Posted by AGORACOM-JC

at 9:00 PM on Sunday, April 21st, 2019

SPONSOR: Enthusiast Gaming Holdings Inc.

(TSX-V: EGLX) Uniting gaming communities with 80 owned and affiliated

websites, currently reaching over 75 million monthly visitors. The

company’s partial 2018 (first 9 months) revenue of $7.4 million

representing a 625% increase over the same period in 2017.

EGLX: TSX-V ———————————-

As millions of dollars pour in, esports teams offer varying visions of the future

Tens of millions of dollars continue to flow towards top esports organizations, with Gen.G announcing a $46 million investment round Wednesday,

A raise featuring money from a mix of Silicon Valley venture capital firms, figures in traditional sports and actor Will Smith.

Gen.G., the parent company of the Overwatch League’s Seoul Dynasty, recently brought in $46 million in fundraising. (Robert Paul/Robert Paul) ByNoah Smith April 17

Tens of millions of dollars continue to flow towards top esports

organizations, with Gen.G announcing a $46 million investment round

Wednesday, a raise featuring money from a mix of Silicon Valley venture

capital firms, figures in traditional sports and actor Will Smith.

Flush with cash, and in some cases strengthened by the enforced

scarcity of a franchise model in publisher-driven leagues built around

games such as Overwatch and League of Legends, esports organizations are

starting to embark on long-term visions to shore up their positions for

the future. The visions themselves are far from uniform however, as

some seek to emulate traditional sports teams while others see something

quite different, operating more like full-on corporations than merely a

competitive organization.

Akin to European sports clubs that have teams which compete in

various sports — think Maccabi Tel Aviv, Real Madrid, and Bayern Munich —

esports organizations are companies that own teams which participate in

several different video games. But for some their business model

extends into other areas as well, including content creation and

apparel. In this way esports organizations are breaking from the

established business models of traditional sports, based heavily on

television broadcast revenue and box office receipts, to reimagine their

place in a new, online and global industry. The financial ecosystem

around many such outfits encompasses competitive video games, player

streaming on platforms like Twitch and Mixer, original unscripted

content and even gambling.

Cloud9, which raised $50 million last year and $25 million in 2017,

has decided to place some of its upcoming focus and capital on creating a

competitive structure for young players.

“Imagine baseball was invented last week, what would Little League

look like?†said Dan Fiden, president of Cloud9. Fiden said that, unlike

traditional sports which have youth leagues, esports for kids is

completely unstructured.

“Some of the players we sign have never been coached in anything ever,†he said.

The organization’s planned Los Angeles headquarters will feature a

public space where fans can meet up, interact with players, watch games

and it will also contain the “equivalent of the esports little league

diamond,†according to Fiden.

“We want to continue to continue to launch programs like this to

learn how best to organize and coach kids. We want to figure out the

curriculum,†Fiden said, but noted his organization’s core business

remains trying to win games.

Gen.G is also trying to move beyond the footprints of existing sports

teams via its international focus and content production, both common

in an industry that has been always been international and which

considers South Korea to be its Mecca. For content, fans expect access

to top players through Twitch and YouTube.

“We don’t have to just build versions of what we’ve seen yesterday,â€

said Gen,G CEO Chris Park, who was previously a senior executive for

Major League Baseball.

Park said his company will continue to place a heavy focus on growing

in China, Korea (they own the Seoul Dynasty team in Overwatch League),

and the United States.

In a departure from traditional sports, he said Gen.G will not only

be looking to attract top players, but top content creators as well,

since they plan to “create content that shows gaming is a culture and

way of life.â€

The 100 Thieves franchise, which received a high profile investment

from singer Drake, has established itself as an apparel company, with

its limited edition gear quickly selling out after its becomes available online.

The differing approaches illustrate that esports is still very much

amorphous and in its very early stages, even as investor attention —

and money — has arrived en masse. Park said that his organization was

“oversubscribed within hours†of announcing their latest raise. Fiden

said there has been “strong interest†in Cloud9 from investors since

2017.

Last year’s notable raises, in addition to Cloud9, include $38

million for Echo Fox, $37 million for TeamSoloMid, and $26 million,

including money from Michael Jordan, for Team Liquid.

A 2018 Goldman Sachs report

stated that esports have landed venture capital investment totaling

$3.3 billion since 2013, and $1.4 billion as of the middle of last year.

“We [the esports industry] look like the NBA did in late 60s, early

70s,†said Canaan Partners’ Maha Ibrahim, who has led the firm’s

investment in Gen.G.

Driving the spiraling valuations and investments, according to

Ibrahim and fellow investor in Gen.G, Roger Lee, of Battery Ventures,

are a mix of Overwatch League’s exposure on ESPN and an overwhelming

amount of data to support the viability of the enterprise. Seventy-nine

percent of esports viewers are under 35 years old and this audience, on

Twitch and YouTube, outstrips HBO, Netflix, and ESPN combined, according to Goldman Sachs.

Lee believes top esports teams have more visibility than a comparable

baseball team, and that once esports starts “generating more interest,

they’ll be worth the same amount.â€

Ibrahim agreed, saying, “Teams will be billion-dollar entities, of that I am sure.â€

For now, valuations, like those for many start-ups, are based on the

hope that attention will be converted to revenue at some future date. A

plurality of team revenue is from sponsorships, according to Goldman

Sachs, which projects that by 2022 that will shift to come from media rights.

Video games, including the professional competitive element, are not

widely seen as a threat by traditional sports leagues or teams —

especially those like the NBA and most of its franchises, which have

co-opted them. But in Hollywood, games like the Fortnite are

increasingly seen as a threat. Netflix, which is expected to spend $15

billion on shows this year said in a recent shareholder letter that, “We compete with (and lose to) Fortnite more than HBO.”

“This is more than a movement, it’s the next generation of media and media consumption,†Ibrahim said.

Posted by AGORACOM-JC

at 12:16 PM on Thursday, April 18th, 2019

SPONSOR: New Age Metals Inc. The company owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces in the Inferred. Learn More.

NAM: TSX-V

———————

Supply And Demand Outlook Favors Palladium Vs. Platinum

Palladium has outperformed platinum ever since the fundamentals of

supply and demand have changed due to the diesel emissions scandal.

The gap between platinum and palladium has shrunk in recent weeks,

which would break the current trend of palladium outperforming platinum

if it continues.

Both the fundamental and technical pictures point to the trend

staying in place relative to platinum and palladium despite the recent

hiccup.

The biggest source of demand for platinum (PPLT) and palladium (PALL)

is the automotive industry where emission standards are becoming

increasingly stringent. These standards are driving demand for platinum

and palladium due to their ability to help reduce harmful emissions. The

result has been a sort of competition between the two of them.

However, the competition has become somewhat one-sided ever since the

platinum market was rocked in 2015 by the emissions scandal or “Diesel

Gate†involving Volkswagen (OTCPK:VWAGY).

The reason is because platinum is heavily used in vehicles with diesel

engines. On the other hand, palladium is associated with gasoline

engines.

Cars powered by diesel engines have since fallen out of favor, and

people are now turning towards cars powered by gasoline engines. This

trend does not look to change anytime soon, but it’s set to continue for

the foreseeable future. This is bullish for palladium and bearish for

platinum. The result can be seen in the supply and demand equation for

palladium and platinum.

The market for palladium has a deficit with a surplus for platinum

The emissions scandal has fundamentally altered the landscape for

vehicles powered by diesel and gasoline engines and, by extension,

platinum and palladium. The former is seeing demand decrease, and the

latter is seeing demand increase as there is a shift away from

diesel-powered cars towards gasoline-powered cars.

The two tables reveal that the platinum market has a surplus, with

supply exceeding net demand. Except for industrial demand, every other

segment, including autocatalyst, jewelry, and investment, is in decline.

While supplies from mining have stayed roughly the same, platinum

recycling is adding to the surplus of platinum in the market. The trend

is clearly bearish for platinum.

Platinum supply and demand (Unit: 1000 oz)

Supply

2016

2017

2018

South Africa

4392

4449

4471

Russia

717

703

657

Others

988

953

980

Total supply

6097

6105

6108

Demand

Autocatalyst

3342

3218

3052

Jewelry

2412

2400

2363

Industrial

1806

2022

2321

Investment

620

361

89

Total demand

8180

8001

7825

Recycling

-1934

-2072

-2215

Net demand

6246

5929

5610

Surplus/deficit

-149

176

498

Source: Johnson Matthey

The opposite is true for palladium. Supply of palladium falls short

of net demand and is driven primarily by the increased demand in the

autocatalyst segment. Recycling has made more palladium available, but

supplies have yet to eliminate the deficit in the market for palladium.

Overall, the trend for palladium looks to be a lot better compared to

platinum.

Palladium supply and demand (Unit: 1000 oz)

Supply

2016

2017

2018

South Africa

2570

2550

2590

Russia

2773

2406

2840

Others

1417

1405

1450

Total supply

6760

6361

6880

Demand

Autocatalyst

7951

8428

8655

Jewelry

191

173

166

Industrial

1875

1832

1855

Investment

-646

-386

-555

Total demand

9371

10047

10121

Recycling

-2491

-2899

-3212

Net demand

6880

7148

6909

Surplus/deficit

-120

-787

-29

The forecast for 2019 calls for more of the same, assuming there are

no unforeseen events that could disrupt the supply and demand equation.

Platinum will have a surplus, and palladium, a deficit. The trend

established in recent years as shown in the two tables is not expected

to change. That is bullish for palladium, but bearish for platinum.

Divergence in prices for platinum and palladium

As a result of a favorable outlook, palladium prices have vastly

outperformed platinum. While platinum used to command a much higher

price than palladium, the roles have now been reversed, and palladium is

now worth more. The chart below tracks the relationship between

platinum and palladium prices.

Notice that at its peak in March, a troy ounce of palladium was worth

almost two ounces of platinum. That ratio has now come down, and

palladium is now worth 1.5 ounces of platinum. A significant change, but

still far removed from the days when platinum was more expensive than

palladium.

However, the fact remains that the gap between platinum and palladium

has shrunk with platinum outperforming palladium during this time

frame. The gap could continue to shrink, but it could also begin to

widen as before. Which of the two is more likely to happen will depend

on a few factors that should be taken into consideration.

Can platinum and palladium be substituted for one another in the manufacture of an autocatalyst?

The short answer is yes, but only to a certain extent. While platinum

and palladium are more suitable and preferred in diesel and gasoline

vehicles, respectively, it is not absolutely necessary. The more

expensive palladium becomes relative to platinum, the more manufacturers

may be inclined to look into replacing palladium with platinum in the

manufacture of an autocatalyst. Not necessarily completely, but at least

partially.

In theory, this should act as a cap on palladium relative to

platinum. If the gap in prices between the two becomes too extreme,

precious metal substitution could force the ratio between palladium and

platinum to reverse and narrow. There would be less demand for palladium

and demand for platinum would increase under these conditions. However,

in practice, it is difficult to replace more expensive palladium with

cheaper platinum.

The two precious metals are only needed in trace amounts, and the

price difference would have to be very severe to make a noticeable

difference in the final cost of a vehicle. It also takes a lot of time

and expense to test that changes in precious metal composition in an

autocatalyst meet desired specifications. In a nutshell, while it’s

possible, it’s almost certainly not worth the trouble to replace

platinum with palladium or vice versa.

Why gold prices affect platinum more than palladium

Unlike palladium, platinum prices are more prone to being influenced by the price of gold (GLD).

The reason is because platinum is heavily used in jewelry, much more

than palladium. Because of this, platinum is in direct competition with

gold. In fact, people often have to decide which of the two, gold or

platinum, they will select in a purchase.

People will more often than not pick gold, but they may be tempted to

go for platinum if the former is much more expensive than the latter.

Rising gold prices are, therefore, good for platinum because it makes

platinum a more attractive substitute. But if gold prices fall, then

there is less need for platinum because most people tend to prefer gold.

It’s, therefore, necessary that we look at gold when considering

where platinum will go relative to palladium. The ratio between gold and

platinum prices has changed recently as gold prices have gone down. A

previous article discussing why gold is likely to face pressure can be

found here.

The chart above tracks the relationship between platinum and gold

prices. Notice that while an ounce of platinum was roughly equal to 60%

of gold at its low, the ratio has gone up and is now at almost 70%. What

this basically means is that platinum’s appeal as an alternative has

declined versus gold. This should be seen as a negative for platinum

demand, which could put downward pressure on the price of platinum.

Palladium looks to be priming itself for a big move

Palladium prices have been going sideways after a big drop from their

recent highs. In fact, the chart pattern for palladium resembles that

of a symmetrical triangle or a coil. If this technical analysis is

correct, then a big move may be coming once consolidation is done. The

triangle could resolve to the downside, but it’s more likely to continue

the long-term trend, which is up.

Both the fundamental and technical pictures suggest that a move to

the upside is the most probable outcome. In contrast, platinum is being

held back by a number of issues as a previous article explains here. This would reverse the narrowing of the spread between platinum and palladium and, instead, widen the gap that exists.

The ratio between palladium and platinum has been stuck at around

1.5, as previous charts reveal. This ratio could decrease further, but

the most likely path is for the ratio to resume its previous uptrend

after the time it has spent consolidating. This would be consistent with

the price of palladium outperforming that of platinum.

Palladium will outperform platinum

It’s important to mention that the long-term picture for platinum and

palladium in terms of demand is not a good one. Recent research

suggests that it will one day be possible to make an autocatalyst

without the need for any precious metals such as platinum and palladium.

If this happens, then both metals will be left without their biggest

source of demand.

Furthermore, electrical vehicles are on the rise, and they do not

emit the harmful emissions that platinum and palladium are tasked with

reducing. The challenge for platinum and palladium will be to find new

applications where they can be used. Otherwise, the future of platinum

and palladium does not look all that bright.

Having said that, palladium is most likely to outperform platinum

with both charts and supply and demand in its favor. There is still a

shortage of palladium that the market will not be able to resolve in the

short term. The supply deficit, combined with the recent consolidation

in prices after a major correction, will most likely result in palladium

rising again.

On the other hand, gold is under pressure, and it’s hard to see

platinum doing well when gold is struggling. There is also a surplus of

platinum that will not go away anytime soon. Therefore, barring a major

supply disruption, such as a major strike that drastically reduces

supplies, platinum is highly unlikely to do as well as palladium.

Platinum may have outperformed palladium in recent weeks, but that

should soon reverse.

Posted by AGORACOM-JC

at 11:32 AM on Thursday, April 18th, 2019

SPONSOR: North Bud Farms Inc. (NBUD:CSE) Sustainable low cost, high

quality cannabinoid production and procurement focusing on both

bio-pharmaceutical development and Cannabinoid Infused Products. Click Here For More Information

While cannabis investors are distracted by seeds and crop yields,

corporations with M&A in mind see a more lucrative future in

brand-building and retail.

Cannabis growers have hardly any revenue and their product is still

illegal in their most desirable market, the U.S. That’s not stopping

investors and corporate giants from spending billions of dollars to

take stakes in these companies. They obviously see growth potential. And

yet the question remains, how do you even value a pot business?

Altria Group Inc., the U.S. tobacco leader and maker of Marlboro cigarettes, announced in December that it was buying 45 percent of Cronos Group Inc.,

one of Canada’s growing number of cannabis producers and among the

industry’s high-flying stocks. The $1.8 billion transaction left us

wondering: How did Altria determine that price? After all, in the period

before the deal, Cronos generated sales of less than $4 million – no,

that’s not a typo – and certainly no profits. Recreational pot had only

just become legal in Canada two months earlier. Altria, a $105 billion

market-cap company that rarely does splashy deals, placed immense value

on a barely existent business in a nascent market.

The projected growth of the worldwide cannabis market has some

investors pouring money into newcomer companies with tiny revenue and no

profits

Source: Arcview Market Research, BDS Analytics

It’s a tricky thing to gauge the worth of assets that will

potentially be highly valuable down the road – but are difficult to

quantify just yet. Looking at other industries where this has been the

case is helpful. Even if their businesses aren’t perfect comparisons,

the method of valuing them can be instructive.

Take the natural-resources space, where the focus is often on

non-financial metrics. They include production capacity and tangible

assets, such as proved oil reserves – which is to say, how much fuel a

producer can likely pump from their land. It can be argued that this

is similar to how individual investors already have been gauging

cannabis companies, dazzled by how many kilograms can be produced and

how many acres of greenhouse they have.

But the downside to this approach for cannabis is that it puts too

much emphasis on supply-chain processes that may become commoditized,

and a rudimentary focus on capacity doesn’t capture how the early movers

in this market can differentiate themselves. The industry’s novelty

also distracts from what can be a challenging business from an

operational standpoint. For example, Aphria Inc.’s share price increased

more than elevenfold over the last five years, but in its latest

quarter the business was hamstrung by supply shortages and packaging

issues.

A better comparison for cannabis may be the biotechnology space.

Deals for drug developers involve big, risky bets on future potential

blockbusters. These products may not generate revenue yet, but they aim

to address very specific markets and are expected to have an economic

moat that wards off competition. For pharmaceuticals, that moat comes

from patent exclusivity that prevents copycat versions of a therapy. In

some ways, this is what the more advanced cannabis companies are looking

to accomplish. They won’t have patents in the same way, but they do aim

to create intellectual property and specialized brands that appeal to

certain types of customers. And they want to be first to form those

customer relationships.

Remember, this market will be far more expansive than simply selling a

box of joints. There’s an opportunity to create all sorts of consumer

products, and the marketing can vary widely – from wellness drinks and

beauty items infused with cannabidiol, or CBD (the part of cannabis that

doesn’t deliver a high), to “sin†products like marijuana-infused

edibles, or something more akin to having a glass of wine.

Taking Off

As the recreational cannabis market surpasses the medical one, it

will become increasingly important for companies to create compelling

brands

Source: Arcview Market Research, BDS Analytics

Look at it this way: Altria doesn’t own tobacco farms. It owns

high-margin brands that source from tobacco growers. So when it’s

studying the future of marijuana, it’s not looking solely at production.

It’s looking for unique brands that can be scaled up by a team with the

necessary know-how. In the case of Cronos, CEO Mike Gorenstein said on

the last earnings call that the company is trying to differentiate

itself with pre-rolled joints, adding that innovation around branding

and efficiency will be “a bigger differentiator than just cultivation.â€

Knowing the important role that brand-building will play in the next phase of the cannabis industry’s growth story,

it’s useful to study these companies’ senior management teams and look

for branding and retail pedigree. It’s a good sign that Cronos’s head of

marketing has had stints at PepsiCo Inc. and Mondelez International

Inc., and that Tilray Inc. has a one-time Starbucks Corp. executive

running its retail strategy.

Green Growth Brands Inc., based in Ohio and Ontario, has a deep bench

of such leaders: Its CEO is Peter Horvath, a former executive at

American Eagle Outfitters Inc., Victoria’s Secret and DSW. His key

deputies come from the likes of Abercrombie & Fitch Inc. and Bath

& Body Works. They are rightly emphasizing that retail expertise is a

point of distinction and an advantage as they develop targeted brands

such as Green Lily, aimed at women, and Camp, aimed at active, outdoorsy

types. This brand-centricity seems to be paying off: Even though Green

Growth doesn’t have as large a market capitalization as the

Canada-based players, it recently scored a partnership with Simon

Property Group Inc. to open more than 100 CBD stores in the mall giant’s shopping centers, and its CBD products will be sold in 96 DSW locations.

That U.S. footprint might do it good down the road, as wider

marijuana legalization seems likely. While much of the focus these days

is around the promise of the Canadian market, it’s important not to let

that obscure what should be the cannabis world’s real end game.

Sizing Up The U.S. Prize

California alone has a larger population than Canada, illustrating

why the U.S. remains such a tantalizing opportunity for the cannabis

industry

Source: Statistics Canada, U.S. Census Bureau

And, in general, the Canadian companies that have received such

bountiful investor buzz are at something of a disadvantage on the

branding front, notes Bethany Gomez, a cannabis industry analyst at

Brightfield Group. Because of strict rules in Canada regarding logo size and other packaging details for currently available cannabis products, they are simply limited in how distinctive they can make their presentation.

Wherever it’s sold, if the cannabis business is to grow as big as the

industry’s bulls hope, it is going to have to successfully court

non-users and infrequent users. That’s where newer innovations, such as

edibles and beauty items, may be more important than smokeable

products.

Not Quite Cannabis Crazy

In U.S. markets that have legalized recreational marijuana, many

people are still not consuming cannabis, underscoring the opportunity to

grow addressable market

Source: BDS Analytics Consumer Insights

The companies that become the breakout stars in the legal cannabis

era will be the ones that have a vision for how to create demand for

such goods, whether through curiosity-inducing product, a great in-store

experience or alluring marketing. These capabilities – not merely

spreading more seeds in soil – should be a critical part of valuing the

pot pioneers.

Posted by AGORACOM-JC

at 10:03 AM on Thursday, April 18th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

Under a 100 percent renewable energy scenario, metal requirements could rise dramatically, requiring new primary and recycled sources

Clean technologies rely on a variety of minerals, principally cobalt, nickel, lithium, copper, aluminum, silver and rare earths. Cobalt, lithium and rare earths are the metals of most concern for increasing demand and supply risks

The growing demand for minerals and metals to build the electric vehicles, solar arrays, wind turbines and other renewable energy infrastructure necessary to meet the ambitious goals of the Paris Climate Agreement could outstrip current production rates for key metals by as early as 2022, according to new research by the UTS Institute for Sustainable Futures.

The study, commissioned and funded by U.S. non-profit organisation

EarthWorks, shows that as demand for minerals such as lithium and rare

earths skyrockets, the already significant environmental and human

impacts of hardrock mining are likely to rise steeply as well. In a

companion white paper, Earthworks makes the case for a broad shift in

the clean technologies sector towards more responsible minerals sourcing.

“We have an opportunity, if we act now, to ensure that our emerging clean energy

economy is truly clean – as well as just and equitable – and not

dependent on dirty mining,” said Payal Sampat, Earthworks Mining

Director. “As we scale up clean energy technologies in pursuit of our

necessarily ambitious climate goals, we must protect community health,

water, human rights and the environment.”

“The responsible materials transition will need to be scaled up just as ambitiously as the 100 percent renewable energy transition,” said Dr Sven Teske, Research Director at the UTS Institute for Sustainable Futures.

Doing so will require a concerted commitment from businesses and

governments, according to the report’s lead author Elsa Dominish, Senior

Research Consultant at the UTS Institute for Sustainable Futures. “We

must dramatically scale up the use of recycled minerals, use materials

far more efficiently, require mining operations to adhere to stringent,

independent environmental and human rights standards, and prioritise

investments in electric-powered public transit.

“The renewable energy transition will only be sustainable if it

ensures human rights for the communities where the mining to supply

renewable energy and battery technologies takes place. If manufacturers

commit to responsible sourcing this will encourage more mines to engage

in responsible practices and certification. There is also an urgent need

to invest in recycling and reuse schemes to ensure the valuable metals

used in these technologies are recovered, so only what is necessary is

mined,” Ms Dominish said.

Research highlights:

Under a 100 percent renewable energy scenario, metal requirements

could rise dramatically, requiring new primary and recycled sources

Clean technologies rely on a variety of minerals, principally

cobalt, nickel, lithium, copper, aluminum, silver and rare earths.

Cobalt, lithium and rare earths are the metals of most concern for

increasing demand and supply risks

Batteries for electric vehicles are the most significant driver of accelerated minerals demand.

Recycled sources can significantly reduce primary demand, but new

mining is likely to take place and new mining developments linked to

renewable energy are already underway

Responsible sourcing is needed when supply cannot be met by recycled sources

Minerals extraction already exacts significant costs on people and the environment, fuelling conflict and human rights

violations, massive water pollution and wildlife and forest

destruction. Most of the world’s cobalt, used in rechargeable batteries

for electric vehicles

and phones, is mined in the Democratic Republic of Congo, often by hand

in unsafe conditions using child labor. Earlier this year in Brazil,

the collapse of two tailings dams at Vale’s Brumadinho iron ore mine

killed hundreds of workers and local residents. Independent research

that analyses decades of data on mine waste dam failures reveals that

these catastrophic failures are occurring more frequently and are

predicted to continue to increase in frequency.

“In Norway, the government tell us we have to sacrifice our fjords to

mine copper for clean energy,” said Silje Karine Muotka, a member of

the Saami Parliament, which is fighting a mine proposal in their

traditional reindeer herding grounds. “I recognise that we need

materials for new technologies, but we should look for ways to get them

that do not harm the environment or threaten native culture.”

“Solar and wind production is growing rapidly, while the cost of clean energy technologies

has continued to fall,” said Danny Kennedy, Managing Director at the

California Clean Energy Fund. “If the clean tech revolution has taught

us anything, it is that humanity possesses boundless capacity for

innovation. Our task is to establish the parameters within which

innovators can innovate to ensure that clean energy is truly clean.”

Earthworks commissioned the ISF research as part of its

newly-launched ‘Making Clean Energy Clean, Just &

Equitable’ initiative, which aims to ensure that the transition to

renewable energy is powered

by responsibly and equitably sourced minerals, minimizing dependence on

new extraction and moving the mining industry toward more responsible

practices.

Posted by AGORACOM-JC

at 4:19 PM on Wednesday, April 17th, 2019

WHY NORTHBUD FARMS?

Canadian regulatory door for CIP (Cannabinoid Infused Products) is opening this year as shown in other legal jurisdictions (Colorado, Washington, Nevada, California)

Infused products sector has become the highest margin segment of the industry

Positioned to be a raw input producer for this space

Currently working with multiple food,

beverage and science companies to provide safe standardized cannabinoid

infused raw inputs for large scale GMP manufacturing of products

Signed Binding Letter of Intent to Enter U.S. Market with Strategic Acquisition of Multi-State Licensed Operator Eureka Vapor Read Release

CHECK OUT OUR RECENT INTERVIEW

FULL DISCLOSURE: NORTHBUD is an advertising client of AGORA Internet Relations Corp.

Tags: CSE, Hemp, Marijuana, stocks, tsx, tsx-v, weed Posted in All Recent Posts, North Bud Farms Inc | Comments Off on CLIENT FEATURE: NORTHBUD $NBUD.ca Signs $20 MILLION Binding LOI For Acquisition of Multi-State Licensed Operator Eureka Vapor WEED.ca $CGC $ACB $APH $CRON.ca $HEXO.ca $TRST.ca $OGI.ca

Posted by AGORACOM-JC

at 11:24 AM on Wednesday, April 17th, 2019

SPONSOR: Enthusiast Gaming Holdings Inc.

(TSX-V: EGLX) Uniting gaming communities with 80 owned and affiliated

websites, currently reaching over 75 million monthly visitors. The

company’s partial 2018 (first 9 months) revenue of $7.4 million

representing a 625% increase over the same period in 2017.

EGLX: TSX-V ———————————-

Will Smith takes slice of Esports team’s US$46 million financing

Actor Will Smith and Japanese soccer legend Keisuke Honda are among the new investors in esports franchise Gen.G, which announced a new $46 million round of financing Wednesday.

Eben Novy-Williams, Bloomberg News

Will Smith reacts at a closing ceremony press conference during the

2018 FIFA World Cup at Luzhniki Stadium on July 13, 2018 in Moscow,

Russia. (Photo by Dan Mullan/Getty Images). , Dan Mullan/Getty Images

Europe

Actor Will Smith and Japanese soccer legend Keisuke Honda are among

the new investors in esports franchise Gen.G, which announced a new $46

million round of financing Wednesday.

Smith and Honda’s Dreamers Fund, a investment vehicle they launched

last year, are joined by Los Angeles Clippers minority owner Dennis Wong

and Michael Zeisser, former chairman of U.S. investments at Alibaba

Group Holding Ltd.

“It’s exciting to see the worlds of technology, media, sports and now

celebrity come together,†said Chris Park, chief executive officer of

Los Angeles-based Gen.G.

Gen.G operates teams in seven different video games and has offices

in China, South Korea and the U.S. Its franchises include the Overwatch

League’s Seoul Dynasty, which will move to South Korea from Los Angeles

next year.

In addition to handling that transition, Gen.G is expanding in China,

investing in player development and trying to increase revenue from

esports-specific areas like streaming and the sale of in-game items.

“The coming years are going see our company really start to

crystallize its identity, not just as a brand, but also as an

enterprise,†Park said.

To that end, Smith and Honda will join 11-time National Basketball

Association All-Star Chris Bosh, already a Gen.G adviser, in helping

grow Gen.G’s media presence. That includes creative and commercial

projects, and helping Gen.G athletes with content creation.

Other new investors in Gen.G include Battery Ventures, New Enterprise

Associates, MasterClass co-founder David Rogier and Stanford

University. Silicon Valley Bank, which helped with the fundraising, is

becoming both an investor and a sponsor.

Posted by AGORACOM-JC

at 10:23 AM on Wednesday, April 17th, 2019

SPONSOR: ThreeD Capital Inc. (IDK:CSE) Led by

legendary financier, Sheldon Inwentash, ThreeD is a Canadian-based

venture capital firm that only invests in best of breed small-cap

companies which are both defensible and mass scalable. More than just

lip service, Inwentash has financed many of Canada’s biggest small-cap

exits. Click Here For More Information.

——————-

Blockchain Goes To Work At Walmart, IBM, Amazon, JPMorgan, Cargill and 45 Other Enterprises

On the Jersey side of the Hudson River just across from Manhattan’s

Financial District, there is a glass-and-steel office tower designed in a

severe International Style aesthetic. “DTCC†is emblazoned across the

top, but few outside of Wall Street realize that in this building,

occupied by the Depository Trust & Clearing Corp., are records for

most of the world’s securities, representing some $48 trillion in

assets—from stocks and bonds to mutual funds and derivatives. In the

1970s, Wall Street created a DTCC predecessor to replace a system that

had been powered by young men running around the cavernous alleys of

lower Manhattan delivering stock certificates from brokerage house to

brokerage house.

DTCC still has paper certificates in its vaults, but records Ârelated

to the 90 million daily transactions it handles are kept electronically

on its servers and backed up in various locations. Thousands of

financial institutions and exchanges in 130 countries rely on DTCC for

custody, clearing, settlement and other clerical Âservices.

In a few months DTCC will begin the largest live implementation of

blockchain, the distributed database technology made popular by the

bitcoin cryptocurrency. Records for about 50,000 accounts in DTCC’s

Trade Information Warehouse, where information on $10 trillion worth of

credit derivatives is stored, will move to a customized digital ledger

called AxCore.

According to Rob Palatnick, DTCC’s chief technology architect, the

warehouse already keeps an electronic “golden record†of events such as

maturity dates, payment calculations and other activities needed to

clear and settle these securities daily. But each participant in a

complicated credit derivatives transaction also keeps its own records,

which must in turn be reconciled multiple times before the investment

matures. By moving those records to the blockchain, visible to all

participants in real time, most of those redundancies won’t be

necessary.

“We’re not talking about eliminating humans and firms,†PaÂlÂatnick

says. “We’re talking about getting rid of layers of databases and

translations between those databases.â€

On the other side of the world, in Taipei, Taiwan, Foxconn, the

electronics giant best known as a manufacturer of iPhones, launched a

Shanghai startup called Chained Finance with a Chinese peer-to-peer

lender. Chained will soon connect Foxconn and its many small suppliers

(and their suppliers’ suppliers) on an Ethereum-based blockchain that

will use its own token and smart contracts (read: automatically

executed) to make payments and provide financing in near real time,

eliminating a daisy chain of paperwork.

“We view blockchain as the skeleton of our work,†says Jack Lee, the

founder of Foxconn’s venture capital arm, which has invested $40 million

in six blockchain startups. “Smart contracts that automatically execute

transactions are the muscles, and tokens are the blood.â€

Welcome to the brave new world of enterprise blockchain, where

corporations are embracing the technology underlying cryptocurrencies

like bitcoin and using it to speed up business processes, increase

transparency and potentially save billions of dollars. At its core,

blockchain is simply a distributed database, with an identical copy

stored on many computers. That facilitates transactions (financial or

otherwise) between individuals (or companies) that don’t know or trust

each other. It’s virtually impossible to cheat, since every transaction

is recorded in many Âplaces and the details of those transactions are

visible to everyone. Companies are already using blockchain to track

fresh-caught tuna from fishing hooks in the South Pacific to grocery

shelves, to speed up insurance claims and to manage medical records.

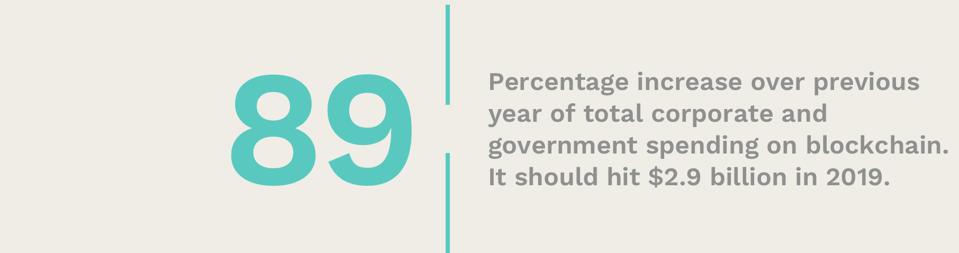

Total corporate and government spending on blockchain should hit $2.9

billion in 2019, an increase of 89% over the previous year, and reach

$12.4 billion by 2022, according to the International Data Corp. When

PwC surveyed 600 “blockchain-savvy†execs last year, 84% said their

companies are involved with blockchain.

To chronicle the rise of so called “enterprise†blockchain, Forbes has

created its first annual Blockchain 50 list of big companies that are

putting the technology to work in Âmeaningful ways. While blockchain’s

first application, cryptocurrency, is struggling to achieve mainstream

adoption, these companies are committing manpower and capital to build

the future on top of shared databases.

The version of a blockchain future these companies are building is,

for the most part, far different from what the founders and early

adopters of blockchain had envisioned. While many cryptoÂcurrency

idealists fantasize about a global, public network of individuals

connected directly and democratically, without middleÂmen, these

companies—many of which are middlemen themselves like DTCC—are building

private networks they will use to profit from centralized management.

Not surprisingly, financial firms—from Allianz to Visa and JPMorgan

Chase—dominate the list. But Blockchain 50 companies run the gamut of

industries, including energy firm BP, retailer Walmart and media company

Comcast.

Because of the lingering bad taste left by bitcoin drug bazaars like

Silk Road and the 2017 digital currency bubble, most companies emphasize

the distinction between crypto and blockchain, shunning the former and

embracing the latter. In some ways the members of the Blockchain 50

represent a bridge between the old and new worlds. Just as internal

computer networks were adopted by companies long before the internet

took off, these firms are starting by adopting distributed ledger

technology at a small scale.

“The era of blockchain tourism has ended,†says Bridget van

Kralingen, Senior Vice President for Platforms & Blockchain. “We’ve

really seen blockchain move from being overshadowed by cryptocurrency to

focus on real business problems and complex processes.â€

In 2009, when Satoshi Nakamoto, bitcoin’s pseudonymous creator,

activated his network, its blockchain was the underlying accounting

system that let anyone with bitcoin transfer money without the need of a

middleman. Transactions are processed in blocks—just a fancy word for a

hunk of data—about every ten minutes, each containing a compressed

version of the previous block, linking them together into a chain.

Instead of relying on a bank or another middleman to keep track of when a

bitcoin leaves one location and arrives at another, the thousands of

computers on the bitcoin network do the work and in exchange for their

efforts are paid in bitcoin.

For most companies this presented a potential problem. While

identities aren’t required to use the bitcoin blockchain, the

transactions themselves are tied to addresses that are publicly

available, meaning that with a bit of work many of these addresses can

be tied to actual people or companies. Thus enterprises like Coca-Cola

and JPMorgan Chase, accustomed to maintaining competitive advantages

based on proprietary processes and control, were initially skeptical of

cryptocurrency.

Businesses also need some control over their data. “The entire

corporate world has been fashioned around who has responsibility over a

particular part of the business flow,†says David Treat, the global head

of Accenture’s Financial Services Blockchain practice. “There can be no

gaps, because that is unacceptable for a multibillion-dollar company.

You cannot have a gap, or you are subject to huge security breaches and

social contract breaches.â€

Perhaps no firm has had a greater influence on the growing corporate

use of blockchain technology than Digital Asset Holdings, a New

York-based startup that hired the former JPMorgan Chase banker Blythe

Masters as its CEO in early 2015. Under Masters, Digital Asset began

making acquisitions and almost immediately purchased a small company

that was in the process of building an “invitation only,†or

permissioned, blockchain. Then in late 2015 Digital Asset donated the

code for its “open ledger†project to the Linux Foundation, which

supports commercial open-source software projects, including the Linux

operating system.

The project was called Hyperledger, and thanks in part to ÂMasters’

connections, its backers read like a who’s who of finance and

technology. Thirty companies are listed as founders, including ABN AMRO,

Accenture, Cisco, CME Group, IBM, Intel, JPMorÂgan Chase, NEC, State

Street, VMware and Wells Fargo. HyperÂledger immediately established

itself as the gold standard for corporate blockchain projects.

What happened next might be considered the Big Bang moment of

enterprise blockchain. In early 2016, IBM donated 44,000 lines of code

to the project, which formed the core of a new blockchain with faster

speeds and increased privacy. No fewer than half of the members of the

Forbes Blockchain 50 are now using that blockchain, known as Hyperledger

Fabric.

“We’ve been very focused on making sure that not only is the

blockchain technology standard but that the documents and data are

standard,†says Marie Wieck, IBM Blockchain’s general manager. “This

standardization allows [the companies] to not spend their time comparing

differences and validity in the documents.â€

Shortly after the launch of Hyperledger, which is a nonprofit

venture, a New York fintech called R3 raised $107 million from the likes

of ING, Barclays and UBS to create a for-profit enterprise blockchain

platform called Corda Enterprise.

As the commercial potential of co-opting blockchain technology became

more apparent, many cryptocurrency startups began to rethink their

models.

For example, San Francisco’s Ripple, originally called OpenCoin and

conceived of as yet another alternative monetary system, expanded its

focus in late 2015 from the cryptocurrency (called ripple and trading as

XRP) to building software for large banks. A bitcoin startup called

Counterparty spawned another company, Symbiont, in March 2015, which

coded a proprietary blockchain that’s now being used by Vanguard for

sharing stock index data. In February 2017, ConsenSys, a Brooklyn-based

collection of crypto companies controlled by one of Ethereum’s founders,

helped launch the Enterprise Ethereum Alliance.

Just as corporate America co-opted counterculture vibes for its

marketing and advertising (“Think Different,†“Don’t Be Evilâ€), its most

forward-thinking businesses are fast incorporating a technology that

was designed in large part to eliminate them.

In insurance, for example, MetLife’s mobile app Vitana bundles

insurance with a test for gestational diabetes that uses a blockchain to

record data and verify and pay claims. In recent testing in Singapore,

where one in five expectant mothers develops gestational diabetes, a

practitioner simply enters a positive test result into a patient’s

electronic medical record and in a matter of seconds MetLife’s smart

contract deposits an insurance payment into that patient’s bank account

to cover the medical expenses associated with the condition. No

paperwork or claim filing necessary.

Similarly, Germany’s Allianz, working with EY, tested moving certain

captive insurance claims processes—often involving many emails,

attachments and phone calls across multiple times zones—to a private

blockchain. The time required to process a claim fell from weeks to

hours.

The French bank BNP Paribas, which has lent money to commodities

traders since the 19th century, is considering using a ledger platform

called Voltron to process letters of credit for traders. Northern Trust

has begun administering private equity funds using Hyperledger Fabric.

Broadridge Financial has been running pilots testing multiple

distributed ledgers for its dominant proxy voting and shareholder

communications business.

“In real time, you know who owns the stock, who’s entitled to vote

and how it’s tied to the universally-agreed-upon shareholder meeting

agenda,†says Michael Tae, Broadridge’s head of strategy.

Golden State Foods, a big McDonald’s supplier that makes more than

400,000 hamburgers per hour, tracks the location and temperature of its

patties with devices like radio-frequency ID tags and Hyperledger

Fabric. The system can immediately alert GSF to conditions that might

lead to spoilage. At the same time, it can optimize inventory levels by

tracking how much meat is in a truck or in a restaurant’s freezer, in

real time.

At this year’s SXSW conference in Austin, Texas, Bumble Bee unveiled

an SAP-built supply-chain blockchain offering complete transparency to

its customers. Soon you will no longer have to take Bumble Bee’s word

for it when its assures you that the 12-ounce package of yellowfin tuna

you just bought was caught by individual fishermen in the South Pacific

and not by a factory ship. The fishing crews, tuna processors and

packers are now entering their own data in real time on Bumble Bee’s

distributed ledger. By summer, Bumble Bee will be sharing that

information with retailers and customers who take the time to check.

From a public relations standpoint alone, Bumble Bee’s SAP blockchain

is likely to bear dividends. In 2017 Greenpeace ranked Bumble Bee 17th

out of 20 tuna brands for its sustainability practices, accusing it of

“greenwashing†a host of bad behaviors with environmentally friendly

marketing.

“Food safety and sustainably sourced product has become an

overwhelmingly important topic in our industry,†says Tony Costa, the

CIO at Bumble Bee. “Leveraging the latest technology enables us to open

it up to more of a public perspective, if you will. So we get out of the

business of managing data. We’re relying on a relationship.â€

In the healthcare business, an estimated 20 cents of every

Âdollar—some $700 billion a year—is wasted because of inefficiencies.

Ciox, a little-known company based in Alpharetta, ÂGeorgia, that manages

medical-records exchanges for 60% of the Âhospitals in the U.S., is

considering developing a private blockchain that healthcare providers

could use—for a fee paid to Ciox—to exchange data. Blockchain 50

enterprises like Ciox and the media giant Comcast, which is toying with

using blockchain to micro-target television advertisements, plan to use

the privacy features of blockchain to profit from their customers’ data

while protecting their identities.

Despite the surge in corporations working on blockchain projects, the

technology is still new, and relatively few have generated significant

revenues or savings.

The one group that is getting rich from the current enterprise

blockchain gold rush: consultants. Deloitte, PwC, KPMG, EY and Tata

Consultancy Services are deploying small armies to preach the virtues of

blockchain to the C-suite and charging huge fees to help companies

implement the technology. (We excluded consultants from the Blockchain

50 because they played a key role in helping us Âcreate the list.)

Deloitte, for example, has 1,400 full-time blockchain employees. India’s

Tata has 1,000 staffers, 600 of them full-time, in its blockchain unit.

Tech firms, including Oracle, SAP and Amazon, are also staking out

their turf.

Part technology firm, part consultant, IBM may be the biggest and

most successful enterprise blockchain company of all. Besides helping

create Hyperledger Fabric, the company has 1,500 staffers—mostly

engineers—devoted to the new technology and reports that its IBM

Blockchain powers 500 client projects.

“The power of any blockchain network is in its participants and its

members,†says IBM’s Wieck. It matters little Âwhether those members are

crypto-idealists or global corporations.

Posted by AGORACOM-JC

at 4:35 PM on Tuesday, April 16th, 2019

PyroGenesis

is one of Canada’s greatest small cap technology companies, with several

successful divisions that are succeeding both globally and at the highest

levels of business. The common denominator for each of them is the

company’s plasma torch technology. For example, 2 US Aircraft Carriers

(and 2 more on the way) have integrated Pyro’s plasma torch technology for

environmental applications. At $13 Billion per carrier now, one can only

imagine the hyper-stringent hoops PyroGenesis had to pass – which puts their

technology at the world class level.

In

addition to other equally impressive applications, the company’s 3D printing

(additive manufacturing) division has also achieved great success in the past

year, culminating with a mutually exclusive partnership agreement with Aubert

& Duval, a subsidiary of the ERAMET Group with 2017 sales of approximately

$CDN 5.4 Billion and assets of approximately $CDN 4.9 billion. For over

100 years, Aubert & Duval has been a world leader in industrializing

high-performance steel, super alloy, aluminum and titanium alloys. More

specifically, they are a recognized supplier of metal powders for additive

manufacturing, serving the Aerospace, Energy, Transport, Medical, Defense,

Automotive and other large scale, demanding markets.

Just

recently, for the second year in a row, the company was nominated for materials

company of the year at the 3D printing awards.

Today,

PyroGenesis announced the spinout of its 3D printing division in order to

unlock value for shareholders and become more attractive to institutional

investors that are strictly focused on 3D printing. In addition, the

company believes that uplisting will also make both the new company and the

existing company more attractive to institutional investors that are precluded

from investing on junior exchanges.

We were

proud to sit down with CEO, Peter Pascali, and discuss all the benefits and

implications of this major development. Grab your favourite drink, sit

back and watch this great interview!

Posted by AGORACOM-JC

at 1:33 PM on Tuesday, April 16th, 2019

Board of Directors is moving forward with the previously announced spin-off of PyroGenesis Additive, a division specializing in developing, commercializing and advancing plasma-atomized metal powder for the additive manufacturing industry.

Additionally, the Company is also considering uplisting its stock to a more senior exchange. Â

MONTREAL, April 16, 2019 — PyroGenesis Canada Inc. (http://pyrogenesis.com) (TSX-V: PYR) (OTCQB: PYRNF) (FRA: 8PY), a high-tech company, (the “Company”, the “Corporation†or “PyroGenesis”) that designs, develops, manufactures and commercializes plasma atomized metal powder, plasma waste-to-energy systems and plasma torch products, today announced that the Board of Directors is moving forward with the previously announced spin-off of PyroGenesis Additive, a division specializing in developing, commercializing and advancing plasma-atomized metal powder for the additive manufacturing (“AMâ€) industry. Additionally, the Company is also considering uplisting its stock to a more senior exchange. Â

Mr. P. Peter Pascali, President and CEO of PyroGenesis, provides this

update on today’s announcements in the following Q&A format. The

questions, for the most part, are derived from inquiries received from

investors, and analysts:

Q. The spin-off of PyroGenesis Additive. It has been a long time in the making.

A. Indeed it has, and for some very good

reasons. The space has been rocked with change and we had to ensure that

our investors received maximum return from the spin-off, and at values

management felt were fair. I believe that there has been no better time

than now to move forward with the spin-off. These strategic delays have

effectively increased shareholder’s value.

Q. Could you explain those reasons to readers who are new to the story?

A. Most certainly.

Almost three years to the day, in the spring of 2016, we announced

our intention to spin-off our additive manufacturing capabilities to

maximize shareholder value and increase options to the Company. The

original idea was to consider a small concurrent financing to fund the

immediate need which was essentially to have a first system in place

producing powders.

Between the announcement and September 2016, while we were weighing

the options and various structures the spin-off could take, GE announced

that they had acquired Arcam and Concept Laser (both manufacturers of

printers which make metal 3D parts).

GE’s acquisitions arguably disrupted the supply chain of titanium

powders to the industry with the indirect acquisition of a subsidiary of

Arcam which had become the dominant supplier of such powder to the

space. It was imperative that we understood the impact of these

acquisitions on our decision to spin-off before we moved forward.

Once we understood the impact of the acquisition on the market, we

decided to postpone the spin-off until our first powder production

system was assembled which was only a few months away. We then waited

until the ramp up was completed. These delays removed any doubts, in the

marketplace, that we could produce quality powders, and as such,

increased the value of the spin-off to current investors.

Given the reception of our powder by the market (in 2018, we were

nominated Materials Company of the Year at the 3D Printing Industry

Awards, which speaks to how much we had accomplished in such a short

time), we felt we were close to a key contract and/or a significant

relationship, and decided to wait until one or the other was in hand.

In the summer of 2018, discussions took place with Aubert & Duval

which lead to the joint press release of January 8, 2019 describing a

mutually exclusive relationship with respect to the distribution of

PyroGenesis’ titanium powder to the AM industry in Europe.

Given what has taken place, and what we know now, management has made

a strategic decision to spin-off PyroGenesis Additive at this time.

Q. Why spin-off PyroGenesis Additive in the first place?

A. There are a number of reasons, but they all boil down to one goal: simplicity.

The reason to spin-off PyroGenesis Additive is primarily to attract

an investor base best suited to their unique value proposition,

particular business operations, and financial characteristics, thereby

maximizing shareholders’ value and placing it in a better position to

generate revenues and develop strategic relationships than had it

remained part of the PyroGenesis stable of technologies.

The simpler an offering is the easier it is for analysts to understand and value it properly. As

it stands now PyroGenesis Additive is part of PyroGenesis Canada Inc’s

offerings which include Drosrite™, US Military, and Purevap™, just to

name a few, and as such makes it complicated to analyze. Add to this

that analysts typically specialize in one sector or another, and as such

may very well be able to fully value PyroGenesis’ Additive’s offering,

but would be hard pressed to do equal justice to PyroGenesis’ other

business lines, and you have a significantly undervalued group of

assets. Spinning one group off would unlock this value.

Simplifying an offering would also make it easier to attract

investment. There are large pools of money interested in investing in

the AM space, but have no desire to have their funds comingled with

unrelated business lines. A spin-off would assure them that such funds

would be used for AM alone.

Last but not least, a spin-off creates a well understood entity with which interested parties could joint venture or acquire. Bottom line: a spin-off creates simplicity, which in and of itself, increases interest, all to the benefit of shareholders.

Q. Any challenges in a spin-off?

A. There are many, but the two that I think

are key are timing and structure. The timing and structure of a

spin-off is critical to its survivability. The spin-off must be done in

a context where it can grow and mature, not much different from a young

adult leaving home.

It is management’s firm belief that given recent announcements, and

what we anticipate taking place in the near term, spinning-off

PyroGenesis Additive is now overdue.

Q. Are there any other factors motivating your decision to spin-off PyroGenesis Additive at this particular time?

A. Yes. There is a huge interest by our

partners to spin-off PyroGenesis Additive for all the reasons given

above. This is a major factor in our decision to move forward now.

Q. You also announced today that you are considering an uplisting. Could you describe what this means?

A. The Company’s stock currently trades on

the TSX Venture Exchange (“TSX-Vâ€). Although a good exchange it does

have its limitations. It may be a good place for a company to list

initially but, in time, a company should consider moving to a bigger and

better exchange. By bigger and better I mean one which will attract

more interest and as such attract greater investment which by default

would translate into a higher stock price. This is a natural progression

and the TSX-V boasts of the number of companies that have uplisted from

their platform.

I think it would be more appropriate to say that we are considering

which exchange to uplist on, rather than considering an uplisting. It

has already been decided that we have to become listed on a more senior

exchange, sooner than later.

Q. What would be the timing and what are the next steps?

A. Both uplistings and spin-offs require

regulatory approval and depending on the type and number of questions

from the regulators, will determine the time it takes to complete.

Assuming nothing out of the ordinary, either one could take 4-6 months.

Next steps would be to engage a Canadian based law firm, which we are

in the process of doing, and to engage an investment bank. We are

currently receiving proposals from investment bankers on both sides of

the border.

Q. What could delay the process?

A. As I said the process requires

regulatory review and approvals. There could be delays associated with

this. Other than that, funds. The process requires capital to complete

although a large part of it is success based and back-ended.

Q. Assuming money is not an object, and that the

regulatory approval process is not unduly burdensome, when are you

targeting these events to be completed?

A. Both in 2019, this year, but failing that, one this year and the other by Q1, 2020.

Q. Do you care to add any concluding remarks?

A. Yes, I would.

There has been a flurry of developments within our PyroGenesis

Additive segment. We started the year by announcing a significant

agreement with a multi-billion-dollar European Company to market our

powders to Europe on a mutually exclusive basis. This was followed by

our unveiling of our NexGen™ Plasma Atomization process with production

rates that shattered all published plasma atomization production rates.

Next, we announced that we had shipped specialty powders to a

government entity which was quickly followed by the announcement that we

had successfully produced titanium powders with the NexGen™. During

this time, we were also nominated for the second year in a row as

Materials Company of the Year at the 3D Printing Industry Awards 2019.

There is a consensus building that such news belongs on a better

platform. Management concurs, and is taking the necessary steps.

PyroGenesis Canada Inc., a high-tech company, is the world leader in the design, development, manufacture and commercialization of advanced plasma processes and products. We provide engineering and manufacturing expertise, cutting-edge contract research, as well as turnkey process equipment packages to the defense, metallurgical, mining, advanced materials (including 3D printing), oil & gas, and environmental industries. With a team of experienced engineers, scientists and technicians working out of our Montreal office and our 3,800 m2 manufacturing facility, PyroGenesis maintains its competitive advantage by remaining at the forefront of technology development and commercialization. Our core competencies allow PyroGenesis to lead the way in providing innovative plasma torches, plasma waste processes, high-temperature metallurgical processes, and engineering services to the global marketplace. Our operations are ISO 9001:2015 certified, and have been since 1997. PyroGenesis is a publicly-traded Canadian Corporation on the TSX Venture Exchange (Ticker Symbol: PYR) and on the OTCQB Marketplace. For more information, please visit www.pyrogenesis.com

This press release contains certain forward-looking statements,

including, without limitation, statements containing the words “may”,

“plan”, “will”, “estimate”, “continue”, “anticipate”, “intend”,

“expect”, “in the process” and other similar expressions which

constitute “forward- looking information” within the meaning of

applicable securities laws. Forward-looking statements reflect the

Corporation’s current expectation and assumptions and are subject to a

number of risks and uncertainties that could cause actual results to

differ materially from those anticipated. These forward-looking

statements involve risks and uncertainties including, but not limited

to, our expectations regarding the acceptance of our products by the

market, our strategy to develop new products and enhance the

capabilities of existing products, our strategy with respect to research

and development, the impact of competitive products and pricing, new

product development, and uncertainties related to the regulatory

approval process. Such statements reflect the current views of the

Corporation with respect to future events and are subject to certain

risks and uncertainties and other risks detailed from time-to-time in

the Corporation’s ongoing filings with the securities regulatory

authorities, which filings can be found at www.sedar.com, or at www.otcmarkets.com. Actual

results, events, and performance may differ materially. Readers are

cautioned not to place undue reliance on these forward-looking

statements. The Corporation undertakes no obligation to publicly update

or revise any forward- looking statements either as a result of new

information, future events or otherwise, except as required by

applicable securities laws. Neither the TSX Venture Exchange, its

Regulation Services Provider (as that term is defined in the policies of

the TSX Venture Exchange) nor the OTCQB accepts responsibility for the

adequacy or accuracy of this press release.

Posted by AGORACOM-JC

at 9:00 PM on Monday, April 15th, 2019

SPONSOR: Esports Entertainment

$GMBL Esports audience is 350M, growing to 590M, Esports wagering is

projected at $23 BILLION by 2020. The company has launched VIE.gg

esports betting platform and has accelerated affiliate marketing

agreements with 190 Esports teams. Click here for more information

GMBL: OTCQB

———————–

HIVE Berlin: Jens Hilgers, Peter Warman Discuss Trends in Esports

Warman spoke about gatekeeping in the industry and the challenges of breaking in, and estimated that between himself and Hilgers, they have collectively taken more than 1,000 calls over the years from people who want to get into esports

At the HIVE esports business

conference in Berlin this week, influential minds from across the

industry gathered to discuss the future of esports. Before the

wide-ranging panels began, Jens Hilgers and Peter Warman took the stage

to explore some of the trends they’ve seen and expect to see in the

future.

Both are long-standing fixtures of the esports industry. Hilgers has spent more than two decades in esports, co-founding Turtle Entertainment and ESL

in 2000 and serving as its CEO until 2010, when he transitioned to the

role of chairman of the board until 2015. He has also co-founded G2 Esports and tools maker DOJO Madness , and is a founding partner in BITKRAFT Esports Ventures . Warman, meanwhile, is the CEO and founder of gaming and esports analytics firm Newzoo , which was established in 2007.

“Every single time that something like that has happened in history, it was the most important and most exciting times for me.â€

Warman spoke about gatekeeping in the

industry and the challenges of breaking in, and estimated that between

himself and Hilgers, they have collectively taken more than 1,000 calls

over the years from people who want to get into esports—whether it’s

startups, brands, media, or financial services. Carefully explaining the

industry to people who are outside of it is critical, although both

said that detailing the subject to government representatives is a less

enjoyable situation.

“You sometimes have to explain what

the hell is going on,†said Warman. Added Hilgers: “I try to avoid those

meetings… those are the most frustrating ones.â€

Many more people in recent years have

seen the boom around esports, said Warman, between the excitement

building around the industry and the money flowing into it. But

newcomers who think that esports is a completely new thing need to be

educated that it’s actually a long-running, gradually-maturing industry,

he said.

“We have to explain to people: this

esports thing—it’s been around for a long time,†said Warman. “It’s not

this ‘hockey stick’ expectation, new industry thing, but a very healthy

and growing business.â€

Amidst all of the excitement and

investment around the space, however, Warman and Hilgers both said that

people in the space need to manage expectations for incoming

stakeholders, in part to help avoid the possibility of a bubble. Warman

added that part of managing expectations is making it clear that the

rise of esports is not a standalone thing—that the underlying growth is

tied into the popularity gaming and other industries and technologies.

It’s also a matter of new generations growing up with gaming, esports,

and digital devices.

“You sometimes have to explain what the hell is going on.â€

“What I’ve been observing for the

last 23 years in my career,†said Hilgers, “is that when we see the

growth year-over-year in esports, it’s mostly driven by digital natives

growing up with video games and the paradigm of esports.â€

Looking back on his career to date,

Hilgers pointed to key games that have defined or redefined genres and

helped boost esports at that time. He noted the impact of Counter-Strike , World of Warcraft , and League of Legends in the past, and more recently Fortnite ,

as each raised the bar for its respective genre and the level of

competition and interest around it. If that kind of trend continues,

then Hilgers said that we could see another paradigm-shifting

competitive game in two to four years’ time that might draw even larger

numbers of players and viewers.

“Every single time that something

like that has happened in history, it was the most important and most

exciting times for me,†said Hilgers, “because these new, genre-defining

games truly elevated competitive multiplayer gaming and esports.â€

Warman pointed to the exponential

growth of both gaming and esports over the years compared to other types

of popular media. He said that the wider gaming industry’s evolving

focus on engaging fans, making them happy, and providing them free tools

before

expecting any kind of payment is helping to drive that. That’s seen

both with free-to-play games and freely-streamed esports tournaments and

related content.

“What makes us very special in games is we put time first before money,†he said. “That’s the secret sauce of our business.â€

“I think there’s going to be a generation of games going forward that

actually will start the design process by reflecting these assumptions

in the right way.â€

But there’s a fine line to walk, he

continued, as some people have more time than money, while others have

plenty of money and are willing to spend it within games. Creators in

both the game development and esports sides of the games industry need

to balance the accessibility on one end with premium features and

services on the other. “We are entertaining people who don’t want to

spend money or don’t have money, but have a lot of time,†said Warman.

“And people that have a shitload of money, and they will all spend it in

our game. One single environment has to serve both. Think about it:

that’s very, very hard.â€

Hilgers spoke about the impact of Fortnite

and how its success has come in part from breaking the mold of the

battle royale genre. It’s a competitive game, yes, but the colorful

experience is also more accessible and targeted at a less die-hard

audience. Games like Apex Legends, Call of Duty , and Overwatch have more of a hardcore fan base, he said, while some Fortnite players simply want to play casually and hang out with friends in the game. It has wide-ranging appeal.

When it comes to the next wave of

esports games, however, he said that developers need to consider the

viewing experience as much as the gameplay and moment-to-moment action.

“Having a game that is equally great to spectate and to watch as it is

to play the game will ultimately make for the best esports games,†said

Hilgers. He doesn’t believe that most games in the market now were built

with that kind of mentality, but that developers are learning lessons

from today’s games and their challenges, and that the next generation of

esports-ready titles will be better poised to deliver on both fronts.

“I think there’s going to be a

generation of games going forward that actually will start the design

process by reflecting these assumptions in the right way,†he said, “and

that will lead to a greater entertainment offering and elevate

esports.â€