Posted by AGORACOM

at 11:07 AM on Tuesday, September 1st, 2020

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

The deepest hole extends to 838.4 metres, intersecting mineralization grading 4.25% nickel and 1.38% copper over 10.7 metres

The deposit remains open at depth

Tartisan completed a Spectral Analysis Survey that identified the Kenbridge Deposit, and has shown a possible extension and three additional trends

Owns 17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property and are drilling their Iska Iska Pollymetallic project in Bolivia

Tartisan currently owns close to 4 million ELO shares

Tartisan owns close to 1,700,000 shares in Class 1 Nickel (CSE:NICO)

Tartisan vended the Alexo- Kelex asset to Class 1 Nickel, who recently listed on CSE

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is equipped with a 623m deep shaft and has never been mined

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits

Plans for Kenbridge include updating PEA, advancing the project through to feasibility and exploring the open mineralization at depth

Recent News

Company has completed a Spectral Analysis Survey

Survey covered the patented and single-cell mining claims that make up the historic land position which contains the Kenbridge Deposit and the surrounding area, identifying several new exploration targets not only for nickel, copper, cobalt, but also for potential gold occurrences

Analysis Survey shows the distribution and intensity of up to 304 minerals, with the first pass showing up to 16 minerals

Each mineral can be classified into an exploration relevance for base metals, precious metals and industrial metals

Tartisan CEO Mark Appleby said, “the survey picked out the Kenbridge Deposit, and has shown the possible extension to the Kenbridge Deposit and three additional trends that relate directly to underlying geology and structure implicit in the Kenbridge Deposit. Of significant interest, the survey found two gold trends as well, which include the Violet and Nina historic gold occurrences. One of the occurrences is almost 54 hectares in size and covers almost all of three of our staked claims on the border of the Kenbridge property.”

DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM

at 10:06 AM on Thursday, August 27th, 2020

SEOUL (Reuters) – Tesla Inc (TSLA.O) CEO Elon Musk has suggested the U.S. electric carmaker may be able to mass produce batteries with 50% more energy density in three to four years, which could even enable electric airplanes.

SEOUL (Reuters) – Tesla Inc (TSLA.O) CEO Elon Musk has suggested the U.S. electric carmaker may be able to mass produce batteries with 50% more energy density in three to four years, which could even enable electric airplanes.

His comments came as speculation is growing about announcements at Tesla’s anticipated “Battery Day” event where it is expected to reveal how it has improved its battery performance.

“400 Wh/kg *with* high cycle life, produced in volume (not just a lab) is not far. Probably 3 to 4 years,” Musk tweeted on Monday in response to a Twitter thread by Sam Korus, an analyst at ARK Investment Management LLC, about why Musk keeps hinting at a Tesla electric plane.

Researchers have said the energy density of Panasonic’s (6752.T) “2170” batteries used in Tesla’s Model 3 is around 260 Wh/kg, meaning a 50% jump from the current energy density which is key to achieving a longer driving range.

Musk said last year that for electric flight to work, the energy density of batteries needed to improve to over 400 Wh/kg, a threshold which may be achieved in five years.

The electric car manufacturer also showed an image where a number of dots are clustered in line formations, sparking speculation among media and fans about what it will reveal at the event. (here)

South Korean battery expert Park Chul-wan said the image may hint at “silicon nanowire anode,” a breakthrough technology which can potentially increase both battery energy density and battery life sharply.

Panasonic Corp (6752.T) earlier told Reuters that it plans to boost the energy density of the original “2170” battery cells it supplies to Tesla by 20% in five years.

Tesla is also working with China’s Contemporary Amperex Technology Ltd (CATL) (300750.SZ) to introduce a new low-cost, long-life battery in its Model 3 sedan in China later this year or early next year, with the batteries designed to last for a million miles of use, Reuters reported in May.

Tesla has said its Battery Day will take place on the same day as its 2020 annual meeting of shareholders on Sept. 22.

A very “limited number of stockholders” will be able to attend both of the events due to pandemic-related restrictions, Tesla said, and a lottery will be held to select attendees.

Posted by AGORACOM

at 9:29 AM on Tuesday, August 25th, 2020

“I’d just like to re-emphasize, any mining companies out there, please mine more nickel,” said Musk

Nickel is arguably the single most important metal component in EV batteries.

In the popular imagination, lithium is the element that powers EVs. However, as Elon Musk has pointed out, the term “lithium-ion batteries” is something of a misnomer, because they don’t really contain that much lithium. “Although [they’re] called lithium-ion, the actual percentage of lithium in a lithium-ion cell is approximately 2%,” Musk explained at Tesla’s 2016 shareholder meeting. “Technically, our cells should be called nickel-graphite, because the primary constituent in the cell as a whole is nickel.”

More recently, Musk reiterated the importance of nickel, and made what sounded to some like an urgent plea for more of the stuff. “I’d just like to re-emphasise, any mining companies out there, please mine more nickel,” said Musk during Tesla’s latest quarterly conference call. “Wherever you are in the world, please mine more nickel and…go for efficiency, obviously environmentally-friendly nickel mining at high volume. Tesla will give you a giant contract for a long period of time, if you mine nickel efficiently and in an environmentally sensitive way.”

However, meeting the expected surge in demand for element #28 may not be so easy, because of various supply-side issues. In a recent interview with Kitco News, Michael Beck, Managing Director at Regent Advisors, said he sees something of a “perfect storm” brewing in the nickel trade.

A Tesla Model 3 contains around 30 kilograms of nickel, Beck told Kitco’s Michael McCrae. “Nickel is probably the single most important metal component in battery fabrication. It’s where all of the energy is stored, and increasingly battery chemistries are being refined to allow the inclusion of as much nickel as possible. The more nickel, the higher the energy density of the battery.”

The spotlight on nickel is a recent development. Nickel prices collapsed in 2007, and there’s been little development of new capacity since then, says Beck. “In this intervening almost 12 years there was no material investment in new nickel capacity. The last 12 years has been a drawdown of excess inventory, and that’s coming to an end. The ramp-up of demand is just beginning.”

The long lead time for bringing new nickel mines into production is another constraining factor. “It takes 7 to 10 years to bring on new nickel projects,” says Beck. “So, you have the makings of a perfect storm. You have a baked-in structural deficit for the next 12 years…you have inventories in the next 18 months going down to almost zero. You also have this new demand source that never existed for nickel.”

Above: Ken Hoffman, senior expert at McKinsey, weighs in on Tesla’s need for nickel in order to expedite the EV revolution (YouTube: Kitco NEWS)

All that would seem to add up to an investment opportunity for somebody. “In the universe of metals, [nickel is] our favorite,” says Beck. “We think in the next two to three years you’re going to see a major up-tick of the nickel price…as shortages emerge, and that’s what’s going to be required to get new investment in the sector.”

So, what companies are poised to take advantage of the coming nickel rush? “Maybe the most interesting in the larger cap of established players is Norilsk,” says Beck. “They’re the number-two nickel producer, and they’re based in Russia. That’s probably the single best large-cap way to get exposure to nickel. It’s a major producer of the metal, and when nickel goes up, their share price goes up accordingly. At the smaller cap end of the spectrum, there are a bunch of smallish nickel explorers and emerging developers.”

Over the next few years, Beck believes that nickel shortages will emerge, and most companies with nickel exposure will benefit. However, there’s another factor in play. Tesla and other EV-makers are naturally eager to get their raw materials from sustainable sources. The industry has invested much effort and cash in cleaning up its supply chain for cobalt. Elon’s recent plea for nickel specified that it needed to be mined in an environmentally sensitive way. (Norilsk, by the way, has recently been involved in not one but two oil spills in Russia’s Arctic region.)

Vancouver-based Giga Metals quickly responded to Elon’s appeal, saying that it has a source of environmentally-responsible nickel in development. As Matthew Hall reports in Mining Technology, Giga Metals owns a property called Turnagain in north-central British Columbia, which it says is one of the largest undeveloped sulphide nickel projects in the world, and also contains cobalt.

Canada has plenty of nickel mines, but Giga Metals has a unique vision for the Turnagain mine. “Our goal is to be the world’s first carbon-neutral mine,” said Giga Metals President Martin Vydra. “We plan to use power from BC Hydro’s clean energy grid, which will involve more capital expenditure than the alternatives, but is the right thing to do.”

Above: Tesla’s Model 3 (Source: EVANNEX; Photo by Casey Murphy)

“If you want environmentally-responsible nickel, I really think you have to look at sulphide deposits in first-world jurisdictions such as Canada and Australia,” said Giga Metals CEO Mark Jarvis. “Canada has several very large, low-grade, open-pittable sulphide nickel deposits waiting to be developed, including Canada Nickel’s Crawford deposit, Waterton’s Dumont deposit and our own Turnagain deposit. Canada has some of the toughest environmental regulations in the world, so if you buy your nickel from Canada, you can be assured that this part of your supply chain is ethically sourced.”

Posted by AGORACOM-JC

at 9:15 PM on Sunday, March 24th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

TN: CSE

Nickel has comeback whiff as EVs fuel demand forecasts

Despite its recent run, the nickel price remains some way from the

“excitement levels†of yesteryear. But as this week’s BHP-Mincor deal

shows, there is a buzz about what could be around the corner, with

inventories falling and demand forecast to soar thanks to nickel’s key

role in lithium batteries.

The swagger of the nickel companies at a battery metals conference in Perth during the week was palpable.

Nickel brigade is confident that excitement-inducing prices are on the way, hence their swagger

After a heroic run to $US7/lb in the middle of last year, the price

got beaten up something shocking in the second half with just about

everything else on US-China trade war fears.

The price has since climbed off the December lows of under $US5/lb to

get back to just under $US6/lb in recent days, leaving it well short of

the $US9/lb pricing that historically starts to get everyone excited

about the metal.

But the nickel brigade is confident that excitement-inducing prices are on the way, hence their swagger.

They point to the ongoing drawdown in LME/SHFE stocks needed to meet

demand from the stainless steel sector in the here-and-now, let alone

the demand tsunami coming from the electric vehicle/battery storage

revolution.

Nickel – particularly the almost boutique, in terms of supply, nickel

sulphide type – is not ready for the revolution, unlike some of the

other key battery materials such as lithium and graphite.

Under-investment has led to a dearth of new discoveries and new

developments, leaving forecasters wondering where the new supply is

going to come from to meet the expected growth in demand from the

EV/battery revolution.

That assumes there is no breakthrough anytime time soon in making the

world’s more abundant laterite nickel ores more competitive in the

supply of high-grade nickel product suitable for use in battery

manufacturing.

There was no fear at the conference of that happening anytime soon.

In broad terms, the nickel boys and girls reckon nickel demand from

the EV/battery sectors could well match that of the (also growing)

stainless sector (73% of the current 2.2mtpa market compared with 5% for

batteries) sometime in the 2020s/early 2030s.

All that explains the renaissance of Australia’s Western Australian-centric nickel industry.

BHP (ASX:BHP) is spending up big on its pivot to the supply of nickel

sulphate to battery makers and it is again investing in sustaining

production at its Nickel West unit out to at least 2040.

Other miners that eventually shut down when the nickel price got ugly

post-2008/2009 are plotting their return, and nickel-focussed explorers

are again getting a good hearing.

Then there are the private equity groups sniffing around the WA scene

for exposure to the nickel thematic before the potentially-manic rush

to secure supplies by end-users – as already witnessed in the lithium

sector – takes hold of the metal.

Some of that was reflected in the move by US private equity group

Black Mountain on to the Poseidon Nickel (ASX:POS) register in a big way

last year and its acquisition of the mothballed Lanfranchi mine from

Panoramic (ASX:PAN).

Now it has to be said that there is no boom in nickel equities just yet.

But stand back if the EV/battery thematic unfolds, as most suspect it

will. Nickel can be the most volatile of metals (small market and slow

response times) and a sharp and lasting price spike could be upon us

before we know it.

Mincor Resources

Mincor’s (ASX:MCR) new managing director of six weeks David Southam

looks sharp in a cuff-linked suit but he is not one to swagger.

Nevertheless, he is set to be as upbeat as they come on the nickel

market and his production revitalisation plans for the group’s Kambalda

operations when he hits the Eastern States next week on an investor

roadshow.

Southam called time on eight years as an executive director at the

$615m nickel producer Western Areas (ASX:WSA) to take on the role at

Mincor. And why wouldn’t he? Western Areas stands to benefit from the

suggested nickel upturn more than most, but there is greater leverage to

the upside at the $90m Mincor.

That is reflected in the fact that back in 2007/2008 when nickel shot

to more than $US20/lb, Mincor was a $1 billion company sitting

comfortably inside the ASX 200, with peak production of 16,500t of

nickel-in-concentrates.

Then the nickel price rot set in (due to the rise of Chinese NPI

production and the absence of the EV/battery thematic), forcing Mincor

to first curtail its nickel operations and then shut them altogether by

early 2016, pending the now unfolding upturn for the metal.

The mines were put on care and maintenance and in the meantime,

Mincor got a handy little gold open-cut gold mining operation going

which continues to help pay the bills.

But the main game has always been plotting a return to nickel

production from existing mines (Ken/McMahon and Durkin North), and a

development of the Cassini discovery.

For that to happen four things are needed. The first is a supportive

nickel price. Thanks to the lower US exchange rate, the Australian

dollar nickel price is just about there to mount an economic case for a

restart.

The second requirement is to avoid the capex slug of having to build

its own nickel concentrator by securing a new agreement to replace the

20-year-old one that recently expired with BHP’s Nickel West.

That was ticked off earlier this week when Southam’s experience with

offtake negotiations at Western Areas came to the fore, with Mincor

securing a “modern†agreement on “substantially†better terms, again

with the logical offtake partner, BHP.

The third requirement is to ensure enough mining inventory to

underpin an initial five-year mine life. Mincor is getting close to

those numbers already but will nevertheless be ramping up its resource

extension drilling.

With one, two and three locked in, attention will turn to funding the return to production, expected to cost about $50-$60m.

That looks to be very do-able, given a re-start pitched towards

achieving annual production of 12,000-14,000t of nickel-in-concentrate

(not far off what used to support a $1bn market cap in the heady days of

2008) is the plan.

Posted by AGORACOM-JC

at 2:30 PM on Friday, February 8th, 2019

.

Announced the appointment of Mr. Aamer Siddiqui as Chief Financial Officer (CFO) of the Company.

Mr. Siddiqui is a Chartered Professional Accountant(CPA) and Chartered Accountant(CA), Chartered Professional Accountants of Canada.

TORONTO, ON / February 8, 2019 / Tartisan Nickel Corp. (CSE: TN, FSE: A2DPCM) (“Tartisan”, or the “Company”) is pleased to announce the appointment of Mr. Aamer Siddiqui as Chief Financial Officer (CFO) of the Company. Mr. Siddiqui is a Chartered Professional Accountant(CPA) and Chartered Accountant(CA), Chartered Professional Accountants of Canada.

Additionally, the Company reports that Tartisan Nickel has engaged

Marrelli Support Services Inc. to provide accounting support services to

the Company.

The Board of Directors of Tartisan Nickel would like to thank

outgoing CFO, Mr. Dan Fuoco, for his support and efforts during his

tenure and wish him well in his new endeavours.

About Tartisan Nickel Corp

The Company is a Canadian mineral exploration and development company

which owns the Kenbridge Nickel-Copper- Cobalt project in Ontario,

Canada. In addition, Tartisan owns a 100% stake in the Don Pancho

Zinc-Manganese Project and a 100% stake in the Ichuna Copper-Silver

Project, both located in Peru. Tartisan Nickel Corp also owns an equity

stake (6 million shares and 3 million full warrants at 40c per share),

in Eloro Resources Ltd. which is exploring the low-sulphidation

epithermal La Victoria Gold/Silver Project, located in Ancash, Peru.

The Company also owns 1,750,000 common shares of VaniCom Resources

Ltd. a private Australian exploration and development resource company.

Tartisan Nickel Corp. common shares are listed on the Canadian

Securities Exchange (CSE: TN, FSE: A2DPCM). Currently, there are

99,703,550 shares outstanding (108,803,550 fully diluted).

For further information, please contact Mr. D. Mark Appleby,

President & CEO and a Director of the Company, at 416-804-0280 ([email protected]). Additional information about Tartisan can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

Jim Steel MBA P.Geo. is the Qualified Person under NI 43-101 and has

read and approved the technical content of this News Release.

This news release may contain forward-looking statements

including but not limited to comments regarding the timing and content

of upcoming work programs, geological interpretations, receipt of

property titles, potential mineral recovery processes, etc.

Forward-looking statements address future events and conditions and

therefore, involve inherent risks and uncertainties. Actual results may

differ materially from those currently anticipated in such statements.

The Canadian Securities Exchange (operated by CNSX Markets Inc.)

has neither approved nor disapproved of the contents of this press

release.

Posted by AGORACOM-JC

at 1:21 PM on Friday, February 8th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) The company’s Kenbridge Property

has a measured and indicated resource of 7.14 million tonnes at 0.62%

nickel, 0.33% copper. Tartisan also has interests in Peru, including a

20 percent equity stake in Eloro Resources and 2 percent NSR in their La

Victoria property. Click her for more information

TN:CSE

———————

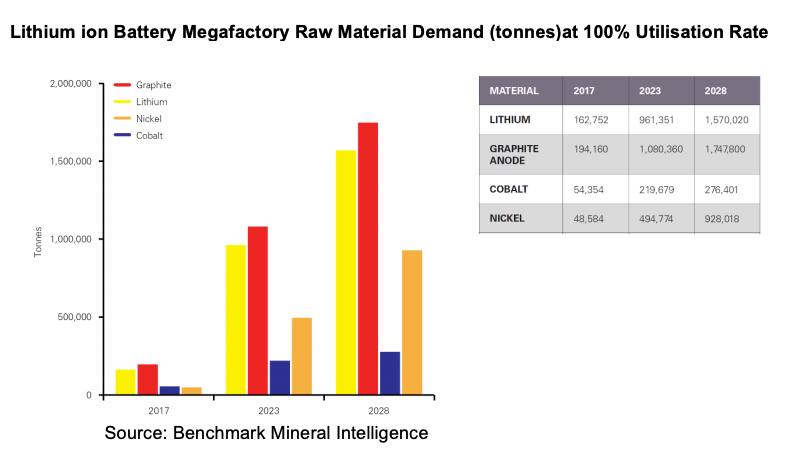

Megafactories buildout could up nickel demand in batteries 19 fold—Benchmark

Moores said that these megafactories are being built almost exclusively to make lithium ion battery cells using two chemistries: nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminium (NCA)

“Under this scenario, lithium demand will increase by over eight times, graphite anode by over seven times, nickel by a massive 19 times

It was encouraging for miners when Simon Moores, managing director, Benchmark Mineral Intelligence, testified before the U.S. Senate Committee on Energy and Natural Resources on Tuesday.

Moores was summoned by the Senate Committee to testify on the

lithium, cobalt, nickel and graphite supply chains for energy storage.

“Benchmark Mineral Intelligence is now tracking 70 lithium ion

battery megafactories under construction across four continents, 46 of

which are based in China with only five currently planned for the US.

When I gave my last testimony in October 2017, the global total was at

17,” Moores said.

Moores said that these megafactories are being built almost

exclusively to make lithium ion battery cells using two chemistries:

nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminium (NCA).

“This means the supply of lithium, cobalt, nickel and manganese to

produce the cathode for these cells, alongside graphite to produce

battery anodes, needs to rapidly evolve for the 21st century,” Moores

testified.

Moores presented a chart based on the assumption that all of these megafactories are built and run at 100% capacity utilization.

“Under this scenario, lithium demand will increase by over eight

times, graphite anode by over seven times, nickel by a massive 19 times,

and cobalt demand will rise four-fold, which takes into account the

industry trend of reducing cobalt usage in a battery,” Moores testified.

Posted by AGORACOM-JC

at 10:12 AM on Monday, January 14th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) The company’s Kenbridge Property

has a measured and indicated resource of 7.14 million tonnes at 0.62%

nickel, 0.33% copper. Tartisan also has interests in Peru, including a

20 percent equity stake in Eloro Resources and 2 percent NSR in their La

Victoria property. Click her for more information

TN:CSE

———————

Investors bet on nickel prices and nickel stocks to rally in 2019

Class 1 nickel demand forecast to increase 17 fold from 2017 to 2025 due to the EV boom

According to McKinsey research if annual electric vehicle (EV) production reaches 31 million vehicles by 2025 as expected then demand for high-purity class 1 nickel is likely to increase significantly from 33 Kt in 2017 to 570 Kt in 2025

Use of nickel has been traced as far back as 3,500 BC. In more recent

times nickel has been used in coins (a nickel), but is best known for

its use in stainless steel driven mostly by Chinese construction. With

the current negative sentiment due to the US-China trade war and some

mild slowdown in China, nickel prices have fallen to a low level, as

have the nickel miners. Provided we don’t head into a significant China

or global slowdown, any resolution in the trade war with China should

lead to some recovery in nickel prices and the nickel miner’s stock

prices.

Class 1 nickel demand forecast to increase 17 fold from 2017 to 2025 due to the EV boom

According to McKinsey research if annual electric vehicle (EV)

production reaches 31 million vehicles by 2025 as expected then demand

for high-purity class 1 nickel is likely to increase significantly from

33 Kt in 2017 to 570 Kt in 2025. Class 1 nickel is the “high purityâ€

nickel that is used in electric vehicle lithium ion batteries. The

stainless steel industry uses both class 1 and class 2 nickel (lower

purity) and is the main driver of overall nickel demand.

McKinsey also states that “a shortfall in class 1 nickel production

seems increasingly likely as current low nickel prices do not support

class 1 nickel capacity expansions and alternative strategies, as a

result, not only will nickel prices likely need to move towards

incentive pricing but the future pricing mechanism is likely to reflect

two distinct nickel products: class 1 and class 2. At the same time we

expect to see two distinct nickel price mechanisms emerge reflecting two

distinct commodities: class 2 nickel, primarily for use in stainless

steel production, trading at a lower price that reflects its abundant

supply; and class 1 nickel trading at LME prices – or above for high-end

nickel powders and pellets used to make nickel sulfates – reflecting

required incentive prices.â€

The key to understand here is that the nickel sulfide ore miners have

a distinct cost advantage when producing the nickel sulfate required

for EV batteries, and demand for class 1 (high purity) nickel is set to

skyrocket.