Posted by AGORACOM

at 3:31 PM on Friday, January 31st, 2020

SPONSOR: ZEN Graphene Solutions: An emerging advanced materials and graphene development company with a focus on new solutions using pure graphene and other two-dimensional materials. Our competitive advantage relies on the unique qualities of our multi-decade supply of precursor materials in the Albany Graphite Deposit. Independent labs in Japan, UK, Israel, USA and Canada confirm this. Click here for more information

The recent report published on Natural Graphite Market Research Report

analyzes various factors impacting the growth trajectory of this

industry. Primary and secondary research is employed to determine the

development aspects and growth path in Natural Graphite Market on the

global, regional and country-level scale. The historic, present and

forecast situations impending the Natural Graphite Industry dynamics,

competition as well as growth constraints are comprehensively studied.

This report is a complete blend of technological innovations, market

risks, opportunities, risks, challenges, and niche Natural Graphite

Industry segments.

Major companies present globally in this report are as follows:

Steel & Refractories Carbon brushes Batteries Automotive parts Lubricants Others

The important market trends, prominent players, product portfolio, manufacturing cost analysis, product types and pricing structure are presented. All crucial factors like Natural Graphite market dynamics, challenges, opportunities, restraints are studied in this report.Â

The up-to-date market information presents the competitive structure

of Natural Graphite Industry to help players in analyzing the

competitive structure for growth and profitability. The notable features

of this report are Natural Graphite Market share based on each product

type, application, player, and region. Profit estimation for all market

segments and sub-segments and consumption ratio.

Key Deliverables of Natural Graphite Research Report are mentioned below:

Renumeration analysis for each application is covered.

Market share per Natural Graphite application is projected during 2020-2026. Consumption aspects for the same are covered.

Natural Graphite Market drivers which will enhance the commercialization matrix to enhance the business sphere is explained.

Vital information regarding challenges, risks, SWOT analysis of top players, and market share is covered.

Consumption rates in Natural Graphite Industry for major regions namely North America, Europe, Asia-Pacific, MEA, South America and the rest of the world is covered.Â

Research Methodology of Natural Graphite Market:

The primary and secondary research methodology is used to gather data

on parent and peer Natural Graphite Market. Industry experts across the

value chain participate in validating the market size, revenue share,

supply-demand scenario, and other key findings. The top-down and

bottom-up approach is used in analyzing the complete market size and

share. The key opinion leaders of Natural Graphite Industry like

marketing directors, VPs, CEOs, technology directors, R&D managers

are interviewed to gather information on supply and demand aspects.

For secondary data sources information is gathered from company

investor reports, annual reports, press releases, government and company

databases, certified journals, publications, and other various other

third-party sources.

Table of Contents Is Segmented As Follows:

Report Overview: Product definition, overview, scope, growth rate comparison by type, application, and region from 2020-2026 is covered.

Executive Summary: Vital information on industry trends, Natural Graphite market size by region and growth rate for the same is provided.

Profiling of Top Natural Graphite Industry players:

All top market players are analyzed based on gross margin, price

revenue, sales, production, and their company details are covered.

Regional Analysis: Top regions and countries are analyzed to gauge the Natural Graphite industry potential and presence on the basis of market size by product type, application, and market forecast. The complete analysis period is from 2014-2026.Â

Posted by AGORACOM

at 2:02 PM on Friday, January 31st, 2020

SPONSOR: Lomiko Metals is focused on the exploration and development of minerals for the new green economy such as lithium and graphite. Lomiko owns 80% of the high-grade La Loutre graphite Property , Lac Des Iles Graphite Property and the 100% owned Quatre Milles Graphite Property. Lomiko is uniquely poised to supply the growing EV battery market. Click Here For More Information

UPS’ venture capital arm, UPS Ventures, has completed a minority investment in Arrival,

which makes electric vehicle (EV) platforms and purpose-built vehicles.

Along with the investment in Arrival, UPS also announced a commitment

to purchase 10,000 electric vehicles to be built for UPS with priority

access to purchase additional electric vehicles.

UPS will collaborate with Arrival to develop a wide range of electric

vehicles with Advanced Driver-Assistance Systems (ADAS). The technology

is designed to increase safety and operating efficiencies, including

the potential for automated movements in UPS depots.

UPS will initiate testing ADAS features later in 2020. Future vehicle

purchases are contingent on successful tests of initial vehicles.

Vehicle purchase prices will not be disclosed.

UPS continues to build an integrated fleet of electric vehicles,

combined with innovative, large-scale fleet charging technology. As

mega-trends like population growth, urban migration, and e-commerce

continue to accelerate, we recognize the need to work with partners

around the world to solve both road congestion and pollution challenges

for our customers and the communities we serve.

Electric vehicles form a cornerstone to our sustainable urban

delivery strategies. Taking an active investment role in Arrival enables

UPS to collaborate on the design and production of the world’s most

advanced electric delivery vehicles.—Juan Perez, UPS chief information and engineering officer

Arrival takes a ground-up approach to the design and production of

its electric vehicles, enabling an efficient path toward mass adoption.

The company produces its own major core vehicle components: chassis,

powertrain, body and electronic controls. Arrival vehicles also use a

modular design with standardized parts, a method that reduces

maintenance and other costs of ownership.

UPS has been a strong strategic partner of Arrival’s, providing

valuable insight into how electric delivery vans are used on the road

and, importantly, how they can be completely optimized for drivers.

Together, our teams have been working hard to create bespoke electric

vehicles, based on our flexible skateboard platforms that meet the

end-to-end needs of UPS from driving, loading/unloading and back-office

operations. We are pleased that today’s investment and vehicle order

creates even closer ties between our two companies.—Denis Sverdlov, Arrival chief executive

Arrival will build the vehicles in micro-factories, using

lightweight, durable materials the company designs and creates in-house.

As an investor, UPS has the option to fast-track orders as necessary. UPS expects to deploy the EVs in Europe and North America.

Arrival is the first commercial vehicle manufacturer to provide

purpose-built electric delivery vehicles to UPS’ specifications and with

a production strategy for global scale. Since 2016, UPS and Arrival

have collaborated to develop concepts of different vehicles sizes.

The companies previously announced they would develop a

state-of-the-art pilot fleet of 35 electric delivery vehicles to be

trialed in London and Paris. Additionally, UPS announced a pioneering

new approach to electric charging and storage that has now been deployed

in UPS’s central London facility.

Posted by AGORACOM

at 2:17 PM on Thursday, January 30th, 2020

SPONSOR: Vertical Exploration is developing its St. Onge Wollastonite as a soil additive for optimizing marijuana growth. Recently engaged AGRINOVA’s Phase 1 Reseach program also demonstrated Wollastonite can potentially become BNQ certified for agricultural use in Quebec. Recently signed distribution agreement with AREV Brands International to Supply St-Onge Wollastonite to the Cannabis and Hemp Industries. Click Here for More Info.

The former NYCO Minerals wollastonite mine. Photo by Carl Heilman II.

The Imerys ore processing operation in Willsboro is closed until

further notice for cleaning of asbestos that has contaminated its

wollastonite products.

A representative of union workers at the plant said the plant

shutdown is temporary, and a plant spokesman preferred to call it a

suspension of work.

The France-based Imerys, which acquired the former NYCO Minerals

mining and processing operations in 2016, learned of the problem this

summer from a customer. The closure brings the latest round of job uncertainties for a mine that

New York voters in 2013 agreed to support by amending the state

constitution to allow an Adirondack land swap that has yet to happen.

“A third party told them about asbestos. It’s in the ore,†said Ray

Bettis, a representative of the United Auto Workers, the union for about

40 workers at the processing operation in Willsboro.

He said the entire workforce was called into a meeting on Wednesday

afternoon. Many were relieved that the announcement was not that the

plant was closing altogether, Bettis said.

Ryan Toohey, a spokesman for the company, confirmed the contamination

problem and said the company intends to reopen for business. He

emphasized the plant’s difficulties are not related to the bankruptcy

protection sought on Wednesday by Imerys Talc America.

The Chapter 11 bankruptcy announcement was related to lawsuits

alleging that the Imerys Talc subsidiaries are liable for products that

have caused ovarian cancer and asbestos-related mesothelioma.

Wollastonite is a mineral used in ceramics, paints, plastics and auto-body parts.

In Essex County, the plant closure also worried workers because of

repeated statements by company officials that sales of wollastonite at

Willsboro, mined by Imerys in nearby Lewis, have been weak.

The plant has been closed since its third shift on Tuesday. The

workers are being paid during the closure, Bettis said, and many will

return on Monday to clean the premises. They will wear masks, he said.

Tests revealed trace levels of asbestos, and only in some products,

the company said, and no contamination in the plant’s air. Toohey issued

a statement that said Imerys has no reason to believe the wollastonite

or the products sold are unsafe for handling and use.

“Out of an abundance of caution, we are temporarily suspending

production and are working to identify the earliest possible date to

resume production with ore that meets our standards,†the company said.

“We remain committed to producing high-quality wollastonite in

Willsboro.â€

The company, which has cut staff and farmed out some work in the past

few years, has 59 employees. It had employed more than 100 six years

ago.

It will be throwing out tons of ore and product from the past 12

months. When workers clean the plants in Willsboro they will be wearing

enhanced safety gear because of expected dusty conditions.

Mark Buckley, a former administrator at the plant who served as its

safety and health director, said an asbestos contamination issue arose

about 16 years ago when a customer discovered the problem. At that time,

the company closed for a few days of cleaning and investigation.

Workers needed to be fitted for masks for protection then. The root of

the asbestos was a rock formation adjoining the ore mine, he said.

The new issue surfaced amid inspections by the U.S. Mine Safety and

Health Administration, which sends inspectors into the plant at least

twice a year. Already, the plant has received 33 citations for

violations this year, according the MSHA web site. An MSHA spokesman was

unavailable.

The plant has a long history as a major employer for mining and

plant processing jobs in the Adirondack hamlets of Lewis and Willsboro,

though Imerys has discontinued its mining employment and contracts the

work to a Vermont excavator.

The plant also received the uncommon opportunity from New York voters

to swap state forest preserve land for the rights to mine wollastonite

in an area of Lewis known as Lot 8. Imerys has yet to take advantage of

that opportunity, granted after heavy lobbying from the former owners

who said they needed Lot 8 to preserve jobs. Voters approved a trade of

200 acres in the Jay Mountain Wilderness for lands of equal or greater

value.

John Brodt, a spokesman for the Imerys mining division, said Imerys

intends to continue testing the ore at Lot 8. Imerys wants to capitalize

on the mining opportunity extended by voters in 2013, he said.

An application, submitted late last year, is pending before the state

Department of Environmental Conservation to conduct horizontal drilling

from the company’s land adjacent to Lot 8, he said. The goal is to add

to previously collected test data before determining the value of Lot 8.

If the company and the state arrive at a land swap deal, the Lot 8 acquisition could happen in 2022, Brodt said.

Posted by AGORACOM

at 1:12 PM on Thursday, January 30th, 2020

https://youtu.be/swY2-K4DXSI

The Morning Drive: The Electric Vehicle Revolution Featuring Lomiko Metals

What is the Upside for Lomiko? We are glad you asked that question! That’s why we need sunglasses. Below is a news report regarding our nearest neighbor that has gone through the PEA and Feasibility process with the result being a Discounted Net Present Value of $ 750 million and a $50+ million market capitalization.

Please note current tonnage amount at Lomiko’s La Loutre Graphene Battery Zone is 3%-3.6% and there is 36 million tonnes in the defined area. The new Refractory Zone at La Loutre was drilled in 2019 and will add much more tonnage, but more importantly, it will increase the grade reported in the new 43-101! Please see the drill map

After a Preliminary Economic Assessment, the La Loutre Project should generate a much larger Discounted Net Present Value than our current market capitalization of $ 4 million.

From news agency Stockwatch: Pierre Renaud and Eric Desaulniers’s Nouveau Monde Graphite Inc. (NOU), unchanged at 20 cents on 219,000 shares, has signed a benefit-sharing agreement with the Municipality of Saint-Michel-des-Saints. Mr. Desaulniers, President and CEO, puts a colourful spin on the arrangement, which he says has strengthened the social, economic and environmental development partnership between the company and the town. Rejean Gouin, mayor of Saint-Michel, is proud of the deal, adding that he is “certain that it will benefit all citizens as well as future generations.”

Matawinie hosts nearly 96 million tonnes indicated at 4.28 per cent graphite and 14 million tonnes inferred at 4.19 per cent, all of it in the West zone of the company’s Tony claim block. A feasibility study, completed late in 2018, was based on a reserve of nearly 60 million tonnes at 4.35 per cent graphite, enough to last about a generation. The study contemplated a mine capable of producing 100,000 tonnes of graphite per year, enough to support a discounted net present value of $750-million after taxes. Still, before the town sees the annual cheques covering 3 per cent of after-tax cash flow, Mr. Desaulniers will have to find the $276-million to build the mine and get it running.

For more information on the Company, review the website at www.lomiko.com, contact A. Paul Gill at 604-729-5312 or email: [email protected].

Posted by AGORACOM

at 10:58 AM on Wednesday, January 29th, 2020

Sponsor: Loncor is a Canadian gold exploration company that controls over 2,400,000 high grade ounces outside of a Barrick JV.. The Ngayu JV property is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

The market is buzzing with

speculation about Barrick Gold Corp. CEO Mark Bristow’s next move, with

Freeport-McMoRan, owner of the giant Grasberg copper and gold mine in

Indonesia, regarded as a potential takeover target.

A tough-talking South African on a mission to shake up the mining

industry. For years the name that would have sprung to mind was Glencore

boss Ivan Glasenberg, but not any more. The sector has another

swashbuckling executive to watch: Mark Bristow, head of Barrick Gold.

Since the geologist took control of the world’s second-biggest gold

miner just over a year ago he has been a whirlwind of activity.

Highlights of the past 12 months include a hostile bid for its arch

rival — now a partner in a joint venture — a buyout of struggling

subsidiary Acacia Mining and more than US$1 billion of asset sales.

But this is just the beginning for 61-year-old Bristow, an adrenalin

junkie who enjoys big game hunting and flying planes. “It has been an

amazing year,†he said during a wide-ranging interview. “We now have a

solid foundation to build on and probably the strongest balance sheet in

the gold industry.â€

The market is buzzing with speculation about Bristow’s next move,

with Freeport-McMoRan, owner of the giant Grasberg copper and gold mine

in Indonesia, regarded as a potential takeover target.

Bristow recently described copper as a “strategic metal†because of

the role it would play in the shift to a greener economy. “The new, big

gold mines are going to come out of the young geologies of the world,â€

he said. “And in young rocks, gold comes in association with copper or

vice versa.â€

Asked if he had discussed the merits of a deal with Freeport chief

executive Richard Adkerson, Bristow said there had been “conversationsâ€

but these had been more theoretical.

“As the leader of the most valuable gold company in the world, I

should be looking at the world’s best gold mines,†he said. “It makes

sense for us to be interested in looking at Grasberg and asking

ourselves whether Freeport is going to remain an independent company or

not.â€

A workaholic who maintains a punishing travel schedule, Bristow

became chief of Barrick in early 2019 after the Toronto-listed company

consummated a nil-premium merger with Randgold Resources, the

Africa-focused miner he built into one of the world’s largest gold

producers.

The idea behind the deal was to create a gold company focused around

five “tier one assets,†mines capable producing more than 500,000oz of

gold annually for at least a decade. The merged entity would be run the

“Randgold Way†— the decentralised, hands-on management philosophy

espoused by Bristow.

When the Randgold merger was announced in September 2018 there were

worries about how Bristow would work alongside Barrick’s executive

chairman John Thornton, a no-nonsense ex-Goldman Sachs banker.

However, Bristow and his close-knit team of executives have been

given their head to run the company. One of his first moves on taking

the helm was to cut almost 100 jobs at Barrick’s head office in Toronto

in an effort to shape what he calls a “lean, mean machine at the top.â€

He has also changed the management teams across nearly all of the

Barrick assets.

Analysts and investors say Bristow has delivered on the big promises

he made at the time of the merger: balance sheet deleveraging, reducing

head office costs and asset sales.

“If the gold price stays around US$1,500 an ounce and we generate the

same sort of free cash flow as [2019 and] deliver on the rest of our

promises as far as realizing the sale of non-core assets we will have

zero net debt [by the end of 2020],†Bristow said.

Barrick and arch rival Newmont Corporation’s deal to combine their

mines in Nevada into a joint venture, after Barrick dropped its hostile

bid for the latter, has also won plaudits. This has been reflected

in Barrick’s share price, which has risen 76 per cent since the Randgold

merger was announced — outperforming Newmont (46 per cent) and the gold

price (31 per cent).

Barrick Gold Corp’s stock chart since the merger with Rangold was announced Sept. 24, 2018. Bloomberg

Still, some investors lament the passing of Randgold. One top-20

shareholder said it would have delivered a better share price

performance had it remained independent — a view backed up by recent

results, which show the Randgold side of the portfolio continuing to

sparkle while the Barrick portion struggles.

Randgold also boasted a generous dividend policy, something Barrick

has yet to match. Analysts estimate Barrick’s dividend would need to

rise two to three times from where it is today to be comparable to

Randgold’s payout. Bristow said Barrick would look at a long-term

dividend policy once its 10-year strategic plan is put in place early

this year. Barrick also remains a very complex business with assets

in the Americas, Africa and Asia, leaving Bristow and his management

team stretched.

“There is a core of 10 Randgold executives who run the business. They

used to fly around all the assets once a quarter,†said one analyst who

used to follow Randgold but does not cover Barrick. “That is more

difficult to do now given the size and scale of the business.â€

A photo of Rangold’s open-pit gold mine in the Democratic Republic of Congo in 2014. Rangold Resources

James Bell, an analyst at RBC Capital Markets, also said the

integration of the two companies had become more complicated because

some of the assets flagged as potentially noncore at the time of the

Barrick deal were now seen as less disposable.

“A good example is Porgera [a mine in Papua New Guinea]. This was an

asset initially flagged as noncore but that’s an asset the company is

now very excited about because management have seen the geological

potential,†he added.

Bristow said Barrick would continue to divest assets where it makes

“good, commercial senseâ€, citing the recent sale of its stake in the

Massawa gold project in Senegal for an upfront payment of US$380

million.

Bristow, who had open heart surgery in 2017 after a doctor spotted a

problem during a routine medical to renew his pilot’s licence, said he

did not know when he would step down.

“I don’t have a particular timeframe but I gave the market a [promise

of at least a] full five years. I am certainly committed to that,†he

said, adding that there was already a pool of executives that are

qualified to lead the organization. “And you can imagine how much better

they are going to be with a bit of coaching in the next couple of

years.â€

Posted by AGORACOM

at 2:07 PM on Tuesday, January 28th, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged of 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits. Click Here For More Info

Excerpts from Crescat Capital November Newsletter:

Precious Metals

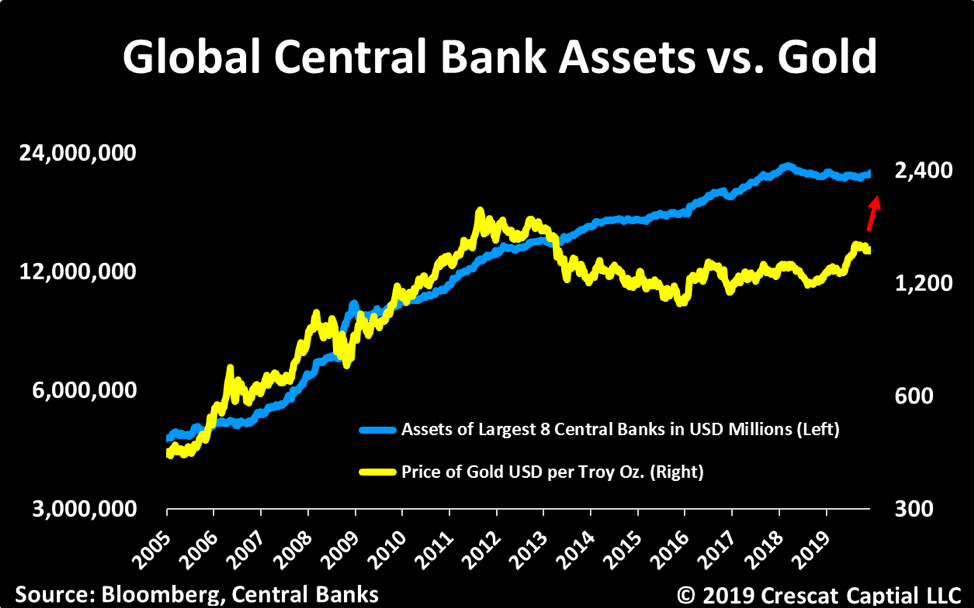

Precious metals are poised to benefit from what we consider to be the

best macro set up we’ve seen in our careers. The stars are all

aligning. We believe strongly that this time monetary policy will come

at a cost. Look in the chart below at how the new wave of global money

printing just initiated by the Fed in response to the Treasury market

funding crisis is highly likely to pull depressed gold prices up with

it.

The imbalance between historically depressed commodity prices

relative to record overvalued US stocks remains at the core of our macro

views. On the long side, we believe strongly commodities offer

tremendous upside potential on many fronts. Precious metals remain our

favorite. We view gold as the ultimate haven asset to likely outperform

in an environment of either a downturn in the business cycle, rising

global currency wars, implosion of fiat currencies backed by record

indebted government, or even a full-blown inflationary set up. These

scenarios are all possible. Our base case is that governments and

central banks will keep their pedals to the metal to attempt to fend off

credit implosion or to mop up after one has already occurred until

inflation becomes a persistent problem.

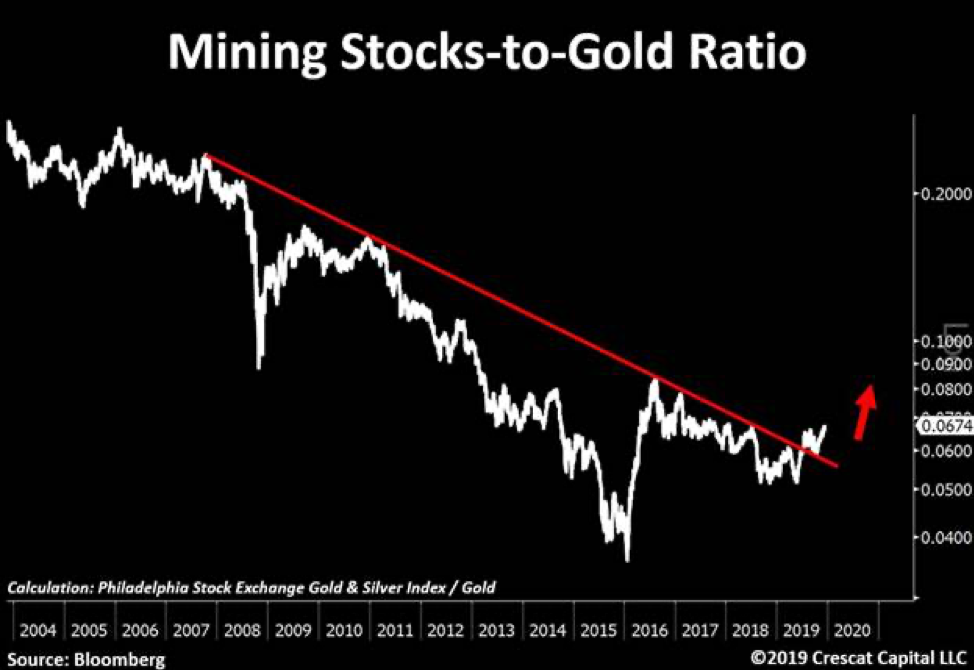

The gold and silver mining industry is precisely where we see one of

the greatest ways to express this investment thesis. These stocks have

been in a severe bear market from 2011 to 2015 and have been formed a

strong base over the last four years. They are offer and incredibly

attractive deep-value opportunity and appear to be just starting to

break out this year. We have done a deep dive in this sector and met

with over 40 different management teams this year. Combining that work

with our proprietary equity models, we are finding some of the greatest

free-cash-flow growth and value opportunities in the market today

unrivaled by any other industry. We have also found undervalued

high-quality exploration assets that will make excellent buyout

candidates.

We recently point out this 12-year breakout in mining stocks relative

to gold now looks as solid as a rock. In our view, this is just the

beginning of a major bull market for this entire industry. We encourage

investors to consider our new Crescat Precious Metals SMA strategy which

is performing extremely well this year.

Zero Discounting for Inflation Risk Today

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, if the global financial markets

cannot absorb the increase in Treasury debt, the Fed will be forced to

monetize it even more. The problem is that the Fed’s panic money

printing at this point in the economic cycle may hasten the unwinding of

the imbalances it is so desperate to maintain because it has perversely

fed the last-gasp melt up of speculation in already record over-valued

and extended equity and corporate credit markets. It is reminiscent of

when the Fed injected emergency cash into the repo market at the peak of

the tech bubble at the end of 1999 to fend off a potential Y2K computer

glitch that led to that market and business cycle top. After 40

years of declining inflation expectations in the US, there is a major

disconnect today between portfolio positioning, valuation, and economic

reality. Too much of the investment world is long the “risk parityâ€

trade to one degree or another, long stocks paired with leveraged long

bonds, a strategy that has back-tested great over the last 40 years, but

one that would be a disaster in a secular rising inflation environment.

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, rising long-term inflation, and

the hidden tax thereon, is the default, bi-partisan plan for the US

government’s future funding regardless of who is in the White House and

Congress after the 2020 elections. The market could start discounting

this sooner rather than later. The Fed’s excessive money printing

may only reinforce the unraveling of financial asset imbalances today as

it leads to rising inflation expectations and thereby a sell-off in

today’s highly over-valued long duration assets including Treasury bonds

and US equities, particularly insanely overvalued growth stocks. We

believe we are in the vicinity of a major US stock market and business

cycle peak.

Posted by AGORACOM

at 1:57 PM on Tuesday, January 28th, 2020

SPONSOR: Lomiko Metals is focused on the exploration and development of minerals for the new green economy such as lithium and graphite. Lomiko owns 80% of the high-grade La Loutre graphite Property , Lac Des Iles Graphite Property and the 100% owned Quatre Milles Graphite Property. Lomiko is uniquely poised to supply the growing EV battery market. Click Here For More Information

According

to research by BloombergNEF, European automakers and governments will

move toward helping curb global warming with stricter carbon emissions

regulations, which could force an electric-vehicle revolution.

In the United States, electric vehicles are primarily being purchased

by consumers that want to take action on their own. Fuel is cheap, the

country doesn’t have a real climate change plan, and large vehicles like

pickups are king. All of this means that there’s little incentive,

beyond the $7,500 federal tax credit, to purchase an EV. That, though,

isn’t the case in other countries like China and, soon to be Europe.

EV Revolution Coming This Year

According

to a report by Bloomberg and a forecast from BloombergNEF, Europe will

see an electric revolution in 2020. The outlet states that the country’s

government will soon look to cut carbon emissions from vehicles as part

of a plan to curb global warming. This, in turn, will force automakers

to introduce electric vehicles.

Bloomberg claims that sales of

electric cars are set to increase to 2.5 million units in 2020. That

figure represents an increase of 20 percent from 2019.

Just like this year, China will continue to lead the way forward for sales. But the country recently decided to reduce subsidies for EV owners,

which could help Europe gain a larger piece of the market. The outlet’s

forecasting claims that Volkswagen’s push to become an electric-vehicle

force will boost the number of electrified vehicles in Europe. In

total, the outlet expects 800,000 electric cars to be sold in Europe in

2020.

“The long-term future is really bright, but in the short

term we’re expecting growth to be relatively slow,” said Colin

McKerracher, an analyst at BloombergNEF. “You’re still in the middle of

this transition, from a market driven by direct subsidies toward one

driven by a combination of real consumer demand and other big policy

mechanisms.”

Better Prices, More Infrastructure Coming

Another

important aspect of electric vehicles that will help sales increase in

Europe are decreasing lithium-ion battery prices. The outlet states that

prices per kilowatt-hour will hit roughly $135 – approximately 13

percent lower than in 2019. With the increase of battery production,

better battery designs, and more sales, battery prices are expected to

tumble.

All of these things mean that more chargers will be

needed. Luckily, public chargers are expected to rise to 1.2 million, up

from 880,000 last year. The increase in chargers will come in part from

governments and energy companies looking to expand infrastructure to

support the increase in demand for electric cars.

Another

interesting trend to look at in 2020 include other forms of electrified

transportation. A few companies, even automakers, showcased flying electric cars at CES.

While it’s unlikely that one would come out in 2020, it’s likely

something that more companies will pursue this year. Other forms of

transportation, including boats could go electric in 2020, too.

Posted by AGORACOM

at 12:39 PM on Tuesday, January 28th, 2020

SPONSOR: Gratomic Inc. (TSX-V: GRAT) Advanced materials company focused on mine to market commercialization of graphite products, most notably high value graphene based components for a range of mass market products. Collaborating with Perpetuus, Gratomic will use Aukam graphite to manufacture graphene products for commercialization on an industrial scale. For More Info Click Here

In the weeks since the Physics World team kicked off the new year by testing a pair of graphene headphones, we’ve received a steady stream of comments about our review and a related segment on our weekly podcast. A few people have asked our opinion of other graphene headphones, and one man went so far as to question whether the “graphene†label he found on an inexpensive pair of headphones was anything more than “misleading click-baitâ€.

I can’t judge any product I haven’t tried, and I also can’t judge a product’s graphene content without taking it apart and getting experts to analyse it. However, with those two caveats firmly in place, here are two facts to consider should you happen to be in the market for graphene headphones (and, by extension, graphene anything).

First, a lot of things contribute to how a pair of headphones will sound. The physical composition of the headphone drivers (graphene, PET, cellulose, or whatever) is only one factor. Others include the method by which those drivers create sound (this blog post explains a few of the possibilities, and their trade-offs); the quality of the other electronics; and simple things like how well the headphones fit over/in your ears. Some of these things are more expensive to optimize than others. The graphene headphones I tested are a high-end product with, it appears, a high-end price, so I suspect they are pretty good at the non-graphene-related aspects of headphone design – and that much of their cost comes from that, not from the graphene.

Second, graphene exists in many forms, with many price points. A lot of physicists are interested in ultra-pure, single-layer graphene, which has amazing electronic properties. This “physicists’ graphene†is difficult (and expensive) to make in macroscopic quantities. However, others are more interested in graphene’s mechanical properties, such as strength and rigidity. To get these properties, you don’t need ultra-pure single-layer graphene. You can get by with a cheaper type, which for argument’s sake I will term “materials scientists’ graphene†(this is an oversimplification, but it conveys the right feel). The proprietary graphene-based material in the headphones I tested was most likely in this category.

But even this type of graphene is expensive relative to a third type

of graphene, which is cheap enough to be added in bulk to substances

like paint

or resin to improve their heat transport and/or electrical

conductivity. As I understand it, this “engineers’ graphene†functions

like a superior version of graphite, and manufacturers are selling it by

the kilo (and maybe, soon, by the tonne).

I’m not trying to start a three-way brawl between physicists,

materials scientists and engineers about which type of graphene is

better. They all have their uses,

and they all qualify as graphene. But here’s the problem: a product can

advertise itself, accurately, as containing graphene even if the

graphene it contains is not of a type or quantity that’s going to make a

difference to its performance. What’s more, if an unscrupulous

manufacturer wants to put graphite in its product and call it

“grapheneâ€, it’s hard for ordinary consumers to know the difference. To

the naked eye, graphene and graphite both look like gritty black

powders. You need more sophisticated testing equipment to distinguish

between them, and between the various grades of graphene.

Certification is a huge issue

for the graphene industry, and a lot of people are working on it.

However, until there’s a strong framework for regulation, the next best

thing is probably to look for independent endorsements by people and

organizations who know what they’re talking about. The headphones I

tried were endorsed by the co-discoverer of graphene, Kostya Novoselov,

as making good use of the material. Since then, I’ve learned of a different make of graphene headphones that has been endorsed by an industry body called the Graphene Council. However, until someone gives Physics World

its own product-testing lab and qualified technicians to run it, that’s

about all I can say – except to add that there are some graphene

products I definitely won’t be testing with my colleagues.

Posted by AGORACOM

at 8:30 AM on Tuesday, January 28th, 2020

Significant upside potential identified at 1,675,000 oz (20.78 Mt @ 2.5 g/t Au) Imbo Concession since 2014 resource estimate

TORONTO, Jan. 28, 2020 — Loncor Resources Inc. (“Loncor” or the “Company“) (TSX: “LN”; OTCQB: “LONCF”) is pleased to provide an update on its activities within the Ngayu Greenstone Belt, where the Company has a dominant foot-print through its joint venture with Barrick Gold (Congo) SARL (“Barrickâ€) and on its own majority-owned prospecting licences and exploitation concessions.

The Ngayu Archean Greenstone Belt of northeastern Democratic Republic of the Congo (the “DRCâ€)

is geologically similar to the belts which host the world class gold

mines of AngloGold Ashanti/Barrick’s Kibali mine in the DRC and

AngloGold Ashanti’s Geita mine in Tanzania. Gold mineralization at Ngayu

is spatially related to Banded Ironstone Formation (“BIFâ€),

which is the case at both Kibali and Geita and is highlighted in

Figures 1 and 2 below. The Ngayu belt is significantly larger in extent

than the Geita belt.

Adumbi Deposit Since the Company’s acquisition of

71.25% of the KGL-Somituri gold project from Kilo Goldmines Ltd. in

September 2019, Loncor has focussed on the Imbo exploitation concession

in the east of the Ngayu belt where an Inferred Mineral Resource of

1.675 million ounces of gold (20.78 million tonnes grading 2.5 g/t Au,

with 71.25% of this Inferred Mineral Resource being attributable to

Loncor via its 71.25% interest) was outlined in January 2014 by

independent consultants Roscoe Postle Associates Inc (“RPAâ€)

on three separate deposits, Adumbi, Kitenge and Manzako (see Figures 3

and 4 below). In this study, RPA made a number of recommendations on

Adumbi, which were subsequently undertaken during the period 2014-18.

The Company’s geological consultants Minecon Resources and Services

Limited (“Mineconâ€) has been assessing the implications of this additional exploration data on Adumbi, which are summarised below.

Additional Drilling RPA recommended additional

drilling at Adumbi to test the down dip/plunge extent of the

mineralization. In 2017, four deeper core holes were drilled below the

previously outlined RPA inferred resource over a strike length of 400

metres and to a maximum depth of 450 metres below surface. All four

holes intersected significant gold mineralization in terms of widths and

grade and are summarised below:

Borehole

From(m)

To(m)

Intercept Width(m)

True Width(m)

Grade (g/t) Au

SADD50

434.73

447.42

12.69

10.67

5.51

SADD51

393.43

402.72

9.29

6.54

4.09

SADD52

389.72

401.87

12.15

7.01

3.24

419.15

428.75

9.60

5.54

5.04

SADD53

346.36

355.63

9.27

5.70

3.71

391.72

415.17

23.45

14.43

6.08

The above drilling results which are shown on the longtitudinal

section (see Figure 5 below), indicate that the gold mineralization is

open along strike and at depth. The drilling of an additional 12 core

holes has the potential to significantly increase the Adumbi mineral

resource as highlighted on the longitudinal section.

Survey and Georeferencing The Adumbi drill hole

collars, trenches, and accessible adits/portals have now been accurately

surveyed and the data appropriately georeferenced. In addition, all

accessible underground excavations and workings have been accurately

surveyed. The new and improved quality of the exploration data will have

positive implications on potential future classification of the mineral

resources.

Re-logging of All Drill Holes The re-logging of

drill holes after the RPA study has defined the presence of five

distinct geological domains in the central part of the Adumbi deposit

where the BIF unit attains a thickness of up to 130 metres (see Figure 4

below). From northeast to southwest:

Upper BIF Sequence: an interbedded sequence of BIF and chlorite schist, 45 to 130 metres in thickness.

Carbonaceous Marker: a distinctive 3 to 17 metre thick unit of black carbonaceous schist with pale argillaceous bands.

Lower BIF Sequence: BIF interbedded with quartz carbonate, carbonaceous and/or chlorite schist in a zone 4 to 30 metres wide.

Footwall Schists: similar to the hanging wall schist sequence.

In the central part of Adumbi, three main zones of gold mineralization are present. These include mineralisation:

Within the Lower BIF Sequence.

In the lower part of the Upper BIF Sequence. Zones 1 and 2 are

separated by the Carbonaceous Marker, which is essentially

unmineralized.

A weaker zone in the upper part of the Upper BIF Sequence.

The lack of a detailed geological model in the previous resource

estimates resulted in wireframes being constructed using only assay

values with little regard to geological domains. This has resulted in

wireframes cross-cutting the geology which could have resulted in

underestimating the previous resource estimate.

Relative Density (“RDâ€) Measurements The increase

in the sample population coupled with the application of a more rigid

RD determination procedure based on recommendations from the RPA

resource study, indicates that the new RD measurements from both

mineralized and unmineralized material and from the various material

types and lithologic units have improved the confidence in the relative

RD determination to be applied to any future resource estimates.

Relative to the 6 oxide RD measurements used for tonnage estimation in

the RPA model, 297 oxide RD measurements within the mineralised domain

were undertaken during the review work. For the transition and fresh

material, equal number of determinations relative to the previous RD

sample volumes were undertaken with the review process employing more

rigid RD determination procedures.

Table 1 below indicates significate positive variance between the

previous model RD and the reviewed work for the oxide and transition

materials.

Table 1: Summary of Previous and Reviewed Mineralised Average RD Measurements

Material Type

RD used in Previous RPA Model

Additional RD Determinations

RD Variance (%)

Oxide

1.80

2.45

36.1

Transition

2.20

2.82

28.2

Fresh

3.00

3.05

1.7

Oxidation and Fresh Rock Surfaces The re-logging

of the core as per the RPA recommendations identified major differences

between the depths of Base of Complete Oxidation (BOCO) and Top of Fresh

Rock (TOFR), and the depths used by RPA in the 2014 model. In the RPA

model, the BOCO was negligible and the TOFR corresponded approximately

to the re-logged BOCO. The deeper levels of oxidation that were observed

during the re-logging exercise should have positive implications for

the Adumbi project with respect to ore type classification and

associated metallurgical recoveries and mining and processing cost

estimates.

Adit Sampling and Georeferencing Following the

accurate surveying of the 10 historical adits and appropriately

georeferencing, the 796 adit samples (1,121 metres in total) when

applied should have positive implications on the data spacing and

classification of any future mineral resources.

In summary, most of the previous recommendations from the 2014 RPA

mineral resource study on Adumbi have been undertaken. In addition, the

previously recommended LIDAR survey by RPA was completed this month over

Adumbi by Southern Mapping of South Africa.

The results of all the above tasks coupled with the higher current

gold price compared with the previous study in 2014 indicate significant

upside at Adumbi. Minecon is undertaking further studies to better

quantify this significant upside. At present and subject to the Company

securing the necessary financing, the Company is planning to drill the

additional 12 deeper holes at Adumbi and then commence a preliminary

economic assessment when an updated mineral resource study will be

undertaken.

Ongoing studies are also continuing by Minecon on further assessing

the data elsewhere on the Imbo exploitation concession including Kitenge

and Manzako.

As announced in November 2019, joint venture partner and operator

Barrick has identified a number of priority drill targets within the

1,894 square kilometre joint venture land package (the “JV Areasâ€)

at Ngayu and that are planned to be drilled during the current dry

season. Drill targets include Bakpau, Lybie-Salisa and Itali in the Imva

area as well as Anguluku in the southwest of the Ngayu belt and

Yambenda in the north. As per the joint venture agreement signed in

January 2016, Barrick manages and funds exploration on the JV Areas at

the Ngayu project until the completion of a pre-feasibility study on any

gold discovery meeting the investment criteria of Barrick. Subject to

the DRC’s free carried interest requirements, Barrick would earn 65% of

any discovery with Loncor holding the balance of 35%. Loncor will be

required, from that point forward, to fund its pro-rata share in respect

of the discovery in order to maintain its 35% interest or be diluted.

About Loncor Resources Inc. Loncor

is a Canadian gold exploration company focused on two projects in the

DRC – the Ngayu and North Kivu projects. Both projects have historic

gold production. Exploration at the Ngayu project is currently being

undertaken by Loncor’s joint venture partner Barrick Gold Corporation

through its DRC subsidiary Barrick Gold (Congo) SARL (“Barrickâ€).

The Ngayu project is 200 kilometres southwest of the Kibali gold mine,

which is operated by Barrick and in 2018 produced approximately 800,000

ounces of gold. As per the joint venture agreement signed in January

2016, Barrick manages and funds exploration at the Ngayu project until

the completion of a pre-feasibility study on any gold discovery meeting

the investment criteria of Barrick. Subject to the DRC’s free carried

interest requirements, Barrick would earn 65% of any discovery with

Loncor holding the balance of 35%. Loncor will be required, from that

point forward, to fund its pro-rata share in respect of the discovery in

order to maintain its 35% interest or be diluted.

Certain parcels of land within the Ngayu project surrounding and

including the Makapela and Yindi prospects have been retained by Loncor

and do not form part of the joint venture with Barrick. Barrick has

certain pre-emptive rights over these two areas. Loncor’s Makapela

prospect has an Indicated Mineral Resource of 614,200 ounces of gold

(2.20 million tonnes grading 8.66 g/t Au) and an Inferred Mineral

Resource of 549,600 ounces of gold (3.22 million tonnes grading 5.30 g/t

Au). Loncor also recently acquired a 71.25% interest in the

KGL-Somituri gold project in the Ngayu gold belt which has an Inferred

Mineral Resource of 1.675 million ounces of gold (20.78 million tonnes

grading 2.5 g/t Au), with 71.25% of this resource being attributable to

Loncor via its 71.25% interest.

Resolute Mining Limited (ASX/LSE: “RSG”) owns 27% of the outstanding

shares of Loncor and holds a pre-emptive right to maintain its pro rata

equity ownership interest in Loncor following the completion by Loncor

of any proposed equity offering. Newmont Goldcorp Corporation (NYSE:

“NEM”; TSX: “NGT”) owns 7.8% of Loncor’s outstanding shares

Additional information with respect to Loncor and its projects can be found on Loncor’s website at www.loncor.com.

Qualified Person Peter N. Cowley, who is President of

Loncor and a “qualified person” as such term is defined in National

Instrument 43-101, has reviewed and approved the technical information

in this press release.

Technical Reports Certain additional information with

respect to the Company’s Ngayu project is contained in the technical

report of Venmyn Rand (Pty) Ltd dated May 29, 2012 and entitled “Updated

National Instrument 43-101 Independent Technical Report on the Ngayu

Gold Project, Orientale Province, Democratic Republic of the Congo”. A

copy of the said report can be obtained from SEDAR at www.sedar.com and

EDGAR at www.sec.gov.

Certain additional information with respect to the Company’s recently

acquired KGL-Somituri project is contained in the technical report of

Roscoe Postle Associates Inc. dated February 28, 2014 and entitled

“Technical Report on the Somituri Project Imbo Licence, Democratic

Republic of the Congo”. A copy of the said report, which was prepared

for, and filed on SEDAR by, Kilo Goldmines Ltd., can be obtained from

SEDAR at www.sedar.com. To the best of the Company’s knowledge,

information and belief, there is no new material scientific or technical

information that would make the disclosure of the KGL-Somituri mineral

resource set out in this press release inaccurate or misleading.

Cautionary Note to U.S. Investors The

United States Securities and Exchange Commission (the “SEC”) permits

U.S. mining companies, in their filings with the SEC, to disclose only

those mineral deposits that a company can economically and legally

extract or produce. Certain terms are used by the Company, such as

“Indicated” and “Inferred” “Resources”, that the SEC guidelines strictly

prohibit U.S. registered companies from including in their filings with

the SEC. U.S. Investors are urged to consider closely the disclosure in

the Company’s Form 20-F annual report, File No. 001- 35124, which may

be secured from the Company, or from the SEC’s website at

http://www.sec.gov/edgar.shtml.

For further information, please visit our website at www.loncor.com,

or contact: Arnold Kondrat, CEO, Toronto, Ontario, Tel: + 1 (416) 366

7300.

Posted by AGORACOM

at 5:17 PM on Monday, January 27th, 2020

SPONSOR: Gratomic Inc. (TSX-V: GRAT) Advanced materials company focused on mine to market commercialization of graphite products, most notably high value graphene based components for a range of mass market products. Collaborating with Perpetuus, Gratomic will use Aukam graphite to manufacture graphene products for commercialization on an industrial scale. For More Info Click Here

Goodyear developed a proprietary compound enhanced with graphene

The rubber is able to deliver low rolling resistance, improved grip in the dry and wet and long-term durability.

Famous tire and rubber company Goodyear has launched two new bicycle tyres, Eagle F1 and Eagle F1 Supersport utilizing graphene technology and weighing just 180g for a 23mm model.

The

new Eagle F1 is an “ultra-high-performance all-round road tire†and the

Eagle F1 Supersport, which is even lighter, is aimed at the upper

echelons of competition and will be suited to road racing, time trial

and triathlon where speed trumps all other requirements.

Goodyear has developed a proprietary compound enhanced with graphene and “next-generation amorphous (non-crystalline) spherical Silica†to create what it labels Dynamic:GSR. The result of this is said to be a rubber that is able to deliver low rolling resistance, improved grip in the dry and wet and long-term durability.

he Eagle F1 comes in five width options from 23 to 32mm, while the Eagle F1 Supersport comes in three widths from 23 to 28mm.

To

produce the new tire Goodyear has invested in its own factory in Taiwan

and has developed a process that allows much greater control over the

construction of the tire. It didn’t share too many details, but it

believes this enhanced precision contributes to significant weight

savings.

Currently the new Eagle F1 and F1 Supersport are only

available as clincher tube-type tires, but a tubeless tire is reportedly

in the pipeline for a launch later this year.

The new tires will cost from £45 and be in shops in February.