Posted by AGORACOM

at 3:03 PM on Thursday, June 25th, 2020

Vancouver, British Columbia–(Newsfile Corp. – June 25, 2020) – Affinity Metals Corp. (TSXV: AFF) (“the Corporation”) (“Affinity”) is pleased to report that it has acquired, through staking, five new mineral properties. Four of the properties are located near Timmins, Ontario, Canada and the fifth is located near Revelstoke, British Columbia, Canada. The Corporation is currently acquiring more detailed information and history on the properties and provided they continue to be seen as properties of merit will provide further background in a news release and on the Corporation’s website at www.affinity-metals.com.

About Affinity Metals

Affinity is focused on the acquisition, exploration and development of strategic metal deposits within North America. Affinity is following a Project Generator model.

In addition to these recent acquisitions, Affinity is advancing the Regal and West Timmins Gold Projects.

The Regal is located near Revelstoke, British Columbia, Canada in the northern end of the prolific Kootenay Arch and hosts two major geophysical anomalies as well as three past producing mines. Recent drill results included a new silver discovery with an 11.10 meter interval of 143.29 g/t silver which included a 0.55 meter interval of 2,612.0 g/t silver.

The West Timmins Gold property is located near Timmins, Ontario, Canada and adjoins Melkior’s Carscallen project. The first drill hole has been completed and the core is now being logged, split and sampled in preparation for assaying.

On behalf of the Board of Directors

Robert Edwards, CEO and Director of Affinity Metals Corp.

Posted by AGORACOM

at 4:03 PM on Wednesday, June 24th, 2020

SPONSOR: Lomiko Metals is focused on the exploration and development of minerals for the new green economy such as lithium and graphite. Lomiko has an option for 100% of the high-grade La Loutre graphite Property, Lac Des Iles Graphite Property and the 100% owned Quatre Milles Graphite Property. Lomiko is uniquely poised to supply the growing EV battery market. Click Here For More Information

The electric vehicle revolution has turned out to be more of an evolution, with the industry making slow and steady progress.

Despite this progress, the electric vehicle industry is still yet to turn a profit as a whole.

The next major step for the industry is to focus on efficiency and profitability, the two factors that will most impact the EV market share.

Many believe electric vehicles are the only future of road transportation. Equally, many are confident they will never replace internal combustion engines—not entirely, anyway. The so-called EV revolution, with sales of electric cars going through the roof and overtaking the sales of ICE cars, has failed to materialize. What the EV industry has instead been going through has been more stable and reliable: an evolution.

During this evolution, cutting battery costs and extending the range have been the two focal points of the EV industry. Now that there are some reliable results in these two respects, it is time to move to the next level: making EVs profitable.

It might come as a surprise that not all EVs are profitable, given that most EV-related headlines in the mainstream media are dedicated to Tesla, and Tesla continues to surprise the market with robust profits. But industry-wide, EVs have yet to turn in a profit, a new report from Lux Research says.

According to the report, the electric vehicle industry has made significant progress on battery costs and range extension, which has helped boost sales. Now, Lux Research analysts say, it is time to focus on efficiency to drive profitability, which would eventually make EVs more popular than ICE engine cars. This, the analysts say, should happen around 2035 or 2040, when plug-in hybrids and battery electric vehicles are expected to account for over half of all car sales.

“Currently, BEVs are more expensive and less convenient to use than their non-electric counterparts, but technology will continue to close this gap,” the lead author of the report, Christopher Robinson said. “We expect to see efficiency front and center as the next major focus of BEV design, with automakers either downsizing packs to increase profitability or offering more range.”

Naturally, the conclusions from the study are not based on research of every single EV that is on the global market. They are based on a representative sample of models, but, Robinson notes, there is a substantial difference between models in terms of profitability.

“Profitability in making electric vehicles ranges significantly between manufacturers. Tesla is likely the most profitable electric vehicle manufacturer with average gross margins around 20% on its vehicles,” the study’s lead author said. “However, that’s not the case for most as GM reported it still loses money on each Chevy Bolt it sells and has been hesitant to ramp up production. As incumbent manufacturers increase production capacity, we do expect profitability to improve through increased volumes of shared parts between models and advancements in batteries, motors, and other electronics in the powertrain.”

And then there are subsidies. Scorned by libertarians as a taxpayer-burdening crutch for industries that should be able to stand on their own two feet, subsidies for electric vehicles will remain in place for the observable future, at least in Europe and China, two of the world’s largest EV markets.

China recently said it would extend EV subsidies for two years, although it had planned to scrap them this year. It will gradually reduce them by 10 percent this year, 20 percent next year, and 30 percent in 2022, but it will keep them in place to stimulate more EV sales. Beijing has a target of 25 percent of all car sales to be EVs.

Meanwhile, Germany and France are even raising their EV subsidies to drive more purchases. These purchases are a big part of their green recovery plan, and in France, they are a big part of the revival of the local car industry, which has already invested heavily in electric vehicle manufacturing capabilities.

Sales of EVs this year will be affected by the pandemic, as will all car sales. BloombergNEF projects an 18-percent decline in EV sales this year but notes long-term demand remains strong.

Still, two more obstacles remain on the road to making EVs the dominant form of road transportation, and Lux Research analysts accurately call them range anxiety and charge time trauma. The reference to mental issues is not accidental. Besides their price, an inherent mistrust of EVs is a big reason why they are not a more common sight on roads and streets around the world.

Resolving these issues will take time, and they cannot be rushed, unless carmakers start handing out free EVs. After all, EVs are not an improvement on the ICE technology the way digital cameras were an improvement on analog ones. EVs are an alternative technology whose main advantage is that it does not emit noxious gases.

There are certainly many people concerned about the environment enough to be willing to spend more on a cleaner vehicle. Yet those who would rather keep their old truck, noxious gases and all, than buy an electric version and worry about charging times and ranges all the time are many more. These are the people whom the EV industry needs to convince that their product is reliable and won’t leave them stranded at a charging station in the middle of nowhere for hours.

Posted by AGORACOM

at 2:08 PM on Wednesday, June 24th, 2020

SPONSOR: Mota Ventures Corp is an established natural health products company focused in the CBD and psychedelic medicine sectors. Through their powerful eCommerce business, Mota is a leading direct-to-consumer provider of a wide range of natural health products throughout the United States and Europe. Click Here for More Info

The remedial potential of psilocybin has helped open the doors to a new world of potential treatments and psychedelic therapies.

Psilocybin and a number of similar psychoactive compounds have begun to show potential as medical therapies.

Psychedelic therapies including psilocybin, MDMA and other psychoactive compounds are slowly beginning to show medical potential as therapies designed to treat mental health concerns. Following the developmental model that saw cannabis rise from an illicit narcotic to a recognized form of medicine in a growing number of jurisdictions around the world, these psychedelic therapies may have the potential to provide significant medical benefits, especially for those suffering from mental health conditions such as post-traumatic stress disorder (PTSD), addiction issues or other ailments.

Psychedelic treatments, including psilocybin, gaining medical acceptance

In North America, a number of leading medical and academic institutions have already begun to explore the potential of psychedelic therapies. For example, in 2017 the US Food and Drug Administration (FDA) granted its “Breakthrough Therapy Designation†to MDMA for the treatment of PTSD. In 2019, 15 sites enrolled subjects in an FDA-regulated Phase 3 clinical trial of MDMA-assisted psychotherapy for PTSD.

According to MAPS, the FDA’s Breakthrough Therapy Designation is intended for drugs that may have the potential to treat a serious or life-threatening disease or condition and preliminary clinical evidence indicates the drugs could demonstrate substantial improvement over existing therapies. Like the US FDA, Health Canada has embraced the medical potential of psychedelic therapies. The Canadian regulatory authority has provided psychedelic therapy company Numinus (TSXV:NUMI) with an updated licence under the Controlled Drug and Substances Act to allow Numinus researchers to standardize the extraction of psilocybin from mushrooms.

Under the company’s existing licence, Numinus is authorized to test, possess, buy and sell MDMA, psilocybin, psilocin, DMT and mescaline. Moving forward, the company intends to pursue the potential benefits of psychedelic therapies through the research, development and distribution of these substances. “We are excited about the future of psychedelics, and our focus will solely be on its therapeutic use,†said Numinus CEO Payton Nyquvest. “Psychedelics will only move forward in a therapeutic and research context, where the application of these substances will only happen in safe, controlled treatment environments. Numinus has these pieces in place today.â€

The initial progress made in the world of psychedelic therapies has begun to reflect many of the early steps made by the cannabis industry on the path to acceptance. Across North America, the regulation of cannabis for strictly medical uses has often predated legal recreational use.

Recognizing the parallels in these emerging industries, a number of companies in the psychedelic therapy space are working with experts from the cannabis industry in order to educate the public and develop safe and consistent treatment options. There are many similarities between the medical cannabis market and the emerging medical psychedelic market; however, the nature of psychedelics involves a much more stringent set of regulations in order to ensure patients receive a treatment tailored to their unique condition. By working with regulators like Health Canada, companies such as Numinus have an opportunity to support the emerging field of psychedelic-assisted therapy and research by establishing safe and standardized dosages and delivery methods.

Future psychedelic therapy research

The challenging nature of mental health conditions such as PTSD, addiction, depression, anxiety and many others has caused neuroscientists to consider new therapies as well. In 2019 John Hopkins Medicine announced the launch of the Center for Psychedelic and Consciousness Research, a research facility focused on the study of compounds including LSD and psilocybin as a means of treating a variety of mental health concerns including anorexia, addiction and depression.

With US$17 million in funding, the center is working to move the field of psychedelic therapies forward while targeting a number of specific conditions. “It’s been hand-to-mouth in this field, and now we have the core funding and infrastructure to really advance psychedelic science in a way that hasn’t been done before,†said Roland Griffiths, the director of the center at Johns Hopkins. “The one that’s crying out to be done is for opiate-use disorder, and we also plan to look at that.â€

Takeaway

Leading health authorities in both Canada and the United States have recognized the potential medical benefits of a number of psychedelic compounds. Through medical licensing agreements and research partnerships, both public and private institutions are slowly beginning to pinpoint the medical conditions that could most benefit from psychedelic therapies. As this research continues to improve our medical understanding of psychedelics, there is potential for new therapies to emerge with direct applications for a number of mental health concerns.

Posted by AGORACOM

at 7:11 AM on Wednesday, June 24th, 2020

TORONTO, June 24, 2020 (GLOBE NEWSWIRE) — Loncor Resources Inc. (“Loncor” or the “Company“) (TSX: “LN”; OTCQB: “LONCF”) announces that its 76.29%-owned subsidiary, Adumbi Mining SARL (“Adumbi Miningâ€), has entered into a joint venture agreement (the “New Barrick JV“) with Barrick Gold (DRC) Limited for two exploitation permits held by Adumbi Mining (the “JV Permitsâ€) covering ground contiguous to the Company’s Imva area within the Ngayu gold belt in the northeast of the Democratic Republic of the Congo (“DRCâ€). The purpose of the New Barrick JV is to conduct exploration on the JV Permit properties to evaluate possible development and mining of such properties.

The Ngayu gold belt lies approximately 220 kilometres from the Kibali gold mine, operated by Barrick (TSX: “ABXâ€; NYSE: “GOLDâ€). Kibali produced record gold production of 814,000 ounces of gold in 2019, at “all-in sustaining costs†of US$693/oz.

The terms of the New Barrick JV are similar to Loncor’s ongoing joint venture agreement with Barrick which covers over 1,894 km2 of ground in the Ngayu gold belt including, among other properties, certain properties in the Imva area. Under the New Barrick JV, Barrick will manage and fund all exploration of the JV Permit properties until the completion of a pre-feasibility study. Once the joint venture committee has determined to move ahead with a full feasibility study, a special purpose vehicle (“SPV“) would be created to hold the specific discovery areas. Subject to the DRC’s free carried interest requirements, Barrick would retain 65% of the SPV with Adumbi Mining holding the balance of 35%. Adumbi Mining would be required, from that point forward, to fund its pro-rata share of the SPV in order to maintain its 35% interest or be diluted.

The closing of the New Barrick JV, which is expected to occur by July 18, 2020, is subject to certain closing conditions customary for transactions of this nature.

Arnold Kondrat, CEO of Loncor, stated: “We are pleased to see Barrick’s confidence in the Ngayu gold belt continue to grow. This New Barrick JV further consolidates the control of the Ngayu gold belt by Loncor and Barrick as partners.â€

About Loncor Resources Inc. Loncor is a Canadian gold exploration company focussed on the Ngayu Greenstone Belt in the North East of the Democratic Republic of the Congo (the “DRCâ€). The Loncor team has over two decades of experience of operating in the DRC. Ngayu has numerous positive indicators based on the geology, artisanal activity, encouraging drill results and an existing gold resource base. The area is 220 kilometres southwest of the Kibali gold mine, which is operated by Barrick Gold (Congo) SARL (“Barrickâ€). In 2019, Kibali produced record gold production of 814,000 ounces at “all-in sustaining costs†of US$693/oz. Barrick has highlighted the Ngayu Greenstone Belt as an area of particular exploration interest and is moving towards earning 65% of any discovery in 1,894 km2 of Loncor ground that they are exploring. As per the joint venture agreement signed in January 2016, Barrick manages and funds exploration on the said ground at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. In a recent announcement Barrick highlighted six prospective drill targets and are moving towards confirmation drilling in 2020. Subject to the DRC’s free carried interest requirements, Barrick would earn 65% of any discovery with Loncor holding the balance of 35%. Loncor will be required, from that point forward, to fund its pro-rata share in respect of the discovery in order to maintain its 35% interest or be diluted.

In addition to the Barrick JV, certain parcels of land within the Ngayu project surrounding and including the Makapela and Adumbi deposits have been retained by Loncor and do not form part of the joint venture with Barrick. Barrick has certain pre-emptive rights over the Makapela deposit. Loncor’s Makapela deposit (which is 100%-owned by Loncor) has an indicated mineral resource of 614,200 ounces of gold (2.20 million tonnes grading 8.66 g/t Au) and an inferred mineral resource of 549,600 ounces of gold (3.22 million tonnes grading 5.30 g/t Au). Adumbi and two neighbouring deposits hold an inferred mineral resource of 2.5 million ounces of gold (30.65 million tonnes grading 2.54 g/t Au), with 76.29% of this resource being attributable to Loncor via its 76.29% interest in the project.

Resolute Mining Limited (ASX/LSE: “RSG”) owns 26% of the outstanding shares of Loncor and holds a pre-emptive right to maintain its pro rata equity ownership interest in Loncor following the completion by Loncor of any proposed equity offering.

Additional information with respect to Loncor and its projects can be found on Loncor’s website at www.loncor.com.

Posted in All Recent Posts, Loncor | Comments Off on Loncor $LN.ca Expands JV Relationship with Barrick in DRC $ABX.ca $NEM $RSG

Posted by AGORACOM

at 1:06 PM on Monday, June 22nd, 2020

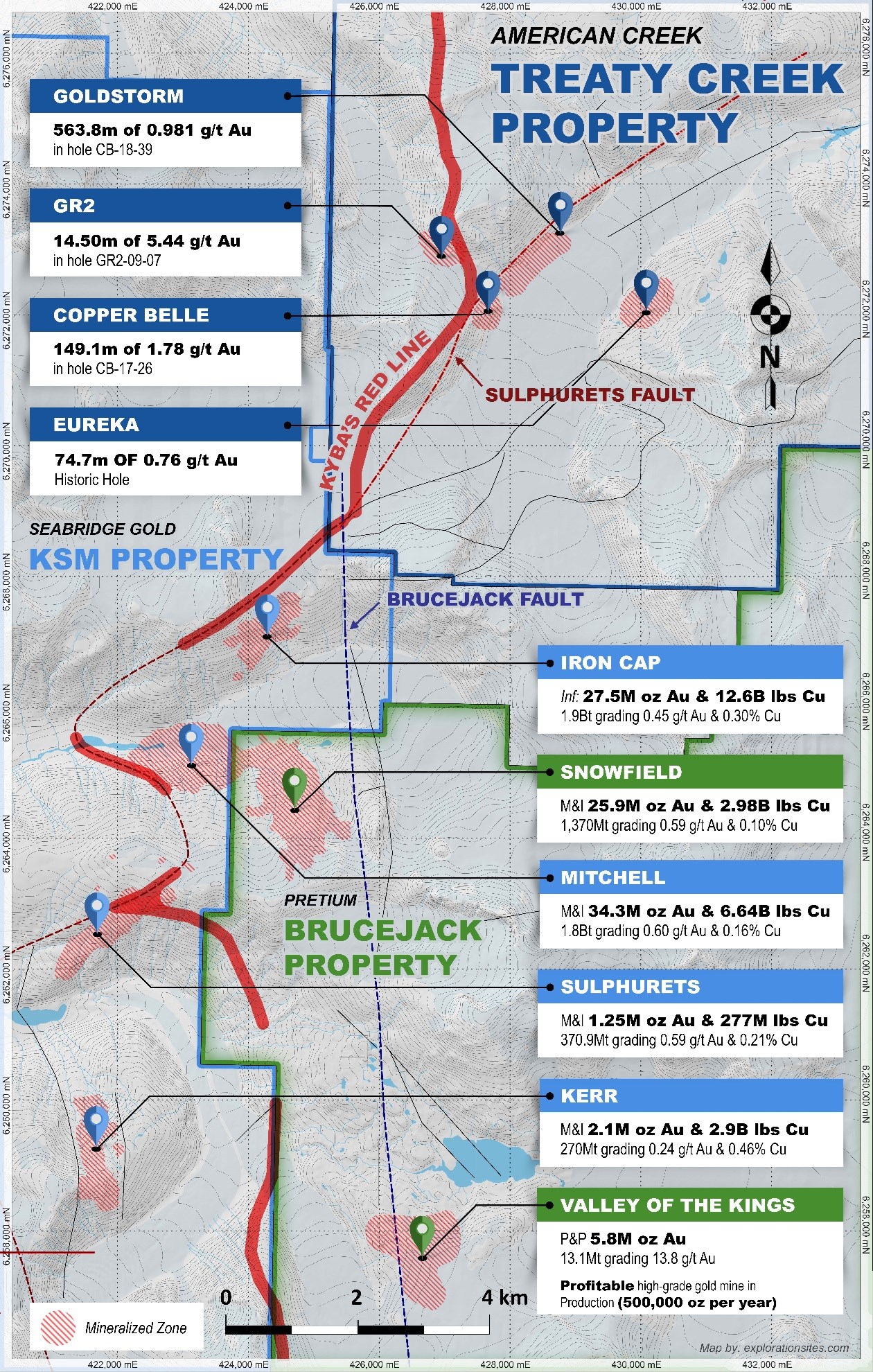

Cardston, Alberta–(Newsfile Corp. – June 22, 2020) – American Creek Resources Ltd. (TSXV: AMK) (“the Corporation”) is pleased to report that its JV partner Tudor Gold Corp has added a third diamond drill rig to the 2020 program as they intensify their exploration efforts at our JV flagship property Treaty Creek, located in the Golden Triangle of Northwestern British Columbia. Diamond drilling started on the Goldstorm Zone with two drill rigs in May.

Tudor Gold Corp’s V.P. Project Development, Ken Konkin, P.Geo. states: “The drilling has gone very well to-date given the early start in May. Both drill rigs are working extremely well as we outline the peripheral edges of the Goldstorm mineralization. We recognize that in order to achieve the goals of having our preliminary drill measured and drill indicated resource estimate completed for year-end, we need to accelerate our drilling production. The Goldstorm system is proving to be very large, as we have currently delineated 850m along the northeastern axis and 600 meters along the southeastern axis and just over 1080 meters at it’s deepest point. Depending on the depths and widths of mineralization encountered, we may require more than three drills to complete this task. Furthermore, we will be drill testing the Perfect Structural Storm (PS2), a new geophysical and geological target located mid-way between our Goldstorm system and Seabridge’s Iron Cap deposit. The first holes at PS2 will be located within a cluster of surface samples that have returned anomalous gold values.”

The 2020 budget allows for 22,500 meters of drilling on the Goldstorm Zone. The gold-copper-silver mineralization remains open to the northeast and to the southeast, as well as to depth. The goal of the 2020 drilling program is to clearly define the limits of the mineralization to facilitate the resource calculations.

Walter Storm, President and CEO stated: “Our entire team has done an excellent job initiating an early start to our drill program in very difficult winter conditions. I am very pleased with the progress made to date. In an effort to extend our drilling season, we have submitted a permit application to the Ministry of Mines to construct a new drill camp that is much lower in elevation than our current camp. This new camp will be beneficial in extending the drill season into the fall months as crews will be able to access the drills without helicopter support, making it a much safer, cost effective and productive drilling season. We continue to work safely and productively, observing the protocols set out in our COVID-19 safety procedures.”

Treaty Creek JV Partnership

The Treaty Creek Project is a Joint Venture with Tudor Gold owning 3/5th and acting as operator. American Creek and Teuton Resources each have a 1/5th interest in the project creating a 3:1 ownership relationship between Tudor Gold and American Creek. American Creek and Teuton are both fully carried until such time as a Production Notice is issued, at which time they are required to contribute their respective 20% share of development costs. Until such time, Tudor is required to fund all exploration and development costs while both American Creek and Teuton have “free rides”.

Treaty Creek Background

The Treaty Creek Project lies in the same hydrothermal system as Pretium’s Brucejack mine and Seabridge’s KSM deposits with far better logistics.

American Creek is a Canadian junior mineral exploration company with a strong portfolio of gold and silver properties in British Columbia. Two of those properties are located in the prolific “Golden Triangle”; the Treaty Creek and the 100% owned past producing Dunwell Mine.

The Corporation also holds the Gold Hill, Austruck-Bonanza, Ample Goldmax, Silver Side, and Glitter King properties located in other prospective areas of the province.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email:[email protected]. Information relating to the Corporation is available on its website at www.americancreek.com

Posted in All Recent Posts | Comments Off on American Creek $AMK.ca Reports 3rd Drill Added on Its JV Treaty Creek Property in the Golden Triangle $TUD.ca $SSI.ca $AOT.ca

Posted by AGORACOM

at 10:00 AM on Monday, June 22nd, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Recently acquired 14km of the potential extension of the new discovery by New Found Gold’s Queensway project to the south.Click Here for More Info

Dear Investors:

The US stock market should not be trading anywhere close to the multiples it is today given the enormity of the macro events that have already unfolded this year:

US and Iran being on the brink of war in January with still unresolved problems.

The virus pandemic that now has an incredibly high probability of a 2nd wave unfolding.

The steepest economic downturn in US history.

Front-month crude oil prices turning negative in April.

20 million of unemployed Americans enjoying a temporary boon of Federal unemployment benefits under the CARES Act, a program that expires at the end of July.

The savings rate shot up to 33% in April, the highest monthly level ever. A new trend in consumer savings versus spending will be a major drag on the overly anticipated recovery.

Government debt outstanding has increased by $2.5 trillion so far this year with the deficit doubling from 5 to 10% while corporate debt issuance is surging. Treasury debt alone has consumed all the money printing by the Fed.

The days for a US-China trade deal are long gone. Since the virus outbreak, relations have deteriorated yet again. The world’s two largest economies are firmly entrenched not just in a trade war but a new cold war.

Riots and protests have been breaking out nationwide in the US with race discrimination and wealth inequality at the core.

The latest Fed liquidity injections have divided the rich and poor to the highest levels since the Great Depression creating class warfare and heightened political conflict.

Conflicts between Beijing and Hong Kong, and even Taiwan, are heating up again with wealth inequality in China and Hong Kong even greater than the US.

Similar to China, Hong Kong suffers from a credit bubble of its own. Poor living standards for the bulk of Hong Kong’s younger population fuels its willingness to protest against the recent interventions by the China Communist Party. Hong Kong’s role as a global banking and trade hub is severely threatened by CCP interventions.

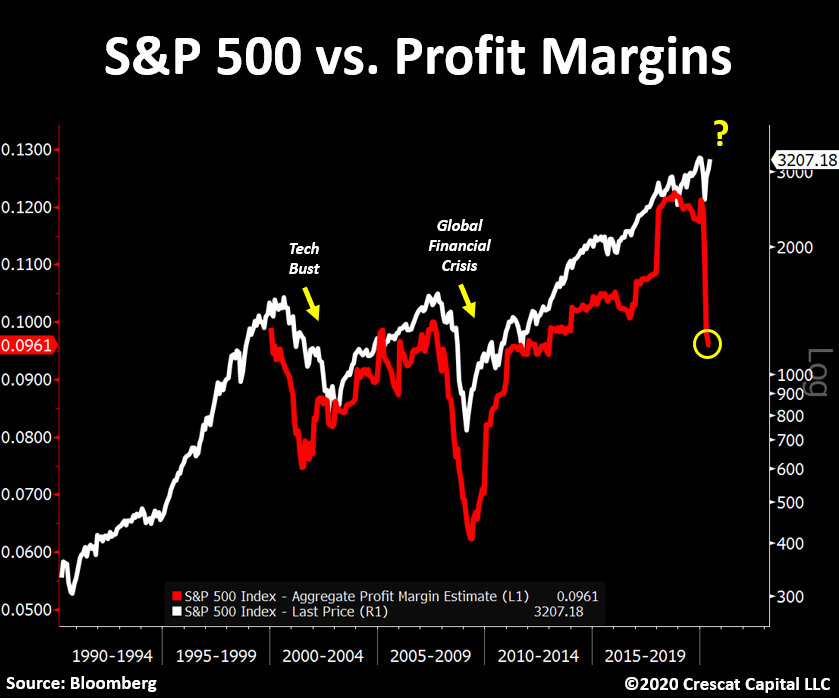

The chart below is a great illustration of how insanely disconnected equity prices are from their underlying fundamentals. S&P 500 profit margin estimates are plunging! “Buy the dip†investors are not paying attention and have simply been too eager to call the bottom.

At Crescat, we are focused on three major macro investing themes in our portfolios today:

Record Overvalued US Stock Market

The US stock market is absurdly overvalued. In our analysis, the gap between current prices and discounted present value of likely future cash flows is the highest ever. Speculation is rampant and being championed by a bold new breed of Millennial day-traders. The mania is based on a widespread hope in Fed money printing. The catalysts for reckoning are numerous as a major cyclical economic downturn has only just begun. With too many afraid to tread there, the potential reward-to-risk tradeoff from shorting stocks is worthy of a significant allocation today. It is perhaps one of the best macro set-ups in US history to rotate out of overvalued stocks and into undervalued precious metals.

New Precious Metals Bull Market

Crescat is working in concert with renowned exploration geologist, Quinton Hennigh, PhD on an exciting new activist investing campaign in the precious metals exploration industry which you can read about below. We are confident that a critical mass of investors will soon realize there is an alternative to buying over-valued US stocks with abysmal growth and profitability outlooks. Those who care about fundamentals can buy historically inexpensive precious metals instead with outstanding macro supply and demand drivers, especially for gold and silver mining companies. We believe we are in the early innings of a major new bull market for precious metals as a non-correlated macro asset class. There is good reason why gold and silver have served as hard money around the world for thousands of years. It is the same reason gold remains the most ubiquitous global central bank reserve asset on the planet. We expect the world’s sovereign treasury departments acting in their national interests to provide strong demand for gold in the current global economic downturn. Treasury departments must consider the value of owning government obligations of highly indebted economies with fiat money printing presses compared to the value of gold today.

China Currency Bubble

With even greater non-performing domestic debt than the US and even greater poverty and wealth inequality, China is run by a totalitarian government responsible for running what in Crescat’s view is the largest banking and currency Ponzi scheme in world history. The inevitable if not imminent implosion of China’s financial system and economy only adds to our globally contagious economic downturn thesis and case for precious metals.

US Imbalances

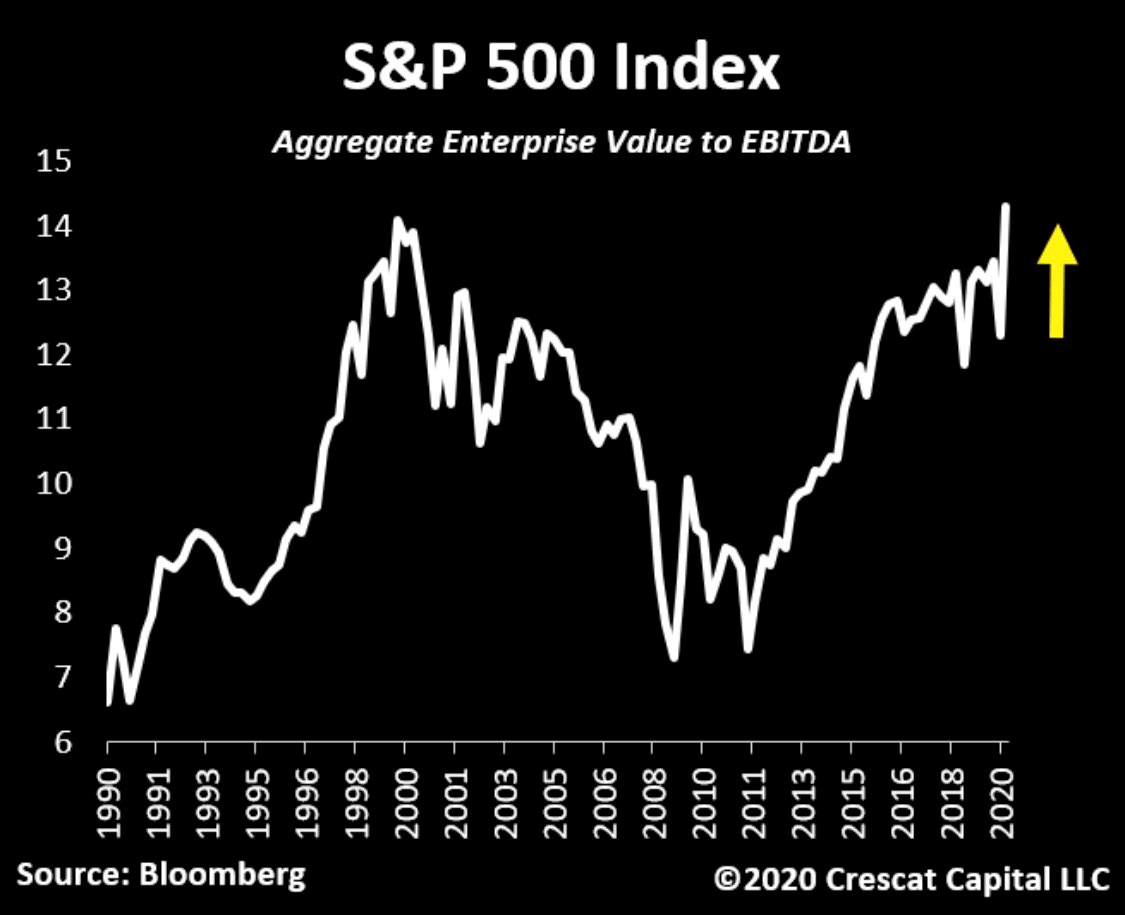

Aggregate enterprise value to EBITDA for the S&P 500 has never been higher. The set-up reminds us of early February when stocks were also grossly misaligned with economic reality. We think we are about to see another reckoning moment which will mark the second leg of the bear market.

Markets driven by euphoria never end well. The US stock market today is in la-la land. It is discounting a new expansion phase of the economy at the same time as a major recession has only just begun. Since the March lows, investors have turned overwhelmingly bullish. They are trusting that central banks’ liquidity will miraculously create economic growth rather than just temporarily ease the pain of declining gross domestic incomes and crushing debt burdens. This delusional thinking is induced by the intense but short acting dopamine response to Fed money printing but completely ignores how business cycles work. Government money printing has failed miserably, repeatedly, throughout history at eliminating recessions and frequently coincides with some of the worst downturns. Today, it is a major symptom of a severe recession if not a depression.

Ongoing government fiscal and monetary stimulus does not prevent economic downturns. To the contrary, such past actions are the moral hazard that is chiefly responsible for the imbalances that have built up over time already, the set-up for today’s recessionary environment in the first place. Brutal bear markets and recessions begin from record asset valuation bubbles and debt imbalances, and that is the case again this time. In our analysis, the current downturn has only just started and has much further to play out. Economic downturns are rarely halted and reversed by government intervention so early in the process. They must play out to bring the necessary creative destruction that sets the stage for a new economic expansion and bull market. That is how the business cycle works. We have not seen anything yet in terms of such a necessary downturn in equity valuations. We only had a brief taste of it in March, the first tremor. It has been followed by a massive, but overzealous relief rally.

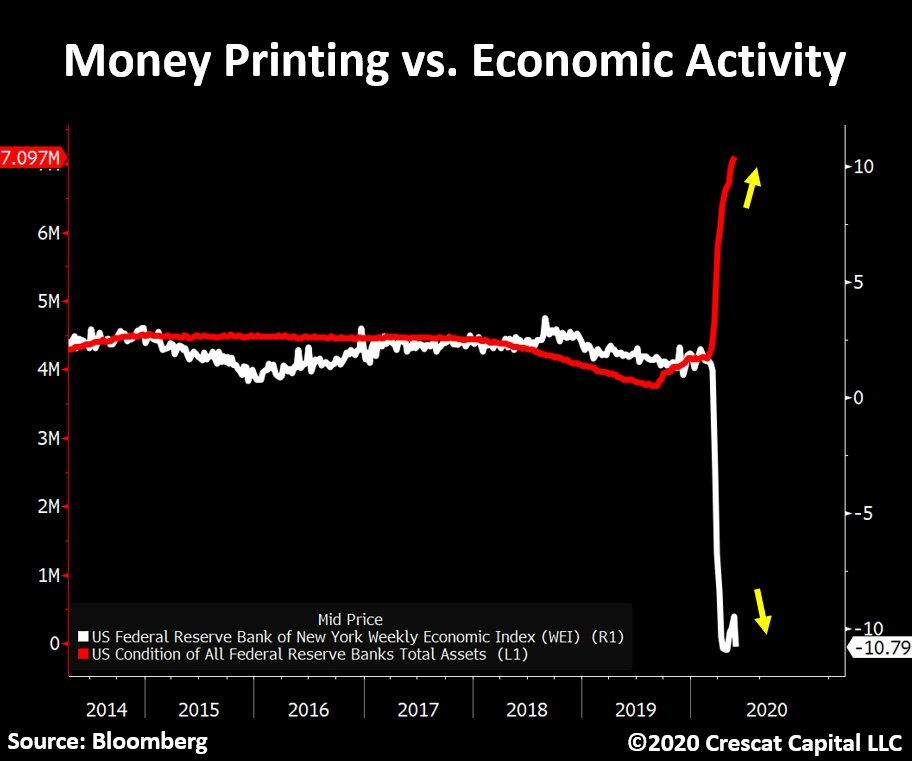

Money printing does not fix the economy. It is visually astonishing how divergent the Fed’s balance sheet assets and the Weekly Economic Index (WEI) has been. Developed by the Federal Reserve of New York, WEI measures activity by combining a series of other baseline indices such as same-store retail sales, consumer sentiment, initial jobless claims, temporary and contract employment, steel production, fuel sales, and even electricity consumption. The chart below shows clearly that this index hasn’t experienced any level of improvement since the March lows, a drastic comparison to the recent vertical growth in Fed’s assets.

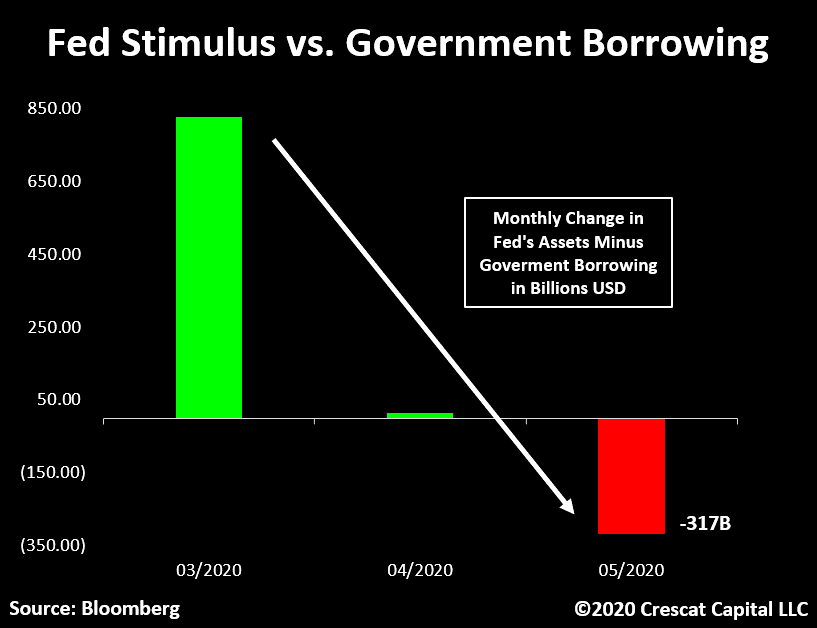

We are also seeing a significant liquidity withdrawal due to the historic debt imbalance today. The Fed’s weekly monetary stimulus has not only been drastically reduced but is also being dwarfed by the amount of government debt growth. We just had the largest monthly net issuance of Treasuries in history, $760B in May alone. This number surpassed the Fed’s quantitative easing by over $300B! It is the largest net decline in Fed assets vs. government debt since the repo crisis started back in September of 2019. The government debt is more than crowding out all the new liquidity.

In our view, the Fed is incapable of injecting enough liquidity to quell the losses in asset values associated with what was $250 trillion in global debt at a record three times global GDP before the Covid-19 crisis even began without also triggering a fiat money crisis. This is what we call a liquidity trap.

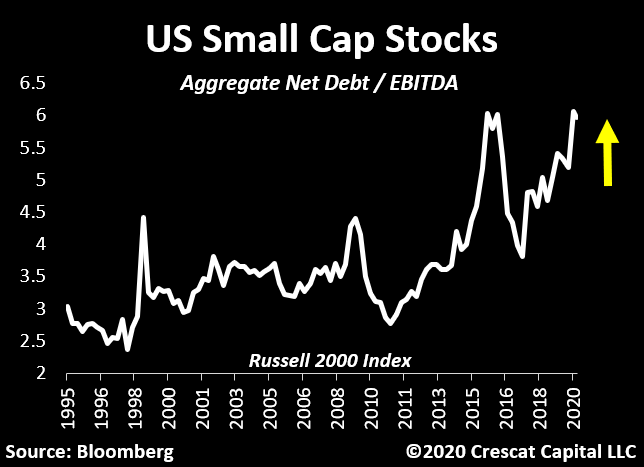

Another part of the market and economy that looks particularly fragile is small cap stocks. These stocks have never been so indebted relative to EBITDA. In terms of valuation, the Russell 2000 stocks now trade at a historic 15x EV to 2020 EBITDA estimates! There is a stunning and totally unwarranted level of optimism still priced into the markets today.

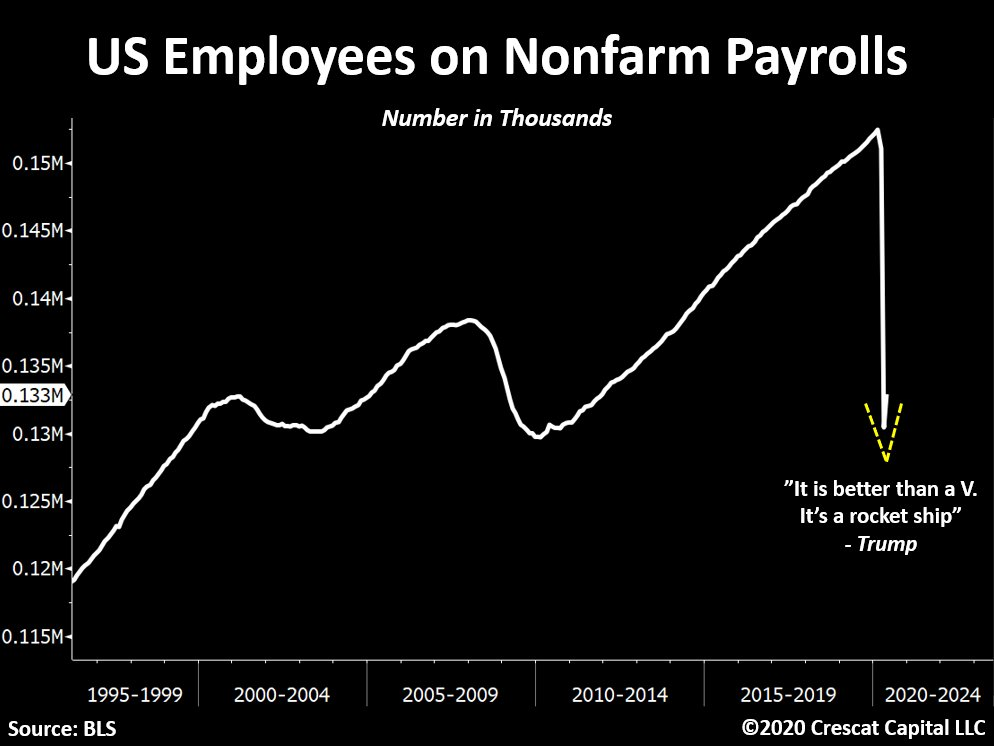

US labor markets unexpectedly improved last month but were not enough to support the bullish narrative of late. To put things into perspective, since the market peak we saw nonfarm payrolls drop by close to 22 million employees. May’s positive number, the best monthly change ever, was an improvement of close to 3 million payrolls, but even the Department of Labor questioned the validity of these numbers. The DOL said it believed the unemployment rate was understated in both April and May while May indeed did register improvement. In any case, we would need 7 months like the prior to regain the same level of strength in labor markets prior to the virus outbreak. The timid “V†shape recovery looks nothing like a “rocket ship†as Trump referred to in one of his recent tweets.

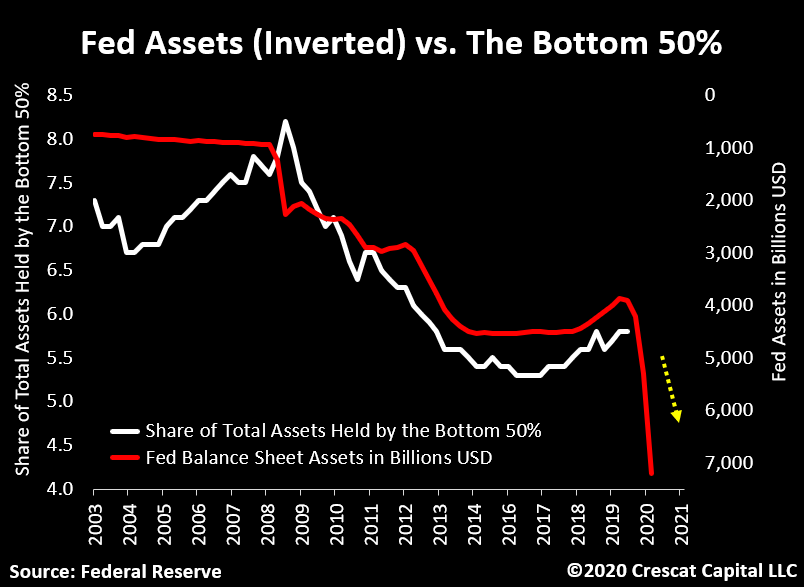

The current monetary stimulus is severely amplifying the wealth gap problem in the US. When inverted, the Fed’s balance sheet asset has followed the share of total assets held by the bottom 50% remarkably close. Logically, this relationship makes sense. As shown in the chart below, since QE 1 started, the less financially privileged parts of the society have suffered from a shrinkage of wealth relative to the overall pie. If the economy continues to prove incapable of growing organically, further monetary stimulus will be necessary and therefore only exacerbating the inequality problem.

Crescat’s New Precious Metals Activist Campaign with Quinton Hennigh as Advisor

With record global debt to GDP, historic US equity valuations, and new fiat money printing around the globe, the macro environment is incredibly bullish for precious metals today. We have been hard at work negotiating deals in select gold and silver exploration companies. In our hedge funds, we have been investing in private placements in public companies, often at significant discounts with warrants. We are building activist positions in some the best properties around the globe at highly attractive valuations after a decade long bear market. We are following the economic and technical advice of renowned exploration geologist, Quinton Hennigh, PhD. Based on his extensive experience and many past successes, we have asked Quinton to serve as Crescat’s geologic and technical advisor. He has identified many of the best next generation mining assets on the planet that are still in hands of junior exploration companies today. We are bringing necessary capital to advance these projects in return for significant stakes.

Quinton has 30 years of exploration experience, starting with Homestake, Newcrest, and Newmont then branching off from there. He is now Chairman and President of Novo Resources, one of Crescat’s largest positions. At Novo, Quinton made a massive nonconventional and potentially highly profitable gold discovery in the Pilbara region of Western Australia. Quinton is credited with the 5 million ounce discovery of the Springpole alkaline gold deposit near Red Lake, Ontario. He was instrumental in recognizing the potential for Fosterville mine in Eastern Australia and advocating for Kirkland Lake to acquire it, which it did in 2016. It was Quinton’s expertise and enthusiasm that made the allocation of capital happen to develop what was arguably the single most economically successful high-grade gold mine of the last decade.

At Crescat, we are striving to recreate that same kind of value again capitalizing on Quinton’s knack for identifying junior companies with high quality assets today that have the potential to be some of the most profitable mines of the next decade. We are bringing friendly activist capital to these exciting new deposits. They are not the same old picked-over carcasses of the last mining cycle. We are investing in a new generation of mining deposits all over the world. Each company is unique and each one has a great story tell. Crescat will be broadcasting a series of live videos with Quinton in the coming days and weeks on Youtube profiling our strategy and the investment thesis behind each of these companies. Each one controls potentially rich underground gold and silver deposits in viable jurisdictions that should propel them to substantially larger valuations in today’s macro environment.

Capitalizing on a new bull market in precious metals is one of our most important themes today. Crescat is infusing important growth capital into carefully vetted companies. In some cases, we are also bringing in new expertise to the board and technical team. Most importantly, and with Quinton’s guidance, we are making sure that our capital is spent on the key technical work needed to validate and expand what are some of the world’s most promising discoveries.

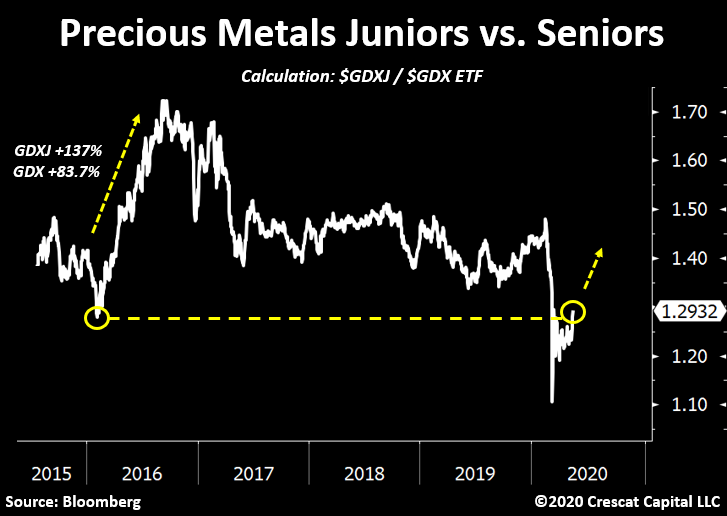

We are encouraged that small cap precious metals miners have recently started to outperform big caps. The junior-to-senior ratio is exactly where it was ahead of the 2016 gold rally. If you recall, back then, after 6 months: the GDX ETF (seniors focused) went up 87% while the GDXJ ETF (juniors focused) was up 137%!

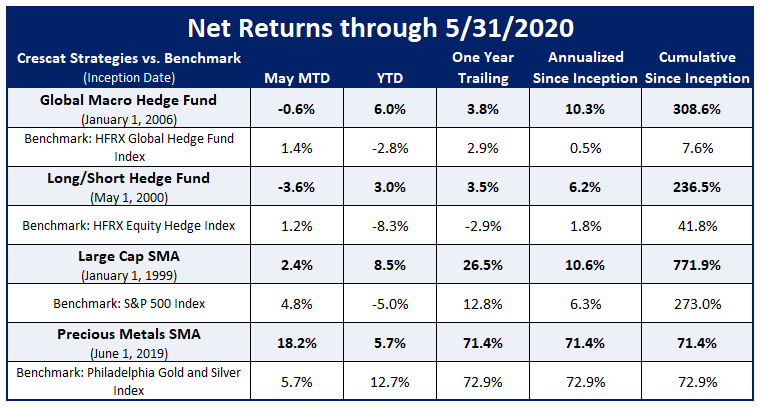

Crescat’s Precious Metals SMA strategy with its overweighting in more of the smaller cap names, including many of Quinton’s favorites, handily outperformed its benchmark in May rising 18.2% for the month versus 5.7% for the Philadelphia Stock Exchange Gold & Silver Index.

China

In our analysis, the Chinese Communist Party is running a $42 trillion banking Ponzi scheme that is ripe to implode in a currency crisis. The US and other highly leveraged democratic developed economies are in bad shape economically today, no doubt, but its peoples need not fall into a Thucydides’ trap, i.e., to be unduly threatened by a perceived rising power. China is a menace to global freedom and democracy, to be sure, but the country has a weak hand economically which will almost certainly be its downfall. It is true and well documented that the CCP runs an unfair technology transfer regime, discriminatory licensing, outbound investment schemes, cyber hacking, and intellectual property theft. As a result, Western democratic advanced economies and their Eastern allies are doing the right thing today by disengaging with the CCP on trade. The Chinese economy is destined to implode on its own, most importantly due to its historic banking imbalances.

We should not forget that US economic prominence in the world is a result of a long-standing Constitution built on core principles that include individual rights and freedoms, rule by the people, freedom from tyranny, checks and balances that prevent abuse of power, and limited government. The grass is most definitely not greener under totalitarian communism which by contrast has a track record of persistent and inevitable economic impoverishment and human rights enslavement. It is important to understand that the imbalances in the Chinese economy are even more extreme than the US which faces its own historic imbalances. As a result, global economic contagion risks remain extremely elevated today. China at the forefront of these risks arguing for a continuation of the serious global financial market downturn and recession that only just began in March.

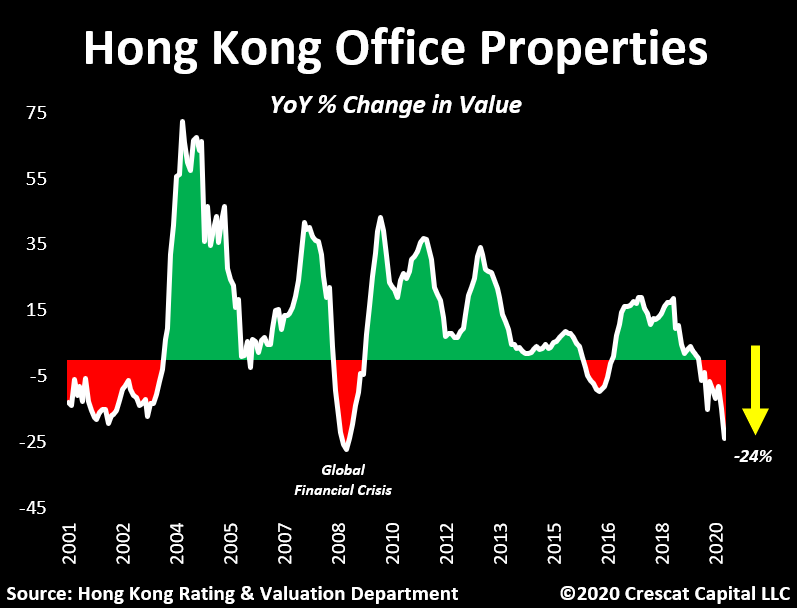

The Chinese Communist Party takeover of Hong Kong along with the dismantling of its democracy has destroyed the former British colony’s status as an international banking haven and jeopardized its special trade status with both the US and the UK. We believe global capital has been fleeing the country and outflow pressure only continues. Meanwhile, Hong Kong sits on one of the most overvalued property markets in the world that has just started to burst. For instance, Hong Kong office properties are now plunging by 24% YoY, the worst decline since I the Global Financial Crisis. One major difference, however, is that Hong Kong’s under-reserved massive $3.3 trillion banking system was not 9 times the size of its economy back then.

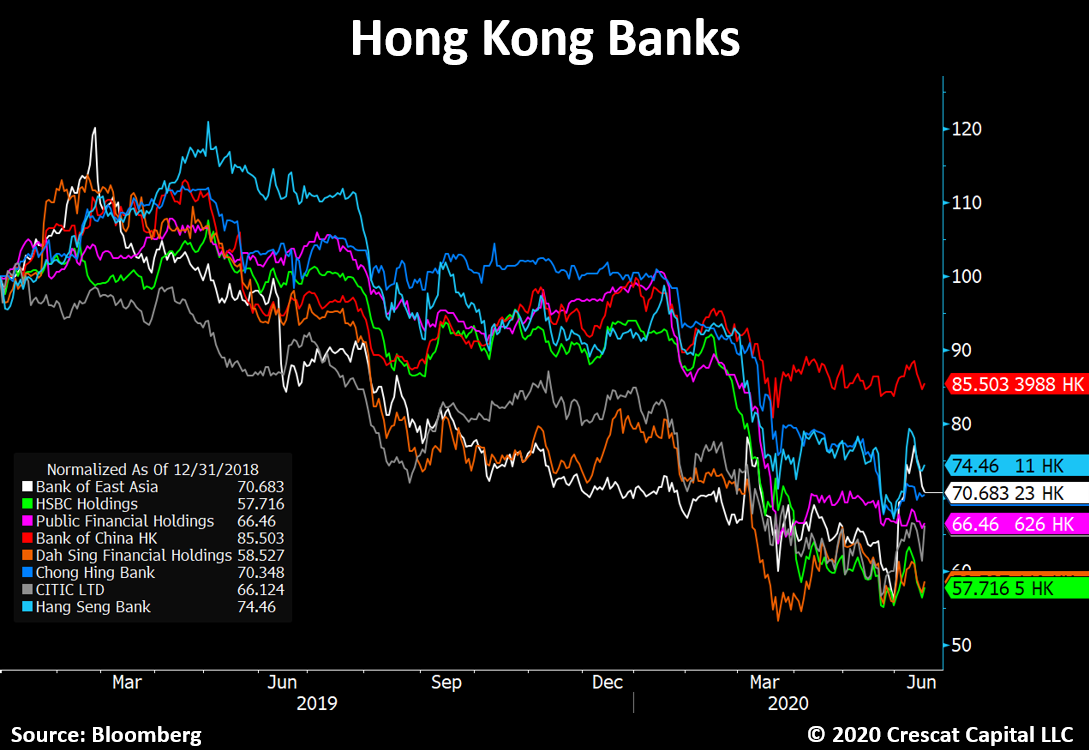

Private non-financial credit in the country is a world beating 300% of GDP. Hong Kong is on the Bank for International Settlements’ crisis watch list for that as well as its record high debt service ratio among all countries. The performance of Hong Kong’s banks over the last two years, as we show below, illustrates the risks to the Hong Kong banking system and the country’s currency peg to the US dollar.

Like with China, the world still believes Hong Kong maintains sufficient foreign reserves to maintain the value of its currency. We believe the reserves supporting both the yuan and Hong Kong dollar are encumbered. Necessarily, these reserves are the collateral in the global interbank FX markets that have been posted in defense of these currencies against years of Chinese capital outflow pressure. We believe China and Hong Kong are not netting the collateral posted for their short FX positions from their FX reserves. A currency crisis is potentially just a margin call away.

Crescat’s Positioning

At Crescat, we remain determined to capitalize on a US equity market downturn via short positions in our hedge fund strategies and believe there is much further downside for stocks at large ahead. Asset bubbles always burst. US stocks prices are way ahead of future fundamentals and poised to disappoint. Equity and credit markets are not immune from a business cycle downturn. They must eventually catch up to the abysmal fundamentals of today’s global economy that is in a severe recession.

With the Covid-19 shutdowns, we just experienced an economic shock likely worse than any single quarter of the Great Depression. It was made worse by the pre-existing imbalances that were threatening to send the economy into a recession of their own accord as had been forewarned by Crescat’s macro model. Yet stock prices are back near record highs and record valuations in response to temporary excitement over massive fiscal and monetary stimulus. It is the same unwarranted speculative mania that was driving the market in 2019 and early 2020, a pumping up of stock prices totally unwarranted by simultaneously deteriorating fundamentals and solely based on the faith in government stimulus.

The macro fundamentals for a new precious metals bull market have never been better as we have outlined herein. We are positioned long gold and silver mining equities across all four Crescat strategies.

Persistent, bi-partisan abuse of Keynesian policies has been a poor substitute for free market capitalism. The lesson is clear. Excessive and ongoing government intervention only creates mounting non-productive debt that stifles future real economic growth. Credit imbalances in the world today are at a historic high relative to global GDP. They are even worse in state-run communist China where historic banking bubbles warn of coming currency crises for both the Chinese yuan and Hong Kong dollar. Crescat Global Macro Fund continues to maintain long US dollar call option positions versus yuan and Hong Kong dollar puts with large US banks counterparties. Our goal is to profit with asymmetric reward-to-risk. While it has yet to play out in the dramatic fashion we envision, we believe it is coming soon.

Profit Attribution by Theme in the Crescat Global Macro Fund

Performance Across All Crescat Strategies

Given the enormous imbalances in the markets today, we believe it is an excellent time to consider an allocation to Crescat’s strategies.

Posted by AGORACOM

at 8:41 AM on Monday, June 22nd, 2020

Barrick Gold commenced drilling on several high priority gold targets

Since entering the JV agreement with Loncor in January 2016, Barrick has conducted various exploratory programs to define drill targets that offer the early potential of attaining “Tier 1†status.

“Tier 1” deposits target a minimum of 5 million ounces

TORONTO, June 22, 2020 (GLOBE NEWSWIRE) — Loncor Resources Inc. (“Loncor” or the “Company“) (TSX: “LN”; OTCQB: “LONCF”) announces that Barrick Gold (Congo) SARL has commenced its core drilling program on several priority gold targets within the Ngayu greenstone belt in the northeast of the Democratic Republic of the Congo (“DRCâ€). The beginning of the drilling campaign signals a significant step in the sequence of events necessary to assess numerous areas of potential. Since entering the JV agreement with Loncor in January 2016, Barrick has conducted various exploratory programs to define drill targets, targets that offer the early potential of attaining “Tier 1†status.

Commenting on the start of drilling at Ngayu, Loncor’s CEO Arnold Kondrat said: “Barrick continues to illustrate the progress that can be made in the DRC. Having built the successful Kibali gold mine approximately 220 kms away, Barrick has now embarked on its drilling program at Ngayu, an area that we believe holds the potential for further significant gold discoveries similar to our own Adumbi deposit.â€

The drilling on the Anguluku prospect is targeting a folded and thrust sequence of mineralised banded ironstone formation (“BIFâ€). Further drilling is planned to be undertaken by Barrick at the other priority targets of Medere, Makasi, Lybie, Salisa and Bakpau NE in the Imva area in the west of the Ngayu belt (see Figure 1 below)

Loncor Continues to Explore – Imbo Exploitation Permit (Loncor 76.29%)

Outside of the Barrick joint venture, exploration activities by Loncor continued on Loncor’s Imbo Project in the east of the Ngayu belt. The Imbo Project contains 2.5 million ounces of inferred mineral resource (30.65 million tonnes grading 2.54 g/t Au), which includes the 2.19 million ounce inferred mineral resource of the Adumbi deposit (28.97 million tonnes grading 2.35 g/t), with 76.29% of this resource being attributable to Loncor via its 76.29% interest in the Imbo Project. Fieldwork by Loncor geologists have been focusing on the Imbo East prospect 12 kilometres southwest of the Adumbi deposit, along the same mineralised structural trend. Gridding, soil and rock sampling are being undertaken over a strike length of 3.6 kilometres at Imbo East.

In addition, two new targets have been generated. Both these target areas were identified from the compilation and interpretation of previous, historical exploration data including soil geochemistry, rock chip and channel sampling. At Mambo Bado, 1.5 kilometres northwest of the Adumbi deposit, a prominent geochemical gold in soil anomaly is located on an extensional, E-W structural jog along the 14-kilometre northwest trending mineralised shear zone within the Imbo permit area. No drilling has been undertaken previously on this promising target. Two kilometres south of the Adumbi deposit, at Lisala, altered and brecciated BIF with anomalous rock sampling requires further follow up with gridding, soil sampling and additional channel sampling.

About Loncor Resources Inc. Loncor is a Canadian gold exploration company focussed on the Ngayu Greenstone Belt in the northeast of the Democratic Republic of the Congo (the “DRCâ€). The Loncor team has over two decades of experience of operating in the DRC. Ngayu has numerous positive indicators based on the geology, artisanal activity, encouraging drill results and an existing gold resource base. The area is 220 kilometres southwest of the Kibali gold mine, which is operated by Barrick Gold (Congo) SARL (“Barrickâ€). In 2019, Kibali produced record gold production of 814,000 ounces at “all-in sustaining costs†of US$693/oz. Barrick has highlighted the Ngayu Greenstone Belt as an area of particular exploration interest and is moving towards earning 65% of any discovery in 1,894 km2 of Loncor ground that they are exploring. As per the joint venture agreement signed in January 2016, Barrick manages and funds exploration on the said ground at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. In a recent announcement Barrick highlighted six prospective drill targets and are moving towards confirmation drilling in 2020. Subject to the DRC’s free carried interest requirements, Barrick would earn 65% of any discovery with Loncor holding the balance of 35%. Loncor will be required, from that point forward, to fund its pro-rata share in respect of the discovery in order to maintain its 35% interest or be diluted.

In addition to the Barrick JV, certain parcels of land within the Ngayu project surrounding and including the Adumbi and Makapela deposits have been retained by Loncor and do not form part of the joint venture with Barrick. Barrick has certain pre-emptive rights over the Makapela deposit. Adumbi and two neighbouring deposits hold an inferred mineral resource of 2.5 million ounces of gold (30.65 million tonnes grading 2.54 g/t Au), with 76.29% of this resource being attributable to Loncor via its 76.29% interest in the project. The Makapela deposit (which is 100%-owned by Loncor) has an indicated mineral resource of 614,200 ounces of gold (2.20 million tonnes grading 8.66 g/t Au) and an inferred mineral resource of 549,600 ounces of gold (3.22 million tonnes grading 5.30 g/t Au).

Resolute Mining Limited (ASX/LSE: “RSG”) owns 26% of the outstanding shares of Loncor and holds a pre-emptive right to maintain its pro rata equity ownership interest in Loncor following the completion by Loncor of any proposed equity offering.

Additional information with respect to Loncor and its projects can be found on Loncor’s website at www.loncor.com.

Posted by AGORACOM

at 8:28 AM on Monday, June 22nd, 2020

Vancouver, British Columbia–(Newsfile Corp. – June 22, 2020) – Sweet Earth Holdings Corp. (CSE: SE) (FSE: 1KZ1) (“Sweet Earth“) and Mota Ventures Corp. (CSE: MOTA) (FSE: 1WZ1) (OTC Pink: PEMTF) (“Mota“) are pleased to announce that they have entered into a letter of intent (the “LOI“) under which Sweet Earth will become the exclusive dog treat provider to Mota’s eCommerce direct consumer brand, Nature’s Exclusive.

Sweet Earth is a complete vertically integrated “farm to shelf” company that is a member of the US Hemp Association and is Leaping Bunny Certified, while Mota is a direct to consumer provider of a wide range of CBD products in the United States and Europe. The two companies (the “Partners“) expect to sell Sweet Earth’s award-winning products, beginning with CBD dog treats and paw and nose balm, through Mota’s consumer brand, Nature’s Exclusive, which is sold in the United States. Mota has initially selected Sweet Earth’s popular Beef and Cheddar Potato CDB Dog Treats to be sold under the Nature’s Exclusive brand.

Sweet Earth’s Dog Treats are Certified Organic and Leaping Bunny Certified1.

Each organic treat is fortified with Vitamin E as a natural preservative.

Packaging will be customized to the specifications of the Nature’s Exclusive brand.

According to Dogs Naturally2, research shows that CDB dog treats are effective dog supplements for:

Arthritis and joint pain

Anxiety

Digestive issues

Neurological disorders (such as seizures and epilepsy)

Blood disorders

According to Today’s Veterinary Business, the U.S. pet treat market reached US$6.7 billion in 2019, with CBD, the largest growth component3 within the pet treat sector. The journal’s research also provides insight into key trends in a sector that has continued to grow at an average 3% CAGR.

Online sales of pet snacks have rapidly grown from 0% to 13%. A catalyst of eCommerce’s rapid market expansion is attributed to the platform’s ability to educate consumers on products prior to purchase.

Dog owners are increasingly focused on quality snacks that are produced locally, as highlighted by the decrease in sales of import treats. Made in the USA4 has become a key factor in consumer purchasing.

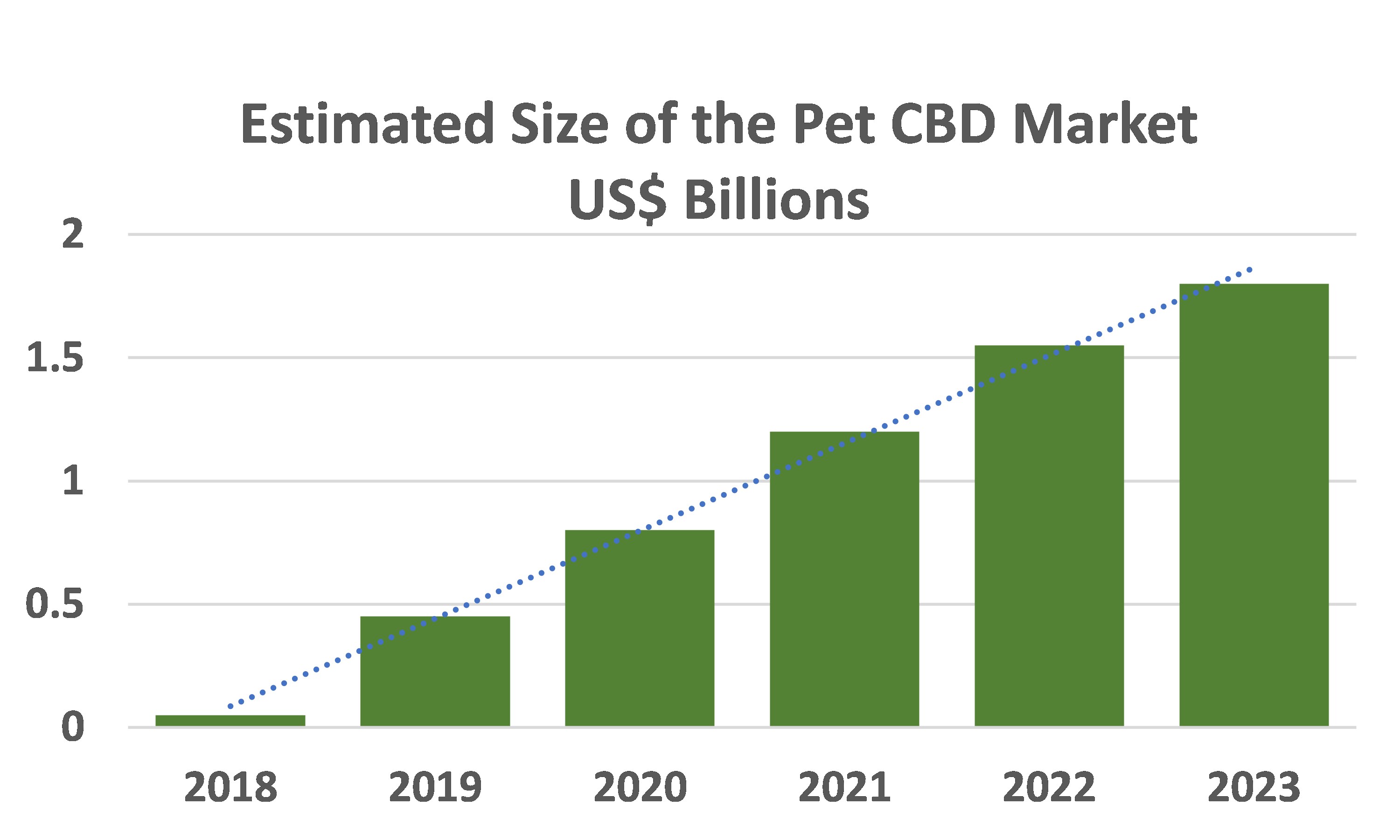

11% of dog owners have purchased dog supplements or treats containing CBD or hemp; however, as highlighted in Figure 2, the segment is far outpacing the overall growth of the pet snack and supplement sector.

Figure 2: Estimated Size and Growth of US CBD Pet Market

Brightfield Group5 estimates the US CDB pet market will increase from less than US$100 million in 2018 to approximately US$1.8 billion in 2023.

The 104% CAGR highlights a product with rapid expansion and penetration into the growing pet snack sector.

Global Market Insight predicts that the Dog Food and Snacks market will surpass US$75.0 billion by 2025 and increase to a CAGR of 4%

Hall of Fame Quarterback and Brand Ambassador to Sweet Earth, Warren Moon, commented, “I think the Partners will make a great team. Both come to the table with value-added capabilities and similar visions of providing high-quality products to discerning consumers.” Sweet Earth President, Amrik Virk commented, “this is a great opportunity for Sweet Earth to team with Mota, which has grown 110% YOY, and recently announced sales of C$5.1 million for the month of May.”

Readers are cautioned that the LOI does not set out the final terms for the collaboration between the Partners. The establishment of the sales partnership remains subject to the negotiation of definitive documentation between the Partners.

About Sweet Earth

Sweet Earth is a vertically integrated “farm to shelf” hemp grower with a farm in Applegate, Oregon, that maintains a full line of hemp and CBD products for the US and global market. Its products combine CBD with herbal and organic ingredients, all of which are selected for their beneficial properties to soothe, rejuvenate, and reduce inflammation. In addition to high-end finished products, Sweet Earth prides itself on sustainability by minimizing the use of plastics in both production and packaging.

Sweet Earth’s in-house genetics team has been working on its own proprietary hemp strain. This strain has been grown in its indoor greenhouse resulting in high yielding CBD rich flower. Sweet Earth looks forward to planting this new strain outdoors for the 2020 season. Sweet Earth products are sold on its website: www.sweetearthcbd.com.

About Mota Ventures Corp.

Mota Ventures is an established e-Commerce, direct to consumer provider of a wide range of natural health products including CBD and psychedelic medicine products in the United States and Europe. In the United States, the company sells a CBD hemp-oil formulation derived from hemp grown and formulated in the US through its Nature’s Exclusive brand. Within Europe, its Sativida brand of award winning 100% organic CBD oils and cosmetics are sold throughout Spain, Portugal, Austria, Germany, France, and the United Kingdom. In Germany, Verrian currently produces natural psilocybin extract capsules under the PSI GEN and PSI GEN+ brand. Mota Ventures is also seeking to acquire additional revenue producing CBD brands and operations in both Europe and North America, with the goal of establishing an international distribution network for CBD products. Low cost production, coupled with international, direct to customer sales channels will provide the foundation for the success of Mota Ventures.

Posted by AGORACOM

at 12:48 PM on Thursday, June 18th, 2020

Retained WSP Canada Inc. (WSP) to assist Vertical with its quarry permitting application.

Vertical’s operations partner, Magnor Exploration Inc., will work with WSP to support the preparation, drafting and submission of the full quarry permitting request

VANCOUVER, BC / ACCESSWIRE / June 18, 2020 / VERTICAL EXPLORATION INC. (TSX-V:VERT) (“Vertical”or “the Company”) is pleased to announce it has retained the services of WSP Canada Inc. (WSP) to assist Vertical with its quarry permitting application to the Government of Quebec for its St-Onge Wollastonite project located in the Lac-Saint-Jean region of Quebec.

Vertical’s operations partner, Magnor Exploration Inc., will work with WSP to support the preparation, drafting and submission of the full quarry permitting request, including an application under Section 22 of the Environmental Quality Act for a Certificate of Authorization (CA) from the Quebec Ministry of Environment and Fight against Climate Change (MELCC) as well as a request for a BEX (Bail d’Exploitation Miniere Permit) from the Quebec Ministry of Energy and Natural Resources (MERN).

WSP Canada Inc. is part of WSP Global Inc., which is one of the world’s leading professional services firms providing engineering and design services to clients in the transportation and infrastructure, property and buildings, environment, power and energy, resources, and industry sectors, as well as offering strategic advisory services. WSP Global Inc. has approximately 49,000 employees working in 500 offices across the globe.

Vertical is very pleased to have retained such a prominent professional services firm to support its quarry permitting application for St-Onge and looks forward to providing further updates on the permitting application in the near future.

Vertical advises that the production decision on the St-Onge deposit was not based on a feasibility study of mineral reserves, demonstrating economic and technical viability, and as a result, there may be an increased uncertainty of achieving any level of recovery of minerals or the cost of such recovery, including increased risks associated with developing a commercially minable deposit. Historically, such projects have a much higher risk of economic and technical failure. There is no guarantee that production will occur as anticipated or that anticipated production costs will be achieved.

ABOUT VERTICAL EXPLORATION

Vertical Exploration’s mission is to identify, acquire, and advance high potential mining prospects located in North America for the benefit of its stakeholders. The Company’s flagship St-Onge Wollastonite property is located in the Lac-Saint-Jean area in the Province of Quebec.

Posted by AGORACOM

at 9:10 AM on Thursday, June 18th, 2020

1st hole drilled to depth of 525m at West Timmins Property

Core logging and sampling will commence shortly and samples will then be submitted for analysis.

Vancouver, British Columbia–(Newsfile Corp. – June 18, 2020) – Affinity Metals Corp. (TSXV: AFF) (“the Corporation”) (“Affinity”) is pleased to report that it has now completed drilling the first hole on the West Timmins property located approximately 29 km southwest of Timmins, Ontario, Canada.

The hole was drilled to a depth of 525 meters. Core logging and sampling will commence shortly and samples will then be submitted for analysis.

The property package consists of 20 mineral tenures spanning 429 hectares. The property directly adjoins to the west and along geological strike to the Melkior Carscallen project with both properties optimally located directly along the northern flank of the prolific Destor Porcupine Fault Zone. Melkior very recently made a significant gold discovery that has attracted not only the market’s attention but also the interest of Kirkland Lake Gold to participate in furthering exploration of the Melkior project model through joint participation.

The ground making up the West Timmins property was included/highlighted as a specific project example which meets exploration model recommendations as outlined within the 2012 published, Timmins Resident Geologist Report: “Recommendations for Exploration – Gold in Felsic Intrusions”. The geological model and potential of the West Timmins property correlate positively with the recent Melkior Carscallen exploration advancements.

The property is road accessible with a major highway (101) and regional scale power utility transmission lines passing directly through the property. Both Induced Polarization and Acoustic EM geophysics surveys have been conducted on the property and will assist in guiding future exploration.

The West Timmins property is located along the same structural and geological trend which hosts the Pan American Silver “Timmins West Mine” located approximately 13 km to the east along highway 101 and is also in close proximity to the Timmins mining camp, which is a major structural control corridor that has produced over 75 million ounces of gold.

About Affinity Metals

Affinity is focused on the acquisition, exploration and development of strategic metal deposits within North America. The Company is structured as a “Prospect Generator”.

In addition to the present work being conducted on the West Timmins property, Affinity is also focused on advancing the Regal Project located near Revelstoke, British Columbia, Canada. The Regal property is located in the northern end of the prolific Kootenay Arch and hosts two major geophysical anomalies as well as three past producing mines. Recent drill results included a new silver discovery with an 11.10 meter interval of 143.29 g/t silver which included a 0.55 meter interval of 2,612.0 g/t silver.

On behalf of the Board of Directors

Robert Edwards, CEO and Director of Affinity Metals Corp.

Given the enormous imbalances in the markets today, we believe it is an excellent time to consider an allocation to Crescat’s strategies.

Given the enormous imbalances in the markets today, we believe it is an excellent time to consider an allocation to Crescat’s strategies.

{kind=link}