Posted by AGORACOM

at 11:30 AM on Friday, May 8th, 2020

PONSOR: Mota is seeking to become a vertically integrated global CBD brand. Mota is creating sales channels and a distribution network internationally through the acquisition of the Sativida and First Class CBD brands. Low cost production, coupled with international, direct to customer sales channels will provide the foundation for the success of Mota. Combined total sales of almost $29,000,000 with a EBITDA of approximately 12.5% (2019) Click Here for More Info

With time ticking down for CBD manufacturers to meet the UK’s deadline for having a validated EU novel food application in hand, two European hemp associations are pooling resources to meet the application’s requirements.

The assistance on offer from the European Industrial Hemp Association in Germany and the Association for the Cannabinoid Industry in the UK highlights the urgency with which suppliers and processors need to move if they hope to be selling cannabidiol supplements and foodstuffs on the British market early next year.

That’s because the UK’s Food Standards Agency (FSA) set a deadline of March 31, 2021, for industry players to gather data on their CBD products and have their novel food applications validated by EU authorities.

The legality of CBD products in the European Union became murky in January 2019, when EU authorities classified all hemp extracts and hemp-derived products containing CBD and other cannabinoids as “novel foods.â€

The designation means that manufacturers need to have their CBD supplements and edible products evaluated and seek permission from EU authorities to place them on the market.

EIHA

European Industrial Hemp Association members agreed last year to submit a joint novel foods application with “a range of CBD extracts†to UK and EU authorities. The group said in February it was receiving membership applications “on almost a daily basis†from interested parties.

This week, the EIHA confirmed a report that revealed the scope and costs associated with its joint novel foods application. The association told Hemp Industry Daily:

An EIHA task force is in the process of choosing four formulations of CBD to be consolidated into one novel food application. The formulations will be finalized at the EIHA general meeting in June.

The joint application project, organized as a limited liability company, will cost at least €2 million ($2.16 million). The EIHA estimates that the required lab analysis of CBD and THC toxicology studies alone will cost €1.8 million ($1.94 million).

The group plans to launch the toxicology studies in June.

The cost of joining the consortium is estimated at €10,000 to €50,000 ($10,800 to $54,000), depending on the size of the company and when it joins. Regular EIHA members will be asked to pay the consortium cost in two installments, with the first next month.

This one-time cost comes in addition to the cost of a regular EIHA membership, which ranges from €2,500 to €10,000 ($2,700 to $10,800), depending on company revenue.

All companies that join the EIHA are obliged to join the novel foods consortium.

The association declined to say how much of the necessary funding for lab tests and toxicology evaluations has been raised so far.

Lorenza Romanese, managing director at the EIHA, said companies outside the European Union can join its novel foods consortium and would be eligible to sell products on the EU market if the joint application achieves authorization.

ACI

The UK’s Association for the Cannabinoid Industry announced this week a free hotline for CBD manufacturers with questions about the novel food application process.

The group also offers paid consulting services for individual applications.

The ACI’s approach pools resources for the data-generation phase while taking an individualized approach for each company’s application. The effort aims to help companies get the research they need, said Shomi Malik, ACI’s development director.

“The most expensive part of this isn’t writing the dossier, it’s generating the data,†Malik said.

“The best of both worlds is to share the costs of the real heavy lifting but still give companies the freedom to do their own individual applications. That’s what we’re trying to do here.â€

The ACI estimates that the cost for the toxicology study alone – the portion it’s looking to syndicate – will cost around £250,000 ($309,000). A full toxicology assessment takes seven to eight months to complete, ACI said, followed by an extra month to generate the data report.

The group said its application consulting services could cost anywhere from €50,000 to €500,000 ($54,000 to $540,000), depending on the size of the company and the number of finished products requiring novel foods authorization.

Malik applauded the EIHA for its collective application option, which he said might appeal to CBD players who haven’t budgeted the financial resources required for an individual application.

“Now that ‘novel foods’ is a binary proposition – you’re either in or you’re out – companies have had to find budgets from somewhere,†he said. “Their objective is to do this the quickest and cheapest way possible.â€

On the other hand, in the event that a collective novel foods application is authorized, parties to the application run the risk of finding themselves in a “regulatory straitjacket†not to deviate from those formulations. This could hinder industry innovation, Malik said.

“You’re in a much better position if you’ve got your own novel food authorization, than if you have to share and compromise with some aspects on the data sharing,†Malik said.

Clock is ticking

Whichever path companies choose, it’s time to start the process for any products they want to keep on the shelves next year, said Garrett Graff, an attorney at Hoban Law Group who advises companies doing business in Europe and the UK.

“It’s important that folks get started now,†Graff told Hemp Industry Daily.

“This is not a commonplace application that takes a couple hours. This will take considerable amounts of planning, coordination, time and financial resources to complete, and engaging as quickly as possible given the forthcoming deadline is important.â€

Posted by AGORACOM

at 10:27 AM on Friday, May 8th, 2020

Sponsor: Loncor, a Canadian gold explorer controlling over 3.6 million high grade ounces outside of a Barrick JV. The Ngayu JV property is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 814,000 ounces of gold in 2019. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting their Tier One investment criteria. Newmont $NGT$NEM owns 7.8%, Resolute $RSG owns 27% Management owns 29% Click Here for More Info

Concerns about the health of the global economy due to the coronavirus pandemic have boosted ‘safe-haven’ gold by 12%

Barrick Gold Corp posted a nearly 55 per cent rise in quarterly profit on Wednesday as gold prices surged, bolstering its ability to snap up mines including in copper, its chief executive said.

Concerns about the health of the global economy due to the coronavirus pandemic have boosted “safe-haven†gold by 12 per cent so far this year, while copper, seen as a bellwether for economic health, is down about 15 per cent.

Barrick CEO Mark Bristow has previously said the world’s No. 2 gold miner could raise its exposure in copper because of its expected higher use in electrification.

He added on Wednesday the relative price performance between copper and gold made deals more attractive.

“(A stronger balance sheet) improves our capacity to take up opportunities that might arise in the short to medium term given the dynamic nature of the global economy,†Bristow told Reuters.

He did not elaborate, but has expressed an interest in acquiring Freeport-McMoran Inc’s flagship Grasberg mine.

Barrick, which maintained its quarterly dividend of 7 cents per share, trimmed its annual production forecast for gold after shutting its mine in Papua New Guinea.

The Canadian miner now expects attributable gold production of 4.6-5.0 million ounces versus 4.8-5.2 million previously.

The government of Papua New Guinea announced in April it would not renew a 20-year special mining lease for the Porgera gold mine, which is jointly owned by Barrick and China’s Zijin Mining, due to environmental damage and social unrest.

Barrick (Niugini) Limited, the local venture in which both miners have a 47.5 per cent stake, had produced about 597,000 ounces of gold in 2019 from the Porgera mine.

Barrick has said it will contest the move, which it regards as “tantamount to nationalization without due process,†and in the meantime has placed Porgera on temporary care and maintenance, while suspending 2020 guidance for the mine.

Bristow said a mediator would be appointed to help negotiations if initial talks between the government and Barrick failed.

The company, with operations in North and South America and Africa, has not closed any of its mines due to coronavirus restrictions which have hit competitors.

Larger rival Newmont, which was forced to shutter some mines in Canada and South America, warned on Tuesday of a financial hit in the second quarter.

Barrick’s first quarter production fell 9 per cent to 1.25 million ounces. Excluding one-off items, Barrick reported a profit of 16 cents per share, in line with analyst estimates.

Posted by AGORACOM

at 10:02 AM on Friday, May 8th, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Recently acquired 14km of the potential extension of the new discovery by New Found Gold’s Queensway project to the south.Click Here for More Info

Gold Bullion Surges above March Lows

Gold Mining Equities Track Gold Higher

Gold Mining Equities vs. S&P 500 Show Convincing Breakout

Markets Recalibrate

Capital markets and society continue to recalibrate from the enormity of the fallout of the COVID-19 pandemic. As difficult as the current situation is, gold fundamentals continue to improve. Gold, as an investment, offers a hedge against the current financial turmoil and has significant capital appreciation potential in the years ahead.

The magnitude of central banks and government actions over the past several weeks will resonate for the rest of this decade. In our March commentary (March Roars in Like a Lion), we mentioned that we are now in the “end game” where debt explodes in the face of a financial calamity (although no one predicted that it would be a pandemic). We will discuss what near-term options the U.S. Federal Reserve (“Fed”) will likely implement, and how gold is likely to respond. We will also look at the recent move higher for gold mining equities.

Gold Bullion: Increased Demand for Physical Gold

Gold bullion ended April at $1,687, adding $109/oz, or +6.9% for the month. Gold began its surge in early April as physical delivery shortages resulted in gold futures (COMEX, New York) trading wildly higher than spot gold (London). COVID-19 has caused refining capacity for gold to decline and greatly restricted the transport of physical gold from London to New York. Typically, gold futures trade fairly tight with spot gold due to arbitrage, but in early April, the spreads spiked as high as $70/oz. The unprecedented fiscal and monetary policy response to the worst economic shock since the Great Depression has put gold squarely into investors’ minds.

Gold is almost always in contango (longer-dated contracts are more expensive than the near month). In April, parts of the gold futures curve traded in a rare backwardation (the near month contract is more expensive), usually indicative of a supply shortage. With the usual gold channels disrupted, futures are pulling spot prices higher as short positions are closed by going long futures. Compounding the disruption was the growing demand for gold in physical form, fueled by soaring investor buying interest. The unprecedented fiscal and monetary policy response to the worst economic shock since the Great Depression has put gold squarely into investors’ minds.

Figure 1. Gold Bullion Surges above March Lows Our short-term target is $1,800, and we expect to reach new all-time highs.

Source: Bloomberg. Data as of 4/30/2020.

Gold Mining Equities: Convincing Breakout in April

Gold equities broke out of a multi-year resistance level on massive buying flows. Using the NYSE Arca Gold Miners Index (GDM)5 as a reference, the 860 index resistance level was taken out convincingly. As shown in Figure 2, there is very little meaningful resistance until 1,200 (+25%). In March, gold equities, like bullion, experienced a forced liquidation event. Selling in GDX forced the ETF to trade at a significant discount to its underlying net asset value (NAV). Like many other ETFs, the selling volumes in GDX outpaced the liquidity in the underlying securities. Off the lows, the price action as measured by volume, breadth and money flow far exceeds the bullish thrust of the 2019 summer rally. This breakout, without question, is impressive on the technical measures.

Figure 2. Gold Mining Equities Track Gold Higher The NYSE Arca Gold Miners Index (GDM) has broken out of a broad base pattern; our short-term target is 1,200.

Source: Bloomberg. Data as of 4/30/2020.

The absolute price action is impressive, but when measured relative to the S&P 500 Index6 (Figure 3), the chart pattern looks even more impressive. Typically, new market leadership is more evident when measured against the broad market index. As shown in Figure 3, the NYSE Arca Gold Miners Index (GDM) relative to the S&P 500 Index has put in a very bullish bottom base pattern. There is a double bottom pattern set up with the right bottom shaping a head and shoulder breakout pattern. This bullish pattern within a bullish pattern is a very positive sign.

Figure 3. Gold Mining Equities vs. S&P 500 Show Convincing Breakout GDM is putting a remarkable long-term basing chart pattern and breaking out in the medium term.

Source: Bloomberg. Data as of 4/30/2020.

Increasing Revenue with Deflationary Input Costs

The gold mining industry, like many other industries, is experiencing disruptions due to pandemic shutdowns. But unlike other industries, gold producers are experiencing a steep increase in the selling price of its product. Gold bullion is up +11% year to date and up over +31% year-over-year (through April 30, 2020). From a cost perspective, energy and labor are typically the two highest cost components for miners. The dramatic fall in crude oil is a rare function of both a supply shock (the Organization of the Petroleum Exporting Countries [OPEC] price war) and a demand shock (pandemic shutdowns) co-occurring. The enormity of both events will have lasting price consequences well beyond a few quarters. Labor, the other component, has been devastated by the pandemic. A tremendous labor crisis is occurring globally. In the U.S. alone, jobless claims have now exceeded 30 million, a crushing toll. Both of these conditions are deflationary shockwaves that will ripple out to all corners of the economy. There is virtually no major cost component (reagents, consumables, equipment) that will not see lower costs. Though near-term gold company earnings may be volatile due to COVID-19 disruptions, the potential increase in long-term profit margins may be unlike anything seen in recent history, and most comparable to the 1930s when gold company revenues soared and costs plummeted.

As QE (quantitative easing) Infinity continues to expand and ZIRP (zero interest rate policy) takes hold in a likely recession (or depression), growth equities will become highly sought after. Gold mining equities will have one of, if not the highest growth in earnings of any industry. Because of the nature of its revenue product (gold bullion), and its input costs (deflation), gold equities will likely develop into a convexity trade. Relative to the broad market, gold mining equities have a more direct path to higher prices. In the absence of earnings and post liquidity lift, general market equities require QE to increase stock prices by suppressing the risk-free rate and credit spreads, thereby reducing the discount rate used to calculate the present value of cash flows. Currently, cash flows are near impossible to forecast. The broad market equity risk is if earnings do not recover for more than a year due to COVID-19 and/or if a risk event pushes up credit spreads (i.e., credit defaults). Both risks are quite high compared to the risk for gold mining equities.

The Likely Market Impact of the Fed Stimulus and Fiscal Policy Response

At the end of April, the Fed Balance Sheet had expanded to $6.66 trillion (previous high was $4.5 trillion) and will climb higher. The final number is unknown due to moving variables and the lack of visibility, but $10 trillion by summer is in the ballpark. The deficit for 2020 is estimated to be $3.7 trillion (18% to 20% of gross domestic product [GDP]), an all-time high with risk to the upside. The debt-to-GDP current expected range of 110% to 120% will probably prove to be too low despite being the highest ever. More billions of dollars, week by week, are being added to a dizzying array of Federal programs, credit facilities and swap lines to mitigate the damage of the pandemic.

The amount of debt is genuinely numbing in its size and scale and will keep growing. Long term, there is very little hope that the economy can grow out of this debt load. To manage this debt, we believe the Fed will need to implement three broad conditions: 1) negative real yields, longer and lower than previously expected; 2) yield curve control to maintain a flat and low rate structure, and 3) a weaker or capped U.S. dollar.

1) Negative Real Interest Rates

We have discussed numerous times the importance of negative real interest rates in reducing (debasing) the debt. The huge increase in debt levels and the likely lingering effects of COVID-19 on the global economy will assure that negative real interest rates will be here for years. There will be a persistent and growing erosion of wealth via negative real yields.

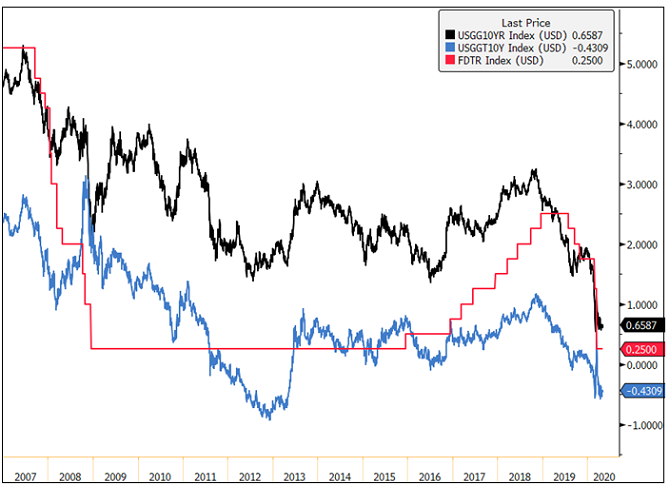

Figure 4. U.S. Real Yields Near Zero The Fed Funds target rate is 0.00-0.25%, and real yields are approximately -0.43%. Gold tends to thrive in low-interest rate environments. Source: Bloomberg. Data as of 5/5/2020. Nominal yields are measured by the USGG10YR Index, representing U.S. generic 10-year bond yields. Real yields are measured by USGGT10Y Index, representing U.S. 10-year TIPs (Treasury Inflation Protected) yields. The FDTR Index represents the Federal Funds Target Rate, which is set by the central bank in its efforts to influence short-term interest rates as part of its monetary policy strategy.

2) Yield Curve Control

Yield curve control was last used during World War II to finance the war. As the term implies, the U.S. government exerted control on both ends of the curve. Yields were capped with the short end lower than the long end. The long end was capped at around 2% irrespective of the economic condition. Controlled low yields provided a stable and manageable interest expense. By issuing more Treasuries in the short end, the government encouraged investors to borrow at the short end and to lend in the long end. Also, by issuing more at the short end of the curve, it ensured there was constant ample liquidity searching for yield. Today’s world is vastly different, but we expect to see a similar effort to control the yield curve. The Fed will continue to use QE Infinity to monetize the majority of bond issuances with an effort to keep rates as low as possible and the curve as flat as possible. For example, the $2.2 trillion of fiscal stimulus announced in March has already been monetized; 10-year Treasury yields are around 0.60% and the Fed Fund Rate is at zero.

3) Lower or Capped U.S. Dollar

We have also discussed the importance of a weaker U.S. dollar in previous commentaries. The impact of the global pandemic and the total collapse of crude oil pricing has elevated the importance of the U.S. dollar significantly. The sudden deceleration in global economic activity has dramatically reduced the flow of U.S. dollars. The U.S. dollar is the world’s reserve currency; about 60% to 70% of the world’s economic activity is transacted in U.S. dollars. Crude oil is one of the most critical sources of U.S. dollar liquidity. At year-end, an oil market of 100 Mb/d (million barrels a day) at $50 per barrel equated to $1.8 trillion of yearly U.S. dollar flows. Today, at 75 MB/d at $20 per barrel, crude oil-based U.S. dollar flows are now at $0.55 trillion. Now apply that to every industry that transacts globally, and the magnitude of U.S. dollar funding shortage becomes apparent.

There is an estimated $12 to $13 trillion of U.S. dollar-denominated debt held by foreign holders. The U.S. dollar is now the biggest financial short and there is a massive ongoing short squeeze as the global shutdown makes funding and servicing of this debt difficult. That the U.S. has launched trillions in fiscal and monetary stimulus, and the U.S. dollar has barely budged is an alarming sight. A runaway U.S. dollar in a financial and economic crisis coupled with a deflationary shockwave would be nothing short of a disaster scenario. In March, we had a small taste of what a U.S. dollar funding shortage and dollar hoarding had on global liquidity.

If the Fed has any chance of making this version of MMT (modern monetary theory) work, it will do everything in its power to keep the U.S. dollar in check and control a flat yield curve. Fighting the Fed’s efforts is this significant mismatch between U.S. dollar assets and liabilities. Historically, this has been the justification to devalue the dollar (or the prevailing reserve currency at the time) to bail out the world. Price regime changes typically occur with currency debasements. If we reach the point where the U.S. dollar stages a significant uncontrolled breakout higher, gold will spike as the market begins to price in the possibility of a reset of asset prices. At that point, gold would become the ultimate convexity trade for U.S. dollar debasement. Dollar debasement is a key tail risk in the end game.

Figure 5. The U.S. Dollar (DXY): Highs of March 2020 will be a Crucial Level

Source: Bloomberg. Data as of 4/30/2020.

A Realignment of Asset Classes

In just a few months, a global pandemic has caused a shutdown of the economy to an estimated tune of -25% annualized GDP for Q2, over 30 million U.S. workers filing jobless claims and trillions of dollars (and growing) added to the debt. Whether the news of the virus gets better or worse in the next few quarters, we will be in a ZIRP environment for years due to the debt level. With the Fed capping rates, yields will remain low and the curve flat whether the economic recovery is V-shaped, U, L, or any other alphabet shape (yield curve control). The economy will no longer determine the level of interest rates and the yield curve. The Fed will keep real interest rates negative; the only question is how negative? Investing in Treasuries has moved from a “return on capital” to a “return OF capital” proposition. Investing in Treasuries today is an erosion of wealth in real dollar terms.

The broader U.S. stock market has now recovered a significant part of its decline entirely due to the sheer amount of stimulus thrown by the Fed. To value the equity market today would require a look past a deep valley of uncertain duration, to the other side that may be changed entirely. As companies pull guidance due to the lack of visibility, equities can only rise mainly by never-ending liquidity. Equity valuations are already back to their all-time highs. Equity markets, like the bond market, will continue to decouple from the economy further.

Gold Makes Sense as Equity Volatility Increases

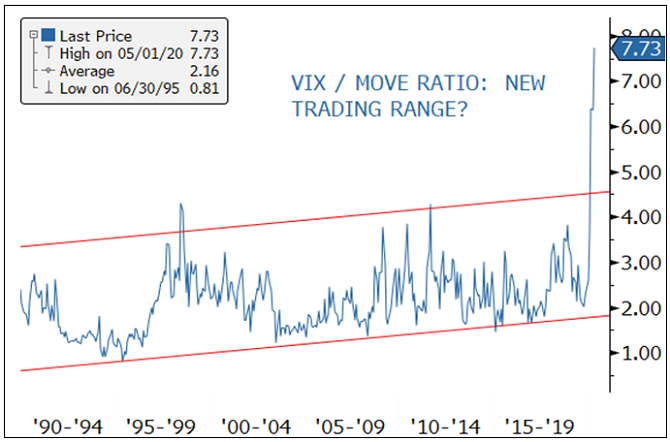

Moreover, if we are correct that the Fed’s main risk focus is containing the U.S. dollar and controlling the yield curve, equity risk (volatility) will trade higher vis-a-vis the U.S. dollar and bond prices than historical parameters (Figure 5). If this becomes the new reality, this repricing of volatility will have a dramatic effect on all asset classes. It will mean more effective equity hedges will be needed, such as gold. The one risk that the Fed cannot remove entirely is a tail risk event in which this current environment is a breeding ground.

Figure 6. Equity Risk Volatility is Trading Higher than Bond Volatility The VIX7 (CBOE Volatility Index for equities) has likely entered into a new trading range relative to the MOVE Index8 (Implied volatility of Treasuries across the yield curve) with far-reaching consequences.

Posted by AGORACOM-JC

at 6:12 PM on Thursday, May 7th, 2020

SPONSOR: Else Nutrition Holdings Inc. (TSX-V: BABY)The award winning, plant-based nutrition company for small cap investors. The company has a $10,000,000 cash balance for US product launch In Q2 2020 with International agreements in Q3. Learn More

My Search for the Healthiest Baby Formula

by Robin Barrie Kaiden, MS, RD, CDN

Robin Barrie Kaiden, MS, RD, CDN is renowned for helping people of all ages embrace a healthier lifestyle through nutrition and fitness counseling. As a Licensed Registered Dietitian and Personal Trainer, her smart and sensible approach to pediatrics, weight loss, sports nutrition, allergies, cardiovascular health, pre/post natal, and other areas of clinical and lifestyle nutrition has resonated with hundreds of people across the United States. Robin received her B.S. and M.S. degrees in Nutrition and Exercise Science from Cornell and Columbia Universities.

A Personal Note from this Pediatric Registered Dietitian and Mom

When I began working as a Registered Dietitian in Pediatric Nutrition over 15 years ago, we, of course, were taught, and shared with patients, that breast milk was the best, healthiest option for feeding babies. When that wasn’t possible, sufficient, or babies were being weaned, I knew that there were a variety of infant and toddler formulas available. We could recommend:

Pre-term infant formula: higher calories and minerals for infants born early

Standard term infant formula: intact milk protein

Gentle/sensitive formulas: whey protein in milk partially broken down

Soy-based formulas: for those with milk intolerance, noting that over 50% of infants who don’t tolerate dairy, also do not tolerate soy protein

Hydrolyzed formulas: proteins are mostly, but not completely broken down

Elemental formulas: proteins completely broken down for severe milk allergies

At this point in my career, I did not study the ingredients of each, but rather selected the best option available to best aid in tolerance, intake and growth for the child. There always seemed to be one that worked well…..at least well enough. The biggest problem with the hydrolyzed and elemental formulas was that they smelled and tasted terrible, and babies often refused to drink them.

Over 8 years ago, when I was pregnant with my first baby, I began to examine the healthiest baby formula options more in depth. I discovered that not much had changed in this industry, except that there were a couple of organic options. After discussing with a colleague, I decided on a formula. When my son was less than a week old, this product was recalled due to high arsenic levels. Plus, it seemed to upset his stomach. When my baby nurse suggested a non-organic, but “gentle†formula, I (reluctantly) agreed. I disliked that it had corn syrup (processed inflammatory sugar) as one of the main ingredients, but I was a new mom, overwhelmed, and figured she had so much experience and knew what she was talking about. Plus, my pediatrician agreed as well. A few weeks later, I just went back to the only other organic option on the market, and my son seemed to tolerate it well enough. It was the best I could find at that time.

When it came time to find the healthiest baby formula for my second child, almost 2.5 years later, I become aware that there were some European products that had better ingredients. However, it was pretty difficult and expensive to get these in the U.S. back then. I took comfort in the fact that my baby would be able to get great nutrition in the form of real food within about 4-5 months, and wean off formula totally at 1 year. But all I could think was that I would love to create a new healthy baby formula myself. Why hadn’t someone come up with a better alternative yet? Aren’t the infant and toddler stages the most important as they are developing and growing so rapidly? Why wouldn’t everyone want offer the best possible nutrients to this group, if/when/after breast milk was not an option.

My children are now in elementary school and the infant/toddler formula industry is still, in my opinion extremely limited. I was thrilled to hear about Else Nutrition, and flattered to consult on their timely products. Formulation of plant-based products is way overdue. In the wake of a huge movement towards plant-based and plant-forward diets, due to increased research and interest, Else is a wonderful product to support infant and toddler Nutrition. Read on to learn about all of its positive attributes.

Benefits of Else Plant-Based Formula Alternative

Choose Else Nutrition because it is:

Organic: This means that the USDA (United States Department of Agriculture) has determined that the ingredients in this healthy baby formula are free of genetically modified organisms (GMOs), fungicides, herbicides, and pesticides. Organic practices result in enhanced soil and water quality and, in general, more overall sustainable farming (1). Translation: Organic foods are beneficial for our environment. Research has shown that organic produce is more nutritious: It has higher levels of antioxidants and lower levels of toxic metals (such as Cadmium). Increased exposure to pesticides has been shown to increase risk for ADHD, Parkinson’s disease, diabetes, and some cancers (2). The effects of chemicals used in conventional farming may be more detrimental to the small developing brains and bodies of babies/children than to those of adults.

Glyphosate-free: Yes, the USDA Organic Label is important, however, it may not be enough today. It ensures that crops are GMO-free, but this doesn’t mean a product is 100% free of pesticides. Glyphosate is an herbicide (pesticide) that is carcinogenic (can cause cancer). Final organic food products are often NOT tested. The USDA does not check for glyphosate residue. The buckwheat and almond sources in Else formulas are glyphosate-free.

Made from clean ingredients: Else formulas are simple and pure. Almonds, buckwheat, and tapioca make up about 92% of the product. The ingredient list is short and easy to understand. There are no added unhealthy oils, inflammatory sugar/corn syrups, artificial sweeteners, or gums/stabilizers/fillers than can upset small bellies. For moms looking to supplement breast milk or wean their children after 1 year of age, it may seem that there are many dairy-free milk substitutes and products on the market today; however, none are quite right for little developing brains and bodies. They are not nearly as nutritionally dense as breast milk (or full-fat dairy milk). They may be low-fat, low in protein, and other nutrients, and often contain added sugars and fillers as mentioned above. They are simply NOT appropriate, and in fact, unhealthy as a foundation for a toddler’s diet. This is especially true for vegans and/or those who truly cannot tolerate dairy protein.

Pleasantly mild in flavor: When babies are weaned off breast milk and/or need a supplement or substitute for human or cow’s milk, they are more likely to accept a drink/formula that tastes great (they are indeed little humans). Other formulas may not be as mild. In fact, the hydrolyzed/elemental formulas have a reputation of smelling bad and tasting worse. Such formulas may be indicated for little ones with dairy allergies and intolerances, and digested well; however, if the child will not drink due to the smell/taste, this can be an issue.

Vegan/Plant-based: In case you haven’t noticed, there has been a huge buzz surrounding “plant-based†and “plant-forward†nutrition. This is not new news to us health professionals. We have always known that a variety of fruits, vegetables, whole grains, legumes, fiber, and healthy fats were integral for good health. The research is finally catching up. We now know that our microbiome (the collection of microorganisms-bacteria, fungi, viruses-that live in/on the human body) can benefit our health, especially immunity, aging, digestion, metabolism, mood and mental health. We can best benefit our microbiome by consuming a diet rich in a variety of plant-based foods. Why not start our little ones on such a diet with a plant-based formula?! Research shows that children on a predominantly plant-based diet have increased microbial biodiversity and richness (3).

Dairy-Free and Soy-free: Infants and toddlers with food allergies, intolerances, and/or sensitivities simply cannot tolerate many formulas on the market today. The incidence of food allergies is on the rise in children and adults. According to the Mayo Clinic: “Food allergy is an immune system reaction that occurs soon after eating a certain food. Even a tiny amount of the allergy-causing food can trigger signs and symptoms such as digestive problems, hives or swollen airways. In some people, a food allergy can cause severe symptoms or even a life-threatening reaction known as anaphylaxis.â€(4) Cow’s milk is the most allergenic food for in children in the U.S. (followed by peanuts, eggs and soy). Most of the formulas on the market are based on cow’s milk.

Else’s products can be tolerated by children with dairy and soy allergies and sensitivities. Anaphylaxis due to almond or buckwheat allergy is very rare (<1% and 1% of anaphylaxis cases in children respectively) with numbers well below egg, wheat, fish, goat/sheep’s milk, lentils, cashew, and peanut.

Also, just as an update and reminder about almonds: recent research demonstrates that delaying introduction of potential allergenic foods (wheat, dairy, eggs, fish and nuts) may actually increase the risk of food allergies and/ or eczema. The American Academy of Asthma, Allergy and Immunology (AAAAI) now recommends they be introduced without delay, and not wait up to 1-3 years of age, as advised in the past (5).

Nutrient composition matches breast milk: We all know that breast milk is the gold standard for feeding infants. However, if and when it is not possible, and/or a child requires supplementation or is being weaned, Else Nutrition provides a formula with nutrients that match that of breast milk. The macronutrients (carbohydrates, fat, and protein) and micronutrients (vitamins and minerals) are the same in Else formula-even though Else is a vegan product. Moms and caregivers can be confident that their babies are being nourished while they slowly learn how to eat solids.

Created and supported by the best team: These formulas were created by leaders in the infant and toddler nutrition industry. Their formulation and ingredients have been tested, approved, and supported by pediatricians, gastroenterologists, registered dietitians, and MOMS and DADS!

Posted by AGORACOM-JC

at 10:39 AM on Thursday, May 7th, 2020

SPONSOR: BetterU Education Corp. aims to provide access to quality education from around the world. The company plans to bridge the prevailing gap in the education and job industry and enhance the lives of its prospective learners by developing an integrated ecosystem. betterU / Ottolearn launch FREE COVID-19 mobile resource toolkit to fight the global crisis – Click here for more information.

Online education now a new normal for govt, edtech platforms

As millions of kids take online school classes from home globally including in India, government along with private education sector have a great responsibility to offer online e-Learning to more than 60 million college students and 1.5 billion school students worldwide, experts said on Thursday

Private colleges in India which were already offering online education for last two decades now have a massive surge in e-Learning demand to meet.

“e-Learning or online education is the new normal. In future, we will see the proliferation of information technology tools and gadgets, post-COVID-19. But internet and broadband will remain an issue,” said Professor NK Goyal, Vice Chairman, ITU APT India and former adviser of Gujarat Technological University.

If e-Learning apps like BYJU’s and Khan academy are targeting schools, others like Adda24x7 are offering specialised coaching for entrance exams like IIT and JEE.

Robust connectivity is undoubtedly critical for the success of e-Learning.

According to Rajan S Mathews, DG, the Cellular Operators Association of India (COAI), post COVID-19, there will be a surge in online education by schools and colleges in the country.

“The telecom industry is fully prepared with 99.9 per cent network capacity. The telecom companies have taken appropriate measures to meet the surge in traffic due to online education and other online activities using telecom infrastructure,” said Mathews.

Union Human Resources and Development (HRD) Minister Ramesh Pokhriyal Nishank recently said that the government is offering a slew of educational applications and platforms for both school and higher education institutes.

In addition to teachers, Nishank urged parents and students to make maximum use of online education to ensure their academic continuity is maintained.

The World University of Design (WUD) claims that it has collected materials for online learning across its courses during the last one year.

“WUD is using technology-enabled AI, supervision technologies and video conferencing and other tools to enable virtual learning. This includes a mix of online platforms for sharing files, conducting meetings and lectures in association with online services iamp; resource providers like Coursera, Bloomsbury, EBSCO etc. as partners in its strategy,” said Dr Sanjay Gupta, Vice Chancellor, World University of Design (WUD).

Posted by AGORACOM-JC

at 10:08 AM on Thursday, May 7th, 2020

SPONSOR: Datametrex AI Limited (TSX-V: DM) A revenue generating small cap A.I. company that NATO and Canadian Defence are using to fight fake news & social media threats. The company is working with US Government agencies on Covid19 and Coronavirus fake news and disinformation. The company also obtained the rights to import and sell COVID-19 test kits from South Korea – Click here for more info.

AI can distinguish between bots and humans based on Twitter activity

Artificial intelligence is being used to spot the difference between human users and fake accounts on Twitter

Researchers found that human users replied between four and five times more often to other tweets than bots did

Real users gradually become more interactive, with the fraction of replies increasing over the course of an hour-long session of Twitter use

Artificial intelligence is being used to spot the difference between human users and fake accounts on Twitter.

Emilio Ferrara at the University of Southern California and his colleagues have trained an AI to detect bots on Twitter based on differences in patterns of activity between real and fake accounts.

The team analysed two separate data sets of Twitter users, which had been classified either manually or by a pre-existing algorithm as either bot or human.

The manually verified data set consisted of 8.4 million tweets from 3500 human accounts, and 3.4 million tweets from 5000 bots.

The researchers found that human users replied between four and five times more often to other tweets than bots did. Real users gradually become more interactive, with the fraction of replies increasing over the course of an hour-long session of Twitter use.

The length of tweets by human users also decreased as sessions progressed. “The amount of information that is exchanged diminishes,†says Ferrara. He believes that the change may result from a cognitive depletion over time, in which people become less likely to expend mental effort composing original content.

Bots, on the other hand, show no changes in their interactivity or the length of information they tweet over time.

Tags: AI, bot, CSE, datametrex, fake news Posted in Datametrex AI Limited | Comments Off on #AI can distinguish between bots and humans based on #Twitter activity – SPONSOR: Datametrex AI Limited $DM.ca

Posted by AGORACOM-JC

at 7:01 AM on Thursday, May 7th, 2020

Signed a binding Letter of Intent to acquire LHE Enterprises Ltd, the holding company of online sportsbook and casino operator Argyll Entertainment AG and its operating support subsidiaries

Argyll has established itself as a fast growing and innovative gaming company within the UK and Irish market

“With Argyll already generating around $12 million in revenue annually, this acquisition will have a major positive impact for our company,†commented Grant Johnson, CEO of Esports Entertainment Group.

BIRKIRKARA, Malta, May 07, 2020 — Esports Entertainment Group, Inc. (NasdaqCM: GMBL, GMBLW) (or the “Companyâ€), a licensed online gambling company with a focus on esports wagering and 18+ gaming, signed a binding Letter of Intent (LOI) to acquire LHE Enterprises Ltd, the holding company of  online sportsbook and casino operator Argyll Entertainment AG and its operating support subsidiaries (â€Argyllâ€).

Since launching its flagship brand, www.sportnation.bet, in the summer of 2017, Argyll has established itself as a fast growing and innovative gaming company within the UK and Irish market leveraging the expertise of its 40 strong staff in marketing, technology, risk management, and regulation to offer its customers an entertaining, safe and secure online gaming experience, an award winning rewards program, and access to exclusive and proprietary sports and gaming content.

“With Argyll already generating around $12 million in revenue annually, this acquisition will have a major positive impact for our company,†commented Grant Johnson, CEO of Esports Entertainment Group. “In the current global environment of COVID-19 there has been a surge of interest in online gaming to fill the void left by traditional sports and other activities. Argyll’s established footprint and revenue base, combined with our strong cash position from our successful April capital raise combined with our esports betting platform, places Esports Entertainment in a great position to capitalize on this evolving opportunity.â€

Argyll, incorporated in Switzerland, with operational support services in London, UK and Malta, is licensed and regulated by the UK Gambling Commission under licence no. 000-045143-R-323955-001 and the Irish Revenue Commissioners under licence reference no. 1014456 to operate online sportsbook and casino sites in the UK and Ireland, respectively.

ABOUT ESPORTS ENTERTAINMENT GROUP

Esports Entertainment Group, Inc. is a licensed online gambling company with a specific focus on esports wagering and 18+ gaming. Esports Entertainment offers fantasy, pools, fixed odds and exchange style wagering on esports events in a licensed, regulated and secure platform to the global esports audience at vie.gg. In addition, Esports Entertainment intends to offer users from around the world the ability to participate in multi-player mobile and PC video game tournaments for cash prizes. Esports Entertainment is led by a team of industry professionals and technical experts from the online gambling and the video game industries, and esports. The Company holds a license to conduct online gambling and 18+ gaming on a global basis in Curacao, Kingdom of the Netherlands. The Company maintains offices in Malta. For more information visit www.esportsentertainmentgroup.com

FORWARD-LOOKING STATEMENTS

The information contained herein includes forward-looking statements. These statements relate to future events or to our future financial performance, and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance, or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. You should not place undue reliance on forward-looking statements since they involve known and unknown risks, uncertainties and other factors which are, in some cases, beyond our control and which could, and likely will, materially affect actual results, levels of activity, performance or achievements. Any forward-looking statement reflects our current views with respect to future events and is subject to these and other risks, uncertainties and assumptions relating to our operations, results of operations, growth strategy and liquidity. We assume no obligation to publicly update or revise these forward-looking statements for any reason, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future. The safe harbor for forward-looking statements contained in the Securities Litigation Reform Act of 1995 protects companies from liability for their forward-looking statements if they comply with the requirements of the Act.

Contact:

U.S. Investor Relations RedChip Companies, Inc. Dave Gentry 407-491-4498 [email protected]

Posted by AGORACOM

at 9:54 AM on Wednesday, May 6th, 2020

Securing the mining licence is a critical step towards moving the Aukam Mine into commercial production

Gratomic can now produce a concentrate of up to 98% Cg

A PEA on the Aukam Processing plant to be undertaken

Diamond drilling will resume at Aukam Graphite mine

TORONTO, ON / ACCESSWIRE / May 6, 2020 / Gratomic Inc. (“GRAT” or the “Company”) (TSXV:GRAT)(FRANKFURT:CB81)(WKN:A143MR) is pleased to announce, further to its Press Release dated March 26, 2020, that it has received confirmation from the Ministry of Mines and Energy of Namibia that the Minister has issued Mining Licence 215 (ML215) for the Company’s Aukam Graphite Property in Namibia. The Licence covers Base and Rare Metals, Industrial Minerals and Precious Metals. The Licence area falls within the proximity of the Aukam Processing Plant and the Graphite bearing shear zone for a total of 5002 hectares (5002 ha). Securing the mining licence is a critical step towards moving the Aukam Mine into commercial production.

The Company has completed 8 months of pilot testing on historically mined product and conducted an internal study on the efficiency of the pilot processing facility on this material. Through rigorous testing and adjustments to the plant, Gratomic can now produce a concentrate of up to 98% Cg. Management has subsequently decided to build a 20 000 tonne per annum processing plant. To date, 90% of construction is complete. Upon completion of the remaining 10%, the Company will initially start processing material from historical workings left at the surface when the mine last operated in 1974.

The Company has recently appointed Dr. Ian Flint to complete a preliminary economic assessment on the Aukam Processing plant. The study, its recommendations, and their subsequent implementation, will ensure the scale up of the existing pilot plant to a commercial scale processing facility that will provide the desired concentrate grades and production rates.

With respect to site exploration, in the coming months diamond drilling will resume at Aukam Graphite. The drilling will be conducted utilizing Company owned drilling equipment, focusing on areas proximal to graphite mineralization, depicted by previous diamond drilling, underground excavation and surface outcrop sampling. The drill targeting will be systematic with the expectation of producing an NI 43-101 resource estimate.

Arno Brand, President and CEO of the Company stated that “we are thrilled to receive the official mining licence for the Aukam Graphite Mine in Namibia. This is a monumental milestone for Gratomic, which took an extensive amount of effort to accomplish. Once the funding is secured, Gratomic will be able to move into the commercialization phase of development.”

Risk Factors

No mineral resources, let alone mineral reserves demonstrating economic viability and technical feasibility, have been delineated on the Aukam Property. The Company is not in a position to demonstrate or disclose any capital and/or operating costs that may be associated with the processing plant.

The Company advises that it has not based its production decision on even the existence of mineral resources let alone on a feasibility study of mineral reserves, demonstrating economic and technical viability, and, as a result, there may be an increased uncertainty of achieving any particular level of recovery of minerals or the cost of such recovery, including increased risks associated with developing a commercially mineable deposit.

Historically, such projects have a much higher risk of economic and technical failure. There is no guarantee that production will begin as anticipated or at all or that anticipated production costs will be achieved.

Failure to commence production would have a material adverse impact on the Company’s ability to generate revenue and cash flow to fund operations. Failure to achieve the anticipated production costs would have a material adverse impact on the Company’s cash flow and future profitability.

Steve Gray, P. Geo. has reviewed and approved the scientific and technical information in this press release and is the Company’s “Qualified Person” as defined by National Instrument 43-101 – Standards of Disclosure for Mineral Projects.

About Gratomic Inc.

Gratomic is an advanced materials company focused on mine to market commercialization of graphite products most notably high value graphene-based components for a range of mass market products. We have a Joint Venture collaboration with Perpetuus Carbon Technology, a leading European manufacturer of graphenes, to use Aukam graphite to manufacture graphene products for commercialization on an industrial scale. The Company is listed on the TSX Venture Exchange under the symbol GRAT.

For more information: visit the website at www.gratomic.ca or contact:

Posted by AGORACOM-JC

at 9:07 AM on Wednesday, May 6th, 2020

Integrated Zoom (NASDAQ:ZM) video conferencing into the Binovi Training Live initiative

Using the real-time capabilities of Zoom conferencing to connect with its network of approximately 20,000 industry professionals,

The company is conducting training on Binovi Pro and Binovi Coach applications, including an active customer success Q&A discussion

Toronto, New York – May 6th, 2020 – Eyecarrot Innovations Corp., (Eyecarrot) (TSXV:EYC) | (OTC:EYCCF) | (2EYA:GR), a leader in human performance neurovision software and hardware, is pleased to announce that it has integrated Zoom (NASDAQ:ZM) video conferencing into the Binovi Training Live initiative. Using the real-time capabilities of Zoom conferencing to connect with its network of approximately 20,000 industry professionals, the company is conducting training on Binovi Pro and Binovi Coach applications, including an active customer success Q&A discussion.

Zoom meetings provide live moderated question-and-answer sessions supported by simple registration to the Binovi Platform. Binovi enhances the active management of vision training patients within a diverse client community of neurovision specialists.

“We are forging forward with Zoom integration and have created a tremendous amount of value for our relationships using our Binovi Pro, Binovi Coach, and Binovi Academy resources. With the spread of COVID-19, governments, learning institutions, and businesses are facing a huge paradigm shift to a remote work, training, and eLearning culture. This shift has created an increase in demand for resources to continue operating as close to “status quo” which will lead to a greater adoption of our platform amongst care providers. We are happy to have built a platform that was designed for supporting patients and athletes remotely,” stated Adam Cegielski, Eyecarrot CEO.

With the global coronavirus pandemic disrupting all large gatherings, demand for remote training is surging, which will undoubtedly drive awareness and adoption of the company’s webinar conferencing and remote training platform. Many global companies including Microsoft (NASDAQ: MSFT), Google, Amazon (NASDAQ: AMZN) and Salesforce have enforced work-from-home policies amid the spread of COVID-19. Enforced social distancing protocols have also increased demand for Eyecarrot’s software as optometry clinics, sports vision specialists, and related industry conferences have suspended traditional services, with employees adopting a work-from-home routine.

“By leveraging Zoom’s video conferencing platform, we’re able to extend our presence beyond our usual face-to-face meetings and demonstrate the value and power of the Binovi Platform to prospective users, new users, and existing users, in an effective manner. We plan on further integrating Zoom’s technology into our own as we move forward,” commented Sam Mithani, Eyecarrot CTO.

Eyecarrot is a human performance technology company that has developed Binovi , a hardware and software-centered platform. Binovi combines hardware, software, specialized expert knowledge, and unique big data insights in order to deliver customized one-on-one training and treatment. Binovi is designed for vision optimization and the enhancement of cognitive skills related to human performance. We are working together under a common banner to help neuro-optometry, vision rehabilitation, and vision performance professionals gain measurable results in less time, and with less effort.

Certain statements contained in this news release constitute “forward-looking information” as such term is used in applicable Canadian securities laws. Forward-looking information is based on plans, expectations and estimates of management at the date the information is provided and is subject to certain factors and assumptions, including, that the Company’s financial condition and development plans do not change as a result of unforeseen events and that the Company obtains regulatory approval. Forward-looking information is subject to a variety of risks and uncertainties and other factors that could cause plans, estimates and actual results to vary materially from those projected in such forward-looking information. Factors that could cause the forward-looking information in this news release to change or to be inaccurate include, but are not limited to, the risk that any of the assumptions referred to prove not to be valid or reliable, that occurrences such as those referred to above are realized and result in delays, or cessation in planned work, that the Company’s financial condition and development plans change, and delays in regulatory approval, as well as the other risks and uncertainties applicable to the Company as set forth in the Company’s continuous disclosure filings filed under the Company’s profile at www.sedar.com . The Company undertakes no obligation to update these forward-looking statements, other than as required by applicable law. Neither TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Posted by AGORACOM-JC

at 8:16 AM on Wednesday, May 6th, 2020

Quebec government recently announced that, effective May 11, 2020, it will begin easing its Covid-19 related restrictions on business operations in the province

Subject to the implementation of said easing measures, NORTHBUD intends to commence scaling its Quebec production accordingly

TORONTO, May 06, 2020 — North Bud Farms Inc. (CSE: NBUD) (OTCQB: NOBDF) (“NORTHBUD” or the “Company“) is pleased to provide shareholders with the following corporate update:

Quebec Cultivation Facility

Easing of Covid-19 Restrictions

The Quebec government recently announced that, effective May 11, 2020, it will begin easing its Covid-19 related restrictions on business operations in the province. Subject to the implementation of said easing measures, NORTHBUD intends to commence scaling its Quebec production accordingly, and has advised its suppliers that it will be ready to receive starting materials quickly upon implementation of the easing measures.

Outdoor Cultivation Licence Application Status

With respect to the Company’s previously disclosed intention to apply for an amendment to its existing cultivation licence at its Quebec facility to allow for outdoor cultivation, the Company is pleased to announce that it has submitted to Health Canada all required materials and documentation for the aforementioned licence amendment, and it now awaits the issuance of a licence to allow for a proposed 1 million square feet of outdoor production. “With the underlying fundamentals and low-cost capacity of our Quebec facility, especially with the expected addition of outdoor capacity, we believe this facility has the potential to add value and we continue to explore collaborations with companies who have established distribution channels and who are relying on the volatile wholesale market to fulfill their cultivation needs,†said Ryan Brown, the Company’s Executive Chairman and Interim CEO. “Management is encouraged by the amount of interest being shown for potential collaborations and will update shareholders when there are any material developments on this front.â€

To date the Company has signed a letter of intent to supply product to a licensed distributor, and is actively negotiating additional supply contracts with other parties. Securing these supply agreements is expected to provide the Company with further insight into revenue potential and operating capital required for its Quebec facility. While the Company has initiated operations at its Quebec facility, currently the Company does not have sufficient working capital and financial resources to commercialize the full capacity of its Quebec facility.

Furthermore, in light of current market conditions, the Company is exploring options to extend its cash runway to further operations, including with respect to staffing decisions.

U.S. Operations

The Company also announces that it has signed a non-binding letter of intent to sell all the shares of its U.S. subsidiary, Bonfire Brands USA, Inc. (“BBUSAâ€), to an entity controlled by Mr. Justin Braune, the President of BBUSA. The proposed transaction is expected to close on or before May 15, 2020, and would constitute a related-party transaction as defined in Multilateral Instrument 61-101 Protection of Minority Security Holders in Special Transactions (“MI 61-101â€). The proposed transaction is exempt from the formal valuation and minority shareholder approval requirements of MI 61-101 as the fair market value of the shares of BBUSA proposed to be sold to the acquiror does not exceed 25% of the Company’s market capitalization. This determination is based upon the fact that the value of the net assets of BBUSA is negligible as the assets acquired were, and continue to be, highly leveraged. In light of the current market conditions, it is no longer economically viable for the Company to continue to try to sustain and develop these assets.

Under the terms of the proposed transaction, which remain subject to the negotiation of a definitive share purchase agreement and customary closing conditions and approvals, the acquiring party will become responsible for and guarantee all of BBUSA’s past and future liabilities and capital requirements, including all of the outstanding intercompany debts owed to NORTHBUD. The acquiror will also retain rights to the name “Bonfire Brands†and the Company will no longer proceed with the change of name and symbol that was approved at the last shareholder meeting. Final terms of the proposed transaction will be announced upon the signing of the definitive agreement.

“The structure of this proposed transaction represents the furtherance of the Company’s previously-announced plan to remove its direct exposure to the U.S. cannabis sector in order to eliminate the increasing administrative and capital costs associated with such holdings. Subject to the structuring of the definitive agreement, this proposed transaction would also significantly reduce dilution of shareholders of the Company by eliminating the need to issue additional shares of NORTHBUD related to the U.S. acquisitions,†said Ryan Brown, NORTHBUD’s Executive Chairman and Interim CEO. “We look forward to the successful completion of this deal to divest our U.S. holdings, which will significantly improve the Company’s balance sheet and available cash flow, a key Company objective in light of the difficult economic climate brought on by Covid-19.â€

About North Bud Farms Inc.

NORTHBUD owns and operates, through its subsidiaries, licensed cannabis facilities in Canada, California and Nevada. Bonfire Brands USA, the Company’s U.S. subsidiary, acquired cannabis production facilities in Salinas, California and Reno, Nevada in late 2019. The Salinas, California 11-acre farm is actively cultivating cannabis in its 60,000 sq. ft. of licensed greenhouse production space. The Reno, Nevada facility, located on 3.2 acres of land, was acquired through the acquisition of Nevada Botanical Science, Inc., and includes a world-class cannabis production, research and development facility with 5,000 sq. ft. of indoor cultivation space which holds medical and adult-use licenses for cultivation, extraction and distribution. Through its Canadian subsidiary, GrowPros MMP Inc., the Company built and owns a state-of-the-art purpose-built cannabis production facility located on 135 acres of agricultural land in Low, Quebec, Canada. The Low, Quebec facility currently has 24,500 sq. ft. of licensed indoor cultivation space; the Company expects to submit its licence application to Health Canada for an additional 1,000,000 sq. ft. of outdoor cultivation space in the near future.

For more information visit: www.northbud.com.

Neither the CSE nor its Regulation Services Provider (as that term is defined in the policies of the CSE) accepts responsibility for the adequacy or accuracy of this release.

Forward-looking Statements

Certain statements and information included in this press release that, to the extent they are not historical fact, constitute forward-looking information or statements (collectively, “forward-looking statementsâ€) within the meaning of applicable securities legislation. Forward-looking statements, include but are not limited to those identified by the expressions “anticipateâ€, “believeâ€, “planâ€, “estimateâ€, “expectâ€, “intendâ€, “mayâ€, “should†and similar expressions to the extent they relate to the Company or its management.

Forward-looking statements, including but not limited to, those regarding the timing of the Company’s filing of its year-end and quarterly financial statements, U.S. and Canadian strategies, the success of the Company’s licence application with Health Canada, the Company’s ability to close its proposed sale of BBUSA, the Company’s ability to execute its strategic plan, conditions in the cannabis market, the Company entering agreements in connection with the B2B supply of cannabis and the Company’s transition into a revenue-generating operational phase of development are based on the reasonable assumptions, estimates, analysis and opinions of management made in light of its experience and its perception of trends, current conditions and expected developments, as well as other factors that management believes to be relevant and reasonable in the circumstances at the date that such statements are made, but which may prove to be incorrect.

Forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause the actual results, performance or achievements of the Company to differ materially from any future results, performance or achievements expressed or implied by the forward-looking statements. Such risks and uncertainties include, among others, the risk factors included in the Company’s final long form prospectus dated August 21, 2018, which is available under the Company’s SEDAR profile at www.sedar.com. Accordingly, readers should not place undue reliance on any such forward-looking statements. Further, any forward-looking statement speaks only as of the date on which such statement is made. New factors emerge from time to time, and it is not possible for the Company’s management to predict all of such factors and to assess in advance the impact of each such factor on the Company’s business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. The Company does not undertake any obligation to update any forward-looking statements to reflect information, events, results, circumstances or otherwise after the date hereof or to reflect the occurrence of unanticipated events, except as required by law including securities laws. This news release does not constitute an offer to sell or a solicitation of any offer to buy any securities of the Company.

FOR ADDITIONAL INFORMATION, PLEASE CONTACT:

North Bud Farms Inc. Edward Miller VP, IR & Communications Office: (855) 628-3420 ext. 3 [email protected]