Posted by AGORACOM-JC

at 1:52 PM on Thursday, August 15th, 2019

SPONSOR: Esports Entertainment

$GMBL Esports audience is 350M, growing to 590M, Esports wagering is

projected at $23 BILLION by 2020. The company has launched VIE.gg

esports betting platform and has accelerated affiliate marketing

agreements with 190 Esports teams. Click here for more information

GMBL: OTCQB

———————–

Kellogg’s shifts sports-related ad spending to esports

The advertiser is shifting more advertising spending to esports because it offers something that most traditional sports cannot — almost unprecedented access to younger people between the ages of 21 and 34 who have high incomes.

For Kellogg’s, esports has gone from an experimental investment to a continuous one

Competitive gaming campaigns are now a staple, rather than a test, on media plans for most Kellogg’s brands.

The advertiser is shifting more advertising spending to esports

because it offers something that most traditional sports cannot — almost

unprecedented access to younger people

between the ages of 21 and 34 who have high incomes. Since it jumped on

the esports bandwagon two years ago, Kellogg’s has steadily made

inroads, moving from experiential activations at tournaments to being

the headline sponsor of them. For Kellogg’s, esports has gone from an

experimental investment to a continuous one, said Dominik Schafhaupt,

marketing manager for snacks in Northern Europe at Kellogg’s.

The scale of those investments will flex depending on the brand and

its target audience as well the market they are based in, said

Schafhaupt who revealed that the advertiser is changing how it funds its

association with esports now that it’s a mainstay on media plans.

Previously, advertisers like Kellogg’s dipped into sponsorship budgets

to fund early forays into the world of competitive gaming. But as the

stakes of making those activations work got bigger so too did the budgets for them, which meant advertisers turned to digital and broader marketing budgets.

“Esports is an element of our communications mix, and there isn’t a single spend pillar it is funded by,†said Schafhaupt.

Perhaps nowhere is this more obvious at Kellogg’s than on its Pringles brand.

The snacks brand has paid to sponsor the League of Legends European

Championships this summer in a deal with its organizer Riot Games. The

partnership comes just seven months after Kellogg’s signed a deal with

gaming community N3rd Street Gamers, which runs its own tournaments.

Marketing partnerships like this tend to average around $2 million

(£1.6 million) to $4 million (£3.3 million) per year and are often done

as multiyear deals, said Rich Routman, president at sports media company

Minute Media. Generally, deals like the one between Kellogg’s and Riot

Games usually consist of marketing rights similar to standard sports

leagues with broadcaster advertising placements, event marketing assets

and marketing partnership rights across the vertical crucial to the

company’s business, said Routman. Yet how all of those assets are added up for commercial fees depends on the seller.

Since there is such a difference in maturity between esports

organizations, sponsorship costs and assets can greatly differ and the

market hasn’t had time to mature properly to dictate the costs.

The deal between Kellogg’s and Riot Games, for instance, is based on

one of several tiered packages sold by the latter. Each package is

weighted toward either media exposure or experiential activations, which

are supported by media impressions and a rate card for the various

assets that can be used. Having that scope between each package means

Riot can create bespoke sponsorships depending on what an advertiser

wants, said Alban Dechelotte, head of business development and

sponsorship for Riot Games.

The Pringles logo will appear on the streams of the tournaments

alongside a call to action when players are entering the game. Those

streams — and subsequently the Pringles brand — will be on both YouTube

and Twitch, which are watched on average by 1.6 million people daily

during the normal season of League of Legends matches, according to Riot

Games. The number of people watching the matches at the same time each

week has hit a peak of over 300,000, up 40% for the same event in 2018,

according to Riot Games.

“Gaming and esports are places where our core target group is, and so

now is the time to get into the community around competitive gaming,â€

said Schafhaupt.

Aside from media exposure, Kellogg’s is also exploring in-game activations.

Millions of Pringles cans across Europe will sport a unique code that

players can redeem to take part in a raffle to win rare characters to

use in the game. Unlike similar activations, which can feel gimmicky,

Kellogg’s is hoping its decision to allow people to use the code to

redeem characters that have been retired and, therefore, are unavailable

swells its cache among the notoriously advertising-adverse gaming

audience.

“I would love to measure my sales off the back of the sponsorship,

but I can’t because we have distribution partners that sit between us

and consumers,†said Schafhaupt. “At the moment, the industry looks at

measurement in esports from a media-value perspective. It’s one of the

areas we’re building on with the sponsorship by looking at how the

community responds to our brand and also the redemption rates of the

code.â€

Posted by AGORACOM-JC

at 11:34 AM on Thursday, August 15th, 2019

SPONSOR: Spyder Cannabis (SPDR:TSXV) went public just a couple of months ago and hit the ground running with 5 operating Canadian retail locations – and a 6th one on the way via an 8,000 sq ft super store in Alberta. Most companies would be ecstatic to have this number of locations – but Spyder just announced a major move into the United States, with a 5 location deal for boutique stores up and down the US Eastern seaboard. The news gets better. If all goes well with these 5 locations, the US outlet partner has a total of 39 locations across 20 states for Spyder to grow into to. Click here for more info.

(TSX-V: SPDR)

Cannabis industry overview: all you need to know

Consumers around the world spent around $12.2 billion on legal cannabis in 2018, according to marijuana research firm BDS Analytics, rising from around $9.5 billion in 2017 and $6.9 billion in 2016.

The firm predicts spending this year will jump 38% to $16.9 billion and believes the industry will deliver a compound annual sales growth of 27% from 2018 to 2022, at which time it expects the market to be worth over $31 billion.

Consumers around the world spent around $12.2 billion on legal

cannabis in 2018, according to marijuana research firm BDS Analytics,

rising from around $9.5 billion in 2017 and $6.9 billion in 2016. The

firm predicts spending this year will jump 38% to $16.9 billion and

believes the industry will deliver a compound annual sales growth of 27%

from 2018 to 2022, at which time it expects the market to be worth over

$31 billion.

Analysts at Jefferies, which reported similar spending figures for

2018 as BDS, believe the legal cannabis market could be worth as much as

$130 billion by 2029. However, that forecast assumes both medicinal and

recreational marijuana is broadly legalised in further major markets

like the US, Europe and Latin America, and that established industries

like pharmaceuticals, beauty and drinks producers start using it in new

products. If the legal picture remained largely the same as it is now,

then the market’s estimated value in a decade is just $50 billion –

which is a huge jump from where sales sit now but ultimately way below

the full potential that could be delivered if the drug was embraced

further.

It is clear the market is set for exponential growth over the coming

years. The global market for illegal marijuana is estimated to be worth

somewhere in the region of $150 billion to $200 billion, so the

legalised market has all that value to chase in addition to new

opportunities, such as formulating new alternative cannabis-based

products.

What is driving the cannabis market forward?

Below are some of the key reasons why the legalised cannabis market is driving forward.

Deregulation and acceptance

From a recreational standpoint, marijuana is the most widely used

drug in the world. Although it still won’t be for everyone, legalisation

is attracting new types of users – and most of them have already tried

marijuana before. According to Deloitte, legalisation is expected to

‘attract more of a conservative experimenter’, those with bigger incomes

and higher education than the typical user using the black market

today. Still, Deloitte reckons that nearly three quarters of all

consumers likely to use legalised marijuana have had prior experience

with recreational cannabis, and over 40% have used it in the past five

years.

There are only two countries that have formally legalised

recreational use of marijuana. Uruguay became the first country to fully

legalise marijuana back in 2013 and was followed by Canada last year.

However, recreational cannabis laws are relaxed in many other countries,

such as in the Netherlands and Portugal where the drug has been

decriminalised, and over 40 countries have legalised medicinal cannabis

in some form, some of which are outlined below:

Argentina

Australia

Canada

Chile

Colombia

Croatia

Cyprus

Czech Republic

Denmark

Finland

Germany

Greece

Irael

Italy

Jamaica

Luxembourg

Macedonia

Malta

Mexico

Netherlands

Norway

Peru

Poland

South Africa

South Korea

Sri Lanka

Switzerland

UK

Uruguay

Zimbabwe

The world is hoping Canada will be able to demonstrate how a fully

legalised marijuana industry can form part of a modern, industrialised

nation in the western world. But the next trigger moment that many are

waiting for is federal approval in the US. Medicinal marijuana has been

legalised by over 30 US states and a further 11 have approved

recreational use with more expected to follow in the coming years.

However, it is yet to be legalised at the federal level, which would

apply one law across the entire country rather than forcing companies to

operate on a state-by-state level.

The picture in Europe is similar. Individual countries are pushing

ahead with their own policies on marijuana use while the law at the EU

level lags behind. The European Monitoring Centre for Drugs and Drug

Addiction says ‘cannabis should be allowed only for “medical and

scientific purposes”‘ and that most countries still regard possession as

a crime that can result in imprisonment. Yet, it adds that several

member states have reduced their penalties for cannabis users, and some

have permitted supply of the drug, which it admits is opening up

discussion. It says European policy is complicated by ‘conflicting

claims’, including decriminalisation or legalisation, medical or

recreational use, and policy success or failure. The initial sign is

that Europe is warming more to reducing the harm of drugs and

decriminalising them, but is further away from embracing the drug in the

same way North America has.

Acceptance of marijuana use is growing. Mexico and Argentina are

leading the charge in Latin America. South Africa and Zimbabwe have

taken the first steps in Africa, while South Korea recently became one

of the first major Asian nations to take steps to make medicinal

marijuana legal.

Billions of investment

There are serious sums being ploughed into this new market as

companies try to get ahead of the game. Data from Dealogic shows there

was over $10 billion worth of mergers and acquisitions (M&A)

activity in the marijuana industry last year – seven times higher than

2017 and not far off the value of the entire legalised cannabis market

worldwide.

Much of the money is coming from well-regarded, established

businesses operating in the pharmaceutical, tobacco, alcohol and

consumer goods businesses that are coming under increasing pressure to

formulate a marijuana strategy as acceptance grows. For example, Constellation Brands,

the maker of Corona beer, completed the biggest deal to date in the

industry after investing $4 billion into Canopy as it pursues new

opportunities in areas like cannabis-infused beverages.

Some have taken a more collaborative approach, with the likes of Molson Coors working with Canadian grower HEXO to develop cannabis-infused drinks, and Canadian cannabis giant Tilray teaming up with both alcohol giant ABInBev and pharmaceutical powerhouse Novartis.

Consolidation among cannabis pure-plays is expected to accelerate over

the coming years, as is the amount of cross-sector investment coming

from other industries.

New cannabis-based products will also widen the appeal of the market

and the growth opportunity for both medicinal and recreational

marijuana. The key for the medicinal market will be providing proven

cannabidiol (CBD) products that can be safely dosed and delivered

without the need to smoke. For the recreational market, where smoking

marijuana will remain (at least in the short term) the preferred method

of choice, the possibilities are endless – baked goods, drinks, olive

oil and honey are just some of the products being infused with cannabis

at present. These ‘edibles’, as they are known, will start to take off

in Canada this year after the government forbid the sale of them during

the first year of recreational use being legalised.

Developing new cannabis products will be key to adoption and uptake.

The main reasons that marijuana users are likely to move to the legal

market is because they expect to get things the black market can’t

offer: such as guaranteed and verifiable quality, new products, or

because they have more control over the potency and type of cannabis

product they purchase.

What could hold the cannabis market back?

Below are some of the key reasons why the legalised cannabis market could be held back.

Regulatory outlook

Although it is highly likely that more countries will embrace

marijuana in the coming years there are several major hurdles to clear.

Having marijuana legalised at the federal level in the US is the key

breakthrough many are waiting for. Letting states manage their own

legislation over the matter causes a string of problems for the market.

Many US cannabis companies can’t get access to banking or financial

services from large lenders in the country who are unwilling to lend to

what is regarded as a ‘grey area’. Marijuana grown in one state can not

be transferred and sold in another, which is one of the key reasons for

the acceleration in consolidation as firms race to buy their way in to

new markets. Marketing, distribution and security laws can also differ

state to state. The complex mismatch of legislation ultimately creates

an uncertain outlook for the US market and raises the costs of

operation.

It is important to stress that there is no guarantee marijuana will

be legislated at the federal level. Although many are expecting it to be

a hot topic in the 2020 election it is unlikely to be a make-or-break

policy area for candidates, especially if they can please both sides of

the argument (by raking in the profits of marijuana through state

legislation without publicly approving it at the federal level). Until

then, it is unlikely the current Republican government, regarded as far

less upbeat on the drug compared to their Democrat rivals, will look to

legalise marijuana at the federal level.

Those countries that have already embraced medicinal marijuana are

the most likely to legalise it at the recreational level. But many

countries that have embraced medicinal marijuana have done so

reluctantly. For example, the UK’s laws on medicinal cannabis are still

very strict and were only introduced following huge media and public

pressure over the case of a very ill 12-year-old boy who had found an

effective treatment using CBD oil. And yet, the UK is the largest

producer of medicinal cannabis in Europe – all of which it is more than

happy to export to the rest of the world.

The attitude in Europe is also vastly different to that of North

America. This is demonstrated by vaping, which in the UK is treated as a

smoking cessation aide aimed at getting people to quit smoking

cigarettes while in the US it is widely marketed much the same way

cigarettes were all those decades ago. While recreational use is common

in some member states there is no appetite to regulate it at the

EU-level. Medicinal marijuana will play a bigger role in Europe over the

coming years but there is unlikely to be any major shift in

recreational laws. While discussion in the US is around how far to take

legalisation and commercialisation, talk in Europe is more on

decriminalisation and reducing harm.

There is little doubt that legislation will warm to marijuana as time

goes on, but there is little certainty over how it will be embraced and

what regulatory model will be deployed.

Financing

As mentioned, the state-by-state management of the marijuana industry

in the US has made it difficult for some to get hold of proper

financing. While a handful of companies such as Tilray, Aurora and Canopy

have emerged as early leaders, none of them are profitable and yet all

of them require the huge sums needed to build an entirely new market and

supply chain. Acquiring and developing the vast land needed to grow the

product, the processing equipment, distribution capabilities and sales

channels is not cheap.

This is one of the reasons why many of the larger players have gone

public so early on, so they can access money from the markets. This has

not been the case in the past: many big tech names refrained from going

public during the tech boom because they had access to plenty of cash

from the banks and private equity. But even the lack of federal law to

govern marijuana in the US complicates things for publicly-listed firms.

For example, a publicly-listed company in Canada cannot operate a

cannabis operation in the US because it is not approved at the federal

level, but a publicly-listed firm in the US can operate anywhere so long

as it is legal there.

With that in mind, many cannabis stocks have funded mergers and

acquisitions using stock, diluting existing investors. Plus, many have

issued convertible notes that provide an immediate injection of cash

into the business but ultimately allow lenders to invest at a huge

discount later on, again diluting other shareholders and placing

pressure on share prices.

With the largest cannabis stocks valued on their future growth

potential rather than past performance, getting access to the crucial

finance needed to deliver that growth is vital.

Taxation and the black market

It can be forgotten that legalising cannabis is about undermining

illicit trade and bringing existing users out of the black market rather

than creating new users, although this will undoubtedly be one

consequence. For this to be successful, governments need to delicately

balance efforts between regulating the industry without placing it under

a huge cost burden.

Drug dealers don’t concern themselves with matters like tax, minimum

wages, cultivation licenses or sales permits. They will always be able

to produce marijuana at a far cheaper cost than a legal operation but

that does not mean legal cannabis can’t be profitable, just that they

won’t enjoy the vast margins enjoyed by illicit traders.

How legalised cannabis – particularly for the recreational market –

is priced will be key to attracting consumers. Data from Deloitte

suggests those currently buying cannabis through illegal channels are

willing to pay more for legal cannabis, so long as it is of a

certifiable quality. However, if legal cannabis is significantly pricier

than what can be bought from a drug dealer then there is a real risk

that many will return to the black market. This could end up being a

volatile cycle: if legal prices rise and waves of customers return to

the black market then there will be an oversupply of legal cannabis,

which in turn would eventually bring the price down again and attract

people back from the black market. In fact, prices in the black market

could be much more stable than that of the legal market. However, this

will not be the case in the medicinal market as it will offer products

designed for specific ailments that won’t be freely available on the

black market. This will also protect the ability of medicinal marijuana

products to charge a much higher price point than a recreational joint

or cannabis cookie.

It is clear, however, that creating a legal cannabis market will not

fully replace existing black markets overnight. Mexico is advancing

toward legalisation and that would represent a significant moment as it

would be the first country that has a prolific drug manufacturing

problem to do so. Still, Vicente Fox, the former president of Mexico

(2000-2006) and now board member of Canadian cannabis company Khiron Life Sciences,

has said legalisation in Mexico as well as the US (where most Mexican

drugs are smuggled into) will only cut around 40% of income flowing to

cartels – a sizeable chunk but far from the levels needed to cripple the

black market.

Governments need to ensure they do not overtax an industry that

already needs large sums to grow and look at the wider picture when

legislating the industry, such as how it could affect healthcare, social

and justice budgets.

Regulatory redtape

When a new industry is emerging there is a battle between industry

and government over who shapes the regulation and who responds to it.

More often than not, industry plays a major role in deciding how it is

regulated through lobbying and governments simply draw the lines of

where the regulation stops. For example, governments around the world

are still trying to figure out how to rein in the likes of Google and Facebook,

who have enjoyed huge regulatory freedom up until recently, and

cryptocurrencies are far from a clean-cut issue but are still being used

by people everyday.

The same will apply to the cannabis industry, which needs to convince

governments not to overburden it. But the health and social

implications of legalising any drug means governments will not allow the

industry to steam ahead like it has with big tech or cryptocurrencies.

However, governments and policy-makers move at a snail’s pace compared

to entrepreneurship and business, and this will slow the progress of

legalised cannabis firms. This has already proven true in places that

have embraced marijuana: initial tax revenues in Canada and California

were much lower than expected during the first year of legalisation

because regulatory red tape stopped the industry from realising its

potential. Big backlogs of sales permits and cultivation licenses were

to blame, demonstrating the infrastructure is not yet in place.

Finding the perfect formula that allows cannabis to be effectively

regulated without hampering the business opportunity will not be easy.

Bricks vs clicks

At a time when bricks-and-mortar stores are falling out of favour and

retailers are shifting their operations online, physical retail outlets

– recreational stores or medical dispensaries – are proving crucial for

legal marijuana sellers in North America. Around 95% of all legal

cannabis sales in some Canadian provinces including Quebec and Nova

Scotia are completed in a physical store with just 5% being bought

online. The need to see and feel the product and the desire to discuss

what is on offer with someone in-the-know is proving an important

selling point for consumers. This is a similar trend to what has

happened with vaping stores, which offer advice and the ability to try

different flavours or strains.

This model means another huge expense for the industry. Running

stores, hiring staff and investing in the logistical and distribution

capabilities needed to supply a network of stores is not cheap, and that

is exacerbated by the fact consumers expect them to be open for long

hours.

The need for a physical place to pick medicinal marijuana is greater

than the need for a store to buy recreational cannabis, in the same way

people prefer to go to a pharmacy to pick up a prescription. However,

more recreational consumers are likely to purchase online once they have

become familiar with the market and some companies are already banking

on this, such as Namaste Technologies which is being dubbed the ‘Amazon

of cannabis’. Although an online model will reduce the costs compared to

opening and running a network of stores, it adds greater pressure on

the need to have the ability to deliver products far and wide – and

quickly. Deloitte has found two-thirds of those willing to purchase

cannabis online expect it to be delivered for free and within two days.

Cannabis is the next big thing but is far from a risk-free ride

There is very good reason to be bullish on the future of cannabis but

finding where the true value in the market at this early stage is

difficult for investors. The biggest cannabis stocks like Tilray, Aurora

and Canopy have already been assigned huge valuations running into the

tens of billions of dollars when they only make hundreds of millions in

revenue each year and report large losses. As was the case with

companies like Twitter to Tesla, it will all be about maintaining

momentum and delivering growth over the coming years and turning to a

profit before the money runs out.

Others may be more attracted to the stocks from the pharmaceutical,

alcohol, tobacco or consumer goods industries that have dipped their toe

into the market because they have established businesses to fall back

on and the financial firepower needed to propel legal cannabis into the

mainstream.

It will be a slow ride for investors looking to get in early and far

from a risk-free journey. Many companies are spending big to carve out a

lead in the market but there is no guarantee that any of them will make

it.

Posted by AGORACOM-JC

at 10:37 AM on Thursday, August 15th, 2019

SPONSOR:ThreeD Capital Inc. (IDK:CSE)

Led by legendary financier, Sheldon Inwentash, ThreeD is a

Canadian-based venture capital firm that only invests in best of breed

small-cap companies which are both defensible and mass scalable. More

than just lip service, Inwentash has financed many of Canada’s biggest

small-cap exits. Click Here For More Information.

IDK: CSE

How Blockchain can further the cause of electric vehicles

According to researchers, EV charging infrastructure could get a further boost if blockchain is integrated into energy systems

Countries such as India and those in the European Union are pulling out all the steps to strengthen the EV ecosystem

Bengaluru: Charged up with the idea that electric

vehicles (EVs) hold the future of energy and transportation, many

countries such as India and those in the European Union are pulling out

all the steps to strengthen the EV ecosystem with battery storage

manufacturing plants, besides offering a host of financial and tax

incentives.

While all these initiatives are steps in the right direction, many

researchers believe the EV charging infrastructure could get a further

boost if blockchain is integrated into energy systems.

A new study by researchers at the University of Waterloo, for

instance, reveals that there is a lack of trust among charging service

providers, property owners and owners of EVs. With an open blockchain

platform, all parties will have access to the data and can see if it has

been tampered with, researchers insist. Their reasoning is that using a

blockchain-oriented charging system will allow EV owners to see if they

are being overcharged while property owners will know if they are being

underpaid.

Blockchain, primarily known for powering cryptocurrencies like

bitcoins, is a form of Distributed Ledger Technology (DLT) that promises

to reduce costs and establish trust, but faces challenges like the

speed of processing transactions. Its popularity lies in the fact that

participants have a copy of the ledger’s data that contains the most

recent transactions or changes, thus reducing the need to establish trust using traditional methods.

“Energy services are increasingly being provided by entities that do

not have well-established trust relationships with their customers and

partners,” said Christian Gorenflo, a PhD candidate in Waterloo’s David

R. Cheriton School of Computer Science, in a 14 August press statement.

“In this context, blockchains are a promising approach for replacing a

central trusted party, for example, making it possible to implement

direct peer-to-peer energy trading,” he added.

In undertaking the study (recently published in the ‘Proceedings of

the Tenth ACM International Conference on Future Energy Systems’),

Gorenflo, his supervisor, professor Srinivasan Keshav of the Cheriton

School of Computer Science, and Lukasz Golab, professor of Management

Science, collaborated with an unnamed EV-charging service provider who

works with property owners to install EV supply equipment that is used

by EV owners for a fee.

The revenue stream from these charging stations is then shared

between the charging service provider and each property owner. The EV

supply equipment is operated by the charging service provider, so the

property owners must trust the provider to compensate them fairly for

the electricity used.

From the case study, the researchers deduced that to incorporate

blockchain technology into an energy system, the involved parties must

first establish trust between themselves. Second, the parties concerned

should design a minimal blockchain system including smart contracts that

resolves the trust issues identified in the first step. Finally, with

the trust-mitigating blockchain in place, the rest of the system can be

migrated iteratively over time. This allows the business model to

eventually grow from a legacy/blockchain hybrid into a truly

decentralized solution, the researchers said.

According to Gorenflo, “In the end, we could even have a system where

there is machine-to-machine communication rather than

people-to-machine. If an autonomous vehicle needs power, it could detect

that and drive to the nearest charging station and communicate on a

platform with that charging station for the power.”

While blockchain implementations in India especially have centred

mostly around the banking, financial and insurance services sector

(BFSI), Jio recently announced it will install one of the largest global blockchain networks in India, comprising “tens of thousands of nodes operational on day one”, over the next 12 months.

That said, integration of blockchain technology into energy trading is now being touted as a promising area of research, and many studies have made efforts in this regard.

Switzerland-based The Share&Charge Foundation, for instance, is

building a decentralized blockchain system for EV charging, to support

payment and contracts. It uses the Open Charge Point Interface protocol

(OCPI) protocol for the peer-to-peer (P2P) connections between service

providers and charge point operators. According to Share&Charge, the

combination of OCPI with blockchain technology can result in secured

contract and connections between parties and improved payment and

settlement.

During the ‘Global Blockchain Congress–Consensus 2018’, organised by

the Department of Information Technology and Electronics, Government of

West Bengal in December 2018, researchers from New-Delhi based The

Energy and Resources Institute (Teri) made a presentation on the

‘Application of Blockchain in Modern Day Power Systems: Trendsetting a

New Paradigm’. Teri’s proposal, made by Alekhya Datta, Fellow, and

Shashank Vyas, Associate Fellow, covered use cases for EVs, distributed

battery storage, grid-connected microgrids, and rooftop solar PV project

financing using blockchain.

As an example, the Teri researchers pointed out that privately-owned

EV charging stations could be used to charge some vehicles passing near

the station and the transaction of bids of charging station owners,

power/energy flow, billing and real-time settlement of payments could be

managed over a blockchain.

Similarly, IIT-Kanpur researchers have proposed that since current billing systems

lack transparency, enabling the service provider to overcharge the

customer, blockchain could be used to develop a “verifiable billing”

system.

Posted by AGORACOM-JC

at 12:10 PM on Wednesday, August 14th, 2019

SPONSOR: Enthusiast Gaming Holdings Inc. (TSX-V: EGLX) Uniting gaming communities with 80 owned and affiliated websites, currently reaching over 75 million monthly visitors. The company exceeded 2018 target with $11.0 million in revenue. Learn More

EGLX: TSX-V

FIFA eWorld Cup 2019 Grand Final generates record viewership

Online viewership increased by 60 per cent from 29m views in 2018 to 47m views in 2019

FIFA eWorld Cup™ Grand Final match carried by 21 broadcasters in more than 75 territories

More than 140m views across EA SPORTS™ FIFA 19 Global Series season since October 2018

FIFA and Electronic Arts Inc. announced today that the FIFA eWorld

Cup™ 2019 experienced another increase in total viewership and achieved

new record figures, generating more than 47 million views across online

platforms during the three-day event.

After impressive numbers throughout the season, FIFA eWorld Cup™ 2019

views increased 60 per cent compared to last year, becoming the most

viewed event of the EA SPORTS™ FIFA 19 Global Series.

The action was streamed in six languages for the first time – Arabic,

Chinese, English, German, Portuguese and Spanish – and was broadcast to

more than 75 territories around the world. Additionally, the EA SPORTS™

FIFA 19 Global Series generated more than 140 million total views

across the 2018/2019 season since kicking off in October 2018.

At the FIFA eWorld Cup™ 2019, the world’s best 32 EA SPORTS™ FIFA 19

players competed to be named champion. Mohammed ‘MoAuba’ Harkous from

Germany was ultimately crowned FIFA eWorld Cup™ Champion 2019, winning

the grand prize of USD 250,000 and an exclusive invitation to The Best FIFA Football Awards™, which take place in Milan on 23 September.

The pinnacle of the EA SPORTS™ FIFA 19 Global Series enjoyed a

fitting climax, with an enthusiastic crowd watching on from The O2,

London’s revered riverside arena, which created a one-of-a-kind

atmosphere in one of the most iconic music and entertainment venues in

the world.

After an expanded calendar which included 17 worldwide league

partners, new events such as the FIFA eNations Cup™ and the eChampions

League, as well as new events all over the globe, the FIFA eWorld Cup™

2019 crowned the world’s best EA SPORTS™ FIFA 19 player.

Speaking about the event, Luis Vicente, Chief Digital Transformation

and Innovation Officer at FIFA said: “The FIFA eWorld Cup™ 2019

showcased once more the growing interest in competitive FIFA and the

huge potential for both viewership and on-site live audiences.

Surpassing 100 million views across the season is another record

milestone for us and our partner EA SPORTS™. With the newly introduced

event structure and rankings this season, the competition level at the

FIFA eWorld Cup™ was the most competitive we’ve ever seen.â€

Vicente added: “With a 60 percent year-on-year increase in

viewership, the new elements added to the FIFA eWorld Cup™ 2019 like the

on-site production in six languages and live music acts complemented

another record-breaking event, resulting in a unique and exciting live

experience for fans at The O2 in London, as well as an enhanced

livestream experience for viewers on FIFA’s digital channels.â€

Reflecting on the FIFA eWorld Cup™ 2019 and the EA SPORTS™ FIFA 19

Global Series, Todd Sitrin, SVP and GM of the EA Competitive Gaming

Division said: “Competitive FIFA viewership growth has skyrocketed. This

growth was fuelled by an expanded EA SPORTS™ FIFA 19 Global Series

which now includes millions of competitors, 17 football league partners

hosting top-flight leagues, and dozens of licensed events being executed

throughout the year. We’re very happy with the results and the fact

that the eSports industry has recognized this franchise as a tier one

eSport.â€

Posted by AGORACOM-JC

at 10:31 AM on Wednesday, August 14th, 2019

SPONSOR: Betteru Education Corp.

aims to provide access to quality education from around the world. The

Company plans to bridge the prevailing gap in the education and job

industry and enhance the lives of its prospective learners by developing

an integrated ecosystem. Click here for more information.

BTRU: TSX-V

The art of new-age learning: A dynamic phenomenon

The e-learning market, valued at over USD 0.25 billion in 2016 is expected to grow to almost USD 1.96 billion by the end of 2021. But this begs the question, why is e-learning on the rise?

E learning, digital education, advantages of e learning, digital learning

It was always going to happen. Art of learning, as we have seen has

always been a dynamic phenomenon. What started as a fiefdom of few in

the age of gurukuls became a fraternity of educators and educated at the

advent of the 21st century.

But what has remained constant is the movement towards a

system that grants more autonomy to the learners, more avenues and tools

to educators and an overall impetus to the knowledge economy. The rise

of e-learning should be viewed in that neon light.

Over the years, numerous articles, blogs, and testimonials have been

written eulogizing, admonishing or elucidating the e-learning fad. All

of them capture one or the other facet of this emerging avenue. But

never have they been so (ir) relevant than now. India, at the moment, is

going through; perhaps its biggest development phase in the education

sector, particularly the one which deals the way knowledge is

disseminated and consumed. Byju, Toppr, Extraclass, you name it.

The probability will be that there are millions who have

heard their name or have used it once. The e-learning market, valued at

over USD 0.25 billion in 2016 is expected to grow to almost USD 1.96

billion by the end of 2021. But this begs the question, why is

e-learning on the rise?

Why is e-learning on the rise?

There are certain benefits to being on an e-learning platform. From

some obvious ones like the flexibility to learn anytime and anywhere to

personalized learning level matching your learning curve, the new way of

teaching offers something that was never possible before.

E-learning platforms offer you with not just a plethora of

disciplines to choose from but also come hard packed with methods that

are easy to grasp and easier to understand.

The application of audio-visual tools, fun animations and

colorful subject material makes it much easier for both the students and

tutors to understand and convey the concepts the books so desperately

try to achieve.

The dearth of physical infrastructure, a reality in many government

run schools, is something that can be easily overcome by adopting

neo-learning tools. All that one need is a working internet connection,

if the course is online or enough electricity hours to charge the

tablets that come in hand. And these are far cheaper to provide than the

usual infrastructures needed to run a school.

Major advantages

Another major advantage that these platforms offer, particularly

extraclass.com is the motivation to learn. It might sound far-fetched

but one of the primary reasons students hate schools or even colleges is

due to lack of motivation to sit in the class the whole day and still

learn nothing by the end of it. The problem is not with teachers, though

they too could use a bit of brushing, but in the mode of education. Not

everyone is blessed with a capability to sit out 8 hours at a stretch.

And faculties, burdened by their already heavy course structure have

little proclivity to make any changes or spare a word or two of

motivation to the students, since there’s syllabus to be completed,

assignments to be checked and administrative work to be done. What we

instead do is assign every child a mentor, a sort of guiding person who

helps them out not just with their course module but also with helping

them chalk out their career opportunities.

Main focus of EdTech startups

But behind this rosy picture lies a disconcerting reality, one which

still needs a lot of work to get affixed. While it is no surprise that

most of the EdTech startups begin by focusing mostly on Tier I and Tier

II cities, the trend is beginning to change. extraclass.com, for

instance, has made it an objective to start from the grassroots and then

make its way upward.

While it’s true that part of it is largely shaped by

relative saturation of the sector in the select cities, the fact remains

that focus on rural areas makes more sense, economically. With

competitive pricing, localized user interface and relevant product

placements, companies can tap into areas that have largely remained

untouched.

The size and demand of the education sector in the country is too

large to be manageable by government or few private players alone. The

time has come to engage players that have solutions that are more in

line with the changing trend of education. And that doesn’t demand

complete replacement of school systems with e-learning.

Both are needed. There is enough space to co-exist. A child is the

greatest asset of a nation and all of us have a role to play in shaping

him/her for the future of their nation, for their society and for

themselves.

Posted by AGORACOM-JC

at 9:21 AM on Wednesday, August 14th, 2019

Announced the completion of its 24,500 square foot phase one indoor cannabis cultivation facility located on 135 acres of land in Low, Quebec, Canada.

This week consultants are finalizing the facility’s Evidence of Readiness Package for submission to Health Canada.

“This is an important milestone for NORTHBUD, as we transition from the construction phase to pre-operational phase,†said Ryan Brown, CEO of NORTHBUD.

TORONTO, Aug. 14, 2019 — North Bud Farms Inc.(CSE: NBUD) (OTCQB: NOBDF) (“NORTHBUD” or the “Company”) is pleased to announce the completion of its 24,500 square foot phase one indoor cannabis cultivation facility located on 135 acres of land in Low, Quebec, Canada. This week consultants are finalizing the facility’s Evidence of Readiness Package for submission to Health Canada.

“This is an important milestone for NORTHBUD, as we transition from

the construction phase to pre-operational phase,†said Ryan Brown, CEO

of NORTHBUD. “We believe that we have built an extremely cost-effective

facility that will allow us to be competitive in all aspects of the

Canadian market. With the addition of over 500,000 square feet of

outdoor production later this year, we anticipate production of over 10

million grams of Cannabis in calendar 2020.â€

Creation of New U.S. Subsidiary

NORTHBUD wishes to inform shareholders that they have established a

wholly owned U.S. based subsidiary. Bonfire Brands USA Inc. has been

established to own and operate NORTHBUD’s proposed acquisitions in the

U.S. markets.

NORTHBUD is pleased to announce that it has appointed Justin Braune

as President of Bonfire Brands USA. Mr. Braune currently serves as the

CEO of EUREKA Vapor and will lead all of the NORTHBUD’s U.S. operations.

Mr. Braune brings over 10 years of industry experience to the

NORTHBUD team. A graduate of the United States Naval Academy, he served

in the U.S. Navy for ten years where he helped manage nuclear reactor

systems aboard the USS Ronald Reagan. He holds an MBA from the

University of Southern California’s Marshall School of Business.

Prior to joining EUREKA Vapor, Mr. Braune served as President at Made

By Science, a startup science and delivery technology company which was

recently acquired by Acreage Holdings. Mr. Braune has served as CEO and

President for multiple startup private and public companies over his

10-year career in the cannabis industry.

“I look forward to working with Justin as we move into the

operational phase of our U.S. expansion plan,†said Ryan Brown, CEO of

NORTHBUD. “Justin has extensive contacts in the U.S. cannabis industry

which will be very valuable as we continue to expand and enter into new

partnerships.â€

About North Bud Farms Inc. North Bud Farms Inc.,

through its wholly owned subsidiary GrowPros MMP Inc., is pursuing a

licence under The Cannabis Act. The Company has built a state-of-the-art

purpose-built cannabis production facility located on 95 acres of

Agricultural Land in Low, Quebec, Canada. North Bud Farms Inc. has

entered into agreements to acquire assets in California, Colorado and

Nevada.

Neither the Canadian Securities Exchange (the “CSEâ€) nor its

Regulation Services Provider (as that term is defined in the policies of

the CSE) accepts responsibility for the adequacy or accuracy of this

release.

Forward-looking statements Certain statements and

information included in this press release that, to the extent they are

not historical fact, constitute forward-looking information or

statements (collectively, “forward-looking statementsâ€) within the

meaning of applicable securities legislation. Forward-looking

statements, including those identified by the expressions “anticipateâ€,

“believeâ€, “planâ€, “estimateâ€, “expectâ€, “intendâ€, “mayâ€, “should†and

similar expressions to the extent they relate to the Company or its

management. Forward-looking statements are based on the reasonable

assumptions, estimates, analysis and opinions of management made in

light of its experience and its perception of trends, current conditions

and expected developments, as well as other factors that management

believes to be relevant and reasonable in the circumstances at the date

that such statements are made, but which may prove to be incorrect.

Forward-looking statements involve known and unknown risks,

uncertainties and other factors that may cause the actual results,

performance or achievements of the Company to differ materially from any

future results, performance or achievements expressed or implied by the

forward-looking statements. Such risks and uncertainties include, among

others, the risk factors included in the Company’s final long form

prospectus dated August 21, 2018, which is available under the Company’s

SEDAR profile at www.sedar.com.

Accordingly, readers should not place undue reliance on any such

forward-looking statements. Further, any forward-looking statement

speaks only as of the date on which such statement is made. New factors

emerge from time to time, and it is not possible for the Company’s

management to predict all of such factors and to assess in advance the

impact of each such factor on the Company’s business or the extent to

which any factor, or combination of factors, may cause actual results to

differ materially from those contained in any forward-looking

statements. The Company does not undertake any obligation to update any

forward-looking statements to reflect information, events, results,

circumstances or otherwise after the date hereof or to reflect the

occurrence of unanticipated events, except as required by law including

securities laws. This news release does not constitute an offer to sell

or a solicitation of any offer to buy any securities of the Company.

FOR ADDITIONAL INFORMATION, PLEASE CONTACT: North Bud Farms Inc. Edward Miller VP, IR & Communications Office: (855) 628-3420 ext. 3 [email protected]

Tags: Cannabis, CBD, CSE, Hemp, Marijuana, otc, stocks, tsx, tsx-v, weed Posted in North Bud Farms Inc | Comments Off on North Bud Farms $NBUD.ca Completes Construction of its Phase One Cultivation Facility and Establishes U.S. Based Subsidiary, Bonfire Brands USA $WEED.ca $CGC $ACB $APH $CRON.ca $HEXO.ca $TRST.ca $OGI.ca

Posted by AGORACOM-JC

at 7:37 AM on Wednesday, August 14th, 2019

Announced the launch of a new same-day delivery service for customers in the Greater Toronto Area.

Spyder customers in the Greater Toronto Area now have the option, for a nominal fee, of choosing guaranteed same-day delivery for vapes and cannabis accessories on orders placed before 2pm.

Vaughan, Ontario–(August 14, 2019) – Â Spyder Cannabis Inc. (TSXV: SPDR) (“Spyder“), an established Canadian cannabis and vape retail operator, announces the launch of a new same-day delivery service for customers in the Greater Toronto Area.

Spyder customers in the Greater Toronto Area now have the option, for

a nominal fee, of choosing guaranteed same-day delivery for vapes and

cannabis accessories on orders placed before 2pm.

“Our decision to launch our same-day delivery service in the GTA is a

clear example of our customer-centric approach. We are committed to

providing our customers with the highest quality products and the most

convenient and personalized service available, “said Dan Pelchovitz,

President and CEO of Spyder Cannabis. “We believe that our same-day

delivery service will give Spyder a significant competitive advantage in

the vapes and cannabis accessory market. We hope to expand the same-day

delivery service to other major Canadian centers in the near future,”

added Dan.

About Spyder Cannabis

Founded in 2014 Spyder is an established chain of three high-end vape

stores, and two cannabis accessory stores, in Ontario, with locations

in Woodbridge, Scarborough, Burlington, Pickering and Niagara Falls. The

Spyder brand is defined by its high-quality proprietary line of

e-juice, liquids and exclusive retail deals, dispensed in uniquely

designed stores creating the optimal customer experience. Spyder is

building off this leading retail, distribution and branding eCig and

vapes company and is pursuing expansion into the legal cannabis and hemp

derived market. Spyder has developed a scalable retail model with plans

to create a significant footprint with targeted and disciplined retail

distribution strategy focusing on Canadian retail and U.S. boutique

retail and kiosks in high traffic peripheral areas

FOR ADDITIONAL INFORMATION, PLEASE CONTACT:

For more information, please contact:

Spyder Cannabis Inc. Dan Pelchovitz President & Chief Executive Officer Contact: Investor Relations Phone: 1-888-504-SPDR (1-888-504-7737) Email: [email protected]

Neither the TSX Venture Exchange nor its Regulation Services Provider

(as that term is defined in the policies of the TSX Venture Exchange)

accepts responsibility for the adequacy or accuracy of this release.

This news release includes statements containing certain

“forward-looking information” within the meaning of applicable

securities laws (“forward-looking statements”). Forward-looking

statements are frequently characterized by words such as “plan”,

“continue”, “expect”, “project”, “intend”, “believe”, “anticipate”,

“estimate”, “may”, “will”, “potential”, “proposed” and other similar

words, or statements that certain events or conditions “may” or “will”

occur..

These statements are only predictions. Various assumptions were used

in drawing the conclusions or making the projections contained in the

forward-looking statements throughout this news release. Forward-looking

statements are based on the opinions and estimates of management at the

date the statements are made. Any number of risks and uncertainties and

other factors that could cause actual events or results to differ

materially from those projected in the forward-looking statements.

Posted by AGORACOM-JC

at 7:30 AM on Wednesday, August 14th, 2019

Highlights:

4,299 patient visits generated revenue of $591,024, compared to 2,187 patient visits that generated $312,485 for Q2 2018.

Strategic redirection:Â The Company has been re-positioning its overall strategy to become a vertically integrated health and wellness brand that connects to its 165,000 patients using a data driven focus to improve patients’ lives with products, technology and health systems.

VANCOUVER, Aug. 14, 2019 – EMPOWER CLINICS INC. (CSE: CBDT) (Frankfurt 8EC) (OTC: EPWCF) (“Empower” or the “Company“), a vertically integrated and growth-oriented CBD life sciences company, and a multi-state operator of medical health & wellness clinics in the U.S., has filed today its unaudited interim condensed consolidated financial statements for the three and six months ended June 30th, 2019 and related management’s discussion and analysis, both of which are available at www.SEDAR.com. All financial information in this press release is reported in United States dollars, unless otherwise indicated.

“The impact of cost cutting measures and the benefit of the Sun

Valley acquisition are now showing up in the financial statements of the

Company” said Steven McAuley, Empower’s Chairman &

CEO. “Even though we can only book two months of Sun Valley’s

performance in 2Q, the significance is notable, and we expect continued

benefits going forward, especially with the new retail product strategy

in-clinics and with the franchise program.”

Q2 2019 Highlights

4,299 patient visits generated revenue of $591,024, compared to 2,187 patient visits that generated $312,485 for Q2 2018.

Net loss of $1,456,505, compared to $3,915,443

for Q2 2018, which was primarily driven by significantly reducing

operating costs through aggressive headcount cuts, facility changes and

lower stock-based compensation expense.

Cash used in operating activities was $1,331,950 for YTD 2019, compared to $2,358,949 for YTD 2018.

Cash at June 30, 2019 of $817,168, compared to $157,668 at December 31, 2018, which was primarily driven by equity financings during the six months ended June 30, 2019.

Recent Highlights

Strategic redirection: The Company has been

re-positioning its overall strategy to become a vertically integrated

health and wellness brand that connects to its 165,000 patients using a

data driven focus to improve patients’ lives with products, technology

and health systems.

Strengthened Management Team: In January 2019, seasoned entrepreneur and executive officer and former GE Capital Managing Director Steven McAuley

was appointed as Empower’s Chairman & CEO. The Empower management

team has since been augmented with critical hires made from the ranks of

investment banking, accounting, marketing and clinic operations among

other disciplines. CFO Mat Lee, appointed on March 19, 2019,

is an experienced accounting and finance executive. To further support

financial and accounting restructuring, the Company engaged the services

of Invictus Accounting Group, a top-tier boutique advisory firm based

in Vancouver, BC.

Experienced and Seasoned Board of Directors: The Company Board of Directors includes its CEO Steven McAuley, Dustin Klein,

the Co-Founder of Sun Valley Clinics and the SVP, Business Development

and Andrejs Bunkse, owner and practicing attorney of Rain Legal and

Counsel to numerous cannabis enterprises in the U.S. and Canada.

Strategic Acquisition: On May 1, 2019, the

Company completed the acquisition of Sun Valley Certification Clinics

Holdings LLC (“Sun Valley”) from Andrea Klein and Dustin Klein and two

minority shareholders, through its wholly-owned subsidiary Empower

Healthcare Assets Inc., for consideration having an aggregate value

of $3,960,000. Sun Valley operates a network of professional medical

cannabis and pain management practices, with five clinics in Arizona,

one clinic in Las Vegas, a tele-medicine platform serving California,

and a fully developed franchise business model for domestic and

international markets.

Strategic Development: The Company has opened its first hemp-derived CBD extraction facility in greater Portland, Oregon

with the first extraction system expected to have the capacity to

produce 6,000 kg of extracted product per year. The Company took

possession of the new extraction facility June 1st, 2019

and has recently been awarded it’s hemp-handlers licence from the Oregon

Department of Agriculture, allowing the Company to enter the next phase

of build-out and full operations in 2019.

2019 Outlook and Catalysts

Enhanced Corporate Governance: The Company has prioritized corporate governance practices under the leadership of its Board of Directors and Chairman Steven McAuley, to ensure financial and accounting controls operate at the highest of standards.

Improved Capital Markets Profile: Empower is

diversifying its business model to become a vertically integrated

operator in the global cannabis sector with a focus on patient care, CBD

product distribution, research & development and CBD product

extraction. The Company believes this will appeal to a broader base of

shareholders and investors and provide greater access to capital and

improved trading liquidity.

Increased Patient Access: With a rapidly expanding

company-owned clinic network and significant expansion opportunity

through the Sun Valley Health franchise model, Empower anticipates it

will grow its total patient list substantially in the years ahead. This

is expected to provide greater opportunity for treatment analysis using

artificial intelligence (AI), through progressive initiatives that

include adding the Endocanna DNA test kit to the Company product &

service offering in clinics and online. Ensuring the Company is a leader

in understanding the efficacy of cannabis-related treatment options is

an imperative.

Focus on CBD Product Sales: The Company has launched

its online store to sell its lines of hemp-derived CBD based products

and premium health & wellness supplements. Customers can purchase

products, including CBD lotions, tinctures, spectrum oils, capsules,

lozenges, patches, e-drinks, topical lotions, gel caps, hemp extract

drops and pet-elixir hemp extract drops. Patients and customers will be

able to access Sun Valley Health customer service, home delivery and

e-commerce platforms.

Market Leading Technology: Empower utilizes

market-leading patient electronic management and POS system that is

HIPAA compliant and provides deep insight to patient care. The Company

supports remote patients using its tele-medicine portal, enabling

patients who do not live near one of its clinic locations, or are

disabled or unable to come to a location, to still benefit from a doctor

consultation.

Launches Nationwide Franchise: The Company has launched

its nationwide franchise program under the Sun Valley Health brand to

dramatically grow our clinic & store footprint increasing direct

access to patients and to sell hemp-derived CBD products and premium

wellness products directly to our customers and online at our new

e-commerce store at www.sunvalleyhealth.com

Opens CBD Extraction Facility: The Company has opened its first hemp-derived CBD extraction facility near Portland, OR

in a region that is surrounded by numerous licensed hemp farms, that

has the potential to produce 6,000kg of extraction distillate or isolate

to serve the Company’s own CBD product lines and other third party

processing contracts.

Financial Summary

$, except where noted

Three months ended

June 30,

Six months ended

June 30,

2019

2018

2019

2018

Patient visits

4,299

2,187

5,497

4,429

Clinic Revenues

591,024

312,485

743,869

614,627

Direct Clinic Expenses

(82,750)

(107,271)

(122,163)

(212,436)

Loss from operations

(1,424,070)

(2,703,891)

(1,703,379)

(3,311,426)

Net loss

(1,456,505)

(3,915,443)

(1,855,047)

(3,754,191)

Net loss per share

(0.01)

(0.06)

(0.02)

(0.08)

Financial Performance

Clinic revenues for Q2 2019 were $591,024, compared to Q2 2018 revenues of $312,485. This increase over the prior year is attributable to the acquisition of Sun Valley Clinics effective May 1, 2019,

and includes two months of accretive revenue. Future results will

include a full three months of results of Sun Valley in quarters going

forward.

Direct clinic expenses for Q2 2019 were $82,750, compared to Q2 2018 direct clinic expenses of $107,271.

These expenses declined despite the increase in revenues due to

improved operational controls to align labor cost with direct patient

consultations. The Company employs a diverse mix of physicians and

practitioners.

Net loss from operations for Q2 2019 was $1,424,070, compared to Q2 2018 net loss of $2,703,891.

This decrease in loss below prior year is primarily attributable to two

factors. Operating expense decreased due to a decrease in salaries and

benefits as a result of aggressive headcount cuts and facility changes.

Additionally, share-based payments decreased due to timing of

share-based awards to management.

Net loss for Q2 2019 was $1,456,505, respectively, compared to Q2 2018 net loss of $3,915,443.

This decrease over prior year is primarily attributable to the decrease

in operating expenses and share-based compensation expense. In

addition, Q2 2018 included listing fees associated with the RTO.

During Q2 2019, the Company used $1,331,950 in cash from operations after changes in non-cash working capital. The Company invested $543,573 for the acquisition of Sun Valley Clinics and raised $2,576,907 via proceeds from various issuances of shares, convertible debentures and notes.

Please refer to the Company’s unaudited condensed interim

consolidated financial statements, related notes and accompanying

management discussion and analysis for a full review of the operations.

ABOUT EMPOWER

Empower is a vertically integrated and growth-oriented CBD life

sciences company, and a multi-state operator of medical health &

wellness clinics, operating the Sun Valley Health clinic brand www.sunvalleyhealth.com, for its nine corporate locations and for franchises in the United States.

As a CBD product manufacturer under the Sollievo brand, the Company

distributes its lines through clinics, online and through retail

partners. Extraction operations are currently being developed in the

Company’s new extraction facility in Oregon.

ON BEHALF OF THE BOARD OF DIRECTORS:

Steven McAuley Chief Executive Officer

DISCLAIMER FOR FORWARD-LOOKING STATEMENTS

This news release contains certain “forward-looking statements”

or “forward-looking information” (collectively “forward looking

statements”) within the meaning of applicable Canadian securities laws. All

statements, other than statements of historical fact, are

forward-looking statements and are based on expectations, estimates and

projections as at the date of this news release. Forward-looking statements

can frequently be identified by words such as “plans”, “continues”,

“expects”, “projects”, “intends”, “believes”, “anticipates”,

“estimates”, “may”, “will”, “potential”, “proposed” and other similar

words, or information that certain events or conditions “may” or “will”

occur. Forward-looking statements in this news release include

statements regarding; the Company’s intention to open a hemp-based CBD

extraction facility, the expected benefits to the Company and its

shareholders as a result of the proposed acquisitions and partnerships;

the terms of the proposed acquisitions and partnerships; the

effectiveness of the extraction technology; the expected benefits for

Empower’s patient base and customers; the benefits of CBD based

products; the effect of the approval of the Farm Bill; the growth of the

Company’s patient list and that the Company will be positioned to be a

market-leading service provider for complex patient requirements in 2019

and beyond. Such statements are only projections, are based on

assumptions known to management at this time, and are subject to risks

and uncertainties that may cause actual results, performance or

developments to differ materially from those contained in the

forward-looking statements, including; that the Company may not open a

hemp-based CBD extraction facility; that the hemp-based CBD extraction

facility may not be fully operational in 2019 if at all; that

legislative changes may have an adverse effect on the Company’s business

and product development; that the Company may not be able to obtain

adequate financing to pursue its business plan; general business,

economic, competitive, political and social uncertainties; failure to

obtain any necessary approvals in connection with the proposed

acquisitions and partnerships; and other factors beyond the Company’s

control. No assurance can be given that any of the events anticipated by

the forward-looking statements will occur or, if they do occur, what

benefits the Company will obtain from them. Readers are cautioned not to

place undue reliance on the forward-looking statements in this release,

which are qualified in their entirety by these cautionary statements.

The Company is under no obligation, and expressly disclaims any

intention or obligation, to update or revise any forward-looking

statements in this release, whether as a result of new information,

future events or otherwise, except as expressly required by applicable

laws.

CONTACTS: Investors: Steve Low, Boom Capital Markets, [email protected], 647-620-5101; Investors: Steven McAuley, CEO, [email protected], 604-789-2146; For French inquiries: Remy Scalabrini, Maricom Inc., E: [email protected], T: (888) 585-MARICopyright CNW Group 2019

Tags: Cannabis, CSE, Hemp, Marijuana, stocks, tsx, tsx-v, weed Posted in All Recent Posts, Empower Clinics Inc. | Comments Off on Empower Clinics $CBDT.ca Reports 2Q 2019 Results Highlighted by an 89% increase in clinic revenues and a 37% decrease in operating expenses compared to 2Q 2018 $WEED.ca $CGC $ACB $APH $CRON.ca $HEXO.ca $OGI.ca

Posted by AGORACOM-JC

at 5:44 PM on Tuesday, August 13th, 2019

SPONSOR:Â Bougainville Ventures Inc (CSE: BOG) provides strategic capital to the thriving cannabis cultivation sector through ownership and development of commercial real estate properties. The company also offers fully built out turnkey facilities equipped with state-of-the-art growing infrastructure to cannabis growers and processors. Click here for more info.

—————–

As demand for CBD explodes, US farmers are seeing dollar signs

According to new data from the US Department of Agriculture (USDA), US farmers more than quadrupled the land planted with hemp in the past year, from 27,424 acres in August 2018 to 128,320 acres today.

In addition to the booming demand for CBD, hemp farmers were likely encouraged by the 2018 Farm Bill, which removed industrial hemp—defined as hemp plants with less than 0.3% THC by dry weight—and its extracts from Schedule I of the Controlled Substances Act

According to new data from the US Department of Agriculture (USDA),

US farmers more than quadrupled the land planted with hemp in the past

year, from 27,424 acres in August 2018 to 128,320 acres today.

In addition to the booming demand for CBD, hemp farmers were likely encouraged by the 2018 Farm Bill,

which removed industrial hemp—defined as hemp plants with less than

0.3% THC by dry weight—and its extracts from Schedule I of the

Controlled Substances Act, where it might have been interpreted as

marijuana, which the US Drug Enforcement Administration states has “no

currently accepted medical use and a high potential for abuse†(despite evidence to the contrary).

While hemp is far from the only crop appearing on more acres this year, it’s clearly smoking the competition.

“There are a lot of things you can do on a farm, but there aren’t a

lot of things you can do to make money,†Will Brownlow, a Kentucky

farmer who had recently started growing hemp, told Quartz in 2018.

He said an acre of soybeans could only get him about $500, but an acre

of hemp—dense with flowers rich in CBD—could yield as much as $30,000.

What’s more, he said, it was relatively easy to cultivate.

“The plant is a weed,†Brownlow said. “And it likes to grow.â€

Posted by AGORACOM-JC

at 2:11 PM on Tuesday, August 13th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

IDK: CSE

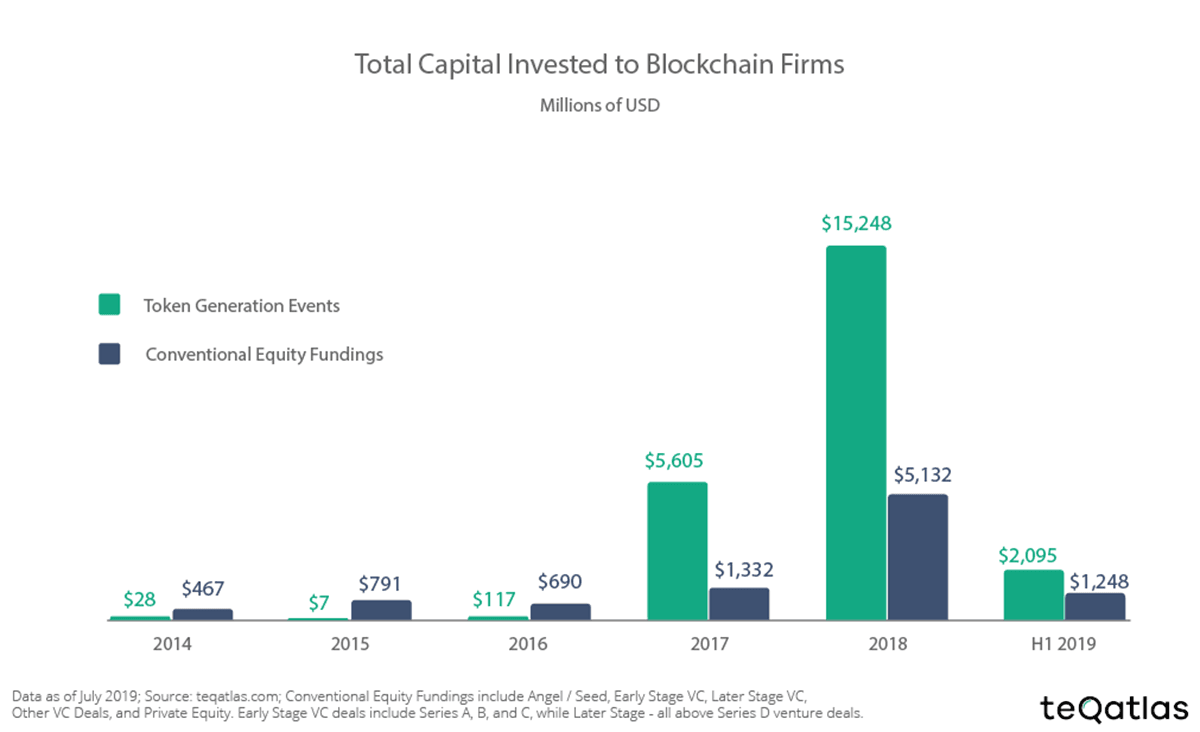

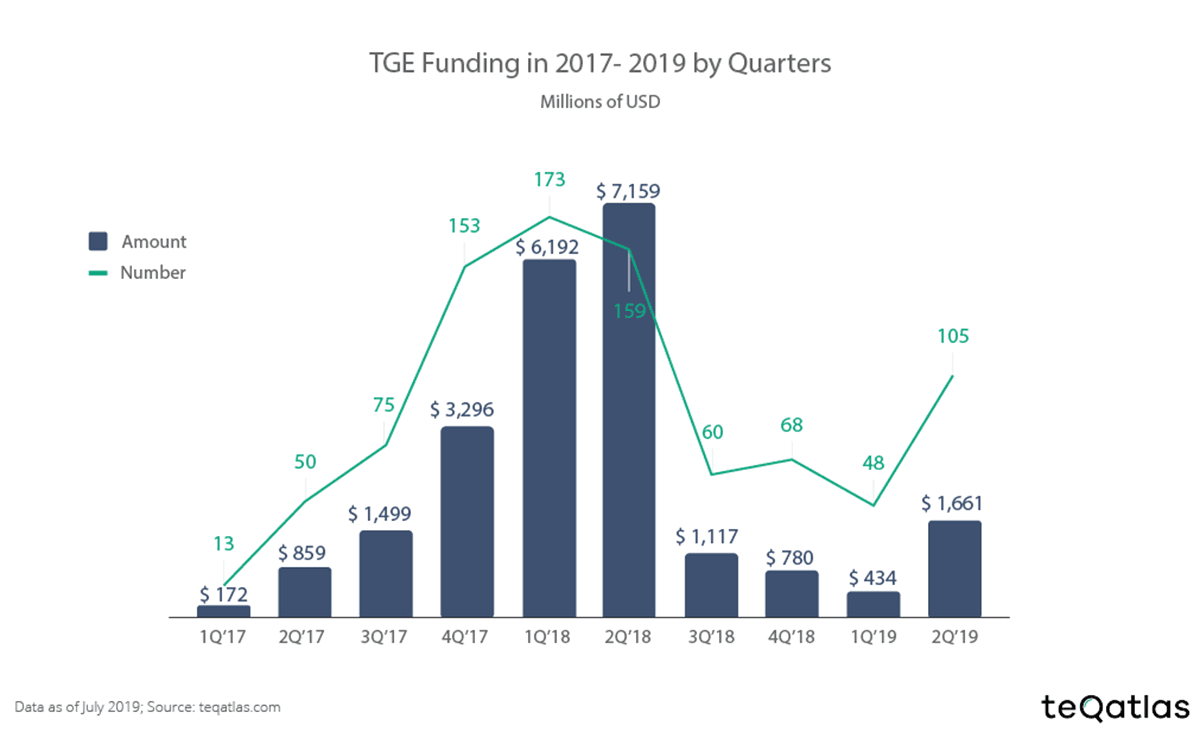

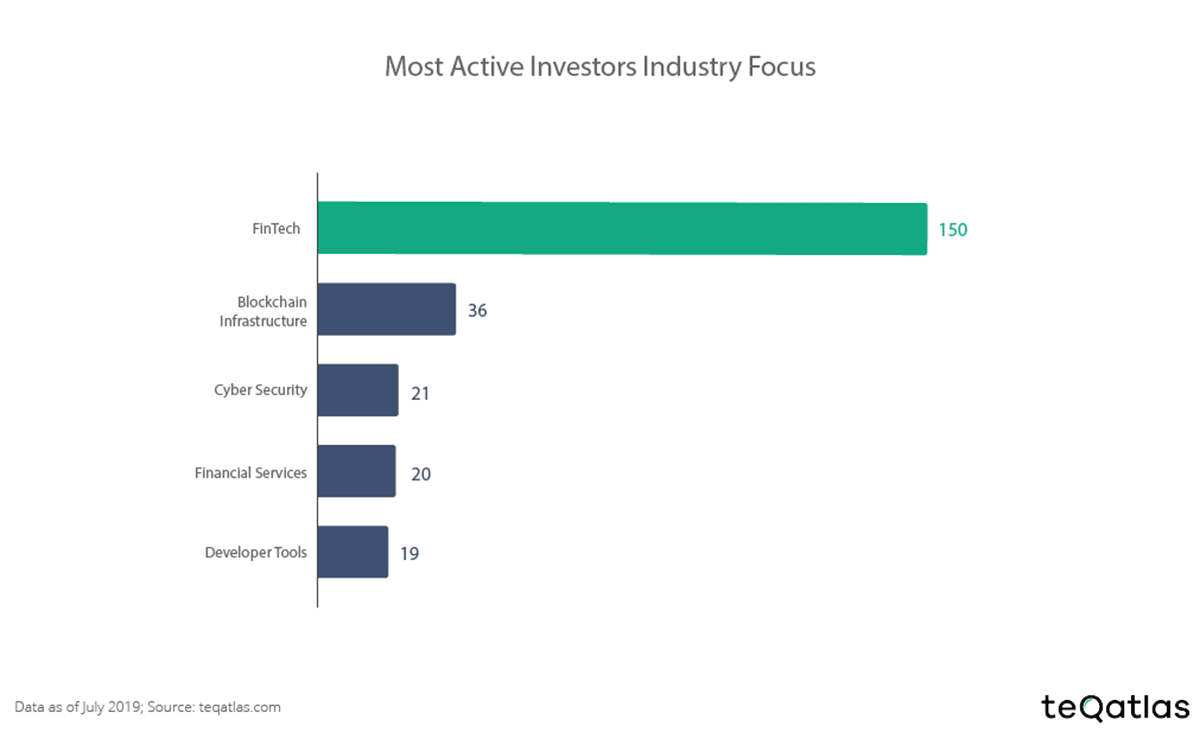

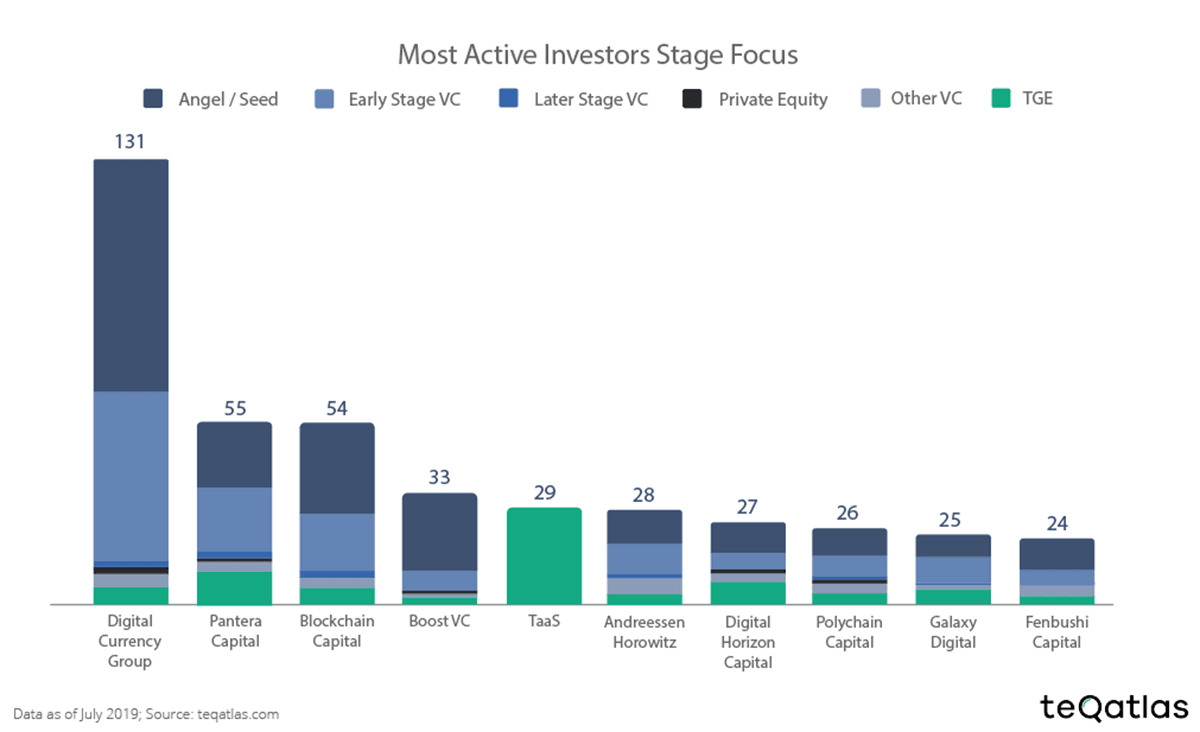

Blockchain Investment Soars In H1 2019: A Look At Trends

Blockchain Investment Trends Research by TeqAtlas includes analysis of 2.5k active blockchain companies that were funded by 1.8k blockchain investors in 2.5k funding rounds through both – conventional and alternative instruments.

While VC activity surpasses Dot-Com era in the U.S., Chinese tech

companies valuations are higher than any time in recent memory, and SoftBank

raised another multi-billion dollar fund, the state of the blockchain

investment market shows indications of maturity and saturation. Although

most blockchain companies are newbies into the market, they still

present an attractive investment potential.

The Blockchain Investment Trends

Research by TeqAtlas includes analysis of 2.5k active blockchain

companies that were funded by 1.8k blockchain investors in 2.5k funding

rounds through both – conventional and alternative instruments.

TeqAtlads takes a comprehensive view of the unique trends that define

blockchain investment market to understand the investor expectations

Investors Continue To View Blockchain A High Return Investment

In the first half of 2019, total capital investment into blockchain

companies has been the opposite of what we saw in the previous year,

which saw a dramatic rise in the amount of capital investment.

The previous year saw a record-breaking $15.2 billion investment in

TGEs (token generation events) and $5.1 billion in conventional equity

funding. In contrast, approx. $2 billion in TGE capital were raised in

the first half of this year. The upward trend is losing steam in the

first half of 2019, after four years of positive growth.

The research still reports a positive, upward trend in terms of

venture capital (VC) injected into blockchain companies. Conventional

equity rounds have accumulated $1.2 billion in the first 6 months of

2019, as compared to $1.3 billion for all of 2017.

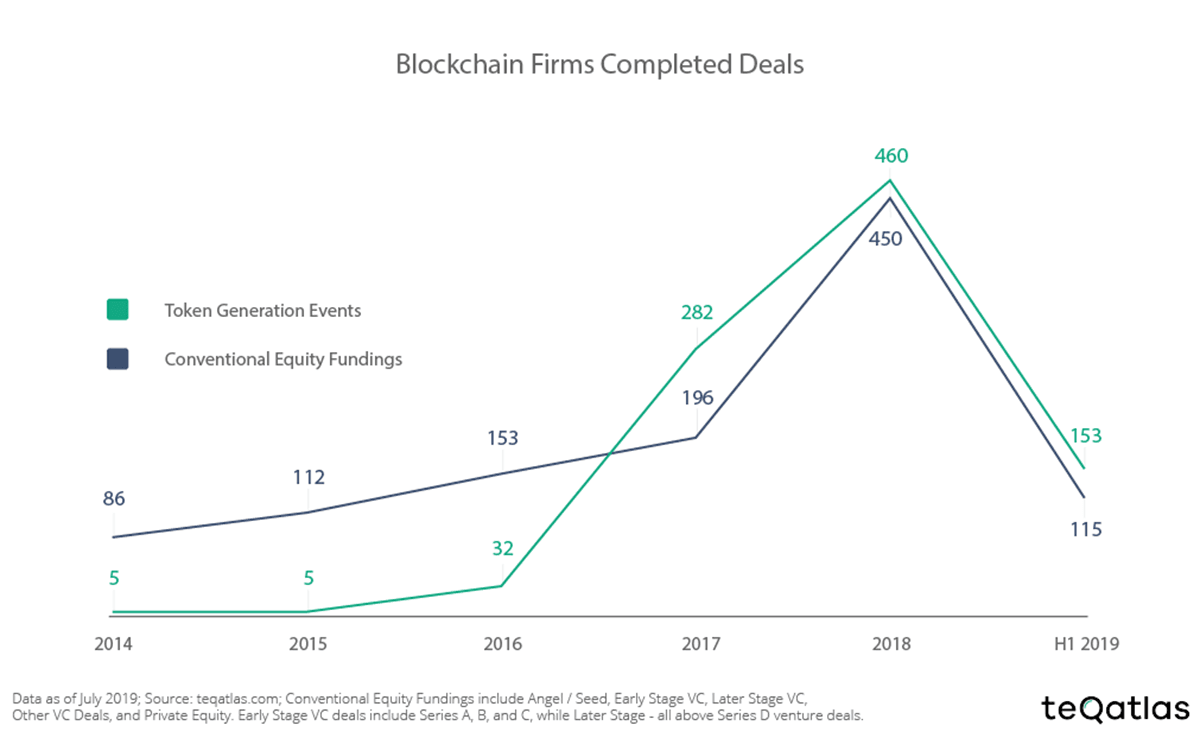

How Did Blockchain Companies Fare In Deal Activity?

Throughout the research, 2018 continued to remain the benchmark for blockchain companies. The height set during the blockchain boom is hard to replicate as the effects of the dramatic fall in value still affect the industry.

In terms of deals, the grand total of investment rounds in the blockchain industry in the first half of 2019 was 268.

For comparison, blockchain companies attracted 910 deals in 2018 and

478 deals in 2017. At the same pace, 2019 might just oust 2017 in terms

of blockchain deal activity.

Surprisingly enough, if you add private equity into the equation, the

total number of conventional funding rounds almost equal the growth

numbers in 2018.

A breakdown of all the blockchain investment funds also reveals that

TGEs were more successful in raising money than Venture Capital rounds –

with the former amassing 26% more on average.

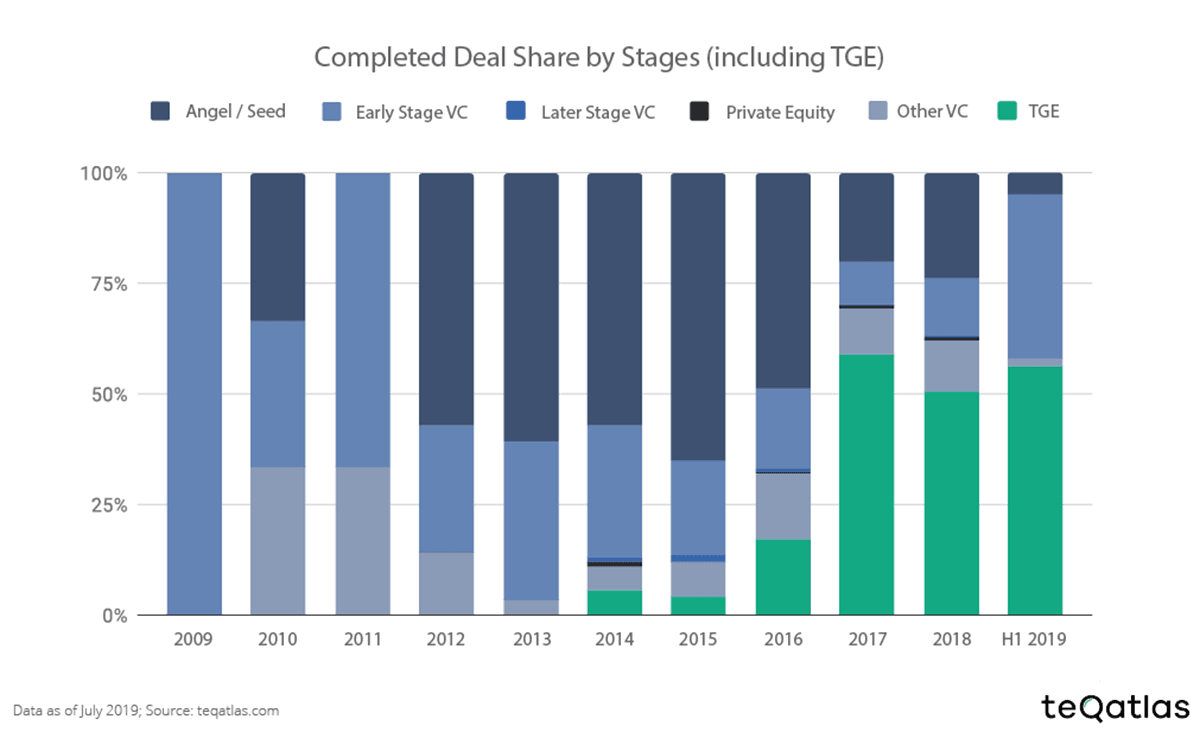

There Is Increasing Interest In Alternative Funding Techniques

Research into completed deals in 2019 shows an emerging trend; investors are increasingly experimenting with alternative funding methods. In fact, a majority (56%) of all closed deals in these six months were secured through TGEs.

Venture capital deals of early-stage funding ensure that traditional

investment comes in second with a 34% share. Early-stage VC rounds form

the major part of conventional funding rounds in terms of the total

capital invested in active Blockchain companies with a 34% share in 1H

2019. If you add in angel seed rounds, this share increases by another

7%.

Equity Funding Has Decreased as compared to 2018

If you analyze the investment pattern from 2014 to the first half of 2019, you are likely to notice that Early-stage VC rounds come out on top for most blockchain investment by stages, with blockchain investments in this stage exceeding $2 billion.

Later Stage Venture Capital Investment Is On The Rise

Later stage venture capital rounds have become increasingly popular,

which means that major players, such as institutional investors, became

interested in this market.

The total amount raised by later-stage blockchain companies backed by

venture capital was $289 million in 2018 only. To compare, the median

round amount of the later-stage IT companies amounted to $11.5 million

in 2018, according to Statista.

The TGE Hype Is Fading Away

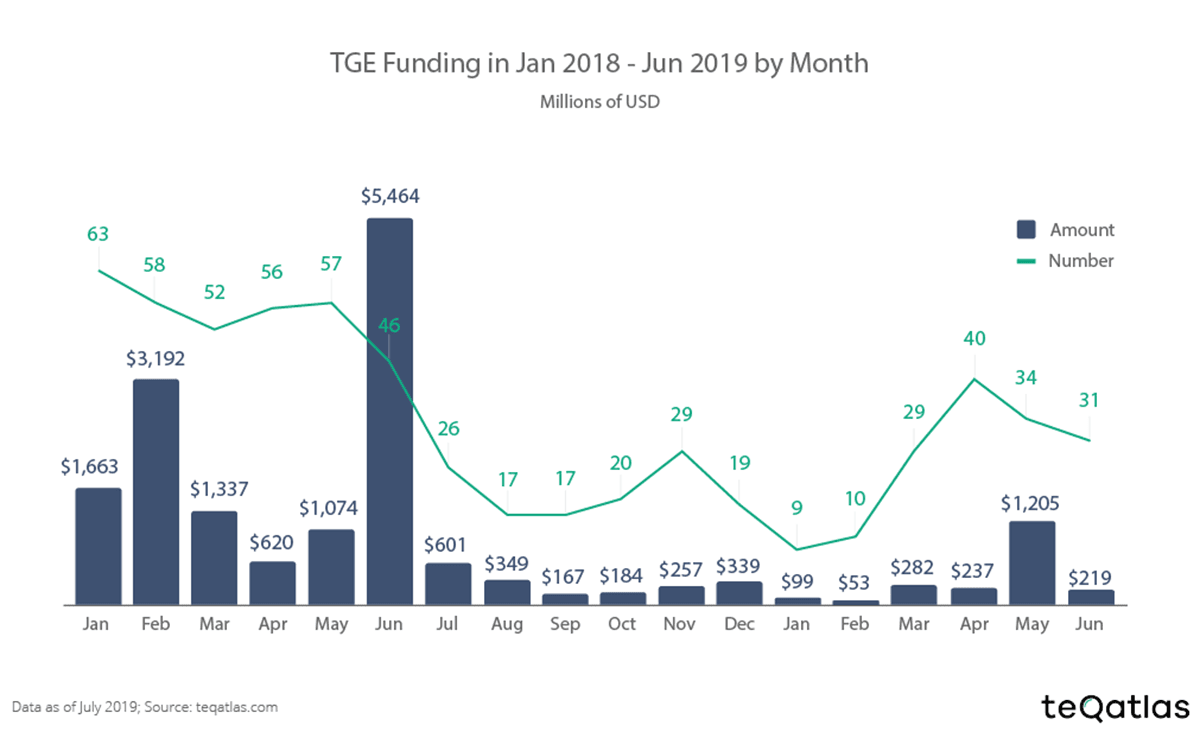

TeqAtlas analyzed TGE investment data for 18 months ending in June 2019 to consider how many investors participate through TGE.

The findings state that – despite minor spikes – the overall trend and interest in token generation

events remain on an all-time low. Blockchain investors tread carefully

when it comes to investing in TGEs, with only 153 deals to show for the

six months of 2019.

Blockchain regulations surrounding TGEs, coupled with the dismal

investment numbers, has led us to predict that they are nowhere near

becoming the principal funding method in the blockchain industry.

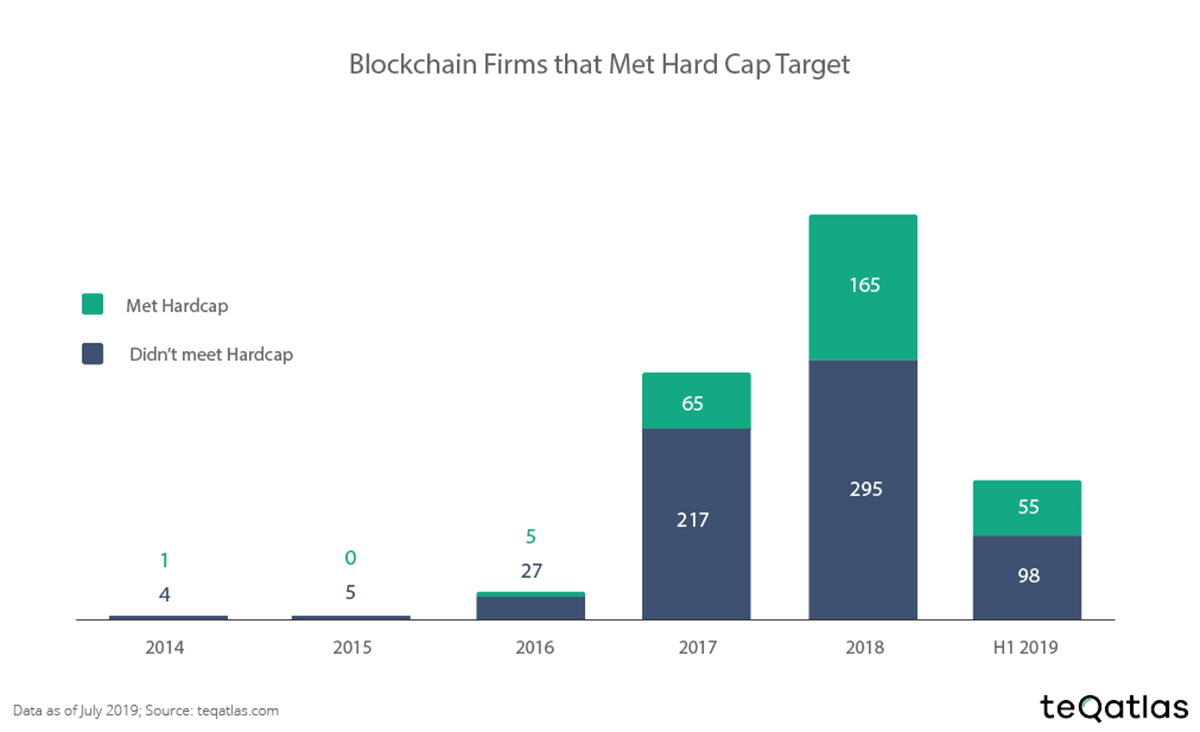

64% Of Startups Don’t Meet Their Hard Cap

Another challenge identified in the research was that startups, due

to being new and relatively inexperienced, often fail to predict their

hard cap amounts accurately.

A mere 36% of startups manage to meet their hard caps during the

token generation event, with the rest failing to do so. Nevertheless,

2019 has been a slightly better year for startups; the percentage of startups that didn’t meet their hard cap dropped 13 points as compared to the previous year.

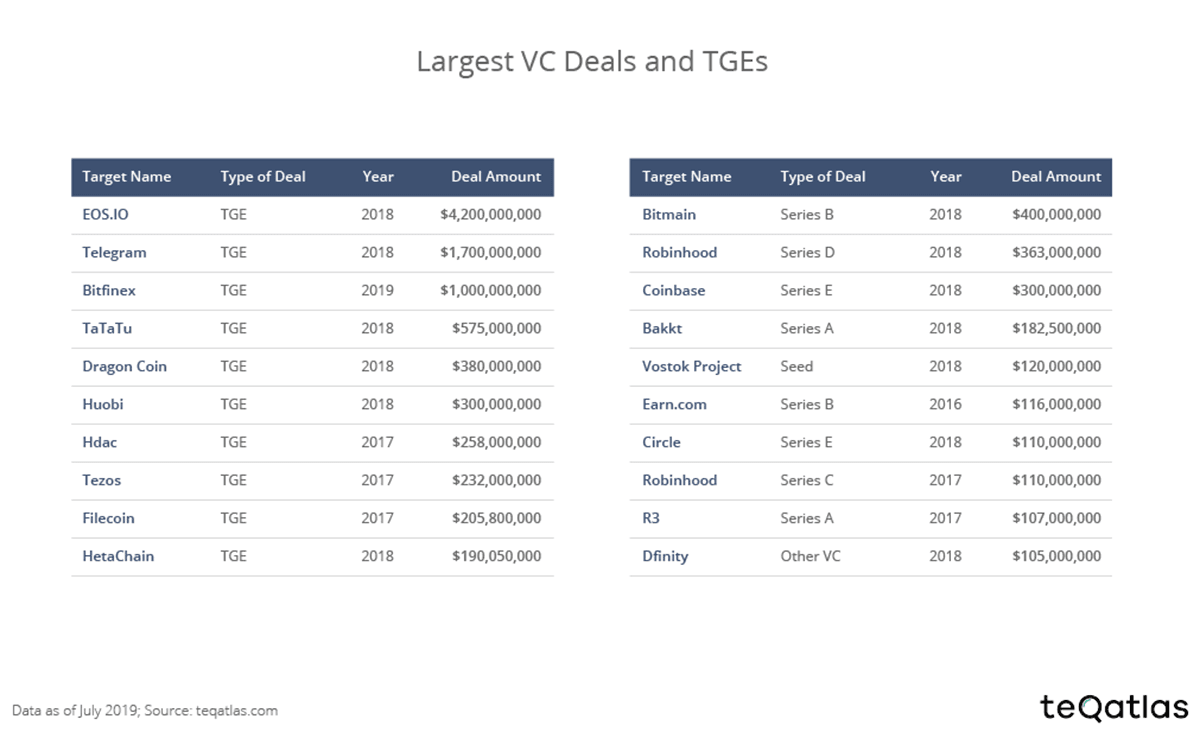

What Are The Biggest Deals since the Blockchain inception?