Posted by AGORACOM

at 7:32 AM on Friday, December 18th, 2020

Vancouver, British Columbia–(Newsfile Corp. – December 18, 2020) – Fabled Silver Gold Corp. (TSXV: FCO) (FSE: 7NQ) (“Fabled” or the “Company“) is pleased to announce the listing of its common shares for trading on the Frankfurt Stock Exchange (“FSE”) under the symbol “7NQ” and WKN # “A2QKYJ “.

The FSE is the world’s third largest organized exchange-trading market in terms of turnover and dealings in securities. With over 3,000 international companies listed on the FSE and investors directly connected to the FSE, the FSE represent 35% of the world’s investment capital.

The Company’s shares will now be cross-listed on the TSX Venture Exchange and the Frankfurt Stock Exchange. Fabled expects the FSE listing will help increase trading liquidity and facilitate investment in the Company by institutional and retail investors across Europe. This listing does not impact the total number of common shares outstanding in the Company.

Mr. Peter Hawley, President and CEO of Fabled, commented: “Fabled is committed to building shareholder value and the Frankfurt Stock Exchange listing will enable international investors to participate in the Company’s growth and development. We feel this is a great opportunity to introduce Fabled to a European investing audience at a time when Fabled is actively drilling at the Santa Maria project.”

Option Grants

Fabled also is pleased to announce that pursuant to its stock option plan it has granted an aggregate of 3,850,000 stock options to certain directors, officers and consultants, each exercisable to acquire one common share of Fabled at an exercise price of $0.08 per common share until December 18, 2030. The stock options vest as to 25% on the date of grant, and as to 25% every 6 months until fully vested.

About Fabled Silver Gold Corp.

Fabled is focused on acquiring, exploring and operating properties that yield near-term metal production. The company has an experienced management team with multiple years of involvement in mining and exploration in Mexico. The company’s mandate is to focus on acquiring precious metal properties in Mexico with blue-sky exploration potential.

The company has entered into an agreement with Golden Minerals Company to acquire the Santa Maria project, a high-grade silver-gold property situated in the centre of the Mexican epithermal silver-gold belt. The belt has been recognized as a significant metallogenic province, which has reportedly produced more silver than any other equivalent area in the world.

For further information please contact:

Mr. Peter J. Hawley, President and C.E.O. Fabled Silver Gold Corp. Phone: (819) 316-0919 [email protected]

Posted by AGORACOM

at 4:32 PM on Monday, December 14th, 2020

Fabled Silver Gold Corp. (TSXV: FCO)The Santa María Property is an under-explored, high-grade silver-gold project with significant exploration potential to expand mineral resources and identify new discoveries.

Fabled Silver Gold Company Highlights:

Commenced drilling on 100% option at Santa Maria Mine in Mexico

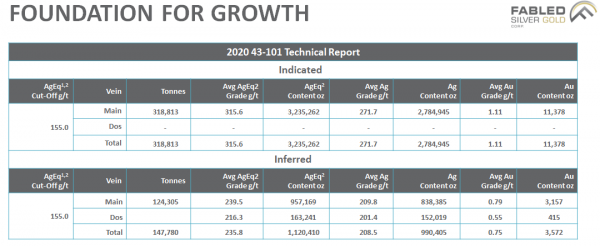

2020 NI 43-101 Resource of 3.2Moz Indicated and 1.1Moz Inferred in two primary veins

Two distinct Epithermal veins have been partially explored

Santa María Property is an under-explored, high-grade silver-gold project with significant exploration potential

19 significant vein structures exists within the property and provides future virgin exploration opportunities

Geophysical survey on the property and has successfully identified multiple targets for exploration and drilling

Santa Maria Deposit

High Grade silver-gold property located in mining friendly jurisdiction of Parrall, Mexico

The Parral mining district is situated in the center of the Mexican Silver belt, a district of epithermal silver gold mineralization

The belt has been recognized as producing more silver than any other equivalent are in the world

2018 PEA very supportive at current market prices

2 Mettalurgical Studies completed

Santa Maria vein structures provide many promising exploration and possibly future mining possibilities

The Santa Maria mine has never been systematically, or explored thoroughly with modern methods

The Asset: Santa Maria Mine 43-101

3.2Moz Indicated and 1.1Moz Inferred in two primary veins

High grade silver-gold property located in the mining friendly jurisdiction of Parrall, Chihuahua, Mexico.

The Parral mining district is situated in the centre of the Mexican silver belt epithermal silver-gold vein districts. The belt has been recognized as a significant metallogenic province, which has reportedly produced more silver than any other equivalent area in the world.

43-101 Technical Report completed on December 02, 2020 by Mineral Resources Engineering.

Significant vein structures within the property provides future exploration and mining opportunities.

Posted by AGORACOM

at 8:25 AM on Monday, December 14th, 2020

Vancouver, British Columbia–(Newsfile Corp. – December 14, 2020) – Fabled Silver Gold Corp. (TSXV: FCO) (“Fabled” or the “Company“) is pleased to announce the completion of the first ever ground geophysical survey on the Santa Maria Property, in Parral, Mexico and subsequent commencement of drilling. Fabled’s management team strongly believes that the Santa María Property is an under-explored, high-grade silver-gold project with significant exploration potential to expand mineral resources and identify new discoveries.

The first phase of drilling will consist of a minimum of 8,000 meters of HQ size core with a Versadrill 1.4 mount track. Drilling is expected to define the Santa Maria veining at depth and to the east and west using the IP anomalies as a target. This will be followed by pure exploration to test virgin IP targets to the north of the property, as identified by the recent survey. Fabled has awarded the surface diamond drill contract to Maza Diamond Drilling SA DE CV.

Peter J. Hawley, CEO and President remarks: “This is the first ever detailed geophysical survey on the property and has successfully identified multiple targets for exploration and drilling, which continues to support our theory of not only multi phases of mineralization but the relationship to structural controls. The results have been incorporated into surfacing mapping, sampling and underground and surface drilling resulting in a new theory of mineralizing events which should enhance our exploration success. Over four years past owners have only drilled approximately 9,600 meters and we are embarking on an initial 8,000-meter program to determine the true potential of the property, which is expected to take five months to complete.”

A video summary of today’s news release is available here.

Geophysical Interpretation and Survey Results

A 3-Dimensional Instantaneous Potential, (“IP”) survey covered the entire property at 50-meter line spacing and was 16 blocks in size with penetration to -500 meters minimum. The complete survey resulted in pseudo sections with 2D inversion for each line, a property plan map for chargeability and resistivity; and interpretative map with axis of anomalies and a Voxel 3-Dimensional model.

In addition, 27 kilometers of ground magnetics was completed over the property resulting in a final product consisting of a topographic plan map, total field, first derivative and reduced to the pole and 3D inversion magnetics.

A total of 11 first priority IP targets have been delineated property wide (see Figure 1 below), which are in a generalized east – west direction. Anomaly IPSM-1 located 400 meters to the east of the last surface expression of the Santa Maria Veins is defined as sub-cropping, (very shallow) and an extension of the Santa Maria veining. All other IP anomalies define new trends in the northern sector and range from shallow in depth to deep seated, +/- 100-150 meters in depth. The deeper anomalies are described as wide bodies in the areas where they intersect the secondary mineralized north – south veining. The geological team has collected 26 surface samples over all anomalies, and these have been submitted to ALS Chihuahua Laboratory for analysis.

Fabled’s reinterpretation of the age and mineralizing events and structures on the Santa Maria property finds that the Santa Maria and Santa Maria dos veins are hosted in a primary generalized east – west trending rhyolite zone and mineralization consists of silver and gold only. Younger Parral formation, post mineralization, sediments overlay the vein trends to the west, east, and in the north of the property.

These sediments have been structurally stressed / sheared in a generalized north – south trend as a result of the San Rafael graben northeast of the property, a major tectonic feature that has a regional effect of the placement of mineralization. These structures not only slightly offset the east – west trending Santa Maria Veins but wide zones of hydrothermal breccias are encountered where the intersection occurs. These north – south trending structures are interfiled with calc silicate veining which surface sampling has determined they not only contain silver – gold values but also lead, zinc, and copper. This has been interpreted to be a second mineralizing event.

Structure on structure creating dialization zones consisting of hydrothermal breccias have been reported in drill hole SM18-03 which reported 43.35 meters grading 0.78 g/t Au, 232.89 g/t Ag including a section reporting 3.35 g/t Au, 1,1012.63 silver over 8.94 meters.

About Fabled Silver Gold Corp.

Fabled is focused on acquiring, exploring and operating properties that yield near-term metal production. The company has an experienced management team with multiple years of involvement in mining and exploration in Mexico. The company’s mandate is to focus on acquiring precious metal properties in Mexico with blue-sky exploration potential.

The company has entered into an agreement with Golden Minerals Company to acquire the Santa Maria project, a high-grade silver-gold property situated in the centre of the Mexican epithermal silver-gold belt. The belt has been recognized as a significant metallogenic province, which has reportedly produced more silver than any other equivalent area in the world.

For further information please contact:

Mr. Peter J. Hawley, President and C.E.O. Fabled Silver Gold Corp. Phone: (819) 316-0919 [email protected]

Posted by AGORACOM

at 2:00 PM on Friday, December 11th, 2020

Beauce Gold Fields is focused on placer to hard rock exploration and discovery in the Beauce region of Southern Quebec. The the St-Simon-les-Mines Gold project is home to Canada’s first gold rush that pre-dates the Yukon Klondike that produced the largest gold nuggets in Canadian mining history (50oz to 71oz). Hosted along a 6 kilometer long placer channel, Beauce has identified a major Fault Line that coincides with an interpreted fault structure across the property. Evidence suggests the erosion of the Fault Line as a probable source of the historical placer gold channel. Click Here for More Info

If you are trying to find gold it helps to know where it came from.

To start with there is only one kind of gold. Placer gold and lode gold both come from the same place and are made of the same stuff. Gold is not actually formed on earth it was formed millions of years ago in distant stars. In large stars, much larger than our sun elements are combined together in their cores through the process of nuclear fusion. Our sun like all stars runs on fusion too but it does not have enough mass to produce atoms larger than carbon or oxygen. Larger stars can generate the gravitational force and heat in their cores necessary to produce elements as heavy as iron. To create things like gold even more energy is required and that takes place in a supernova.

When a large star runs out of light matter the fusion reaction is no longer sustainable and the star begins to collapse on itself very rapidly. The supernova collapse takes place in a matter of seconds. While the star is collapsing it produces heat very rapidly and explodes in what is essentially a humongous nuclear bomb. Supernova events are so bright and powerful that they are brighter than then entire galaxy that hosts the star. This nuclear explosion allows for higher energy fusion reactions that can produce heavy elements like gold. The explosion also scatters the newly created material over great distances.

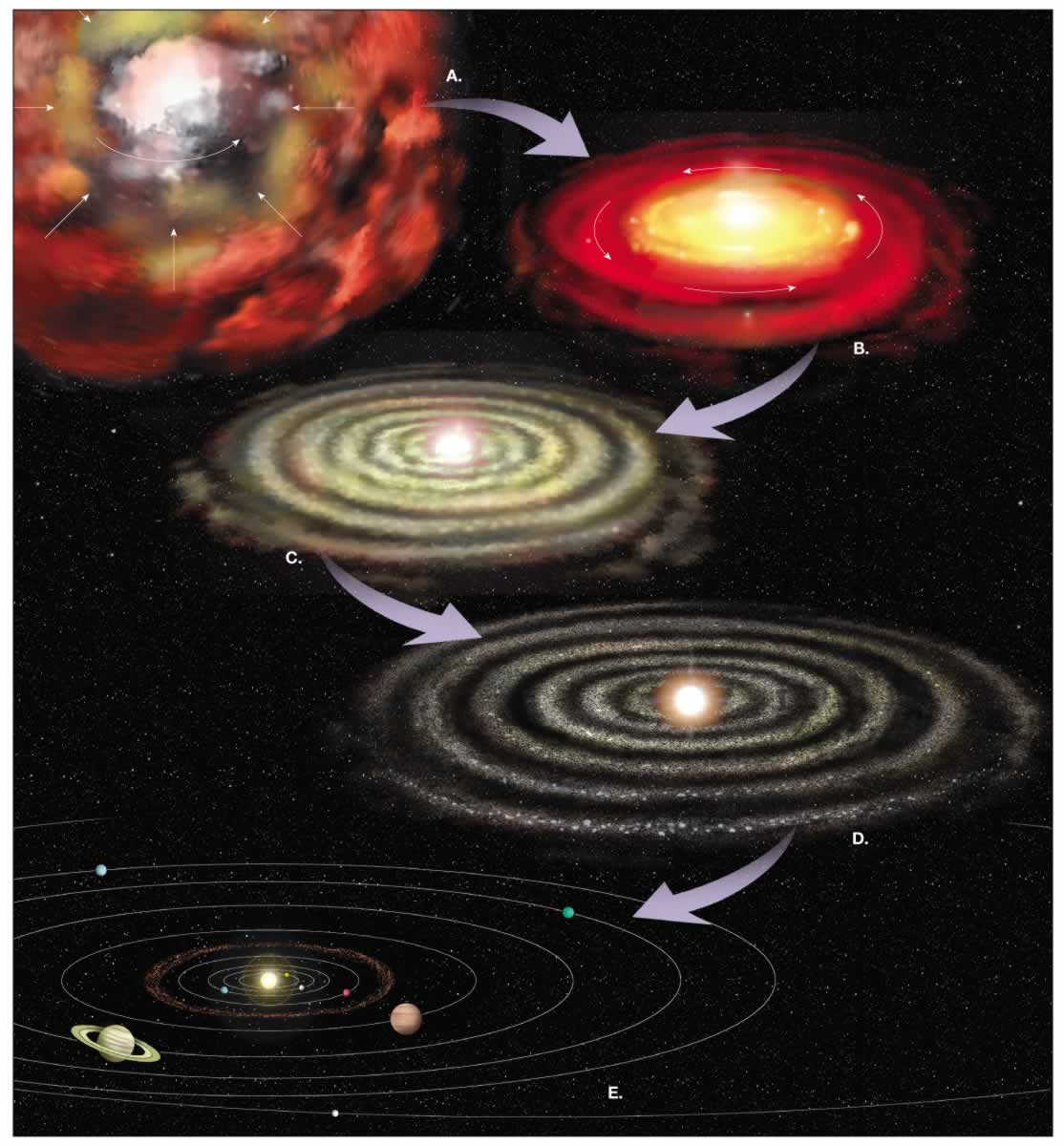

So how did the star dust make it into the mountains and rivers on earth? When our solar system began approximately 4.6 billion years ago it was a cloud of dust and gas called a nebula. This nebula was composed of the remains from older stars that had spread their guts around the universe in supernova explosions. The molecules of the nebula naturally pulled on each other by the force of gravity growing more and more dense. As the nebula was collapsing in on itself it also started to spin faster and faster. The condensing and spinning action formed the nebula into a disk, much like you spin dough into a pizza. In the center where the force of gravity is the strongest a new star was created, our sun. The swirling mass around the sun clumped together into the planets, moons, asteroid and comets that we see today.

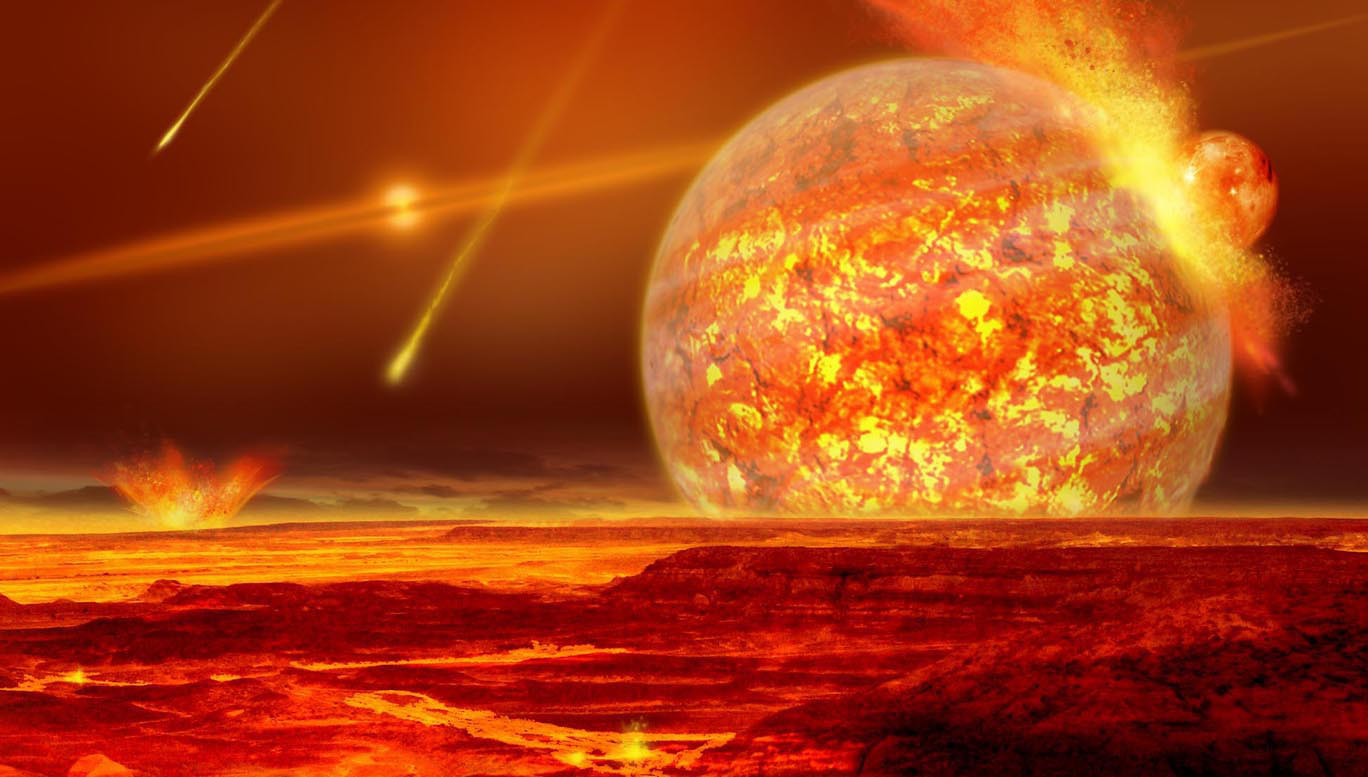

The early solar system was different that it is today. The big planets did not form all at once, it was a gradual process. Small plantoids formed first and crashed and coalesced into each other to form larger planets. In theory the distribution of gold was basically even in all the rocky material that made up the early solar system. In the early earth, while it was still completely molten the heavy material (such as iron and precious metals like gold) all sunk to the center of the planet to form the core. The process is similar to the way that dense material sinks to the bottom of your gold pan. If you could mine the core you would be very rich but it would be very difficult with current gold mining equipment. Current scientific theories estimate that there is enough gold in the core to cover the surface of the earth with a 4 meter thick layer of pure gold.

We can only reach gold that is trapped in the crust of the earth. The precious metals in the crust were put there by meteor bombardments that took place after the crust had formed. As these meteorites crashed into the surface of the earth they disintegrated and mixed their material into the upper mantle. The meteorite guts had the effect of enriching the amount of precious metals in the crust.

So we know where gold came from and how it was formed. Stay tuned for a future post to learn how the gold formed into deposits in the mountains and streams that we mine.

Posted by AGORACOM

at 12:42 PM on Friday, December 11th, 2020

SPONSOR: Arctic Star Exploration is currently exploiting the Diagras Diamond Property, NWT. Adjoined by both Diavik and Ekati Mines, Arctic has combined known data on Diagras with modern Gravity and EM geophysical survey techniques to delineate viable Kimberlite targets. Arctic Star is currently preparing a drill program. CLICK HERE FOR MORE INFO

We have seen how the industry has undergone significant changes over the past 20 years and how smaller companies have emerged to play an increasingly important role in supplying rough diamonds to the world.

These changes have come about at least partly due to the discovery of diamonds in locations outside of Southern Africa, which was where the vast majority of diamonds had been mined for nearly a century. South Africa is also where De Beers established its dominance of the industry. The discovery of diamonds elsewhere in the world has therefore been a key factor in the diamond giant’s gradual decline in market share.

According to Kimberley Process rough diamond statistics, 22 countries produced rough diamonds in 2014. The top six producing countries accounted for over 90% of production by value. A closer analysis of global diamond mining is key to learning more about the industry’s recent evolution, and to developing an image of where it might be heading in the future.

To start, I will focus on the top six producing nations, each of whose policies and methods of distribution shape the industry.

Russia

Diamonds were first discovered in Russia in the mid 1950s in the Sakha (Yakutia) Republic in northeastern Siberia. Interestingly, the search for diamonds in Russia, which began in 1947 following the end of World War Two, was not initiated for financial gain. Stalin understood that in order to rebuild the shattered Soviet Union after the war, he would need access to a large supply of industrial diamonds. These diamonds were required for a number of mechanical operations such as drilling, abrasive grit, precision cutting and other digging processes. However, at the time, De Beers controlled the sale of rough diamonds and Stalin knew that this left him precariously dependent.

Russian geologists had recognized as early as the 1930s that parts of Siberia exhibited very similar geological characteristics to the kimberlite-rich regions of South Africa. Teams of geologists were dispatched to Siberia and these expeditions did not disappoint. In 1955, the Mirny (Mir) kimberlite was discovered and mining commenced in 1957.

The purpose of searching for diamonds in Russia was to develop a supply of industrial stones for tools and equipment. Thus, when Mir produced a vast supply of gem quality stones, the state found itself in the grips of an unexpected predicament. By the mid 1960s, Russia had begun selling its gem diamond production to De Beers, a relationship that would remain intact for more than 40 years.

Today Russia maintains more than a dozen active open-pit diamond mines and is the world’s number one producer of rough diamonds by value and by carat volume. Russia’s known diamond reserves have long been shrouded in mystery, but according to state-owned miner ALROSA, which controls the vast majority of diamond mining in the country, its reserves exceed one billion carats. This should allow the country to maintain its position as a dominant player in the industry for several decades to come.

Botswana

Botswana officially gained independence from the UK on September 30, 1966. The country’s first kimberlite was identified just five months later. This initial discovery was followed shortly by numerous others which quickly established the nation as a diamond powerhouse and helped to propel its population out of crushing poverty.

Botswanan diamonds truly took to the skies when it was determined that the AK1 mine, now Orapa, could be seen from the sky and was frequently used as a landmark by South African pilots navigating their way to Europe.

Today, Botswana ranks second only to Russia in rough diamond production by value, driven primarily by the two richest mines in the world – Orapa and Jwaneng. However, it is the country’s recent efforts to leverage its diamond resources to further benefit its people that has earned the attention of the diamond world.

In 2011, the Botswanan government and De Beers announced a landmark deal that would eventually see De Beers’ entire sorting and sales operations moved from London to Gaborone – the capital of Botswana. Also as part of the deal, the government was given the opportunity to market a portion of local production through its own subsidiary company, now known as Okavango Diamond Company. In this way, Botswana has a solid mechanism for understanding the change in market prices for its resources.

By all accounts, Botswana’s diamond revenues have been put to very good use in helping lift the country out of poverty. In the late 1960s, Botswana was one of the poorest countries in the world with a GDP per capita of around $70. Today it ranks among the top African countries for per capita GDP, and consistently ranks near the top among Africa countries in terms of literacy, education, health care and low-levels of government corruption.

The Botswanan government has embarked on a bold experiment to extract maximum benefit from its natural resources by establishing Botswana as a diamond trading and manufacturing hub, in order to achieve stability for after its resources are depleted. Other nations are taking notice, and the Botswana model may be looked to in the future more and more frequently.

Canada

Though Canada’s history as a diamond-producing nation is short, it is now the world’s third largest producer by value. In fact, diamond deposits have been found scattered across the country’s vast expanses, and it offers much promise for continued exploration and development. Two large diamond projects are set to go into production as soon as late 2016 and early 2017 – the Renard and Gahcho Que projects.

Diamonds were first discovered in Canada in the early 1990s by two geologists who resisted the conventional wisdom that local geology would not support a diamond find. The discovery of the Ekati Diamond Mine triggered one of the most intense prospecting rushes in North American history, bringing teams from all over the world to scour the area. Geologists were literally staking their claims with wooden posts, so much so that local lumber suppliers could not keep up with the demand for wood.

It is said that the team of geologists who discovered the Diavik Diamond Mine initially planned to stake out a different location, but had to “settle” for what they were given because the person ahead of them in line at the mineral claims office took the area they were first interested in.

Most of Canada’s diamond projects are clustered in the far reaches of the northern Arctic region known locally as the Barren Lands. These barely hospitable tundra experience winter temperatures that average -35 degrees Celsius, often dipping below -50. This makes mining a challenge and the mining camps in these regions function more like enclosed cities, almost entirely sheltered from the harsh weather outside.

This region is also known for having been carved from the glacial movements of the last ice age. There are so many lakes in the area, numbering in the tens of thousands, that many remain unnamed to this day. In fact, some of the country’s most prolific diamond deposits have been found located beneath lakes. The Diavik Diamond Mine, located underneath 56 meters of water in Lac De Gras, necessitated the construction of a massive retaining wall and the removal of millions of liters of water to access the high-value kimberlite underneath the lake-bed.

Angola

Diamonds were first discovered in Angola’s Lunda Norte province near the border with Zaire in 1913. Angola is rich in both kimberlite deposits and alluvial diamonds washed out from their kimberlite hosts by ancient river systems.

The country has suffered from political instability for decades after gaining independence from Portugal in 1975. Shortly afterwards gaining independence, a civil war erupted that would last more than 25 years. As a result, large mining companies have been somewhat reluctant to invest in mining in Angola, and the country is believed to possess significant diamond resources that remain undiscovered.

In 2011, Angola introduced new legislation aimed at attracting foreign investment into its diamonds sector to help boost production. The plan has shown some early results. In 2015, ALROSA announced that it would invest $1.2 billion into the country to further develop producing assets and to increase exploration work in the country.

Keeping pace with the recent string of large diamond discoveries around the world, Australia-based Lucapa Diamonds announced in February that it had unearthed the 27th largest diamond ever from its Lulu mine in Angola. The gem was sold recently for $16 million.

South Africa

For decades South Africa was the epicenter of diamond mining. The discovery of the Eureka Diamond in 1866 by a young farmer named Erasmus Jacobs set off a prospecting rush unparalleled at that time. In a few short years, numerous alluvial and kimberlite operations were established. This new supply helped to replace the dwindling supplies from Brazil and India, and make diamonds accessible to vastly more people than ever before.

While South Africa still has more than ten producing diamond mines, its importance in the diamond world is slowly declining. Many mines have reached the end of their lifecycle and have moved to underground mining, which is often slow and more expensive than mining in an open pit. Although South Africa is still the fifth largest producer of diamonds in the world, with value in excess of $1 billion annually, in the absence of a major new mine discovery its importance will decline significantly over the coming decade.

Namibia

At number six in the diamond producing nations rankings, Namibia boasts the highest value per carat diamonds in the world. Namibian diamonds are mostly found in the ocean, along the country’s 1,570 kilometer coastline. Over millions of years, the area became a drainage basin covering the Kaapvaal Craton, which emptied water into the Atlantic Ocean. This water eroded diamond-bearing kimberlites and transported diamonds into the ocean. Over time, ocean currents churned up the area and deposited the diamonds in seabed trap sites as well as inland along the coast.

Because these diamonds travelled huge distances, often in rough conditions, only the strongest diamonds survived the journey. As a result, Namibian diamonds have exhibit the highest proportion of gem quality stones anywhere in the world, and this results in a very high average value per carat. These diamonds are mined mostly from boats and barges that drill and extract material from the seabed through long hoses.

Diamond production by country has changed significantly in recent years and this has had important implications on the industry and the power of companies within it. Next week I will look at some of the smaller producing nations, some of which are on the rise while others are in decline.

The views expressed here are solely those of the author in his private capacity. No one should act upon any opinion or information in this website without consulting a professional qualified adviser.

Posted by AGORACOM

at 10:20 AM on Wednesday, December 2nd, 2020

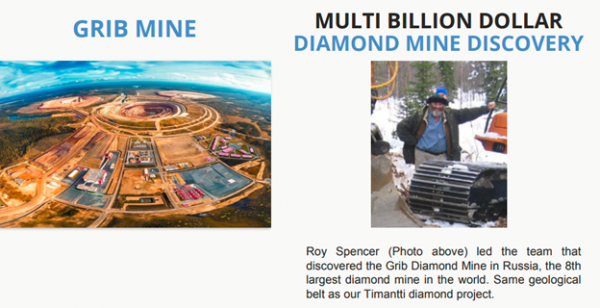

The 3 Reasons Why Arctic Star Is A World Class, Small Cap Diamond Explorer

Arctic Star Exploration (ADD:TSXV / ASDZF:OTCQB / 82A1.F:FRA) is in the diamond finding business.

The Company owns 100% of its flagship Timantti Diamond Project in Finland, where Arctic Star has discovered three diamondiferous kimberlites that may represent the first finds in a large kimberlite field. If you don’t know what a kimberlite is, keep drilling down and see below because this is truly exciting.

The project is located on the same geological belt as the Grib Diamond Mine in Russia, just 450 kms away. The Grib mine is one of the largest diamond mines in the world and was discovered by a team led by Arctic Star Director Roy Spencer. Keep drilling down to see more about him.

For those investors who have a little more experience and find themselves asking Why Finland? You should know that Finland was ranked as the World’s #2 mining jurisdiction in the world by the Fraser Institute 2020. In addition to its flagship project in Finland, the Company also controls diamond exploration properties in Nunavut (Stein) and the Northwest Territories of Canada (Diagras and Redemption).

But the real secret of Arctic Star is that it has tremendous potential to revolutionize the way in which Diamonds are discovered – and become a pioneer in the exploration industry – by finding diamonds in a place where no previous explorer has thought to do so. More than just a wild theory, Arctic Star has the team to back it up.

Here are the 3 things you need to know

1. World Class Diamond Finders

Arctic Star exploration has a highly experienced diamond exploration team previously responsible for numerous world class diamond mine discoveries. The team is led by Buddy Doyle who originally discovered Diavik Mine, Canada’s largest diamond mine in terms of carat production. Diavik’s exceptional grades make it one of the most valuable diamond mines in the world. Diavik is located in the Northwest Territories of Canada, where Arctic Star has 2 of their diamond properties.

Few geologists have seen 2 projects from discovery through to decision to mine. Mr. Doyle is recognized by his peers in the exploration industry as an authority on diamond exploration and kimberlite geology, and has authored/co-authored numerous papers on these subjects. He was awarded the 2007 Hugo Dummitt Award for excellence in Diamond exploration.

Roy Spencer – If that wasn’t enough, the geologist who discovered the multi-billion-dollar Grib Diamond Mine in Russia (see above). which is just 450 KMs away from Arctic Star’s project in Finland, has now joined Arctic’s Board of Directors! Clearly, the Arctic Star team has the credibility necessary to put forth a new thesis on how to find diamonds.

2. Brand New Exploration Model To Find Diamonds

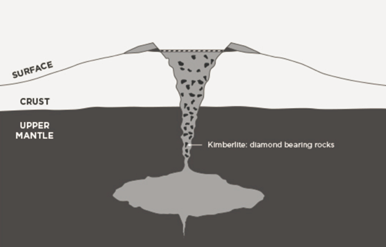

In order to find diamonds, you need to first find Kimberlites. What are Kimberlites? Essentially, they are the rocks which contain diamonds. These kimberlite rocks are found underground in vertical structures known as kimberlite pipes. To illustrate in simple terms, see this basic image of a kimberlite pipe with kimberlite rocks inside of it.

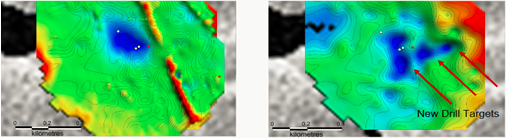

Kimberlite pipes are the biggest source of diamonds today. When exploration companies go looking for kimberlites, the industry standard for finding them is to look for magnetic signatures. This is done by taking a magnetic survey from the air and/or ground. with a device called a magnetometer. Now, most of you won’t understand what you are looking at – but here is an example of one of the company’s magnetic surveys on its Canadian Diagras property.

The most important thing to understand is that the industry looks for magnetic signatures ….. but Buddy Doyle and the accomplished Arctic Star team have developed a NON MAGNETIC THESIS. They believe they will find economic diamonds by locating Kimberlite that do not have a magnetic signature where previous explores sought not to look. Arctic in a sense is exploring for diamonds the opposite way the industry traditionally does. Arctic acquired property big mining company’s dropped, because they looked at them one way. Arctic is looking differently and success is occurring quickly for this small, yet accomplished exploration outfit. There are already multiple drill ready targets in 2 countries using this new way of looking for diamonds.

Arctic offers multiple opportunities in 2 countries to turn the Diamond Industry on notice with a discovery.

3. Arctic Star Has Two Diamond Projects Ready To Verify Its Non-Magnetic Theory

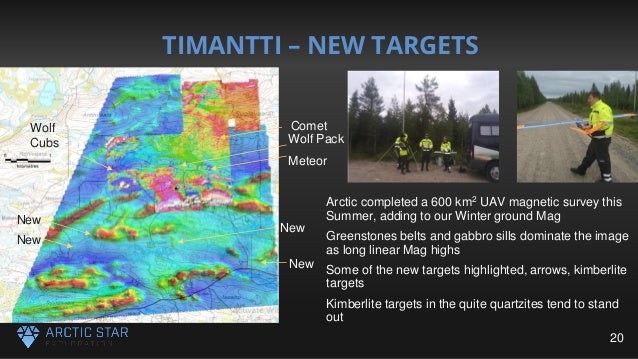

Arctic has 2 diamond projects on which to verify its theory: Diagras in Northwest Territories of Canada and Timantti in Finland, where early exploration searching for Non-Magnetic signatures has already yielded multiple new diamond target

A. Diagras is next to Diavik (Canada’s largest diamond mine) and is drill ready to prove Buddy’s theory. Arctic has plans to drill in 2020

B. Timantti in Finland has 3 separate target areas and 6 targets altogether identified through non-magnetic signatures as a means to find diamonds and further excel Buddy’s theory, it is the company’s goal to drill test in 2020

If Buddy Doyle and the Arctic Star team are correct it will create a new discovery process for understanding how diamonds are brought to surface in areas previous explorers cared not to look. Arctic Star has the potential to create multiple discoveries and copycat companies trying to duplicate their success.

However, there is only one Buddy Doyle and Roy Spencer, which is why Arctic Star is the one Diamond Exploration Company every investor should be aware of.

Posted by AGORACOM

at 7:27 AM on Tuesday, December 1st, 2020

St-Georges Eco-Mining Corp. (CSE:SX) (CNSX:SX.CN)(OTC:SXOOF) (FSE:85G1) is pleased to announce that it has signed a Binding Letter of Intent with Altair International (US-OTC: ATAO) pursuant to which St-Georges has agreed to provide access to its patent pending lithium processing technology for lithium-in-clay mineral deposits, and also agreed to jointly develop a patentable electric vehicle battery recycling industrial process.

In return for the access to the lithium processing technology and as part of their contribution in the development of patentable intellectual property in regard to EV Battery Recycling, Altair will issue 2,000,000 common shares at signature of this Binding LOI. The company will also commit to 2 subsequent share issuance of 2 million shares each, the first at the filing of a joint patent application in regards to the battery recycling R&D effort and the second at the start of an Industrial Pilot Plant demonstrator of the battery recycling process. If all milestones are completed, a total of 6 million common shares of Altair will be issued in favor of St-Georges.

Altair will also make a total of US $300,000 cash payments to St-Georges. A first payment of US $150,000 on or before April 1st, 2021 and a second payment of US $150,000 on or before August 1st, 2021. Both companies will contribute equally to the battery recycling research & development effort and to the design and construction of a battery recycling industrial pilot-plant circuit in St-Georges contracted installations in Quebec.

Royalties

On Altair Nevada Lithium Project

The Parties will establish a 5% royalty stream on the commercial output of the Nevada Property for the whole mine life period. This royalty will be transferable at the discretion of St-Georges or its successors. It will be opposable to any successors of Altair as a lien on the mining assets. St-Georges and Altair will negotiate a right of first refusal in favor of Altair. The royalty, to be negotiated within the guidelines of the “Royalty Formula”, will take the form of a Net Revenue Interest or Net Revenue Return (“NRR“).

Based on the location of the lithium-in-clay mineral project of Altair, 20% of the established NRR will be assigned to Iconic Minerals (TSX-V: ICM) based on current active agreements between the two companies.

On the Commercial Recycling of EV Batteries

The parties will establish a mutually beneficial partnership royalty stream on the commercial implementation and output of the battery recycling technology. The proportionate ownership will be transferable at the discretion of St-Georges, Altair or its successors.

The parties agreed to enter into a long form Definitive Agreement on or before February 5, 2021. Definitive agreement will be subject to review by regulatory authorities.

The companies expect to issue additional information in the coming weeks regarding the joint battery recycling technology development effort.

Vilhjalmur Thor Vilhjalmsson, St-Georges’ President & CEO commented: “(…) With the continued work of our research and development team, it is a great pleasure to team up with Altair to take this process further. The SX team has been looking at alternative methods, including using our proprietary technology in recycling EV batteries. We can see this as an opportunity to further broaden the scope of our developments and welcome the partnership. This will also enable us to finetune the Nevada operations already in place with Iconic Minerals over the forthcoming years (…)”

Leonard Lovallo, President of Altair, commented that “We believe that the lithium extraction and purification processes which St-Georges has developed have the potential to reshape the economics of the lithium mining sector, and we are incredibly excited to have partnered with them on this endeavor. As the demand and marketplace for lithium continues to expand with the ever-increasing popularity of EV vehicles across the globe, the scope and applications of the technologies which we are partnering with St-Georges on will only increase.”

Lithium Processing Technology Update

St-Georges technical team is now ready to initiate work aimed at optimizing the purification process of its lithium process and recuperation technology. The objectives are to minimize chemical losses, optimize total process recovery and optimizing the value of the byproducts. The company also intends to validate multiple resources and assure the selectivity of lithium recovery works on different types of resources.

Multiple initiatives will be run in parallel with the company’s strategic partners and suppliers. This effort should lead to a complete metallurgical simulation to size and price equipment. St-Georges is committed to utilizing multiple laboratories in parallel in order to protect intellectual proprietary processes and to accelerate IP extension.

St-Georges contractors have completed the preparation of a spodumene concentrate sourced from a Quebec based mineral resources and the company is now ready to initial leaching tests in a pilot plant environment. The company is expecting material recently prepared from the Bonnie Claire Project in Nevada from its partner Iconic Minerals. The company expects to run a complete pilot mining processing circuit on reception of the material. This next development effort should establish the recuperation and purification parameters needed specifically for that project as well as the final tweaked chemical recipe for the resin used to coat the lithium balls used in the last recuperation and refining stage.

ON BEHALF OF THE BOARD OF DIRECTORS

“Vilhjalmur T. Vilhjalmsson”

VILHJALMUR THOR VILHJALMSSON President & CEO

About St-Georges

St-Georges is developing new technologies to solve some of the most common environmental problems in the mining industry. The Company controls all the active mineral tenures in Iceland. It also explores for nickel & PGEs on the Julie Nickel Project and the Manicougan Palladium Project on the Quebec’s North Shore.

Posted by AGORACOM

at 9:32 AM on Wednesday, November 25th, 2020

Planning to Use Hydrothermal Energy to Drill Iceland Gold Targets

St-Georges Eco-Mining Corp. plans on reviving Iceland’s long-dormant gold mining industry by using its vast abundance of renewable energy to drill for gold. St. George’s emphasis will be on making the most eco-friendly and socially responsible gold in the world.

St-Georges, is the only junior exploration company to own all the mineral rights of a western country

Controls all the active mineral tenures in Iceland

St-Georges plans to mine with robots, while the equipment and processing primarily will use electricity made from geothermal and hydro power by Landsvirkjun, the state-owned power company

Iceland is one of the countries with the highest ratio of green energy globally

Thormodsdalur Projectis the most advanced project in Iceland

Drilled a 124-meter-deep (407-foot-deep) hole in Thormodsdalur, outside Reykjavik, in September

Drilling up to 1,000 meters or up to 25 new shallow holes on the Thor Gold project

Opportunity to extract epithermal gold with geothermal power

Total area in excess of 4,600 km2 with 9 prospecting licences

Mineralization bearing outcrops were identified and sampled and brought to St-Georges’ secure facilities in Reykjavik for petrographic analysis in October

Iceland Resources ehf ( 100% St. George Eco-Mining )

Controls all the active mineral tenures

Including drill ready Thor Gold Project

One of the countries with the highest ratio of green energy

100% renewable energy and zero carbon footprint.

Mining In Iceland

St. George’s emphasis will be on making the most eco-friendly and socially responsible gold in the world

St. George’s anticipates Iceland’s gold to be sold with a premium.

St. George’s ideology is about making minimal disturbances to the ground.

Thormodsdalur have minimal visible activity when mining activity starts

St-Georges will use all the material extracted from the ground during the mining process

After the minerals are separated, the remainder would be used in building material and concrete.

FULL DISCLOSURE: St. George’s Eco-Mining is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM

at 8:48 AM on Monday, November 23rd, 2020

Interval contained gold mineralization averaging 0.24 g/t over 80 meters with gold grades ranging from 0.01 g/t up to 6.21 g/t.

Reykjavik – TheNewswire – November 23, 2020 -St-Georges Eco-Mining Corp. (CSE:SX) (CNSX:SX.CN)(OTC:SXOOF) (FSE:85G1) is pleased to disclose the results of the reverse circulation research hole TRC 20-01 authorised prior to the acquisition of Melmis EHF earlier this fall.

The 124m hole intersected a broad zone of low grade disseminated mineralization near surface. At depth of 41.5m the team intersected and confirmed with preliminary assays the existence of a thick interval that contained gold mineralization averaging 0.24 g/t over 80 meters with gold grades ranging from 0.01 g/t up to 6.21 g/t.

Within that zone a section of 9.9 meters averaged 0.7 g/t gold starting at 55 meters depth and included 2.1 meters of 1.67 g/t gold. A separate zone assayed 6.21 g/t over 0.3 meters at a depth of 98 meters.

The company is in the process of renting new facilities that will allow a streamlined sampling process. As soon as the installation is ready, all samples on 30cm intervals will be relogged and certain samples will be reanalyzed for gold and trace elements by independent laboratories in Dublin Ireland. Duplicate samples are a necessary protocol when gold values exceed one g/t gold in a known low sulfidation vein system with historic high-grade gold values. Trace element geochemistry may further assist in vectoring in on the better parts of the system. The company expects to conduct the next hole at an angle of 85? from the same location to confirm its hypothesis.

This initial hole was drilled between two previously known mineralized and drilled areas of the project. The purpose of the hole was to provide continuity of alteration and mineralization between these two zones. Additional holes are planned along strike and at depth as a follow-up of hole TRC 20-01. This RC hole was drilled at -45 degrees and azimuth 110?. Following the acquisition of Melmis, St-Georges is less restricted on the location and depth of future drilling.

Based on geological logging to date, mineralization is disseminated over a thicker interval and not limited to quartz veining which is the preferential host for high-grade gold elsewhere in the Thor system.

Based on the results from this recent hole, St-Georges geological team believes that we are looking at a strong hydrothermal system that is mineralized with gold over apparent broad widths currently more than 700 meters of strike.

Iceland Resources, St-Georges’ Iceland wholly owned subsidiary’s CEO, Thordis Bjork Sigurbjornsdottir, commented: “(…) We are very pleased with the preliminary results from our maiden hole within the project, we feel it supports our theory in regards of the geological settings and that the system could potentially prove to be expanded on a much larger surface than what was previously expected. These results are encouraging on our path to our first maiden resource. The team is evaluating next steps and is anticipating additional positive surprises with further work(…)”.

Quality Control

Samples were collected in buckets then sealed and transported directly from the site to Iceland Resources’ secured warehouse facilities in Reykjavik by the SX geological team. The geological team sampled each bucket. The samples along with duplicate and Q/C blank samples were added to 2 shipments that traveled by plane to ALS Global Laboratories (ISO/IEC 17025 accredited) in Loughrea, Ireland. All samples were tested using four acid trace analysis (ME-ICP61).

About Thor Gold

The Thormodsdalur Gold Project is located about 20km east of the city center of Reykjavik and south-east of the Lake Hafravatn. The project was discovered in 1908. The property produced a gold concentrate from 1911 to 1925, which shipped to Germany for processing. Over 300 meters of tunnels explored and mined one or more quartz veins and wall rock below open cuts at the surface.

Studies between 1996 and 2013 identified the project mineralization as a low sulfidation system hosted by basic to intermediate flows of Pliocene to Miocene age. The host contains banded chalcedony and ginguro within a fault zone up to 5 meters in width. To date, the identified gold trend has a known strike length of 700 meters determined by drill intercepts. Petrographic analysis of the vein material identified gold occurring in its free form and as part of an assemblage with pyrite and chalcopyrite. Petrographic and XRD studies show an evolution of the vein system from the zeolite assemblage to quartz-adularia and lastly, to minor calcite.

Thirty-two holes have been drilled within the license area, for a total of 2439 meters excluding the 124 meters reverse circulation hole drilled by St-Georges in the Fall of 2020.Gold values vary from less than 0.5 g/t to a maximum of 415 g/t. (These values were obtained from selected random intervals and cannot be construed to be representative of any particular thickness or overall length.) Historically, the best intercepts from the diamond drilling are 33.5m of 8.0 g/t Au (true thickness) and 5.2m of 35.4 g/t Au (true thickness).

Gary McLearn, A professional geoscientist (Ontario APGO #2900) and an Independent Qualified Person as defined by National Instrument 43-101, has prepared, supervised the preparation or approved the scientific and technical disclosure in the news release.

The technical information in this release has been reviewed and approved by Mr. Herb Duerr, P. Geo. St-Georges’ director, a qualified person as defined by National Instrument 43-101 Standards of Disclosure for Mineral Projects.

ON BEHALF OF THE BOARD OF DIRECTORS

“Vilhjalmur T. Vilhjalmsson”

VILHJALMUR THOR VILHJALMSSON President & CEO

About St-Georges

St-Georges is developing new technologies to solve some of the most common environmental problems in the mining industry. The Company controls all the active mineral tenures in Iceland. It also explores for nickel & PGEs on the Julie Nickel Project and the Manicougan Palladium Project on the Quebec’s North Shore.

Posted by AGORACOM

at 11:46 AM on Friday, November 20th, 2020

SPONSOR: Arctic Star Exploration is currently exploiting the Diagras Diamond Property, NWT. Adjoined by both Diavik and Ekati Mines, Arctic has combined known data on Diagras with modern Gravity and EM geophysical survey techniques to delineate viable Kimberlite targets. Arctic Star is currently preparing a drill program. CLICK HERE FOR MORE INFO

Iconic Tiffany & Co. is among the most recognizable brand names in the world and one of the most valuable retail jewelry companies. A 2015 brand survey ranked it as the 66th most valuable brand name in the world, with a brand value in excess of $6 billion. Surprisingly, however, the company did not get its start in jewelry nor was it even called Tiffany & Co. The company began operating in 1837 as Tiffany & Young, a stationary and fancy goods emporium in lower Manhattan founded by Charles Lewis Tiffany and John B. Young. It wasn’t until Charles Tiffany took control of the company in 1853 that he shortened the name to Tiffany & Company, and established the firm’s emphasis on diamond jewelry.

Charles Tiffany was born in 1812 in Killingly, Connecticut. At the age of 15, he began to manage a small general store started by his father. At the age of 25, with a loan of $1,000 he received from his father, he opened a store with his friend John Young, whose sister he was dating and would later marry. The pair developed a reputation for selling only the finest quality goods and specialized in Bohemian glass and porcelain. The company was changed to Tiffany, Young & Ellis in 1941 after they brought on a partner, J.L. Ellis. Unlike any other store in the 1930s, Tiffany would clearly mark a price on every item to avoid haggling over prices and give birth to the ‘price tag.’ Legend has it that after their first three days in business, the store had brought in just $4.94 in sales.

But the partners persevered, and by 1845 they would establish the first-ever mail order catalog in the United States, known as the “blue book.” Charles Tiffany would establish the color palate for his catalogue in the familiar Tiffany blue we know today. He would soon extend the same color scheme to all Tiffany marketing and packaging materials, later culminating in the immortal Tiffany Blue Box. Some believe that the robin-egg blue color was chosen because of the popularity of the turquoise gemstone as a wedding day memento in that era. Tiffany blue is now one of the very few trademarked colors in the world.

By 1848, the company would begin focusing more on jewelry, most of which was imported from Europe. John Young would have the good favor of being in Paris on a buying trip in 1848 at the height of France’s second revolution. Many wealthy nobles, who were desperate to flee Paris, sold their diamonds to him in large quantities at heavily discounted prices. He would return with the gems to America, and the company would shift its interests to diamonds and precious jewelry. Two years later, they would open a location in Paris at 79 Rue de Richelieu. Its presence in Paris allowed the firm to keep abreast of the latest trends from Europe. In 1851, after observing the popularity of silver jewelry in England, Charles Tiffany would adopt the standards of English silver, coining the term ‘sterling silver’ in the United States.

After buying control of the company in 1953, Tiffany would establish himself as one of the world’s pre-eminent jewelers. But as the American Civil War became a reality in the early 1860s, Tiffany recognized the demand for expensive jewelry was likely to wane. He shifted his focus towards supplying swords, medals and light armor for the war. His role as a designer and supplier of Civil War medals would not be forgotten after the war’s end. In 1877, he was commissioned to design a medal for the New York Police Department. Their “NY” logo design, would become immortalized when the New York Yankees Baseball team adopted it as their logo in 1909, and today it is one of the most valuable sports brands in the world. The company would later be asked by the US Navy to design a medal for a sailor or Marine who “in action involving actual conflict with the enemy, distinguishes himself conspicuously by gallantry and intrepidity at the risk of his life above and beyond the call of duty without detriment to his mission.” The design would become known as the Tiffany Cross Medal of Honor, and it has been awarded to 22 people.

The end of the war also permitted Charles Tiffany’s focus on diamonds to begin anew. By the 1870s, Tiffany would be known as the King of Diamonds, and his influence and buying power continued to grow. His innovative work won acclaim at international expositions (Paris 1878, 1884, 1889, 1900; Chicago 1893). In 1867, Tiffany & Co. won the Award of Merit at the Paris Exposition Universelle, the first time an American company had been so honored by a European jury.

In 1879, Tiffany acquired a 287-carat yellow diamond mined in South Africa two years earlier. He would entrust its cutting to a 23-year old gemologist who had just joined the company. The now famous Tiffany Yellow is an 82-facet cushion shape weighing 128.54 carats. In over 100 years, the stone is only known to have been worn by two women: Mrs. Sheldon Whitehouse at the 1957 Tiffany Ball and Aubrey Hepburn in 1961 in a publicity photo for the movie, Breakfast at Tiffany’s.

In 1886, frustrated by ring settings that covered all but the table of a diamond, Charles Tiffany himself designed a new clasp to allow more of each diamond’s brilliance to be seen. What soon became known as the Tiffany Setting, was a six-claw setting with minimal use of metal that would expose more of the diamond. It has been called the most “brilliant ring ever” and is now a universal term to describe any diamond mounted in a claw setting, Tiffany or not.

In 1887, Charles Tiffany successfully purchased about one third of the French crown jewels when they were sold off after the collapse of the Second French Empire. One of his buyers, Thomas Banks, was coincidentally in Paris at the time, and Tiffany became the single largest buyer during the sale, which further raised his prominence and influence among wealthy European society. He purchased several famous stones, including some depicted in artwork having been worn by Queen Elizabeth I and Napoleon.

By the time of his death in 1902 at the age of 90, Charles Tiffany had transformed a $1,000 investment into a $35 million dollar fortune. At the time, that represented 1/616th of the entire United States GNP.

{kind=link}