Posted by AGORACOM-JC

at 12:07 PM on Thursday, October 31st, 2019

Company has notified BWA Group plc (London, England) (NEX:BWAP) of its intention to convert GBP300,000 ($511,000) of Convertible Loan notes “CLN” into 60,000,000 ordinary shares in BWA Group plc.

Shares will be admitted to trading on the NEX Exchange Growth Market in London, effective November 6, 2019

Montreal – October 31, 2019 –St-Georges Eco-Mining Corp. (CSE:SX) (OTC:SXOOF) (FSE: 85G1) is pleased to inform its shareholders that the Company has notified BWA Group plc (London, England) (NEX:BWAP) of its intention to convert GBP300,000 ($511,000) of Convertible Loan notes “CLN” into 60,000,000 ordinary shares in BWA Group plc.

The Company has been notified by

BWA Group plc that the shares will be admitted to trading on the NEX

Exchange Growth Market in London, effective November 6, 2019. Following

the allotment of these ordinary shares, St-Georges will hold 60,000,000

ordinary shares of BWA Group plc, representing 23.75% of this

corporation’s enlarged issued share capital.

The Company received GBP2,451,409

($4,183,000) of convertible loan notes on September 30, 2019 in relation

to sale of its subsidiary Kings of the North to BWA Group plc. After

the conversion, St-Georges has GBP2,151,409 worth of loan notes

outstanding at an approximate value of $3,671,427.

ON BEHALF OF THE BOARD OF DIRECTORS

“Mark Billings”

MARK BILLINGS

Chairman

About St-Georges

St-Georges is developing new

technologies to solve some of the most common environmental problems in

the mining industry. The Company controls directly or indirectly,

through rights of first refusal, all of the active mineral tenures in

Iceland. It also explores for nickel on the Julie Nickel Project &

for industrial minerals on Quebec’s North Shore and for lithium and rare

metals in Northern Quebec and in the Abitibi region. Headquartered in

Montreal, St-Georges’ stock is listed on the CSE under the symbol SX, on

the US OTC under the Symbol SXOOF and on the Frankfurt Stock Exchange

under the symbol 85G1.

The

Canadian Securities Exchange (CSE) has not reviewed and does not accept

responsibility for the adequacy or the accuracy of the contents of this

release.

Posted by AGORACOM-JC

at 11:33 AM on Thursday, October 31st, 2019

SPONSOR: CardioComm Solutions (EKG: TSX-V)

– The heartbeat of cardiovascular medicine and telemedicine. Patented

systems enable medical professionals, patients, and other healthcare

professionals, clinics, hospitals and call centres to access and manage

patient information in a secure and reliable environment.

EKG: TSX-V ———————-

Five rehab hospitals across the country will soon be testing a

digital therapeutic platform that combines music with AI and mHealth

sensors to help stroke survivors with walking problems.

Hospitals will be testing a digital therapeutic device developed by Portland, ME-based MedRhythms, which is seeking US Food and Drug Administration approval for the service.

The program will study the mHealth device’s impact on walking among a group of patients who have walking impairments as a result of a stroke

October 29, 2019 – Five rehabilitation hospitals will be testing a

telehealth platform for stroke treatment that integrates music with AI

and mHealth sensors for guided therapy.

The hospitals will be testing a digital therapeutic device developed

by Portland, ME-based MedRhythms, which is seeking US Food and Drug

Administration approval for the service. The program will study the

mHealth device’s impact on walking among a group of patients who have

walking impairments as a result of a stroke.

“Right now, the MedRhythms digital therapeutic technology is a novel

treatment for a subset of individuals that have few, if any, effective

treatment options,†David Putrino, director of the Abilities Research

Center (ARC) for the Department of Rehabilitation and Human Performance

at the Mount Sinai Health System, said in a press release.

“The mission of the ARC is to identify and validate novel technologies

that have the potential to significantly enhance the rehabilitation of

people who are recovering from brain injuries and neurological

conditions, including chronic stroke.â€

Putrino will lead the research project at New York-based Mount Sinai.

Also participating in the study are the Shirley Ryan AbilityLab in

Chicago, the Kessler Foundation in New Jersey and Spauld ing

Rehabilitation Hospital and the Boston University Neuromotor Recovery

Laboratory, both in Boston.

“The digital therapeutics industry has the potential to transform

rehabilitation and disrupt healthcare, and it is imperative for

companies in this space to run full-scale, multisite RCTs like

MedRhythms is doing,†Putrino added.

MedRhytms began as a digital therapy program launched out of

Spaulding Rehab, part of the Partners HealthCare network, and has been

building a portfolio of digital therapeutic treatments for treatment of

neurological injury and disease, including Parkinson’s Disease and

Multiple Sclerosis. The company is also looking to apply the treatment

to senior care and fall prevention programs.

The company’s first and signature product is MedRhythms Stride, a

digital health platform for stroke rehabilitation that focuses on

Rhythmic Auditory Simulation (RAS). mHealth sensors attached to a

patient’s feet gather gait parameters, which are then analyzed by a

smartphone app that pairs the patient’s gait with music.

“Rhythm is the main driver of the interventions we have,†Owen McCarthy, the company’s president and founder, told mHealthIntelligence in a 2018 interview. “And it’s the type of thing we’re going to see more and more of in healthcare.â€

This past June, the company announced a partnership

with Health Catalyst’s new life sciences business to make its platform

available to payers and providers looking for new ways to enhance stroke

rehabilitation programs.

“This partnership comes at a crucial time in the digital therapeutics

industry,†Carlos Rodarte, senior vice president of strategy and

business development for the life sciences at Health Catalyst, said in a

press release. “Several companies in this field have completed or are

completing important trials demonstrating the significant clinical

impact of true, validated and regulated digital therapeutics, paving the

way for an entire new industry in digital health which has disruptive

potential globally to deliver rapid, efficient therapies for patients

with unmet needs.â€

Tags: EKG, mhealth, small cap stocks, stocks, tsx, tsx-v Posted in CardioComm Solutions | Comments Off on CardioComm Solutions $EKG.ca – Hospitals to Test Music-Based #mHealth Platform for Stroke Treatment $ATE.ca $TLT.ca $OGI.ca $ACST.ca $IPA.ca

Posted by AGORACOM-JC

at 10:24 AM on Thursday, October 31st, 2019

SPONSOR:ThreeD Capital Inc. (IDK:CSE)

Led by legendary financier, Sheldon Inwentash, ThreeD is a

Canadian-based venture capital firm that only invests in best of breed

small-cap companies which are both defensible and mass scalable. More

than just lip service, Inwentash has financed many of Canada’s biggest

small-cap exits. Click Here For More Information.

IDK: CSE

Bitcoin And Crypto Is Heading For An Epic Social Media Showdown

While the social media monetary situation is not this clear cut, both

Dorsey and Zuckerberg have emerged as champions of two similar but

opposing ideas; the internet needs its own currency, one sees it as

centralised, through Facebook, the other sees it as decentralised,

through bitcoin.

“I believe that this is something that needs to get built,”

Zuckerberg told U.S. senators last week, defending Facebook’s

involvement in the controversial libra project and arguing libra could

bring financial maturity to millions, if not billions, of people around

the world.

Zuckerberg also warned the U.S. could fall behind other countries if

lawmakers moved to block the development of libra and similar digital

money projects.

Posted by AGORACOM-JC

at 9:08 AM on Thursday, October 31st, 2019

Announced its collaboration with Professor Lionel ROUÉ of the Institut National de Recherche Scientifique (INRS)

Aimed at evaluating the electrochemical performances of different materials produced by the HPQ PUREVAP™Quartz Reduction Reactor for Li-ion batteries

MONTREAL, Oct. 31, 2019 — HPQ Silicon Resources Inc. – TSX-V: HPQ; OTCPink: URAGF; FWB: UGE (“HPQ†or “the Companyâ€) is pleased to announce its collaboration with Professor Lionel ROUÉ of the Institut National de Recherche Scientifique (INRS) within the scope of projects aimed at evaluating the electrochemical performances of different materials produced by the HPQ PUREVAP™Quartz Reduction Reactor (“QRR”) for Li-ion batteries.

Professor Lionel ROUÉ of the INRS-EMT has developed a scientific

program focused on the study of new electrode materials for various

applications of industrial interest (batteries, aluminium production,

etc.). In recent years, a significant part of its research activities

has been devoted to the study of Si anodes for Li-ion batteries and the

development of in-situ characterization methods applied to batteries.

He is the author of more than 150 publications, including twenty

articles and 2 patents on Si-based anodes for Li-ion batteries. He was

awarded the Energia Prize by the Quebec Association for the Mastery of

Energy for his work in this field.

EVALUATING WORLDWIDE BATTERY MARKET POTENTIAL OF MATERIALS PRODUCED BY PUREVAP™

The first goal of the association is determining the commercial potential of materials produced by the PUREVAPTM

QRR as anode material for the Li-ion battery market and ascertaining

whether their usage within Li-ion batteries could lead to a significant

increase in their energy density, which is crucial for some

applications, especially electric vehicles.

In the second phase, the electrochemical performance of PUREVAPTM silicon based porous silicon wafers made using Apollon Solar’s patented process will be tested.

“Silicon’s potential to meet energy storage demand is generating massive investments. Collaborating

with a world-class university center, HPQ will be able to validate the

potential of silicon materials produced from the PUREVAP™QRR as high-capacity anode materials for Li-ion batteries†said Bernard Tourillon, President & CEO of HPQ Silicon Resources Inc. Mr. Tourillon added: “HPQ, working with PyroGenesis, Apollon and the INRS Energy Materials Telecommunications (EMT) Research Centre, fully intends to use its Gen3 PUREVAP™ QRR to produce and market Silicon materials for batteriesâ€.

GLOBAL ENERGY STORAGE MARKET READY TO EXPLODE

A recent report

projects that energy storage deployments are estimated to grow 1,300%

from a 12 Gigawatt-hour market in 2018 to a 158 Gigawatt-hour market in

2024. An estimated US$71 billion in investments will be made into

storage systems where batteries will make up the lion’s share of capital

deployment. Research suggests

that replacing graphite materials with Silicon anodes in Li-Ion

Batteries promises an almost tenfold (10x) increase in the specific

capacity of the anode, inducing a 20-40% gain in the energy density of

Li-ion batteries.

About Silicon

Silicon (Si) is one of today’s strategic materials needed to fulfil

the renewable energy revolution presently under way. Silicon does not

exist in its pure state; it must be extracted from quartz, one of the

most abundant minerals of the earth’s crust and other expensive raw

materials in a carbothermic process.

About HPQ Silicon

HPQ Silicon Resources Inc. is a TSX-V listed company developing, in

collaboration with industry leader PyroGenesis (TSX-V: PYR) the

innovative PUREVAPTM “Quartz Reduction Reactors†(QRR), a truly

2.0 Carbothermic process (patent pending), which will permit the

transformation and purification of quartz (SiO2) into Metallurgical

Grade Silicon (Mg-Si) at prices that will propagate its significant

renewable energy potential.

HPQ is also working with industry leader Apollon Solar to develop: Porous silicon wafers manufacturing using PUREVAP™

Silicon (PVAP Si) that can be used as anode for all-solid-state and

Li-ion batteries; and a metallurgical pathway of producing Solar Grade

Silicon Metal (SoG Si) that will take full advantage of the PUREVAPTM QRR

one-step production of high purity silicon (Si) and significantly

reduce the Capex and Opex associated with the transformation of quartz

(SiO2) into SoG-Si.

HPQ focus is becoming the lowest cost producer of Silicon (Si), High

Purity Silicon (Si), Porous Silicon Wafers and Solar Grade Silicon Metal

(SoG-Si). The pilot plant equipment that will validate the commercial

potential of the process is on schedule to start in 2019.

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

Disclaimers:

The Corporation’s interest in developing the PUREVAP™ QRR and any

projected capital or operating cost savings associated with its

development should not be construed as being related to the establishing

the economic viability or technical feasibility of the Company’s

Roncevaux Quartz Project, Matapedia Area, in the Gaspe Region, Province

of Quebec.

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward-looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Company’s current expectation and assumptions and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Company with respect to future events and are subject to certain risks

and uncertainties and other risks detailed from time-to-time in the

Company’s on-going filings with the security’s regulatory authorities,

which filings can be found at www.sedar.com. Actual results, events, and

performance may differ materially. Readers are cautioned not to place

undue reliance on these forward-looking statements. The Company

undertakes no obligation to publicly update or revise any

forward-looking statements either as a result of new information, future

events or otherwise, except as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

For further information contact Bernard J. Tourillon, Chairman, President and CEO Tel (514) 907-1011 Patrick Levasseur, Vice-President and COO Tel: (514) 262-9239 http://www.hpqsilicon.com Email: [email protected]

Posted by AGORACOM-JC

at 11:03 AM on Wednesday, October 30th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

TN: CSE —————————-

A nickel for your thoughts – The price of nickel has run up to a five-year high of late

The price of nickel has run up to a five-year high of late, defying softness in the rest of the base metal complex.

The reasons are both simple and complicated. The price of nickel

doubled in two years, from US$4 per lb. in August 2017 to US$8 per lb. a

few weeks ago. The reasons:

· Robust demand. Nickel is primarily used to make stainless steel. And despite slowing growth, stainless steel demand keeps marching up.

In the first half of 2019, for instance, Chinese stainless steel

production was up 8.5% yearover-year. (As the chart suggests, forecasts

predict softening of demand in the current quarter.)

· China makes most of the world’s stainless steel. And China gets the

nickel for that steel from its own mines as well as mines in Indonesia

and the Philippines, many of which produce a lowgrade, high-impurity ore

called nickel pig iron (NPI). NPI production has

ballooned over the last decade, enough that as of 2020 the world will

get more of its nickel from NPI than from conventional nickel ores.

However, this reliance on NPI brings with it a few problems.

· Indonesia will implement a ban on nickel ore exports at the start of 2020.

This has been in the works for some time but until a few months ago the

ban was not scheduled to take effect until 2022. Indonesia produces

roughly ~12% of global supply, so this ban is significant. The idea is

to push the development of domestic smelters, which would keep more of

the resource upside in country versus exporting raw ore. This is in the

works – the country already has 11 nickel smelters and 25 more are

planned or under construction – so Indonesian nickel supplies should

slide in the near term but recover within about three years. However,

the smelters in China that relied on Indonesia’s nickel pig iron (NPI)

ore will have to find feed elsewhere; the main candidate is the

Philippines, where ore is generally lower grade. The only other option

is to upgrade to processing Class I ores. Either move would increase

costs overall, which supports a higher nickel price.

· Batteries. Eighty percent of the world’s nickel

goes into stainless steel, so steel certainly drives the market. But

many of the batteries that power laptops, electric vehicles, phones, and

even power grids require nickel. This has transformed nickel from a one

trick pony to a two trick market – and if electric cars take off then

nickel’s battery market will take off right alongside. Right now

batteries consume 5% of global nickel but demand is rising rapidly and

is expected to reach 8% by 2020. Vice President of market analysis and

economics for BHP, Dr Huw McKay, says he sees a future where batteries

and stainless steel become “equally important†nickel consumers. Global

nickel demand currently sits around 2 million tonnes per annum; it is

expected to grow to 6 million tonnes per annum by 2035 with batteries

accounting for almost half of demand growth.

· In addition, batteries cannot use nickel from NPI, as impurities are too high, so the battery factor has divided the nickel market into two parts

– high purity Class I nickel and lower purity Class II. All of this has

two important effects: it is bringing energy metal investors into the

nickel space and it is underlining that NPI, which has been the dominant

source of nickel growth for the last 10-plus years, will not solve the

nickel supply gap going forward.

· To address that second point and boost production of Class I

nickel, China is developing several mines tapping into nickel laterite

deposits. Nickel laterite is easy to mine but very difficult to process,

requiring high pressure acid leaching (HPAL). Most analysts are

highly skeptical that China’s planned HPAL facilities will come online

anywhere near their projected timelines or budgets, as these facilities are notoriously difficult and expensive.

· Because NPI has ballooned so in the last decade, explorers and developers have not looked for conventional nickel deposits. There

is a true lack of development-stage nickel projects with conventional

sulphide deposits that could be built to fill supply gaps.

· Current mine-specific supply issues. The biggest

producer of NPI in the Philippines just ran out of ore. The Ramu project

in Papua New Guinea is temporarily suspended, which removes 35,000

tonnes of annual nickel supply.

· Stockpiles are falling – and fast. Nickel stockpiles have been declining for five years.

This is what happens when a market is persistently undersupplied. But

as you can see, the decline accelerated in the last two years…and

stockpiles dropped off a cliff a few weeks ago.

The cliff is likely the result of panic buying and/or stockpiling ahead of the Indonesian ban.

I told you it was complicated!

Complicated is normal for nickel, which has a long track record of

extreme price moves. In 2008 a supply shortage drove the price as high

as US$22 per lb. before steel mills found substitutes, 7 including

manganese, and within 18 months the price was back at US$4.50 per lb.

(The Great Financial Crisis likely exacerbated the price decline.)

The Bear Case

The key question on this side is: to what extent is speculation driving nickel?

If speculators are pushing the price up, entering the space now is

risky because (1) speculative tides turn fast and (2) that turn would

likely transpire in the next 6 to 9 months. Indonesia’s ban comes into

effect in January 1 so over the next six months the impacts start to

play out.

It’s clear that stockpile drawdowns are at least in part because

smelters and speculators have been stockpiling metal privately. That

metal will be used or sold to ease any nickel price jumps.

If increased physical metal availability coincides with the absence of speculative upside pressure…nickel could turn down fast.

On top of all that, there are reasons to believe (1) stainless steel

demand will weaken to end this year, (2) EV demand is taking longer to

ramp than expected, (3) scrap usage is increasing, and (4) rising

backwardation alongside falling physical premiums is a sign that actual

demand is lower than perceived.

The fourth point above needs some explaining. In a tight market,

limited stockpiles lead to backwardation – people paying more for metal

today than in the future. Backwardation should only happen when the

current physical market is very tight. If that’s the case, there should

also be high physical premiums, which are extra amounts paid for actual

metal now (rather than paper metal).

What weird about nickel is that premiums are down sharply, from $200

per tonne a few months ago to negative $50 per tonne today. It’s the

first-time premiums have ever gone negative in China and something that

is very rare across the metals complex. European nickel briquette

premiums are also down 80% in recent months.

The dark blue line below shows physical premiums. The light blue line

shows the difference between current and three-month nickel prices; a

positive Cash-3M is backwardation.

<

This suggests:

· The physical market is not that tight

· Speculation in the paper market is driving the price

· Speculation is not simply investors; nickel users and producers are

also playing games (stockpiling) to boost the price. When they stop,

the price will lose ground rapidly.

The Bottom Line

Nickel may or may not continue its bull run from here. The fact the

physical premiums are so low when prices have gained so much and the

paper market is in backwardation is definitely concerning, enough that I

am not ready to enter the space right now. The fact that nickel spot

price recently stepped back almost 10% reinforces my outlook.

However, in the medium and long term this is a market that has good

opportunity. Stainless steel demand growth is reliable. The battery

space will need more and more Class I nickel with each year. The

pipeline of new projects is very limited, especially if you (like me)

see China struggling with its nickel laterite output mines and HPAL

facilities.

I might be wrong and my hesitation on entering now may mean missing

out on near term upside, but such decisions are common in this sector!

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in Tartisan Nickel | Comments Off on Tartisan #Nickel $TN.ca – A nickel for your thoughts – The price of nickel has run up to a five-year high of late $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 10:29 AM on Wednesday, October 30th, 2019

SPONSOR:ThreeD Capital Inc. (IDK:CSE)

Led by legendary financier, Sheldon Inwentash, ThreeD is a

Canadian-based venture capital firm that only invests in best of breed

small-cap companies which are both defensible and mass scalable. More

than just lip service, Inwentash has financed many of Canada’s biggest

small-cap exits. Click Here For More Information.

IDK: CSE

Twitter’s Dorsey puts another bet on crypto

Bitcoin proponent Twitter CEO Jack Dorsey continues to bet on crypto by investing in CoinList, a two-year-old venture that helps startups raise money through token sales.

The company says it connects investors with thoroughly vetted

blockchain-related companies in compliance with crypto regulations.

CoinList has supported more than $800M of token offerings since August 2017.

Dorsey participated in a recent $10M funding round, the Wall Street Journal reports.

The new capital will help with its plans to offer new services

including a new exchange, CoinList Trade, and a crypto wallet.

Posted by AGORACOM-JC

at 9:00 AM on Wednesday, October 30th, 2019

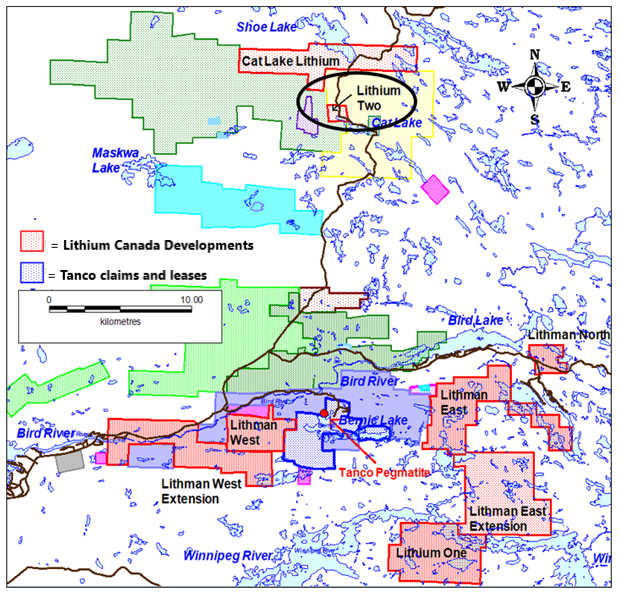

A drill permit has been issued by the Manitoba government for a drill program on the company’s Lithium Two Project.

NAM has 100% ownership of eight pegmatite hosted Lithium and Rare Element Projects in the Winnipeg River Pegmatite Field, located in southeast (SE) Manitoba.

Exploration in SE Manitoba is focused on Lithium-bearing pegmatites.

Archaeological Assessment in progress on Lithium One as part of the drill permit process.

The eight projects are strategically situated within the Winnipeg River Pegmatite Field, which hosts the world-class Tanco Pegmatite that has been mined for Tantalum, Cesium and Spodumene (one of the primary Lithium minerals) in varying capacities, since 1969.

NAM management is finalizing a plan for a 1,500-metre drill program on Lithium Two.

October 30th, 2019 – Rockport, Canada – New Age Metals Inc. (NAM) (TSX.V: NAM; OTCQB: NMTLF; FSE: P7J) New Age Metals is pleased to announce that a drill permit has been issued to the company’s wholly owned subsidiary, Lithium Canada Development by the Manitoba government for the company’s Lithium Two Project located in the Cat Lake area of southeast (SE) Manitoba.

The Winnipeg River Pegmatite Field

The

Winnipeg River-Cat Lake Pegmatite Field in SE Manitoba is host to

numerous pegmatite deposits and contains the world-class Tanco

Pegmatite. The Tanco pegmatite has been mined since 1969 in

varying capacities for spodumene (Li rich mineral), Tantalum and Cesium.

The pegmatite field contains at least 10 pegmatite groups and hosts

hundreds of pegmatite bodies. Many of the pegmatites are lithium

bearing.

The Tanco Mine, which was owned by the

Cabot Corporation, was recently sold to Sinomine Rare Metals Resources

Co. Ltd. (Sinomine) at a purchase price of $130 million ($US). Sinomine

is a joint stock public company based in China, principally engaged in

the provision of geological exploration, mining investment and base

metal chemical manufacturing. This transaction certainly adds new

interest in the region as to the potential of the pegmatite field and

lithium and/or rare element potential in the area. This sale should

advance the Lithium production potential of the area as Lithium Ore feed

may be required in the event that Sinomine commences lithium

production.

Lithium Two Project

The Lithium Two Project is located

approximately 20 kilometres north of the Tanco Mine and is an active

area for Lithium exploration. Several companies are active in the

immediate region, exploring for Lithium.

Surface exploration was carried out on the Lithium Two Project during the summer of 2018 (see News Release October 30th, 2018).

The exploration work was designed to examine the known surface

pegmatites to aid in the determination of drill targets. The field

program also focussed on more detailed structural geological mapping and

mapping of the westward extent of the Eagle Pegmatite. The Lithium Two

Project has several historically known Spodumene bearing pegmatites (see

Figure 2).

Click Image To View Full Size

Figure 1: Manitoba Lithium and Rare Element Projects 2019

The Eagle Pegmatite was drilled in 1947

with a historic (non 43-101 compliant) tonnage estimate of 544,460

tonnes with a grade of 1.4% Li2O to the 61-metre level. These historical

estimates do not use categories that conform to current CIM Definition

Standards on Mineral Resources and Mineral Reserves as outlined in

National Instrument 43-101, Standards of Disclosure for Mineral Projects

(“NI 43-101”) and have not been redefined to conform to current CIM

Definition Standards. A qualified person has not done sufficient work to

classify the historical estimates as current mineral resources and the

Company is not treating the historical estimates as current mineral

resources. Investors are cautioned that the historical estimates do not

mean or imply that economic deposits exist on the properties. The

Company has not undertaken any independent investigation of the

historical estimates or other information contained in this press

release nor has it independently analyzed the results of the previous

exploration work in order to verify the accuracy of the information. The

Company believes that these historical estimates and other information

contained in this news release are relevant to continuing exploration on

the properties as it identifies significant mineralization that will be

the target of future exploration and development.

The Eagle Pegmatite was historically reported to remain open to depth.

The FD5 Pegmatite, located east of the Eagle Pegmatite has never been

drilled. Historic assessment reports revealed a Spodumene bearing

pegmatite drilled in the late 1940’s, located approximately 500 metres

southeast of the Eagle Pegmatite but is not exposed on surface. No

assays were provided in the report at the time. This pegmatite, as well as the Eagle and FD5, will be tested during an upcoming recommended drill program.

Click Image To View Full Size

Figure 2: 2018 Lithium Assays at the Lithium Two Project, SE Manitoba

The Eagle Pegmatite has been mapped on surface for over 850 metres and has surface assays of 0.1 to 3.8% Li2O.

The FD5 pegmatite had surface assays from 0.1 to 3.3% Li2O. In

geological terms, the pegmatites encountered on the Lithium Two Project

are LCT Type (Lithium-Cesium-Tantalum) Pegmatites and are in the

Albite-Spodumene Subgroup. Spodumene is expressed in the pegmatites as

small green blades up to 3 centimetres in length. The Eagle Pegmatite is

a west-northwest to west-striking, vertically dipping, lenticular

pegmatite dyke intruded into mafic volcanics. The widths of the

pegmatite have been measured to be between 2 to 10 metres. The Eagle

Pegmatite system appears to be a swarm of closely spaced pegmatite

bodies.

Phase 1 Drill Program Planning in Progress

A drill program of 1,500 metres is planned

to test three spodumene bearing pegmatite targets. A drill permit has

recently been issued by the Manitoba government.

Lithium One Drill Program

Recently,

NAM engaged White Spruce Archaeology as part of its Exploration

Agreement with the Sagkeeng First Nation to conduct an archaeological

assessment on the proposed drill sites for Lithium One as part of the

drill permitting process. The assessment was completed in October

and the report is pending. A 1,500 metre drill program is planned to

test targets on the Silverleaf pegmatite ( News Release Sept 27, 1018) situated in the Lithium One project area.

NAM/AAZ Property Option Update

JV partner Azincourt Energy (AAZ) and NAM

are in discussions regarding AAZ’s compliance for its contractual

obligations as part of the option agreement with NAM. NAM and AAZ are in

continuing talks regarding a revision to the existing option agreement

or termination.

OPT-IN LIST

If you have not done so already, we encourage you to sign up on our website (www.newagemetals.com) to receive our updated news.

ABOUT NAM’S PGM DIVISION

NAM’s flagship project is its 100% owned River Valley PGM Project (NAM Website – River Valley Project)

in the Sudbury Mining District of Northern Ontario (100 km east of

Sudbury, Ontario). Recently the company announced the results of the

first PEA (see News Release – June 27th, 2019)

completed on the River Valley Project. The PEA has been developed by

various independent consultants – P&E Mining Consultants Inc.

(P&E) was responsible for the open pit mining, surface

infrastructure, tailings facility, and project economics; DRA Americas

Inc. (“DRA”) was responsible for all metallurgical test work and

processing aspects of the Project; and WSP Canada Inc. (“WSP”) was

responsible for the Mineral Resource Estimate. The

PEA is a preliminary report but it has demonstrated that there are

positive economics for a large-scale mining open pit operation, with 14

years of Palladium and Platinum production.

The

Genesis project is a PGM-Cu-Ni property located in the northeastern

Chugach Mountains, 75 paved road miles north of the all-season port city

of Valdez, Alaska. The project is within 3 km of the all-season

paved Richardson Highway and a high capacity electric power line. The

project is covered by 4,144 hectares of State of Alaska mining claims

owned 100% by New Age Metals. Past exploration has revealed the presence

of chromite-associated platinum and palladium mineralization and

stratabound Ni-Cu-PGM mineralization within magmatic layers of the

Tonsina Ultramafic Complex. Pyrrhotite, pentlandite, and chalcopyrite

occur in disseminations and net textured segregations associated with

platinum and palladium sulfides. There has been limited exploration over

the Genesis project and there has been no past exploration drilling on

the project. NAM management is actively seeking an option/joint-venture partner for this road accessible PGM and Multiple Element Project.

QUALIFIED PERSON

The contents contained herein that

relate to exploration results or geological aspects is based on

information compiled, reviewed or prepared by Carey Galeschuk, P. Geo., a

consulting geoscientist for New Age Metals. Mr. Galeschuk is the

Qualified Person as defined by National Instrument 43-101 and has

reviewed and approved the technical content of this news release.

On behalf of the Board of Directors

“Harry Barr”

Harry G. Barr

Chairman and CEO

Neither the TSX Venture Exchange nor its

Regulation Services Provider (as that term is defined in the policies

of the TSX Venture Exchange) accepts responsibility for the adequacy or

accuracy of this release.

Cautionary Note Regarding Forward

Looking Statements: This release contains forward-looking statements

that involve risks and uncertainties. These statements may differ

materially from actual future events or results and are based on current

expectations or beliefs. For this purpose, statements of historical

fact may be deemed to be forward-looking statements. In addition,

forward-looking statements include statements in which the Company uses

words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”,

“confident”, “intend”, “strategy”, “plan”, “will”, “estimate”,

“project”, “goal”, “target”, “prospects”, “optimistic” or similar

expressions. These statements by their nature involve risks and

uncertainties, and actual results may differ materially depending on a

variety of important factors, including, among others, the Company’s

ability and continuation of efforts to timely and completely make

available adequate current public information, additional or different

regulatory and legal requirements and restrictions that may be imposed,

and other factors as may be discussed in the documents filed by the

Company on SEDAR (www.sedar.com), including the most recent reports that

identify important risk factors that could cause actual results to

differ from those contained in the forward-looking statements. The

Company does not undertake any obligation to review or confirm analysts’

expectations or estimates or to release publicly any revisions to any

forward-looking statements to reflect events or circumstances after the

date hereof or to reflect the occurrence of unanticipated events.

Investors should not place undue reliance on forward-looking statements.

Posted by AGORACOM-JC

at 8:24 AM on Wednesday, October 30th, 2019

Company has completed a harvest totaling 13,000 lbs of dried bio-mass of hemp from the Oregon hemp farm.

The dried bio-mass hemp is currently being stored at a local drying facility located near Eugene, Oregon.

The value for the crop in its current state is estimated to be worth $200,000 – $300,000 USD.

VANCOUVER, British Columbia, Oct. 30, 2019 — PRIMO NUTRACEUTICALS INC. (CSE: PRMO) (OTC: BUGVF) (FSE: 8BV) (DEU: 8BV) (MUN: 8BV) (STU: 8BV) (“Primo” or the “Company”)is pleased to announce that further to the Company news release dated October 1, 2019 the Company has completed a harvest totaling 13,000 lbs of dried bio-mass of hemp from the Oregon hemp farm. The dried bio-mass hemp is currently being stored at a local drying facility located near Eugene, Oregon. The value for the crop in its current state is estimated to be worth $200,000 – $300,000 USD. This will be added to the 28 kilo grams of crude oil currently in inventor from last year’s harvest.Â

The completion of the 2019 harvest season is a major milestone for

the company and for the hemp farm in Oregon, as this is the first year

hemp has been federally legal since the Farm Bill was passed. This year

in Oregon alone there are nearly 63,000 acres registered growing hemp

compared to the 11,500 acres growing hemp registered in 2018. This is a

significant increase in the amount of hemp being grown, which solidifies

the Primo strategy of providing drying facilities to the ever growing

hemp market in Oregon. Primo plans to have its first drying facility

built and in operation by the end of the first quarter of next year.

President, Andy Jagpal Comments:

“I am very proud and excited with the amount of dried hemp that was

harvested as it surpassed our expectations by a few thousand pounds.

During a time in the cannabis market where companies have spent tens of

millions of dollars building out facilities and cultivation

infrastructure and have little to show for it, we have two harvests

under our belt and product in inventory ready for sale. Together with

this year’s harvest and last year’s inventory we estimate our inventory

alone to be worth between $400,000 and $500,000 USD.â€

VP Sales & Distribution, Andy Dhaliwal Comments:

“The on-hand inventory and quality of the hemp as starting material

is a major advantage in the current marketplace. While the revenue

opportunities from the harvest are extremely promising, the hemp

processing infrastructure supports the expansion of our in-house product

lines, and increases our white-label offering to the USA market as

well. Both of which are tremendous assets for the company.â€

About Primo Nutraceuticals, Inc.

Primo Nutraceuticals Inc. (“Primo” or the “Company”) provides

strategic capital to the thriving cannabis cultivation sector through

ownership and development of commercial real estate and farm friendly

properties. Primo is dedicated to funding the rapid growth in

production, processing, retail and branding of cannabis and cannabis

related products in Canada and the United States. Primo provides fully

built out turnkey facilities equipped with state-of-the-art growing

infrastructure to cannabis growers and processors. In addition to the

Company’s flagship hemp project in Oregon State and the Greenhouse

campus in Washington State, Primo has invested in several brands and is

pursuing partnerships with retailers and distribution companies in

Canada and the United States. Primo’s management is in the process of

building a corporate road map to further vertically integrate the

Company, specifically by way of “Primo†branded retail outlets –

offering “Thrive,” “Primo,” and a selection of curated partner brands.

The Company possesses proprietary formulas for cannabis edibles,

topical, and tinctures. Primo is focused on building a strong presence

in the hemp industry with the objective of extracting and

selling cannabinoids (CBD) products in both Canada and the United

States.

On behalf of the Board of Directors PRIMO NUTRACEUTICALS INC.

FORWARD LOOKING STATEMENTS: This news release

contains certain forward-looking statements within the meaning of

Canadian securities laws. Forward-looking statements are based on the

expectations and opinions of the Company’s management on the date the

statements are made. The assumptions used in the preparation of such

statements, although considered reasonable at the time of preparation,

may prove to be imprecise and, as such, undue reliance should not be

placed on forward-looking statements. The Company expressly disclaims

any intention or obligation to update or revise any forward-looking

statements whether as a result of new information, future events or

otherwise.

No regulatory authority has approved or disapproved the information contained in this news release.

Posted by AGORACOM-JC

at 9:36 AM on Wednesday, October 23rd, 2019

When the Wall Street Journal calls your Gold Report “The Gold Standard Of Gold Research”, it is safe to say you are a global influencer and expert in all things gold.

This is Ronnie Stoeferle, whose “In Gold We Trust” report has also been downloaded 1.8 million times in English, German and Mandarin in case anyone had any doubt as to his expertise.

Today, Ronnie became the founding member of the Affinity Metals (AFF:TSXV) Advisory Board, which implies that we can expect others to be appointed as well. Why would Ronnie join a company with a market cap under $5,000,000? You’ll have to watch the interview to find out … but here are a couple of hints:

1. Affinity Metals flagship project, the Regal, has reported HISTORICAL reserves of 590,703 tonnes grading 71.6 grams per tonne silver, 2.66 per cent lead, 1.26 per cent zinc, 1.1 per cent copper, 0.13 per cent tin and 0.015 per cent tungsten. These were prepated prior to 43-101 standards and should not be relied upon until they are brought into compliance with 43-101 standards.

2. A Technical Report, which was prepared in 1971 using a silver price of $1.75 per troy ounce, makes a positive recommendation for production, including the establishment of a 500 ton per day concentrator with a 400 ton per day silver, lead and zinc circuit and a 100 ton per day tin, tungsten and copper circuit.

These are just 2 factors that led Ronnie to declare that Affnity Metals is “one of the largest investments in my private portfolio”.

Grab your favourite beverage, kick back and watch this great interview with both Ronnie and Affinity CEO, Rob Edwards.

Posted by AGORACOM-JC

at 5:45 PM on Friday, October 18th, 2019

HPQ Silicon makes its strongest case ever for the lead it has taken in the commercialization of its’

Solar grade silicon;

Silicon wafers for Li-ion batteries

High purity silicon for high value niche applications;

Metallurgical grade silicon at prices the industry has never seen before;

More than just lip service that we have typically come to expect from 98% of small cap companies, the Company’s pilot plant is about to go live and produce test samples of silicon wafers for batteries and is supported by not 1 but 2 (TWO) world class technology partners that validate both the HPQ process and commercialization plan.

This is a powerful presentation that is worthy of your time to watch and learn about the rise of HPQ Silicon.