- 1.078 gpt AuEq over 345.0 Meters Within 921.0 Meters of 0.821 gpt AuEq (Hole GS-20-83) at the Goldstorm Zone, Treaty Creek, Located in B.C.’s Golden Triangle

Cardston, Alberta–(Newsfile Corp. – December 16, 2020) – American Creek Resources Ltd. (TSXV: AMK) (“the Corporation”) is pleased to present results for the fifth set of diamond drill holes for the Goldstorm Zone at their flagship property, Treaty Creek. The project is located in the heart of the Golden Triangle of northwestern British Columbia and is on-trend from Seabridge’s KSM Project located five kilometers southwest of the Goldstorm Zone. Results from 12 diamond drill holes have recently been received from MSA Labs with final results from another 11 diamond drill holes pending. All drill holes have successfully intersected the Goldstorm System, expanding and defining the mineralization along the northeast and southeast axes, as well as to depth. The Goldstorm System 300 Horizon has now been traced for 1100 meters along the northeast axis and, as well, the CS-600 and DS-5 zones have been expanded to the northeast and to depth. All 39 drill holes completed at Goldstorm during the 2020 program have encountered significant precious metal mineralization. The 2020 Treaty Creek Diamond Drill Program was completed last week, and field personnel have winterized the camp. The track-components of two track-mounted diamond drills remain on site ready for start-up of the 2021 exploration season.

Tudor Gold’s Vice President of Project Development, Ken Konkin, P.Geo., states: “We are very pleased with the results obtained from all 39 drill holes completed this year to-date and we anticipate the release of the final 11 holes of the year within a few weeks. This brings the total to 50 drill holes that were completed this year at the Goldstorm Zone. These latest holes continued to expand the limits of the mineralized targets along the northeastern and the southeastern axes, and to depth. For a fifth consecutive press release, we have surpassed our best result from last years’ drill hole program (0.697 AuEq over 1081.5 meters in hole GS-19-47) with drill holes GS-20-83 and GS-20-94 as described in the headline. The final 11 drill holes represent over 9600 meters of drilling and we expect that MSA Labs will complete the analysis of these final samples as soon as possible.”

Treaty Creek Highlights include:

- Twelve drill holes presented in this press release total 11,551.1 meters.

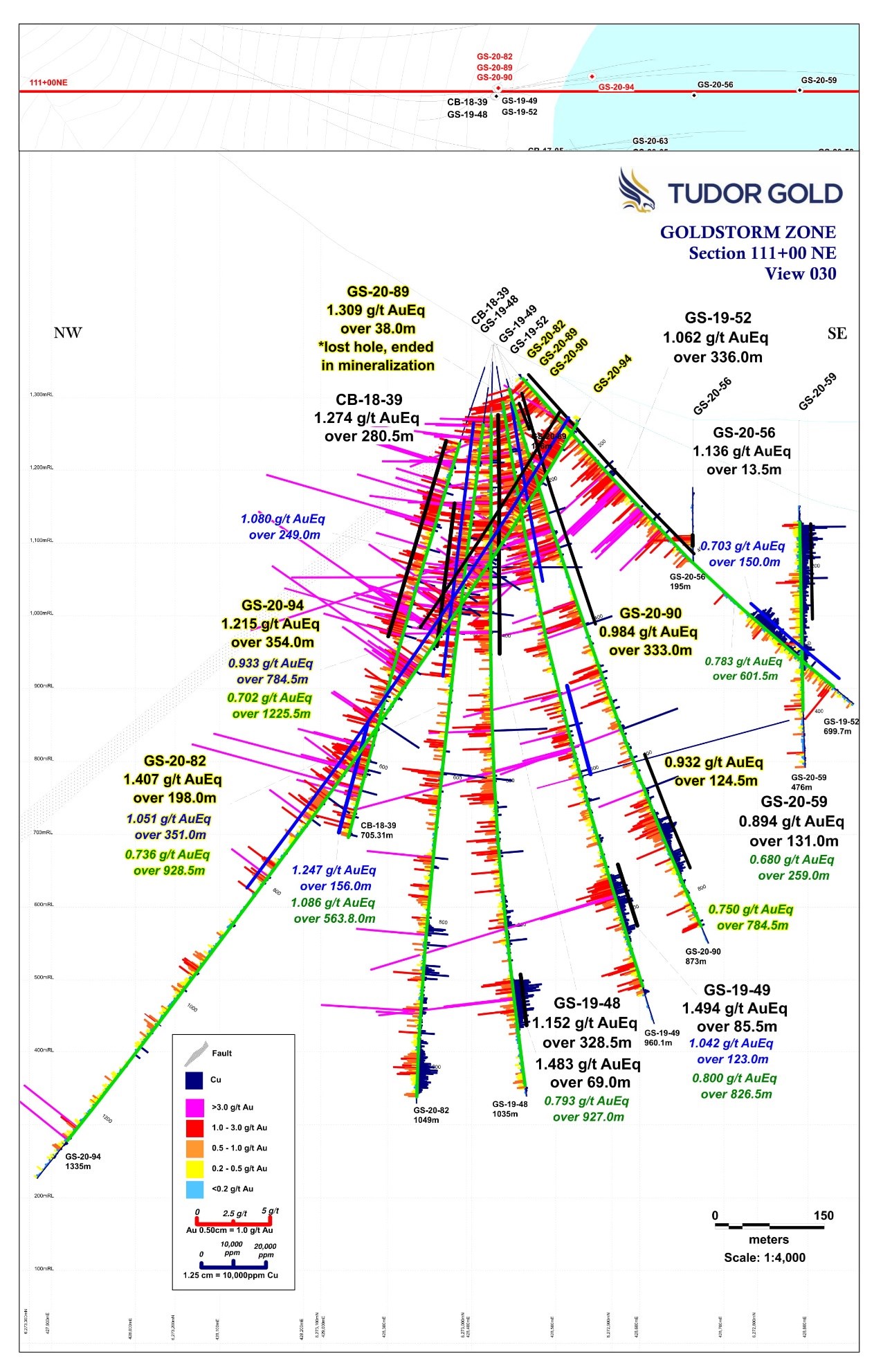

- The best results were from GS-20-94, a near-surface 354.0 meter intercept (36.0-390 m) averaging 1.215 gpt AuEq and GS-20-82 with a 351m intercept (113.0-464.0 m) averaging 1.051 gpt AuEq. Both holes are located on Section 111+00 NE.

- Equally impressive was drill hole GS-20-83 that also had a near-surface intercept over a similar 345.0 meters (73.5-418.5 m) that averaged 1.078 gpt AuEq on Section 112+50 NE.

- More Core Drilling did an excellent job completing 50 HQ/NQ2 diamond drill holes totaling 43,972 meters at Goldstorm and 1,636 meters at the Perfect Storm Target with three drill holes.

The following three tables below provide the complete list of composited drill hole results as well as the drill hole data including hole location, elevation, depth, dip and azimuth.

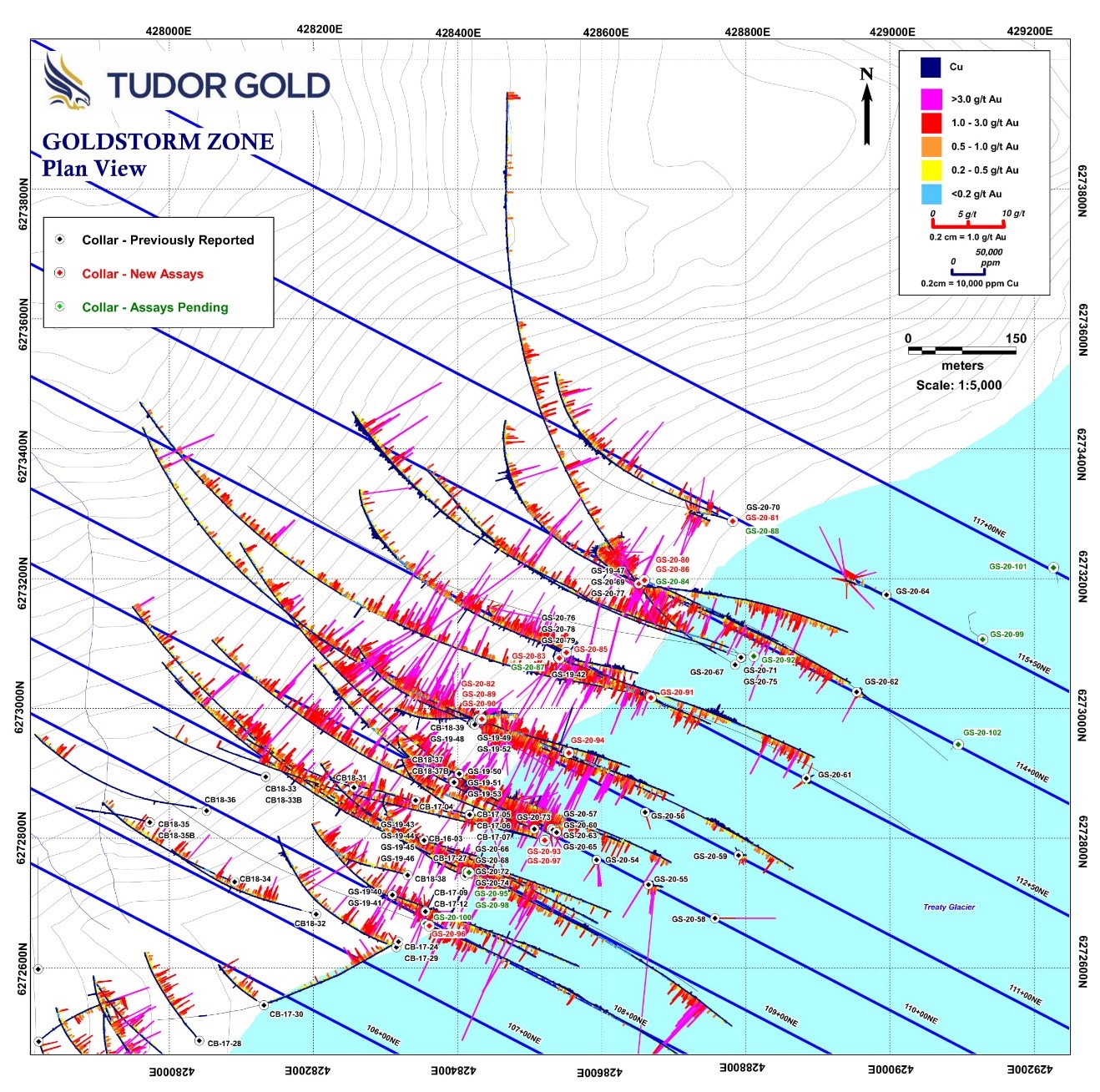

Table l: Results Goldstorm Zone Press Release December 15th 2020

| Section | Hole | Zone | From | To | Interval (m) | Au | Ag | Cu | AuEQ |

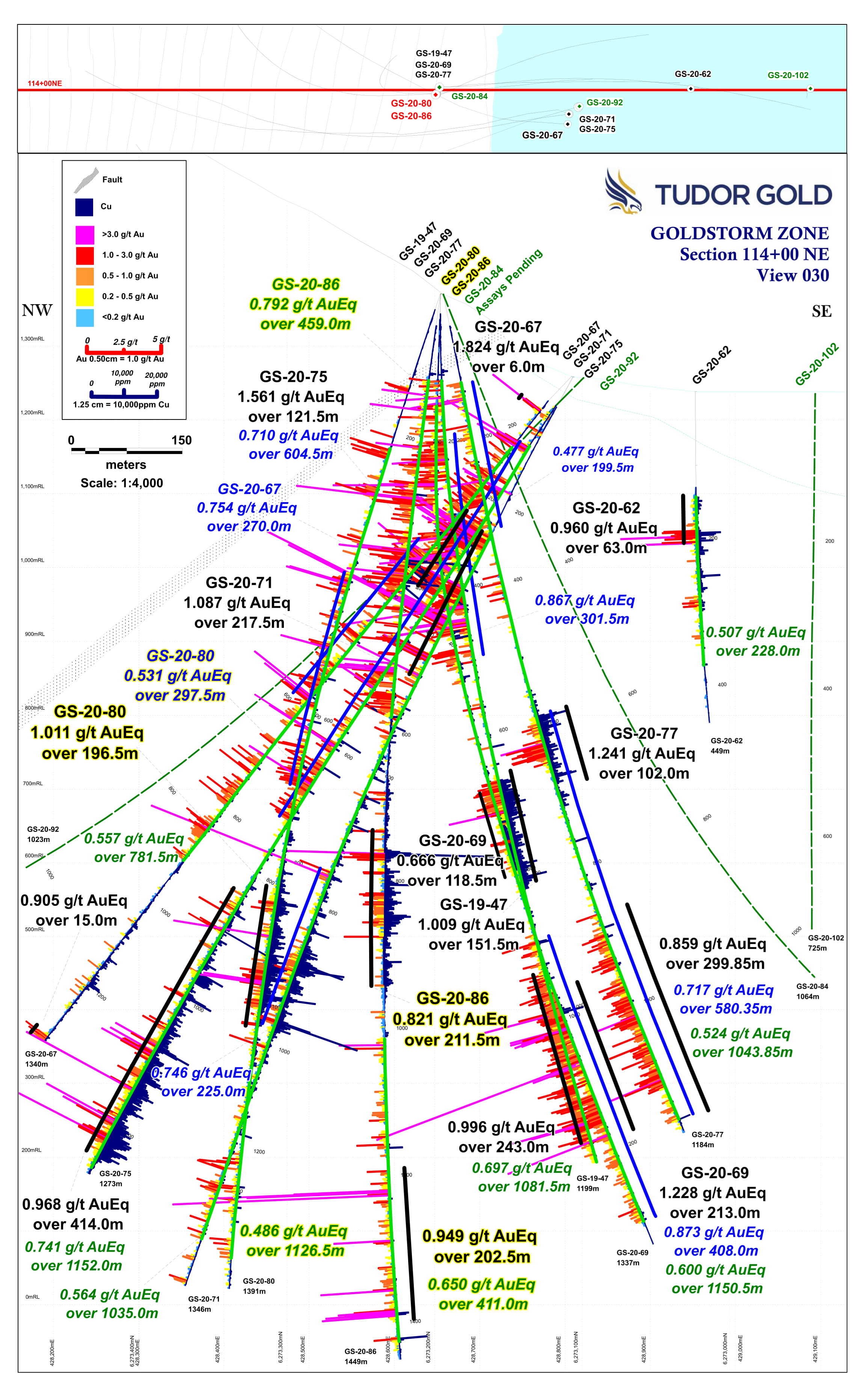

| 114+00 NE | GS-20-80 | 300H + CS600 | 222.50 | 1349.00 | 1126.50 | 0.369 | 1.66 | 653 | 0.486 |

| including 300H | 398.00 | 695.50 | 297.50 | 0.488 | 1.98 | 135 | 0.531 | ||

| and including CS600 | 831.50 | 1028.00 | 196.50 | 0.572 | 3.25 | 2703 | 1.011 | ||

| 115+50 NE | GS-20-81 | 300H + CS600 + DS5 | 558.40 | 1389.50 | 831.10 | 0.422 | 1.56 | 940 | 0.580 |

| including 300H + CS600 | 558.40 | 957.50 | 399.10 | 0.529 | 1.96 | 1712 | 0.807 | ||

| with 300H | 558.40 | 636.50 | 78.10 | 1.047 | 1.52 | 139 | 1.086 | ||

| and with CS600 | 704.00 | 957.50 | 253.50 | 0.481 | 2.37 | 2494 | 0.879 | ||

| 111+00 NE | GS-20-82 | 300H + CS600 | 113.00 | 1041.50 | 928.50 | 0.629 | 2.46 | 519 | 0.736 |

| including 300H | 113.00 | 464.00 | 351.00 | 0.969 | 3.56 | 263 | 1.051 | ||

| with 300H | 224.00 | 422.00 | 198.00 | 1.283 | 5.29 | 408 | 1.407 | ||

| 112+50 NE | GS-20-83 | 300H + CS600 + DS5 | 73.50 | 994.50 | 921.00 | 0.676 | 3.97 | 655 | 0.821 |

| including 300H | 73.50 | 418.50 | 345.00 | 1.008 | 3.48 | 191 | 1.078 | ||

| and including CS600 | 566.45 | 727.50 | 161.05 | 0.426 | 3.90 | 2863 | 0.898 | ||

| and including DS5 | 813.00 | 994.50 | 181.50 | 0.919 | 7.33 | 190 | 1.035 | ||

| 112+50 NE | GS-20-85 | 300H | 66.50 | 692.00 | 625.50 | 0.748 | 3.80 | 275 | 0.834 |

| CS600 | 752.00 | 989.00 | 237.00 | 0.241 | 2.23 | 1734 | 0.524 | ||

| DS5 | 1118.00 | 1278.50 | 160.50 | 0.511 | 2.11 | 128 | 0.555 | ||

| 114+00 NE | GS-20-86 | 300H | 118.50 | 577.50 | 459.00 | 0.712 | 3.43 | 263 | 0.792 |

| CS600 | 730.50 | 942.00 | 211.50 | 0.469 | 2.49 | 2172 | 0.821 | ||

| DS5 | 1014.00 | 1425.00 | 411.00 | 0.595 | 2.85 | 145 | 0.650 | ||

| including | 1192.50 | 1395.00 | 202.50 | 0.889 | 3.39 | 130 | 0.949 | ||

| 111+00 NE | GS-20-89* | 300H | 87.00 | 125.00 | 38.00 | 1.142 | 12.85 | 91 | 1.309 |

| 111+00 NE | GS-20-90 | 300H + CS600 | 63.00 | 847.50 | 784.50 | 0.646 | 2.89 | 465 | 0.750 |

| including 300H | 72.00 | 405.00 | 333.00 | 0.915 | 3.60 | 177 | 0.984 | ||

| and including CS600 | 643.50 | 768.00 | 124.50 | 0.635 | 4.60 | 1632 | 0.932 | ||

| 110+00 NE | GS-20-93* | 300H | 20.50 | 237.50 | 217.00 | 0.535 | 3.40 | 152 | 0.599 |

| incl. | 20.50 | 131.00 | 110.50 | 0.850 | 5.49 | 206 | 0.946 | ||

| 111+00 NE | GS-20-94 | 300H | 36.00 | 1261.50 | 1225.50 | 0.646 | 2.50 | 178 | 0.702 |

| including | 36.00 | 390.00 | 354.00 | 1.123 | 4.14 | 287 | 1.215 | ||

| or including | 36.00 | 820.50 | 784.50 | 0.856 | 3.45 | 239 | 0.933 | ||

| 108+00 NE | GS-20-96 | 300H | 6.00 | 109.50 | 103.50 | 0.804 | 2.27 | 129 | 0.850 |

| CS600 | 279.00 | 385.50 | 106.50 | 0.228 | 3.77 | 1235 | 0.457 | ||

| 110+00 NE | GS-20-97 | 300H | 18.40 | 584.00 | 565.60 | 0.609 | 1.95 | 107 | 0.648 |

| incl. | 18.40 | 381.50 | 363.10 | 0.693 | 2.35 | 141 | 0.742 |

*lost drill hole in mineralization

- All assay values are uncut, and intervals reflect drilled intercept lengths.

- HQ and NQ2 diameter core samples were sawn in half and typically sampled at standard 1.5m intervals.

- The following metal prices were used to calculate the Au Eq metal content: Gold $1322/oz, Ag: $15.91/oz, Cu: $2.86/lb. Calculations used the formula Au Eq g/t = (Au g/t) + (Ag g/t x 0.012) + (Cu% x 1.4835). All metals are reported in USD and calculations do not consider metal recoveries. True widths have not been determined as the mineralized body remains open in all directions. Further drilling is required to determine the mineralized body orientation and true widths.

Table ll: Drill Data for Holes in Press Release December 15th, 2020

Table II and Table III

To view an enhanced version of Table II and Table III, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_002full.jpg

Attached are Sections 108+00 NE, 110+00 NE, 111+00 NE, 112+50 NE, 114+00 NE and 115+50 NE showing holes traces with histogram plots for gold and copper results and a Plan Map showing the drill hole and section locations.

Walter Storm, President and CEO, stated: “We are very pleased to announce the safe successful completion of our 2020 diamond drill hole program. We completed over four times the amount of drilling from the previous year’s program, greatly advancing Tudor’s flagship Treaty Creek Property. We completed almost 44,000 meters of drilling at the Goldstorm System and over 1,600 meters of drilling at the Perfect Storm target. Once we receive the final results from the last eleven drill holes, we will then pass the data to our resource engineers and geoscientists for an initial resource estimate. Continued drilling is required for 2021 to locate the limits or edges of the mineralized system. Due to the size and robust nature of the mineralization, the Goldstorm System remains open on all fronts and to depth. We are proud of what we have achieved in these last two years of exploration and in-particular, the great effort to withstand the harsh winter elements during November and December at Treaty Creek to bring the 2020 drill campaign to a safe close. Our commitment is to continue to advance the project as quickly as possible. We have left the track-drill carriage components for two track-mounted drill rigs on-site so our team can get an early start to the 2021 drill season. We look forward to receiving the final results of the eleven drill holes from MSA Labs within a couple of weeks to complete the 2020 exploration season on schedule.”

Tudor Gold Corp and our associated service companies have taken extreme measures to maintain the highest professional standards while working within COVID-19 health and safety protocols.

Darren Blaney, CEO of American Creek, commented: “We are extremely impressed with the drill program our JV partner Tudor Gold has completed this year and with the significant potential deposit that it has revealed. The Goldstorm zone already appears to be world-scale in size and yet is still open from the northeast to the southeast and remarkably, also at depth. The Magnetotelluric survey done in 2016, which shows potential continuation of gold mineralization well beyond the extent of this year’s drilling of Goldstorm, has proven to be very accurate. That same survey data also shows tremendous potential at the Perfect Storm zone which, due to permitting restraints, was only able to have the outer halo drill tested this year, and yet the drilling still encountered gold mineralization.

“Recognition must be given to both Tudor Gold and More Core for initiating the drill program in early May and carrying through to December. This is no small feat in the Golden Triangle region. While bad weather and Covid-19 limited many projects within the area this season, Tudor and More Core delivered an incredible 45 km of drilling with every hole encountering significant gold mineralization.

“We look forward to the remaining holes, the metallurgical work, and ultimately the maiden resource calculation of the Goldstorm on Treaty Creek sometime in the new year.”

QA/QC

Drill core samples were prepared at MSA Labs’ Preparation Laboratory in Terrace, BC and assayed at MSA Labs’ Geochemical Laboratory in Langley, BC. Analytical accuracy and precision are monitored by the submission of blanks, certified standards and duplicate samples inserted at regular intervals into the sample stream by Tudor Gold personnel. MSA Laboratories quality system complies with the requirements for the Company. International Standards ISO 17025 and ISO 9001. MSA Labs is independent of the company.

Qualified Person

The Qualified Person for Tudor’s news release for the purposes of National Instrument 43-101 is Tudor’s Vice President of Project Development, Ken Konkin, P.Geo. He has read and approved the scientific and technical information that forms the basis for their disclosure contained in their news release.

The Qualified Person for this news release is James A. McCrea, P. Geo., for the purposes of National Instrument 43-101. While American Creek has not independently confirmed Tudor’s information, Mr. McCrea has read and approved the scientific and technical information that forms the basis for the disclosure contained in this news release.

Treaty Creek JV Partnership

The Treaty Creek Project is a Joint Venture with Tudor Gold owning 3/5th and acting as operator. American Creek and Teuton Resources each have a 1/5th interest in the project creating a 3:1 ownership relationship between Tudor Gold and American Creek. American Creek and Teuton are both fully carried until such time as a Production Notice is issued, at which time they are required to contribute their respective 20% share of development costs. Until such time, Tudor is required to fund all exploration and development costs while both American Creek and Teuton have “free rides”.

Treaty Creek Background

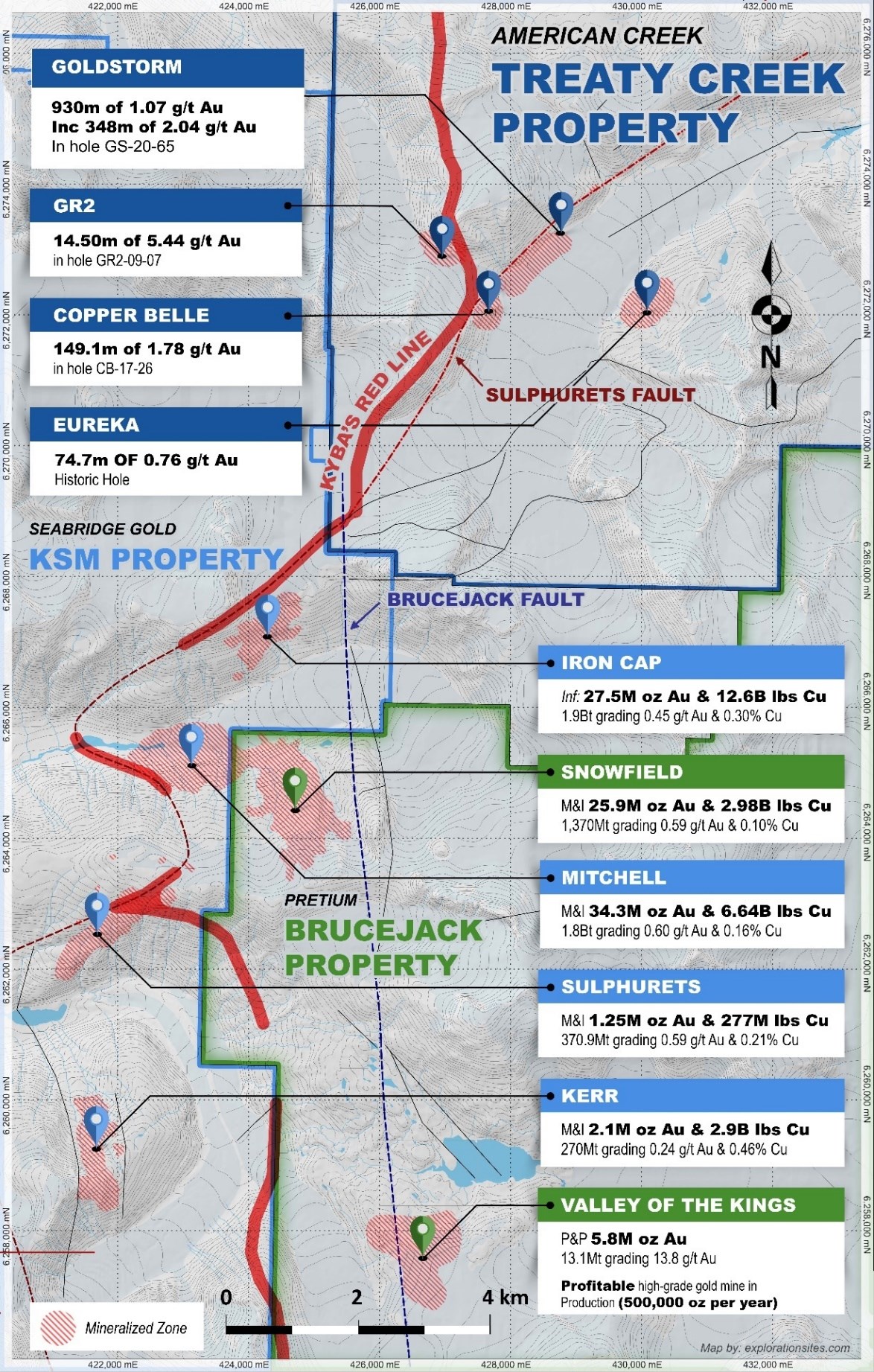

The Treaty Creek Project lies in the same hydrothermal system as Pretium’s Brucejack mine and Seabridge’s KSM deposits however, with far better logistics.

For a better understanding of the mineralized zones at the Goldstorm, please view this video (which shows the original 20,000m planned drill program opposed to the 40,000m+ drill program that has taken place).

Sulphurets Hydrothermal System

To view an enhanced version of this map, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_003full.jpg

About American Creek

American Creek is a Canadian junior mineral exploration company with a strong portfolio of gold and silver properties in British Columbia.

Three of those properties are located in the prolific “Golden Triangle”; the Treaty Creek JV with Tudor Gold/Walter Storm, the D-1 McBride, and the 100% owned past producing Dunwell Mine.

The Corporation also holds the Gold Hill, Austruck-Bonanza, Ample Goldmax, Silver Side, and Glitter King properties located in other prospective areas of the province.

See additional images of drill locations in this press release at www.americancreek.com.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

This news release contains forward-looking statements. These statements are based on current expectations and assumptions that are subject to risks and uncertainties. Readers should not place undue importance on forward-looking information and should not rely upon this information as of any other date. Actual results could differ materially because of factors discussed in the Corporation’s management discussion and analysis filed with applicable Canadian securities regulators, which can be found under the Corporation’s profile on www.sedar.com. The Corporation does not assume any obligation to update any forward-looking statements.

To view an enhanced version of this map, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_004full.jpg

To view an enhanced version of this map, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_005full.jpg

To view an enhanced version of this map, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_006full.jpg

To view an enhanced version of this map, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_007full.jpg

To view an enhanced version of this map, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_008full.jpg

To view an enhanced version of this map, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_009full.jpg

To view an enhanced version of this map, please visit:

https://orders.newsfilecorp.com/files/682/70402_5f70404f040adb98_010full.jpg

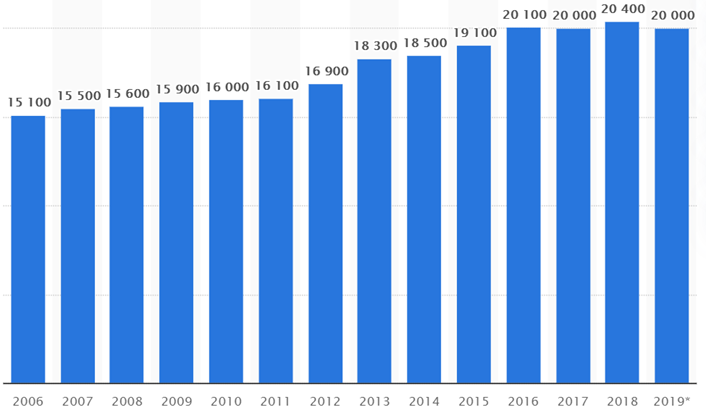

Total copper mine production worldwide from 2006 to 2019 (in 1,000 metric tons)

Total copper mine production worldwide from 2006 to 2019 (in 1,000 metric tons)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

.jpg){kind=link}