Posted by AGORACOM-JC

at 12:40 PM on Friday, April 3rd, 2020

Global Leaders in Mobile ECG Connectivity

20 years of medical credibility licensing technologies to hospitals, physicians, remote patient monitoring platforms, research groups and commercial call centers

Sold into > 20 countries, with the largest customer base located in the US

Class II medical device clearances and device agnostic for collecting, viewing, recording, analyzing and storing of ECGs for management of patient and consumer health

ECG solutions for both consumer (OTC) and medical (Rx) markets

Owns all IP and source code

Market expert contributor for reports in mâ€health, mobile cardiac monitoring and new advances in consumer health and wellness monitoring

Recent Highlights

CardioComm Solutions Partners with CareOS to Bring Consumer ECG Monitoring into the Connected Home

Entered into a partnership agreement with CareOS SAS (France), a subsidiary of Baracoda Group, to provide consumer ECG monitoring technologies through the CareOS Poseidon smart mirror health and beauty hub

The partnership will see CardioComm’s FDA and Health Canada cleared GEMS™ ECG management software and Smart Monitoring ECG reading service integrated into the touch and gesture controlled smart mirror

GEMSTM software will be capable of recognizing ECG devices made by multiple device manufacturers which will permit CareOS customers more options in choosing a device of their preference.

Posted by AGORACOM

at 11:27 AM on Friday, April 3rd, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Recently acquired 14km of the potential extension of the new discovery by New Found Gold’s Queensway project to the south.Click Here for More Info

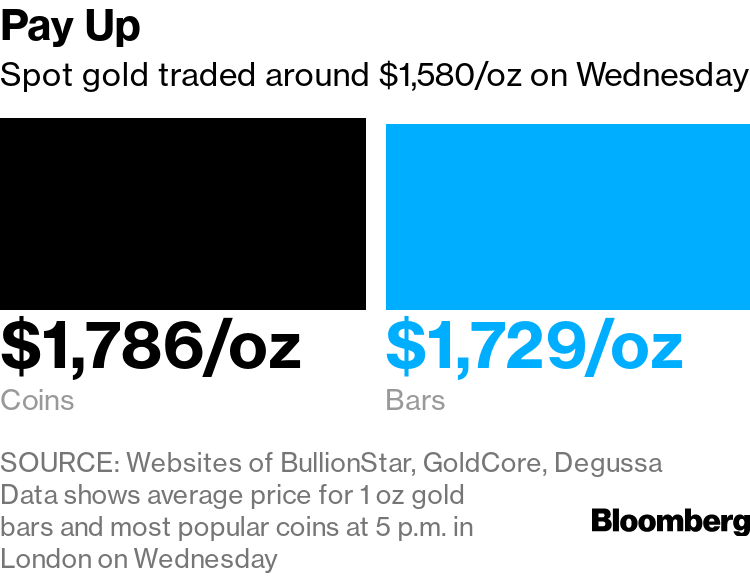

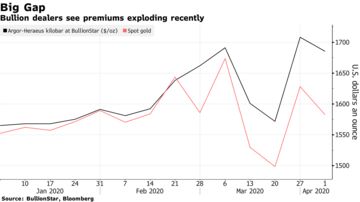

Small gold bars and coins are in high demand from consumers

The size of different products is a key reason for the crunch

Surging demand and disruptions from the coronavirus pandemic have created a shortage of the small gold bars most popular with consumers.

When people are worried about the future they turn to gold to protect their savings. That’s rarely been more true than today.

Surging demand and disruptions from the coronavirus pandemic have created a shortage of the small gold bars most popular with consumers. Those who do manage to get their hands on metal have to pay up –- well above the per-ounce prices being quoted on financial markets in London and New York.

Some dealers are desperately contacting clients to see if anyone is willing to sell their gold bars and coins, and offering a rare premium over spot prices. Others have given up trying to trade altogether.

“People want to buy, not to sell gold,†said Mark O’Byrne, the founder of GoldCore, a dealer based in Dublin. “We have a buyers’ waiting list and we emailed our clients seeing who wished to sell their gold. At this time there is roughly only one or two sellers for every 99 buyers.â€

Size is a key reason for the crunch. While there’s plenty of gold in a big trading hub like London, banks and other institutional investors there typically use large bars of 400 ounces. That’s not practical for a regular person who may not want to cough up more than $600,000 for a single bar. Instead, retail investors prefer kilobars (about 32 ounces), 1-ounce bars and coins, or something even smaller.

Those smaller items are getting hard to find for several reasons. First, of course, demand has exploded. But there’s also been pressure on supply, as global travel shuts down and some refineries and mints have stopped operating or capped production because of local lockdowns.

Premiums in the retail market “have exploded,†said Markus Krall, chief executive of German precious-metals retailer Degussa. The average price of products in shops is somewhere between 10% and 15% over spot prices, which he’s never seen before, Krall said. Demand, too, is at the highest level he’s experienced.

Certain products also command more of a premium than others. Kilobars manufactured by Argor-Heraeus SA, one of the big Swiss refiners whose plant has been closed since last week due to the health crisis, were selling for over 6% above spot, said Ronan Manly, an analyst at Singapore dealer BullionStar.

“We are seeing an unprecedented situation where huge customer demand and the disconnect between physical prices and spot prices is driving buy premiums high,†he said. Spot prices coming from London or New York “are completely detached from the reality on the ground.â€

Posted by AGORACOM

at 9:54 AM on Friday, April 3rd, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged 0.683 g/t Au over 780m in a vertical intercept. 2020 drilling plans 18,000 to 20,000 metres from 7-10 drill platforms with four diamond drill rigs. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits and is fully funded for exploration in 2020. Click Here For More Info

The nations of the world had 34,700 tons of gold reserves, as of January 2020.

Countries maintain gold reserves to stabilize currency against hyperinflation, particularly in the event of a major crisis like the one many economies worldwide currently face as a result of the coronavirus pandemic. Relatively few countries, however, have large gold reserves. In fact, over 80% of the world’s national gold reserves is held by the central banks and finance ministries of just 25 countries.

To determine the countries that control the world’s gold, 24/7 Wall St. reviewed data on gold reserves by country in tonnes – or metric tons – as of January 2020 from the World Gold Council. Data on gold as a share of a country’s total foreign exchange reserves also came from the WGC and is current as of January 2020.

The value of a country’s gold reserves in U.S. dollars was calculated using exchange rates current as of March 13, 2020. GDP and GDP per capita figures in 2018 are from the World Bank and are in constant 2011 international dollars. Data on population is also from the World Bank and is for 2018 or for the most recent period available.

Many, but not all of the countries on this list, are among the wealthiest nations on Earth, as these countries are able to buy up substantial gold reserves. These are the 25 richest countries in the world.

While some countries on this list have obtained gold reserves by purchasing from other countries, many of the nations with the biggest gold reserves, such as China, the United States, and Russia, are also the top gold-producing countries. China, the largest producer of gold in the world, alone accounted for 14% of global gold production in 2016.Â

25. Venezuela

• Gold reserves as of January 2020: 161.2 tonnes

• Gold reserves in USD as of January 2020: $8.1 billion

• Gold as % of total foreign exchange reserves: 81.0%

• GDP: $271 billion ($9,402 per capita)

• Population: 28.9 million

24. Algeria

• Gold reserves as of January 2020: 173.6 tonnes

• Gold reserves in USD as of January 2020: $8.7 billion

• Gold as % of total foreign exchange reserves: 11.6%

• GDP: $580 billion ($13,737 per capita)

• Population: 42.2 million

23. Philippines

• Gold reserves as of January 2020: 197.9 tonnes

• Gold reserves in USD as of January 2020: $9.9 billion

• Gold as % of total foreign exchange reserves: 11.2%

• GDP: $847 billion ($7,943 per capita)

• Population: 106.7 million

22. Belgium

• Gold reserves as of January 2020: 227.4 tonnes

• Gold reserves in USD as of January 2020: $11.4 billion

• Gold as % of total foreign exchange reserves: 39.5%

• GDP: $498 billion ($43,582 per capita)

• Population: 11.4 million

21. Poland

• Gold reserves as of January 2020: 228.6 tonnes

• Gold reserves in USD as of January 2020: $11.5 billion

• Gold as % of total foreign exchange reserves: 9.3%

• GDP: $1.1 trillion ($28,786 per capita)

• Population: 38 million

20. Austria

• Gold reserves as of January 2020: 280.0 tonnes

• Gold reserves in USD as of January 2020: $14.1 billion

• Gold as % of total foreign exchange reserves: 56.1%

• GDP: $409 billion ($46,260 per capita)

• Population: 8.8 million

19. Spain

• Gold reserves as of January 2020: 281.6 tonnes

• Gold reserves in USD as of January 2020: $14.1 billion

• Gold as % of total foreign exchange reserves: 19.1%

• GDP: $1.6 trillion ($34,831 per capita)

• Population: 46.7 million

18. Lebanon

• Gold reserves as of January 2020: 286.8 tonnes

• Gold reserves in USD as of January 2020: $14.4 billion

• Gold as % of total foreign exchange reserves: 27.3%

• GDP: $79 billion ($11,607 per capita)

• Population: 6.8 million

17. United Kingdom

• Gold reserves as of January 2020: 310.3 tonnes

• Gold reserves in USD as of January 2020: $15.6 billion

• Gold as % of total foreign exchange reserves: 9.3%

• GDP: $2.7 trillion ($40,522 per capita)

• Population: 66.5 million

16. Saudi Arabia

• Gold reserves as of January 2020: 323.1 tonnes

• Gold reserves in USD as of January 2020: $16.2 billion

• Gold as % of total foreign exchange reserves: 3.2%

• GDP: $1.7 trillion ($49,101 per capita)

• Population: 33.7 million

15. Uzbekistan

• Gold reserves as of January 2020: 333.7 tonnes

• Gold reserves in USD as of January 2020: $16.8 billion

• Gold as % of total foreign exchange reserves: 56.7%

• GDP: $250 billion ($7,592 per capita)

• Population: 33 million

14. Portugal

• Gold reserves as of January 2020: 382.5 tonnes

• Gold reserves in USD as of January 2020: $19.2 billion

• Gold as % of total foreign exchange reserves: 76.8%

• GDP: $298 billion ($28,999 per capita)

• Population: 10.3 million

13. Kazakhstan

• Gold reserves as of January 2020: 386.5 tonnes

• Gold reserves in USD as of January 2020: $19.4 billion

• Gold as % of total foreign exchange reserves: 67.1%

• GDP: $452 billion ($24,738 per capita)

• Population: 18.3 million

12. Taiwan, province of China

• Gold reserves as of January 2020: 422.4 tonnes

• Gold reserves in USD as of January 2020: $21.2 billion

• Gold as % of total foreign exchange reserves: 4.3%

• GDP: N/A

• Population: N/A

11. Turkey

• Gold reserves as of January 2020: 428.7 tonnes

• Gold reserves in USD as of January 2020: $21.5 billion

• Gold as % of total foreign exchange reserves: 21.8%

• GDP: $2.1 trillion ($25,358 per capita)

• Population: 82.3 million

10. Netherlands

• Gold reserves as of January 2020: 612.5 tonnes

• Gold reserves in USD as of January 2020: $30.8 billion

• Gold as % of total foreign exchange reserves: 70.2%

• GDP: $858 billion ($49,787 per capita)

• Population: 17.2 million

9. India

• Gold reserves as of January 2020: 635 tonnes

• Gold reserves in USD as of January 2020: $31.9 billion

• Gold as % of total foreign exchange reserves: 7%

• GDP: $9.3 trillion ($6,888 per capita)

• Population: 1.4 billion

8. Japan

• Gold reserves as of January 2020: 765.2 tonnes

• Gold reserves in USD as of January 2020: $38.4 billion

• Gold as % of total foreign exchange reserves: 2.9%

• GDP: $5 trillion ($39,294 per capita)

• Population: 126.5 million

7. Switzerland

• Gold reserves as of January 2020: 1,040.0 tonnes

• Gold reserves in USD as of January 2020: $52.3 billion

• Gold as % of total foreign exchange reserves: 6.2%

• GDP: $505 billion ($59,317 per capita)

• Population: 8.5 million

6. China

• Gold reserves as of January 2020: 1,948.3 tonnes

• Gold reserves in USD as of January 2020: $97.9 billion

• Gold as % of total foreign exchange reserves: 3.1%

• GDP: $22.5 trillion ($16,182 per capita)

• Population: 1.4 billion

5. Russia

• Gold reserves as of January 2020: 2,279.2 tonnes

• Gold reserves in USD as of January 2020: $114.5 billion

• Gold as % of total foreign exchange reserves: 20.6%

• GDP: $3.8 trillion ($24,791 per capita)

• Population: 144.5 million

4. France

• Gold reserves as of January 2020: 2,436.0 tonnes

• Gold reserves in USD as of January 2020: $122.4 billion

• Gold as % of total foreign exchange reserves: 63.6%

• GDP: $2.6 trillion ($39,556 per capita)

• Population: 67 million

3. Italy

• Gold reserves as of January 2020: 2,451.8 tonnes

• Gold reserves in USD as of January 2020: $123.2 billion

• Gold as % of total foreign exchange reserves: 69.3%

• GDP: $2.2 trillion ($35,828 per capita)

• Population: 60.4 million

2. Germany

• Gold reserves as of January 2020: 3,366.5 tonnes

• Gold reserves in USD as of January 2020: $169.1 billion

• Gold as % of total foreign exchange reserves: 74%

• GDP: $3.8 trillion ($45,936 per capita)

• Population: 82.9 million

1. United States

• Gold reserves as of January 2020: 8,133.5 tonnes

• Gold reserves in USD as of January 2020: $408.7 billion

• Gold as % of total foreign exchange reserves: 77.9%

Posted by AGORACOM

at 8:03 PM on Thursday, April 2nd, 2020

Sponsor: Affinity Metals Corp. (TSX-V: AFF) is a Canadian mineral exploration company building a strong portfolio of mineral projects in North America. The Corporation’s flagship property is the drill ready Regal Property near Revelstoke, BC where Affinity Metals is making preparations for a spring drill program to test two large Z-TEM anomalies. Click Here for More Info

BMO Capital Markets upgraded its forecast for gold prices Wednesday while downgrading the outlook for many other commodities.

BMO sees gold averaging $1,660 an ounce in the second quarter and rising to $1,700 in the fourth. The bank’s full-year forecast is now at $1,654, increasing to $1,698 next year.

The bank looks for silver to average $15.50 an ounce in the second quarter, then $18.50 in the next two quarters, with a full-year average of $17.18. The 2021 outlook was put at $18.05.

A previously expected global economic and industrial recovery in 2020 has been “stopped in its tracks†by the COVID-19 pandemic, BMO said. Businesses are shutting down around the world to slow the spread of the virus. As a result, the bank now expects a 0.8% contraction in global industrial production this year, the first slowdown since 2009. “And as a result, we have revised down our 2020 outlook across many of the commodities we cover, while pushing gold expectations higher,†BMO said.

Nevertheless, prices for all commodities – with the exception of iron ore – are likely to be higher next year, as supportive government stimulus efforts take hold, BMO said.

“We see gold as a natural beneficiary of even lower global interest rates and its safe-haven status should receive another airing in 2020,†BMO said. “Meanwhile, we see silver as not only hanging on gold’s coattails, but also potentially outperforming should governments move towards fiscal spending on 5G and solar technology.â€

Analysts pointed out that after the 2008 global financial crisis, gold and silver prices recovered months ahead of the global industrial economy.

Meanwhile, BMO said the platinum and palladium markets are likely to be volatile with both weaker auto sales and supply. However, since palladium stocks are already low, another price rally is likely when the auto industry restarts, BMO continued.

Platinum is seen averaging $950 an ounce in the second quarter and $1,000 in the fourth, with a full-year forecast of $971. Palladium is seen averaging $2,500 in the second quarter but falling to $2,250 in the fourth for a full-year average of $2,313.

BMO said its biggest downward revision to commodity prices in 2020 was in copper, but the outlook for other base metals was also lowered, including aluminum, zinc and nickel. These are all industrial metals. Copper is seen averaging $2.27 a pound in the second quarter and $2.33 for the full year.

Posted by AGORACOM-JC

at 1:57 PM on Thursday, April 2nd, 2020

SPONSOR: New Age Metals Inc. The company owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces Inferred. Learn More.

Bulls need to overcome 2,350: Palladium price analysis

Palladium has staged a major recovery after the popular metal received a strong boost from the Federal Reserve’s unlimited bond-buying program

Palladium price analysis highlights that a strong recovery from the 1,500 level has occurred

Palladium has staged a major recovery after the popular metal received a strong boost from the Federal Reserve’s unlimited bond-buying programme.

Palladium price analysis shows that the metal needs to overcome the 2,350 resistance level to keep the recent bullish momentum intact.

Palladium medium-term price trend

Palladium recently staged a strong recovery from just below the 1,500 level, after the FED’s QE programme boosted palladium prices.

Palladium price analysis shows that bearish MACD price divergence on the daily time frame has been completely reversed after the latest decline.

The daily time frame also shows that a bearish head-and-shoulders pattern played out to the downside, and reached its overall downside objective.

Drawing a Fibonacci retracement from the all-time price high to the March low, palladium is currently testing the 61.8 retracement of the mentioned sequence.

The 2,575 resistance level is the next major resistance area to watch if a breakout above the 2,350 level occurs, while failure to surpass the 2,350 level could result in a pullback towards the 50 per cent Fibonacci level, around the 2,180 level.

Saudi vs Russia oil price war

Palladium short-term price trend

Palladium price analysis over the short term shows that the price is consolidating around the metal’s 200-period moving average, around the 2,300 level.

The one-hour time frame is currently showing that a large amount of bearish MACD price divergence has formed during the latest rally.

Looking more closely at the bearish price divergence, the MACD price divergence extends down towards the 1,700 level.

Failure to gain traction above the 2,300 level could result in a drop towards the 1,700 level, which would reverse the bearish MACD divergence.

Palladium technical summary

Palladium price analysis highlights that a strong recovery from the 1,500 level has occurred. The lower time frames are warning that bearish MACD price divergence extends down towards the 1,700 level.

Posted by AGORACOM-JC

at 1:27 PM on Thursday, April 2nd, 2020

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has interests in Peru, including a 20 percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property. Click her for more information

Have the next crop of battery metals producers been oversold?

Could a large global recession as a result of the COVID-19 crisis alter the consensus long term outlook for battery raw materials like lithium, cobalt, graphite, nickel and copper?

No, says CRU Group senior analyst George Heppel. Irrespective of temporary recessions or market downturns, electrification of the global automotive sector remains “inevitable†in the long run.

Right now, COVID-19 is freezing the embryonic battery supply chain. But for the next crop of battery metals producers — impacted by the broader share market rout — ‘deals and discussions’ are very much continuing behind the scenes.

The short-term outlook for the lithium-ion supply chain, like everything else, is uncertain. Could a large global recession as a result of the COVID-19 crisis alter the consensus long term outlook for battery raw materials like lithium, cobalt, graphite, nickel and copper?

No, says CRU Group senior analyst George Heppel. Irrespective of temporary recessions or market downturns, electrification of the global automotive sector remains “inevitable†in the long run.

“Investment in e-mobility reduces CO2 emissions, improves air quality and will eventually make a huge amount of financial sense to the average consumer as battery costs decline and manufacturing scale ramps up,†he says.

The future remains bright for high quality battery facing stocks, especially those placed to take advantage of the next upsurge in demand in 2022/2023.

In the short-term, Heppel says the automotive sector – and EVs by extension – are experiencing a reduction in demand due to quarantine.

“Many consumers in key markets can’t leave their house for non-essential reasons right now, let alone buy cars,†he says.

“We have heard reports that 85 per cent of automotive manufacturing capacity in Germany is currently idle as a result of the pandemic.

“However, in theory this should create ‘pent up demand’ which is released when quarantines are relaxed.â€

Ongoing economic uncertainty will also hinder attempts to push new battery metals projects into production in the short-term, Benchmark Mineral Intelligence analyst Andrew Miller says.

“As a result, the potential for a supply crunch over the coming years will increase – money needs to go into new expansions today to fuel the growth in EV production in 2022/23 onwards,†he says.

Battery focused nickel sulphide play Blackstone Minerals (ASX:BSX) agrees that supply will tighten due to the reduced funding into new projects going forward “which will reduce the supply of nickel (particularly from laterites) and only increase the gap between supply and demandâ€.

“Tread carefully, but I believe now is the time to be buying those mining stocks you’ve been watching for months,†Blackstone managing director Scott Williamson told Stockhead.

“I can’t see the junior battery metals miners getting any cheaper than they are today.â€

“What was meant to be the year battery demand diversified outside China may now see China play a more important role than ever before,†he says.

“There are also expectations that EVs will be included in the country’s stimulus efforts which could bolster the long-term outlook.â€

China moving to insulate domestic #EV market as the country’s supply chain ramps back up following Q1 slowdown. More of these types of policies likely to follow over coming months: https://t.co/XUea3iteT5

Advanced explorer AVZ Minerals (ASX:AVZ) is driving the mammoth Manono project in the DRC toward a development decision.

As part of that process, it is aiming to lock in a lithium offtake and strategic investment deal with Chinese firm Yibin Tianyi.

Yibin Tianyi is set to become a key cog in the supply chain of Contemporary Amperex Technology (CATL), the world’s biggest lithium-ion battery maker.

AVZ managing director Nigel Ferguson told Stockhead the company had seen “increased and faster responses†out of the companies they were talking to in China over the last few weeks.

“They appear to be re-awakening after the significant lock downs there,†he says.

“OEM/car manufacturers are committed to their EV plans, and while the current events are certainly causing disruptions, I have not heard of any OEM changing its long-term EV growth plans.

“For AVZ, with our significant long-life, high-quality resource underpinned by the EV thematic, the future is very bright. Current share price values certainly do not represent that.â€

Posted by AGORACOM-JC

at 11:49 AM on Wednesday, April 1st, 2020

SPONSOR: CardioComm Solutions (EKG: TSX-V) – The heartbeat of cardiovascular medicine and telemedicine. Patented systems enable medical professionals, patients, and other healthcare professionals, clinics, hospitals and call centres to access and manage patient information in a secure and reliable environment.

mHealth Project to Crowdsource Consumer Data for Coronavirus Research

UCSF researchers are deploying an mHealth app to gather information on daily health habits

They’re hoping to gain insight on how behaviors might affect the course of the virus or outcomes in those who are infected

March 31, 2020 – mHealth researchers are using smartphones to crowdsource Coronavirus research.

The University of California at San Francisco has launched COVID-19 Citizen Science (CCS), a project aimed at gathering insights from people around the world on the virus. Participants are being asked to download an mHealth app, complete a survey about their daily health habits, complete a weekly follow-up survey and pass it on to friends.

“We are asking each participant to share the link to recruit at least five others,†Gregory Marcus, MD, MAS, a professor at UCSF’s Department of Medicine and the project’s co-leader, said in a press release. “We want to demonstrate that the number of people signing up for this scientific study and contributing their data can increase exponentially, faster than the disease itself.â€

Participants will also be able to provide continuous GPS data and information from mHealth wearables, such as Fitbit activity bands and smartwatches.

(For more coronavirus updates, visit our resource page, updated twice daily by Xtelligent Healthcare Media.)

Marcos is no stranger to telehealth projects. In 2013 he helped to launch the Health eHeart Study, which used online and mHealth tools to collect and analyze heart health data. That, in turn, led to the launch of a study in 2018 that combined mHealth wearables with AI to determine whether a cardiac monitoring platform could help detect early signs of diabetes.

Marcos says CCS aims to identify behaviors, influences and factors that might affect the course of the virus and outcomes after infection, and he feels the study could be the largest-ever prospective epidemiological study of infectious diseases.

“Social distancing keeps many protected,†he said, “but joining together to contribute data will help us beat this thing.â€

Posted by AGORACOM-JC

at 11:21 AM on Wednesday, April 1st, 2020

SPONSOR: BetterU Education Corp. aims to provide access to quality education from around the world. The company plans to bridge the prevailing gap in the education and job industry and enhance the lives of its prospective learners by developing an integrated ecosystem. betterU / Ottolearn launch FREE COVID-19 mobile resource toolkit to fight the global crisis – Click here for more information.

The Past, Present And Future Of Edtech Startups

Between January 2014 and September 2019, more than 4,450 edtech startups have been launched in India

An analysis of China’s current state of startup ecosystem will have very few but clear winners, one of which is the edtech sector. In India too, with the nationwide lockdown, there is a sudden surge in demand for edtech startups even as others are struggling to find a way out. Ecommerce and edtech are two sectors that may survive this rock phase, say experts.

However, as of now, it will not be wrong to say that edtech is yet to gain mass traction. Despite the launch of 4,450 edtech startups in the country, India has only one unicorn in the sector, BYJU’s, with a $5.7 Bn valuation. In fact, as we have mentioned in our earlier reports, BYJU’s also had to spend a good ten years to reach the valuation. The startup worked in stealth mode from 2011 to 2015 and the app was launched only in 2015.

For new entrepreneurs in the space, staying afloat has been all the more difficult. There is still a lack of warm reception for tech in India and many other countries. What a classroom can offer in terms of interpersonal skills, is something tech may not be able to replace, say educational experts.

“In our view, the failure rate for edtech startups is comparable with any other sector. Given that education is a high-involvement category and a career-affecting service, tech adoption is usually lower compared to other services and products. Hence, edtech startups can take more time to scale up than in some of the other categories,†Pranjal Kumar, CFO and head of education fund at Bertelsmann, told us earlier.

Funding And M&As In Edtech

According to DataLabs by Inc42, between January 2014 and September 2019, more than 4,450 edtech startups have been launched in India. However, 25% of startups have shut shop while only 4.17% of startups have raised funds. BYJU’s grabbed 65% of the total funding in edtech startups. The startups are, till date, finding it difficult to create a steady revenue stream.

To a great extent venture capitalists (VC) are playing an important role in helping the startup ecosystem, including edtech, largely considered futuristic. “VC investments have often been likened to rocket fuel or running on a treadmill. When we come in and invest we want to see you grow 5x over the next 15-18 months and keep that momentum going after each round of financing,†said Sajith Pai, Director, Blume Ventures.

The VCs who have been supporting BYJU’S, Vedantu, Toppr and others in the Indian edtech industry to scale-up businesses would be as below:

Blume Ventures: Blume has made six investments in edtech at pre-series A and seed stage. The investments have been in an array of segments within edtech including online test-prep, gamified learning, B2B white label apps for coaching classes and others.

Sequoia Capital: Known to be very active in the fintech segment, with 13 deals in 2019, Sequoia grabbed 10 deals in the edtech sector in 2019.

Omidyar Network: The VC firm makes equity investments in early-stage enterprises and provides grants to nonprofits in education and others.

Nexus Venture Partners: The venture fund has backed startups such as Unacademy, Quizizz, WhiteHat Jr among others

SAIF Partners: Toppr and Unacademy are some of the key investments by the VC in the Indian edtech market so far

Accel Partners: They have invested in startups including Edupristine and Vedantu

InnoVen Capital: The two prominent companies funded by InnoVen India include BYJU’S and Eruditus

Other than the above, Helion Venture Partners, Indian Angel Network (IAN) and India Educational Investment Fund are some of the prominent funds in the sector.

The edtech ecosystem also saw Initial Public Offering (IPO), and mergers and acquisitions, the two of the most common exit strategies in any startup ecosystem. As per DataLabs’ The Future Of India’s $2 Bn Edtech Opportunity Report 2020 between 2014 and 2019, a total of 35 edtech startups underwent merger or acquisition. The report also states that the Indian edtech startup ecosystem has seen the participation of 28 active acquirers, 54% of which hail from the education technology sector itself.

Posted by AGORACOM

at 10:05 AM on Wednesday, April 1st, 2020

SPONSOR: Lomiko Metals is focused on the exploration and development of minerals for the new green economy such as lithium and graphite. Lomiko owns 80% of the high-grade La Loutre graphite Property, Lac Des Iles Graphite Property and the 100% owned Quatre Milles Graphite Property. Lomiko is uniquely poised to supply the growing EV battery market. Click Here For More Information

Beyond lithium-ion technology, graphene can enhance the performance of next generation lithium-sulphur batteries. The battery promises lower costs due to the use of widely available sulphur as the cathode. Combined with a lithium metal anode and improvements to specific energy (Wh/kg) have also been achieved. Unfortunately, there are similarities between silicon and sulphur in that sulphur is also prone to stability issues – polysulphides tend to dissolve and diffuse to the anode where they react and cause a loss of active material. Furthermore, sulphur is not conductive and also expands during lithiation, though not to the extremes of silicon, and so requires both conductive additives and space within the electrode for the sulphur to expand into. Norwegian start-up Graphene Batteries employ a graphene network which provides a conductive network, space for volume expansion and may also help to trap polysulphides from diffusing to the anode. Nevertheless, the lithium-sulphur chemistry is still at the very early stages of commercialisation with various performance parameters needing to be improved upon and demonstrated.

The highly specific surface area and conductivity of graphene meant its first application in energy storage, that gained traction, was not in batteries but supercapacitors (capacitance is directly proportional to surface area). The theoretical specific capacitance of a single graphene layer is 550 F/g, 3-4 times the capacitance achieved from activated carbon in organic electrolyte (the incumbent electrode material). Companies are exploring μF chips through to kF modules for IoT devices through to wind turbines and off-road vehicles. All are looking at different ways to cost-effectively incorporate graphene without re-stacking or by appropriately modifying the surface. Unfortunately, the use of graphene has so far resulted in minimal improvements to specific capacitance or energy density. Graphene has been able to further improve power density but given power and fast charge/discharge capability are already strengths of supercapacitors, it is unlikely to unlock significant new markets.

Graphene can help enable lithium-sulphur technology and improve supercapacitor performance but IDTechEx believe they are most likely to occupy niche positions in the energy storage market, see “Advanced Li-ion & Beyond Li-ion Batteries 2018-2028â€. Li-ion technology is set to dominate over the coming decade and here, graphene can play an important role. Analysts at UK-based market research company, IDTechEx, cover various aspects of the energy storage and graphene markets, assessing the trends, bottlenecks and market potential of new materials and technologies. The newly updated report “Li-ion Batteries 2020-2030†provides a comprehensive view of the Li-ion market and the opportunities for new materials, while the report “Graphene, 2D Materials and Carbon Nanotubes 2019-2029†provides detailed analysis of the titled materials, their commercial progress and their prospects moving forward. For the full portfolio of energy research available from IDTechEx please visit www.IDTechEx.com/research/ES.

Posted by AGORACOM

at 4:21 PM on Tuesday, March 31st, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Recently acquired 14km of the potential extension of the new discovery by New Found Gold’s Queensway project to the south.Click Here for More Info

Dear Investors:

Are you looking for securities to buy to take advantage of the

carnage in the financial markets from the coronavirus? Baron Rothschild,

the 18th-century British banker advised that “The time to buy is when

there’s blood in the streets, even if it is your own.†He made a fortune

buying government bonds in the panic that followed the Battle of

Waterloo against Napoleon. But it’s not sovereign debt of the world’s

superpowers that is on sale today; it’s not the S&P 500 or Dow

either.

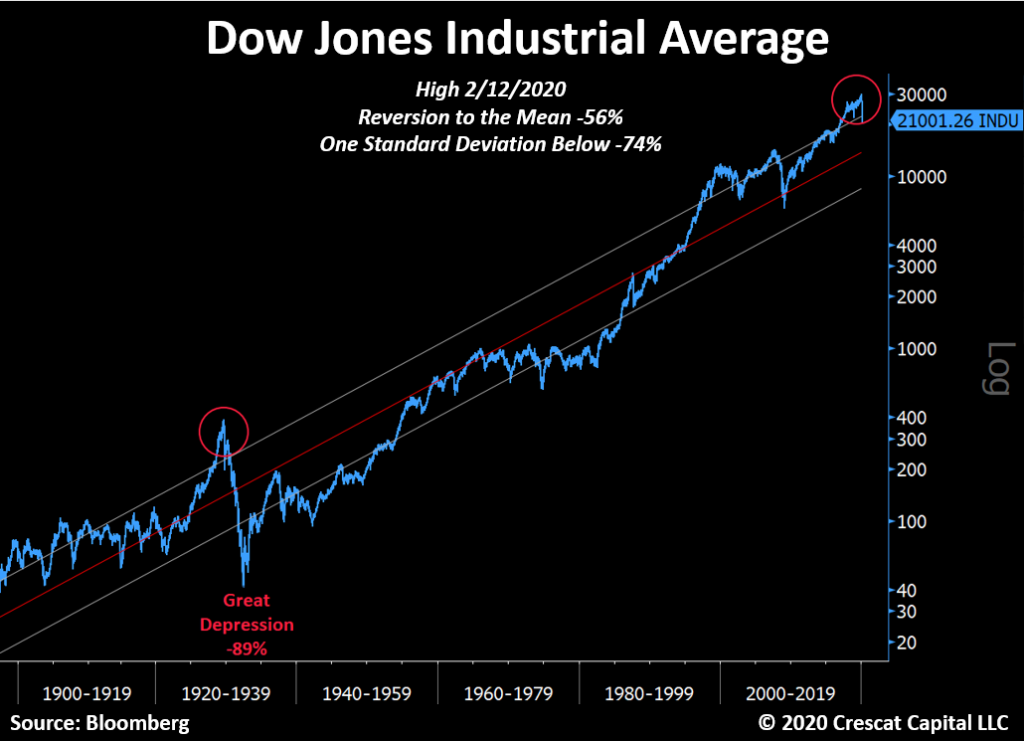

US government bonds already had their biggest year-over-year rally

ever, and at record low yields, they are no bargain. As for US stocks,

it’s only the first month after what we believe was a historic market

top. The problem is that the pandemic just so happened to strike at the

time of the most over-valued US stock market ever based on a composite

of eight valuation indicators tracked by Crescat, even higher than 1929

and 2000. It also hit after a record long bull market and economic

expansion. The stock market was already ripe for a major downturn based

on an onslaught of deteriorating macro and fundamental data even before

the global health emergency.

As we show in the chart above, we believe there is much more downside

still ahead for US stocks as a major global recession from nosebleed

debt-to-GDP levels has only just begun. Corporate earnings are now

poised to plunge and unemployment to surge. These things are perfectly

normal. There is a business cycle after all. It must play out as always

to purge the economy and markets of their sins and prepare the way for

the next growth phase. From the February top for large cap stocks, it

would take a 56% selloff just to get to long term mean valuations, a 74%

decline to get to one standard deviation below that. In the worst bear

markets, valuations get to two standard deviations below the mean. Such

realities happened at the depth of the Great Depression, the 1973-4 bear

market, and the 1982 double-dip recession. 1932 was an 89% drop from

the peak. The initial decline in this market so far is comparable to

1929 in speed and magnitude. There will certainly be bounces, but even

after an almost 30% fall in the S&P 500 through yesterday’s close,

we are not even close to the “blood in the street†valuations that

should mark the bottom for stocks in the current global recession that

has only just begun.

But value investors do not have to despair today. There is one area

of the stock market that already offers historic low valuations and an

incredible buying opportunity right now. Small cap gold and silver

mining companies just retested the lows of a 9-year bear market. Last

Friday, they were down 84% from their last bull market peak in December

2010! This was a double-bottom retest at a likely higher low compared to

the January 2016 low when they were down 87%. Now that is what we call

mass murder! In the chart below, we show that precious metals juniors

reached record low valuations last Friday relative to gold which is

still up 18% year-over-year. Mad value. Look at that beautiful

divergence and base. The baby was thrown out with the bathwater in a

mass margin call. Last time the ratio was in this vicinity, junior gold

and silver miners rallied 200% in 8 months. Crescat owns a portfolio of

premier, hand-picked juniors as part of our precious metals SMA and in

both hedge funds where clients can gain exposure today. We significantly

increased our exposure in our hedge funds amidst the massacre last

week.

The entire precious metals group was a casualty of a liquidity

crisis, the forced margin call selling for stocks and corporate credit

at large in the precipitous market decline. But it was also a victim of a

meltdown in dubious levered gold and silver ETF products. These

products such as JNUG and NUGT already had a horrific tracking error.

Nobody should have ever been investing in them in the first place. Gold

stocks are volatile enough on an unlevered basis.

The chief culprit in the ETF space last week was the $3 billion

leveraged assets, Direxion Daily Jr. Gold Bull 3x ETF. It absolutely

imploded, dropping 95% through last Friday from its recent high on

February 21. The fiasco in JNUG was insult to injury for long-time

precious metals investors, especially those invested in silver and in

junior miners. It was also an incredible buying opportunity that Crescat

took advantage of, especially in its hedge funds, where the profits

from our short positions at large allowed us to step up. Last week’s

action may have marked a major bottom for precious metals mining stocks

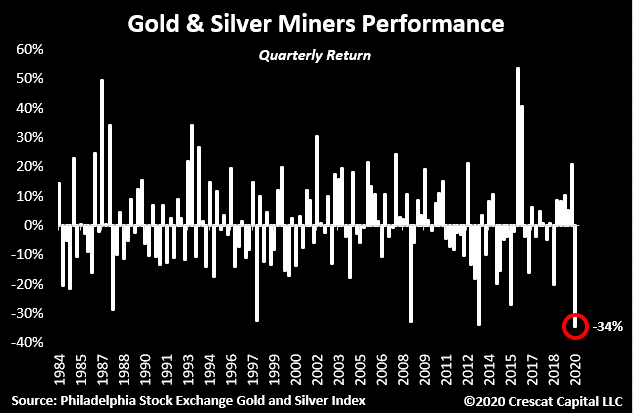

and ideally a bottom for battered silver this week. As of Friday, miners

were on track for their worst quarter ever as we show below.

The gold and silver stock selloff has exposed enormous free cash flow

yields today among precious metals mining producers of 10, 20, 30, 40,

even 50%. This is completely opposite the stock market at large.

Meanwhile, the pure-play junior mining explorers have some of the

world’s most attractive gold and silver deposits that can be bought at

historic low valuations to proven reserves and resources in the ground.

These companies are the beneficiaries of under-investment in exploration

and development by the senior producers over the entire precious metals

bear market. That rebound may have started yesterday in the mining

stocks especially the juniors. It is a historic setup right now for the

entire precious metals complex. Central banks are coming in, guns

blazing.

Meanwhile, the fundamentals have never been better for gold and

silver prices to rise making the discounted present value of these

companies even better. Global central bank money printing is poised to

explode which is important because the world fiat monetary base is the

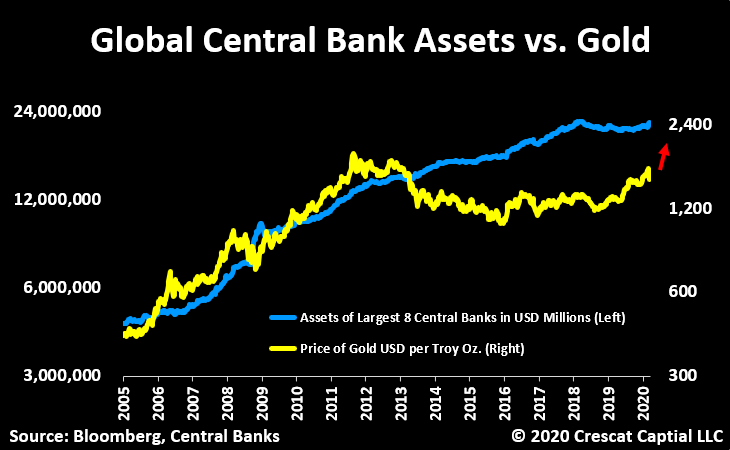

biggest single macro driver of gold prices. Gold itself is already

undervalued relative to global central bank assets which targets gold at

$2400 an ounce today.

At the same time, the price of gold is the biggest macro driver of

the price of silver, which is gold on steroids. Silver today is the

absolute cheapest it has ever been relative to gold and represents an

incredible bargain. We think silver is poised to skyrocket along with

mining stocks in what should be one of the biggest V-shaped recoveries

in the entire financial markets in the near term.

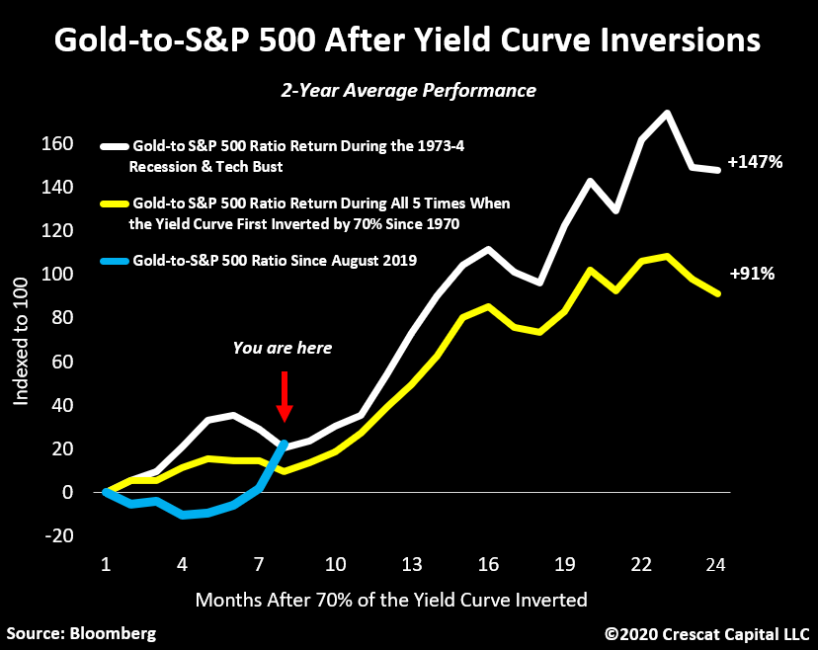

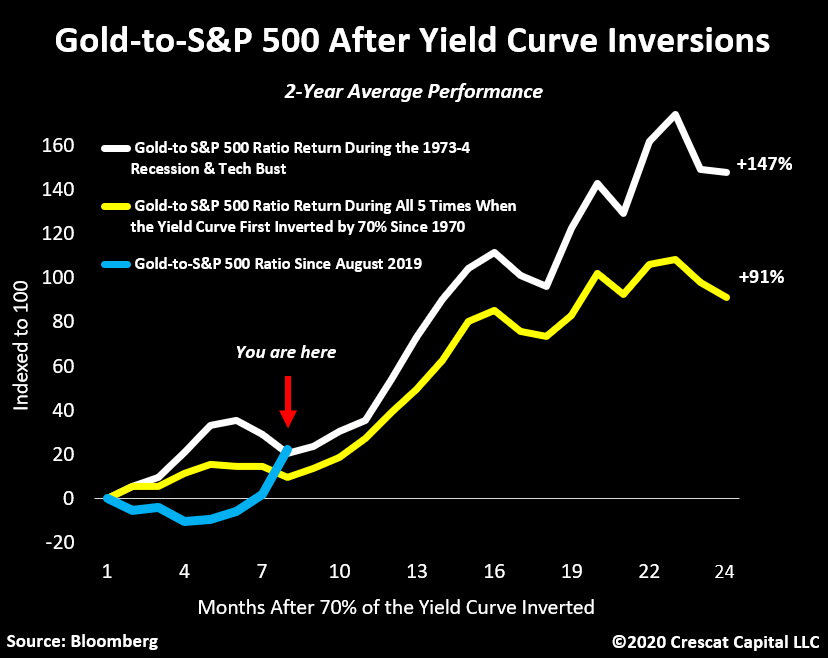

As we have shown in our prior letters, when the yield curve first

inverts by 70% or more, there is a high probability of a recession and

bear market. At that point, historically it has paid to buy gold and

sell stocks for the next 2 years. We went above 70% inversions in August

2019. At Crescat, we continue to express both sides of this trade in

our hedge funds and our firm at large. The gold-to-S&P 500 ratio is

up 28% since last August. The first part of the move was mostly driven

by the rise in gold. Since February 19, its been driven by the decline

in stocks. Now we’re at the place where historically both legs start to

work in tandem, and yesterday that was evident with one of our best days

ever in both Crescat hedge funds.

The Fed has not exhausted all its bullets. It has many forms of

monetary stimulus. It can print more money and take interest rates into

negative territory if need be. As the downturn in the business cycle

becomes more pronounced, these policies will become increasingly called

upon. That’s precisely what we are seeing today. Rate cuts everywhere,

QE announcements, even forms of helicopter money are being implemented.

It won’t save the economic cycle from its normal course, instead, it

should only invigorate the reasons for owning precious metals. Central

bank money printing and inflationary fiscal policy will almost certainly

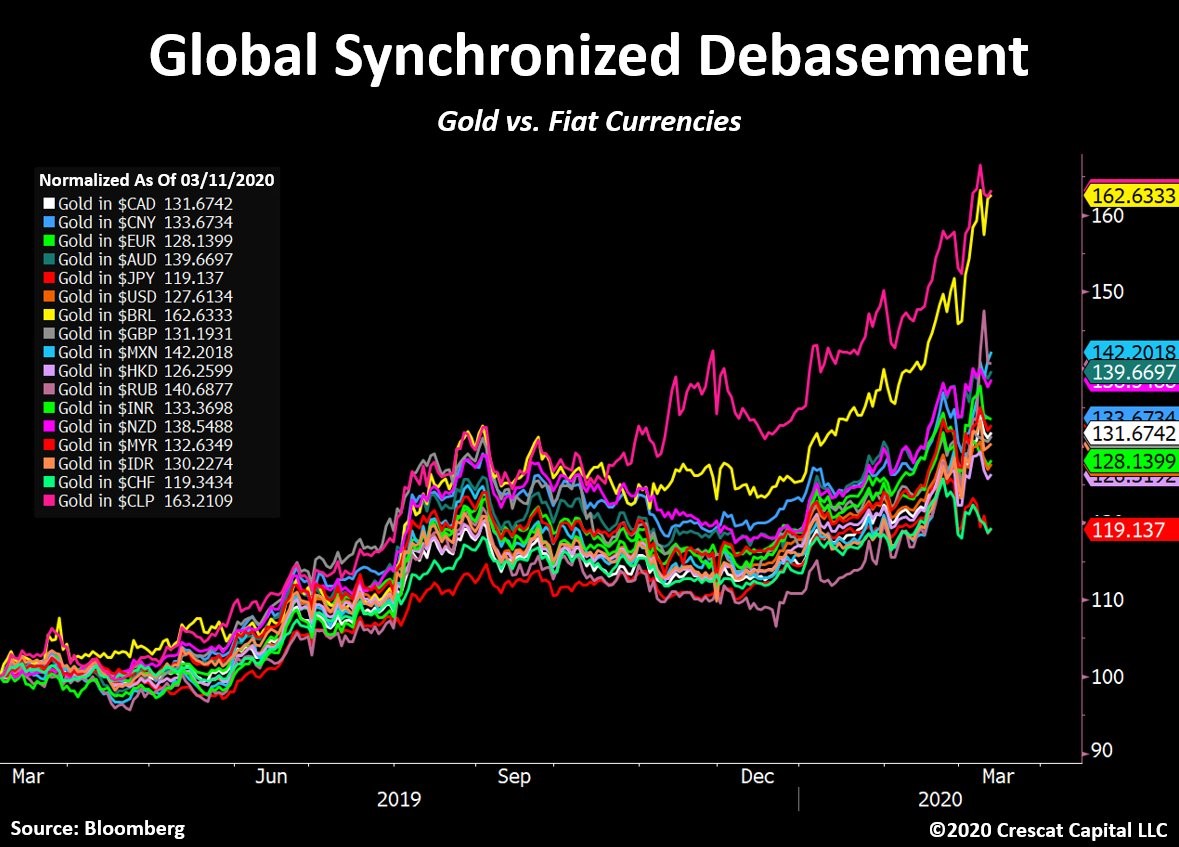

intensify. This is incredibly bullish for precious metals. We are in a

global synchronized debasement environment. Gold has already been

appreciating in all major fiat currencies in the world over the last

year.

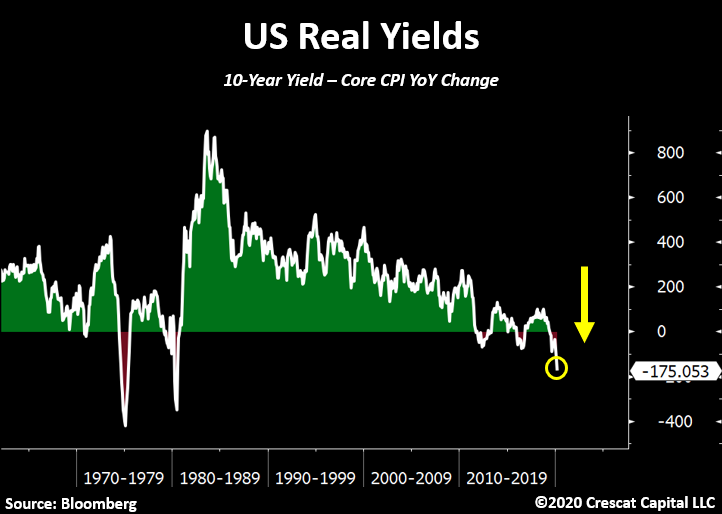

While yields continue to make historic lows worldwide, in real terms

they have reached even more extreme levels. For instance, the US 10-year

yield is now almost 2 percentage points below inflation. This just

further strengthens our precious metals’ long thesis.

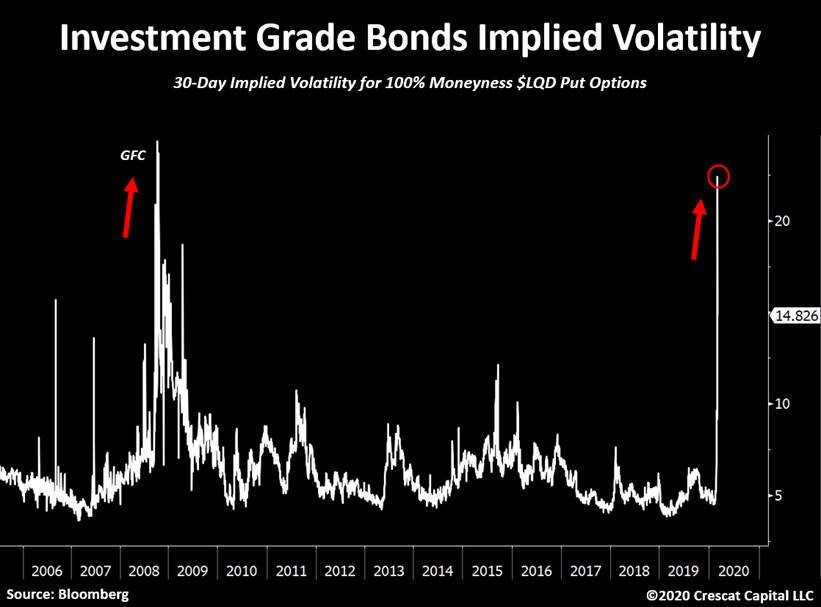

Even investment grade (IG) bonds are now blowing up. Implied

volatility for IG bonds is surging! It’s now at its highest level since

the Great Recession. Last week, the LQD (ETF) plunged 8% in 3 days,

which is equivalent to a 10 standard deviation move. Declines as such

only happened one other time in history, September 2008. We believe the

corporate debt market crisis has just begun.

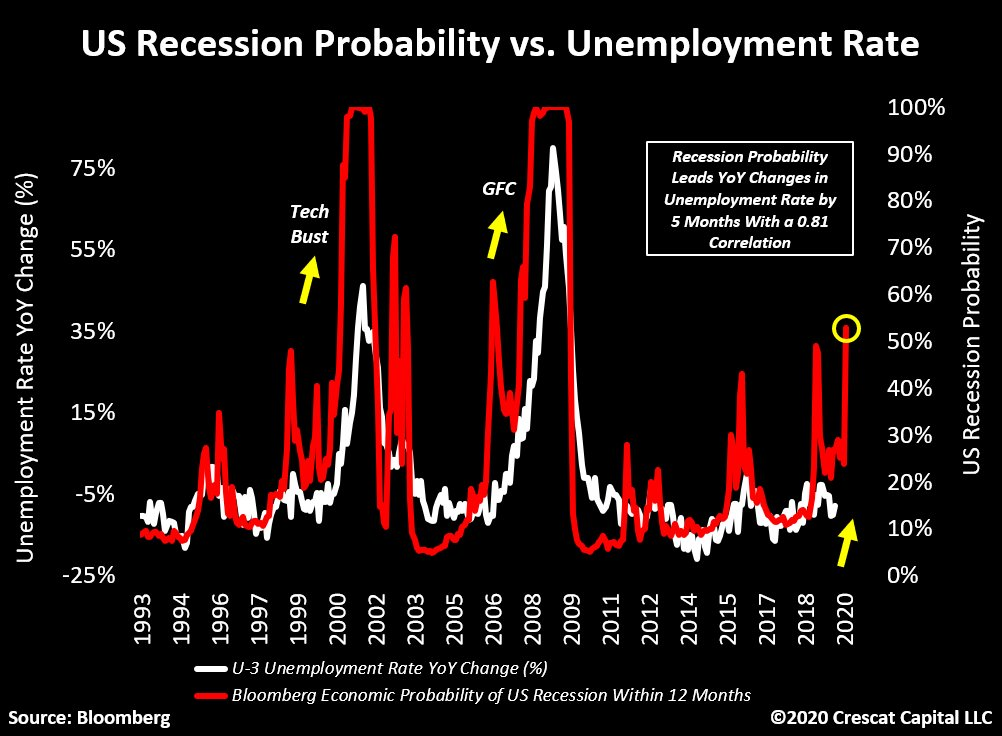

Stocks are acting like it’s the Great Depression again and we believe

a recession has already begun. The probability for a US recession, as

measure by this Bloomberg indicator, just surged above 50%. It’s

currently at its highest level since the global financial crisis. This

indicator leads changes in unemployment by 5 months with a 0.81

correlation. It suggests that the labor market has peaked.

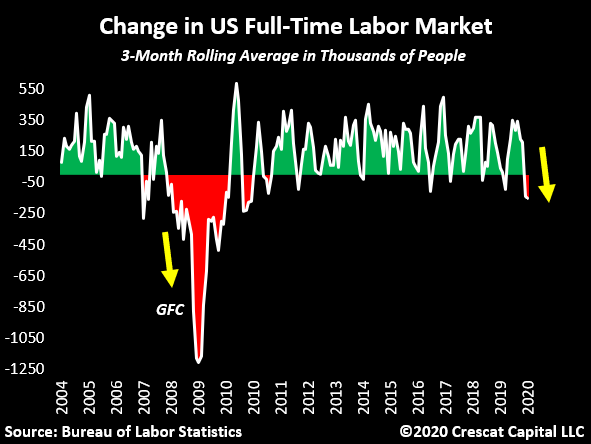

We have also recently noted that the number of full-time employed

people is now contracting. This was already rolling over in January.

With the recent impacts from the virus outbreak, we believe this number

will be plunging imminently.

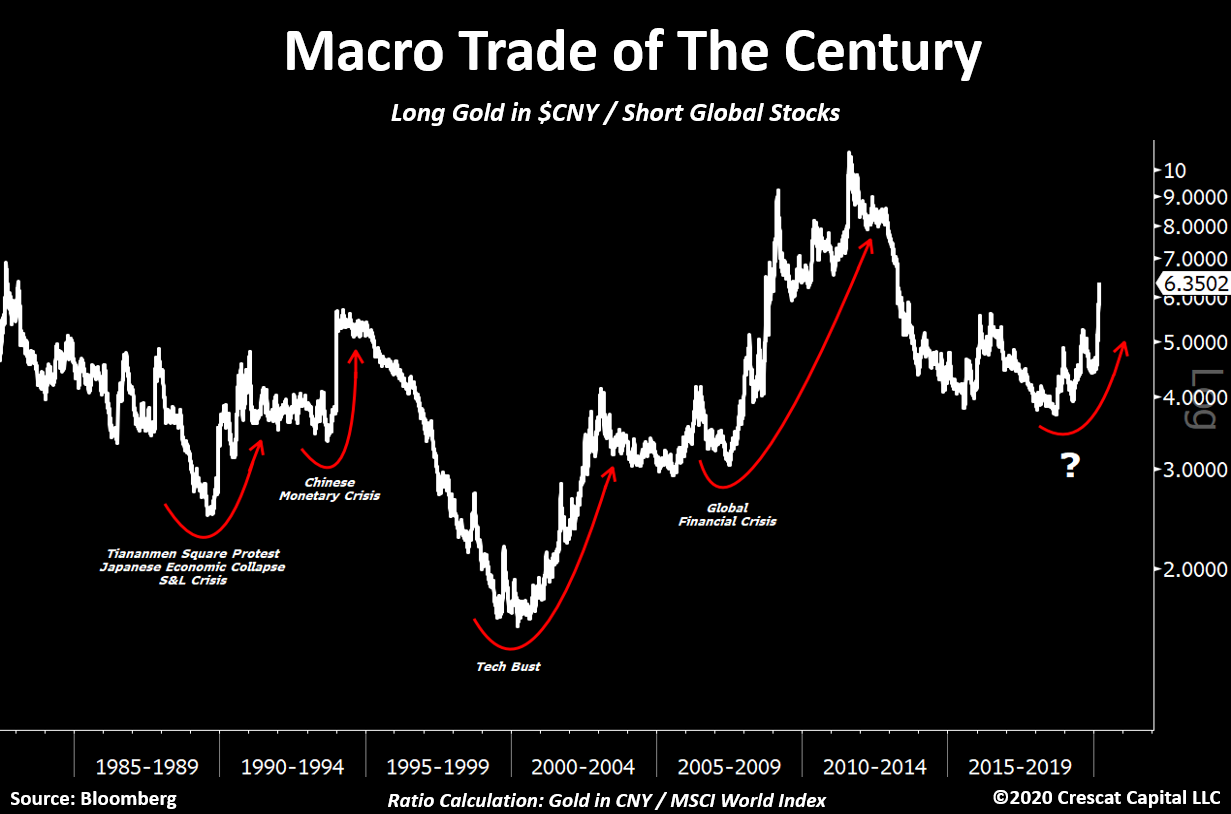

Macro Trade of the Century

Crescat’s “Macro Trade of the Century†has been working phenomenally

well since the market top. We believe our in-depth analysis looking at

the history of economic cycles and the development of macro models is

paying off tremendously. This is just the beginning of this three-legged

trade. The global economy has just entered a recession and the

fundamental damage of the virus outbreak on an already over-leveraged

economy will be greater than anything we have ever seen. We have massive

underfunded pensions with governments and corporations record indebted,

while wealth inequality is at an extreme across the globe. It is not

the ideal mix for asset prices that remain grossly overvalued worldwide.

When investors ask us if our macro themes to position for the

downturn have already played out, the answer is absolutely not. There is

so much more to go. We explain it in three ways:

1) The bursting of China’s credit bubble, the largest we’ve seen in

history, has yet to materialize in its most brutal manner. As macro

imbalances unfold worldwide, the Chinese current account should only

continue to shrink and exacerbate its dollar shortage problem. We expect

that a large devaluation in its currency versus USD is coming soon. We

haven’t seen anything yet. We remain positioned for this in an

asymmetric way through put options in our global macro fund in the yuan

and the Hong Kong dollar.

2) Except for last year, gold, silver, and the precious metals’

miners haven’t yet performed in the way we think they will. Instead they

have recoiled in a major way YTD. Meanwhile, central banks are clearly

losing control of financial markets and further monetary stimulus

appears unavoidable. The entire precious metals’ industry should benefit

from this macro backdrop. The near- and medium-term upside opportunity

in the entire precious metals complex has never looked more attractive

than it does today.

3) Equity markets remain about 30% above their median valuations

throughout history. The coming downturn is one that will likely not stop

at the median. As we showed above, we believe there is much more

downside ahead for stocks at large before we reach the trough of the

current global recession.

In our hedge funds, we added significantly to our precious metals

positions with gains from our short sales late last week. We have also

recently been harvesting profits in some of the most beaten down of our

shorts. We remain net short global equities but much less so than a

month ago and with less gross exposure overall. As a value-oriented

global macro asset management firm, we believe there is so much more to

play out as the economic cycle has only just begun to turn down. We are

not perma-bears, but we are determined to capitalize on this downturn.

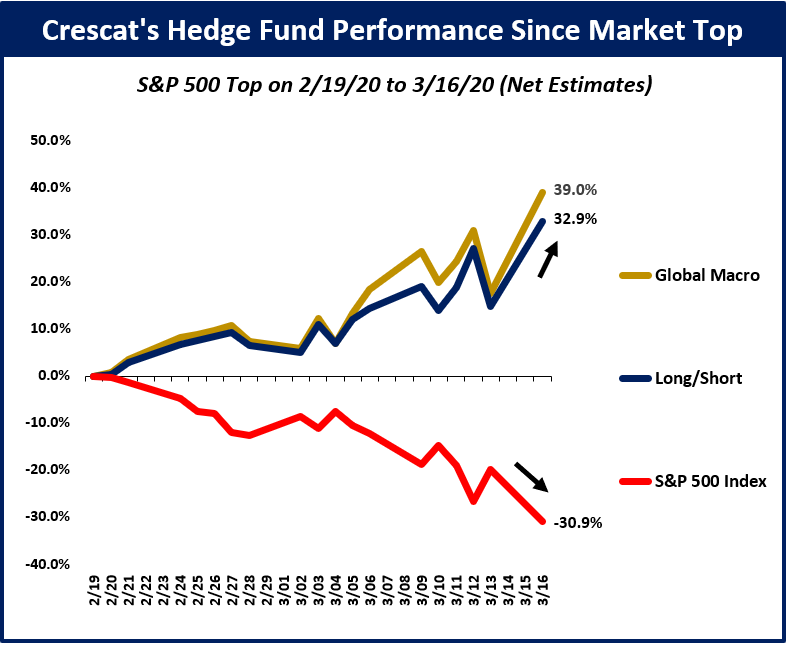

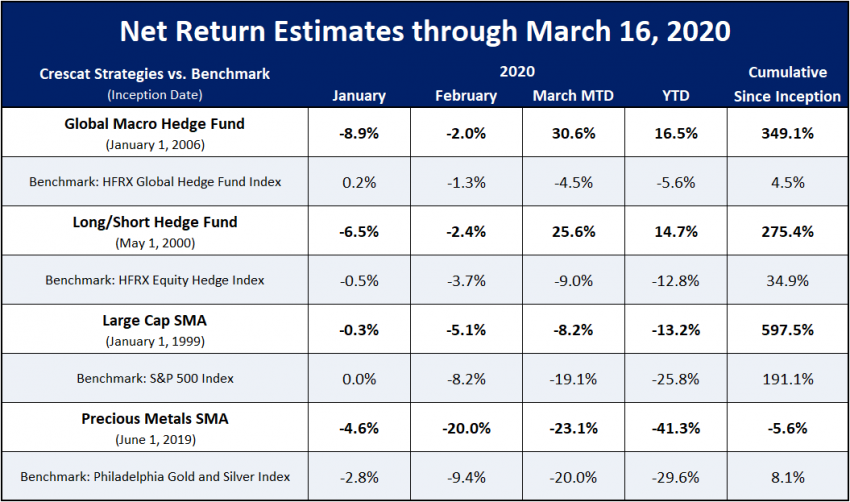

Crescat Performance Update

We have been telling our hedge fund clients for the past several

quarters that we have been tactically positioned for a market and

economic downturn ripe to unfold. Indeed, it has finally begun. Below,

we show how our hedge funds have been performing since the top in the

S&P 500 on February 19:

If you are interested in learning more about Crescat or investing with us, we encourage you to contact Linda Carleu Smith at [email protected] or (303) 228-7371.