems where it

aids in converting toxic pollutants into less-harmful CO2 and water

vapour. To a lesser extent, it is also used in electronics, dentistry

and jewellery. The metal is mined primarily in Russia and South Africa,

and mostly extracted as a secondary product from mines focused on other

metals such as platinum or nickel. Who would have thought a by-product

could have surged to a value of over US$1,800/oz!

Simply put, supply hasn’t responded to growing demand. Usage is

increasing as governments, especially China, tighten regulations to

crack down on pollution from vehicles, forcing automakers to increase

the amount of precious metal they use. Globally, it also looks like

we’ve been buying fewer diesel cars (which mostly use platinum) and

instead sticking with petrol powered vehicles (which use palladium)

following news that some diesel car makers were cutting corners on

carbon emissions tests.

Furthermore, population growth has not eased, and the electric car

take-up has been slower than many predicted, perhaps due to pricing and

convenience. We are still relying on petrol power (particularly in the

emerging markets).

Source: Metals Focus

Palladium’s status as a by-product to platinum or nickel mining means

output tends to lag price gains. In fact, the amount of palladium

produced is projected to fall short of demand for an eighth straight

year in 2019. That’s helped drive price to all-time high. While some

obscure metals are still more valuable, such as rhodium, palladium has

ballooned and has outpaced gold for most of this year.

Gaining any direct exposure to an investment in palladium is a

difficult proposition and would be most easily achieved via ETFs e.g.

the Aberdeen Standard Physical Palladium Shares ETF (PALL).

Posted by AGORACOM-JC

at 9:00 AM on Wednesday, October 30th, 2019

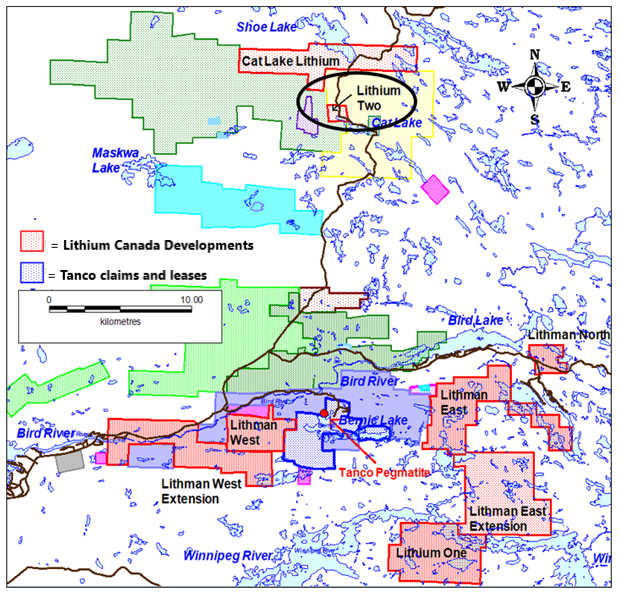

A drill permit has been issued by the Manitoba government for a drill program on the company’s Lithium Two Project.

NAM has 100% ownership of eight pegmatite hosted Lithium and Rare Element Projects in the Winnipeg River Pegmatite Field, located in southeast (SE) Manitoba.

Exploration in SE Manitoba is focused on Lithium-bearing pegmatites.

Archaeological Assessment in progress on Lithium One as part of the drill permit process.

The eight projects are strategically situated within the Winnipeg River Pegmatite Field, which hosts the world-class Tanco Pegmatite that has been mined for Tantalum, Cesium and Spodumene (one of the primary Lithium minerals) in varying capacities, since 1969.

NAM management is finalizing a plan for a 1,500-metre drill program on Lithium Two.

October 30th, 2019 – Rockport, Canada – New Age Metals Inc. (NAM) (TSX.V: NAM; OTCQB: NMTLF; FSE: P7J) New Age Metals is pleased to announce that a drill permit has been issued to the company’s wholly owned subsidiary, Lithium Canada Development by the Manitoba government for the company’s Lithium Two Project located in the Cat Lake area of southeast (SE) Manitoba.

The Winnipeg River Pegmatite Field

The

Winnipeg River-Cat Lake Pegmatite Field in SE Manitoba is host to

numerous pegmatite deposits and contains the world-class Tanco

Pegmatite. The Tanco pegmatite has been mined since 1969 in

varying capacities for spodumene (Li rich mineral), Tantalum and Cesium.

The pegmatite field contains at least 10 pegmatite groups and hosts

hundreds of pegmatite bodies. Many of the pegmatites are lithium

bearing.

The Tanco Mine, which was owned by the

Cabot Corporation, was recently sold to Sinomine Rare Metals Resources

Co. Ltd. (Sinomine) at a purchase price of $130 million ($US). Sinomine

is a joint stock public company based in China, principally engaged in

the provision of geological exploration, mining investment and base

metal chemical manufacturing. This transaction certainly adds new

interest in the region as to the potential of the pegmatite field and

lithium and/or rare element potential in the area. This sale should

advance the Lithium production potential of the area as Lithium Ore feed

may be required in the event that Sinomine commences lithium

production.

Lithium Two Project

The Lithium Two Project is located

approximately 20 kilometres north of the Tanco Mine and is an active

area for Lithium exploration. Several companies are active in the

immediate region, exploring for Lithium.

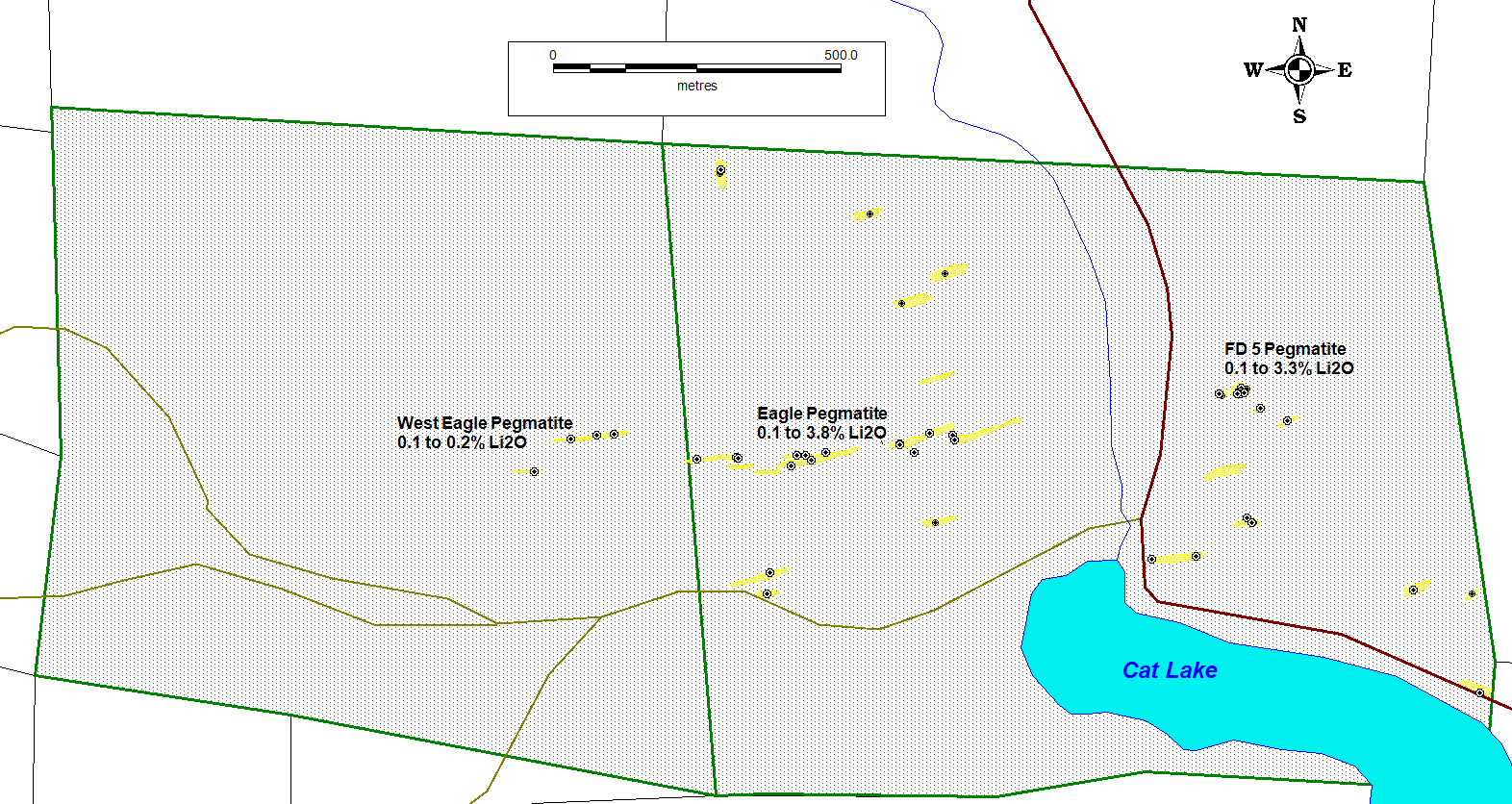

Surface exploration was carried out on the Lithium Two Project during the summer of 2018 (see News Release October 30th, 2018).

The exploration work was designed to examine the known surface

pegmatites to aid in the determination of drill targets. The field

program also focussed on more detailed structural geological mapping and

mapping of the westward extent of the Eagle Pegmatite. The Lithium Two

Project has several historically known Spodumene bearing pegmatites (see

Figure 2).

Click Image To View Full Size

Figure 1: Manitoba Lithium and Rare Element Projects 2019

The Eagle Pegmatite was drilled in 1947

with a historic (non 43-101 compliant) tonnage estimate of 544,460

tonnes with a grade of 1.4% Li2O to the 61-metre level. These historical

estimates do not use categories that conform to current CIM Definition

Standards on Mineral Resources and Mineral Reserves as outlined in

National Instrument 43-101, Standards of Disclosure for Mineral Projects

(“NI 43-101”) and have not been redefined to conform to current CIM

Definition Standards. A qualified person has not done sufficient work to

classify the historical estimates as current mineral resources and the

Company is not treating the historical estimates as current mineral

resources. Investors are cautioned that the historical estimates do not

mean or imply that economic deposits exist on the properties. The

Company has not undertaken any independent investigation of the

historical estimates or other information contained in this press

release nor has it independently analyzed the results of the previous

exploration work in order to verify the accuracy of the information. The

Company believes that these historical estimates and other information

contained in this news release are relevant to continuing exploration on

the properties as it identifies significant mineralization that will be

the target of future exploration and development.

The Eagle Pegmatite was historically reported to remain open to depth.

The FD5 Pegmatite, located east of the Eagle Pegmatite has never been

drilled. Historic assessment reports revealed a Spodumene bearing

pegmatite drilled in the late 1940’s, located approximately 500 metres

southeast of the Eagle Pegmatite but is not exposed on surface. No

assays were provided in the report at the time. This pegmatite, as well as the Eagle and FD5, will be tested during an upcoming recommended drill program.

Click Image To View Full Size

Figure 2: 2018 Lithium Assays at the Lithium Two Project, SE Manitoba

The Eagle Pegmatite has been mapped on surface for over 850 metres and has surface assays of 0.1 to 3.8% Li2O.

The FD5 pegmatite had surface assays from 0.1 to 3.3% Li2O. In

geological terms, the pegmatites encountered on the Lithium Two Project

are LCT Type (Lithium-Cesium-Tantalum) Pegmatites and are in the

Albite-Spodumene Subgroup. Spodumene is expressed in the pegmatites as

small green blades up to 3 centimetres in length. The Eagle Pegmatite is

a west-northwest to west-striking, vertically dipping, lenticular

pegmatite dyke intruded into mafic volcanics. The widths of the

pegmatite have been measured to be between 2 to 10 metres. The Eagle

Pegmatite system appears to be a swarm of closely spaced pegmatite

bodies.

Phase 1 Drill Program Planning in Progress

A drill program of 1,500 metres is planned

to test three spodumene bearing pegmatite targets. A drill permit has

recently been issued by the Manitoba government.

Lithium One Drill Program

Recently,

NAM engaged White Spruce Archaeology as part of its Exploration

Agreement with the Sagkeeng First Nation to conduct an archaeological

assessment on the proposed drill sites for Lithium One as part of the

drill permitting process. The assessment was completed in October

and the report is pending. A 1,500 metre drill program is planned to

test targets on the Silverleaf pegmatite ( News Release Sept 27, 1018) situated in the Lithium One project area.

NAM/AAZ Property Option Update

JV partner Azincourt Energy (AAZ) and NAM

are in discussions regarding AAZ’s compliance for its contractual

obligations as part of the option agreement with NAM. NAM and AAZ are in

continuing talks regarding a revision to the existing option agreement

or termination.

OPT-IN LIST

If you have not done so already, we encourage you to sign up on our website (www.newagemetals.com) to receive our updated news.

ABOUT NAM’S PGM DIVISION

NAM’s flagship project is its 100% owned River Valley PGM Project (NAM Website – River Valley Project)

in the Sudbury Mining District of Northern Ontario (100 km east of

Sudbury, Ontario). Recently the company announced the results of the

first PEA (see News Release – June 27th, 2019)

completed on the River Valley Project. The PEA has been developed by

various independent consultants – P&E Mining Consultants Inc.

(P&E) was responsible for the open pit mining, surface

infrastructure, tailings facility, and project economics; DRA Americas

Inc. (“DRA”) was responsible for all metallurgical test work and

processing aspects of the Project; and WSP Canada Inc. (“WSP”) was

responsible for the Mineral Resource Estimate. The

PEA is a preliminary report but it has demonstrated that there are

positive economics for a large-scale mining open pit operation, with 14

years of Palladium and Platinum production.

The

Genesis project is a PGM-Cu-Ni property located in the northeastern

Chugach Mountains, 75 paved road miles north of the all-season port city

of Valdez, Alaska. The project is within 3 km of the all-season

paved Richardson Highway and a high capacity electric power line. The

project is covered by 4,144 hectares of State of Alaska mining claims

owned 100% by New Age Metals. Past exploration has revealed the presence

of chromite-associated platinum and palladium mineralization and

stratabound Ni-Cu-PGM mineralization within magmatic layers of the

Tonsina Ultramafic Complex. Pyrrhotite, pentlandite, and chalcopyrite

occur in disseminations and net textured segregations associated with

platinum and palladium sulfides. There has been limited exploration over

the Genesis project and there has been no past exploration drilling on

the project. NAM management is actively seeking an option/joint-venture partner for this road accessible PGM and Multiple Element Project.

QUALIFIED PERSON

The contents contained herein that

relate to exploration results or geological aspects is based on

information compiled, reviewed or prepared by Carey Galeschuk, P. Geo., a

consulting geoscientist for New Age Metals. Mr. Galeschuk is the

Qualified Person as defined by National Instrument 43-101 and has

reviewed and approved the technical content of this news release.

On behalf of the Board of Directors

“Harry Barr”

Harry G. Barr

Chairman and CEO

Neither the TSX Venture Exchange nor its

Regulation Services Provider (as that term is defined in the policies

of the TSX Venture Exchange) accepts responsibility for the adequacy or

accuracy of this release.

Cautionary Note Regarding Forward

Looking Statements: This release contains forward-looking statements

that involve risks and uncertainties. These statements may differ

materially from actual future events or results and are based on current

expectations or beliefs. For this purpose, statements of historical

fact may be deemed to be forward-looking statements. In addition,

forward-looking statements include statements in which the Company uses

words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”,

“confident”, “intend”, “strategy”, “plan”, “will”, “estimate”,

“project”, “goal”, “target”, “prospects”, “optimistic” or similar

expressions. These statements by their nature involve risks and

uncertainties, and actual results may differ materially depending on a

variety of important factors, including, among others, the Company’s

ability and continuation of efforts to timely and completely make

available adequate current public information, additional or different

regulatory and legal requirements and restrictions that may be imposed,

and other factors as may be discussed in the documents filed by the

Company on SEDAR (www.sedar.com), including the most recent reports that

identify important risk factors that could cause actual results to

differ from those contained in the forward-looking statements. The

Company does not undertake any obligation to review or confirm analysts’

expectations or estimates or to release publicly any revisions to any

forward-looking statements to reflect events or circumstances after the

date hereof or to reflect the occurrence of unanticipated events.

Investors should not place undue reliance on forward-looking statements.