Posted by AGORACOM-JC

at 4:25 PM on Monday, May 27th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)

Kenbridge Property has a measured and indicated resource of 7.14

million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has

interests in Peru, including a 20 percent equity stake in Eloro

Resources and 2 percent NSR in their La Victoria property. Click her for more information

Benchmark nickel on the London Metal Exchange surged nearly $500 in about 10 minutes in the morning, spurred by Chinese investors covering short positions, traders said, continuing the rally in the afternoon.

That sent nickel surging 5 per cent to a peak of $12,495 a tonne, the highest since April 30, before paring gains in closing open outcry activity to a bid of $12,370, a rise of 4 per cent.

Published on: May 26, 2019

Nickel — the key metal mined in Sudbury — spiked to its highest level

in over two weeks last week as bearish investors covered positions,

while other industrial metals gained on a weaker American dollar and

hopes for a U.S.-China trade deal.

World stocks edged higher and oil prices also recovered from bruising

falls last week after U.S. President Donald Trump nurtured hopes of

progress in U.S.-China talks.

“With the stock markets popping up a tad this morning and also the

dollar strength pausing, that’s giving the market an excuse to cover

some shorts ahead of the weekend, which is a long weekend in the UK and

US,†said Ole Hansen, head of commodity strategy at Saxo Bank in

Copenhagen.

“But we are by no means out of the woods yet, if anything, it may just be the market pausing before we hit the next headline.â€

Benchmark nickel on the London Metal Exchange surged nearly $500 in

about 10 minutes in the morning, spurred by Chinese investors covering

short positions, traders said, continuing the rally in the afternoon.

That sent nickel surging 5 per cent to a peak of $12,495 a tonne, the

highest since April 30, before paring gains in closing open outcry

activity to a bid of $12,370, a rise of 4 per cent.

Put another way, nickel finished At US$5.5980 on Friday, up 0.2161 cents from the day before.

The move higher in nickel gained steam as it broke through its 200-day moving average, a key technical level, traders said.

* NICKEL FORECAST: Fitch on Friday revised down its London

three-month nickel average price forecast for 2019 to $13,250 a tonne,

from $14,500 estimated earlier, on rising global economic risks, an

escalating trade dispute and disappointing refined nickel demand from

China so far this year.

* COPPER: Three-month LME copper (another key metal in Sudbury)

climbed 0.5 per cent to finish at $5,955 a tonne in closing rings, but

on a weekly basis it marked a sixth consecutive decline.

Posted by AGORACOM-JC

at 9:00 PM on Sunday, May 26th, 2019

SPONSOR: Tartisan Nickel (TN:CSE)Â Kenbridge Property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has interests in Peru, including a 20 percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property. Click her for more information

Nickel Prices Could “Go Through The Roof”; Watch For Signs – Expert

In the next five to ten years, the electric vehicle (EV) revolution will likely dominate the nickel space and will be sending prices much higher…

Guest(s): Alex Laugharne Principal Consultant, CRU Group

Laugharne said that nickel sulfide producers and the metallurgical laterite producers, who are most closely linked to EVs, are undergoing technological changes that may leave a supply gap in the nickel market.

“I think you’re seeing a lot of people being hesitant to invest in

new supply in the space because of this potential latent capacity. If

they do encounter technical difficulties, may fail to materialize, and

in that scenario, we may end up with a real crunch that could cause

nickel prices, and in particular, nickel sulfide prices, or pure nickel

prices to go through the roof,†he told Kitco News on the sidelines of

the Mines and Money New York conference.

Posted by AGORACOM-JC

at 10:37 AM on Tuesday, May 21st, 2019

SPONSOR: Tartisan Nickel (TN:CSE)Â Kenbridge Property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper. Tartisan also has interests in Peru, including a 20 percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property. Click her for more information

Right now, many cannot see the forest for the trees. By that I mean the big picture for EVs and EV metals demand.

What percentage of buyers do you think will buy an electric car by

end 2022 if it is cheaper to buy, cheaper to run, and cheaper to

maintain?

What if 50% of buyers want to buy an electric car in 2022, and 75% by 2025.

In a recent British survey, 71% of British car buyers said they are considering an electric car as their next vehicle.

In this article, my goal is to remind investors that the electric

vehicle [EV] and EV metal miners (lithium, cobalt, graphite, nickel)

opportunity is a long-term event. By this I mean the next decade or two.

If as I have forecast electric cars continue to gain in popularity,

then the demand boom for EVs and the EV metal miners will be

unprecedented in history and we will see an EV metals super-cycle over

the next decade or two.

Right now, many cannot see the forest for the trees

In the world of electric vehicle metals (particularly the key battery

metals lithium, cobalt, graphite and nickel) market participants

continually focus on what will happen this year, and what will stock

prices do in the next 1 year. The problem here is that short-term market

events can mean we sell down our stocks at the worst possible time when

the market is negative and we forget to see the big picture.

Take the lithium and cobalt markets the past year. Concerns of

oversupply have caused large sell-offs in the lithium and cobalt miners.

Retail investors have fled the market. Does this really make sense when

we look at the big picture over the next decade?

The big picture for EVs and EV metals over the next decade or two

Investors should focus on what lies ahead in the next decade or two. For example:

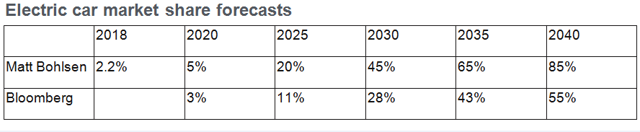

According to Bloomberg, we can expect EV sales to increase (from 2017 levels of 1.1%) 10x by 2025, 27x by 2030, 50x by 2040.

CNBC reported that JP Morgan forecasts “electric cars would take 35 percent of the global market by 2025 and 48 percent by 2030.”

The chart below compares my electric car penetration forecast to Bloomberg’s forecast.

Bloomberg forecasts annual electric vehicle sales – 30m by 2030, 60m by 2040

Do these forecasts sound realistic or possible? Only readers can decide for themselves.

My view remains that by end 2022, an electric car will start to

become cheaper than a conventional Internal Combustion Engine [ICE] car

(assuming zero subsidies). This is based on lithium-ion battery prices

falling ~16% pa, which has been the case the past decade. With 76

lithium-ion battery megafactories to be in production by about 2028

(~45 in production now) this looks highly realistic as scale and fierce

competition take effect.

My model forecasts a 60kWh battery will sell for less than an ICE engine system by end 2022 (earlier for a 50kWh battery)

Source: My Model

My forecast above states by end 2022, a 60kWh lithium-ion battery

will sell for US$5,300 which is less than the cost of a standard car’s

engine system (includes the engine, exhaust, transmission, petrol tank,

etc.).

If the above forecast is correct, it will mean a consumer by end 2022 can buy an electric car cheaper than a comparable ICE car. Furthermore, the electric car will have up to 10x cheaper running costs (electricity vs. gasoline) and up to 10x cheaper maintenance costs.

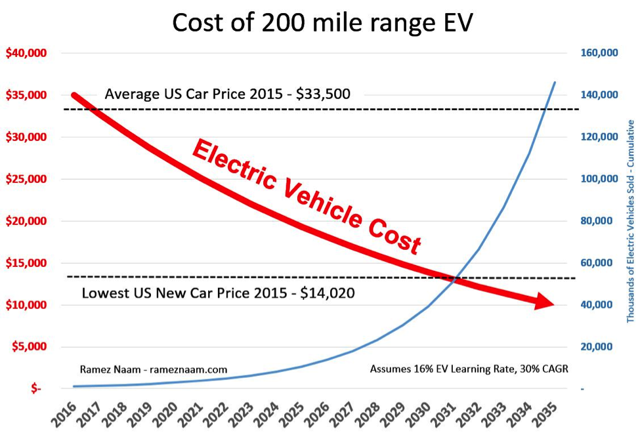

Once this happens, who would buy an ICE car if they are happy with a range of at least 208 miles or 335 kms (Tesla (TSLA) Model S 2012 model range).

The chart below shows by ~2017/18, an electric car can sell cheaper

than the average US conventional car, and by ~2031, an electric car can

be cheaper than the lowest priced new US conventional car. In 2018,

Reuters reported

in ‘VW plans to sell electric Tesla rival for less than $23,000:

source’ “Volkswagen intends to sell electric cars for less than 20,000

euros ($22,836).”

Electric car selling prices are forecast to fall rapidly as battery costs fall

What percentage of buyers do you think will buy an electric car by

end 2022 if it is cheaper to buy, cheaper to run, and cheaper to

maintain than a comparable ICE car?

Added to the above headline the electric car will have better acceleration and be more trendy than an ICE car.

Given the above, it would seem quite clear to me that most people if

given the option will choose an electric car post 2022. Certainly, by

2025, when an electric car is even cheaper it would seem almost everyone

will want one.

If again the above assumptions are correct, then electric car

penetration rates will be way higher than my forecasts above. For

example, my end 2022 forecast is at 10%, and end 2025 is at 20%. The

real demand could in fact be 3-5x higher than my forecasts, and higher

than Bloomberg’s forecasts. Perhaps JP Morgan’s forecasts of 35% by 2025 (and 48% by 2030) will be a better guide.

Nearly 75% of car buyers are considering an electric car as their

next vehicle. Sales of electric and hybrid cars will overtake petrol and

diesel by 2030, report claims. Searches for alternative fuel vehicles

on Auto Trader up by 40% in 2018. The British public’s appetite for electric vehicles

is growing significantly, according to a new report published by Auto

Trader. Almost three quarters (71%) of car owners said they’d consider

buying an electric vehicle as their next car, which is a huge leap from the 25% who answered positively when asked the same question in 2017.

What if 50% of buyers want to buy an electric car post 2022, and 75% by 2025

Clearly, if we get to levels above 50% by 2022, the electric car industry would probably not be able to meet this demand.

For example, the lithium demand to meet 50% electric car penetration

rates by end 2022 would be ~2.6mtpa. This would be almost 10x the level

of lithium demand from 2018. Similar problems would occur with the other

EV metals as well as the battery and electric car producers.

In other words, we could very well see a period post 2022 until

perhaps 2030 where people will be on waiting lists to get an electric

car. Similar to the ~400,000 list for the Tesla Model 3, but several magnitudes higher. Even the expensive Porsche Taycan (OTCPK:POAHY) already has a 20,000 waiting list.

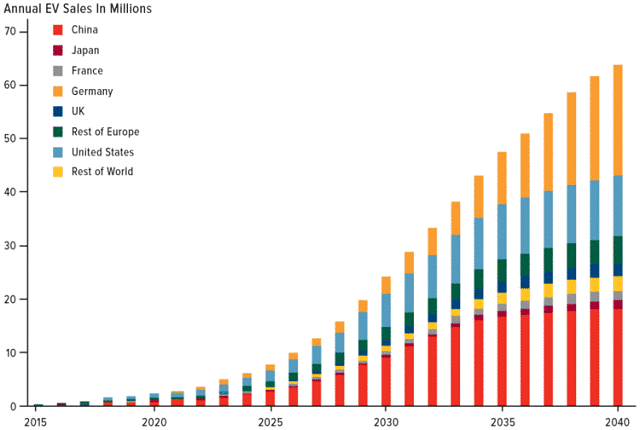

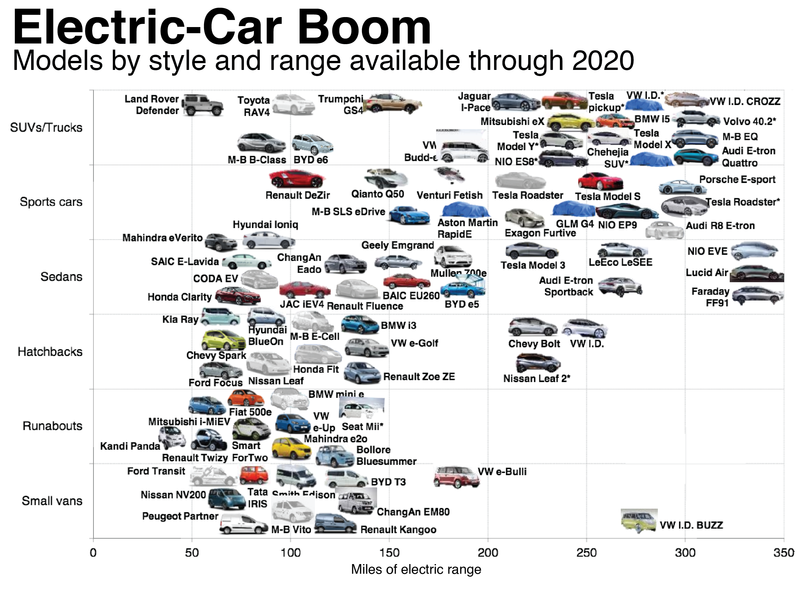

The car companies and 76 megafactories confirm the boom is coming

BNEF forecasts by 2020 there will be over 289 different models of

electric cars across the spectrum. Added to this will be electrification

across the entire transport sector (limited for planes) and widespread

adoption of energy storage (home, office, utility).

My purpose in this article is to encourage investors to think outside

the box, or to have a clearer view of the big picture. Demand levels of

50% electric cars by end 2022 once an electric car is cheaper to

buy/run/maintain would seem very logical.

Should this occur, then we will see an EV metals super-cycle. Waiting

lists for electric cars will become normal, battery shortages the norm,

and very strong EV metal prices a reality.

While 2018 and early 2019 have been bleak for the EV metal miner

stocks, I would encourage investors to think beyond 2019, and towards

2022 which is less than 3 years away. The quality EV metal miners that

are very oversold today may look like absolute bargains tomorrow.

I suggest to investors that 2019 is very likely the “calm before the storm of demand” for the EV metal miners.

Posted by AGORACOM-JC

at 9:00 PM on Sunday, May 12th, 2019

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is

equipped with a 623m deep shaft and has never been mined.

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits.

Plans for Kenbridge include updating PEA,

advancing the project through to feasibility and exploring the open

mineralization at depth

FULL DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM-JC

at 9:00 AM on Thursday, May 9th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

Tesla’s warning on battery mineral shortage addressed in new mining-reform legislation

Representatives in the US government who are both aware and focused on the shortage issue have introduced legislation in the Senate to address delays rooted in the federal approval process.

The bill, titled the “American Mineral Security Actâ€, was presented at the same closed-door conference where Tesla expressed its concerns last week.

Tesla is concerned about a global shortage of minerals required for

production of electric vehicle batteries, with the electric car maker

recently warning major industry players and US government

representatives of an upcoming mineral supply challenge due to

underinvestment in mining sources, according to a report published by Reuters.

Representatives in the US government who are both aware and focused on

the shortage issue have introduced legislation in the Senate to address

delays rooted in the federal approval process. The bill, titled the

“American Mineral Security Actâ€, was presented at the same closed-door

conference where Tesla expressed its concerns last week.

“Our bill takes steps that are long overdue to reverse our damaging

foreign dependence and position ourselves to compete in growth

industries like electric vehicles and energy storage,†Lisa Murkowski

(R-Alaska), the main sponsor of the bill,

said in a statement about the legislation. Senators Joe Manchin (D-W.

Virginia), Martha McSally (R-Arizona), and Dan Sullivan (R-Alaska) are

co-sponsors.

The bill specifically requires that a list of critical minerals be compiled

at least every three years along with a resource assessment of those

minerals nationwide. This data is then used to target and implement

reforms in the federal regulatory process aimed at reducing

government-driven delays in the mining approval process.

Aerial images of the Tesla Gigafactory as of August 28, 2018. [Credit: Joshua Mcdonald]

As a major consumer of minerals required for the production of

electric vehicle (EV) batteries and other vehicle parts, Tesla will need

stable access to mined resources like copper, nickel, and lithium in

the long term. The expansion of the EV market will continue to increase

demand for these resources. Other tech players such as Amazon and

Alphabet also need the same resources for the production of their

digital assistants and home connectivity devices.

Tesla’s global supply manager for battery metals, Sarah Maryssael,

spoke with representatives present at the industry conference about

Tesla’s concerns regarding the company’s mineral needs. Maryssael noted

that a “huge potential†existed for mining partnerships in Australia and

the US to help with the supply issue, possibly citing a preliminary

deal between the two countries for a joint effort towards research and

development in the area.

The global demand for copper, in particular, is expected to increase

from the current 38,000 tons per day to 1.5 million tons by 2030, and

this estimate has driven major copper production companies to expand its

mining activities in the US and Indonesia. Electric cars use twice as

much copper as gas-powered cars, making the EV industry particularly

sensitive to its market availability.

Tesla’s needs from the mineral industry go well beyond copper. The

company’s Nevada-based Gigafactory 1 facility is expected to hit 255 GWh

annual production of batteries once complete. At that rate, the current

global supply of lithium will need to increase nearly three times over

to meet the demand. Unlike copper, though, investments in lithium

production are ongoing, and Tesla’s ramping need for the mineral is

driving significant expansion in part of the mineral market.

Tags: CSE, nickel, nickel demand, small cap stocks, stocks, tsx, tsx-v Posted in Tartisan Nickel | Comments Off on Tartisan #Nickel $TN.ca – Tesla’s $TSLA warning on #battery mineral shortage addressed in new mining-reform legislation $ROX.ca $FF.ca $EDG.ca $AGL.ca $ANZ.ca

Posted by AGORACOM-JC

at 10:37 AM on Friday, May 3rd, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

Tesla warns of upcoming shortages of battery minerals, like nickel, copper, & lithium

Tesla is worried that there soon will be some upcoming global shortages of minerals used to make batteries for electric cars, like nickel, copper, and lithium.

The battery supply chain is an essential part of the electric revolution and the automakers who want to achieve mass production, like Tesla, need to be involved in every aspect of it.

Tesla is worried that there soon will be some upcoming global

shortages of minerals used to make batteries for electric cars, like

nickel, copper, and lithium.

The electric revolution in the auto industry is increasing the demand

for batteries at an incredible pace and in turn, it’s increasing the

demand for some specific minerals used in the production of li-ion

battery cells.

It’s difficult to understand just how big of an impact electric vehicles are on the battery market.

For example, Tesla became the world’s biggest battery consumer just a

few years after achieving volume production of its electric vehicles.

At a Benchmark Minerals Intelligence conference today in Washington,

Sarah Maryssael, Tesla’s global supply manager for battery metals, said

that the automaker is concerned about some of those minerals, according

to sources at the event via Reuters:

“Sarah Maryssael, Tesla’s global supply manager for battery metals,

told a closed-door Washington conference of miners, regulators and

lawmakers that the automaker sees a shortage of key EV minerals coming

in the near future, according to the sources.â€

Update: Reuters updated their story to that a Tesla

spokesman said: the comments were industry-specific and referring to the

long-term supply challenges that may occur with regards to these

metals.

Many companies are worried about cobalt, which is not widely mined.

Tesla uses less cobalt on average in its batteries than the rest of the

industry.

Instead, Tesla is more concerned with nickel even though its more widely mined around the world:

“Maryssael added, according to the sources, that Tesla will continue

to focus more on nickel, part of a plan by Chief Executive Elon Musk to

use less cobalt in battery cathodes. Cobalt is primarily mined in the

Democratic Republic of the Congo, and some extraction techniques –

especially those using child labor – have made its use deeply unpopular

across the battery industry, especially with Musk.â€

The Tesla executive also said that the automaker sees “huge potential†to work with mines in Australia or the United States.

The battery supply chain is an essential part of the electric

revolution and the automakers who want to achieve mass production, like

Tesla, need to be involved in every aspect of it.

Tesla knows that and it has been deeply involved down to the mining

level since embarking in the Gigafactory 1 project with Panasonic.

The company rarely comments on supply problems at the mineral level and when it has in the past, it mainly brushed off concerns.

That’s partly because cobalt has been the main concern for many

automakers and Tesla’s use in cobalt in its proprietary battery

chemistry is somewhat limited.

Nickel and copper are the most common minerals in its batteries, but there are also the most commonly mined.

It’s interesting that they are now warning that there could be

shortages. It’s another indication that the growth in the industry is

going to happen fast in the next few years with so many different mass

market EV programs in the work.

Those are good problems to have because they indicate that we are

going in the right direction and they are somewhat easily solvable. They

just require investments.

Posted by AGORACOM-JC

at 10:59 AM on Thursday, May 2nd, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

Nickel use in electric vehicle batteries has doubled year-on-year, according to research consultancy Adamas Intelligence.

Adamas said this week that 104% more nickel was deployed in new passenger EV batteries in February, up 104% year-on-year.

Manganese deployment was up by 96% and cobalt deployment was up 87% for the same period.

“While usage of all three cathode metals saw major gains from

February 2018 through February 2019, nickel enjoyed the greatest gains

on account of the auto industry’s ongoing shift from no or low-nickel

cathodes, such as LFP or NCM 111, to varieties with higher

concentrations of nickel, such as NCM 523, NCM 622, and NCM 811,” Adamas

said.

Batteries are still only estimated to account for less than 5% of global nickel demand.

The Tesla Model 3 accounted for more than 400 tonnes of nickel use in

February, followed by the Nissan Leaf, Tesla Model X, Tesla Model S and

Hyundai Kona.

The five models were responsible for almost 50% of all nickel deployed in EV batteries globally during February.

Adamas said lithium carbonate equivalent deployment in EV batteries rose by 76% year-on-year in February.

The top five cell suppliers by LCE deployed in February 2019 were

Panasonic, LG Chem, CATL, BYD and Samsung SDI, which accounted for

nearly 75% of all LCE deployed in passenger EV batteries.

Posted by AGORACOM-JC

at 10:03 AM on Thursday, April 18th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

Under a 100 percent renewable energy scenario, metal requirements could rise dramatically, requiring new primary and recycled sources

Clean technologies rely on a variety of minerals, principally cobalt, nickel, lithium, copper, aluminum, silver and rare earths. Cobalt, lithium and rare earths are the metals of most concern for increasing demand and supply risks

The growing demand for minerals and metals to build the electric vehicles, solar arrays, wind turbines and other renewable energy infrastructure necessary to meet the ambitious goals of the Paris Climate Agreement could outstrip current production rates for key metals by as early as 2022, according to new research by the UTS Institute for Sustainable Futures.

The study, commissioned and funded by U.S. non-profit organisation

EarthWorks, shows that as demand for minerals such as lithium and rare

earths skyrockets, the already significant environmental and human

impacts of hardrock mining are likely to rise steeply as well. In a

companion white paper, Earthworks makes the case for a broad shift in

the clean technologies sector towards more responsible minerals sourcing.

“We have an opportunity, if we act now, to ensure that our emerging clean energy

economy is truly clean – as well as just and equitable – and not

dependent on dirty mining,” said Payal Sampat, Earthworks Mining

Director. “As we scale up clean energy technologies in pursuit of our

necessarily ambitious climate goals, we must protect community health,

water, human rights and the environment.”

“The responsible materials transition will need to be scaled up just as ambitiously as the 100 percent renewable energy transition,” said Dr Sven Teske, Research Director at the UTS Institute for Sustainable Futures.

Doing so will require a concerted commitment from businesses and

governments, according to the report’s lead author Elsa Dominish, Senior

Research Consultant at the UTS Institute for Sustainable Futures. “We

must dramatically scale up the use of recycled minerals, use materials

far more efficiently, require mining operations to adhere to stringent,

independent environmental and human rights standards, and prioritise

investments in electric-powered public transit.

“The renewable energy transition will only be sustainable if it

ensures human rights for the communities where the mining to supply

renewable energy and battery technologies takes place. If manufacturers

commit to responsible sourcing this will encourage more mines to engage

in responsible practices and certification. There is also an urgent need

to invest in recycling and reuse schemes to ensure the valuable metals

used in these technologies are recovered, so only what is necessary is

mined,” Ms Dominish said.

Research highlights:

Under a 100 percent renewable energy scenario, metal requirements

could rise dramatically, requiring new primary and recycled sources

Clean technologies rely on a variety of minerals, principally

cobalt, nickel, lithium, copper, aluminum, silver and rare earths.

Cobalt, lithium and rare earths are the metals of most concern for

increasing demand and supply risks

Batteries for electric vehicles are the most significant driver of accelerated minerals demand.

Recycled sources can significantly reduce primary demand, but new

mining is likely to take place and new mining developments linked to

renewable energy are already underway

Responsible sourcing is needed when supply cannot be met by recycled sources

Minerals extraction already exacts significant costs on people and the environment, fuelling conflict and human rights

violations, massive water pollution and wildlife and forest

destruction. Most of the world’s cobalt, used in rechargeable batteries

for electric vehicles

and phones, is mined in the Democratic Republic of Congo, often by hand

in unsafe conditions using child labor. Earlier this year in Brazil,

the collapse of two tailings dams at Vale’s Brumadinho iron ore mine

killed hundreds of workers and local residents. Independent research

that analyses decades of data on mine waste dam failures reveals that

these catastrophic failures are occurring more frequently and are

predicted to continue to increase in frequency.

“In Norway, the government tell us we have to sacrifice our fjords to

mine copper for clean energy,” said Silje Karine Muotka, a member of

the Saami Parliament, which is fighting a mine proposal in their

traditional reindeer herding grounds. “I recognise that we need

materials for new technologies, but we should look for ways to get them

that do not harm the environment or threaten native culture.”

“Solar and wind production is growing rapidly, while the cost of clean energy technologies

has continued to fall,” said Danny Kennedy, Managing Director at the

California Clean Energy Fund. “If the clean tech revolution has taught

us anything, it is that humanity possesses boundless capacity for

innovation. Our task is to establish the parameters within which

innovators can innovate to ensure that clean energy is truly clean.”

Earthworks commissioned the ISF research as part of its

newly-launched ‘Making Clean Energy Clean, Just &

Equitable’ initiative, which aims to ensure that the transition to

renewable energy is powered

by responsibly and equitably sourced minerals, minimizing dependence on

new extraction and moving the mining industry toward more responsible

practices.

Posted by AGORACOM-JC

at 2:23 PM on Monday, April 15th, 2019

Investment Highlights

Kenbridge property has a measured and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33% copper

17.5 (21.8 fully diluted) percent equity stake in Eloro Resources and 2 percent NSR in their La Victoria property

Kenbridge Ni Project (ON, Canada)

Advanced stage deposit remains open in three directions, is

equipped with a 623m deep shaft and has never been mined.

Preliminary Economic Assessment completed and updated returned robust project economics and operating costs including a NPV of C$253M and cash costs of US$3.47/lb of nickel net of copper credits.

Plans for Kenbridge include updating PEA,

advancing the project through to feasibility and exploring the open

mineralization at depth

FULL DISCLOSURE: Tartisan Nickel Corp. is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM-JC

at 9:45 PM on Sunday, April 14th, 2019

SPONSOR: Tartisan Nickel (TN:CSE) Kenbridge Property has a measured

and indicated resource of 7.14 million tonnes at 0.62% nickel, 0.33%

copper. Tartisan also has interests in Peru, including a 20 percent

equity stake in Eloro Resources and 2 percent NSR in their La Victoria

property. Click her for more information

Healthy growth in nickel demand from the stainless steel and battery sectors and shrinking inventories on the Shanghai Futures Exchange and London Metal Exchange bode well for nickel prices

Nickel inventories at both LME and SHFE warehouses have been on a downward trajectory since 2018

Stainless steel demand still dominates, but EV sector grows faster

By: Violet Li

Healthy growth in nickel demand from the stainless steel and

battery sectors and shrinking inventories on the Shanghai Futures

Exchange and London Metal Exchange bode well for nickel prices,

Macquarie Capital senior commodities consultant Jim Lennon said.

“Our view is that we have these two drivers in demand: stainless steel

and batteries, and nickel inventories have been falling over the last

few years. I think it will [continue to] fall over the next few years;

the nickel market will remain in a deficit between supply and demand,

which should push prices higher,†Lennon said at Fastmarkets Battery

Materials Conference in Shanghai on Thursday April 11.

Lennon did not give a breakdown of the forecast price at the presentation.

Nickel inventories at both LME and SHFE warehouses have been on a

downward trajectory since 2018. LME nickel stocks totaled 182,446 tonnes

as of April 1, down by 50% from 368,430 tonnes on January 1, 2018.

Meanwhile, nickel stocks in SHFE-approved warehouses fell by 80% during

the same period, to 9,749 tonnes on April 4 from 48,920 tonnes on

January 1, 2018.

Lennon concluded the large decline in stock levels reflects deficits and some financial buying of stocks.

“Last year there’s probably about 50,000 tonnes of inventories

transferred from the LME warehouses in Asia into non-reported

inventories in Europe, held by banks and traders, partly for reasons of a

positive outlook for the market or better premiums in the European

area,†Lennon said.

Stainless steel demand still dominates, but EV sector grows faster Stainless

steel takes up 70% of global nickel usage compared with a small

fraction of 6% of nickel used by the electric vehicle (EV) sector,

Lennon said. But EV demand growth is speeding up, he said.

“Total world production of stainless steel in 2016 grew by 8.5%, 2017 by

6% and last year by 5%. This year, our projection is 3.5-4%, so we do

see some slowdown but still a steady growth rate. Nickel usage in

batteries will grow by 30-40% [in 2019], so the underlying growth in

nickel [consumption] continues to be quite impressive,†Lennon said.

Notably, more nickel briquette was used in the EV sector following

rising demand for batteries and this has raised the nickel briquette

premium over the past year.

Fastmarkets MB’s monthly duty-free

nickel briquette premium cif Shanghai stood at $240-270 per tonne at the

end of March, up from $220-260 per tonne at the launch of the

assessment in August last year.

Nickel briquette is the one of

the main raw materials of nickel sulfate, a key material used in the

production of nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminium

(NCA) batteries used in EVs.