Posted by AGORACOM-JC

at 12:45 PM on Tuesday, February 11th, 2020

SPONSOR: BetterU Education Corp.

aims to provide access to quality education from around the world. The

company plans to bridge the prevailing gap in the education and job

industry and enhance the lives of its prospective learners by developing

an integrated ecosystem. Click here for more information.

Indian edtech company Think and Learn, the owner and operator of learning app Byju’s, is now valued at about US$8.2 billion, following a fresh US$200 million funding by private equity firm General Atlantic, a person familiar with the company’s thinking said.

The latest injection in the company’s series F round comes after Tiger Global’s US$200 million investment last month.

“General Atlantic has been one of our strongest partners, and this

additional investment shows their confidence in our vision, growth, and

future,†Byju’s founder Byju Raveendran said in a press release.

The education app creates learning programs for K-12 students, as

well as for other competitive exams. It currently has 42 million

registered users and 3 million paid subscribers, according to the

company.

AD. Remove this ad space by subscribing. Support independent journalism.

This latest fundraise comes amid reports of turmoil at other Indian

unicorns. The snafu at SoftBank-backed WeWork has forced many to pivot

and focus on profitability, which has hurt growth prospects at a time

when India’s economy is slowing.

Byju’s is one of the few profitable startups in India. It got its start in 2005, when Raveendran took a break as a service engineer for a shipping company to coach students.

The company turned profitable on a full-year basis for the financial

year that ended in March 2019, Byju’s said. According to the firm, net

profit stood at about US$2.8 million, with revenue of about US$207

million. It had earned about US$73 million in revenue a year earlier.

However, Byju’s didn’t provide a figure for the bottom line for fiscal

year 2018.

Byju’s is on track to earn a little more than US$420 million for the

financial year that will end in March 2020, it said. The company adds

that students use the app for some 71 minutes on average daily, and

renewal rates are currently at 85%.

The firm raised US$150 million in July 2019 via a round led by

sovereign wealth fund Qatar Investment Authority. Edtech investor Owl

Ventures was also involved in the fundraise. Their investment in Byju’s

marked the first time that the two firms backed an Indian startup.

AD. Remove this ad space by subscribing. Support independent journalism.

Four months earlier in March, Byju’s raised about US$11.4 million from General Atlantic and Tencent, which took its valuation to about US$4 billion.

Other notable investors in the company are Naspers, the

Chan-Zuckerberg Initiative, Sequoia Capital, and Lightspeed Venture

Partners, among others.

Posted by AGORACOM-JC

at 12:15 PM on Tuesday, February 11th, 2020

SPONSOR: New Age Metals Inc.

The company owns one of North America’s largest primary platinum

group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral

Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an

additional 1,059,000 PdEq Ounces Inferred. Learn More.

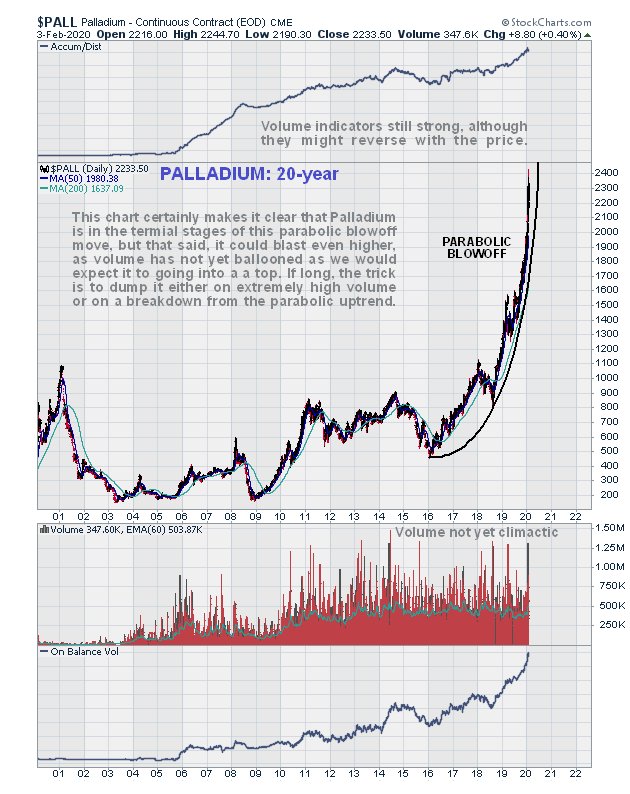

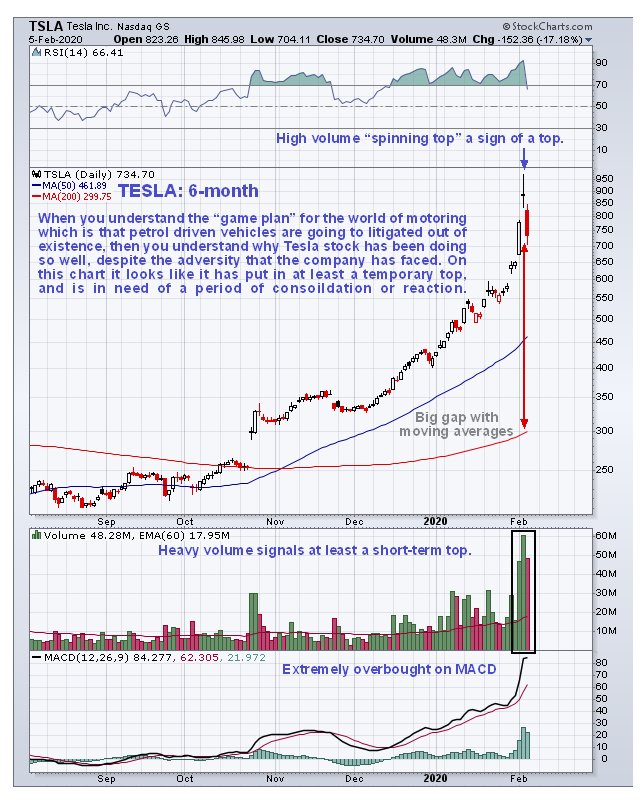

Palladium, Tesla and the Imposition of Electric Vehicles

What underlies the tremendous runup in the price of Palladium and now the giant spike in Tesla stock? They are connected.

Tesla stock has spiked despite its self-driving cars doing strange things like running people over and spontaneously combusting.

By: Clive P. Maund

What underlies the tremendous runup in the price of Palladium and now

the giant spike in Tesla stock? They are connected. Tesla stock has

spiked despite its self-driving cars doing strange things like running

people over and spontaneously combusting. The reason for this is the

relentless drive towards electric cars which will result in a massive

increase in demand for palladium and electric car manufacturers like

Tesla becoming mainstream.

The elites have a Master Plan to push ordinary motorists off the road

and back onto public transport, and they will realize this by using the

environmental scare to effectively outlaw petrol driven cars and force a

transfer to expensive electric cars, which will be out of reach of many

motorists because of their cost. Greta is a pawn in this game. The

means by which they will outlaw petrol (and diesel) driven cars is to

class carbon dioxide as an emission, which they have already done, and

then make the emissions standards tighter and tighter until petrol

driven cars are forced off the road. Since anything that burns anything

creates carbon dioxide, which is essentially an inert natural gas, it is

clear that petrol driven cars cannot reduce their carbon dioxide

emissions to zero, so their fate is already sealed. You may be asking

what is the motivation for doing this. There are a number of reasons.

One is to reduce the profligate consumption of oil by the masses for

their personal transportation and the resulting pollution. Another is

control – a public who lack personal transportation and the freedom it

brings are of course easier to control and direct. Lastly it will free

up the roads for the elites, who will suffer less from delays caused by

traffic congestion resulting from the masses on the move, since they,

the elites, will always be able to afford private vehicles, no matter

what they cost. The masses will not resist this transformation of their

lives. First of all they are ignorant and have no idea of the plans for

them that are already at an advanced stage. Secondly, they are too cowed

and docile to do anything about it even if they did know. Now that you

know what is set out above, you should be able to readily appreciate why

the price of palladium, and of Tesla stock, have been soaring. Let’s

now proceed to look at their extraordinary charts. Starting with

palladium, we see on its long-term 20-year chart that after essentially

tracking sideways for many years, the phase of accelerated advance

really didn’t begin until mid-2018, and it was only later in 2018 that

it broke out above its highs way back in 2001. So the dramatic

acceleration in its rate of advance has been going on for 18 months or

less.

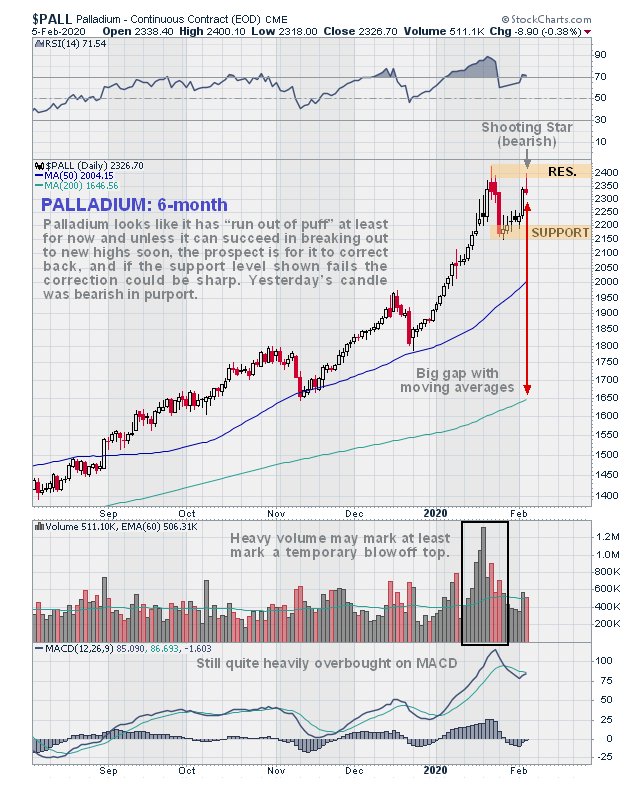

We can see the period of accelerated advance in more detail on

the 5-year chart, and how the point of origin of the accelerating

parabolic uptrend is at the start of 2016. The price only cleared the

resistance at the 2001 highs in the $1080 area as recently as late 2018

and it is only over the past 6 months or so that we have seen dramatic

acceleration. This chart makes clear that as the price has now run way

ahead of its parabolic supporting uptrend, there is plenty of room for

it to correct back or consolidate without breaking down from the

uptrend, although it could well spike even higher from here, with

speculation now rampant.

On the 6-month chart we can see that at the recent peak volume

became really heavy, which puts us on notice that even if this wasn’t

the top for this run, a top may not be far off.

Turning now to Tesla, we can see that it has suddenly gone

vertical in recent weeks, which implies that the age of the electric

vehicle is almost upon us. Even so, this move looks extreme, especially

on long-term charts and suggests that a reaction back or period of

consolidation is now likely over the short-term.

Modern cars have become a nightmare of over-regulation and

control and it’s going to get a lot worse. They got rid of ignition keys

so that you now have a push button start and have to pay for very

expensive key fobs. All modern cars look the same because of draconian

regulations regarding impacts and safety, and they are all designed in

the same wind tunnel. For unknown reasons – probably bigger profits for

the manufacturers – most cars are the same standard colors. “You can

have any color you like sir, as long as its black, red, silver or

white.†The core of the car is too heavy for safety reasons and is

compensated for by flimsy bodywork, in order to meet fuel consumption

targets. Bumpers, which used to be designed to take impacts with no

damage or resulting cost, are now made of delicate painted structures

which cost a fortune to fix after even the slightest impact, but that’s

no problem because the insurance covers it, except that this means

raised insurance premiums. You can’t turn the engine off and open the

door and listen to the radio on a hot day, because either it switches it

off or starts making stupid bleeping noises. Some new cars switch the

engine off every time you come to a stop, and you have to be at a dead

stop to put it in gear etc. Your location is always known because the

car is computerized and online, which incidentally means that it is

theoretically possible to hack the car remotely and cause it to crash,

by say, locking the brakes. For this reason also you can never be sure

that any conversation you have in the car is private – they could be

broadcasting it live in the Superbowl stadium. Even for a 100 meter trip

down the road the baby or child has to be strapped into a child seat.

The list is endless and the future is going to be even worse. Rear view

mirrors are going to be swapped for cameras that display on the central

screen, so if anything goes wrong with it you have an expensive

replacement of the entire system. There are going to be cameras mounted

on /in the dash that monitor your facial expressions and if you look

drunk or tired, the onboard computer will seize control of the car and

force it to pull over. Likewise your days of breaking speed limits are

over, since the car won’t let you. No wonder teens are not interested in

cars anymore – you won’t hear any of them saying told my girl I had to forget her, rather buy me a new carburetor.

Posted by AGORACOM-JC

at 11:22 AM on Tuesday, February 11th, 2020

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

The burgeoning electric vehicle (EV) sector has taken the mining industry by storm in the last five years

The burgeoning electric vehicle (EV) sector has taken the

mining industry by storm in the last five years with the metals and

minerals used in the production of battery energy storage, including

cobalt, lithium, graphite, nickel and vanadium taking centre stage.

Nickel takes the lead as battery metal of choice

The significant interest in these battery metals has caused a flurry

of mining companies to enter the race to extract them, causing prices to

surge.

Fast-forward to 2019 and the picture looks very different, prices

have plummeted, mostly due to demand struggling to keep up with supply,

and in some cases better metal substitutes being found.

However, one thing remains clear, the future global demand outlook

for EVs remains strong and so does the need for energy storage in

renewable energy applications.

Cobalt and lithium – the battery metals front runners

According to Diego Oliva-Velez, commodities analyst at Fitch Solutions, lithium

and cobalt prices are likely to remain subdued over the coming months

as demand struggles to keep up with new supply coming online.

Because cobalt and lithium have received significant investor

interest since 2015 due to their increasing use in lithium-ion

batteries, which power the burgeoning electric vehicle industry, the

resultant demand and prices for both metals have been on the rise.

“For instance, cobalt prices rose over 300% in the period from 2016

to 2018, while South America lithium carbonate prices rallied over 170%

during a similar time frame,†says Oliva-Velez.

“However, rising prices have also spurred a flurry of investments

into new cobalt and lithium projects that have significantly loosened

both markets – which caused prices to start to unwind since 2018.

The demand outlook for both EV metals waned in 2019, as the removal

of Chinese government subsidies to EV manufacturers caused a slowdown

across the industry.

In March 2019, the Chinese government announced that from July

onwards subsidies for pure battery electric vehicles with driving ranges

of 400 km or more would be cut by half.

Furthermore, to qualify for subsidies, electric vehicles now need to

have a range of at least 250 km, compared with 150 km previously.

Without these subsidies, Chinese EV manufacturers are having to raise

the prices of their vehicles, leading to reduced sales and output

numbers over the past months, as they become less affordable to

consumers.

However, the Fitch Solutions Autos team believes the subsidy cuts

will only have a short-term impact on China’s EV market, as revised

government policy calls for a more profound engagement from

manufacturers to preserve EV market growth rates, while rising

competition will continue to support the EV segment.

Fitch Solutions’ Autos team also highlight that the new policy sets

out sales targets for car manufacturers, whereby they must generate

credits for selling EVs, which should prop up EV production.

Furthermore, they expect carmakers will move to offset the impact of

the EV subsidies cuts with price reductions, which will see demand for

EVs remain robust over 2020.

Fitch Solutions forecast EV sales in China to average 20% year-on-year in 2020, slightly up from 19% in 2019.

Despite announcements of supply cutbacks (such as the premature

closure of Glencore’s Mutanda cobalt mine in the Democratic Republic of

Congo in late 2019) and rising demand, there are a number of new

projects due to come online, including Chemaf Sarl’s Mutoshi mine in the

DRC, CleanTeQ Holdings’ Sunrise nickel cobalt scandium project and

Australian Mines’ Sconi project, both in Australia.

As a result, Fitch Solutions retains the view that both markets will

remain largely in oversupply next year – keeping a lid on prices.

Nevertheless, Oliva-Velez expects demand growth for lithium and

cobalt to improve in 2020 following a disappointing 2019, as low prices

attract purchases from EV battery manufacturers and Chinese EV sales

hold strong.

Nickel takes the lead as battery metal of choice

Fitch Solutions’ outlook for nickel over 2020 is more positive as the

market will remain in deficit, buoyed by a ban on Indonesian ore

exports from January 2020 and ongoing support from the Chinese stainless

steel sector.

Despite a steep fall in prices since October 2019, Fitch Solutions

believe that prices will rebound from spot levels into 2020 and average

US$15 000/t throughout 2020, buoyed by a tight fundamental picture.

Moreover, the global nickel market is expected to remain in a deficit

of 12 200 t in 2020, driven by sustained demand from stainless steel

production in China.

Based on findings from Fitch Solutions’

own proprietary model, nickel is set to be the primary demand

beneficiary of the EV revolution on the metals side in the longer term

beyond 2021, significantly ahead of lithium or cobalt – as the use of

nickel-heavy NMC cathodes among manufacturers become increasingly

prevalent over the same period.

The NMC cathode will become the chemistry of choice for EV

manufacturers over the coming years, due to its high energy density,

thermal stability and low cost.

Currently, most NMC cathodes are referred to as NMC 622, so-called

due to the ratio of metals they contain (6 parts nickel, 2 parts

manganese and 2 parts cobalt).

However, due to concerns relating to the price and sustainable

sourcing of cobalt, battery manufacturers are in the process of

increasing the share of nickel in these cathodes in order to achieve a

ratio of 811 (8 parts nickel, 1 part manganese and 1 part cobalt).

“We forecast that the share of NMC cathodes will account for 82% of

all new NMC battery sales by 2029, up from just 2% in 2019. This

transition will lead to an increase in average nickel content from 7.24

kg to 16.76 kg for each NMC cathode produced over the same period,†says

Oliva-Velez.

Nickel upsurge reduces demand for cobalt

The transition towards nickel-heavy NMC 811 cathodes will lead to

lower demand for cobalt, which will increasingly be shunned by

manufacturers due to price and sustainability considerations.

The unstable and restricted supply of cobalt from the DRC – the

largest producer by a significant margin – makes the metal prone to

price spikes, as witnessed over 2017.

Secondly, the questionable ethical nature of cobalt supplied by the

DRC, due to the prevalence of child labour and conflict mines in the

country, will drive battery makers away from the metal in an effort to

mitigate reputational risk.

“As a result, we forecast cumulative demand for cobalt from EV

batteries over 2019 to 2028 to amount to 218 000 t, considerably less

than nickel, lithium and even manganese,†Oliva-Velez points out.

Lithium remains an integral battery metal going forward

Lithium is found in both the anode and cathode of all lithium-ion

battery chemistries, being the key element that allows batteries to

charge and discharge.

Furthermore, unlike cobalt, global lithium supply is more diversified

across a number of better regulated jurisdictions such as Chile,

Australia, Argentina and China – making it less prone to price spikes or

environmental, social and governance (ESG) concerns.

As a result, lithium will continue to be an integral component of all

EV batteries moving forward – supporting global demand levels for the

metal over the next 10 years.

Therefore, in the longer term, prices of all key battery metals are

set to rise as demand from the EV industry ramps up, with nickel being

the primary demand beneficiary.

Graphite – new low-cost sources needed

The biggest driver of the flake graphite market has been the

introduction of new supply from Africa – primarily from Madagascar and

Mozambique.

In 2018, ASX-listed Syrah Resources brought the world’s largest flake

graphite operation into production and the new production volumes

introduced to the market from its Balama graphite project in Mozambique

have added to excess graphite capacities in China – which has been the

world’s leading graphite supplier for a generation. [Insert image of

Balama here]

As China focuses its domestic graphite output on value-added markets,

there remains a need for need for new low-cost sources of flake

graphite material – the anode material of choice for commercial

lithium-ion rechargeable batteries – and Africa has several promising

projects aiming to fill this role to global markets, according to Andrew

Miller, head of price assessments at Benchmark Mineral Intelligence.

“At this stage the introduction of new graphite material from Africa

has overtaken the demand growth, which will be largely driven by the

production of lithium-ion battery anodes and, ultimately, EV penetration

rates,†says Miller.

Moving forward there is a significant backlog to overcome in the

market which is likely to see continued depressed prices into 2020.

Longer-term however, the industry is still faced with the major task of

expanding graphite production to meet the projected growth in battery

demand and the low graphite prices of today will not be capable to

support the development of many new projects.

As a result, Miller says the market is in a transition period with

demand growth on the horizon and an abundance of feedstock material –

the question is how much of this can be used in the lithium-ion battery

supply chain and how much of this will be available ahead of the major

ramp up of battery projects.

Vanadium – the key to renewable energy storage

According to AIM-listed Bushveld Minerals, a low-cost, vertically

integrated primary vanadium producer with assets in South Africa,

Vanadium currently benefits from having two strong uses driving its

demand.

One, the traditional steel sector, where vanadium is used as a

strengthening alloy, which boasts a steady growth trajectory according

to most general forecasts due to an increase in intensity in use of

vanadium.

Two, the energy storage sector, where vanadium is the primary input

into vanadium redox flow batteries (VRFBs), which not only benefits the

burgeoning renewable energy sector, but significantly, and perhaps more

importantly, helps make existing power systems more efficient through

load balancing and other forms of grid savings.

Upside in demand from the energy storage sector

Research from Navigant forecasts that the size of the energy storage

market will reach US$50 billion within the next 10 years, which

represents a growth rate of 58% a year to exceed 100 GWh of capacity by

2027.

While multiple technologies are expected to be successful due to

their unique technical and cost advantages and suitability to local

conditions, VRFBs are expected to capture approximately 18% of the

market, which equates to 20 GWh of demand and nearly $10 billion in

revenue in the coming decade.

This confidence is shared by the World Bank, which recently allocated

$1 billion to a global battery storage programme (aiming to raise an

additional $4 billion in co-investment) to drive market creation and

help drive down battery prices in low- and middle-income countries.

From a VFRB deployment perspective, there are already a number of

large VRFB projects in progress, including the largest VRFB in the world

currently under construction, demonstrating the technological benefits

and proven use-cases in countries with established power grid

infrastructure.

In South Africa, the country’s recently published Integrated Resource

Plan 2019 specifically seeks novel ways to improve grid reliability and

access to power over the long-term, with a dedicated allocation of over

2 GW for new energy storage.

As a result of these developments, Bushveld Minerals founder and CEO

Fortune Mojapelo is confident that vanadium will continue to feed the

primary steel market, while gaining further market share of the

important energy sector through VRFBs.

Tags: CSE, nickel, nickel demand, stocks, tsx, tsx-v Posted in Tartisan Nickel | Comments Off on The burgeoning electric vehicle #EV sector has taken the #mining industry by storm in the last five years – SPONSOR Tartisan #Nickel $TN.ca – $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 8:40 AM on Tuesday, February 11th, 2020

After the successful GEN2 PUREVAPTM QRR proof of concept test, PyroGenesis finalised the engineering designs and the plans required to upgrade a PUREVAPTM QRR into a PUREVAPTM reactor that can transform melted silicon metal into spherical Nano-Powders and Nanowires

As a result of this work, a new provisional patent application was filed to protect this new process.

MONTREAL, Feb. 11, 2020 — HPQ Silicon Resources Inc. (“HPQâ€Â or the “Companyâ€)TSX-V: HPQ; FWB: UGE; Other OTC : URAGF; (“HPQâ€) would like to update shareholders on the steps being undertaken by HPQ and PyroGenesis Canada Inc. (TSX-V: PYR) (“PyroGenesisâ€) to advance the development of a new low cost manufacturing process that can produce the Spherical Silicon Metal (Si) Nano-Powders and Si Nanowires needed for the next generation of Lithium-ion (Li-ion) Si batteries.

BUILT ON 5 YEARS OF PUREVAPTM QUARTZ REDUCTION REACTOR (QRR) DEVELOPMENT KNOW-HOW

After the successful GEN2 PUREVAPTM QRR proof of concept test, PyroGenesis finalised the engineering designs and the plans required to upgrade a PUREVAPTM QRR into a PUREVAPTM

reactor that can transform melted silicon metal into spherical

Nano-Powders and Nanowires. As a result of this work, a new provisional

patent application was filed to protect this new process.

DEVELOPING THE PUREVAPTMSILICON METAL NANO REACTOR (SiNR)

The new PUREVAPTM process is a Silicon Metal Nano Reactor, (PUREVAPTM SiNR), that incorporates the PUREVAPTM QRR (patent

pending) unique capability of removing impurities from Silicon Metal

(Si) into a novel proprietary process that allows different purities of

Si feed stock to be melted into liquid Si. This liquid Si can then be

synthesized into the Spherical Silicon Metal Nano Powders and Nanowires sought after by Corporations looking into building the next generation of Lithium-ion batteries.

“The PUREVAPTM SiNR opens up a unique multibillion-dollar

business opportunity for HPQ and PyroGenesis. PyroGenesis has a long

track record of taking high-tech industrial projects from proof of

concept to global commercial scalability, so we are very confident about

the prospect of being one of the first companies coming to market with a

low cost process that makes the spherical Silicon Metal Nano-Powders

and Nanowires that next generation Li-ion battery manufacturers are

seeking,†said Bernard Tourillon, President and CEO HPQ Silicon. “Silicon Metal’s potential to meet energy storage demand is undeniable and generating massive investments, as well as, serious industry interest, so our timing could not be better.â€

GEN2 PUREVAPTM QRR CONVERTED INTO A PROOF OF COMMERCIAL SCALABILITY PUREVAPTMSINR

The quickest way to demonstrate the capabilities of the PUREVAPTM SiNR process is to upgrade the existing GEN2 PUREVAPTMQRR into PUREVAPTM SiNR

test bed, run a series of tests to confirm the scalability, the

low-cost nature of the process and its feedstock flexibility. During

these tests, Spherical Silicon Metal Nano-Powders and Nanowires samples

will be produced and sent to either research centers for independent

valuation or made available to potential end users looking at

manufacturing next generation Li-ion batteries. Successful tests will

demonstrate the process flexibility in making a range of advanced

Silicon Metal materials. The preliminary timeline is for the reactor

conversion to be completed over the next coming months, with a goal of

being able to have samples ready in this fiscal year.

SPHERICAL Si NANO POWDERS AND NANOWIRES KEY TO HIGHER ENERGY DENSITY LI-ION BATTERIES

Spherical Silicon Metal Nano-Powders and Si Nanowires have been identified

as key elements that will allow the manufacture of high-performance

Li-ion batteries using Silicon Metal (Si) anodes needed to deliver on

the research

promises of an almost tenfold (10x) increase in the specific capacity

of the anode, inducing a 20-40% gain in the energy density of Li-ion

batteries. Current manufacturing methods for Silicon Metal Nano-Powders

are expensive, not very scalable and not commercially feasible with US$

30,000/kg1 selling prices, while manufacturing Silicon Metal Nanowires

is so prohibitive that only government funded special projects can

afford them.

“The opportunities that are being developed with the PUREVAP™

process is nothing short of intoxicating,†said M. P Peter Pascali,

President and CEO of PyroGenesis Canada Inc. “We never thought, when we

first embarked on this project, that we would be developing

game-changing technology sought after by the Lithium-ion battery market.

We are looking forward to successfully incorporating and upgrading the

PUREVAP QRR™ into the PUREVAP™ Nano reactor to produce Spherical

Silicon Metal (Si) Nano-Powders and Si Nanowires needed for the next

generation of Lithium-ion (Li-ion) Si batteries.â€

About Silicon Metal

Silicon Metal (Si) is one of today’s strategic materials needed to

fulfil the renewable energy revolution presently under way. Silicon does

not exist in its pure state; it must be extracted from quartz, one of

the most abundant minerals of the earth’s crust and other expensive raw

materials in a carbothermic process.

About HPQ Silicon

HPQ Silicon Resources Inc. (TSX-V: HPQ) is developing, with PyroGenesis Canada Inc.(TSX-V: PYR), a high-tech company that designs, develops, manufactures and commercializes plasma base processes, the innovative PUREVAPTM “Quartz Reduction Reactors†(QRR),

a truly 2.0 Carbothermic process (patent pending), which will permit

the One Step transformation of Quartz (SiO2) into High Purity Silicon

(Si) at prices that will propagate its considerable renewable energy

potential. The Gen3 PUREVAPTM QRR pilot plant that will validate the commercial potential of the process is scheduled to start during Q1 2020.

HPQ, working with PyroGenesis, is also developing the PUREVAPTM Silicon Metal Nano Reactor (SiNR),

a proprietary process a that can use as feedstock different purities of

Silicon Metal (SI), melted them into liquid Si that can then be

synthesized into the Spherical Silicon Metal Nano Powders and Nanowires

necessary for the next generation of Lithium-ion batteries. During H1

2020, the plan is to validate our game changing manufacturing approach

by upgrading our existing Gen2 PUREVAPTMQRR reactor into a PUREVAPTMSINR to produce spherical Silicon Metal (Si) nano-powders and nanowires samples for industry participants and research institutions’.

Concurrently, HPQ is also working with industry leader Apollon Solar to develop a manufacturing capability that uses the High Purity Silicon (Si) made with the PUREVAP™

to make Porous silicon wafers needed for solid-state Li-ion batteries.

The first Silicon wafer should be ready to be ship for testing to a

battery manufacturer (under NDA) during H1 2020.

Finally, with Apollon Solar, we are also looking into developing a

metallurgical pathway of producing Solar Grade Silicon Metal (SoG Si)

that will take full advantage of the PUREVAPTM QRR one-step production of Silicon (Si) material of 4N+ purity with low boron count (< 1 ppm).

The focus of HPQ focus is to become the lowest cost producer of

Silicon Metal (Si), High Purity Silicon Metal (Si), Spherical Si

nano-powders for Next Gen Li-ion batteries, Porous Silicon Wafers for

Solid states Li-ion batteries, Porous Silicon Powders for Li-ion

batteries and Solar Grade Silicon Metal (SoG-Si).

This News Release is available on the company’s CEO Verified Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

Disclaimers:

The Corporation’s interest in developing the PUREVAP™ QRR and any

projected capital or operating cost savings associated with its

development should not be construed as being related to the establishing

the economic viability or technical feasibility of any of the Company’s

Quartz Projects.

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward-looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Company’s current expectation and assumptions and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Company with respect to future events and are subject to certain risks

and uncertainties and other risks detailed from time-to-time in the

Company’s on-going filings with the security’s regulatory authorities,

which filings can be found at www.sedar.com. Actual results, events, and

performance may differ materially. Readers are cautioned not to place

undue reliance on these forward-looking statements. The Company

undertakes no obligation to publicly update or revise any

forward-looking statements either as a result of new information, future

events or otherwise, except as required by applicable securities laws.

Neither the TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in the policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

For further information contact Bernard J. Tourillon, Chairman, President and CEO Tel (514) 907-1011 Patrick Levasseur, Vice-President and COO Tel: (514) 262-9239 http://www.hpqsilicon.com Email: [email protected]

Tags: CSE, High Purity Quartz, High purity silicon, stocks, tsx, tsx-v Posted in Featured, HPQ-Silicon Resources Inc. | Comments Off on Developing New #PUREVAP™ Silicon Metal Nano Reactor for Low-Cost Manufacturing of Spherical Silicon Metal Nanopowders & Nanowires for Next Generation Li-ion Batteries $HPQ.ca $PYR.ca $FSLR $SPWR $CSIQ $PYR.ca $XMG.ca

Posted by AGORACOM-JC

at 6:31 AM on Tuesday, February 11th, 2020

Announced that patient visits in corporate clinics increased by 188% in January 2020 versus the same period in 2019, with total patient visits of 1,750 in January 2020 compared to 607 in January 2019.

VANCOUVER, BC /February 11, 2020 / EMPOWER CLINICS INC. (CSE:CBDT)(OTC:EPWCF)(Frankfurt:8EC) (“Empower” or the “Company“), a vertically integrated and growth-oriented CBD life sciences company is pleased to announce that patient visits in corporate clinics increased by 188% in January 2020 versus the same period in 2019, with total patient visits of 1,750 in January 2020 compared to 607 in January 2019.

“January patient volumes were strong, setting the stage for

potentially record first quarter patient visits, that are always focused

on the patient experience, it’s a competitive advantage and I continue

to be impressed with how our team members care for each and every

patient they see.” said Steven McAuley, Chairman & CEO of Empower.

“Looking forward, we are excited for our next franchise signings and the

expansion of our product lines, adding to the in-clinic retail

experience we are building.”

The Company utilizes it’s technology platform to communicate with

patients by text message, email and call center ensuring appointments

are confirmed and expected patient visits take place as planned.

The Company’s Sun Valley Health division also completed the set up

and build out of it’s retail product counter and sales areas in it’s

Tucson, AZ location, to showcase it’s CBD product line with over 50

unique SKU’s. Patients and customers can purchase product in clinic

locations or online at www.sunvalleyhealth.com.

ABOUT EMPOWER

Empower is a vertically-integrated health & wellness brand with

it’s first hemp-derived CBD extraction facility under development, the

Company produces its proprietary line of cannabidiol (CBD) based

products and distributes products through company owned and franchised

clinics, with wholesale partnerships, online channels and with new

retail opportunities nationwide in the U.S. The company is a leading

multi-state operator of a network of physician-staffed wellness clinics,

focused on helping patients improve and protect their health, through

innovative physician recommended treatment options. The company has

commenced activity on how to connect its significant data, to the

potential of the efficacy of alternative treatment options related to

hemp-derived cannabidiol (CBD) therapies.

Investors: Dustin Klein SVP, Business Development [email protected] 720-352-1398

For French inquiries: Remy Scalabrini, Maricom Inc., E: [email protected], T: (888) 585-MARI

DISCLAIMER FOR FORWARD-LOOKING STATEMENTS

This news release contains certain “forward-looking statements”

or “forward-looking information” (collectively “forward looking

statements”) within the meaning of applicable Canadian securities laws.

All statements, other than statements of historical fact, are

forward-looking statements and are based on expectations, estimates and

projections as at the date of this news release.Forward-looking statements

can frequently be identified by words such as “plans”, “continues”,

“expects”, “projects”, “intends”, “believes”, “anticipates”,

“estimates”, “may”, “will”, “potential”, “proposed” and other similar

words, or information that certain events or conditions “may” or “will”

occur. Forward-looking statements in this news release include

statements regarding; the Company’s intention to open a hemp-based CBD

extraction facility, the expected benefits to the Company and its

shareholders as a result of the proposed acquisitions and partnerships;

the effectiveness of the extraction technology; the expected benefits

for Empower’s patient base and customers; the benefits of CBD based

products; the effect of the approval of the Farm Bill; the growth of the

Company’s patient list and that the Company will be positioned to be a

market-leading service provider for complex patient requirements in 2019

and beyond. Such statements are only projections, are based on

assumptions known to management at this time, and are subject to risks

and uncertainties that may cause actual results, performance or

developments to differ materially from those contained in the

forward-looking statements, including; that the Company may not open a

hemp-based CBD extraction facility; that legislative changes may have an

adverse effect on the Company’s business and product development; that

the Company may not be able to obtain adequate financing to pursue its

business plan; general business, economic, competitive, political and

social uncertainties; failure to obtain any necessary approvals in

connection with the proposed acquisitions and partnerships; and other

factors beyond the Company’s control. No assurance can be given that any

of the events anticipated by the forward-looking statements will occur

or, if they do occur, what benefits the Company will obtain from them.

Readers are cautioned not to place undue reliance on the forward-looking

statements in this release, which are qualified in their entirety by

these cautionary statements. The Company is under no obligation, and

expressly disclaims any intention or obligation, to update or revise any

forward-looking statements in this release, whether as a result of new

information, future events or otherwise, except as expressly required by

applicable laws.

Posted by AGORACOM-JC

at 4:58 PM on Monday, February 10th, 2020

SPONSOR: New Age Metals Inc.

The company owns one of North America’s largest primary platinum

group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral

Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an

additional 1,059,000 PdEq Ounces Inferred. Learn More.

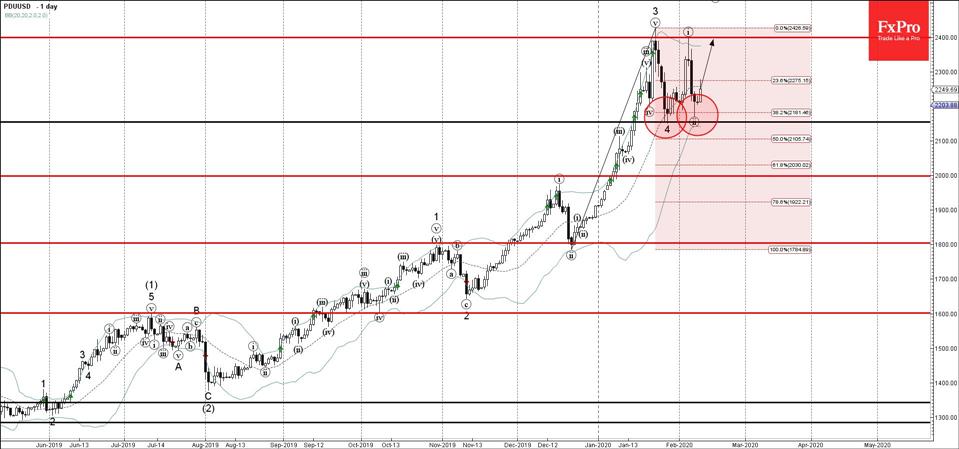

Palladium Wave Analysis 10 February, 2019

Palladium reversed from support area

Likely to rise to 2400.00

Palladium recently reversed up from the support zone located between

the key level 2155.00 (low of the previous short-term correction 4),

lower daily Bollinger Band and the 38.2% Fibonacci correction of the

pervious upward impulse 3 from December.

The upward reversal from this support area created the daily Japanese candlesticks reversal pattern Hammer.

Palladium is likely to rise further toward the next resistance level 2400.00 (top of the pervious impulse waves 3 and (i)).

Posted by AGORACOM-JC

at 3:51 PM on Monday, February 10th, 2020

SPONSOR: NORTHBUD (NBUD:CSE)

Sustainable low cost, high quality cannabinoid production and

procurement focusing on both bio-pharmaceutical development and

Cannabinoid Infused Products. Learn More.

Everything Canadians need to know about Legalization 2.0

Edibles, extracts, topicals, and vapes are finally legal in Canada. Billed as Legalization 2.0, the regulations came into effect on October 17, 2019 and products have slowly begun to trickle onto the market ever since.

Edibles, extracts, topicals, and vapes are finally legal

in Canada. Billed as Legalization 2.0, the regulations came into effect

on October 17, 2019 and products have slowly begun to trickle onto the

market ever since.

From how to consume, to what to consume, here’s everything Canadians need to know about Legalization 2.0.

Edibles 101

Cannabis-infused edibles are now available for sale through licensed

retailers in Canada, though there are strict rules around marketing and

dosing, including a limit of 10 mg of THC per packaged item.

Edibles in the form of food products, lozenges, and

beverages can produce effective, long-lasting, and safe experiences.

These forms of cannabis can also produce unpredictable effects that may feel like overdose symptoms. The difference is, of course, the dose, although it’s worth noting that while consuming too much can feel very unpleasant, no one has ever died from it.

It can take anywhere from 30 minutes to four hours for an edible to

fully kick in. Health Canada suggests that adults who use cannabis,

regardless of how they consume it, shouldn’t combine it with alcohol,

nicotine or other drugs.

Posted by AGORACOM-JC

at 3:41 PM on Monday, February 10th, 2020

Highlights

Lithium Processing: technology initiatives, patent formalization, battery recycling process and lithium metal manufacturing;

Pilot plant potentially de-risked through discussions with ready-built facilities;

Montreal, Montreal -Â February 10, 2020 – St-Georges Eco-Mining Corp. (CSE:SX)Â (CNSX:SX.CN)Â (OTC:SXOOF) (FSE:85G1)Â would like to update its shareholders on its on-going corporate developments.

In

the past six months, St-Georges has successfully executed its strategy

to strengthen and expand its focus on its green extraction metallurgical

processes development and re-center its exploration efforts on energy

metals in Quebec and Iceland. The team has also added a

Palladium-Rhodium project in Quebec and has advanced its Thor Gold

Project in Iceland to drill-ready status. Significant changes in the

Company operations, namely the sale of King of the North in September

and the spin-off of ZeU Crypto Networks Inc. in December, has allowed

the Company to free up resources that can now be allocated to the core

competencies of the Company.

Highlights

– Lithium Processing: technology initiatives, patent formalization, battery recycling process and lithium metal manufacturing;

– Pilot plant potentially de-risked through discussions with ready-built facilities;

– Hydro-Dam Project in Iceland advancing on its environmental permits;

– Status of Other Holdings.

Mineral Processing Research & Development

Lithium Processing Technology

Stage

I of the development of the Company’s lithium processing technology, in

collaboration with Iconic Minerals (TSX-V: ICM), was completed in the

first half of 2019 (See July 24, 2019 Press Release). Following the

delivery of the Stage I independent report to ICM, St-Georges has

accelerated the work and obtained results on many tasks that are part of

Stage II and Stage III of the planned development.

On-going testing has confirmed, so far, the portability of the process developed for sediments to hard rock sources of lithium.

The

Company is looking at opportunities to apply its technologies to other

advanced mining projects, in particular, ones that currently produce

spodumene concentrate, but have not yet decided to build an expensive

tech plant for refining. Potential adopters of the technology have been

identified, and discussions initiated. In addition, the Company is

looking at the potential to retrofit existing facilities. Management

will update the public on the status of these discussions when

materiality requires it.

St-Georges

filed the final documentation with the US Patent Office allowing its

patent application to move from its provisional status to the formal

patent application stage. The Company also filed a PCT application for

the same patent potentially giving it protection in an additional 152

countries. The final version of the patent application now allows for

the recovery of lithium from recycled batteries. St-Georges intends to

position itself as an ideal partner to provide strategic materials to

the battery industry, which includes recycling and recovery of the new

generation of batteries, including solid-state batteries. Additionally,

this patent application covers recycling as well as lithium metal and

alloys manufacturing.

Pilot Plant(s)

St-Georges’

management and the metallurgical team have worked on the design, the

sourcing of equipment, and the financial aspects of its proposed pilot

plant for the better part of the last six months. In an effort to lower

the risk of the proposal, the team has initiated discussions with

ready-built facilities with extra capacity. This could allow St-Georges

to build its pilot plant’s processing circuit faster with only minor

modifications to the ready-built facilities. Early estimates confirm

that capital expenditure should only be a fraction of the original

budgeted cost as the Company will be leasing the facilities long-term.

The Company expects to have secured an agreement for the pilot plant

facilities in Q2 2020.

Mineral Exploration

Julie Nickel Project

Following

last year’s fieldwork, the Company’s geological team and exploration

sub-contractors are planning additional drilling on the Julie Nickel

property. The exploration plan for the coming years will be presented to

the local stakeholders and First Nations in Q1, and the updated

permitting request should be filed by Q2 for work in early summer.

Additional bulk sampling should be performed to advance a nickel-iron

initiative by the Company’s metallurgical team.

Preliminary discussions are on-going with a ferronickel consortium planning a project in Quebec.

Manicouagan Palladium-Rhodium Project

Much

like the Julie Project, the Manicouagan Project has nickel and copper

that meets the conventional concentrates requirements based on the type

of sulphates it contains. Additionally, the recrystallized nature of

this region lends itself to higher recoveries of each crystal form and

better conversion.

The

presence of well-known high-grade Palladium-Rhodium-Ruthenium surface

showings (See January 27, 2020, Press Release), regardless of size,

allows St-Georges to significantly reduce its costs to acquire PGE

concentrate material for metallurgical bench testing of its processing

and refining metallurgical process for Palladium-Rhodium-Ruthenium.

St-Georges

exploration team is planning a pre-drilling surface campaign to obtain

permitting to intervene on-site in mid-summer. At the same time,

St-Georges’ management is having early-stage discussions with potential

farm-in or earn-in partners to advance the project at a faster pace.

Borealis EHF

The

hybrid decentralized and distributed ledger-driven derivative trading

platform is coming together at a good pace. Regulatory discussions are

now in control of the timeline for the delivery of the platform.

Islensk Vatnsorka Hf – Iceland Hydro-Electric Dam Project

Islensk

informed the Company that the permitting process is moving within the

expected timeline and according to expectations. The Company still

believes that the project will be fully permitted by the end of 2020.

Iceland Resources EHF/St-Georges Iceland ltd

On

August 21, 2019, the Icelandic authorities approved St-Georges’

previously disclosed work program for the coming year (See March 2, 2019

Press Release). The core projects have seen a fair share of exploration

work, while some secondary projects have been repeatedly delayed due to

extreme weather conditions in northern and eastern Iceland.

Work

on the Thor Gold Project has brought it to drill-ready status. Surface

rights and environmental conditions are no longer problematic, and the

Company has requested a legal opinion to confirm that it can drill on

the sole basis of its central government license.

The

Company did, however, take samples at Thor during the winter season

that are currently being analyzed. The Company is now preparing a bulk

sample program at Thor. The material will be sent to be processed in

Canada as soon as the weather allows it sometime in Q2.

The

Company is currently in discussions to acquire the balance of the

surface rights that escape its ownership on the project and is looking

to acquire the last portion equity own by a third party in the Thor Gold

Project.

Status of other holdings

The Company currently holds the following assets as of January 31, 2020.

Vilhjalmur Thor Vilhjalmsson, President and CEO of St-Georges, commented: “(…)

the last six months have been for the Company both challenging but

exciting. With the successful listing of ZeU Crypto Networks Inc., the

sale of KOTN, funding above market prices, and now faster-than-expected

progress in regards to the pilot plant, the team has shown its

capabilities to deliver.”

St-Georges

is developing new technologies to solve some of the most common

environmental problems in the mining industry. The Company controls

directly or indirectly, through rights of first refusal, all the active

mineral tenures in Iceland. It also explores for nickel-copper-cobalt

and Palladium-Palladium-Rhodium-Ruthenium on the Julie Nickel Project

& the Manicouagan Palladium-Rhodium Project on the Quebec’s North

Shore. Headquartered in Montreal, St-Georges’ stock is listed on the CSE

under the symbol SX, on the US OTC under the Symbol SXOOF and on the

Frankfurt Stock Exchange under the symbol 85G1.

The

Canadian Securities Exchange (CSE) has not reviewed and does not accept

responsibility for the adequacy or the accuracy of the contents of this

release.

Posted by AGORACOM-JC

at 12:45 PM on Monday, February 10th, 2020

SPONSOR: BetterU Education Corp.

aims to provide access to quality education from around the world. The

company plans to bridge the prevailing gap in the education and job

industry and enhance the lives of its prospective learners by developing

an integrated ecosystem. Click here for more information.

The Landscape Of Edtech: Mapping The Innovation Revamping Education In India

Over $1.8 Bn has been invested into Indian edtech startups from 2014 to 2019

The test prep segment has the highest capital inflow and the greatest demand in India

India’s tech economy growth has pushed the demand for skill development solutions

From classrooms to smart devices, the medium of education and learning in India has gone through a paradigm shift. With over 665 Mn

wireless internet subscribers (Q3 2019), India has seen a massive 14%

increase in the addressable base for internet services in just one year.

This rate of adoption has meant great things for startups and digital

products and services and has given rise to personalisation and

convenience when it comes to the school curriculum and off-classroom

learning.

The growing popularity of online learning has provided a major push

to two of the top subsectors in the edtech market— test preparation

(from K-12 to entrance exams) and online certification. To put this into

perspective, between 2014 to 2019, startups in test prep and online

certification startups earned a whopping 88% ($1.6 Bn) of the total

capital inflow in edtech.

The skewness in funding and investor interest for test prep and

online certification startups is in line with the prevalence of the

grades-first mentality in the Indian market as well as the need for

skilled tech labour. These products are highly in demand in the Indian

market because they mirror the traditional climb up the education ladder

— preparation for exams and getting the right certificate for

employment.

Posted by AGORACOM

at 3:00 PM on Friday, February 7th, 2020

SPONSOR: New Age Metals Inc. The company owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces Inferred. Learn More.

Summary

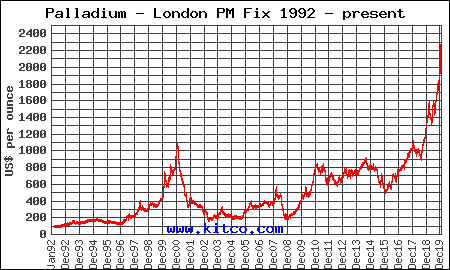

The palladium market will remain tight and pressure prices higher.

Sibanye Gold with the Stillwater Mine has plunged back into SA.

The Aberdene palladium ETF and Canadian palladium juniors are the best proxies.

Palladium has been the best performing commodity in the past two

years or so, jumping over 100% and there is more to go. This palladium

bull market is much different than the last one. The bull market from

1997 to 2000 was about 3 years and then palladium dropped giving up most

of the gains in less than a year. There was a nice bump up from the

2008 crisis and then the price traded sideways for several years. The

price bottomed at the end of 2015 with the severe bear market in

precious metals. Since then, the price has been going steadily higher

with a major break out in 2016. This bull market is not going to end

anytime soon for the reasons below.

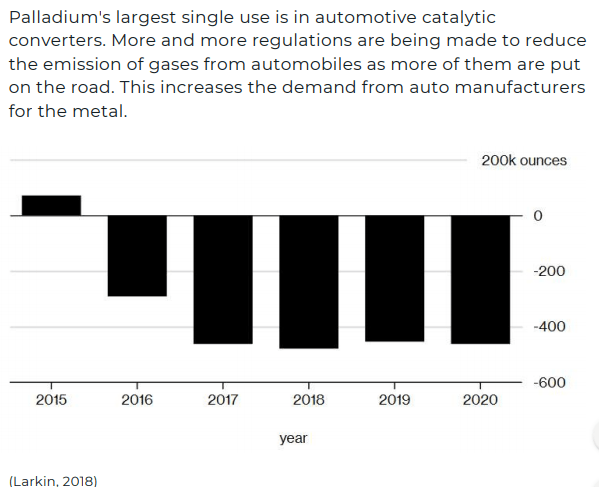

Palladium is mostly used in the auto industry for pollution control

with catalytic converters. Electric vehicles will be a long time coming

to replace any significant amount of gasoline/diesel driven vehicles.

Meanwhile, pollution standards are being tightened that will keep demand

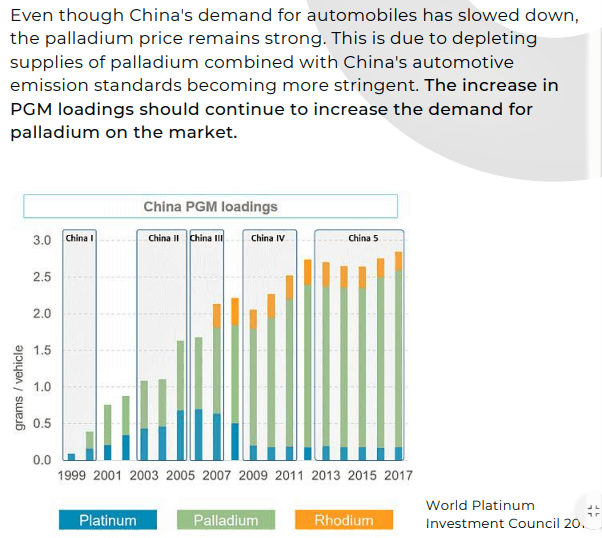

high. China has been gobbling up palladium since their China 5

pollution standards took effect in 2013. China 6 will now be coming into effect that will increase loads per vehicle of palladium. Many analysts have been commenting that China has been secretly stock piling the metal and is driving prices.

Palladium demand by Sector

There is no doubt the demand will remain strong, but the real

story is on the supply side. This next graphic illustrates the supply

deficit since 2016.

It is obvious to expect an increased demand from China as pollution regulations are tightened with ‘China 6’.

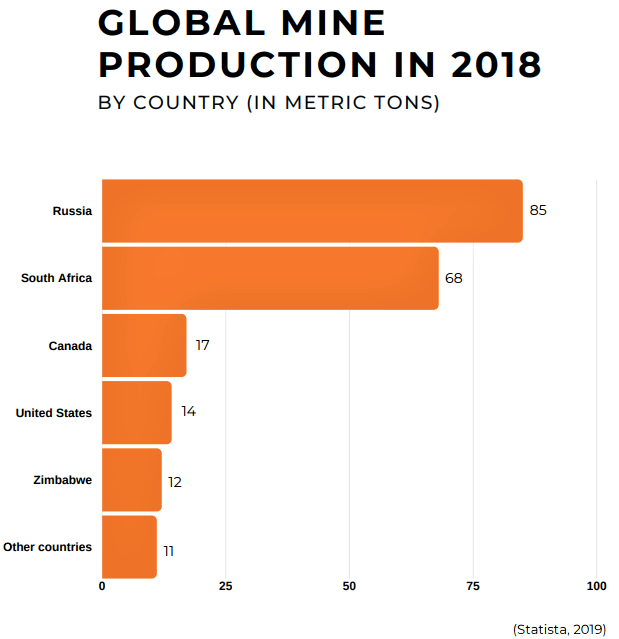

This next graphic of global mine production is very important because of the palladium supply is in a very unstable region.

The Russian supply from Norilsk Nickel has always been quite stable

and is of no concern, but as investors, we cannot participate there.

South Africa is the other big producer and that country is becoming very

unstable and more worrisome, that is where most of the future reserves

are.

The world’s largest PMG reserves are in South Africa, precisely in

the Bushveld Complex (in the central-Northern part of the country) which

alone accounts for about 50% of the world’s palladium resources, but,

overall, South Africa has reserves of 63 million kilograms which

represent over 91% of the worldwide availability.

South African (SA) mines have always been plagued with labour issues,

strikes, and high costs. To make matters worse, the country is now

facing an energy crisis with rolling blackouts shutting down mines. The country will probably become much more unstable, with unemployment hitting 10-year highs.

Half of their youth are unemployed and the company that provides 95% of

the electricity (when it can) is reporting record financial losses.

This is a country teetering on the brink of chaos that will likely be

very disruptive to PGM mine supply. I am avoiding palladium and platinum investments there.

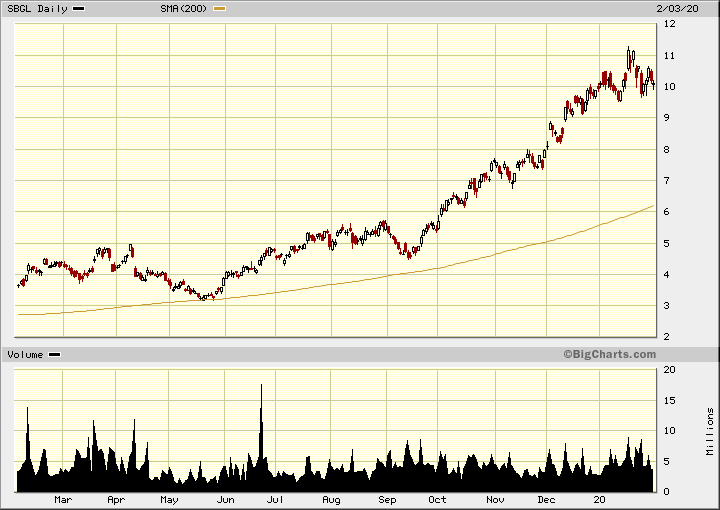

With all the issues in SA, Sibanye Gold (SBGL)

began diversifying out of the country and acquired the Stillwater PGM

mine in the US. That use to be my favourite stock to play palladium bull

markets. However, they jumped right back into the fray, acquiring

Lonmin in 2019, a struggling SA, PGM producer. They promptly cut 5,000

jobs at the mine and it now appears Sibanye is moving more into PGMs

from gold. According to what was released in the acquisition news,

Sibanye PGM production will increase from around 1.7M ounces per year

to 2.8M ounces/year. This compares to about 600,000 ounces/year at the

US Stillwater complex plus about 700,000 ounces produced through the

recycling unit, noted from the 2018 annual report.

SA PGM production was 627,991 ounces (this will increase significantly with Lonmin acquisition)

SA gold production was 344,752 ounces (this amount is well below normal because of mine strike)

US PGM production was 284,773 ounces

US PGM recycling was 421,450 ounces

The stock has done well with the rising palladium price, but at these

stock prices and the move back to SA, it has become too risky. I would

suggest selling at these prices.

To highlight risks further, the Q1 2019 financial report highlights a -63% decline in SA gold production in Q1 2019 compared to Q1 201 because of the labour strike. This news out on February 2nd

states that 19 attacks on SA gold facilities nearly doubled from last

year. On December 15, 2019, attackers took hostages and plundered the

smelting plant at Gold Fields Ltd.‘s South Deep mine. “Mining companies are being attacked by thugs and armed gangs and there is a lack of police response,” said Neal Froneman, CEO of Sibanye Gold Ltd., which repelled an attack on its Cooke mine two weeks ago. “It eventually has a knock-on impact into society, it’s lawlessness, it’s anarchy.”

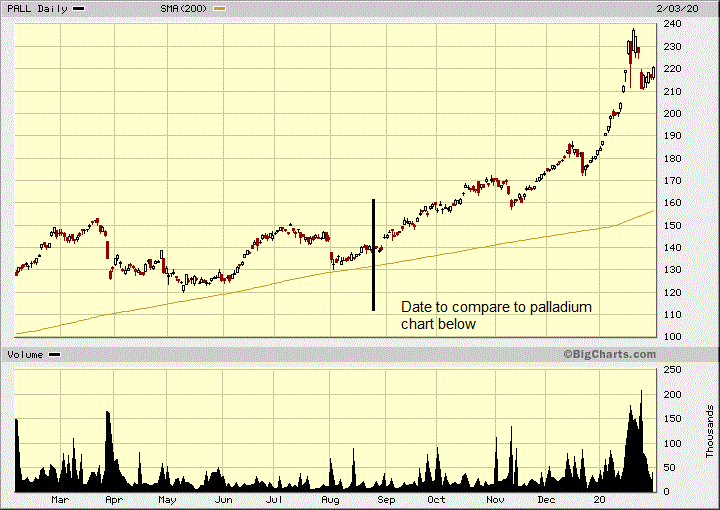

There is the Aberdeen Standard Physical Palladium ETF Trust (PALL).

The investment objective of the Trust is for the Shares to reflect the

performance of the price of palladium, less the expenses of the Trust’s

operations. The ETF Trust physically holds palladium in JPMorgan vaults

in London and Zurich. PALL tracks the movements in palladium spot prices

fairly well and is the best direct exposure to palladium. Aberdeen

purchased the fund effective October 1, 2018, from ETF Securities. The

Aberdeen website is terrible, it just diverts you to something else they

are trying to sell. You can find some more info at etf.com.

One disadvantage, as a Trust it will often trade at a discount to NAV, so short term may not always reflect palladium movements precisely.

The chart of PALL reveals quite a jump in volume on the last rally. I

do not find this alarming, but shows it is really the first time the

palladium market has caught retail interest.

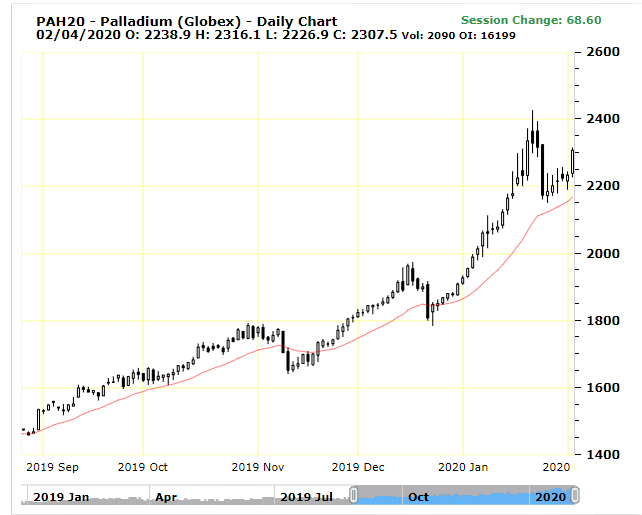

If we compare to the short-term chart on palladium below, it is easy

to see that PALL has tracked the palladium price very well. After a

needed correction, the price jumped higher on Monday. This is probably a

start to the next rally.

There is also Sprott Physical Platinum and Palladium Trust (SPPP), but it is split 50/50 between the two metals.

Canada is the third-largest producing country, so an obvious place to

look. A lot of the palladium production comes from major miners in the

Sudbury nickel/copper complex as a byproduct. Obviously, this is a good

area to look and there was an excellent proxy for investors called North

American Palladium that was operating the Lac Des Isles palladium mine.

Unfortunately, for us, investors, it was bought out last year by SA producer Implats.

The area had a number of discoveries back in the last bull market

around the year 2000, and I visited a number of those projects back

then. I believe the best one in this area is Canadian Palladium that acquired the East Bull project last year. There is also Palladium One that is not Canada but not in SA either.

Palladium One Mining (OTC:NKORF) – PGM project is in Finland.

Shares outstanding 111 million, 185 million fully diluted

Their LK project is located in north-central Finland, approximately

40 km north of the company’s exploration office in the town of

Taivalkoski. The property is 160 km (by road) east-southeast of

Rovaniemi and 190 km northeast of the port city of Oulu. Finland is a

very stable jurisdiction and has a viable mining sector.

The company is run by CEO/President, Derrick Weyrauch, CPA, CA who is

an experienced mining executive and corporate director. Mr. Weyrauch’s

background includes finance, risk management, corporate restructuring

and turnarounds, coupled with M&A strategy development, execution

and post transaction integration. He is the co-founder of Magna Mining

Corp. and is a former corporate director of a number of companies

including Eco Oro Minerals Corp., Jaguar Mining Inc., and Banro Corp.

and is a former CFO of Jaguar Mining Inc. and Andina Minerals Inc.

Currently, he is a non-executive director and at Cabral Gold Inc.

The LK Project is 100% owned by Palladium One Mining Inc.

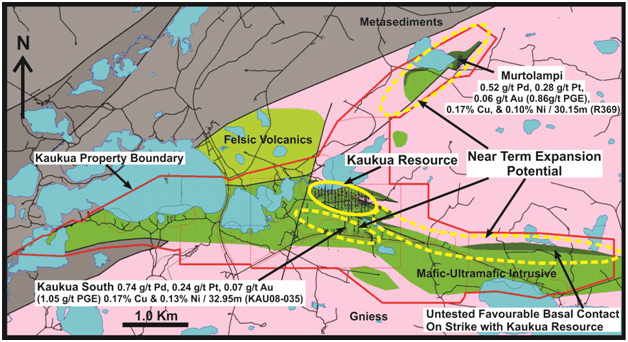

Palladium One released a mineral resource estimate for the Kaukua deposit within the 100-per-cent-owned Lantinen Koillismaa (LK) project.

Highlights:

An optimized pit-constrained mineral resource, at a 0.3-g/t palladium cut-off;

635,600 PdEq (palladium equivalent) ounces of indicated resources grading 1.80 g/t PdEq contained in 11 million tonnes;

525,800 PdEq ounces of inferred resources grading 1.50 g/t PdEq contained in 11 million tonnes.

Significant potential exists to expand the historic Haukiaho

deposit along strike both to the east and west. For example, 1960s-era

historic drilling by Outokumpu about two km east of the historic 2013

Haukiaho inferred resource returned up to 36.36 m grading 0.20 per cent

Cu and 0.19 per cent Ni from 1.64 m to 38.00 m downhole in hole R692 (no

PGE analysis was conducted). Reconnaissance prospecting by Palladium

One in the vicinity of this historic drill hole returned up to 0.51 per

cent Cu, 0.33 per cent Ni, 0.19 g/t Pt, 0.56 g/t Pd and 0.21 g/t Au

(0.96 g/t PGE) (see press release dated Aug. 12, 2019). Palladium one

recently applied for the Haukiaho East reservation (see press release

date Sept. 5, 2019), which, if approved, the company would control about

24 km of the favourable Haukiaho basal contact.”

The company plans to conduct

a 75-line-kilometre induced polarization (IP) geophysical program,

along with a diamond drilling program of up to 5,000 metres, at the LK

project. Both drilling and geophysics contractor are expected to be

mandated soon.

The Tyko Ni-Cu-PGE project, i65km northeast of Marathon Ontario, Canada.

The Tyko project is an early stage, high sulphide tenor, nickel

focused project with recent drill hole intercepts returning up to 1.06 Ni over 6.22 m including 4.71% Ni over 0.87m in hole TK-16-010 (see press release dated June 8, 2016). On January 21, 2019, Palladium One reported prospecting samples with assay results of up to 0.74% Ni, 4.09% Cu, and 2.51g/t PGE

on the Tyko Nickel-Copper-PGE Property. This project has some

palladium, but if it is developed to a resource, it will be more like

the Sudbury copper and nickel mines with PGMs as a byproduct.

The company is well financed, closing a C$3,786,180 private placement

at C$0.06 per unit issuing 63,102,999 units. Eric Sprott took down

20,000,000 units. While funding is required, this is quite a bit of

dilution.

Currently, the stock is priced around $0.18 so all the warrants and

options are well in the money. So is appropriate to use the fully

diluted shares outstanding for valuation.

Market cap – $20 million. Market cap fully diluted Cdn $33.3 million

Subtracting $3.8 million financing from the market cap, it values

their 635,600 PdEq indicated resource at C$25 per ounce and fully

diluted at C$46 per ounce. This is a quite low valuation.

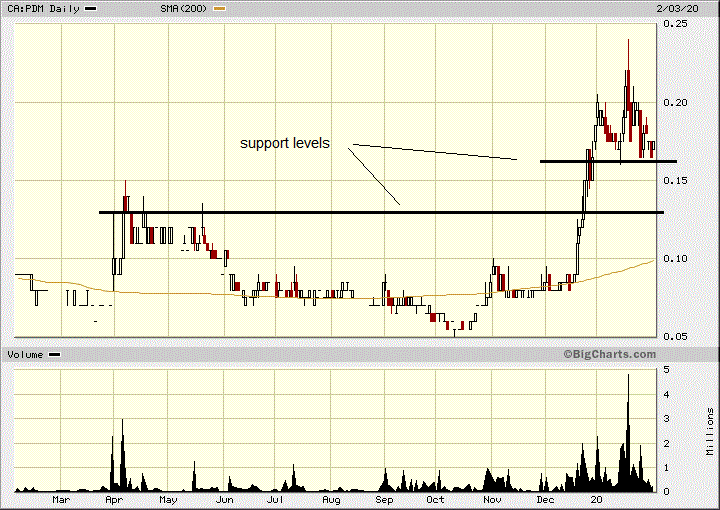

The stock mostly trades on the TSXV symbol (PDM), so I used the C$

chart. Support is around 16 cents and 12.5 cents. If 16 cents holds, the

stock could begin a leg higher.

Canadian Palladium

Shares outstanding 100.3 million approx.

All warrants and options are at 30 cents and higher.

What I consider one of the most important highlights is the company

is run by Wayne Tisdale. In the last 10 years, he has advanced three

juniors and sold them for large profits for their shareholders. He

helped start and finance the Rainy River project which was sold to NewGold in 2013 for $310 million. He developed US Cobalt and, in 2018, sold it to First Cobalt in a transaction worth $150 million to his shareholders’ delight. Going back further, he helped finance oil & gas company Ryland Oil that was bought out by Crescent Point in 2010 for a $121.8 million

valuation. Mr. Tisdale has a keen eye to find projects that can quickly

be advanced further to make them prime acquisition targets. Canadian

Palladium only has a market value now of about C$20 million, and I have

little doubt that Mr. Tisdale is going to do it again with Canadian Palladium.

Highlights:

Company run by Wayne Tisdale

Low market valuation – C$31 per ounce

East Bull with 43-101, 523,000 inferred palladium equivalent resource

East Bull can open to depth and along strike

Widely spaced drilling only needs infill drilling to upgrade and expand resource

Close to Sudbury complex where ore can be processed

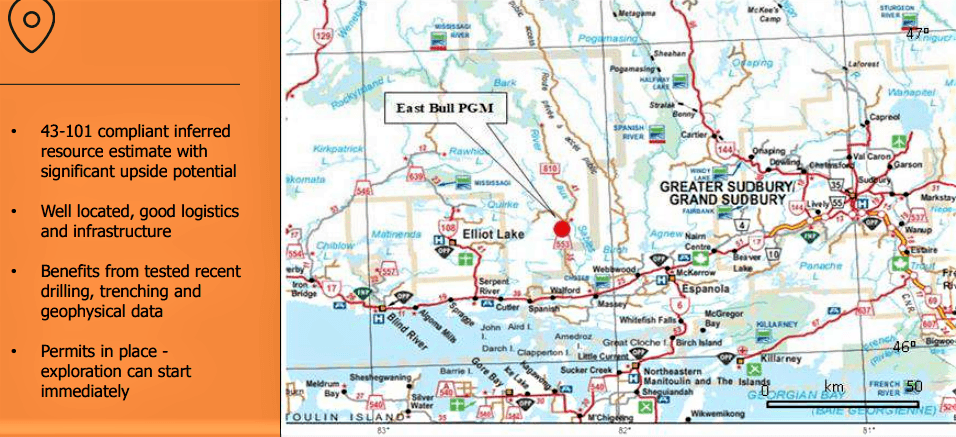

Projects – East Bull, Ontario Canada

East Bull was drilled by Freewest and Mustang Minerals back in the

2000 era and now has a 43-101, 523,000 ounces inferred palladium

equivalent resource. A private company, Pavey Ark Minerals had the

property and in 2017 they twinned old drill holes and completed the work

to bring the project to 43-101 standards. Canadian Palladium (formerly

21C Metals) acquired a 100% option on the project last February.

This graphic from their presentation is a good summary and shows the location

In the 1999, 2000 period, Freewest drilled 27 holes for a total of

2,902 meters and carried out extensive surface trenching. Work by

Mustang on the eastern part of the Property (claim 1227910) included 11

drill holes for a total of 1,766 meters. The work by Freewest and

Mustang forms the majority of the data for the current resource

estimate. Additionally, Pavey Ark reviewed and re-sampled drill core

from the 27 BQ and NQ holes from the Freewest drilling program. Pavey

Ark’s exploration results in 2017 included;

hole EB17-01 that intersected 12.0 m at 2.87 g/t PGM+Au, 0.23% Cu and 0.13% Ni and

hole EB17-03 that intersected 7.0 m of 3.21 g/t PGM+Au, 0.16% Cu and 0.07% Ni.

(Note: Au = gold, Cu = copper, and Ni = nickel.)

In 2019, BULL completed their initial exploration program at East Bull and reported results Sept. 17, 2019.

These are highlights from the first sampling program on the East Bull

palladium project and field program on the Agnew Lake project:

Seventy-three grab samples were selected to help identify the

palladium-bearing rock types of the mineralized trend. Grab samples are

used to determine the presence mineralization and may not be indicative

of the overall grade of the zone

Sampling successfully defined locations for channel sampling and the

higher grades could indicate potential zones within the mineralized

zone for higher-grade starter pits

Range of palladium assay sample results were 37 samples below 0.1

g/t palladium, 17 between 0.1 and 0.5 g/t with 14 above 1 g/t. Nine of

these ran between 2 and 6.5 g/t

Geological mapping and review of the Freewest diamond drilling in

2000, indicates the northeast-trending faults are composed of multiple

intrusions of mafic to diabase dikes. Left lateral movement on the dikes

is measured to be up to 100 metres

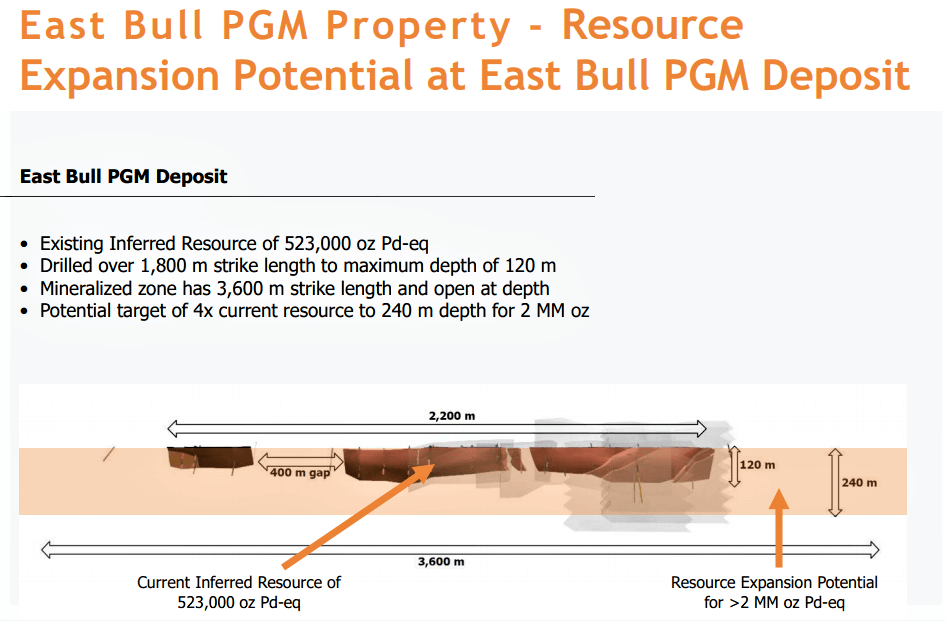

This graphic gives a good snapshot of the current resource and

expansion potential. Mineralization starts at surface and the system

appears to be about 30 meters wide. This would be an open-pit operation.

Agnew Lake property

It is located 80 kms. west of Sudbury, Ont., home of Glencore and

Vale’s Canadian nickel-copper-platinum-group-elements mining and

smelting operations. The Agnew Lake property comprises over 260 claims

(about 6,000 hectares) and is part of the larger East Bull Lake-Agnew

Lake mafic-ultramafic complex.

The Agnew Lake magmas have major element compositions that are very

similar to the model parent liquids proposed for the mafic portions of

the Stillwater and Bushveld complexes. The Agnew intrusion and the East

Bull Lake intrusion are also considered to host significant PGE-Cu-Ni

mineralization in marginal rock units (Peck & James, 1990; Peck et

al., 1993a, 1993b, 1995; Vogel et al., 1997).

Financial/Summary

Last financial statements show just over $400,000 cash. The company

just closed a $4 million financing at 12 cents per share. Eric Sprott

bought 12.5 million shares of that financing.

Wayne Tisdale has been successful in financing and increasing the

value of properties and dealing them off for large profits. I believe he

will do it again and also has a loyal following of shareholders from

his past success. BULL just acquired the property last year and there

has been little exploration and no drilling so it has been under the

radar until the recent financing. The discovery is on the surface, so

will be cheap to mine and is close to the Sudbury complex where refiners

can recover PGMs. There is a couple other palladium exploration plays

in Canada, but they are mostly old stale stories and I believe none have

the short-term potential that the East Bull project has.

The current market cap is $20.1 Million less the $4 million financing

gives an enterprise value of C$31 per ounce on their 523,000-ounce

Pd-eq inferred resource. Part of the reason for the low value is the

resource is only inferred. If drilling success starts to prove larger

potential and the resource moves up to the measured and indicated

category it could easily increase the value potential.

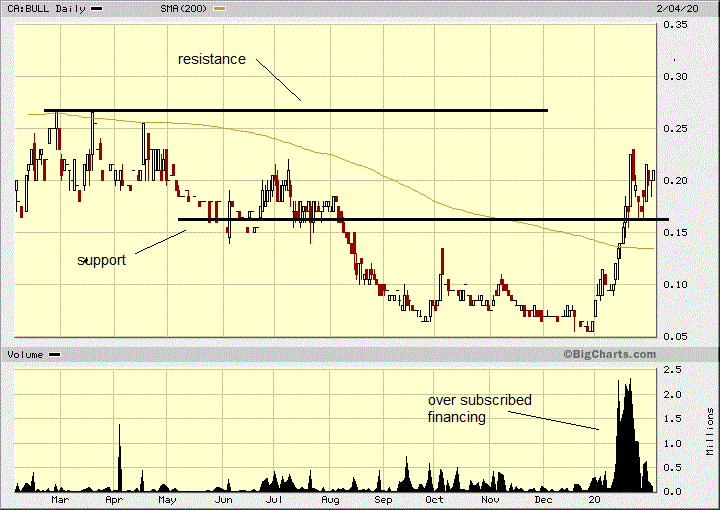

Only exploration news last year was sample results that came out last

September just when the junior market started heading south. The stock

made a decent move higher than just drifted lower until a typical

year-end bottom. The stock took off when it hit 12 cents on good volume.

This is when they began marketing a financing that was way

oversubscribed in one day. Probably spill over buying drove the stock up

to the 23-cent level. The stock then came back to support around 16

cents and bounced off higher. Drill news will likely cause the next move

higher with the old highs around 27 cents last year as the first major

resistance.

Conclusion

A recent update on palladium by TD Securities

highlights tightening emission controls and South Africa as I have, but

most interesting is the lack of speculative trading positions. TD

comments positions held by traders are below average. This rally has

room to move and if excessive speculation builds it could go way higher.

Regardless of whether palladium is $1,200 or $2,400 per ounce,

palladium discoveries and deposits will be worth premium valuations,

especially in stable jurisdictions. The potential for discoveries in

South Africa is very good but the political risks are rising. Ivanhoe

Mines (OTCQX:IVPAF), Eastplats, and Platinum Group Metals (PLG)

have projects in SA, and if I had to pick one there, it would be

Platinum Group Metals because they have the most leverage to platinum

and palladium prices.

The best direct related investment to palladium is the PALL ETF, but

it does not offer any leverage. There are not any 2 times or 3 times

palladium ETFs. This leaves the best leverage to junior palladium

companies and there are few. I prefer those outside of SA like Canadian

Palladium and Palladium One. I prefer Canadian Palladium because of the

CEO’s track record, their resource is on surface, near PGM smelters and

likely cheaper exploration costs in Canada vs Finland. For

diversification, owning more than one palladium play is not a bad idea.

Disclosure: I am/we are long DCNNF. I wrote

this article myself, and it expresses my own opinions. I am not

receiving compensation for it (other than from Seeking Alpha). I have no

business relationship with any company whose stock is mentioned in this

article.

Additional disclosure: Canadian Palladium is a paid advertiser at affiliate playstocks.net