Posted by AGORACOM-JC

at 3:12 PM on Friday, December 11th, 2020

Avicanna (AVCN: TSX) (AVCN: OTCQX) (0NN: FSE) is a vertically-integrated biopharmaceutical company developing and commercializing various cannabinoid-based products for the global marketplace.

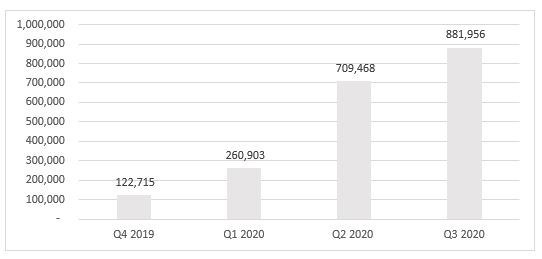

Third Quarter Highlights

$882K in revenue, an increase of 24% from Q2-2020,

Double-digit growth, quarter over quarter from Q4-2019

In addition, the Company was able to reach a major milestone with the launch of certain products from its RHO Phyto product line in Canada and further diversified its revenue streams.

When we say vertically integrated, we mean it. Avicanna has 4 fully operating divisions to address the entire market for Cannabis products as follows:

1. The company has a full line of high end CBD based skin care products serving the consumer retail segment with Canadian distribution through Medical Cannabis by Shoppers, as well as global distribution later this year.

2. Avicanna’s superior medical cannabis line also features products distributed through Medical Cannabis by Shoppers, the online arm of Canada’s largest drugstore chain.

Recently Launched Medical Cannabis Program with its RHO Phyto™ Formulary Nationwide in Colombia (Read More)

Leveraging thesuccessful launch ofthe Company’sRHO Phyto™brandedadvancedmedical cannabisproduct linein Canada,the portfolio of preparations,including oil drops, sublingual sprays, capsules and topicals,are nowavailablenationwide inColombia through physician prescription.

The medical programincludesAvicanna’s 3pillarsaimed at setting the gold standard for medical cannabis in Colombia andotherLatin American markets, including

3. Avicanna also hosts a full pipeline of Pharmaceuticals in various stages of trials to address Dermatology, Psychiatry, Neurology, Pain and Oncology. Three of the company’s products are already as far as phase 2.

Posted by AGORACOM

at 2:00 PM on Friday, December 11th, 2020

Beauce Gold Fields is focused on placer to hard rock exploration and discovery in the Beauce region of Southern Quebec. The the St-Simon-les-Mines Gold project is home to Canada’s first gold rush that pre-dates the Yukon Klondike that produced the largest gold nuggets in Canadian mining history (50oz to 71oz). Hosted along a 6 kilometer long placer channel, Beauce has identified a major Fault Line that coincides with an interpreted fault structure across the property. Evidence suggests the erosion of the Fault Line as a probable source of the historical placer gold channel. Click Here for More Info

If you are trying to find gold it helps to know where it came from.

To start with there is only one kind of gold. Placer gold and lode gold both come from the same place and are made of the same stuff. Gold is not actually formed on earth it was formed millions of years ago in distant stars. In large stars, much larger than our sun elements are combined together in their cores through the process of nuclear fusion. Our sun like all stars runs on fusion too but it does not have enough mass to produce atoms larger than carbon or oxygen. Larger stars can generate the gravitational force and heat in their cores necessary to produce elements as heavy as iron. To create things like gold even more energy is required and that takes place in a supernova.

When a large star runs out of light matter the fusion reaction is no longer sustainable and the star begins to collapse on itself very rapidly. The supernova collapse takes place in a matter of seconds. While the star is collapsing it produces heat very rapidly and explodes in what is essentially a humongous nuclear bomb. Supernova events are so bright and powerful that they are brighter than then entire galaxy that hosts the star. This nuclear explosion allows for higher energy fusion reactions that can produce heavy elements like gold. The explosion also scatters the newly created material over great distances.

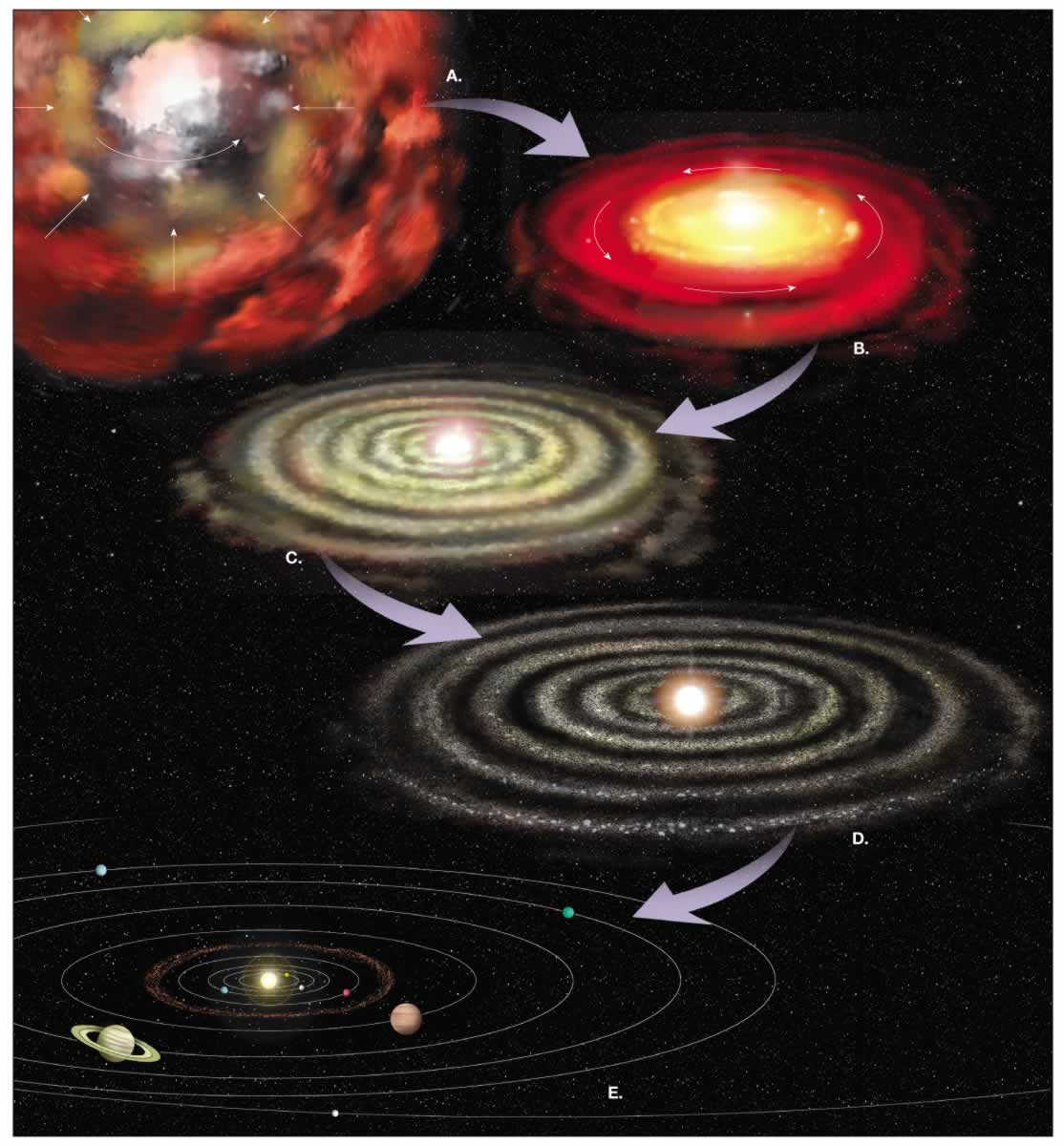

So how did the star dust make it into the mountains and rivers on earth? When our solar system began approximately 4.6 billion years ago it was a cloud of dust and gas called a nebula. This nebula was composed of the remains from older stars that had spread their guts around the universe in supernova explosions. The molecules of the nebula naturally pulled on each other by the force of gravity growing more and more dense. As the nebula was collapsing in on itself it also started to spin faster and faster. The condensing and spinning action formed the nebula into a disk, much like you spin dough into a pizza. In the center where the force of gravity is the strongest a new star was created, our sun. The swirling mass around the sun clumped together into the planets, moons, asteroid and comets that we see today.

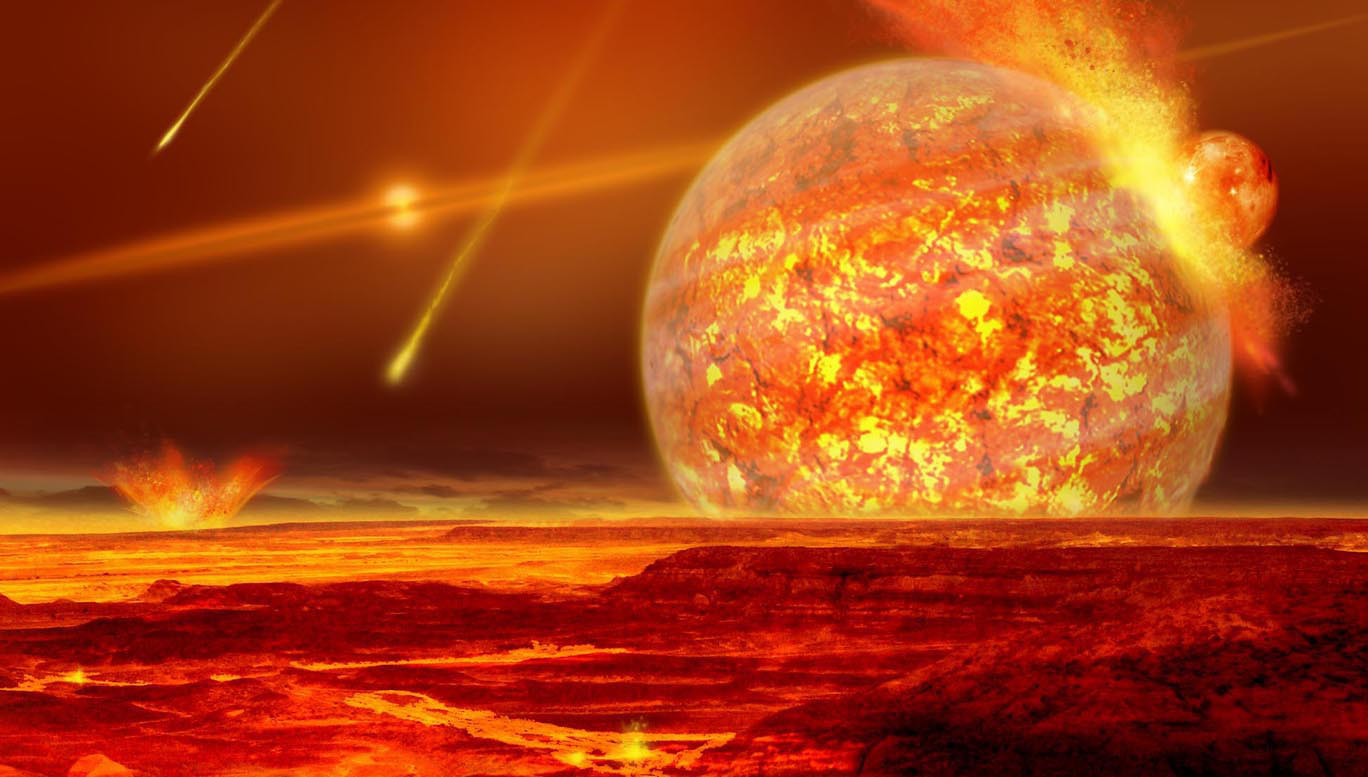

The early solar system was different that it is today. The big planets did not form all at once, it was a gradual process. Small plantoids formed first and crashed and coalesced into each other to form larger planets. In theory the distribution of gold was basically even in all the rocky material that made up the early solar system. In the early earth, while it was still completely molten the heavy material (such as iron and precious metals like gold) all sunk to the center of the planet to form the core. The process is similar to the way that dense material sinks to the bottom of your gold pan. If you could mine the core you would be very rich but it would be very difficult with current gold mining equipment. Current scientific theories estimate that there is enough gold in the core to cover the surface of the earth with a 4 meter thick layer of pure gold.

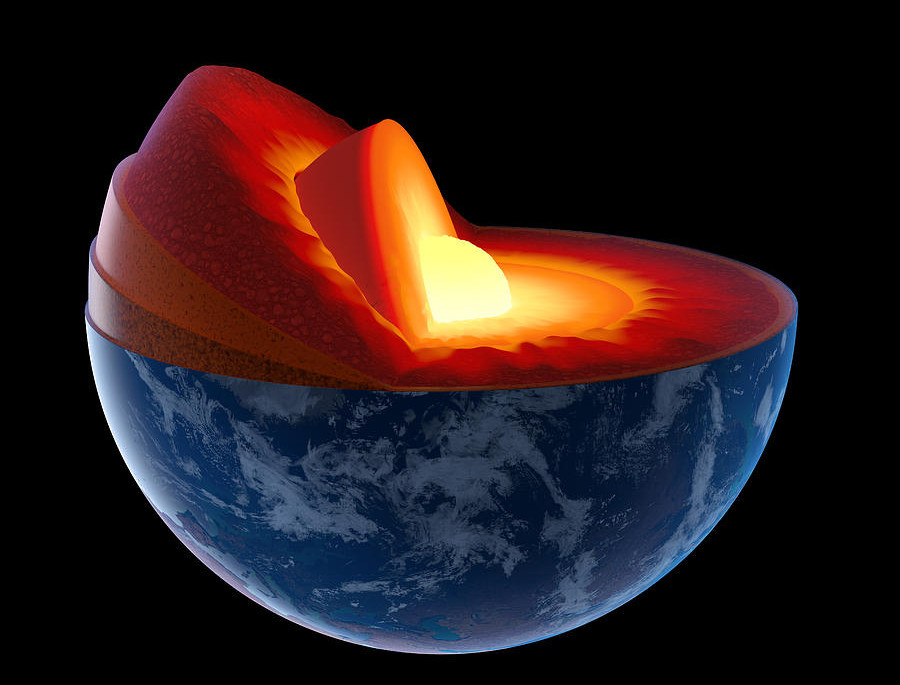

We can only reach gold that is trapped in the crust of the earth. The precious metals in the crust were put there by meteor bombardments that took place after the crust had formed. As these meteorites crashed into the surface of the earth they disintegrated and mixed their material into the upper mantle. The meteorite guts had the effect of enriching the amount of precious metals in the crust.

So we know where gold came from and how it was formed. Stay tuned for a future post to learn how the gold formed into deposits in the mountains and streams that we mine.

Posted by AGORACOM

at 1:47 PM on Friday, December 11th, 2020

Affinity Metals discusses rational for recently acquired Carscallen Extension property. The Carscallen Extension immediately adjoins the Melkior/Kirkland Lake Gold JV Carscallen Project located approximately 6 km west of Pan American Silver’s West Timmins Mine and approximately 25 KM West of Timmins. The company has recently announced the commencement of drilling on trend with the projected extension of the Shenkman-ZamZam gold system which has been the focus of the Melkior/Kirkland Lake Gold JV.

Posted by AGORACOM

at 1:30 PM on Friday, December 11th, 2020

SPONSOR: Thoughtful Brands is an established natural health products company focused in the CBD and psychedelic medicine sectors. Through their powerful eCommerce business Thoughtful is a leading direct-to-consumer provider of a wide range of natural health products throughout the United States and Europe. Click Here For More Info

Lawmakers took a step Monday to reduce penalties for possession of magic mushrooms, a criminal justice reform move that also brings them closer to passing a bill to guide the marijuana industry in New Jersey.

The Assembly Judiciary Committee voted 4-1 with one abstention to advance the bill (A5084). It does not decriminalize psilocybin, but makes possession of up to one ounce a disorderly persons offense rather than a third degree crime. That would drop penalties to a maximum of a $1,000 fine and six months in jail.

Currently, those convicted can face between three and five years in prison.

“It’s much simpler than what appears on the surface,” Assemblyman James Kennedy, D-Union, who sponsored the bill, said during Monday’s hearing. “This is really a downgrading of the charges.”

The move to legalize marijuana has been underway in New Jersey since 2014, but mushrooms only came up last month.

As lawmakers sought to pass a bill that would end arrests for up to six ounces of marijuana, Sen. Nicholas Scutari, D-Union, added a provision to downgrade penalties for psilocybin.

The measure passed the Senate by a vote of 29-4, but the Assembly did not put the amended bill for a full floor vote. The mushrooms came unexpectedly and took away from bill’s goal of ending tens of thousands of annual marijuana arrests that disproportionately involve minorities, some said.

Last week, Kennedy introduced the new bill to separate magic mushrooms. That cleared the way for conversations to resume on both the marijuana decriminalization bill and the bill that will establish rules and regulations for the legal industry.

Lawmakers came to a compromise on the setting rules for a new marijuana industry late Friday, and plan to hold a full vote on the legislation on Dec. 17. The Senate will have to repass its decriminalization bill without the mushroom provision and move on its own version.

New Jersey is not the first state to reconsider its laws on psychedelic mushrooms.

Colorado voted to decriminalize mushrooms in 2019 and Oregon voted this November to legalize their use for medicinal purposes. Several cities in California as well as Washington, D.C., have moved to end arrests over mushroom possession.

Some studies show promising medical benefits of psilocybin to treat depression and anxiety, particularly in cancer patients or others with chronic illnesses, like HIV, Mathew Johnson, a professor of psychiatry at and behavioral sciences at Johns Hopkins Medicine, said during the hearing.

He also said psilocybin carries no risk of an overdose, and the greatest risk comes from people making poor choices while impaired, or from people with certain psychological issues like schizophrenia having adverse reactions.

“When you include it even amongst a large group of legal and illegal drugs…psilocybin mushrooms always falls towards the bottom of the rankings in terms of harms to self or harms to others,” he said.

Some lawmakers remained hesitant.

“I think the bill sends the message to young people in our state that the recreational use and misuse of these substances is really not that big a deal,” said Christopher P. DePhillips, R-Bergen, who voted no on the bill.

Those in favor reiterated that the bill would not legalize or decriminalize the use of psilocybin, but would carry a punishment that more closely fit the crime.

“We open up job opportunities to so many folks who may have done this as a one-off, and then suffered with a life-long third degree indictable conviction,” said Assemblyman Raj Mukherji, D-Hudson.

“I think that public policy will be better served by treating this as a criminal act, but as a disorderly persons offense,” he said.

Posted by AGORACOM

at 12:42 PM on Friday, December 11th, 2020

SPONSOR: Arctic Star Exploration is currently exploiting the Diagras Diamond Property, NWT. Adjoined by both Diavik and Ekati Mines, Arctic has combined known data on Diagras with modern Gravity and EM geophysical survey techniques to delineate viable Kimberlite targets. Arctic Star is currently preparing a drill program. CLICK HERE FOR MORE INFO

We have seen how the industry has undergone significant changes over the past 20 years and how smaller companies have emerged to play an increasingly important role in supplying rough diamonds to the world.

These changes have come about at least partly due to the discovery of diamonds in locations outside of Southern Africa, which was where the vast majority of diamonds had been mined for nearly a century. South Africa is also where De Beers established its dominance of the industry. The discovery of diamonds elsewhere in the world has therefore been a key factor in the diamond giant’s gradual decline in market share.

According to Kimberley Process rough diamond statistics, 22 countries produced rough diamonds in 2014. The top six producing countries accounted for over 90% of production by value. A closer analysis of global diamond mining is key to learning more about the industry’s recent evolution, and to developing an image of where it might be heading in the future.

To start, I will focus on the top six producing nations, each of whose policies and methods of distribution shape the industry.

Russia

Diamonds were first discovered in Russia in the mid 1950s in the Sakha (Yakutia) Republic in northeastern Siberia. Interestingly, the search for diamonds in Russia, which began in 1947 following the end of World War Two, was not initiated for financial gain. Stalin understood that in order to rebuild the shattered Soviet Union after the war, he would need access to a large supply of industrial diamonds. These diamonds were required for a number of mechanical operations such as drilling, abrasive grit, precision cutting and other digging processes. However, at the time, De Beers controlled the sale of rough diamonds and Stalin knew that this left him precariously dependent.

Russian geologists had recognized as early as the 1930s that parts of Siberia exhibited very similar geological characteristics to the kimberlite-rich regions of South Africa. Teams of geologists were dispatched to Siberia and these expeditions did not disappoint. In 1955, the Mirny (Mir) kimberlite was discovered and mining commenced in 1957.

The purpose of searching for diamonds in Russia was to develop a supply of industrial stones for tools and equipment. Thus, when Mir produced a vast supply of gem quality stones, the state found itself in the grips of an unexpected predicament. By the mid 1960s, Russia had begun selling its gem diamond production to De Beers, a relationship that would remain intact for more than 40 years.

Today Russia maintains more than a dozen active open-pit diamond mines and is the world’s number one producer of rough diamonds by value and by carat volume. Russia’s known diamond reserves have long been shrouded in mystery, but according to state-owned miner ALROSA, which controls the vast majority of diamond mining in the country, its reserves exceed one billion carats. This should allow the country to maintain its position as a dominant player in the industry for several decades to come.

Botswana

Botswana officially gained independence from the UK on September 30, 1966. The country’s first kimberlite was identified just five months later. This initial discovery was followed shortly by numerous others which quickly established the nation as a diamond powerhouse and helped to propel its population out of crushing poverty.

Botswanan diamonds truly took to the skies when it was determined that the AK1 mine, now Orapa, could be seen from the sky and was frequently used as a landmark by South African pilots navigating their way to Europe.

Today, Botswana ranks second only to Russia in rough diamond production by value, driven primarily by the two richest mines in the world – Orapa and Jwaneng. However, it is the country’s recent efforts to leverage its diamond resources to further benefit its people that has earned the attention of the diamond world.

In 2011, the Botswanan government and De Beers announced a landmark deal that would eventually see De Beers’ entire sorting and sales operations moved from London to Gaborone – the capital of Botswana. Also as part of the deal, the government was given the opportunity to market a portion of local production through its own subsidiary company, now known as Okavango Diamond Company. In this way, Botswana has a solid mechanism for understanding the change in market prices for its resources.

By all accounts, Botswana’s diamond revenues have been put to very good use in helping lift the country out of poverty. In the late 1960s, Botswana was one of the poorest countries in the world with a GDP per capita of around $70. Today it ranks among the top African countries for per capita GDP, and consistently ranks near the top among Africa countries in terms of literacy, education, health care and low-levels of government corruption.

The Botswanan government has embarked on a bold experiment to extract maximum benefit from its natural resources by establishing Botswana as a diamond trading and manufacturing hub, in order to achieve stability for after its resources are depleted. Other nations are taking notice, and the Botswana model may be looked to in the future more and more frequently.

Canada

Though Canada’s history as a diamond-producing nation is short, it is now the world’s third largest producer by value. In fact, diamond deposits have been found scattered across the country’s vast expanses, and it offers much promise for continued exploration and development. Two large diamond projects are set to go into production as soon as late 2016 and early 2017 – the Renard and Gahcho Que projects.

Diamonds were first discovered in Canada in the early 1990s by two geologists who resisted the conventional wisdom that local geology would not support a diamond find. The discovery of the Ekati Diamond Mine triggered one of the most intense prospecting rushes in North American history, bringing teams from all over the world to scour the area. Geologists were literally staking their claims with wooden posts, so much so that local lumber suppliers could not keep up with the demand for wood.

It is said that the team of geologists who discovered the Diavik Diamond Mine initially planned to stake out a different location, but had to “settle” for what they were given because the person ahead of them in line at the mineral claims office took the area they were first interested in.

Most of Canada’s diamond projects are clustered in the far reaches of the northern Arctic region known locally as the Barren Lands. These barely hospitable tundra experience winter temperatures that average -35 degrees Celsius, often dipping below -50. This makes mining a challenge and the mining camps in these regions function more like enclosed cities, almost entirely sheltered from the harsh weather outside.

This region is also known for having been carved from the glacial movements of the last ice age. There are so many lakes in the area, numbering in the tens of thousands, that many remain unnamed to this day. In fact, some of the country’s most prolific diamond deposits have been found located beneath lakes. The Diavik Diamond Mine, located underneath 56 meters of water in Lac De Gras, necessitated the construction of a massive retaining wall and the removal of millions of liters of water to access the high-value kimberlite underneath the lake-bed.

Angola

Diamonds were first discovered in Angola’s Lunda Norte province near the border with Zaire in 1913. Angola is rich in both kimberlite deposits and alluvial diamonds washed out from their kimberlite hosts by ancient river systems.

The country has suffered from political instability for decades after gaining independence from Portugal in 1975. Shortly afterwards gaining independence, a civil war erupted that would last more than 25 years. As a result, large mining companies have been somewhat reluctant to invest in mining in Angola, and the country is believed to possess significant diamond resources that remain undiscovered.

In 2011, Angola introduced new legislation aimed at attracting foreign investment into its diamonds sector to help boost production. The plan has shown some early results. In 2015, ALROSA announced that it would invest $1.2 billion into the country to further develop producing assets and to increase exploration work in the country.

Keeping pace with the recent string of large diamond discoveries around the world, Australia-based Lucapa Diamonds announced in February that it had unearthed the 27th largest diamond ever from its Lulu mine in Angola. The gem was sold recently for $16 million.

South Africa

For decades South Africa was the epicenter of diamond mining. The discovery of the Eureka Diamond in 1866 by a young farmer named Erasmus Jacobs set off a prospecting rush unparalleled at that time. In a few short years, numerous alluvial and kimberlite operations were established. This new supply helped to replace the dwindling supplies from Brazil and India, and make diamonds accessible to vastly more people than ever before.

While South Africa still has more than ten producing diamond mines, its importance in the diamond world is slowly declining. Many mines have reached the end of their lifecycle and have moved to underground mining, which is often slow and more expensive than mining in an open pit. Although South Africa is still the fifth largest producer of diamonds in the world, with value in excess of $1 billion annually, in the absence of a major new mine discovery its importance will decline significantly over the coming decade.

Namibia

At number six in the diamond producing nations rankings, Namibia boasts the highest value per carat diamonds in the world. Namibian diamonds are mostly found in the ocean, along the country’s 1,570 kilometer coastline. Over millions of years, the area became a drainage basin covering the Kaapvaal Craton, which emptied water into the Atlantic Ocean. This water eroded diamond-bearing kimberlites and transported diamonds into the ocean. Over time, ocean currents churned up the area and deposited the diamonds in seabed trap sites as well as inland along the coast.

Because these diamonds travelled huge distances, often in rough conditions, only the strongest diamonds survived the journey. As a result, Namibian diamonds have exhibit the highest proportion of gem quality stones anywhere in the world, and this results in a very high average value per carat. These diamonds are mined mostly from boats and barges that drill and extract material from the seabed through long hoses.

Diamond production by country has changed significantly in recent years and this has had important implications on the industry and the power of companies within it. Next week I will look at some of the smaller producing nations, some of which are on the rise while others are in decline.

The views expressed here are solely those of the author in his private capacity. No one should act upon any opinion or information in this website without consulting a professional qualified adviser.

Posted by AGORACOM-JC

at 11:06 AM on Friday, December 11th, 2020

Peter Pascali, Chief Executive Officer & Chair, PyroGenesis Canada Inc. (TSX: PYR) and his team joined Berk Sumen, Head, Company Services, TMX Group, to celebrate the Company’s graduation from TSX Venture Exchange to Toronto Stock Exchange and open the market.

Posted by AGORACOM-JC

at 7:38 AM on Friday, December 11th, 2020

Announced that its Gold River and Cubeler Lending Hub platforms are now ready to support China’s new Digital Currency Electronic Payment (DC/EP).

Unlike cryptocurrencies such as Bitcoin, China’s DC/EP is legal tender, it’s backed by yuan deposits, centralized and not anonymous.

It is managed by China’s Central Bank, which requires the country’s banks to convert a part of their yuan holdings into DC/EP form and distribute them to businesses and citizens via mobile technology.

The DC/EP took over five years to develop and is expected to help bring China’s unbanked population into the mainstream economy and accelerate the country’s move to a cashless society.

Montreal, Quebec–(December 11, 2020) – Peak Fintech Group Inc. (CSE: PKK) (OTCQX: PKKFF) (“Peak” or the “Company”), an innovative Fintech service provider to the Chinese commercial lending sector, today announced that its Gold River and Cubeler Lending Hub platforms are now ready to support China’s new Digital Currency Electronic Payment (DC/EP).

Unlike cryptocurrencies such as Bitcoin, China’s DC/EP is legal tender, it’s backed by yuan deposits, centralized and not anonymous. It is managed by China’s Central Bank, which requires the country’s banks to convert a part of their yuan holdings into DC/EP form and distribute them to businesses and citizens via mobile technology. The DC/EP took over five years to develop and is expected to help bring China’s unbanked population into the mainstream economy and accelerate the country’s move to a cashless society.

Peak began preparing its platforms for the DC/EP last month with the hiring of former People’s Bank of China senior manager, Mr. Wenjun Wu, as a special advisor to assist the Company in that capacity. Through Mr. Wu’s expertise in the matter and his relationship with the Postal Savings Bank of China (http://www.psbc.com/en/), one of a select few banks with the DC/EP API, Peak’s platforms are now among the first to provide clients with the ability to conduct DC/EP transactions. In addition to its inherent security features, the DC/EP offers several benefits to businesses and financial institutions alike. For instance, loans and credit transactions conducted in DC/EP will on average carry lower interest rates than similar transactions conducted in regular yuan and transactions will be settled instantly, all of which are expected to make DC/EP transactions the preferred way of conducting business in China, and a way to increase transaction volume on Peak’s platforms. The Company plans to run a pilot project beginning later this month with a few supply-chain financing related transactions before making the feature available to all Gold River and Lending Hub clients.

Peak’s DC/EP pilot project will coincide with the arrival of Xingcheng Special Steel Works Ltd. (“XSSW”) (https://xctg.citicsteel.com/) to the Cubeler Lending Hub Ecosystem. XSSW is a subsidiary of conglomerate CITIC Ltd. (https://www.citic.com/en/). It’s the 2nd largest supplier of specialized steel products in China servicing a variety of industries and manufacturers with products such as bearings, alloy steel wires, plates, rods and springs that go into the making of numerous products. Peak and XSSW were connected through the Jiangyin Financial Centre following a series of financing requests from Jiangyin manufacturers to purchase material from XSSW. By officially adding XSSW to Lending Hub’s list of approved suppliers and working in partnership with XSSW, Peak will now be able to offer its supply-chain financing services to all XSSW clients through joint marketing initiatives.

Wall Street Reporter’s NEXT SUPER STOCK Livestream – December 15, 2020

Peak will be a featured presenter at Wall Street Reporter’s NEXT SUPER STOCK livestream conference on Tuesday, December 15, 2020 at 1:00pm EST. CEO Johnson Joseph will discuss Peak’s latest news events and answer investor audience questions. Those interested can click the following link to register and join the livestream: Next Super Stock Livestream Registration.

About Peak Fintech Group Inc.:

Peak Fintech Group Inc. is the parent company of a group of innovative financial technology (Fintech) subsidiaries operating in China’s commercial lending industry. Peak’s subsidiaries use technology, analytics and artificial intelligence to create an ecosystem of lenders, borrowers and other participants in China’s commercial lending space where lending operations are conducted rapidly, safely, efficiently and with the utmost transparency. For more information: http://www.peakfintechgroup.com

For more information, please contact:

CHF Capital Markets Cathy Hume, CEO 416-868-1079 ext.: 251 [email protected]

Peak Fintech Group Inc. Johnson Joseph, President and CEO 514-340-7775 ext.: 501 [email protected]

This news release may include certain forward-looking information, including statements relating to business and operating strategies, plans and prospects for revenue growth, using words including “anticipate”, “believe”, “could”, “expect”, “intend”, “may”, “plan”, “potential”, “project”, “seek”, “should”, “will”, “would” and similar expressions, which are intended to identify a number of these forward-looking statements. Forward-looking information reflects current views with respect to current events and is not a guarantee of future performance and is subject to risks, uncertainties and assumptions. The Company undertakes no obligation to publicly update or review any forward-looking information contained in this news release, except as may be required by applicable laws, rules and regulations. Readers are urged to consider these factors carefully in evaluating any forward-looking information.

Posted by AGORACOM-JC

at 7:26 PM on Thursday, December 10th, 2020

Datamerex (DM:TSXV) has the rare benefit that most small cap companies would only dream of …. 2 successful independent divisions that are each capable of being a company maker.

The first division is their Artificial Intelligence driven social media monitoring and discovery product … and this isn’t some basic social media monitoring tool for keywords. Clients include Canadian Federal Government, DRDC, Health Canada, United States Air Force and LOTTE (a $2.6B South Korean multinational conglomerate.

As a result of the highest level security clearances required to do this level of work, Datametrex was well positioned with deep roots in South Korea to add their second, though unintended division of COVID-19 test kit distribution. Again, this isn’t some small cap stretch trying to capitalize on a trend for the sake of stock promotion. Rather, when the Canadian Government came calling for assistance in importing and distributing COVID-19 test kits, Datametrex stepped up to the task thanks to its security clearances already in place in both countries.

Since then, the company has signed multiple multi-million dollar COVID-19 test kit supply agreements with mining companies, a $20M CAD agreement with the television and film industry and various educational institutions.

As a result, Datametrex has had its’ best year ever in the first 3 quarters of 2020 as follows:

Record revenue of $7.6 million for the nine-month 2020 period compared to $2.6 in 2019

Record revenue of $4.9 million was generated in Q3

First ever positive EBIDTA quarter

Watch this powerful interview with CEO Marshall Gunter to discuss the year that was … and why he’s so optimistic about 2021.

Posted by AGORACOM-JC

at 6:20 PM on Thursday, December 10th, 2020

Announced that it has received interest for up to $2 Million of units pursuant to a non-brokered financing, which will close prior to the unrelated, best efforts brokered private placement of units which the Company previously announced on December 7, 2020.

The gross proceeds of these unrelated offerings together will be up to $3.15 Million. The Units in each of the Brokered Offering and Non-Brokered Offering are being offered at $0.15 per Unit, with each Unit comprised of one common share of the Company and one Common Share purchase warrant

Each Warrant shall be exercisable to acquire one Common Share at an exercise price of $0.20 per Warrant Share for a period of 24 months from the applicable closing.

TORONTO, ON / December 10, 2020 /KABN Systems NA Holdings Corp. (CSE:KABN) (the “Company” or “KABN North America” or “KABN NA“), a Canadian Fintech company that specializes in continuous online identity verification, management and monetization in Canada and the U.S., is pleased to announce that it has received interest for up to $2 Million of units (“Units“) pursuant to a non-brokered financing (the “Non-Brokered Offering“), which will close prior to the unrelated, best efforts brokered private placement (“Brokered Offering“) of units which the Company previously announced on December 7, 2020. The gross proceeds of these unrelated offerings together will be up to $3.15 Million. The Units in each of the Brokered Offering and Non-Brokered Offering are being offered at $0.15 per Unit, with each Unit comprised of one common share of the Company (a “Common Share“) and one Common Share purchase warrant (a “Warrant“). Each Warrant shall be exercisable to acquire one Common Share (a “Warrant Share“) at an exercise price of $0.20 per Warrant Share for a period of 24 months from the applicable closing.

The Brokered Offering is expected to close on or about December 29, 2020, or on such earlier date as agreed upon between the Company and Agent, and the Non-Brokered Offering is expected to close on or about December 21, 2020, or on such earlier date as the Company determines, and each is subject to certain conditions, including receipt of subscription agreements and payment of the subscription amounts by subscribers. The Units to be issued will have a hold period of four months and one day from the applicable closing.

The securities described herein have not been, and will not be, registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act“), or any state securities laws, and accordingly, may not be offered or sold within the United States except in compliance with the registration requirements of the U.S. Securities Act and applicable state securities requirements or pursuant to exemptions therefrom. This press release does not constitute an offer to sell or a solicitation to buy any securities in any jurisdiction.

About KABN North America KABN Systems NA Holdings Corp. through its wholly owned subsidiary KABN Systems North America Inc. focuses on the verification, management and monetization of digital identity, empowering users to control and benefit from the use of their online identity. KABN NA’s propriety technology suite includes 4 key products:

Liquid Avatarallows users to create high quality digital icons representing their online personas. These icons, in conjunction with KABN ID, allow users to manage and control their Self Sovereign Identity and to use Liquid Avatars to share verifiable credentials, including access, identity and designation credentials, and public and permission based private data when they want and with whom they want.

KABN ID is an Always On, biometric and blockchain based digital identity validation and verification platform allowing users to continuously and confidently prove themselves throughout the online community.

KABN Card is a Visa approved prepaid card program allowing users to manage both digital and fiat currencies and earn cashback and other loyalty incentives.

KABN KASHis a cashback, loyalty and engagement program that powers the KABN NA’s revenue ecosystem. KABN NA provides its products and services at no cost to consumers and generates revenues through permission-based partner programs.

KABN Systems NA Holding Corp. is a publicly listed company listed on the Canadian Securities Exchange under the symbol “KABN.”

For further information, please contact: David Lucatch 647-725-7742 Ext. 701 [email protected]

The CSE has not reviewed and does not accept responsibility for the adequacy or accuracy of this release.

This news release does not constitute an offer to sell, or a solicitation of an offer to buy, any securities under the KABN Financing in the United States. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”) or any state securities laws and may not be offered or sold within the United States or to U.S. Persons unless registered under the U.S. Securities Act and applicable state securities laws or an exemption from such registration is available.

Forward-Looking Information and Statements This press release contains certain “forward-looking information” within the meaning of applicable Canadian securities legislation and may also contain statements that may constitute “forward-looking statements” within the meaning of the safe harbor provisions of the United States Private Securities Litigation Reform Act of 1995. Such forward-looking information and forward-looking statements are not representative of historical facts or information or current condition, but instead represent only the Company’s beliefs regarding future events, plans or objectives, many of which, by their nature, are inherently uncertain and outside of the Company’s control. Generally, such forward-looking information or forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or may contain statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “will continue”, “will occur” or “will be achieved”. The forward-looking information and forward-looking statements contained herein includes statements regarding the anticipated proceeds of the Non-Brokered Offering and Brokered Offering, the closing date of each of the Non-Brokered Offering and Brokered Offering and statements that suggest that the Non-Brokered Offering and Brokered Offering will be completed and may include, but is not limited to, information concerning the ability of the Company to generate revenues, roll out new programs and to successfully achieve business objectives, including to accelerate the Company’s development, customer acquisition and business platform, and expectations for other economic, business, and/or competitive factors.

By identifying such information and statements in this manner, the Company is alerting the reader that such information and statements are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such information and statements. In addition, in connection with the forward-looking information and forward-looking statements contained in this press release, the Company has made certain assumptions. Among the key factors that could cause actual results to differ materially from those projected in the forward-looking information and statements are the following: changes in general economic, business and political conditions, including changes in the financial markets; changes in applicable laws; compliance with extensive government regulation. Should one or more of these risks, uncertainties or other factors materialize, or should assumptions underlying the forward-looking information or statements prove incorrect, actual results may vary materially from those described herein as intended, planned, anticipated, believed, estimated or expected.

Although the Company believes that the assumptions and factors used in preparing, and the expectations contained in, the forward-looking information and statements are reasonable, undue reliance should not be placed on such information and statements, and no assurance or guarantee can be given that such forward-looking information and statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information and statements. The forward-looking information and forward-looking statements contained in this press release are made as of the date of this press release, and the Company does not undertake to update any forward-looking information and/or forward-looking statements that are contained or referenced herein, except in accordance with applicable securities laws.

Posted by AGORACOM-JC

at 4:02 PM on Thursday, December 10th, 2020

Kontrol Energy (KNR:CSE) (KNRLF:OTCQB) is the Google NEST of smart building technology, with the Blue Chip client base to prove it. As such, when COVID-19 started shutting down buildings, arenas and complexes, their announcement the Receipt Of Positive Lab Results for Live COVID-19 Testing was taken very seriously by the investment community, with the stock smashing through to all-time highs and consolidating nicely in the $3.50 range.

Much of that consolidation came as a result of “impatient investors” who unrealistically demanded immediate and big sales agreements for the BioCloud unit, priced at $US 12,000 EACH. But KNR CEO Paul Ghezzi and his team know that real success comes from building a real foundation – and they did that in a mind boggling 3 months. We’ve been in the smallcap business long enough to know that pulling off the following in 3 months is damn near impossible, until now:

DISTRIBUTION – On December 1, 2020 KNR announced Entering into Exclusive Distribution Agreement with United Safety and Survivability Corporation for BioCloud Technology Distribution in North America, Australia and New Zealand. The exclusivity applies to the industries defined as buses, rail and locomotive, subways, ambulances, fire trucks, first responder and military vehicles, with applicable associated facilities in the geography of North America , Australia , and New Zealand . The exclusivity period is 12 months with a six month mutual renewal option and is based on 5,000 units of BioCloud per annum, on a best efforts basis, to retain exclusivity. Pricing will not be disclosed for industry competitive purposes.

In addition, KNR has also entered into two non-exclusive BioCloud distribution agreements covering Ontario and Saskatchewan.

MANUFACTURING – KNR has engaged OES Inc. a local design and contract manufacturer in London, Ontario to produce the BioCloud units. OES Inc. has a long and established history of assisting with the design and manufacturing of complex technology. Initial maximum capacity has been set at 10,000 units per month.

With all its ducks lined up and ready, CEO Paul Ghezzi says Kontrol is now well positioned for commercialization and believes 2021 is going to provide investors what they have long been waiting for. Well, at least those investors that didn’t think 3 months was an unreasonable amount of time do all of this in. Everybody else will just have to wait to see BioCloud in a building near them and wonder what could have been.

Watch or listen to this powerful interview with Kontrol Energy CEO, Paul Ghezzi.