Posted by AGORACOM-JC

at 2:23 PM on Monday, April 15th, 2019

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is

equipped with a 623m deep shaft and has never been mined.

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits.

Plans for Kenbridge include updating PEA,

advancing the project through to feasibility and exploring the open

mineralization at depth

FULL DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM-JC

at 9:45 PM on Sunday, April 14th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

Healthy growth in nickel demand from the stainless steel and battery sectors and shrinking inventories on the Shanghai Futures Exchange and London Metal Exchange bode well for nickel prices

Nickel inventories at both LME and SHFE warehouses have been on a downward trajectory since 2018

Stainless steel demand still dominates, but EV sector grows faster

By: Violet Li

Healthy growth in nickel demand from the stainless steel and

battery sectors and shrinking inventories on the Shanghai Futures

Exchange and London Metal Exchange bode well for nickel prices,

Macquarie Capital senior commodities consultant Jim Lennon said.

“Our view is that we have these two drivers in demand: stainless steel

and batteries, and nickel inventories have been falling over the last

few years. I think it will [continue to] fall over the next few years;

the nickel market will remain in a deficit between supply and demand,

which should push prices higher,†Lennon said at Fastmarkets Battery

Materials Conference in Shanghai on Thursday April 11.

Lennon did not give a breakdown of the forecast price at the presentation.

Nickel inventories at both LME and SHFE warehouses have been on a

downward trajectory since 2018. LME nickel stocks totaled 182,446 tonnes

as of April 1, down by 50% from 368,430 tonnes on January 1, 2018.

Meanwhile, nickel stocks in SHFE-approved warehouses fell by 80% during

the same period, to 9,749 tonnes on April 4 from 48,920 tonnes on

January 1, 2018.

Lennon concluded the large decline in stock levels reflects deficits and some financial buying of stocks.

“Last year there’s probably about 50,000 tonnes of inventories

transferred from the LME warehouses in Asia into non-reported

inventories in Europe, held by banks and traders, partly for reasons of a

positive outlook for the market or better premiums in the European

area,†Lennon said.

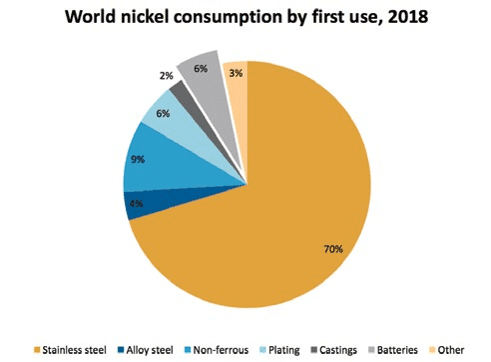

Stainless steel demand still dominates, but EV sector grows faster Stainless

steel takes up 70% of global nickel usage compared with a small

fraction of 6% of nickel used by the electric vehicle (EV) sector,

Lennon said. But EV demand growth is speeding up, he said.

“Total world production of stainless steel in 2016 grew by 8.5%, 2017 by

6% and last year by 5%. This year, our projection is 3.5-4%, so we do

see some slowdown but still a steady growth rate. Nickel usage in

batteries will grow by 30-40% [in 2019], so the underlying growth in

nickel [consumption] continues to be quite impressive,†Lennon said.

Notably, more nickel briquette was used in the EV sector following

rising demand for batteries and this has raised the nickel briquette

premium over the past year.

Fastmarkets MB’s monthly duty-free

nickel briquette premium cif Shanghai stood at $240-270 per tonne at the

end of March, up from $220-260 per tonne at the launch of the

assessment in August last year.

Nickel briquette is the one of

the main raw materials of nickel sulfate, a key material used in the

production of nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminium

(NCA) batteries used in EVs.

Posted by AGORACOM-JC

at 2:47 PM on Wednesday, April 10th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

The production of EVs is still small-scale, and last year they accounted for only 2.5% of global vehicle sales, however the 60% growth YoY was significant.

Even with consensus trend of a growth rate of 25-30% in sales a year, the share of EVs will grow steadily. April 9, 2019

By Jim Lennon, Managing Director, Red Door Research Ltd

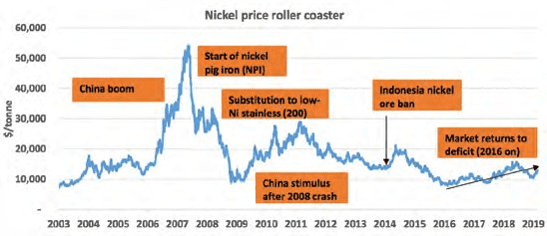

Historically, nickel has been a boom/ bust metal. Over the past 20 years, we’ve seen one of the most incredible booms in this metal followed by a prolonged bust. However, we think this metal is now on the cusp of another boom, due to the likely switch from internal combustion engines to electric vehicles (powered by high-nickel lithium-ion batteries) in the coming decades.

Since the price boom of 2006/07, it has been a rough time for nickel.

As one of the main beneficiaries of the take-off in Chinese demand in

the 2000s, nickel quickly came became a victim of its own success. After

peaking at an all-time high of over $50,000/t in May 2007, prices fell

to below $10,000/t by late-2008. High prices led to Chinese substitution

away from the standard 300-series stainless steel, which contains 8%

nickel, to 200-series stainless steel, containing only 1-2% nickel.

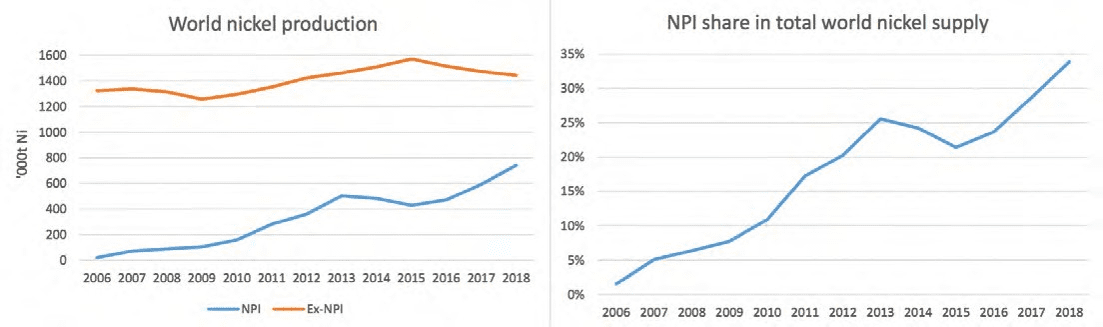

On the supply side, high nickel prices led to the development of a

new source of nickel in the form of nickel pig iron. Nickel pig iron is a

cheap alternative to pure nickel, used in the production of stainless

steel. It’s made in an energy-intensive way, using blast and electric

furnaces, and low-grade laterite nickel ores, mainly from the

Philippines and Indonesia. Nickel pig iron now accounts for 35% of

global nickel supply, compared to near- zero in 2006.

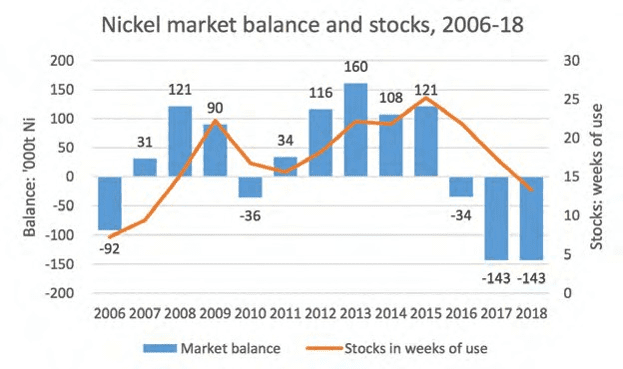

The low-point for nickel prices came in February 2016, when prices

dipped below $8,000/t, resulting in over 80% of the global industry

losing cash. Combined market inventories reached almost six months of

consumption by the end of 2015, one of the highest levels ever seen in

this market.

The combination of large closures of supply (over 200,000t) and a

steady recovery in global demand has led to a remarkable recovery in the

market over the past three years, with prices at one stage doubling

from their lows.

The recovery in the past year or so has been hesitant given the

still-high level of inventories hanging over the market, and

uncertainties in Indonesian and Filipino government policy.

Despite a large deficit between supply and demand last year, prices

were also hit by global macroeconomic concerns, including fears of a

Chinese slowdown and the negative impact on global growth from a

US-China and US-everyone else trade war.

So far, so good. Nickel prices have recovered to levels that are

acceptable to most producers, but they still remain well below levels

needed to incentivise investment in the next generation of supply.

Nickel supply has become reliant on growth in nickel pig iron to meet

incremental demand growth, and production by non-nickel pig iron

producers in aggregate has been declining in recent years due to massive

under investment in sustaining capital (see chart above).

This would be acceptable if the growth in nickel demand would

continue to come mainly from stainless steel, but there is a new kid on

the block: batteries. The use of nickel in batteries threatens a major

transformation of nickel supply and demand over the next decade.

Last year, primary nickel use in batteries was just below 6% of total

nickel demand compared with 70% for stainless steel. So far, the impact

of nickel use in batteries on nickel pricing has been small, but that’s

about to change – and probably sooner than many think.

Driven by governmental policy and environmental concerns, the

switchover of the existing car fleet from internal combustion engines to

hybrid, and ultimately fully electric vehicles (EVs), is now under way.

The production of EVs is still small-scale, and last year they

accounted for only 2.5% of global vehicle sales, however the 60% growth

YoY was significant. Even with consensus trend of a growth rate of

25-30% in sales a year, the share of EVs will grow steadily.

The predominant battery technology, at least for the next decade, is

lithium-ion batteries. The big kicker for nickel over the other raw

materials in the batteries (cobalt, manganese, lithium and graphite) is

that, in order to increase the energy density of the batteries (raising

the range between charges) and to reduce cobalt usage (perceived to be

overly dependent on the Congo for supplies), the amount of nickel used

per battery could easily more than double over the next 5-7 years.

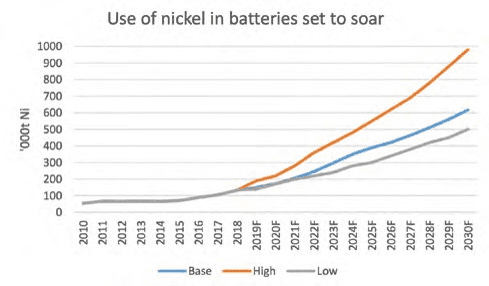

There is massive forecast uncertainty regarding the growth in

electric vehicles and the take-up of different battery technologies (see

chart below). This is always the case with breakthrough technologies,

and history shows that forecasts are almost always too conservative

(just look at the move from horses to internal combustion engines, and

in the switch from fixed-line phones to mobile phones).

For that reason, we see a skewing of the high-case to the upside.

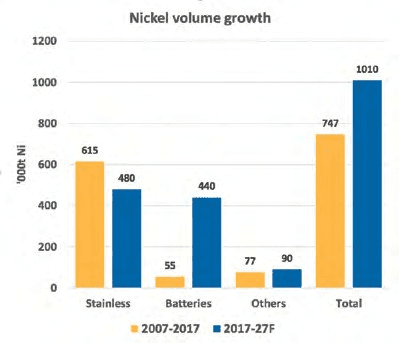

Using the base case forecast, we foresee 440kt growth in nickel use in

batteries over the next 10 years. Due to stainless steel’s dominant

share of demand, stainless will continue to grow, and the need for new

nickel supply in all uses will exceed 1mt, compared with 747kt within

the next decade.

The nickel requirements for battery makers are very specific, with

the main input being high-purity nickel sulphate. Until now, the main

inputs for nickel sulphate production have been nickel-cobalt

intermediates from the high-pressure acid leach (HPAL) and nickel

leaching processes (nickel-cobalt hydroxides and sulphides), and class 1

nickel powders and briquettes. Class 1 nickel powders and briquettes

are preferable to class 1 cathodes, due to their ability to dissolve

quickly in sulphuric acid to make nickel sulphate.

We think the bulk of future demand for nickel in batteries will be

met by the planned construction of HPAL and its capacity to make

nickel-cobalt hydroxides. Projects currently exist in Australia, Turkey,

Papua New Guinea, and Indonesia. Demand will also be met by existing

nickel powder and briquette producers, who currently sell to the

stainless steel industry.

Over the past six months, the nickel market has been rocked by

announcements of multiple Chinese investments in Indonesia totalling

over 150ktpa of nickel, seemingly at extremely low capital costs (under

$20,000/t of nickel capacity) and extremely quick construction times

(1-2 years). History suggests that these expectations are too optimistic

and that projects built over the past 25 years have a tendency to cost

2-3 times more than original estimates and take 2-3 times longer to

build and reach full capacity.

The reality is that all of these projects – and more – will be needed

to meet burgeoning demand for nickel for batteries in the 2020s. Nickel

prices are likely to rise to the $15-20,000/t range over the next five

years as a result of an expected ongoing deficit between supply and

demand, and in order to incentivise new investment. Exciting times are

ahead for the nickel market.

Posted by AGORACOM-JC

at 9:15 PM on Sunday, March 31st, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has interests in Peru, including a 20 percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property. Click her for more information

Producers of electric vehicle (EV) batteries doubled their use of cobalt and nickel last year as auto manufacturing demand increased, according to South Korea’s INI Research and Consulting

Battery industry’s cobalt demand last year rose by 102pc from 2017 to 16,629t, while nickel use climbed by 101pc to 41,521t.

The battery industry’s cobalt demand last year rose by 102pc from

2017 to 16,629t, while nickel use climbed by 101pc to 41,521t. Lithium

use for EV batteries increased by 76pc to 10,902t, while manganese

demand rose by 36pc to 17,673t, as a shift toward more high-capacity

models pushed consumption toward cobalt and nickel that yield higher

energy density.

Shipments of EVs with lithium secondary batteries last year rose by

71pc by capacity to 95.7GWh, INI said. China remained the global leader

in EV demand, accounting for 58pc of car shipments. China also had a

126pc rise in cobalt use to 9,092t and a 123pc gain in nickel

consumption to 17,605t. Chinese lithium demand climbed by 78pc to

6,461t.

South Korean battery producers were cut out of the Chinese EV boom

because cars equipped with their products were excluded from qualifying

for generous government subsidies on vehicle purchases. This market

barrier saw South Korean demand for EV battery materials rise just by

46pc last year in each segment, pushing lithium use to 1,538t, nickel

demand to 6,150t and cobalt to 3,194t.

But China’s EV subsidies are scheduled to end next year, with South

Korean battery producers to capitalise with production expansions. Much

of the growth will not show in statistics as South Korean demand because

most of the new production lines will be in China, Europe and the US.

South Korea’s SK Innovation started work this week on a $1bn plant in

the US state of Georgia that is scheduled to be completed in 2021,

aiming to boost the company’s production capacity to 60GWh by 2022 from

4.7GWh currently.

Japanese cobalt demand rose by 116pc in 2018 to 4,330t, while the

country’s nickel use rose by 108pc to 17,739t, INI said. Japan had the

largest gain in lithium use, up by 93pc to 2,891t. But its manganese

demand dropped by 29pc to 2,134t.

EV battery producers have formed partnerships with materials

producers to help stabilise their supply lines, INI said. But the

industry needs to minimise use of cobalt and develop next generation

products that use less of the element because of its high and volatile

cost, it added.

Posted by AGORACOM-JC

at 8:24 AM on Tuesday, March 26th, 2019

Company has signed a binding Letter of Intent with Klondike Bay Resources Limited to purchase a 100% interest in certain claims in the Sault Ste. Marie Mining District in Ontario.

The claims are located in Vankoughnet Township, Sault Ste. Marie Mining District, Ontario and the purchase terms call for total cash payments of $25,000; the issuance of 500,000 common shares in the capital of Tartisan Nickel Corp.

TORONTO, ON / March 26, 2019 / Tartisan Nickel Corp. (CSE: TN; US-OTC: TTSRF; FSE: A2D) (“Tartisan”, or the “Company”) is pleased to announce that the Company has signed a binding Letter of Intent with Klondike Bay Resources Limited to purchase a 100% interest in certain claims in the Sault Ste. Marie Mining District in Ontario.

The claims are located in Vankoughnet Township, Sault Ste. Marie

Mining District, Ontario and the purchase terms call for total cash

payments of $25,000; the issuance of 500,000 common shares in the

capital of Tartisan Nickel Corp. and a 2% net smelter return royalty

(subject to a 1% buy-back provision for $250,000).

The Sill Lake Lead-Silver Project consists of 13 single cell mining

claims and four boundary cell claims which represents 372.8 hectares.

Lead-silver mineralization was discovered at Sill Lake in 1892, when a

30m adit was driven to a 17m internal shaft, with approximately 40m of

lateral development to exploit a lead-silver vein. This was later

defined by other explorers including some 3750m of diamond drilling

along a defined steeply dipping mineralized trend some 850m in length,

with mineralized widths varying between 1.5m and 4.5m. The Project has

seen two distinct periods of underground development and production and

it is estimated that 7,000 tonnes of ore containing lead and silver were

mined. In 2010, a historical NI 43-101 Technical Report gave a measured

and indicated mineral resource of 112,751 tonnes at 134 g/t silver;

0.62% lead, and 0.21% zinc. The historical resource estimate used a

silver cutoff grade of 60 g/t; but no cutoff grade for the base metal

content was used.

Tartisan CEO Mr. Mark Appleby noted, “The purchase of the Sill Lake

Lead-Silver claims is in keeping with our strategy of acquiring advanced

properties with long term potential. Sill Lake is an excellent project

to generate shareholder value in the short term.”

About Tartisan Nickel Corp.

Tartisan Nickel Corp. is a Canadian based mineral exploration and

development company which owns a 100% stake in the Kenbridge

Nickel-Copper Project in Ontario; a 100% interest in the Don Pancho

Zinc-Lead-Silver Project in Peru just 9 km from Trevali’s Santander

mine. Tartisan also owns a 100% stake in the Ichuna Copper-Silver

Project, also in Peru, contiguous to Buenaventura’s San Gabriel

property. Company financial strength is provided by a significant equity

stake in Eloro Resources Ltd, which is exploring the low-sulphidation

epithermal La Victoria Gold/Silver Project in Ancash, Peru.

Tartisan Nickel Corp. common shares are listed on the Canadian

Securities Exchange (CSE: TN; US-OTC: TTSRF; FSE: A2D). Currently, there

are 99,703,550 shares outstanding (105,803,550 fully diluted).

For further information, please contact Mr. D. Mark Appleby,

President & CEO and a Director of the Company, at 416-804-0280 ([email protected]). Additional information about Tartisan can be found at the Company’s website at www.tartisannickel.com or on SEDAR at www.sedar.com.

Jim Steel MBA P.Geo. is the Qualified Person under NI 43-101 and has

read and approved the technical content of this News Release.

This news release may contain forward-looking statements

including but not limited to comments regarding the timing and content

of upcoming work programs, geological interpretations, receipt of

property titles, potential mineral recovery processes, etc.

Forward-looking statements address future events and conditions and

therefore, involve inherent risks and uncertainties. Actual results may

differ materially from those currently anticipated in such statements.

The Canadian Securities Exchange (operated by CNSX Markets Inc.)

has neither approved nor disapproved of the contents of this press

release.

SOURCE: Tartisan Nickel Corp.

Tags: nickel, nickel demand, stocks, tsx, tsx-v Posted in Featured, Tartisan Nickel | Comments Off on Tartisan Nickel Corp. $TN.ca Signs Binding Letter of Intent to Purchase Sill Lake Lead-Silver Property, Ontario $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 9:15 PM on Sunday, March 24th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

TN: CSE

Nickel has comeback whiff as EVs fuel demand forecasts

Despite its recent run, the nickel price remains some way from the

“excitement levels†of yesteryear. But as this week’s BHP-Mincor deal

shows, there is a buzz about what could be around the corner, with

inventories falling and demand forecast to soar thanks to nickel’s key

role in lithium batteries.

The swagger of the nickel companies at a battery metals conference in Perth during the week was palpable.

Nickel brigade is confident that excitement-inducing prices are on the way, hence their swagger

After a heroic run to $US7/lb in the middle of last year, the price

got beaten up something shocking in the second half with just about

everything else on US-China trade war fears.

The price has since climbed off the December lows of under $US5/lb to

get back to just under $US6/lb in recent days, leaving it well short of

the $US9/lb pricing that historically starts to get everyone excited

about the metal.

But the nickel brigade is confident that excitement-inducing prices are on the way, hence their swagger.

They point to the ongoing drawdown in LME/SHFE stocks needed to meet

demand from the stainless steel sector in the here-and-now, let alone

the demand tsunami coming from the electric vehicle/battery storage

revolution.

Nickel – particularly the almost boutique, in terms of supply, nickel

sulphide type – is not ready for the revolution, unlike some of the

other key battery materials such as lithium and graphite.

Under-investment has led to a dearth of new discoveries and new

developments, leaving forecasters wondering where the new supply is

going to come from to meet the expected growth in demand from the

EV/battery revolution.

That assumes there is no breakthrough anytime time soon in making the

world’s more abundant laterite nickel ores more competitive in the

supply of high-grade nickel product suitable for use in battery

manufacturing.

There was no fear at the conference of that happening anytime soon.

In broad terms, the nickel boys and girls reckon nickel demand from

the EV/battery sectors could well match that of the (also growing)

stainless sector (73% of the current 2.2mtpa market compared with 5% for

batteries) sometime in the 2020s/early 2030s.

All that explains the renaissance of Australia’s Western Australian-centric nickel industry.

BHP (ASX:BHP) is spending up big on its pivot to the supply of nickel

sulphate to battery makers and it is again investing in sustaining

production at its Nickel West unit out to at least 2040.

Other miners that eventually shut down when the nickel price got ugly

post-2008/2009 are plotting their return, and nickel-focussed explorers

are again getting a good hearing.

Then there are the private equity groups sniffing around the WA scene

for exposure to the nickel thematic before the potentially-manic rush

to secure supplies by end-users – as already witnessed in the lithium

sector – takes hold of the metal.

Some of that was reflected in the move by US private equity group

Black Mountain on to the Poseidon Nickel (ASX:POS) register in a big way

last year and its acquisition of the mothballed Lanfranchi mine from

Panoramic (ASX:PAN).

Now it has to be said that there is no boom in nickel equities just yet.

But stand back if the EV/battery thematic unfolds, as most suspect it

will. Nickel can be the most volatile of metals (small market and slow

response times) and a sharp and lasting price spike could be upon us

before we know it.

Mincor Resources

Mincor’s (ASX:MCR) new managing director of six weeks David Southam

looks sharp in a cuff-linked suit but he is not one to swagger.

Nevertheless, he is set to be as upbeat as they come on the nickel

market and his production revitalisation plans for the group’s Kambalda

operations when he hits the Eastern States next week on an investor

roadshow.

Southam called time on eight years as an executive director at the

$615m nickel producer Western Areas (ASX:WSA) to take on the role at

Mincor. And why wouldn’t he? Western Areas stands to benefit from the

suggested nickel upturn more than most, but there is greater leverage to

the upside at the $90m Mincor.

That is reflected in the fact that back in 2007/2008 when nickel shot

to more than $US20/lb, Mincor was a $1 billion company sitting

comfortably inside the ASX 200, with peak production of 16,500t of

nickel-in-concentrates.

Then the nickel price rot set in (due to the rise of Chinese NPI

production and the absence of the EV/battery thematic), forcing Mincor

to first curtail its nickel operations and then shut them altogether by

early 2016, pending the now unfolding upturn for the metal.

The mines were put on care and maintenance and in the meantime,

Mincor got a handy little gold open-cut gold mining operation going

which continues to help pay the bills.

But the main game has always been plotting a return to nickel

production from existing mines (Ken/McMahon and Durkin North), and a

development of the Cassini discovery.

For that to happen four things are needed. The first is a supportive

nickel price. Thanks to the lower US exchange rate, the Australian

dollar nickel price is just about there to mount an economic case for a

restart.

The second requirement is to avoid the capex slug of having to build

its own nickel concentrator by securing a new agreement to replace the

20-year-old one that recently expired with BHP’s Nickel West.

That was ticked off earlier this week when Southam’s experience with

offtake negotiations at Western Areas came to the fore, with Mincor

securing a “modern†agreement on “substantially†better terms, again

with the logical offtake partner, BHP.

The third requirement is to ensure enough mining inventory to

underpin an initial five-year mine life. Mincor is getting close to

those numbers already but will nevertheless be ramping up its resource

extension drilling.

With one, two and three locked in, attention will turn to funding the return to production, expected to cost about $50-$60m.

That looks to be very do-able, given a re-start pitched towards

achieving annual production of 12,000-14,000t of nickel-in-concentrate

(not far off what used to support a $1bn market cap in the heady days of

2008) is the plan.

Posted by AGORACOM-JC

at 10:00 AM on Friday, March 22nd, 2019

Tartisan Nickel (TN:CSE) Kenbridge Property has a measured and

indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

TN:CSE

———————

Chinese electric vehicle makers are gorging on nickel

Battery metals tracker Adamas Intelligence says Chinese electric vehicle manufacturers deployed 253% more nickel in passenger EV batteries in January this year compared to 2018.

The Dutch-Canadian research company, which tracks EV registrations and battery chemistries in more than 80 countries says the jump is due to an ongoing shift from lithium iron phosphate (LFP) to nickel-cobalt-manganese (NCM) cathodes. The average EV registered in China in January 2019 contained nearly double the mass of battery metals/materials as the year prior

First generation NCM batteries contained around a third cobalt with a

chemical composition of 111 – 1 part nickel, 1 part cobalt and 1 part

manganese, but NCM batteries with higher nickel content (622 and 523

chemistries) have become standard in China.

According to Adamas, China is now the the largest market for

passenger EV battery nickel, ahead of Japan and the US, which were the

two largest markets in January 2018. Nickel used in car batteries jumped

88% in Germany and 54% in the US year-on-year.

The EV boom in China is only accelerating, and Adamas says despite

being a seasonally slow month in January 2019, 3.27 GWh of passenger EV

battery capacity was deployed in the world’s largest car market, an

increase of 439% over January 2018 levels:

Even more remarkable, from January 2018 through January 2019, the

sales-weighted average passenger EV battery capacity in China increased

by a staggering 95%, from 14.9 kWh to 29.1 kWh, meaning that the average

EV registered in China in January 2019 contained nearly double the mass

of battery metals/materials as the year prior.

The price of nickel is up more than 20% in 2019 as stocks held in

warehouses around the world registered with the London Metal Exchange

fall to multi-year lows.

Tags: nickel, stocks, tsx, tsx-v Posted in All Recent Posts, Tartisan Nickel | Comments Off on Tartisan Nickel Corp. $TN.ca – Chinese electric vehicle #EV makers are gorging on #nickel $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 3:21 PM on Wednesday, March 20th, 2019

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is

equipped with a 623m deep shaft and has never been mined.

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits.

Plans for Kenbridge include updating PEA,

advancing the project through to feasibility and exploring the open

mineralization at depth

FULL DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM-JC

at 1:52 PM on Thursday, March 14th, 2019

Tartisan Nickel (TN:CSE) Kenbridge Property has a measured and

indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

One of Australia’s largest high-grade nickel producers

Western Areas (ASX: WSA), reported a significant increase in inbound off-take inquiries for nickel sulphide concentrate post current contract periods.

According to the company’s managing director, Dan Lougher, this new

trend is primarily linked to the accelerating electric vehicle battery

sector.

Addressing the second day of the Paydirt 2019 Battery Minerals

Conference in Perth, Lougher said some of the new inquiry was driven in

part by the company’s second largest offtake partner, China’s largest

stainless steel producer, Tsingshan.

“Players looking to lock in new long-term contracts will be doing so

at a time technological changes in the battery space are favouring the

new NCM 811 classification (Nickel, Cobalt, Manganese) which research

indicates will be the fastest growing battery combination by 2025,â€

Lougher said. “These battery cells offer better energy density, allowing

fewer and/or lower weight batteries in cars — but they will require

even more nickel.â€

Nickel. Photo from Wikimedia Commons.

The executive noted that the need for nickel is starting to rise at a

time when its price is too low to incentivize new project development,

something that can take up to three years. In his view, this means that

supply markets are likely to diverge and split between stainless steel, a

sector that consumes 72% of global nickel production, and EV demand,

which currently accounts for 4% of total global nickel consumption but

has been growing by 30-40% a year.

“In addition, nickel supply pressure is being exacerbated by

non-ferrous alloys which command 10% of total global markets but are

booming due to strong growth in aerospace industries and a recovery in

oil and gas investment internationally,†Lougher said.

According to the director, all these demand pressures should call for

higher nickel prices. He said one particular force pushing for a higher

price tag is the fact that the chemistry for lithium-ion batteries

favours nickel sulphide styles but very little of the known nickel

sulphide ore bodies worldwide are left to be developed.

“This lack of these ore bodies was already an issue for the nickel

industry so if EVs are to become a reality in day-to-day motoring, then

higher nickel prices will be required. The new demand nickel units will

have to be sourced increasingly from nickel laterites which are victim

to higher processing costs,†he said.

Posted by AGORACOM-JC

at 11:18 AM on Wednesday, March 13th, 2019

Tartisan Nickel (TN:CSE) Kenbridge Property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has interests in Peru, including a 20 percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property. Click her for more information

TN:CSE

———————

Dear Tartisan Investors,

The recently published article below

is a preamble to a more comprehensive report on the Nickel sector which

will be published on March 31st. The Case for Nickel is being made

……….happy reading.

Regards,

Mark

The Case For Nickel: (Roskill Information Services)

The

nickel price had another volatile year in 20‌18, averaging US$13,‌116/t

compared to US$10,‌408/t in 20‌17. The price still swung wildly over

the course of the year, however, rising from around US$12,‌700/t at the

beginning of 20‌18 to over US$15,‌700/t by early June. From there,

however, the price slumped and by the end of 20‌18, the LME nickel cash

price was trading at around US$10,‌600/t. Early 20‌19 has seen a

recovery and by early March, the price was trading back above

US13,‌000/t.

The market was in deficit for the second year

running in 20‌18, despite a 6.8% y-on-y jump in supply that came mainly

from China and Indonesia. China’s output of refined nickel jumped based

on an increase in nickel pig iron (NPI) production, thanks to increased

availability of nickel ores from Indonesia. The supply growth from

Indonesia, driven by the ramp-up of domestic NPI capacity, has been

stellar: the country became the second-largest producer of refined

nickel in 20‌18; three years previously, it was the tenth largest.

The

growth in supply in 20‌18 was still not sufficient to offset the 6.3%

y-on-y rise in demand, however. Demand from the stainless steel sector,

which accounted for 70% of global primary nickel demand, continued to

grow. The rise in crude stainless production in 20‌18 came mainly from

China and Indonesia, two countries that rely heavily on primary nickel

units rather than scrap, to produce stainless steel.

At the other

end of the first-use spectrum, the battery sector only accounted for 3%

of global primary nickel usage in 20‌18. The use of nickel in batteries

is expected to grow particularly strongly in the next decade, thanks to

the rise in electric vehicle use. Roskill estimates that by 20‌28, the

battery sector will be the second-largest consumer of primary nickel.

The

upshot of the second-consecutive market deficit has been a rapid

drawdown in exchange stocks. Inventories of nickel on the LME and ShFE

combined dropped by 189kt in 20‌18, more than the market deficit. This

could indicate that some producers picked up material in order to boost

their production inventory in anticipation of tighter market conditions.

The scale of the drawdown, however, leads us to believe that some of

this material has merely been moved by financiers away from the

statistical clarity of exchange storage to the statistical darkness of

off-warrant warehouses, with the aim of returning this material to the

market when prices have risen further.

Tartisan will endeavour to

forward you the full March 31st report – and presumably doesn’t hurt to

remind all that Tartisan Nickel owns one of the premier assets in

Canada in this space ! (100mm lbs Ni, 50mm lbs Cu)

Regards,

Tartisan Nickel Corp. (CSE:TN) D. Mark Appleby Suite1060, 44 Victoria Street Toronto, Ontario M5C 1Y2 www.tartisannickel.com Ph: 416-804-0280