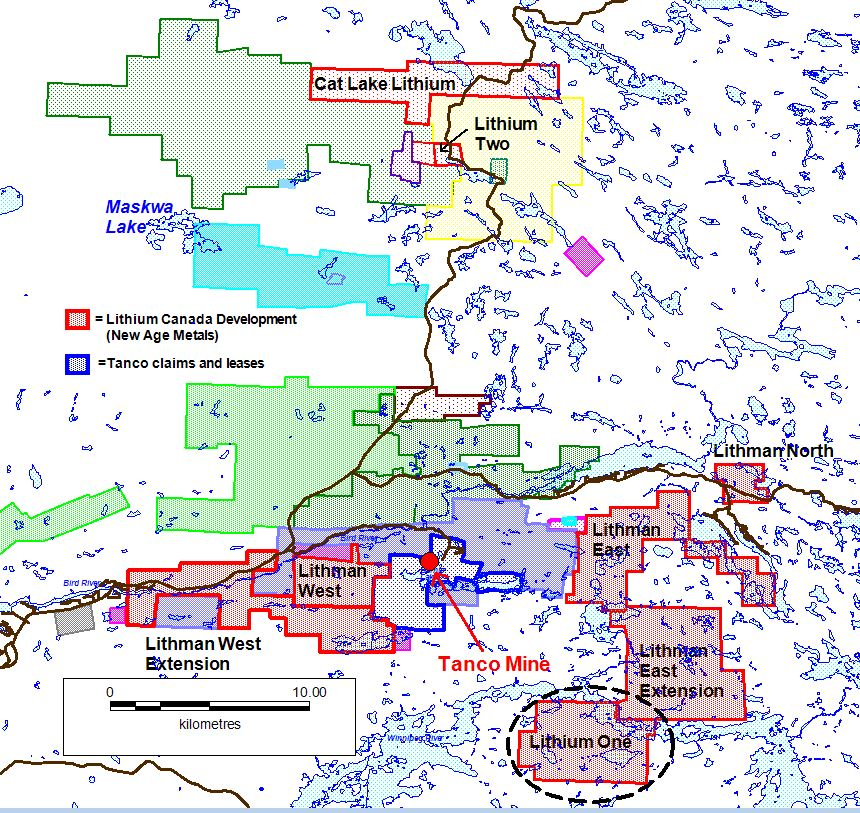

- – The NAM/AAZ Option/Joint Venture has eight pegmatite hosted Lithium Projects in the Winnipeg River Pegmatite Field, located in SE Manitoba- The mineral claims are 100% owned by NAM’s Lithium Division, Lithium Canada Development- The eight projects are strategically situated within the Winnipeg River Pegmatite Field, which hosts the world class Tanco Pegmatite that has been mined for Tantalum, Cesium and Spodumene (one of the primary Lithium bearing minerals) in varying capacities, since 1969.

– 2018 surface exploration has been completed on the Lithium Two, and Lithman East Projects and is underway on Lithium One.

– Drill permits have been applied for on the Lithium Two and Lithium One Projects and the company is awaiting approval from the Manitoba government.

– NAMs flagship project is the 100% owned River Valley Project, North America’s largest undeveloped primary Platinum Group Metals (PGM) Project in Sudbury, Ontario. See the most recent press releases and our Chairman’s message for the River Valley Project PEA dated July 25, 2018 and August 1, 2018 at our website (www.newagemetals.com) .

September, 27th 2018 / Rockport, Canada – New Age Metals Inc. (NAM) (TSX.V: NAM; OTCQB: NMTLF; FSE: P7J.F) New Age Metals is pleased to provide an update on the present exploration program with regards to the company’s Manitoba Lithium Projects. Currently surface exploration is focusing on the Lithium One Project (see Figure 1). The company’s Lithium Division, Lithium Canada Developments, has an aggressive exploration and development plan for 2018/2019. NAM’s Manitoba projects are financed via an Option/Joint Venture agreement with Azincourt Energy (AAZ) (see News Release Jan 18th, 2018).

Lithium One Exploration Update

Reconnaissance field exploration by the company in 2016 returned assays from surface exposed pegmatites up to 4.33% Li2O (see News Release – Dec 8th, 2016) from the Silverleaf Pegmatite. There are several clusters of pegmatites that are being explored during the 2018 field exploration season.

Click Image To View Full Size

Figure 1: NAM/AAZ Joint Venture Project Location Map – Winnipeg River Pegmatite Field. Lithium One Project is highlighted.

The Annie Pegmatite area (see Figure 2) is generally underlain by a broad continuous multiphase unit of pegmatitic granite. Detailed mapping has revealed at least 2 distinct structurally orientations of evolved pegmatite units that may be strataform or oblique along fault structures that offset established stratigraphy. Lithium bearing mineralogy has been discovered in these strataform and oblique evolved pegmatitic structures. Pending assay analysis for Lithium and other mineralogical content at observed sites within the Annie Pegmatite, an exploration targeting recommendation will be prepared. These targeting recommendations will hopefully help define potential structural connection implications between the Annie and Silverleaf showings, should they exist.

Click Image To View Full Size

Figure 2: Annie Pegmatite showing in outcrop with abundant SQUI (Spodumene Quartz Intergrowths) mineralization – The pen in the photo is 8 cm in length.

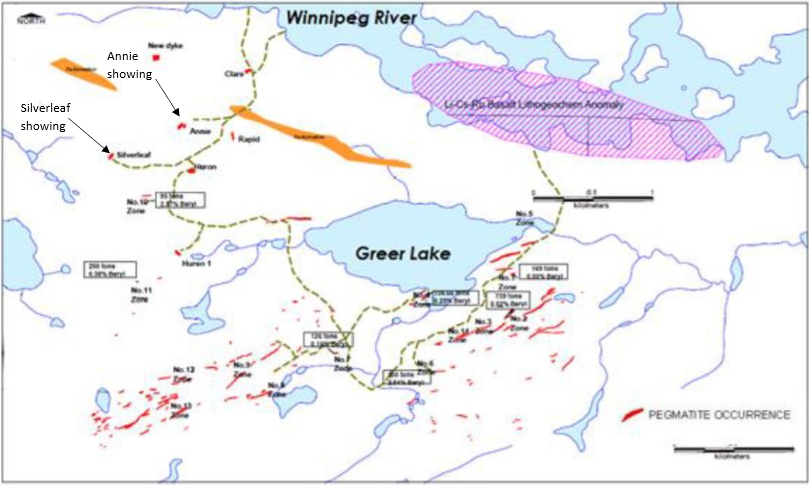

Sampling and mapping are ongoing. Several batches of samples have been sent to the lab for analysis. Numerous pegmatites are being explored on the Lithium One Project (see Figure 3).

Click Image To View Full Size

Figure 3: Pegmatite Location Map. Lithium One Project – Manitoba. The circle in the top left of the map is around the two pegmatite showings – Silverleaf and Annie on the Lithium One Project.

The Silverleaf Pegmatite (see Figure 4) is one of the most spectacular and mineralogically complex pegmatites known on the property. Figure 4 is a photo of the spectacular spodumene-lepidolite mineralization seen on surface. Numerous other interesting pegmatites have been mapped with the focus being to understand and increase the potential of the project.

Click Image To View Full Size

Figure 4: White spodumene blades in a matrix of lepidolite (Lithium Mica) from the Silverleaf showing.

Joint Venture Agreement

In January of 2018, NAM announced a signed final agreement with Azincourt Energy Corp. (TSX.V: AAZ) for the Manitoba Lithium Projects, (News Release: January 15, 2018). This Pegmatite Field hosts the world class Tanco Pegmatite that has been mined for Tantalum, Cesium and Spodumene (one of the primary Lithium ore minerals) in varying capacities, since 1969. NAM’s Lithium Projects are strategically situated in this prolific Pegmatite Field. Presently, NAM, under its subsidiary Lithium Canada Developments, is one of the largest mineral claim holders in the Winnipeg River Pegmatite Field for Lithium. Azincourt Energy Corp. as our option/joint venture is financed for and has committed to a minimum of $600,000 to be expended on exploration in Manitoba for 2018.

OPT-IN LIST

If you have not done so already, we encourage you to sign up on our website (www.newagemetals.com) to receive our updated news.

ABOUT NAM’S PGM DIVISION

NAM’s flagship project is its 100% owned River Valley PGM Project (NAM Website – River Valley Project) in the Sudbury Mining District of Northern Ontario (100 km east of Sudbury, Ontario). See results from the most recent NI 43-101 resource update below in Table 1. NAM management and consultants are currently designing a complete drill program to be executed in 2019 for the River Valley Project. This plan will consider previously proposed drill parameters and will be based on the most recent geophysical assessment and consultant expertise. The projects first economic study, a Preliminary Economic Assessment (PEA) is underway and is being overseen by Mr. Michael Neumann, P.Eng., a veteran mining engineer and one of NAM’s directors. See the most recent press releases for the River Valley Project PEA which detail the appointment of P&E Mining Consultants and DRA Americas to jointly conduct the study, dated July 25, 2018 and August 1, 2018 respectively. Our new Fall Chairman’s message can be accessed at our website (www.newagemetals.com) .

On April 4th, 2018, NAM signed an agreement with one of Alaska’s top geological consulting companies. The companies stated objective is to acquire additional PGM and Rare Metal projects in Alaska. On April 18th, 2018, NAM announced the right to purchase 100% of the Genesis PGM Project, NAM’s first Alaskan PGM acquisition related to the April 4th agreement. The Genesis PGM Project is a road accessible, under explored, highly prospective, multi-prospect drill ready Palladium (Pd)- Platinum (Pt)- Nickel (Ni)- Copper (Cu) property. A comprehensive report on previous exploration and future phases of work was completed by Avalon Development of Fairbanks Alaska in August 2018 on Genesis. A full sampling program will be conducted to continue to outline additional mineralization along the 800-meter by 40-meter mineralized zone

On August 29, the Avalon report was submitted to NAM, management is actively seeking an option/joint-venture partner for this road accessible PGM and Multiple Element Project using the Prospector Generator business model.

The results of the updated Mineral Resource Estimate for NAM’s flagship River Valley PGM Project are tabulated in Table 1 below (0.4 g/t PdEq cut-off).

| Class | Tonnes

‘,000 |

Pd (g/t) | Pt (g/t) | Rh (g/t) | Au (g/t) | Cu (%) | Ni (%) | Co (%) | PdEq (g/t) |

| Measured | 62,877.5 | 0.49 | 0.19 | 0.02 | 0.03 | 0.05 | 0.01 | 0.002 | 0.99 |

| Indicated | 97,855.2 | 0.40 | 0.16 | 0.02 | 0.03 | 0.05 | 0.01 | 0.002 | 0.83 |

| Meas +Ind | 160,732.7 | 0.44 | 0.17 | 0.02 | 0.03 | 0.05 | 0.01 | 0.002 | 0.90 |

| Inferred | 127,662.0 | 0.27 | 0.12 | 0.01 | 0.02 | 0.05 | 0.02 | 0.002 | 0.66 |

| Class | PGM + Au (oz) | PdEq (oz) | PtEq (oz) | AuEq (oz) |

| Measured | 1,440,200 | 1,999,600 | 1,999,600 | 1,136,900 |

| Indicated | 1,856,900 | 2,626,700 | 2,626,700 | 1,463,800 |

| Meas +Ind | 3,297,200 | 4,626,300 | 4,626,300 | 2,600,700 |

| Inferred | 1,578,400 | 2,713,900 | 2,713,900 | 1,323,800 |

Notes:

- A.CIM definition standards were followed for the resource estimation.

- B.The 2018 Mineral Resource models used Ordinary Kriging grade estimation within a three-dimensional block model with mineralized zones defined by wireframed solids.

- C.A base cut-off grade of 0.4 g/t PdEq was used for reporting Mineral Resources.

- D.Palladium Equivalent (PdEq) calculated using (US$): $1,000/oz Pd, $1,000/oz Pt, $1,350/oz Au, $1750/oz Rh, $3.20/lb Cu, $5.50/lb Ni, $36/lb Co.

- E.Numbers may not add exactly due to rounding.

- F.Mineral Resources that are not Mineral Reserves do not have economic viability.

- G. The Inferred Mineral Resource in this estimate has a lower level of confidence that that applied to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of the Inferred Mineral Resource could be upgraded to an Indicated Mineral Resource with continued exploration.

QUALIFIED PERSON

The contents contained herein that relate to Exploration Results or Mineral Resources is based on information compiled, reviewed or prepared by Carey Galeschuk, a consulting geoscientist for New Age Metals. Mr. Galeschuk is the Qualified Person as defined by National Instrument 43-101 and has reviewed and approved the technical content of this news release with regard to technical aspects of the Lithium Division.

On behalf of the Board of Directors

“Harry Barr”

Harry G. Barr

Chairman and CEO

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Cautionary Note Regarding Forward Looking Statements: This release contains forward-looking statements that involve risks and uncertainties. These statements may differ materially from actual future events or results and are based on current expectations or beliefs. For this purpose, statements of historical fact may be deemed to be forward-looking statements. In addition, forward-looking statements include statements in which the Company uses words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”, “confident”, “intend”, “strategy”, “plan”, “will”, “estimate”, “project”, “goal”, “target”, “prospects”, “optimistic” or similar expressions. These statements by their nature involve risks and uncertainties, and actual results may differ materially depending on a variety of important factors, including, among others, the Company’s ability and continuation of efforts to timely and completely make available adequate current public information, additional or different regulatory and legal requirements and restrictions that may be imposed, and other factors as may be discussed in the documents filed by the Company on SEDAR (www.sedar.com), including the most recent reports that identify important risk factors that could cause actual results to differ from those contained in the forward-looking statements. The Company does not undertake any obligation to review or confirm analysts’ expectations or estimates or to release publicly any revisions to any forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. Investors should not place undue reliance on forward-looking statements.