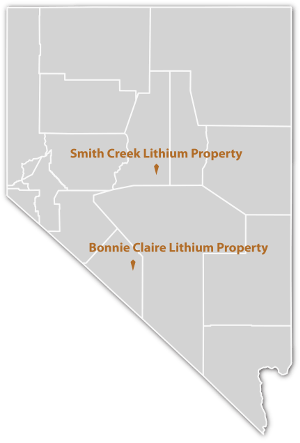

Iconic Minerals has three highly prospective Lithium exploration

properties located in Nevada, the Bonnie Claire Sarcobatus Valley

Lithium property, the Smith Valley Creek Property, and the Third Nevada

Lithium Property.

Bonnie Claire Property

Property Overview

11.8 Billion pounds of lithium carbonate equivalent (28.5 Million tonnes of LCE) Inferred Resource (43-101).

Potential to be the largest lithium resource globally (based on size)

Bonnie Claire is a 100% owned lithium brine property comprising of

23,100 acres of contiguous placer claims, currently in control of 28.75

square miles (75 km2) located in Nye County, Nevada.

Property area is contained within a valley that is 60kms from the

only producing lithium mine in North America (Albermarle Silver Peak

Mine).

Over +20 miles (+30 km) long and 12 miles (20 km) wide into which streams from an +800 mi2 (2,070 km2) drainage basin empty.

Sampling of salt flats within the basin, have found lithium values in salt samples yielding up to 340 ppm.

Current claim block covers the gravity low and associated mud flats

that could be used for evaporation ponds if significant lithium brines

are discovered in drilling.

Preliminary NI 43-101 Technical Report completed Read More

A total 5,550 feet has been drilled at the Bonnie Claire with an average 963+ppm from four drill holes

Great infrastructure

Local end-users

Property Details Snapshot

Drainage Basin (20 x 30 kms)

830 square miles

Gravity Lows (length)

20 x 30 kms

Valley Sediment (Range)

460 – 610m (1,500 to 2,000ft)

BLM Drilling Permits

Drilling Program

Drilling completion of first of three test wells

Smith Creek Valley Property

Controls 808 placer claims totaling 25.25 square miles (65.4 km2) over a major gravity low.

The enclosed Smith Creek Valley Basin covers 582 square miles (1,507

km2), which is slightly larger than Clayton Valley Basin where lithium

brines are produced.

Smith Creek Valley is over +40 miles (+64 km) long in a north-northeast direction and averages 9 miles (14.5 km) in width.

The vast majority of rock weathering into the basin is felsic ash flow tuff, which is an excellent source of lithium.

Lithium Brine Benefits

Lower Cost Exploration

Easy access because flat and arid

Decreased environmental impact

Shorter Timeline to Production

Requires Less Capital

Lower Cost Production than bedrock

Found beneath salt flats in brine bearing aquifers

Easily pumped to Surface from vertical production well

After evaporation lithium recovered in small on site mill

Potassium may also be recovered

Nevada is a Geopolitically Stable Jurisdiction

Gold Projects

The company’s Gold exploration portfolio includes the Hercules

property in the Como mining district, 17 kms from the famous Comstock

Lode mine, the New Pass property in the New Pass mining district, and

the Squaw Creek property located in the northern area of the Carlin

Trend.

Situated within and on the margins of the Como mining district, located in Lyon County, Nevada.

Como district was worked as early as the late 1850s, before the

famous Comstock Lode deposit was discovered about 10 miles (16 km.) to

the north by prospectors following float upstream from placer gold

deposits at Dayton.

By the early 1860’s the Como district was abandoned due to the rich

lodes having been discovered at Virginia City (Russell, 1981).

In the late 1880’s the Hercules Mining Company explored the occurred

with the excavation of another 1,500 feet (450 m) of underground

workings.

Gold and silver property which, is comprised of 107 unpatented lode mining claims (2,231 acres).

The property is located in eastern Churchill County, Nevada; in the

New Pass Mining District, 27 miles west of Austin, Nevada and 105 miles

east of Reno.

Iconic Minerals has a controlling interest in the property, in a

joint venture with White Knight Gold U.S. Inc., (now U.S. Gold), with

Iconic earning a 50% interest.

Property is located 42 miles due north

of Battle Mountain, Nevada and lies between the Midas and Ivanhoe mining

districts on the northern portion of the Carlin Trend, six miles north

of the Dee Mine in the Lower Plate Bootstrap Window.

Iconic’s Research and Development partner

St-Georges’ metallurgists report that they

have successfully improved the concentration of lithium in the

Sediments, originally reported in December using mechanical separation

and selective leaching of other elements within the Sediments.

The additional tests St-Georges completed

in Stage 2, through selective leaching methods, have improved the

elimination of barren material from 55% to 85%-88%, while retaining 100%

of the lithium.

Upon completion approximately 12% to 15%

of the original material remains for further processing and

purification. This process may significantly reduce the cost of

production.

Lithium also leachable by water

FULL DISCLOSURE: Iconic Minerals is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM-JC

at 9:45 PM on Sunday, March 17th, 2019

SPONSOR: New Age Metals Inc.

(TSX-V: NAM) The company’s new Lithium Division has already made

significant acquisitions in Canada and the USA. The company also owns

one of North America’s largest primary platinum group metals deposit in

Sudbury, Canada. Learn More.

NAM: TSX-V

———————

Huge demand for copper, cobalt, lithium and nickel in the offing as EV uptake increases

Purkiss’s presentation also emphasises an increasing amount of nickel content in lithium nickel manganese cobalt oxide (NMC) batteries, adding that nickel input primarily sourced from sulphides is a declining supply source.

Creamer Media Senior Deputy Editor Contract Publishing and Sales

Investors focused on the mining

sector may not fully appreciate how quickly the electric vehicle (EV)

is being adopted globally, in light of the world pursuing a low-carbon

emissions future, says battery metals investment vehicle Cobalt 27 Capital chairperson and CEO Anthony Milewski, who warns of a potential deficit in the supply of the metals critical to achieving this future.

Global management consultancy firm McKinsey & Company says 2017

marked the first time EV sales passed the one- million mark, noting in

May 2018 that, by 2020, EV producers could be moving 4.5- million units,

about 5% of the overall global light-vehicle market.

Also presenting at this year’s MiningIndaba was nickel-focused development vehicle Consolidated Nickel Mines (CNM) CEO Simon Purkiss, who provided an update on the restarting of the company’s Munali nickel mine, in southern Zambia.

Purkiss points to EV growth being an important factor in nickel’s

demand-side development, noting a rapid increase in EV uptake, with financialservices company Credit Suisse predicting EV growth to 3.1- million units by 2021 and 14.2-million units by 2025.

CNM identified Munali, where operations

stopped in November 2011, owing to low nickel prices and poor

operational performance by the previous owners, as key to its

consolidation of nickel prospects in Southern Africa.

Purkiss told delegates that financing of the restart was complete and,

with the mine ramping up and the process plant being commissioned, first

concentrates were expected in February and were on track to being

transported to one of the nickel and copper smelters in the Southern Africa Development Community region in the first quarter of this year.

Purkiss says project economics were improved by changing the mining

method, revising the metallurgical process and optimising the labour

structure. Munali will produce low-cost nickel concentrate at $9 200/t

of nickel, while, in the long term, CNM expects lower-cost nickel

sulphate production of $5 000/t.

The company predicts global nickel stocks will decline until a

trigger point is reached, at which time restocking will take place.

Subsequently, says Purkiss, nickel prices will start rising, probably

rapidly, and nickel pig iron production will restart, but only to fill

Chinese stainless-steel demand, which will still be limited.

Purkiss’s presentation also emphasises an increasing amount of nickel content in lithium nickel manganese cobalt oxide (NMC) batteries, adding that nickel input primarily sourced from sulphides is a declining supply source.

Supporting his statement, a report on the lithium-ion battery market by Dublin-based market researcher Research & Markets foresees the market for NMC growing at a higher compound annual growth rate over 2018 to 2024.

EVs require high capacity and high power that can only be provided by using the NMC

battery type, says the researcher. “The use of new electrolytes and

additives support the charging of a cell up to 4.4 V/cell. The NMC cell is growing in its range as the three components involved are easy to blend together and can be made useful for a range of applications, from the automotive industry to energystoragesystems.â€

The lithium-ion battery market is estimated to grow exponentially

from $37.4-billion in 2018 to $92.2-billion by 2024. Research &

Markets attributes the growth of the market not only to increased demand

for plug-in vehicles but also to the growing need for automation and battery-operated materials- handling equipment, the increasing demand for smart devices and other industrial goods, and the high requirement of lithium-ion batteries for various industrial applications.

“However, factors such as safety issues related to storage and the transport of spent batteries hinder the market growth,†adds Research and Markets.

Nonetheless, Milewski is adamant that the level of activity in the EV

battery metals space is only the ‘tip of the iceberg’, with the broader

uptake of EVs yet to be fully realised.

He says demand for cobalt really depends on EV penetration. A material increase in the production of cobalt, a by-product of copper and nickel mining, is foreseen once demand for the metal more than doubles when EVs account for 15% of the world’s car sales.

“Cobalt 27, which owns the world’s largest private stockpile of physical cobalt,

is positioned to take advantage of the early stages of the battery

metals upcycle, where large- scale base metals producers are actively

seeking to leverage by-product metals, such as cobalt, to fund mine expansion and repay debt using alternative, nondilutive sources of capital,†he tells Mining Weekly.

Officially, 105 000 t of cobalt is supplied globally, but Milewski says the unofficial figure is closer to between 115 000 t and 125 000 t of cobalt. This discrepancy, he says, is due to production being skewed by supply from undocumented artisanal mining in the Democratic Republic of Congo (DRC), where as much as 70% to 75% of the world’s cobalt is produced.

“With 98% of global cobalt supply a relatively small by-product of nickel and coppermining, one of Cobalt 27’s core principles is to invest in geopolitically stable jurisdictions outside the DRC. We believe the primary issue facing cobalt supply is the major concentration of cobalt reserves and production in the DRC, and the underlying human rights, environmental issues and political uncertainty associated with the country,†he adds.

The ethical sourcing of cobalt from the DRC continues to challenge the sector’s supply chain,

with Milewski highlighting the significant challenges faced by industry

participants in their attempts to promote the adoption of solutions that may be highly impractical in terms of the DRCbusinessenvironment. Although, he adds, not all artisanal mining is bad, addressing the operations that are unethical will take years and large amounts of money.

A second challenge artisanal mining poses to the growth of the EV market involves the environmentally unfriendly mining methods practised, contradicting the intentions of early EV adopters: people concerned about the environment. However, other metals, such as lithium, whose mining process is highly reliant on water, also face challenges. “Each commodity has its own set of particular challenges,†adds Milewski.

Supply and Demand

As the electrification story unfolds, in 2025 and beyond, this sector could account for between 13% and 15% of the current copper market. “This is a massive demand, relative to the size of the copper market. Electrification is the much bigger story, as batteries will make energy

much more accessible, but the type of battery used is dependent on the

application and metals available to specific countries,†notes Milewski.

Market research specialist BMI Research last year forecast global copper

output to climb from 23.4-million tonnes in 2018 to 29.9-million tonnes

by 2027, averaging yearly growth of 2.7%. The global refined copper balance was also forecast to register a deficit of 251 000 t in 2018 and remain undersupplied through 2023.

In terms of nickel, BMI Research expects global yearly production to

reach 2.9-million tonnes by 2027, according to its ‘Strategic Metals and

Rare Earths Market Outlook – Q32018’ report.

Milewski says the size of the copper and nickel markets will continue to dwarf that of cobalt, predicting greater focus on investment and development around these metals.

However, he sees a lag in satisfying the need for these “future metals†and building the mines required to fulfil that need.

The issue is not whether there are enough of these metals in the

ground, but whether funding is being made available to miners for the

development of the operations necessary to meet future demand. Other than diversified miner Rio Tinto or Australian mining giant BHP, “I can’t think of any other mining company that has developed a mine recently for over $2-billionâ€, states Milewski.

Noting that capital markets are generally efficient, he says directors can make their miningprojects

look as attractive as possible, but “if the markets are closed, they

are closedâ€. Higher commodity prices could, however, spur investment in

the cobalt, copper, lithium and nickel markets, Milewski adds.

Sadly, with two-thirds of the world’s cobalt originating from coppermining in the DRC, where cobalt was declared a strategic metal last year, a supply surge from the country has resulted in a price slump. Subsequently, some major miners, such as Glencore, have implemented cost-cutting procedures to compensate for the two-year low. At its Mutanda mine, Glencore has retrenched workers and decided against renewing contracts with external contractors.

The suspension at ERG’s Boss Mining comes at a time of strained relations between the DRC and investors after the nation last year introduced a 10% levy on cobalt exports, owing to cobalt’s strategic metal status.

Future metals have the attention of investors, as they primarily impact the low-carbon future and awareness is growing among mining companies of the benefit of aligning with the delivery of a low-carbon emissions future, with Glencore, for example, over the last year having adjusted its marketing message, says Milewski.

“Where mining companies are able to raise money presently is in this space,†he explains, adding that Rio Tinto is also looking into low-carbon-emission-metals- related projects.

Copper, cobalt,

lithium and nickel are the core metals that will be impacted on by the

pursuit of the world’s low-carbon-emissions future and whether other

metals will join the story, only time will tell. Besides these

mainstream metals, Milewski highlights interest in graphene, vanadium

and certain zinc chemistries. “These metals are sitting on the sidelines

and only time will tell if the technology will develop to grow their demand,†he concludes.

The company based its prediction on the uptake of EVs locally

matching the global average, which it says will account for up to 11% of

all new-car sales in 2025.

“Actual EV car sales have far outpaced expectations and are going to have a tremendous impact on the demand for materials such as copper, cobalt, lithium and nickel,†says Milewski. Having recently spoken at the Investing in African MiningIndaba conference, which was held at the Cape Town International Convention Centre, in South Africa’s Western Cape, from February 4 to 7, Milewski highlights that most conversations at the event were around these metals.

Posted by AGORACOM-JC

at 4:54 PM on Thursday, February 28th, 2019

NOTICE: Iconic Minerals – Fox Business Network – Thursday, February 28, 2019

The Company would like to give notice to its shareholders that the Company’s CEO (Richard Kern) will be featured on national Fox Business Network on Thursday, February 28, 2019 at 9:46 PM Eastern, 8:46 PM Central, 7:46 PM Mountain and 6:46 PM Pacific Time.

In this five minute segment, Richard Kern will be providing comments on

the lithium industry while onsite in Nevada, at the Bonnie Claire

property.

Please keep in mind that the allotted time slot may not be exact, and

the segment could air within an hour of the above scheduled times.

Posted by AGORACOM-JC

at 4:27 PM on Thursday, February 28th, 2019

(TSXV: ICM) (OTC Pink: BVTEF) (FSE: YQGB)

Why Iconic Minerals?

Bonnie Claire Lithium property hosts 11.8 Billion pounds of lithium carbonate equivalent (28.5 Million tonnes of LCE) Inferred Resource (43-101).

Potential to be the largest lithium resource globally (based on size)

Initial leaching tests applying dilute acid to the drill cuttings resulted in recoveries as high as 98%.

Two other highly prospective Lithium exploration properties also located in Nevada.

Lithium Projects

Iconic Minerals has three highly prospective Lithium exploration

properties located in Nevada, the Bonnie Claire Sarcobatus Valley

Lithium property, the Smith Valley Creek Property, and the Third Nevada

Lithium Property.

Bonnie Claire Property

Property Overview

11.8 Billion pounds of lithium carbonate equivalent (28.5 Million tonnes of LCE) Inferred Resource (43-101).

Potential to be the largest lithium resource globally (based on size)

Bonnie

Claire is a 100% owned lithium brine property comprising of 23,100

acres of contiguous placer claims, currently in control of 28.75 square

miles (75 km2) located in Nye County, Nevada.

Property

area is contained within a valley that is 60kms from the only producing

lithium mine in North America (Albermarle Silver Peak Mine).

Over +20 miles (+30 km) long and 12 miles (20 km) wide into which streams from an +800 mi2 (2,070 km2) drainage basin empty.

Sampling of salt flats within the basin, have found lithium values in salt samples yielding up to 340 ppm.

Current

claim block covers the gravity low and associated mud flats that could

be used for evaporation ponds if significant lithium brines are

discovered in drilling.

Preliminary NI 43-101 Technical Report completed Read More

A total 5,550 feet has been drilled at the Bonnie Claire with an average 963+ppm from four drill holes

Great infrastructure

Local end-users

Property Details Snapshot

Drainage Basin (20 x 30 kms)

830 square miles

Gravity Lows (length)

20 x 30 kms

Valley Sediment (Range)

460 – 610m (1,500 to 2,000ft)

BLM Drilling Permits

Drilling Program

Drilling completion of first of three test wells

Smith Creek Valley Property

Controls 808 placer claims totaling 25.25 square miles (65.4 km2) over a major gravity low.

The enclosed Smith Creek Valley Basin covers 582 square miles (1,507

km2), which is slightly larger than Clayton Valley Basin where lithium

brines are produced.

Smith Creek Valley is over +40 miles (+64 km) long in a north-northeast direction and averages 9 miles (14.5 km) in width.

The vast majority of rock weathering into the basin is felsic ash flow tuff, which is an excellent source of lithium.

Lithium Brine Benefits

Lower Cost Exploration

Easy access because flat and arid

Decreased environmental impact

Shorter Timeline to Production

Requires Less Capital

Lower Cost Production than bedrock

Found beneath salt flats in brine bearing aquifers

Easily pumped to Surface from vertical production well

After evaporation lithium recovered in small on site mill

Potassium may also be recovered

Nevada is a Geopolitically Stable Jurisdiction

Gold Projects

The company’s Gold exploration portfolio includes the Hercules

property in the Como mining district, 17 kms from the famous Comstock

Lode mine, the New Pass property in the New Pass mining district, and

the Squaw Creek property located in the northern area of the Carlin

Trend.

Situated within and on the margins of the Como mining district, located in Lyon County, Nevada.

Como district was worked as early as the late 1850s, before the

famous Comstock Lode deposit was discovered about 10 miles (16 km.) to

the north by prospectors following float upstream from placer gold

deposits at Dayton.

By the early 1860’s the Como district was abandoned due to the rich

lodes having been discovered at Virginia City (Russell, 1981).

In the late 1880’s the Hercules Mining Company explored the occurred

with the excavation of another 1,500 feet (450 m) of underground

workings.

Gold and silver property which, is comprised of 107 unpatented lode mining claims (2,231 acres).

The property is located in eastern Churchill County, Nevada; in the

New Pass Mining District, 27 miles west of Austin, Nevada and 105 miles

east of Reno.

Iconic Minerals has a controlling interest in the property, in a

joint venture with White Knight Gold U.S. Inc., (now U.S. Gold), with

Iconic earning a 50% interest.

Property

is located 42 miles due north of Battle Mountain, Nevada and lies

between the Midas and Ivanhoe mining districts on the northern portion

of the Carlin Trend, six miles north of the Dee Mine in the Lower Plate

Bootstrap Window.

Iconic’s Research and Development partner

St-Georges’

metallurgists report that they have successfully improved the

concentration of lithium in the Sediments, originally reported in

December using mechanical separation and selective leaching of other

elements within the Sediments.

The

additional tests St-Georges completed in Stage 2, through selective

leaching methods, have improved the elimination of barren material from

55% to 85%-88%, while retaining 100% of the lithium.

Upon

completion approximately 12% to 15% of the original material remains

for further processing and purification. This process may significantly

reduce the cost of production.

Posted by AGORACOM-JC

at 1:31 PM on Thursday, January 3rd, 2019

SPONSOR: New Age Metals Inc. (TSX-V: NAM) The company’s new Lithium Division has already made significant acquisitions in Canada and the USA. The company also owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. Learn More.

———————–

Blackwater founder launches fund to invest in electric car battery metals

Blackwater founder Erik Prince aims to raise as much as $500 million to invest in metals needed for making the batteries that power electric vehicles (EVs), the Financial Times reports.

Fund will focus mainly on cobalt, copper and lithium assets

Erik Prince, the founder of controversial U.S. private security firm Blackwater and an informal campaign adviser to President Donald Trump, is looking to raise as much as $500m to invest in metals used in the batteries that power electric cars. (Image courtesy of Miller Center | Flickr.)

Blackwater founder Erik Prince aims to raise as much as $500 million

to invest in metals needed for making the batteries that power electric

vehicles (EVs), the Financial Times reports.

Prince, who besides starting the controversial private security

company is known for have been an informal campaign adviser to US

President Donald Trump, said the fund will bring unexplored deposits

into production and then sell them to large miners after four to five

years.

The fund will focus mainly on cobalt, copper and lithium assets located mainly in Africa and Asia, Prince told FT.com.

“For all the talk of our virtual world, the innovation, you can’t

build these vehicles without minerals that come from generally weird,

hard-to-access places,†he said.

Metals such as cobalt, lithium, nickel and copper have seen demand soar in recent years as the shift away from

cars powered by fossil fuels gains momentum and mining companies are

investing billions of dollars into developing deposits of those key

commodities.

Experts expect the need for the commodity from battery makers alone to jump 650% by 2027, while overall demand is forecast to rise more than threefold in the next nine years.

Prices, however, are projected to drop in the early 2020s as a result

of an ever-rising number of projects expected to come online.

Prince sold Blackwater in 2010, after it was hit with a series of

lawsuits. Since then, he’s been running Frontier Services Group, which

provides integrated security, logistics and insurance services in

frontier markets and is backed by Hong Kong investor Chun Shun Ko and

China’s CITIC Group.

Frontier has also invested in a bauxite mine in Guinea, and identified a copper and cobalt deposit in the Congo.

Prince’s sister Elisabeth Dee DeVos is Trump’s education secretary.

Posted by AGORACOM-JC

at 11:19 AM on Wednesday, December 12th, 2018

SPONSOR: New Age Metals Inc. (TSX-V: NAM) The company’s new Lithium Division has already made significant acquisitions in Canada and the USA. The company also owns one of North America’s largest primary platinum group metals deposit in Sudbury, Canada. The property hosts M+I 4,626,250 Palladium Equivalent Ounces. Click here for more information.

——————–

Brazilian pre-operational miner Sigma Lithium Resources expects the premium for high-quality lithium hydroxide monohydrate that goes into battery production to rise in the next few years while demand for electric vehicles (EVs) grows, vice-chairman Ana Cabral told Fastmarkets.

“We believe prices for technical grade lithium hydroxide, at 56.5%, will fall further from now on, but premium for 90% content and beyond are set to increase as the material starts going into EV battery output,†she said.

By: Renata Rostas

Brazilian pre-operational miner Sigma Lithium Resources expects the

premium for high-quality lithium hydroxide monohydrate that goes into

battery production to rise in the next few years while demand for

electric vehicles (EVs) grows, vice-chairman Ana Cabral told

Fastmarkets.

“We believe prices for technical grade lithium hydroxide, at 56.5%,

will fall further from now on, but premium for 90% content and beyond

are set to increase as the material starts going into EV battery

output,†she said.

Fastmarkets assessed spot 56.5% lithium hydroxide prices in China

at 105,000-115,000 yuan ($15,209-16,658) per tonne on December 6,

unchanged from a week before but lower than this year’s peak of

148,000-153,000 yuan per tonne on January 11.

“Battery makers are increasingly looking for low-impurity, high-content

lithium, and being able to deliver this product right now is key in our

industry,†Cabral said. “We aim to produce refined material with high

grades, and you can count on your fingers how many companies, mostly in

Australia, do that.â€

Sigma Lithium owns a spodumene pegmatite

mine in Brazil’s Vale do Jequitinhonha, a region in the southeastern

state of Minas Gerais whose GDP per capita ranks as the 121st lowest out

of 137 meso-regions.

The company aims to start industrial

operations in the fourth quarter of 2019 and produce 240,000 tonnes per

year of spodumene concentrates (6-8% lithium oxide) by 2020, in “phase

2†of the plant.

A pilot 12,000-tpy capacity, or phase 1, is

currently in place, meant for product approvals from clients while the

miner finishes a feasibility study for the project. The study is

scheduled to be finished by February 2019, Cabral said.

Japanese trader Mitsui has agreed to buy a third of initial commercial

output in the second phase of operations, for $30 million, with an

option to maintain its 33% proportion at a possible phase 3. A

pre-payment will be done as soon as the feasibility study is ready,

allowing the company to finance the start-up.

“We have

continued discussing other offtake and similar agreements,†Cabral said.

“There are more traders that wish to secure their supply, but we want

to close deals with different types of companies and geographies, to

diversify our portfolio.â€

Posted by AGORACOM-JC

at 9:37 AM on Tuesday, November 13th, 2018

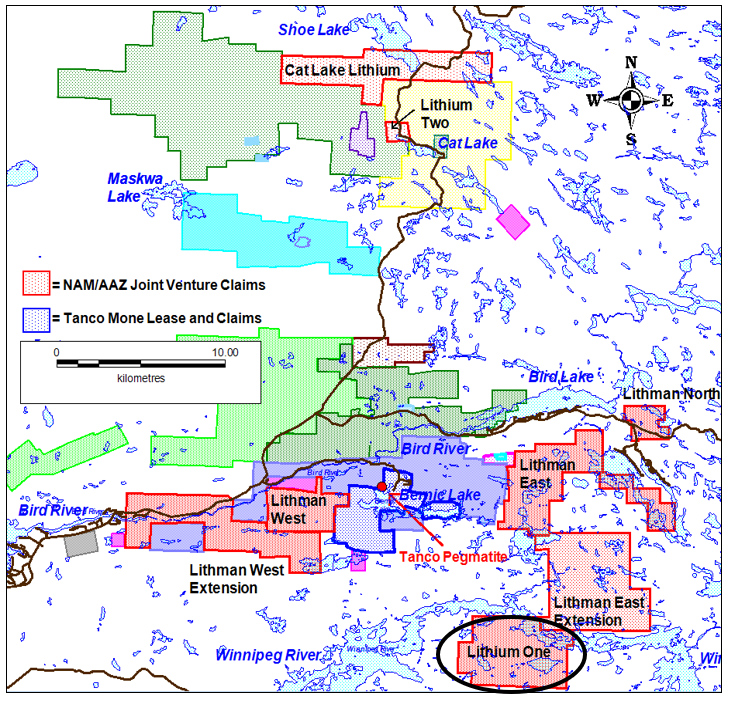

New Age Metals has an Option/Joint-Venture agreement with partner Azincourt Energy Corp (AAZ) on its eight pegmatite hosted Lithium Projects in the Winnipeg River Pegmatite Field, located in SE Manitoba- Exploration in southeast Manitoba is focused on Lithium-bearing pegmatites and other rare metals.- Rubidium Oxide is a highly insoluble thermally stable Rubidium source suitable for glass, optic and ceramic applications. Rubidium is recovered commercially from Lepidolite as a by-product of lithium extraction.

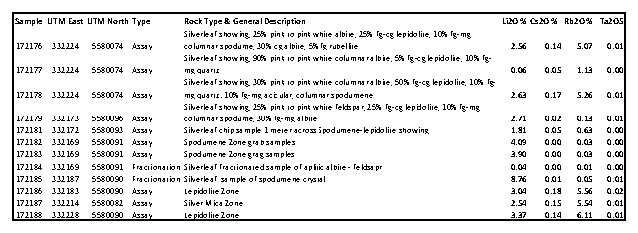

Mapping and sampling at the Silverleaf Pegmatite on the Lithium One Project returned numerous samples of strong lithium mineralization with assays up to 4.1% Li2O and Rubidium up to 6.1% Rb2O on the Silverleaf Pegmatite.

Drill permits have been applied for on the Lithium Two and Lithium One Projects and the company is awaiting approval from the province

The company recently signed an Exploration Agreement with the Sagkeeng First Nation, see news release dated October 25, 2018.

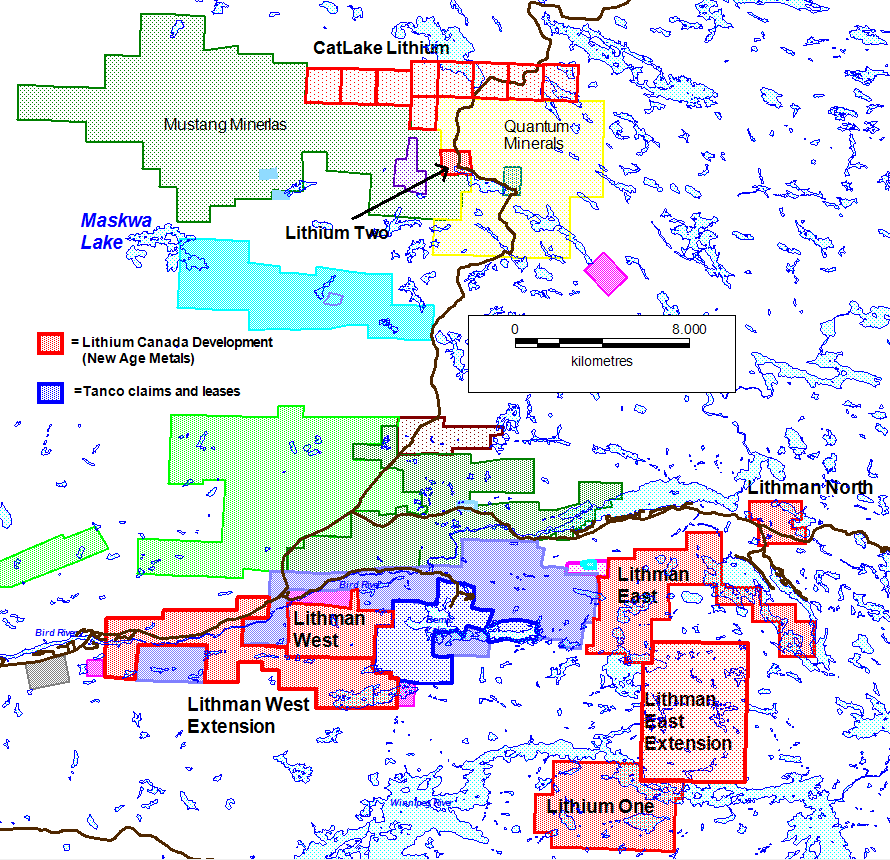

November 13th, 2018 / Rockport, Canada – New Age Metals Inc. (NAM) (TSX.V: NAM; OTCQB: NMTLF; FSE: P7J.F) New Age Metals is pleased to provide an update on the current surface exploration program on the company’s Lithium One Project. The company’s Lithium Division, Lithium Canada Development, has an aggressive exploration program for 2018. The Joint Venture with New Age Metals and Azincourt Energy, has eight Lithium Projects in the Winnipeg River Pegmatite Field, located in SE Manitoba (Figure 1).

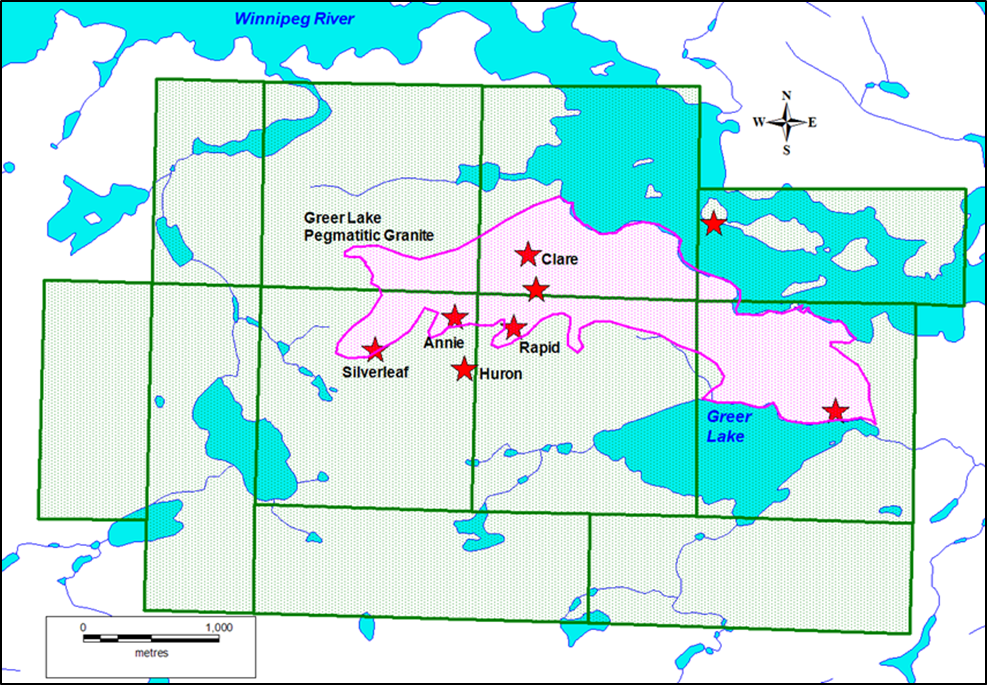

Lithium One Project

A field crew was active in the late summer and early fall exploring on the Lithium One Project. The reported results are from the Silverleaf Pegmatite (Figure 2). The Annie and other pegmatites from the Lithium One Project have been assayed and assay results are pending.

The Lithium One Project is located 125 kilometres northeast of Winnipeg, Manitoba and is geologically characterized as being a part of the Cat Lake-Winnipeg River Pegmatite Field.

Click Image To View Full Size

Figure 1: Claim Map of the Bird River Area Showing the Joint Venture Project Locations

This Pegmatite Field is host to the world-class Tanco Pegmatite, which has been mined since 1969 for Tantalum, Cesium, and Spodumene (a Lithium bearing ore). Historically the Lithium One Project area is known for the presence of numerous surface Pegmatites of various dimensions and compositions (see Figure 3).

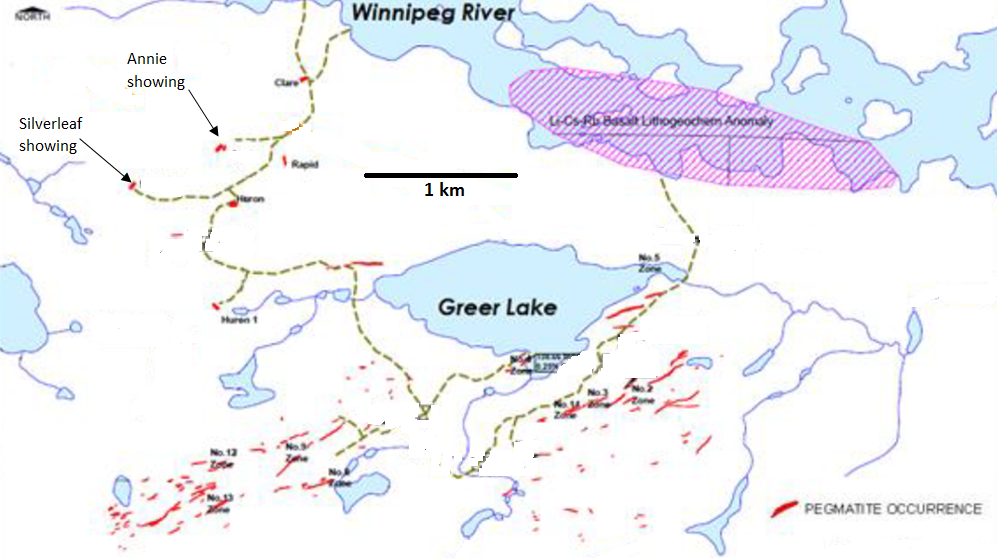

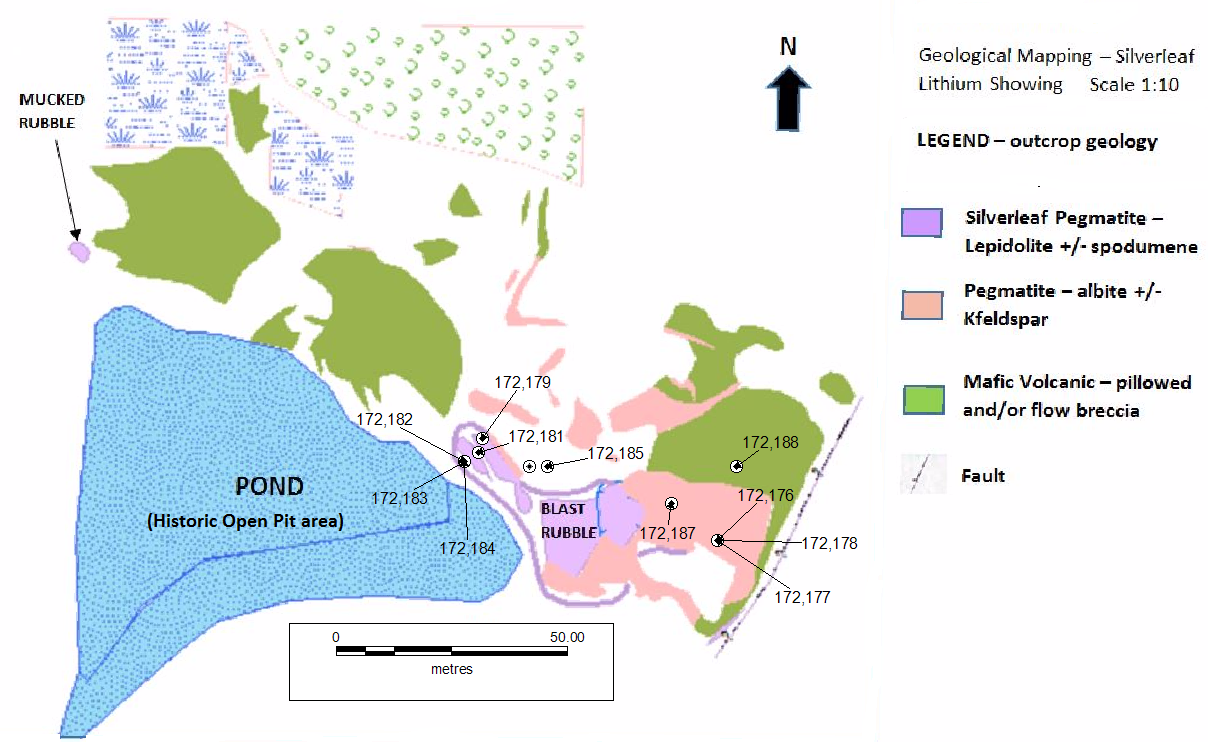

The Silverleaf Pegmatite (Figure 4) is a zoned complex Lithium-bearing Pegmatite with a surface exposure of approximately 80 metres x 45 metres. The Pegmatite is exposed in the northeast and strikes under cover to the southwest. Samples taken from the Lepidolite-Spodumene Zone yielded assays from 1.81% to 4.09% Li2O and 0.63% to 6.11% Rb2O.

This zone is approximately 50 metres x 20 metres in size and extends into a historic excavated open pit. The historic open pit area originates from the late 1920s, when a bulk sample of Spodumene was mined from the southwest side of the Silverleaf Pegmatite. Large scale mining operations were not undertaken at that time. The area has seen sporadic exploration activity with focus on base metals and tantalum with minor exploration for Lithium.

In an effort to check the purity of the Spodumene, a sample of Spodumene blades was sampled from the Silverleaf Pegmatite. This sample yielded an assay of 8.76 % Li2O. A review of Spodumene mineral data at the Webmineral website indicates that Spodumene crystal can

(https://webmineral.com/data/Spodumene.shtml#.W-ShltVKipo) have a Lithium content from 3.73 to 8.03% Li2O. This would tend to indicate that the Spodumene crystals present at the Silverleaf Pegmatite are of a very high Lithium content.

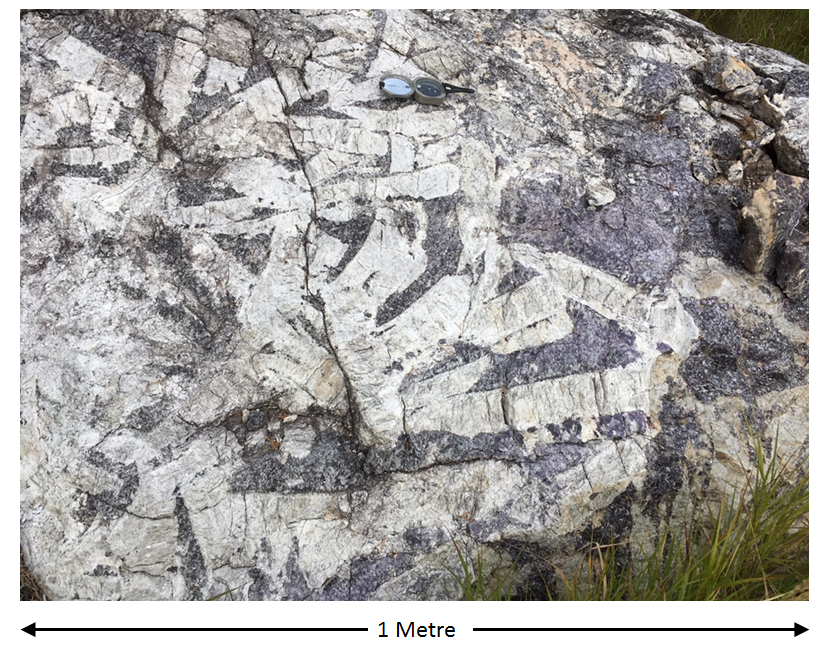

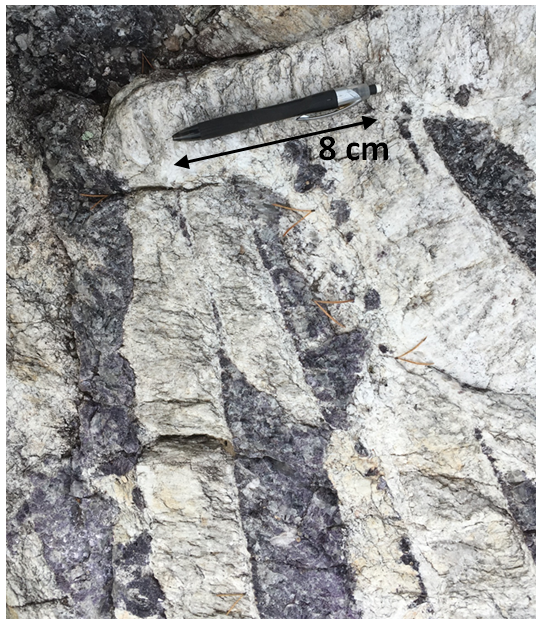

The Spodumene blades at the surface of the Silverleaf Pegmatite can reach a length of up to 40 centimeters and a width of 10 centimeters (see Figure 5 and 6). The Spodumene blades are surrounded by Lithium bearing purple micas (Lepidolite).

Click Image To View Full Size

Figure 3: Pegmatite map of the Lithium One Project

Table 1: 2018 Samples from the Silverleaf Pegmatite

Click Image To View Full Size

Click Image To View Full Size

Figure 4: Geological mapping of the Silverleaf Pegmatite, Lithium One Project

In geological terms, the Silverleaf Pegmatites encountered on the Lithium One Project is a LCT Type (Lithium-Cesium-Tantalum) Pegmatites

QA/QC Protocol

All samples were analyzed at the Activation Laboratories facility, in Ancaster, Ontario. Samples were prepared, using the lab’s Code RX1 procedure. Samples are crushed, up to 95% passing through a 10 mesh, riffle split, and then pulverized, with mild steel, to 95%, passing 105 ?m. Analyses were completed, using the lab’s Ultratrace 7 Package; a Sodium Peroxide Fusion which allows for total metal recovery and is effective for analysis of Sulphides and refractory minerals. Assay analyses are carried out, using ICP-OES and ICP-MS instrumentation. New Age Metals implemented a QA/QC field program with insertion of blanks at regular intervals. Activation Laboratories has their own internal QA/QC procedures that it carries out for all sample batches.

In January of 2018, NAM announced a signed final agreement with Azincourt Energy Corp. (TSX.V: AAZ) for the Manitoba Lithium Projects. (News Release: January 15th, 2018) This Pegmatite Field hosts the world class Tanco Pegmatite that has been mined for Tantalum, Cesium and Spodumene (one of the primary Lithium ore minerals) in varying capacities, since 1969. NAM’s Lithium Projects are strategically situated in this prolific Pegmatite Field. Presently, NAM, under its subsidiary Lithium Canada Developments, is one of the largest mineral claim holders in the Winnipeg River Pegmatite Field for Lithium. Azincourt Energy Corp. as our option/joint venture is financed for and has committed to a minimum of $600,000 to be expended on exploration in Manitoba for 2018. See news release dated Janurary 15, 2018.

OPT-IN LIST

If you have not done so already, we encourage you to sign up on our website (www.newagemetals.com) to receive our updated news.

ABOUT NAM’S PGM DIVISION

NAM’s flagship project is its 100% owned River Valley PGM Project (NAM Website – River Valley Project) in the Sudbury Mining District of Northern Ontario (100 km east of Sudbury, Ontario). See results from the most recent NI 43-101 resource update below in Table 1. NAM management and consultants are currently designing a complete drill program to be executed in 2019 for the River Valley Project. This plan will consider previously proposed drill parameters and will be based on the most recent geophysical assessment and consultant expertise. The projects first economic study, a Preliminary Economic Assessment (PEA) is underway and is being overseen by Mr. Michael Neumann, P.Eng., a veteran mining engineer and one of NAM’s directors. See the most recent press releases for the River Valley Project PEA which detail the appointment of P&E Mining Consultants and DRA Americas to jointly conduct the study, dated July 25, 2018 and August 1, 2018 respectively. Our new Fall Chairman’s message can be accessed at our website (www.newagemetals.com) .

On April 4th, 2018, NAM signed an agreement with one of Alaska’s top geological consulting companies. The companies stated objective is to acquire additional PGM and Rare Metal projects in Alaska. On April 18th, 2018, NAM announced the right to purchase 100% of the Genesis PGM Project, NAM’s first Alaskan PGM acquisition related to the April 4th agreement. The Genesis PGM Project is a road accessible, under explored, highly prospective, multi-prospect drill ready Palladium (Pd)- Platinum (Pt)- Nickel (Ni)- Copper (Cu) property. A comprehensive report on previous exploration and future phases of work was completed by Avalon Development of Fairbanks Alaska in August 2018 on Genesis. A full sampling program will be conducted to continue to outline additional mineralization along the 800-meter by 40-meter mineralized zone

On August 29, the Avalon report was submitted to NAM, management is actively seeking an option/joint-venture partner for this road accessible PGM and Multiple Element Project using the Prospector Generator business model.

The results of the updated Mineral Resource Estimate for NAM’s flagship River Valley PGM Project are tabulated in Table 1 below (0.4 g/t PdEq cut-off).

Class

Tonnes

‘,000

Pd (g/t)

Pt (g/t)

Rh (g/t)

Au (g/t)

Cu (%)

Ni (%)

Co (%)

PdEq (g/t)

Measured

62,877.5

0.49

0.19

0.02

0.03

0.05

0.01

0.002

0.99

Indicated

97,855.2

0.40

0.16

0.02

0.03

0.05

0.01

0.002

0.83

Meas +Ind

160,732.7

0.44

0.17

0.02

0.03

0.05

0.01

0.002

0.90

Inferred

127,662.0

0.27

0.12

0.01

0.02

0.05

0.02

0.002

0.66

Class

PGM + Au (oz)

PdEq (oz)

PtEq (oz)

AuEq (oz)

Measured

1,440,200

1,999,600

1,999,600

1,136,900

Indicated

1,856,900

2,626,700

2,626,700

1,463,800

Meas +Ind

3,297,200

4,626,300

4,626,300

2,600,700

Inferred

1,578,400

2,713,900

2,713,900

1,323,800

Notes:

A.CIM definition standards were followed for the resource estimation.

B.The 2018 Mineral Resource models used Ordinary Kriging grade estimation within a three-dimensional block model with mineralized zones defined by wireframed solids.

C.A base cut-off grade of 0.4 g/t PdEq was used for reporting Mineral Resources.

F.Mineral Resources that are not Mineral Reserves do not have economic viability.

G. The Inferred Mineral Resource in this estimate has a lower level of confidence that that applied to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of the Inferred Mineral Resource could be upgraded to an Indicated Mineral Resource with continued exploration.

QUALIFIED PERSON

The contents contained herein that relate to Exploration Results or Mineral Resources is based on information compiled, reviewed or prepared by Carey Galeschuk, a consulting geoscientist for New Age Metals. Mr. Galeschuk is the Qualified Person as defined by National Instrument 43-101 and has reviewed and approved the technical content of this news release.

On behalf of the Board of Directors

“Harry Barr”

Harry G. Barr

Chairman and CEO

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Cautionary Note Regarding Forward Looking Statements: This release contains forward-looking statements that involve risks and uncertainties. These statements may differ materially from actual future events or results and are based on current expectations or beliefs. For this purpose, statements of historical fact may be deemed to be forward-looking statements. In addition, forward-looking statements include statements in which the Company uses words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”, “confident”, “intend”, “strategy”, “plan”, “will”, “estimate”, “project”, “goal”, “target”, “prospects”, “optimistic” or similar expressions. These statements by their nature involve risks and uncertainties, and actual results may differ materially depending on a variety of important factors, including, among others, the Company’s ability and continuation of efforts to timely and completely make available adequate current public information, additional or different regulatory and legal requirements and restrictions that may be imposed, and other factors as may be discussed in the documents filed by the Company on SEDAR (www.sedar.com), including the most recent reports that identify important risk factors that could cause actual results to differ from those contained in the forward-looking statements. The Company does not undertake any obligation to review or confirm analysts’ expectations or estimates or to release publicly any revisions to any forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. Investors should not place undue reliance on forward-looking statements.

Posted by AGORACOM-JC

at 12:01 PM on Thursday, June 28th, 2018

Outlook for lithium continues to shine, with demand from companies that produce batteries to power electric cars, laptops and other high-tech devices, expected to increase 650% by 2027

Overall lithium demand forecast to rise more than threefold over that period, a new study shows

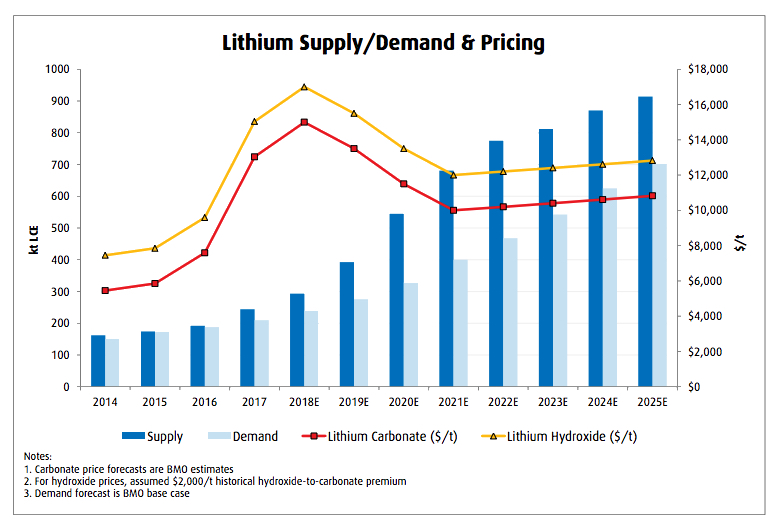

The outlook for lithium continues to shine, with demand from companies that produce batteries to power electric cars, laptops and other high-tech devices, expected to increase 650% by 2027, with overall lithium demand forecast to rise more than threefold over that period, a new study shows.

While the next nine years will drain less than 1% of the reserves in the ground, battery makers will need more lithium to support their production, which will boost demand for the key metal almost 16% to reach 1 million tonnes, according to Roskill’s 15th edition market outlook report.

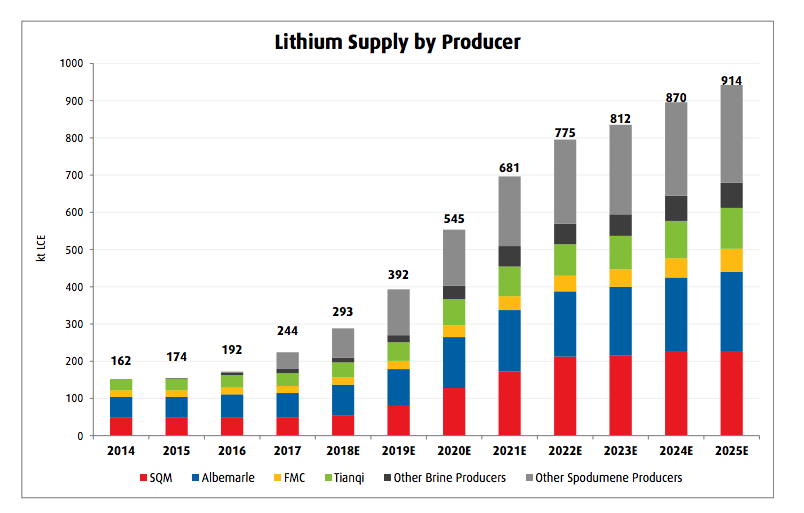

Expected supply, however, is far from the astronomical figure forecast by the research firm, with Canada’s Bank of Montreal expecting between 80,000 and 91,500 tonnes of lithium coming from mines by 2025. And BMO’s numbers include recently up-sized expansion plans by the market leaders, Chile’s SQM, China’s Tianqi Lithium, Albemarle and FMC, as well as Nemaska Lithium’s plans to build a spodumene mine in northwestern Quebec, Canada.

Wave of much-needed spodumene based supply coming online. (Source: BMO Capital Markets, companies reports.)

Roskill estimates that demand from lithium-ion battery manufacturers will grow from 46% last year to 83% by 2027. Use of lithium hydroxide, in turn, is also forecast to become more prevalent, increasing from 25% of lithium compounds used in rechargeable batteries in 2021 to 55% by 2027.

The analysts expect the market for battery-grade lithium compounds to remain tight, however, as installing new battery grade capacity has proven complex and forecast demand growth is greatest for these products.

In terms of lithium prices, they are expected to peak in 2018, as greater supply availability of mined and refined lithium will enter the market in coming years, causing prices to briefly fall back in 2019, with a floor of $11,000/t battery grade lithium carbonate, Roskill says.

Beyond 2021, the research firm expects lithium prices to rise  above 2018 levels again, as continued demand growth for battery grade lithium compounds will apply greater demand-side pressure on prices.

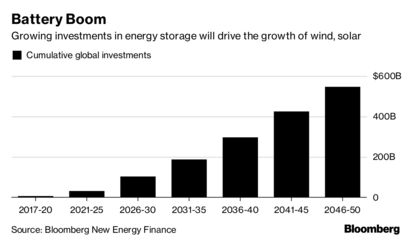

(Bloomberg) — Batteries will attract $548 billion in investments by 2050 as costs fall and homes and businesses push to use more clean energy.

That’s one of the conclusions of the New Energy Outlook released Tuesday by analysts at Bloomberg New Energy Finance. Batteries will become increasingly viable on the grid as demand for electric cars spurs manufacturing of lithium-ion systems, driving down prices.

Batteries will allow more solar and wind to meet demand — even when the sun isn’t shining or wind isn’t blowing, helping end the era of fossil fuel dominance on the grid by mid-century, BNEF said. Battery prices are expected to fall to $70 a kilowatt-hour by 2030, down 67 percent from today, according to the report. BNEF expects 1,288 gigawatts of new batteries to be commissioned by 2050.

“It’s a matter of ‘when and how’ and not ‘if’ wind, solar and battery technologies will disrupt electricity delivery all over the world,†Seb Henbest, lead author the report, said in an interview.

Posted by AGORACOM-JC

at 9:52 AM on Wednesday, June 6th, 2018

Lithium Canada Development is the 100% owned subsidiary of New Age Metals (NAM) who presently has an agreement with Azincourt Energy Corporation (AAZ) whereby AAZ will now commit an additional $250,000 in exploration expenditures and issue NAM an additional 250,000 shares of AAZ. This increases AAZ’s initial 50% exploration expenditure earn in for AAZ from $2.6 million to $2.850 million. This acquisition will also increase the shares to be issued to NAM from 1.5 million to 1.75 million, and adds an additional 2% royalty for NAM, for a total of eight royalties on the Lithium Projects in this pegmatite field. For additional information on the NAM/AAZ option/joint-venture and recent acquisitions, see the news releases dated Jan 15, 2018, May 2, 2018,May 10, 2018.

The recent project acquisition has strengthened New Age Metal/Azincourt Joint Venture position as the largest claim holder in the Winnipeg River Pegmatite Field as they are now in possession of an approximate total of 14,100 hectares (34,800 acres). These Manitoba projects that have excellent infrastructure are located in a mining friendly jurisdiction. The Joint Venture now has eight projects in this large lithium-bearing pegmatite field.

Preliminary field work and additional ground proofing is currently in progress on the Lithium Two Project. The objective of this work is to finalize a drill plan and initiate a drill program, which is slated for Q3/Q4 2018. Management of both companies plan to update their shareholders and interested parties with a complete exploration plans for all eight projects before the end of June and as the summer/fall progresses. The minimum exploration budget for 2018 is $600,000.

Lithium has an ever increasing demand for batteries in electric cars cellphones, laptops, solar storage, wireless charging and renewable energy products.

NAM’s Platinum Group Metals (PGM) Division, more specifically our River Valley PGM project in Sudbury, Ontario, is the largest undeveloped primary platinum group metal project in North America, and management is advancing the project towards its first economic study, more specifically, a Preliminary Economic Assessment (PEA). See news releases dated May 8, 2018 and May 23, 2018.

June 6th, 2018 / Rockport, Canada – New Age Metals Inc. (TSX.V: NAM; OTCQB: NMTLF; FSE: P7J.F) is pleased to announce that its wholly owned subsidiary, Lithium Canada Developments (LCD), has acquired a 100% interest in the CATLAKE Lithium Project, by way of staking, in southeast Manitoba. The project has good infrastructure and is located in a region known for mining in the province.

The new CATLAKE Project consists of 9 claims for a total of an approximately 2000 hectares (4950acres) (Figure 1). It is located approximately 24 kilometers directly north of the Tanco Pegmatite. The world-class Tanco Pegmatite has been mined for Tantalum, Cesium and Spodumene (one of the primary Lithium ore minerals) in varying capacities, since 1969 at the Tanco Mine.

Click Image To View Full Size

Figure 1: CATLAKE Lithium Project Claim Outline

CATLAKE Lithium Project

The CATLAKE Lithium Project is located directly north of the Lithium Two Project. The Lithium Two Project contains several lithium bearing pegmatites with a historic non 43-101 compliant 1947 drilled resource on the Eagle Pegmatite of 545,000 tonnes of 1.4% Li2O to a depth of only 60 meters. Historical reports have suggested that the Eagle Pegmatite is open to depth and along strike. Preliminary field work and additional ground proofing is currently in progress on the Lithium Two Project. The objective of this work is to finalize a drill plan and initiate a drill program, which is slated for Q3/Q4 2018. Management of both companies plan to update their shareholders and interested parties with a complete exploration plans for all eight projects before the end of June and as the summer/fall progresses. The minimum exploration budget for 2018 is $600,000.

The new claims were staked to add to the company’s expanding lithium exploration portfolio and to have a larger presence in the CATLAKE area which has seen an increase in recent exploration activity. Companies such as Quantum Minerals, Mustang Minerals and Equitorial Exploration are also active in this promising new lithium and rare metals region. The new claims are situated north of Quantum Minerals recent claim acquisition. They are staked over portions of the greenstone belt at CATLAKE and along the trend that hosts the Irgon Pegmatite (Quantum Minerals), both which hosts lithium-bearing pegmatites. .

The pegmatites in this region of southeast Manitoba are described as being a part of the Winnipeg River Pegmatite Field. Several large lithium-bearing pegmatites exist in this historic area and exploration activity in the region is increasing. This pegmatite field is host to the world-class Tanco Pegmatite, which is a highly fractionated Lithium-Cesium-Tantalum (LCT Type) pegmatite and has been mined in varying capacities since 1969. The LCT-type pegmatites can contain large amounts of Spodumene (one of the primary ores used in hard rock lithium extraction) and are a primary geological target in hard rock lithium exploration. They also can contain economic qualities of tantalum and cesium as well as other lithium bearing minerals such as mica.

OPT-IN LIST

If you have not done so already, we encourage you to sign up on our website (www.newagemetals.com) to receive our updated news or click here.

ABOUT NAM’S PGM DIVISION

NAM’s flagship project is its 100% owned River Valley PGM Project (NAM Website – River Valley Project) in the Sudbury Mining District of Northern Ontario (100 km east of Sudbury, Ontario). Presently the River Valley Project is North America’s largest undeveloped primary PGM deposit with Measured + Indicated resources of 160 million tones @ 0.44 g/t Palladium, 0.17 g/t Platinum, 0.03 g/t Gold, with a total metal grade of 0.64 g/t at a cut-off grade of 0.4 g/t equating to 3,297,173 ounces PGM plus Gold and 4,626,250 PdEq Ounces (Table 1). This equates to 4,626,250 PdEq ounces M+I and 2,713,933 PdEq ounces in inferred (see May 8th, 2018 press release). Having completed a 2018 NI-43-101 resource update the company is finalizing its 2018 exploration programs which will include geophysics, and extensive drill programs, which are all working towards the completion of a Preliminary Economic Assessment (PEA). Our objective is to develop a series of open pits (bulk mining) over the 16 kilometers of mineralization, concentrate on site, and ship the concentrates to the long-established Sudbury Metallurgical Complex. On May 23rd, 2018, NAM’s board approved a Preliminary Economic Assessment (PEA) on River Valley Platinum Group Metals Project’s. This will be the first economic study on the project. Alaska: April 4th, 2018, NAM signed an agreement with one of Alaska’s top geological consulting companies. The companies stated objective is to acquire additional PGM and Rare Metal projects in Alaska. On April 18th, 2018, NAM announced the right to purchase 100% of the Genesis PGM Project, NAM’s first Alaskan PGM acquisition related to the April 4th agreement. The Genesis PGM Project is a road accessible, under explored, highly prospective, multi-prospect drill ready Pd-Pt-Ni-Cu property.

The results of the new resource estimation are tabulated in Table 1 below (0.4 PdEq cut-off).

Class

Tonnes

‘,000

Pd (g/t)

Pt (g/t)

Rh (g/t)

Au (g/t)

Cu (%)

Ni (%)

Co (%)

PdEq (g/t)

Total Measured

62,877.5

0.49

0.19

0.02

0.03

0.05

0.01

0.002

0.99

Total Indicated

97,855.2

0.40

0.16

0.02

0.03

0.05

0.01

0.002

0.83

Total Meas +Ind

160,732.7

0.44

0.17

0.02

0.03

0.05

0.01

0.002

0.90

Inferred

127,662.0

0.27

0.12

0.01

0.02

0.05

0.02

0.002

0.66

Class

PGM + Au (oz)

PdEq (oz)

PtEq (oz)

AuEq (oz)

Total Measured

1,440,248

1,999,575

1,999,575

1,136,930

Total Indicated

1,856,925

2,626,675

2,626,675

1,463,793

Total Meas +Ind

3,297,173

4,626,250

4,626,250

2,600,724

Inferred

1,578,367

2,713,933

2,713,933

1,323,809

Notes:

1. CIM definition standards were followed for the resource estimation.

2. The 2018 resource models used Ordinary Krig grade estimation within a three-dimensional block model with mineralized zones defined by wireframed solids.

3. A base cut-off grade of 0.4 % g/t PdEq was used for reporting resources.

6. Mineral Resources that are not mineral reserves do not have economic viability

7. The quantity and grade of reported inferred resources in this estimation are uncertain in nature and there has been insufficient exploration to define these inferred resources as an indicated or measured mineral resource and it is uncertain if further exploration will result in upgrading them to an indicated or measured mineral resource category.

ABOUT NAM’S LITHIUM DIVISION

The Company has seven pegmatite hosted Lithium Projects in the Winnipeg River Pegmatite Field, located in SE Manitoba, with focus on Lithium bearing pegmatites. Three of the projects are drill ready. This Pegmatite Field hosts the world class Tanco Pegmatite that has been mined for Tantalum, Cesium and Spodumene (one of the primary Lithium ore minerals) in varying capacities, since 1969. NAM’s Lithium Projects are strategically situated in this prolific Pegmatite Field. Presently, NAM is the largest mineral claim holders for Lithium in the Winnipeg River Pegmatite Field. Lithium Canada Development is the 100% owned subsidiary of New Age Metals (NAM) who presently has an agreement with Azincourt Energy Corporation (AAZ) whereby AAZ will now commit an additional $250,000 in exploration expenditures and issue NAM an additional 250,000 shares of AAZ. This increases AAZ’s initial 50% exploration expenditure earn in for AAZ from $2.6 million to $2.850 million. This acquisition will also increase the shares to be issued to NAM from 1.5 million to 1.75 million, and adds an additional 2% royalty for NAM, for a total of eight royalties on the Lithium Projects in this pegmatite field. For additional information on the NAM/AAZ option/joint-venture and recent acquisitions, see the news releases dated Jan 15, 2018, May 2, 2018, May 10, 2018.

QUALIFIED PERSON

The contents contained herein that relate to Exploration Results or Mineral Resources is based on information compiled, reviewed or prepared by Carey Galeschuk, a consulting geoscientist for New Age Metals. Mr. Galeschuk is the Qualified Person as defined by National Instrument 43-101 and has reviewed and approved the technical content of this news release.

On behalf of the Board of Directors

“Harry Barr”

Harry G. Barr

Chairman and CEO

ADDITIONAL INFORMATION

Should you have additional inquiries, please contact Paul Poggione, Corporate Development, Tel: 1-613-659-2773, email: [email protected].

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Cautionary Note Regarding Forward Looking Statements: This release contains forward-looking statements that involve risks and uncertainties. These statements may differ materially from actual future events or results and are based on current expectations or beliefs. For this purpose, statements of historical fact may be deemed to be forward-looking statements. In addition, forward-looking statements include statements in which the Company uses words such as “continue”, “efforts”, “expect”, “believe”, “anticipate”, “confident”, “intend”, “strategy”, “plan”, “will”, “estimate”, “project”, “goal”, “target”, “prospects”, “optimistic” or similar expressions. These statements by their nature involve risks and uncertainties, and actual results may differ materially depending on a variety of important factors, including, among others, the Company’s ability and continuation of efforts to timely and completely make available adequate current public information, additional or different regulatory and legal requirements and restrictions that may be imposed, and other factors as may be discussed in the documents filed by the Company on SEDAR (www.sedar.com), including the most recent reports that identify important risk factors that could cause actual results to differ from those contained in the forward-looking statements. The Company does not undertake any obligation to review or confirm analysts’ expectations or estimates or to release publicly any revisions to any forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events. Investors should not place undue reliance on forward-looking statements.

Wave of much-needed spodumene based supply coming online. (Source:

Wave of much-needed spodumene based supply coming online. (Source:  Source:

Source: