Posted by AGORACOM-JC

at 9:17 AM on Thursday, July 25th, 2019

The Genesis PGM Project is a road accessible, under explored, highly prospective multi-prospect drill ready Pd-Pt-Ni-Cu property that warrants initial drilling, additional surface mapping, sampling to expand the known footprint of mineralization and to determine the ultimate size and grade of the layered mineralization outlined to date.

A 3-phase summer work program has been initiated on the project which is intended to map potential hydrothermal alteration anomalies and define structural domains to better define drill targets on the Project.

A mineralized horizon has been identified in outcrop sampling for 850 m along strike and a 40 m true thickness. (for more information please click to the April 18, 2018 news release).

The identification of two different styles of PGM/ Multi-Element mineralization at Sheep Hill suggests that multiple mineralizing events have occurred.

NAM management is actively seeking an option/joint-venture partner for this road accessible PGM/Multiple Element Project using the Prospector Generator business model.

July 25th, 2019 – Rockport, Canada – New Age Metals Inc. (TSXV:NAM)(OTC:NMTLF)(FSE:P7J) is pleased to announce it has engaged Avalon Development Corp (Avalon) of Alaska, USA to carry out a field work program on its Genesis PGM-Ni-Cu Project in Alaska.

Genesis Project Summer 2019 Field Program

The summer 2019 field program on

Genesis is intended to map hydrothermal alteration to better define

drill targets on the Project and will be comprised of 3 phases of work;

ASTER Imaging and Interpretation, Landsat TM Imagery Processing and

Interpretation and ground induced polarization, Airborne Magnetics and

EM Reinterpretation. A detailed description of each phase of work

follows:

Phase 1: ASTER Imaging and Interpretation

The main objective of the ASTER (Advanced

Spaceborne Thermal Emission and Reflection Radiometer) processing and

interpretation is to map potential alteration targets to aid

district-scale PGM-Cu-Ni sulfide exploration. The end goal of this phase

is to generate 3 false color images: a 15-meter false-color image

composed of three VNIR bands, a 30-meter false-color image composed of

three SWIR bands, and a 90-meter false-color image composed of three TIR

bands. Each false-color image is designed to enhance the alteration

targets so they show up distinctively as color anomalies.

Phase 2: Landsat TM Imagery Processing and Interpretation

Interpret potential general clay alteration

targets and potential iron-oxide alteration targets to generate a

30-meter true-color image to aid visual interpretation of the iron-oxide

targets.

Phase 3: Airborne Magnetics and EM Reinterpretation

1. Reprocess existing State of Alaska

airborne magnetic data in 2D and 3D formats to outline chromite-bearing

PGM accumulations and identify structural domains.

2. Reprocess existing State of Alaska

airborne EM data in 2D and 3D formats to outline PGM-Cu-Ni sulfide

conductors and identify structural domains.

3. Reprocessing of a limited ground IP

program completed over the Sheep Hill prospect area to better define

strucutural details and target PGM-Cu-Ni sulfide-bearing horizons.

Merits of the Genesis PGM Project

The Genesis PGM Project is an under explored, highly prospective multi-prospect drill ready Pd-Pt-Ni-Cu property

that warrants follow-up drilling, additional surface mapping, sampling

to expand the known footprint of mineralization and to determine the

ultimate size and grade of the layered mineralization outlined to date.

The stable land status, ease of access and superb infrastructure make

this project prospective for year-around exploration, development and

production.

Significant aspects of the Genesis PGM Project include:

– Drill

ready PGM-Ni-Cu reef style target with 2.4 grams/ton Palladium (Pd), 2.4

grams/ton Platinum (Pt), 0.96% Nickle (Ni), and 0.58% Copper (Cu).

– Reef mineralization is open to the west, east, north, and at depth

– Mineralized reef identified in outcrop for 850 m along strike and a 40 m true thickness

– Separate style of chromite mineralization contains Platinum Group Metals (PGM) up to 2.5 g/t Pd and 2.8 g/t Pt.

– Known PGM mineralization covers a distance of 9 km across the prospect.

– No historic drilling has been done on the project.

– Project is within 3 km of a paved highway and electric transmission line.

– Project is on stable State of Alaska claims.

– Fraser Institute’s 2017 survey of mining companies has Alaska ranked as the 10th best jurisdiction in the world for mining.

Click Image To View Full Size

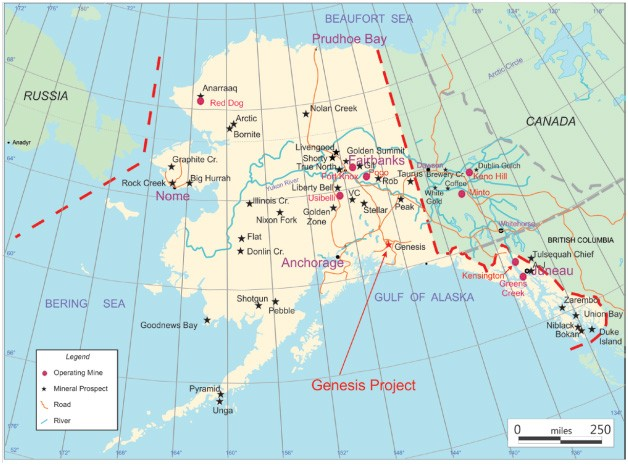

Figure 1: Location of the Genesis Project, Nelchina Mining

District, Alaska. The Genesis project is a Ni-Cu-PGM property located

in the northeastern Chugach Mountains, 75 road miles north of the city

of Valdez, Alaska. The project is within 3 km of the all-season paved Richardson Highway and a high capacity electric power line. The project is covered by 4,144 hectares (10,240 acres) of State of Alaska mining claims owned 100% by New Age Metals.

ABOUT NAM’S PGM DIVISION

NAM’s flagship project is its 100% owned River Valley PGM Project (NAM Website – River Valley Project)

in the Sudbury Mining District of Northern Ontario (100 km east of

Sudbury, Ontario). Recently the company announced the results of the

first PEA (see News Release – June 27th, 2019) completed on the River Valley Project. The

PEA has been developed by various independent consultants – P&E

Mining Consultants Inc. (P&E) was responsible for the open pit

mining, surface infrastructure, tailings facility, and project

economics; DRA Americas Inc. (“DRA”) was responsible for all

metallurgical test work and processing aspects of the Project; and WSP

Canada Inc. (“WSP”) was responsible for the Mineral Resource Estimate. The

PEA is a preliminary report but it has demonstrated that there are

positive economics for a large-scale mining open pit operation, with 14

years of Palladium and Platinum production.

On April 4th, 2018, NAM signed an agreement with one of Alaska’s top geological consulting companies. The companies stated objective is to acquire additional PGM and Rare Metal projects in Alaska. On April 18th, 2018,

NAM announced the right to purchase 100% of the Genesis PGM Project,

NAM’s first Alaskan PGM acquisition related to the April 4th

agreement. The Genesis PGM Project is a road accessible, under

explored, highly prospective, multi-prospect drill ready Palladium (Pd)-

Platinum (Pt)- Nickel (Ni)- Copper (Cu) property. A

comprehensive report on previous exploration and future phases of work

was completed by Avalon Development of Fairbanks Alaska in August 2018

on Genesis.

On August 29, the Avalon report was submitted to NAM, management is actively seeking an option/joint-venture partner for this road accessible PGM and Multiple Element Project using the Prospector Generator business model.

QUALIFIED PERSON

The contents contained herein that relate

to Exploration Results or Mineral Resources is based on information

compiled, reviewed or prepared by Curt Freeman, a consulting

geoscientist for New Age Metals. Mr. Freeman is the Qualified Person as

defined by National Instrument 43-101 and is the owner of Avalon

Development Corp. and Anglo Alaska Gold Corp, which is the vendor of the

Genesis PGM Project. Mr. Freeman has reviewed and approved the

technical content of this news release.

On behalf of the Board of Directors “Harry Barr” Harry G. Barr Chairman and CEO

Neither the TSX Venture Exchange

nor its Regulation Services Provider (as that term is defined in the

policies of the TSX Venture Exchange) accepts responsibility for the

adequacy or accuracy of this release.

Cautionary Note Regarding Forward

Looking Statements: This release contains forward-looking statements

that involve risks and uncertainties. These statements may differ

materially from actual future events or results and are based on current

expectations or beliefs. For this purpose, statements of historical

fact may be deemed to be forward-looking statements. In addition,

forward-looking statements include statements in which the Company uses

words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”,

“confident”, “intend”, “strategy”, “plan”, “will”, “estimate”,

“project”, “goal”, “target”, “prospects”, “optimistic” or similar

expressions. These statements by their nature involve risks and

uncertainties, and actual results may differ materially depending on a

variety of important factors, including, among others, the Company’s

ability and continuation of efforts to timely and completely make

available adequate current public information, additional or different

regulatory and legal requirements and restrictions that may be imposed,

and other factors as may be discussed in the documents filed by the

Company on SEDAR (www.sedar.com), including the most recent reports that

identify important risk factors that could cause actual results to

differ from those contained in the forward-looking statements. The

Company does not undertake any obligation to review or confirm analysts’

expectations or estimates or to release publicly any revisions to any

forward-looking statements to reflect events or circumstances after the

date hereof or to reflect the occurrence of unanticipated events.

Investors should not place undue reliance on forward-looking statements.

Posted by AGORACOM-JC

at 11:31 AM on Thursday, June 27th, 2019

Life of mine (LOM) of 14 years, with 6 million tonnes annually of potential process plant feed at an average grade of 0.88 g/t Palladium Equivalent (PdEq) and process recovery rate of 80%, resulting in an annual average payable Pd production of 119,000 ounces

Pre-Production capital requirements: $495 M

Undiscounted cash flow before income and mining taxes of $586M

Undiscounted cash flow after income and mining taxes of $384M

June 27th, 2019 – Rockport, Canada – New Age Metals Inc. (NAM) (TSX.V: NAM; OTCQB: NMTLF; FSE: P7J.F) Harry Barr, Chairman & CEO, stated; “We are pleased to update our shareholders and interested parties as to the results of the initial Preliminary Economic Assessment (PEA) for the company’s 100% owned River Valley PGM Project in Sudbury, Ontario Canada. The PEA has been developed by various independent consultants – P&E Mining Consultants Inc. (P&E) was responsible for the open pit mining, surface infrastructure, tailings facility, and project economics; DRA Americas Inc. (“DRA”) was responsible for all metallurgical test work and processing aspects of the Project; and WSP Canada Inc. (“WSP”) was responsible for the Mineral Resource Estimate. The PEA demonstrates positive economics for a large-scale mining open pit operation, with 14 years of Palladium and Platinum production.”

Go-Forward Plan: In

order to enhance the Project, the PEA has outlined a phased work

approach to completing a Pre-Feasibility study. This includes advanced

metallurgical testing to improve / confirm process recoveries and more

accurately estimate concentrate grades, geotechnical logging of drill

core, with new geotechnical holes to create a 3D geomechanical block

model and estimate pit wall angles, hydrogeological studies that will

estimate water inflows to the open pits and generate a site water and

management plan. The Pre-Feasibility study will update the Project study

to a higher level of precision.

NAM plans to continue to improve

the River Valley Project’s value proposition by drill testing

geophysical anomalies found during the 2018 geophysics campaign,

continuing the geophysical program throughout the 16 kilometres of the

contact mineralization adding significant potential to find new

deposits, drilling near the defined open pit shells to increase the mine

life, drilling deeper to test the open-ended Deposit at depth, and

re-assaying existing drill core for Rhodium in order that Rhodium may be

added to the Project’s metal suite.

Technical Report: For

readers to fully understand the information in this news release, they

should read the PEA Technical Report in its entirety which the Company

expects to file in accordance with NI 43-101 within 45 days from the

date of this news release on SEDAR (www.sedar.com)

and it will also be available at that time on the New Age Metals

website, including all qualifications, assumptions and exclusions that

relate to the PEA. The Technical Report is intended to be read in its

entirety, and sections should not be read or relied upon out of context.

PEA Highlights (CDN$ unless otherwise noted):

– Life of mine (LOM) of 14 years,

with 6 million tonnes annually of potential process plant feed at an

average grade of 0.88 g/t Palladium Equivalent (PdEq) and process

recovery rate of 80%, resulting in an annual average payable Pd

production of 119,000 ounces

– Pre-Production capital requirements: $495 M

– Undiscounted cash flow before income and mining taxes of $586M

– Undiscounted cash flow after income and mining taxes of $384M

– Average unit operating cost of $19.50/tonne over the life-of-mine

– LOM average operating cash cost

of $971 per ounce (US$709/oz) and all-in sustaining cash cost of $972

per ounce (US$709/oz) at a 1.37 CDN: USD exchange rate.

– A mining contractor will be engaged for the open pit mining

– Pre-tax NPV (5%): $262M, After-tax NPV (5%): $139 M

– Pre-tax IRR: 13%, After-tax IRR: 10%

– Assumed metal prices of US$1,200/oz Pd, US$1,050/oz Pt, US$1,350/oz Au, US$3.25/lb Cu, US$8.00/lb Ni, US$35/lb Co

– Using a + 20% Pd price

sensitivity (to the base case of US$1,200/oz Pd) US$1,440 /oz Pd returns

a pre-tax IRR of 19% and an after tax-IRR of 15%. Palladium price as of June 25, 2019 is US$1,510/oz Pd, which would return a pre-tax IRR of 21% and an after-tax IRR of 16%.

– River Valley process plant feed will be treated by a conventional sulphide flotation process plant to produce a single saleable PGM concentrate that will be transported to the Sudbury area for smelting/refining

– Potential for up to 325 jobs at the peak of production

PEA Summary

The PEA parameters are summarized in Table 1.

(*) Cautionary statement NI 43-101:

The PEA was prepared in accordance with National Instrument 43-101

Standards of Disclosure for Mineral Projects (“NI 43-101”). Readers are

cautioned that the PEA is preliminary in nature. It includes Inferred

Mineral Resources that are considered too speculative geologically to

have the economic considerations applied to them that would enable them

to be categorized as Mineral Reserves, and there is no certainty that

the PEA will be realized. Mineral Resources that are not Mineral

Reserves do not have demonstrated economic viability. All currency is stated as CDN$ unless stated otherwise.

Table 1: PEA Summary Parameters

Assumptions

Palladium Price (Base case) US$/oz

1,200

Exchange Rate US$:CDN$

1.37

Production Profile

Total Tonnes Processed

78,100,000

Process Plant Head Grade PdEq g/t

0.88

Mine Life (years)

14

Daily process plant throughput (tpd)

16,440

Palladium Process Plant Recovery

80%

Total Payable Palladium Equivalent Ounces

1,600,000

Average annual Palladium Production Ounces

119,000

Operating Costs

Unit Operating Costs (per tonne processed)

19.50

Mining Costs

10.20

Processing Costs

8.44

G&A

0.90

LOM Average Cash Cost US$/oz

709

Capital Requirements

Pre-Production Capital Cost

$495.1 M

Sustaining Capital Cost (Life of Mine) Including Salvage

$1.0 M

Project Economics

Royalties

3% (Buy down to 1.5% with $1,500,000 payment)

Royalty Payable After $1.5M Payment

$39.7 M

Taxes

$202.3 M

Pre-Tax

NPV (5% Discount Rate)

$262 M

IRR

13%

Payback (years)

6.6

Cumulative Undiscounted Cash Flows

$586 M

After-Tax

NPV (5% Discount Rate)

$139 M

IRR

10%

Payback (years)

7.0

Cumulative Undiscounted Cash Flows

$384 M

Operating Cost

Table 2: Operating Cost Summary.

OPERATING COST

LOM ($/t)

Mining Cost

$/t material

2.28

Mining Cost

$/t feed

10.20

Processing Cost

$/t feed

8.44

G&A

$/t feed

0.90

Unit Operating

$/t feed

19.50

Capital Cost

Table 3: Capital Cost Summary

Development Capital

Initial (Y-2, Y-1) ($ M)

Sustaining ($’ M)

Total LOM ($’ M)

Mine Pre-Stripping

17.3

17.3

Process Plant Incl. Indirects

401.3

401.3

TMF

8.0

8.0

Mine Site Infrastructure

10.0

10.0

Office, Warehouse, Shops

10.0

10.0

Owner Cost

5.0

5.0

10% Contingency

43.4

43.4

Initial Project Capital

495.1

495.1

Sustaining Capital

Closure Bond

26.0

26.0

Salvage Value

-25.0

-25.0

Total Sustaining Capital

1.0

1.0

Total Capital

495.1

1.0

496.1

Project Economics and Sensitivities

The economic results of the PEA are

summarized in Table 4 on an after-tax basis. The sensitivities and the

impact of cash flows have been calculated for +/- 20% variations against

the base case.

Table 4: Project Economics Sensitivity.

Project Sensitivity Analysis

Pd Price Sensitivity

%

-20%

-15%

-10%

-5%

Base Case

+5%

+10%

+15%

+20%

Spot

US$/oz

960

1,020

1,080

1,140

1,200

1,260

1,320

1,380

1,440

1,510

NPV (CDN$ M)

-23

16

59

98

139

179

220

260

300

347

IRR (%)

4

6

7

8

10

11

12

13

15

16

OPEX Sensitivity

%

-20%

-15%

-10%

-5%

Base Case

+5%

+10%

+15%

+20%

Cost Per Tonne

16

17

18

18

19

20

21

22

23

NPV (CDN$ M)

212

194

175

157

139

120

102

83

68

IRR (%)

14

12

11

10

10

9

8

7

7

CAPEX Sensitivity

%

-20%

-15%

-10%

-5%

Base Case

+5%

+10%

+15%

+20%

CAPEX (CDN$ M)

397

422

446

471

496

521

546

570

595

NPV (CDN$ M)

284

248

212

175

139

102

64

28

-6

IRR (%)

14

13

12

11

10

8

7

6

5

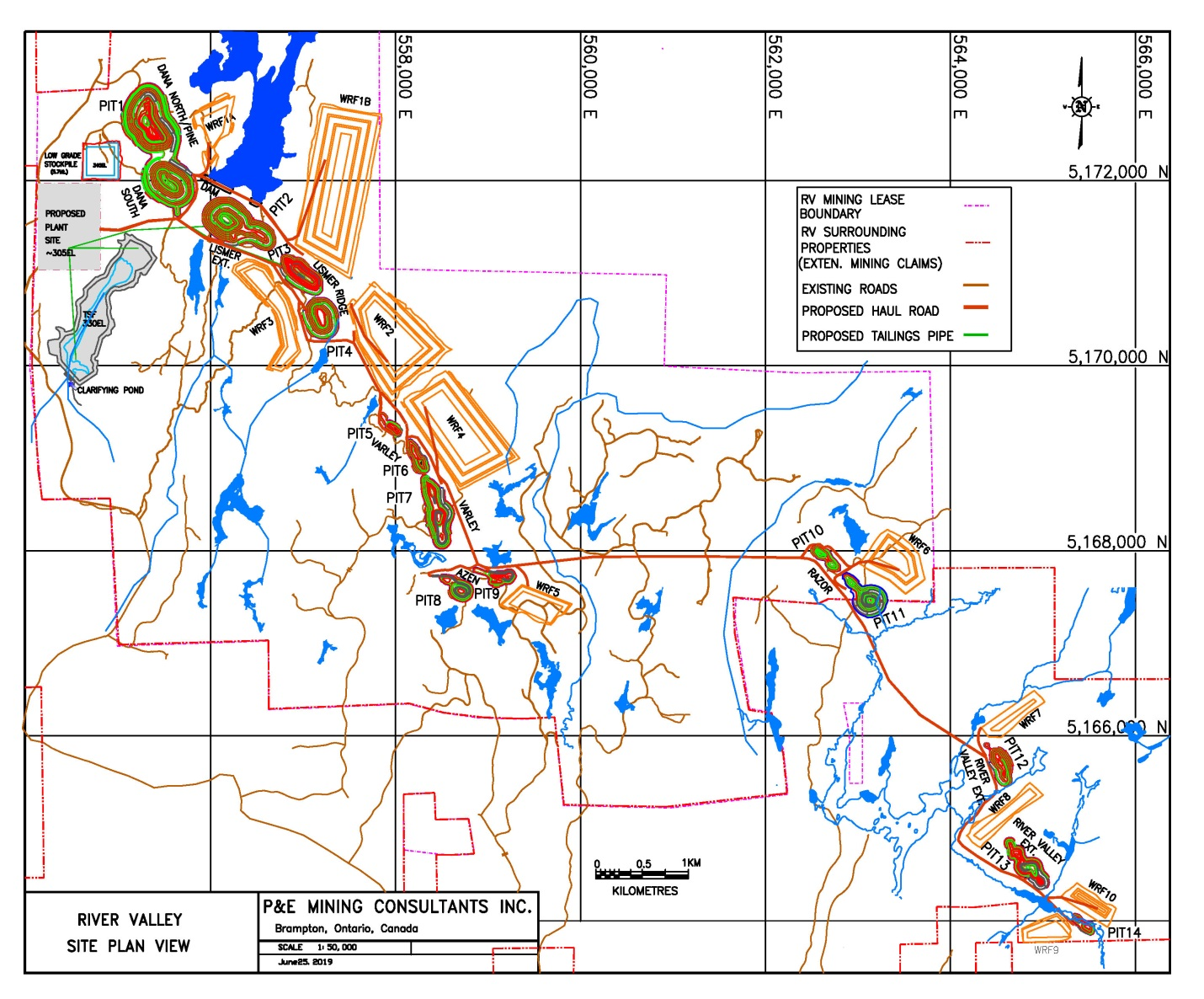

River Valley Project Site Plan

See the image below that shows a site

plan from the River Valley PEA. The map shows all of the 14 open pits

that have been used in the engineering design of the Project as well as

the proposed process plant site, low-grade stockpile, waste rock storage

facilities, tailings storage facility and site infrastructure.

Click Image To View Full Size

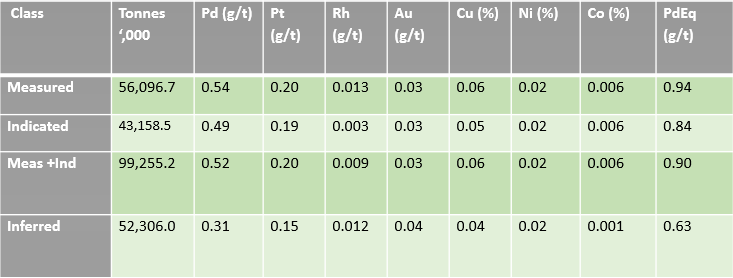

Mineral Resource

The pit constrained Mineral Resource

Estimate which formed the basis of the PEA, is set out in Table 5 and

was prepared by WSP under the supervision of Todd McCracken, P. Geo., an

“Independent Qualified Person”, as defined in NI 43-101. The effective

date of this Mineral Resource Estimate is January 9, 2019. The Mineral

Resource database contains 710 boreholes with 106,554 assays records in

the database, and 2,642 surface channel samplings. The Mineral Resource

Estimate update was completed on the Dana North, Dana South, Pine,

Banshee, Lismer, Lismer Extension, Varley, Azen, Razor, and River Valley

Extension Zones, using the ordinary kriging (OK) methodology on a

capped and composited borehole dataset consistent with industry

standards. Validation of the results was conducted thought the use of

visual inspection, swath plots and global statistical comparison of the

model against inverse distance squared (ID2) and nearest neighbour (NN) models.

Table 5: Pit Constrained Mineral Resource Estimate for River Valley PGM Project – Effective January 9, 2019.

Click Image To View Full Size

Class

PGM + Au (oz)

PdEq (oz)

PtEq (oz)

Measured

1,394,000

1,701,000

1,701,000

Indicated

983,000

1,166,000

1,166,000

Meas +Ind

2,377,000

2,867,000

2,867,000

Inferred

841,000

1,059,000

1,059,000

Notes:

1.CIM definition standards were followed for the Mineral Resource Estimate.

2.The 2018 Mineral

Resource models used Ordinary Kriging grade estimation within a

three-dimensional block model with mineralized zones defined by

wireframed solids.

3.A base cut-off

grade of 0.35 g/t PdEq was used for reporting Mineral Resources in a

constrained pit and 2.00 g/t PdEq was used for reporting the Mineral

Resources under the pit.

6.Mineral Resources that are not Mineral Reserves do not have economic viability

7. The Inferred

Mineral Resource in this estimate has a lower level of confidence than

that applied to an Indicated Mineral Resource and must not be converted

to a Mineral Reserve. It is reasonably expected that the majority of the

Inferred Mineral Resource could be upgraded to an Indicated Mineral

Resource with continued exploration.

Mining and Processing

The PEA is preliminary

in nature, and includes Inferred Mineral Resources that are considered

too speculative geologically to have the economic considerations applied

to them that would enable them to be categorized as

Mineral Reserves. There is no certainty that the Preliminary Economic

Assessment will be realized.

The River Valley Project is expected

to be mined by a contractor. Initial mining will occur at the northwest

end of the Deposit, close to the proposed process plant site. A series

of 14 open pits will be mined, and will progress in a southeasterly

direction. Pit numbers 1 to 4 contain the bulk of the mineralized

process plant feed.

Annual process plant feed of up to 6

Mtpy (0.5 Mtpm) is planned, at an average strip ratio of 3.6:1 over the

life-of-mine. It is anticipated that a fleet of 221 t haul trucks, 29 m3

excavators and 254 mm diameter hole rotary drills will be utilized,

following industry standard conventional open pit mining techniques.

The process plant is designed to

produce a single saleable PGM concentrate using conventional sulphide

flotation techniques. The concentrate will be trucked to a

smelter/refinery in the Sudbury area.

The Run-Of-Mine (ROM) feed from the

mine will be crushed in a single primary jaw crushing stage prior to the

grinding circuit. The crusher discharge will be conveyed to a live

stockpile, which will provide an operating buffer between the crushing

and grinding circuits.

The grinding circuit will consist of a SAG mill in closed circuit with a pebble crusher and two ball mills in parallel.

The process plant design considers

three stages of cleaner flotation and is designed to process 21,920 tpd

(6.0 Mtpy) of ROM feed.

The flotation circuit configuration and design are based on the locked cycle tests conducted by SGS Canada in 2013.

Concentrate and tailings products

will be dewatered using high-rate thickeners and the concentrate will be

further dewatered by conventional plate and frame vacuum filtration.

Process water will be recovered from

the concentrate and tailings thickener overflow. Raw water is assumed to

be sourced from the local environment and will be used as makeup water.

It is assumed that 10% of the raw water requirement will be recycled

from the tailings pond.

Conventional tailings deposition techniques will be utilized.

A 230 kV transmission line is located

passing through the village of Warren, approximately 22 km from the

Project. A 115 kV transmission line passes through the village of Field,

located approximately 15 km to the east of the Project. It is assumed

that electrical power will be provided by the local utility via either

of these overland power lines. Diesel generators will be used to supply

emergency power.

Project Enhancement Opportunities

The PEA demonstrates that River

Valley has the potential to be economically viable. The PEA also

outlines several opportunities to enhance Project value. Additional

opportunities include:

Area of Focus

Opportunities to Explore

Management Target

Geotechnical study

– Geotechnical logging of drill core,

with new geotechnical holes to create a 3D geomechanical block model

and estimate pit wall slope angles

– Estimate pit wall slopes

Hydrogeological study

– Estimate water in-flows to the open pits and generate a site water management plan

– Site water management plan

Increase the Project Mineral Resource base

– Additional drilling in the footwall to expand the Mineral Resource.

After the ground proofing and surface exploration program conducted in

Summer 2018 which followed up on the most recent induced polarization

geophysical survey by Abitibi, NAM management has designed a 3-phase

5,000 metre drill program to test the new geophysical anomalies. See the

map figure below which shows these new geophysical anomalies and

potential targets for the next stage of drilling at River Valley

superimposed over the upper 4 kilometres of the project map.

Click Image To View Full Size

– Drilling near the defined open pit shells to increase the mine life.

– Drilling deeper to test the open-ended deposit at depth. Average drill hole depth is 220 metres below surface.

– Increase tonnes, grade and mine life of Project

– Continue to drill recent footwall discoveries

– Add additional Mineral Resources to the Project.

Mineral Resource

– In-fill drilling to convert Inferred Mineral Resources to Indicated Mineral Resources

– Improve Mineral Resource classification

Mineral Resource

– Step-out drilling to increase the Mineral Resource Estimate

– Increase the size of the Mineral Resource Estimate

Metallurgical testing

– Advanced metallurgical testing to

confirm or potentially improve process recoveries and more accurately

estimate concentrate grades produced

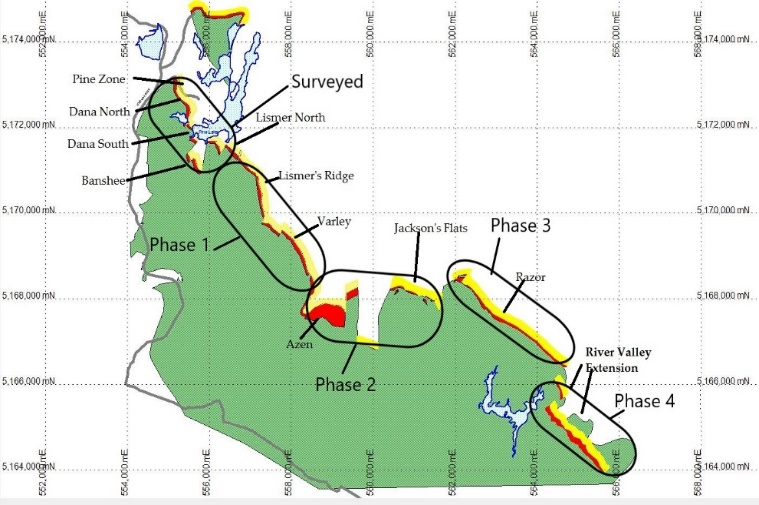

– Achieve a process recovery equal or greater than 80%.

Geophysical surveys

– Continue with induced polarization

geophysical surveys over the 12.5 kilometres of the contact / footwall

that has not been surveyed in the 2017 and 2018 programs

conducted on the Project. This work can be carried out in phases as

funding is available or until the contact / footwall is covered, see the

map figure below that shows a proposed scenario for how to phase the

work.

Click Image To View Full Size

– Outline new targets highlighting new potential footwall discoveries over the entire Project

Advanced sampling for Rhodium

– Re-assaying existing core for

Rhodium. Rhodium has been identified, however, insufficient assaying in

the past has not allowed for Rhodium’s inclusion in the Mineral Resource

Estimate.

– Quantify the amount of Rhodium in the Project and add this to the existing Mineral Resource Estimate

Pre-Feasibility study

– Updated Mineral Resource Estimate,

optimize the mine plan, process plant design, and Project economics.

Address environmental aspects.

– Update the Project study to a higher level of precision

Qualified Persons and NI 43-101 Disclosure

The PEA was prepared under the supervision

of Eugene Puritch, P.Eng. of P&E Mining Consultants Inc. The Mineral

Resource Estimate was prepared by Todd McCracken, P.Geo. of WSP Canada

Inc. Metallurgical testwork and process plant design and cost estimates

were prepared by Jim Kambossos, P. Eng. of DRA Americas

Inc. All three are independent Qualified Persons in accordance with NI

43-101. Mr. Puritch has reviewed and approved the technical information

in this release. Michael Neumann, P.Eng. Managing Director for NAM is

the company Qualified Person as defined by National Instrument 43-101

and has reviewed and approved the technical content of this news

release.

On behalf of the Board of Directors

“Harry Barr”

Harry G. Barr, Chairman and CEO

For further information on New Age Metals,

please contact Harry Barr and/or Anthony Ghitter, Business Development

at 613-659-2773, or [email protected]

Neither the TSX Venture Exchange nor

its Regulation Services Provider (as that term is defined in the

policies of the TSX Venture Exchange) accepts responsibility for the

adequacy or accuracy of this release.

Cautionary Note Regarding Forward

Looking Statements: This release contains forward-looking statements

that involve risks and uncertainties. These statements may differ

materially from actual future events or results and are based on current

expectations or beliefs. For this purpose, statements of historical

fact may be deemed to be forward-looking statements. In addition,

forward-looking statements include statements in which the Company uses

words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”,

“confident”, “intend”, “strategy”, “plan”, “will”, “estimate”,

“project”, “goal”, “target”, “prospects”, “optimistic” or similar

expressions. These statements by their nature involve risks and

uncertainties, and actual results may differ materially depending on a

variety of important factors, including, among others, the Company’s

ability and continuation of efforts to timely and completely make

available adequate current public information, additional or different

regulatory and legal requirements and restrictions that may be imposed,

and other factors as may be discussed in the documents filed by the

Company on SEDAR (www.sedar.com), including the most recent reports that

identify important risk factors that could cause actual results to

differ from those contained in the forward-looking statements. The

Company does not undertake any obligation to review or confirm analysts’

expectations or estimates or to release publicly any revisions to any

forward-looking statements to reflect events or circumstances after the

date hereof or to reflect the occurrence of unanticipated events.

Investors should not place undue reliance on forward-looking statements.

Posted by AGORACOM-JC

at 10:52 AM on Tuesday, June 25th, 2019

SPONSOR: New Age Metals Inc. The company’s Lithium Division has already made significant acquisitions in Canada and the USA. The company also owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces in the Inferred. Learn More.

NAM: TSX-V

———————

China’s breaking up the EV battery monopoly it carefully created

As China phases out subsidies

for electric vehicles next year, it’s also ending a related policy that

effectively shut out foreign battery makers, creating the domestic

monopoly we see today.

China’s Ministry of Industry and Information Technology (MIIT) announced yesterday

(June 25, link in Chinese) it is dropping its practice of publishing

lists of battery makers that met technical standards. The policy, put in

place in 2015, was meant to help develop the industry. Supplying the

information to get on the list was supposedly voluntary

(link in Chinese), but in reality, using the batteries on the

ministry’s lists made it more likely car makers would qualify for

government subsidies. As of 2016, the last time the list was updated, it

included a total of 57 companies—none of them foreign firms.

As a result, the top 10 battery makers powering the world’s largest EV market are all Chinese

(link in Chinese), according to 2018 data from the China Battery

Industry Association. That means China dominates the value-added chain

for domestically made electric vehicles, since batteries contribute 40%

of the cost of an EV—quite a contrast to the value added when China assembles an iPhone.

Financial newspaper Economic Observer noted

(link in Chinese) in April last year that Chinese car makers made their

component decisions from the lists, while local governments and

investment firms also consulted them. “Associated with subsidies, these

became known as the ‘white lists,’†the newspaper said.

The lists included CATL, the world’s largest EV battery maker

(Quartz membership), which supplies Chinese and foreign carmakers that

include state-owned BJEV, one of the country’s biggest manufacturers,

Volkswagen, Daimler, BMW, Honda, and Shanghai-based startu NIO.

The world’s biggest EV manufacturer, BYD, is also the country’s

second-biggest battery supplier, since it makes the batteries for its

own electric cars—last year it sold some 100,000 of them. Both BYD and CATL could supply batteries to Toyota cars soon. In third place is Guoxuan High Tech, a major supplier to state-owned carmaker BAIC Motor, the parent company of BJEV.

Taking away the lists could benefit established foreign battery

makers. “It’s a gesture of China opening up, along with pressure from

G20 and trade,†says Qiu Kaijun, who runs an EV news blog

(Quartz membership). Chinese president Xi Jinping is set to discuss

US-China trade tensions with US president Donald Trump on the sidelines

of the G20 meeting of leaders of top economies, which begins in Japan

Friday.

Before the policy was put in place, when China’s EV market was starting to take off, foreign firms like LG and fellow South Korean major Samsung were about to expand

(link in Chinese) in China. In 2015, LG had opened a battery factory in

China’s eastern city Nanjing that could supply to more than 100,000 EVs (link in Chinese), yet it never got on the white list and the factory ended up being sold to Zhejiang-based carmaker Geely in 2017 (link in Chinese).

“Earlier, all the subsidies went to those using Chinese EV

batteries—if you use LG and Samsung, you won’t get subsidies,†said

Angus Chan, a Shanghai-based auto analyst at Bocom International, “When

2020 comes, it will be free-market competition. It’s straightforward for

carmakers—energy density, safety, and price… Everybody is on the same

racing starting point in the post-subsidy era.â€

China began reducing its massive subsidies two years ago, and will move to a credit system next year.

The scrapping of the battery lists comes at a time when China has

rolled out the welcome mat for foreign EV firms in other ways. China last year said it would phase out

foreign investment limits for car manufacturing, a rule that earlier

made it impossible for foreign car makers to set up shop in China

without a local partner. That reform began with manufacturers of

electric vehicles, allowing Tesla to become the first foreign car maker

with a wholly-owned plant in China. Located in Shanghai, it is taking

orders for the first made-in-China Teslas, which are expected to roll out in the next six months.

Other new rules limiting the number of new factories in a province

mean Tesla’s factory has put a spanner in the works for local

manufacturers who were also hoping to set up near one of the country’s

most important cities for EV sales. It’s clear China’s EV industry is

going to put under greater pressure as a result of these moves—which

could improve their technologies, or kill off some of the weaker firms.

“What happens after the typhoon passes?†asked Zeng Yuqun, CATL’s founder, in an internal email (link in Chinese) in 2017. “Can a pig really fly?â€

He was referring to a Chinese allegory—“When the typhoon comes, the

pig will flyâ€â€”comparing the government subsidies to strong winds lifting

the company’s fortunes, and warning of a possible heavy landing once

those winds die down.

Looking for more in-depth coverage? Sign up to become a member and read more in-depth coverage of China’s electric-car boom in our field guide.

Posted by AGORACOM-JC

at 9:58 AM on Tuesday, May 28th, 2019

The River Valley Project is the largest

undeveloped primary Platinum Group Metal (PGM) mineral resource in

North America. The Project has excellent infrastructure and is within

100 kilometres of the Sudbury Metallurgical Complex. The Project is 100%

owned by New Age Metals.

The Project’s first economic study a

Preliminary Economic Assessment (PEA) is underway and management plans

to release the summary press release by the end of the second quarter.

The price of an ounce of Palladium

represents a 35% price increase in the last 12 months. As such, for

2019, precious metals consultancy, Metals Focus believes

that professional investors will eventually return to palladium, with

an annual average price of US$1,490 per oz. in 2019. Rhodium, which is

also present at River Valley, has seen a price increase of over 15% this

YTD at US$2,860 per oz.

For Platinum, a turnaround in investor

sentiment stimulated heavy buying of platinum Exchange Traded Funds

(ETF’s) in early 2019. Investors were motivated by supply disruption

risks and an improving outlook for auto demand.

Drill permits for our Lithium Two and

Lithium One Projects in Manitoba have been applied for and the company

is in the final approval process from the province of Manitoba.

The Company is actively seeking a strategic partner for our Genesis PGM/Polymetallic Project in Alaska

May 28th, 2019 / Rockport, Canada – New Age Metals Inc. (TSX.V: NAM; OTCQB: NMTLF; FSE: P7J.F) Harry Barr, Chairman & CEO, stated; “We are pleased to update our shareholders and interested parties as to our ongoing activities in both our PGM and Lithium divisions. Specifically, give a progress update on the River Valley Project Preliminary Economic Assessment (PEA). This update will detail our exploration and development plans for both the PGM and Lithium divisions in 2019. Furthermore, we will highlight the current PGM market and particularly Palladium and Platinum price trends.”

Update on the PEA

NAM commissioned

both P&E Mining Consultants (P&E) and DRA Americas (DRA) to

complete the River Valley Project’s first economic study, a Preliminary

Economic Assessment (PEA) in August 2018.

The company has been informed by its engineering consultants that the preliminary

PEA mine plan, production schedule and financial model is nearing

completion, and we plan to release the highlights of the study in a

press release before the end of the second quarter this year.

At this

stage, the PEA is focused on investigating the mining potential of the

project, including the latest discovery, the Pine Zone and other

footwall mineralization potential. The study will also help define areas

of the project that require additional exploration and development.

The objective of

the PEA would be to create a conceptual mine plan, mine schedule, a

capital cost estimate, and operating cost estimate incorporated into a

financial model to provide total cash flow, net present value (NPV), and

internal rate of return (IRR).

River Valley PGM Project Goals & Objectives

During 2019, the company’s exploration & development objectives are as follows:

1.Complete the re-stated resource calculation (Q1 2019);

2.Complete the Projects first economic study, PEA (Q2 2019);

3.Complete surface exploration on

additional target areas based on recommendations of the updated 43-101

and the 2017/2018 geophysics (slated for Q3-Q4 2019);

4.Arrange additional funding for continued development of the project (ongoing);

5.Conduct a 5000-metre drill program focusing in the northern portion of the Project;

6.Solicit a strategic partner to aid in

further exploration and development of the Project. Potential major

partners are waiting for the PEA results to complete additional due

diligence on River Valley.

Palladium, Platinum, Rhodium Price & Performance

There are various reasons why the Palladium

(Pd) price movement has occurred and more to suggest that Pd price may

continue to rise. First, there are continued supply deficits forecasted

for Pd and in 2019 alone Johnson Matthey (JM) expects that it could

exceed a million ounces (PGM Market Report – May 2019). Emissions

standards are increasing worldwide as is the preference for larger

vehicles, both of which require more Pd to be used in the catalytic

converters.

The PGM’s Platinum, Palladium and Rhodium

are extensively used in catalytic converters to convert harmful gasses

like hydrocarbon emissions into less harmful substances. The allowable

limits of carbon monoxide (CO) and hydrocarbon (HC) from gasoline

passenger vehicles in China will be reduced by 60% by 2025 (SFA Oxford,

2019).

The Chinese emission standard story alone

tends itself to the increase in Pd demand to grow by 500,000 ounces by

2021. To summarize, the Palladium fundamentals and forecasts align well

with the timeline for development of our River Valley Project.

The platinum market is expected to move

into deficit in 2019, with a resurgence in investor activity outweighing

modest falls in industrial and jewellery demand. Johnson Matthey also

expects a tentative recovery in autocatalyst consumption, as stricter

heavy duty emissions legislation is enforced first in China and then in

India. JM forecasts a modest increase in primary supplies, but this

could be tempered by electricity shortages and, potentially, industrial

action in South Africa, while growth in recycling may be dampened by

processing capacity constraints in some regions.

Both Platinum and Palladium are considered

precious metals, like Gold and are used as a store of value. Rhodium,

which is also present at River Valley, has seen a price increase of over

15% this year at US$2,860 per oz.

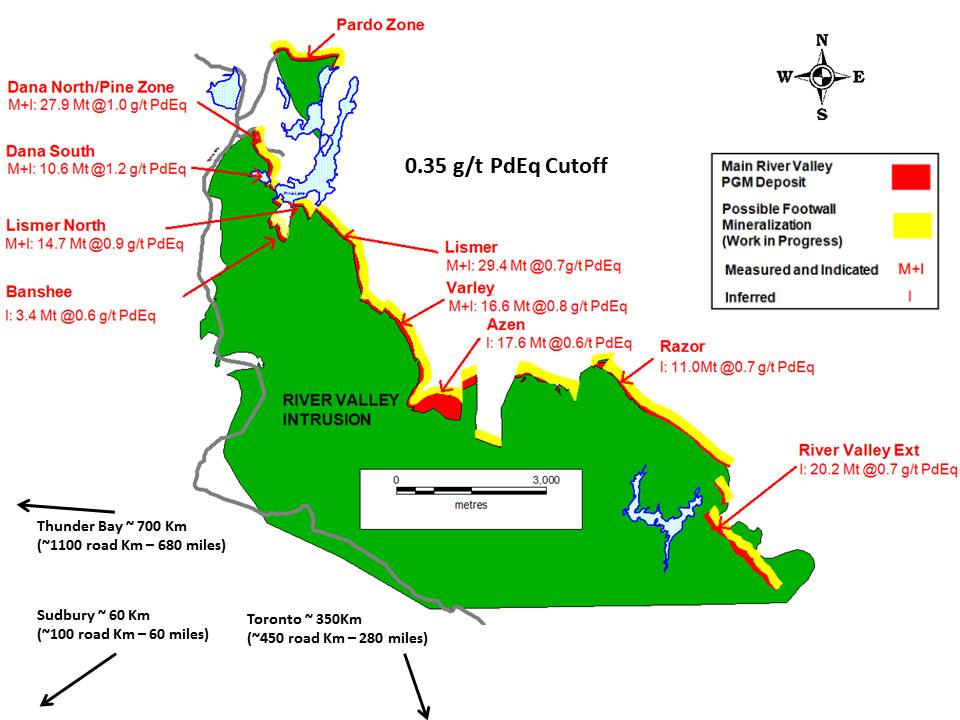

2019 Mineral Resource Update

On January 9, 2019 NAM filed its latest

Mineral Resource Estimate on the River Valley Project. The May 2018

Resource Estimate presented a global mineral inventory. The January 2019

Resource presents a pit constrained mineral resource that shows

reasonable prospects for eventual economic extraction. The results of

the updated Mineral Resource Estimate are tabulated in Table 1 below

(0.35 g/t PdEq open pit and 2.0 g.t PdEq underground cut-off). This

43-101 Technical Report is available on SEDAR. See page 4.

Table 1: Results from the January 2019 NI 43-101 Mineral Resource Estimate.

Click Image To View Full Size

Class

PGM + Au (oz)

PdEq (oz)

PtEq (oz)

Measured

1,394,000

1,701,000

1,701,000

Indicated

983,000

1,166,000

1,166,000

Meas +Ind

2,377,000

2,867,000

2,867,000

Inferred

841,000

1,059,000

1,059,000

Notes:

1.CIM definition standards were followed for the Mineral Resource Estimate.

2.The 2018 Mineral Resource models used

Ordinary Kriging grade estimation within a three-dimensional block model

with mineralized zones defined by wireframed solids.

3.A base cut-off grade of 0.35 g/t PdEq

was used for reporting Mineral Resources in a constrained pit and 2.00

g/t PdEq was used for reporting the Mineral Resources under the pit.

6.Mineral Resources that are not Mineral Reserves do not have economic viability

7. The Inferred Mineral Resource in this

estimate has a lower level of confidence than that applied to an

Indicated Mineral Resource and must not be converted to a Mineral

Reserve. It is reasonably expected that the majority of the Inferred

Mineral Resource could be upgraded to an Indicated Mineral Resource with

continued exploration.

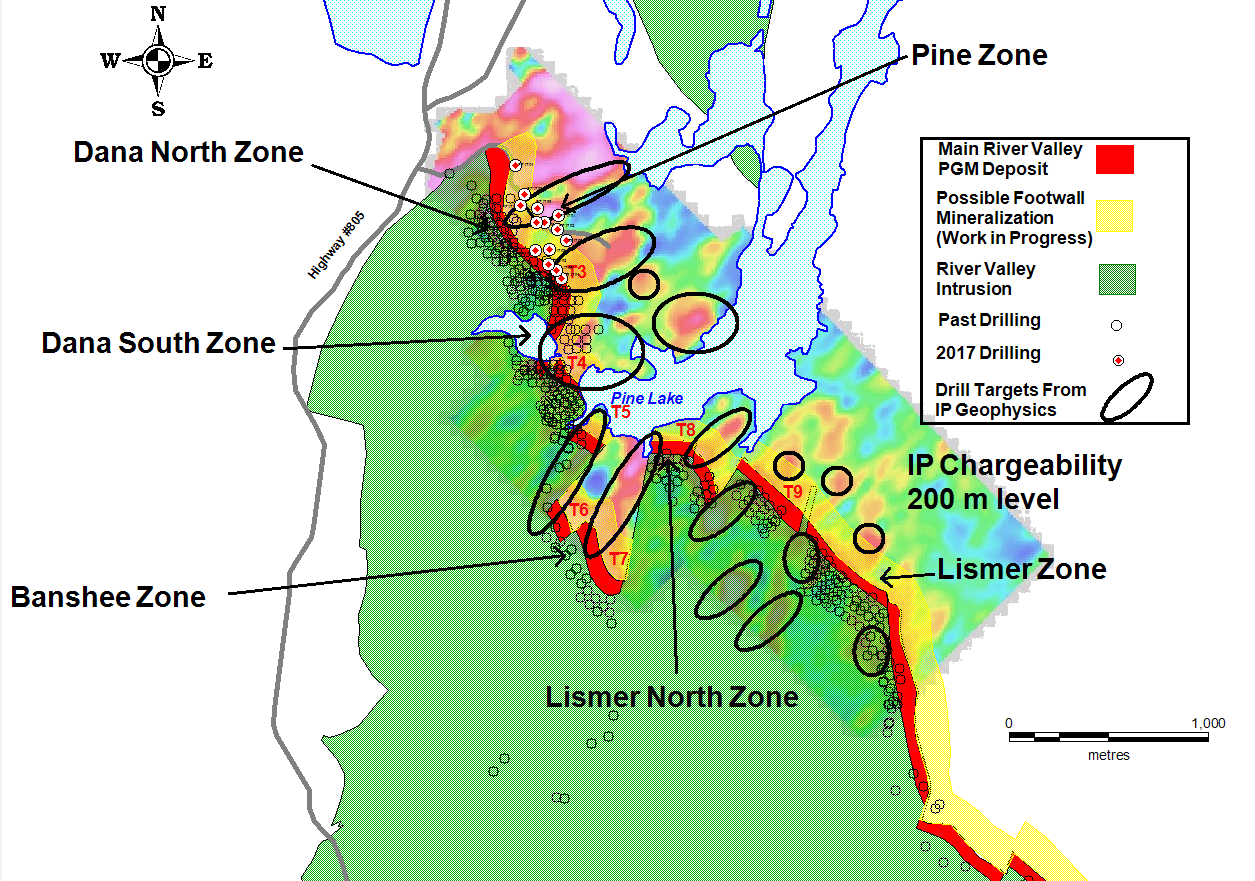

Click Image To View Full Size

Figure

1: The Yellow Band represents the footwall potential area of the River

Valley Deposit based on the results of the Pine Zone where footwall

mineralization was noted to extend 150 metres eastward from the Pine

Zone/ T3 main deposit.

At

present the only area that has confirmed footwall mineralization is in

the Pine Zone (defined from 2015 to 2017 drilling). Geophysics and

exploration continues

to test other areas of the Deposit. Management’s specific focus is to

outline a potentially economic Mineral Resource in the northern portion

of the Project that can be subsequently developed as a series of open

pits (bulk mining), crushed,and concentrate on site, with concentrate shipped to a smelter in Sudbury.

2019 Exploration Plan – River Valley PGM Project

To date an approximate 160,441 metres (481,323 feet) in 710 drill holes have

been conducted by the company as operators on the River Valley Project.

Several independent 43-101 compliant resource estimates have previously

been generated for the deposit through the exploration and development

phases. The River Valley Deposit’s

present resource, with approximately 2.9M PdEq ounces in Measured Plus

Indicated mineral resources and near-surface mineralization, covers a

total of 16 kilometers of strike. The company continues to explore and enhance the River Valley PGM Deposit.

After the ground proofing and surface

exploration program conducted in the Summer/Fall of 2018, (which

followed up on the most recent induced polarization survey by Abitibi

Geophysics) NAM management has designed a 5,000 metre drill programs to

test the new geophysical anomalies. See Figure 2 below, which shows these new geophysical anomalies and potential targets for the next stage of drilling at River Valley superimposed over the upper 4 kilometres of the project map.

Click Image To View Full Size

Figure 2:

Northern portion of the project with superimposed 2018 merged IP at

-100m level. Retrieved from River Valley Geophysical review by

Geoscience North (Alan King, P. Geo., M.Sc.)

2019 Exploration Plans for Lithium Division

The Company has eight pegmatite hosted

Lithium Projects in the Winnipeg River Pegmatite Field, located in SE

Manitoba. In 2018 NAM conducted surface exploration programs on our

Lithman East, Lithman North, Lithium One and Lithium Two projects. The

programs consisted of reviewing, characterising and sampling the known

surface pegmatites. Samples were taken from the Eagle and FD5 pegmatites

on Lithium Two and returned results of up to 3.8% Li2O. On Lithium One,

samples were taken from the known Silverleaf and Annie pegmatites and

returned significant Li20 assays of up to 4.1%.

In 2019, the Company plans to drill the Lithium Two Project first. Drill

permits have been applied for and the company is awaiting approval from

the province. The application has been accepted by the relevant parties

to date and is in the final stages of the approval process. The first

drill permit is expected to be issued in June 2019.

Genesis PGM / Polymetallic Project

On April 4th, 2018,

NAM signed an agreement with one of Alaska’s top geological consulting

companies. The company’s stated objective is to acquire additional PGM

and Rare Metal projects in Alaska. On April 18th, 2018,

NAM announced the right to purchase 100% of the Genesis

PGM/Polymetallic Project, NAM’s first Alaskan PGM acquisition related to

the April 4th

agreement. The Genesis PGM/Polymetallic Project is a road accessible,

under explored, highly prospective and multi-prospect drill ready

Palladium (Pd)- Platinum (Pt)- Nickel (Ni)- Copper (Cu) property. A

comprehensive report on previous exploration and future phases of work

was completed by Avalon Development of Fairbanks Alaska in August 2018

on Genesis. (available here).

A 2019 sampling program will be conducted to continue to outline

additional mineralization along the 800-metre by 40-metre mineralized

zone. Management is actively seeking an option/joint-venture partner for

this road accessible PGM and multiple element Project using the

Prospector Generator business model.

Opt-in List

If you have not done so already, we encourage you to sign up on our website (www.newagemetals.com) to receive our updated news.

QUALIFIED PERSON

The contents contained herein that relate

to Exploration Results or Mineral Resources is based on information

compiled, reviewed or prepared by Carey Galeschuk, a consulting

geoscientist for New Age Metals. Mr. Galeschuk is the Qualified Person

as defined by National Instrument 43-101 and has reviewed and approved

the technical content of this news release.

On behalf of the Board of Directors

“Harry Barr”

Harry G. Barr

Chairman and CEO

For further information on New Age Metals,

please contact Anthony Ghitter or Cody Hunt, Business Development at

613-659-2773, or [email protected]

Neither the TSX Venture Exchange nor its

Regulation Services Provider (as that term is defined in the policies of

the TSX Venture Exchange) accepts responsibility for the adequacy or

accuracy of this release.

Cautionary Note Regarding Forward Looking

Statements: This release contains forward-looking statements that

involve risks and uncertainties. These statements may differ materially

from actual future events or results and are based on current

expectations or beliefs. For this purpose, statements of historical fact

may be deemed to be forward-looking statements. In addition,

forward-looking statements include statements in which the Company uses

words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”,

“confident”, “intend”, “strategy”, “plan”, “will”, “estimate”,

“project”, “goal”, “target”, “prospects”, “optimistic” or similar

expressions. These statements by their nature involve risks and

uncertainties, and actual results may differ materially depending on a

variety of important factors, including, among others, the Company’s

ability and continuation of efforts to timely and completely make

available adequate current public information, additional or different

regulatory and legal requirements and restrictions that may be imposed,

and other factors as may be discussed in the documents filed by the

Company on SEDAR (www.sedar.com), including the most recent reports that

identify important risk factors that could cause actual results to

differ from those contained in the forward-looking statements. The

Company does not undertake any obligation to review or confirm analysts’

expectations or estimates or to release publicly any revisions to any

forward-looking statements to reflect events or circumstances after the

date hereof or to reflect the occurrence of unanticipated events.

Investors should not place undue reliance on forward-looking statements.

Posted by AGORACOM-JC

at 3:16 PM on Monday, May 27th, 2019

SPONSOR: New Age Metals Inc. The company’s new Lithium Division has already made significant acquisitions in Canada and the USA. The company also owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces in the Inferred. Learn More.

NAM: TSX-V

———————

The lithium industry needs a $17b injection to meet 2025 demand – here come the deals

One expert says at least US$12 billion ($17.3 billion) needs to be invested in new lithium projects by 2025 if the industry is to have any realistic hope of matching supply with demand

Corporate deals in the lithium industry are heating up at a time when

there is a predicted multi-billion-dollar cash injection needed to ramp

up supply to meet rapidly growing demand.

One expert says at least US$12 billion ($17.3 billion) needs to be

invested in new lithium projects by 2025 if the industry is to have any

realistic hope of matching supply with demand.

US lithium expert Joe Lowry told delegates at the Latin America

Downunder mining conference in Perth that the ‘Big Four’ global lithium

producers – SQM, Albemarle, Jiangxi Ganfeng Lithium and Tianqi – could

not alone meet 2025 lithium demand.

“Overall, the industry faces a lack of financing and needs to inject

more than US$12 billion within five years to have a chance of meeting

demand,†he said.

“This requirement is exacerbated further by known and emerging

failures in lithium start-ups which have demonstrated a lack of

necessary skillsets – high profile failures that have discouraged sector

investment.

“There will not be any significant lithium chemical oversupply

anytime soon. While there have been many optimistic supply forecasts,

recent results speak for themselves.â€

He dismissed the forecasts of oversupply as a myth.

“The ‘myth’ is driven by reports from ‘big bank’ analysts and

supported by statements by Chilean regulator, CORFO, after its revised

agreements allowing Albemarle and SQM to produce more material from the

Atacama brine resource,†Lowry said.

“The reality is increasing production quickly is not so easy.”

Last year there was about 270,000 tonnes of lithium demand and Lowry estimates that will rise to about 1 million tonnes in 2025.

“It’s pretty much not argued anymore that e-mobility is happening —

whether it’s EVs or scooters or ferries in Scandinavia, the transition

to e-mobility is on,†Lowry said.

“My numbers are actually some of the lower numbers out there.â€

Battery-related lithium demand in 2018 accounted for 60 per cent, up from 25 per cent five years earlier.

“So this market is becoming a battery-related market. There’s really no question about that,†Lowry said.

But new lithium supply is hard to bring online and SQM, Albemarle,

Jiangxi Ganfeng Lithium and Tianqi are likely only be able to maintain

their 68 per cent market share, according to Lowry.

“Almost every lithium project that has ever started with optimism has

taken three or four years longer to reach full capacity and that’s what

we’re seeing,†he said.

“That means there’s a lot of juniors or smaller companies around the world that need to get financed and need to get moving.â€

The cash injection gives Galaxy a roughly 11.5 per cent interest, and

a blocking stake, in Alliance, managing director Mark Calderwood told Stockhead.

Galaxy’s investment was part of a larger $32.5m placement at 20c per

share, which also included $10m from a subsidiary of Jiangxi Special

Electric Motor Co.

Jiangxi has about a 9.9 per cent stake in Alliance.

“I guess from [Galaxy’s] point of view it’s stopping us from being a

target for someone else to come and grab, and we were the cheapest

lithium miner in the market,†Calderwood said.

“Both Jiangxi and Galaxy are a lot bigger than we are, they’re both

experts in their sectors so that’s good for us and it enables us to be

cooperative in the future.

“Both parties have either a blocking stake or almost a blocking stake.â€

Australia’s downstream gaining momentum

Right now, Australia has absolutely zero per cent share of the global

lithium chemical market, but the Galaxy-Alliance deal is another step

towards building the country’s downstream industry.

“I think [Galaxy] has desires to go further downstream as well, and

Jiangxi [Ganfeng Lithium] already has that joint venture with Jiangxi

Special Electric Motors, which is downstream, but there’s other things

we can do as well,†Calderwood said.

The research partnership of 58 industry, academic and government

partners will address industry-identified gaps in the battery industries

value chain.

The goal is to expand battery minerals and chemicals production and

develop opportunities for manufacturing batteries in Australia.

Good time to invest

Lowry says rapidly rising demand and the difficulty in bringing new

lithium supply online supports his “thesis†that the market is going to

outgrow supply.

“Anyone who is interested in investing in the lithium market has a

great opportunity now because share prices are very, very depressed,†he

said.

“If you look at the market caps of some of the Australian companies,

even the ‘Big Four’ companies, their market caps are very much down from

where they were a couple of years ago.

“So if you’re interested in lithium, I would tell you now’s a good time to get in.â€

Posted by AGORACOM-JC

at 3:19 PM on Thursday, May 9th, 2019

SPONSOR: New Age Metals Inc.

The company’s new Lithium Division has already made significant

acquisitions in Canada and the USA. The company also owns one of North

America’s largest primary platinum group metals deposit in Sudbury,

Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq

Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces

in the Inferred. Learn More.

NAM: TSX-V

———————

EV ‘arms race’ revs up Murkowski’s old minerals bill

E&E News staff Energywire: Thursday, May 9, 2019

The Tesla Model S (left) and Model X charging side by side. Steve Jurvetson/Wikimedia Commons

An old proposal to jump-start American mining has been recharged by a

newfound focus on electric vehicles and the elements needed to power

them.

Congress has bandied about ideas for mining more “critical minerals”

for as long as the United States has been losing ground to other

nations, namely China, in supplying elements used in military, energy

and emerging technologies.

But a different narrative took center stage when Sen. Lisa Murkowski

(R-Alaska) introduced her latest critical minerals bill last week:

fixing the EV supply squeeze (Energywire, May 3).

The Senate Energy and Natural Resources Committee chairwoman

advocated helping the United States “compete in growth industries like

electric vehicles and energy storage,” while her co-sponsor and

committee ranking member, Sen. Joe Manchin (D-W.Va.), said he was “very

much concerned” about lithium-ion batteries.

Sources traced the new emphasis to a recent closed-door summit of automakers, mining companies and federal officials.

Murkowski teased her bill at a Washington, D.C., event organized by

Benchmark Minerals, a consulting firm specializing in battery mineral

supply chains.

Despite its small size — 26 employees — Benchmark has increasing influence on Capitol Hill.

Reached by phone yesterday, Benchmark founder Simon Moores declined

to say who attended the summit, but he said the fact that Murkowski

highlighted lithium, cobalt, graphite and nickel was “a reaction” to his

testifying to her committee twice in as many years.

“For me, the most important development is that focus on these four

[minerals]

for electric vehicles,” he said. “And that is a big step

forward in my eyes because it refines the focus and refines the

discussion.”

Robert Mintak, CEO of Canadian mining company Standard Lithium Ltd.,

also declined to go into detail about the Benchmark summit, only saying

it was “well-attended across numerous agencies.”

“The narrative is being curated to make the current state of the

nation understand that it isn’t a tree-hugging narrative,” he said.

“There’s an opportunity you need to get in front of.”

The strategy

The EV rebranding appears to be a marketing maneuver, said Jim

Constantopoulos, a geology professor at Eastern New Mexico University

and director of its Miles Mineral Museum.

“Those folks that would be more likely to drive an EV … would

normally be opposed to any sort of mining, let alone a bill that would

eliminate roadblocks to mining,” Constantopoulos said. “By referring to

it as an EV bill, they might garner some support from that sector.”

Senate Energy and Natural Resources Chairwoman Lisa Murkowski (R-Alaska). Energy and Natural Resources Committee

Environmentalists have generally condemned critical minerals

legislation as an excuse to slash environmental standards. Murkowski’s

bill would task federal agencies with streamlining mine permitting.

President Trump has ordered his administration to do the same. Under

an executive order, the U.S. Geological Survey created a list of 35

critical minerals and the Department of Commerce set to work drafting a

report of policy recommendations to mine more of each of them.

The report was due in November, but industry advocates expect the White House to publish its findings as soon as next week.

“I know we’re getting close on the strategy, but to my knowledge, the

White House is still deciding on a rollout date,” USGS spokesman Alex

Demas said.

The White House declined to speculate on any announcement.

‘Barely even in the game’

Benchmark says about 1.7 terawatt-hours’ worth of battery factory

projects are in the development pipeline — or roughly the equivalent of

24 million to 26 million EVs, depending on the battery pack.

“We are in the midst of a global battery arms race in which the U.S.

is presently a bystander,” Moores told lawmakers in February (E&E Daily, Feb. 6).

Most of the world’s lithium comes from a region in South America

crisscrossed by massive salt flats. About 1% of the world’s raw lithium

comes from the United States. North America’s only active lithium

operation is the Silver Peak mine in Nevada, although the Los Angeles Timesreported this week about a battle brewing over a second one in Death Valley.

“Despite significant domestic resources, we’re barely even in the

game,” said National Mining Association President and CEO Hal Quinn.

As for cobalt, about 68% comes from the Democratic Republic of Congo,

where a small percentage of the mineral is illegally mined using child

labor, according to a 2017 Amnesty International report.

The industry is actively looking to cut back on cobalt, but even if

they are successful, new battery production will still increase demand.

“There’s no way that entire battery industry can just abandon cobalt

as a critical element for their cathode,” Benchmark consultant and

former Tesla employee Vivas Kumar said at another recent event in New

York.

Where do companies stand?

Automakers have generally supported previous critical minerals bills, and this year is no different.

The Alliance of Automobile Manufacturers, a powerful trade group that

represents Ford Motor Co. and General Motors Co., has not changed its

stance since testifying in support of the bill in 2014.

“Whether it’s the aluminum in automotive frames, the platinum in

catalytic converters, or the lithium and nickel in electric vehicle

batteries, minerals are vital components in every automobile on the road

today, and future models,” spokesman Wade Newton said in an email.

But Tesla declined to comment, as did Fiat Chrysler Automobiles. A Ford spokeswoman redirected inquiries to the Auto Alliance.

The Electric Drive Transportation Association, which advocates for

electric vehicle makers and other companies in the electric and hybrid

vehicle industry, said it had yet to thoroughly examine Murkowski’s

legislation.

“We appreciate the bipartisan effort to reinforce the supply chain

for electric vehicles and are currently reviewing the bill,” spokesman

Jake Styacich said.

While the talking point has changed, China remains the foremost national security concern.

In 2015, the Chinese government published a plan for its

manufacturing sector, Made in China 2025, which identified battery

minerals as a key area in which to seek dominance.

Robbie Diamond, president of Securing America’s Future Energy, a

group fighting foreign oil dependence, called it a “wake-up call.”

“We do not want to go from dependence on oil and troubles in the Middle East to dependence on China for batteries,” he said.

Diamond cited Moores’ February testimony as evidence.

He added: “Anybody who takes our security seriously has to ask themselves the question: Can we fall this far behind?”

Reporters Dylan Brown, Kelsey Brugger, Timothy Cama, David Iaconangelo and Maxine Joselow contributed.

Posted by AGORACOM-JC

at 12:16 PM on Thursday, April 18th, 2019

SPONSOR: New Age Metals Inc. The company owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Updated NI 43-101 Mineral Resource Estimate 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces in the Inferred. Learn More.

NAM: TSX-V

———————

Supply And Demand Outlook Favors Palladium Vs. Platinum

Palladium has outperformed platinum ever since the fundamentals of

supply and demand have changed due to the diesel emissions scandal.

The gap between platinum and palladium has shrunk in recent weeks,

which would break the current trend of palladium outperforming platinum

if it continues.

Both the fundamental and technical pictures point to the trend

staying in place relative to platinum and palladium despite the recent

hiccup.

The biggest source of demand for platinum (PPLT) and palladium (PALL)

is the automotive industry where emission standards are becoming

increasingly stringent. These standards are driving demand for platinum

and palladium due to their ability to help reduce harmful emissions. The

result has been a sort of competition between the two of them.

However, the competition has become somewhat one-sided ever since the

platinum market was rocked in 2015 by the emissions scandal or “Diesel

Gate†involving Volkswagen (OTCPK:VWAGY).

The reason is because platinum is heavily used in vehicles with diesel

engines. On the other hand, palladium is associated with gasoline

engines.

Cars powered by diesel engines have since fallen out of favor, and

people are now turning towards cars powered by gasoline engines. This

trend does not look to change anytime soon, but it’s set to continue for

the foreseeable future. This is bullish for palladium and bearish for

platinum. The result can be seen in the supply and demand equation for

palladium and platinum.

The market for palladium has a deficit with a surplus for platinum

The emissions scandal has fundamentally altered the landscape for

vehicles powered by diesel and gasoline engines and, by extension,

platinum and palladium. The former is seeing demand decrease, and the

latter is seeing demand increase as there is a shift away from

diesel-powered cars towards gasoline-powered cars.

The two tables reveal that the platinum market has a surplus, with

supply exceeding net demand. Except for industrial demand, every other

segment, including autocatalyst, jewelry, and investment, is in decline.

While supplies from mining have stayed roughly the same, platinum

recycling is adding to the surplus of platinum in the market. The trend

is clearly bearish for platinum.

Platinum supply and demand (Unit: 1000 oz)

Supply

2016

2017

2018

South Africa

4392

4449

4471

Russia

717

703

657

Others

988

953

980

Total supply

6097

6105

6108

Demand

Autocatalyst

3342

3218

3052

Jewelry

2412

2400

2363

Industrial

1806

2022

2321

Investment

620

361

89

Total demand

8180

8001

7825

Recycling

-1934

-2072

-2215

Net demand

6246

5929

5610

Surplus/deficit

-149

176

498

Source: Johnson Matthey

The opposite is true for palladium. Supply of palladium falls short

of net demand and is driven primarily by the increased demand in the

autocatalyst segment. Recycling has made more palladium available, but

supplies have yet to eliminate the deficit in the market for palladium.

Overall, the trend for palladium looks to be a lot better compared to

platinum.

Palladium supply and demand (Unit: 1000 oz)

Supply

2016

2017

2018

South Africa

2570

2550

2590

Russia

2773

2406

2840

Others

1417

1405

1450

Total supply

6760

6361

6880

Demand

Autocatalyst

7951

8428

8655

Jewelry

191

173

166

Industrial

1875

1832

1855

Investment

-646

-386

-555

Total demand

9371

10047

10121

Recycling

-2491

-2899

-3212

Net demand

6880

7148

6909

Surplus/deficit

-120

-787

-29

The forecast for 2019 calls for more of the same, assuming there are

no unforeseen events that could disrupt the supply and demand equation.

Platinum will have a surplus, and palladium, a deficit. The trend

established in recent years as shown in the two tables is not expected

to change. That is bullish for palladium, but bearish for platinum.

Divergence in prices for platinum and palladium

As a result of a favorable outlook, palladium prices have vastly

outperformed platinum. While platinum used to command a much higher

price than palladium, the roles have now been reversed, and palladium is

now worth more. The chart below tracks the relationship between

platinum and palladium prices.

Notice that at its peak in March, a troy ounce of palladium was worth

almost two ounces of platinum. That ratio has now come down, and

palladium is now worth 1.5 ounces of platinum. A significant change, but

still far removed from the days when platinum was more expensive than

palladium.

However, the fact remains that the gap between platinum and palladium

has shrunk with platinum outperforming palladium during this time

frame. The gap could continue to shrink, but it could also begin to

widen as before. Which of the two is more likely to happen will depend

on a few factors that should be taken into consideration.

Can platinum and palladium be substituted for one another in the manufacture of an autocatalyst?

The short answer is yes, but only to a certain extent. While platinum

and palladium are more suitable and preferred in diesel and gasoline

vehicles, respectively, it is not absolutely necessary. The more

expensive palladium becomes relative to platinum, the more manufacturers

may be inclined to look into replacing palladium with platinum in the

manufacture of an autocatalyst. Not necessarily completely, but at least

partially.

In theory, this should act as a cap on palladium relative to

platinum. If the gap in prices between the two becomes too extreme,

precious metal substitution could force the ratio between palladium and

platinum to reverse and narrow. There would be less demand for palladium

and demand for platinum would increase under these conditions. However,

in practice, it is difficult to replace more expensive palladium with

cheaper platinum.

The two precious metals are only needed in trace amounts, and the

price difference would have to be very severe to make a noticeable

difference in the final cost of a vehicle. It also takes a lot of time

and expense to test that changes in precious metal composition in an

autocatalyst meet desired specifications. In a nutshell, while it’s

possible, it’s almost certainly not worth the trouble to replace

platinum with palladium or vice versa.

Why gold prices affect platinum more than palladium

Unlike palladium, platinum prices are more prone to being influenced by the price of gold (GLD).

The reason is because platinum is heavily used in jewelry, much more

than palladium. Because of this, platinum is in direct competition with

gold. In fact, people often have to decide which of the two, gold or

platinum, they will select in a purchase.

People will more often than not pick gold, but they may be tempted to

go for platinum if the former is much more expensive than the latter.

Rising gold prices are, therefore, good for platinum because it makes

platinum a more attractive substitute. But if gold prices fall, then

there is less need for platinum because most people tend to prefer gold.

It’s, therefore, necessary that we look at gold when considering

where platinum will go relative to palladium. The ratio between gold and

platinum prices has changed recently as gold prices have gone down. A

previous article discussing why gold is likely to face pressure can be

found here.

The chart above tracks the relationship between platinum and gold

prices. Notice that while an ounce of platinum was roughly equal to 60%

of gold at its low, the ratio has gone up and is now at almost 70%. What

this basically means is that platinum’s appeal as an alternative has

declined versus gold. This should be seen as a negative for platinum

demand, which could put downward pressure on the price of platinum.

Palladium looks to be priming itself for a big move

Palladium prices have been going sideways after a big drop from their

recent highs. In fact, the chart pattern for palladium resembles that

of a symmetrical triangle or a coil. If this technical analysis is

correct, then a big move may be coming once consolidation is done. The

triangle could resolve to the downside, but it’s more likely to continue

the long-term trend, which is up.

Both the fundamental and technical pictures suggest that a move to

the upside is the most probable outcome. In contrast, platinum is being

held back by a number of issues as a previous article explains here. This would reverse the narrowing of the spread between platinum and palladium and, instead, widen the gap that exists.

The ratio between palladium and platinum has been stuck at around

1.5, as previous charts reveal. This ratio could decrease further, but

the most likely path is for the ratio to resume its previous uptrend

after the time it has spent consolidating. This would be consistent with

the price of palladium outperforming that of platinum.

Palladium will outperform platinum

It’s important to mention that the long-term picture for platinum and

palladium in terms of demand is not a good one. Recent research

suggests that it will one day be possible to make an autocatalyst

without the need for any precious metals such as platinum and palladium.

If this happens, then both metals will be left without their biggest

source of demand.

Furthermore, electrical vehicles are on the rise, and they do not

emit the harmful emissions that platinum and palladium are tasked with

reducing. The challenge for platinum and palladium will be to find new