Posted by AGORACOM

at 9:11 AM on Wednesday, March 25th, 2020

Cardston, Alberta–(Newsfile Corp. – March 25, 2020) – American Creek Resources (TSXV: AMK) (the “Corporation”

or “American Creek”) is pleased to announce its partner Tudor Gold

Corp. (TSXV: TUD) (FSE: TUC) (“Tudor Gold”) has sufficient funds to

execute a significantly larger drilling and exploration program, than

the 2019 program, on the Goldstorm Zone at Treaty Creek project this

year. With the capital raised in December 2019, as well as the recent

warrants exercises, the Tudor Gold has a good cash position to execute a

fully funded and very ambitious drill program at Treaty Creek this

year. Tudor Gold is currently in the final stages of finalizing all

preparations needed for the upcoming 2020 drill program at Treaty Creek.

Tudor

Gold’s Vice President of Project Development, Ken Konkin, P.Geo.,

states: “The Goldstorm system is currently open at depth and along the

northeast axis of the mineralized body. The drill program is designed to

extend and to explore the limits of Goldstorm system to the southeast

as well as to the northeast and to depth. We anticipate drilling

approximately 18,000 to 20,000 metres of HQ and NQ diameter core from

7-10 drill platforms with four diamond drill rigs. Compared to the drill

program last year (14 diamond drill holes over 9,781.8 meters), the

planned 2020 drill program will be much larger.”

The current known

length of the northeast axis of the Goldstorm System is over 850 meters

long and the southeast axis is at least 600m across. The system remains

open in all directions and to depth. The best mineralization

encountered to date is from the two consecutive 150m step-out holes to

the Northeast: GS-19-42 yielded 0.849 g/t Au Eq over 780 m with 1.275

g/t Au Eq over 370.5m and GS-19-47 yielded 0.697 g/t Au Eq over 1,081.5m

with 0.867 g/t Au Eq over 301.5m.

The best southeast extension

came from GS-19-52 which yielded 0.783 g/t Au Eq over 601.5m intercept

with 1.062 g/t Au Eq over 336.0m intercept. (results from the company’s

NR dated March 3rd, 2020).

Tudor Gold response to COVID-19:

Tudor

Gold has introduced additional precautionary steps to manage and

respond to the risks associated with COVID-19 virus. This includes, for

example the cancellation of all non-essential global travel and the

reducing in person meetings and transitioning to teleconferencing where

possible. Vancouver office staff are now working from home until

government advisories change.

Tudor Gold is regularly monitoring

the situation and following local and national health authority

requirements and recommendations.

Walter Storm, President and CEO of Tudor Gold stated:

“We are taking all appropriate measures to protect the safety, health

and well-being of our people and all those who interact with our

business. Tudor Gold is following guidance and directives as updated by

federal, regional and provincial health authorities in respect of

general and drill-site specific protocols. We are very fortunate to have

a strong balance sheet amidst the volatile market created by COVID-19.”

Qualified Person

The

Qualified Person for this news release for the purposes of National

Instrument 43-101 is the Company’s Vice President of Project

Development, Ken Konkin, P.Geo. He has read and approved the scientific

and technical information that forms the basis for the disclosure

contained in this news release.

Treaty Creek JV Partnership

The Treaty Creek Project is a Joint Venture with Tudor Gold owning 3/5th and acting as operator. American Creek and Teuton Resources each have a 1/5th

interest in the project. American Creek and Teuton are both fully

carried until such time as a Production Notice is issued, at which time

they are required to contribute their respective 20% share of

development costs. Until such time, Tudor is required to fund all

exploration and development costs while both American Creek and Teuton

have “free rides”.

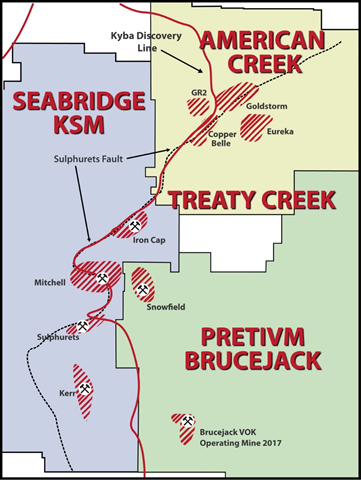

Treaty Creek Background

The

Treaty Creek Project lies in the same hydrothermal system as Pretium’s

Brucejack mine and Seabridge’s KSM deposits with far better logistics.

American

Creek is a Canadian junior mineral exploration company with a strong

portfolio of gold and silver properties in British Columbia. Three of

those properties are located in the prolific “Golden Triangle”; the

Treaty Creek and Electrum joint venture projects with Tudor Gold/Walter

Storm as well as the 100% owned past producing Dunwell Mine.

The

Corporation also holds the Gold Hill, Austruck-Bonanza, Ample Goldmax,

Silver Side, and Glitter King properties located in other prospective

areas of the province.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com

Posted by AGORACOM

at 11:49 AM on Friday, March 20th, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged of 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits. Click Here For More Info

Credit Deflation and Gold

Gold and precious metals mining shares are casualties of panic

selling across all financial markets. The scenario is similar to what

happened in 2008 during the global financial crisis (GFC). When the

general selling exhausted itself in late 2008, gold and mining shares

delivered superior absolute and relative performance for the following

three years. We believe that this pattern is likely to repeat following

this sell-off.

While COVID-19 outbreak is grabbing the headlines, the far bigger

story is the deflation of financial assets that it has triggered and the

resulting loss of investment confidence. Markets that had been priced

for perfection must now reckon with a likely recession, soaring fiscal

deficits and the very real possibility of a sustained bear market.

In our opinion, even though the economy will recover from the

downturn and the health scare will prove to be temporary, financial

asset valuations are unlikely to return to pre-crash manic levels. In

mid-February, the Wilshire 5000 Stock Index1 traded at approximately

145% to gross domestic product (GDP),2 its second highest level since

1950, and only slightly below the 2000 peak (see Figure 1). At this

writing, the ratio has fallen to 114% (as of 3/17/2020), which is still

very expensive by historical standards. Valuations are driven by

investor psychology, leverage and the liquidity necessary to support

leverage. All three may have been critically impaired for the near to

intermediate term.

Figure 1. Total U.S. Corporate Equities and U.S. GDP (1950-2020)

If financial assets struggle, interest in gold is very likely to

widen. Gold may have been caught up in the recent stampede for

liquidity, but it has delivered good relative performance on a

year-to-date basis; gold bullion is up 0.73% as of March 17, compared to

-25.17% for the S&P 500 Index.3 The 12-month figures (as of

3/17/2020) are even more impressive: gold has returned 17.19% vs. -8.54%

for the S&P 500.

On a peak-to-trough basis for the last few weeks, gold has declined

roughly 12%. Other safe haven assets have experienced the same pressure.

For example, the yield on 30-year U.S. Treasury bond rose from less

than 1.0% to 1.5% in only a few days, a drawdown of more than 30%. What

this shows is that quality assets will be sold by portfolio managers

desperate to reduce leverage. Low-grade assets cannot be sold quickly

enough to meet margin calls.

It was leverage that inflated valuations, not fundamental economic

growth and strong year-over-year earnings. In fact, corporate pre-tax

profits have been declining since Q3 2014. Figure 2 shows pretax profits

on a quarterly basis since 2014.

Figure 2. U.S. Corporate Pre-Tax Profits Have Been Declining ($Billions)

The illusion of earnings growth that has captivated investor

psychology was achieved through share buybacks and increased leverage.

Growth of earnings per share, not the same as profit growth, has been

juiced by financial engineering. The same can be said for returns on

financial assets. The amount and location of leverage within the economy

and financial markets is opaque but may well have reached high tide for

many years. A post-recession economic recovery will not necessarily,

and does not have to, translate into strong returns from investing in

financial assets.

Global Debt Has Increased +100% Since 2007

In popular thinking, the current U.S. administration, or the one that

follows it, will pull every trick out of the bag to stimulate the

economy. This belief will likely excite investors from time to time in

anticipation of a rebound. Unfortunately, the financial markets are

experiencing a deflationary bust that could spread to general economic

activity. Public policy has all but exhausted the potential benefits of

resorting to traditional monetary and fiscal solutions. The marginal

benefit to economic growth from heaping on new layers of debt is capped

by the law of diminishing returns, as shown by Figure 4 from Rosenberg

Economics. Since 2007, global debt increased 110% vs. 46% for global

GDP:

Figure 3. Global Debt vs. Global GDP ($ Trillions)

Source: Rosenberg Economics. Data as of 12/31/2019.

Central banks have few conventional tools remaining to combat credit

deflation. An impotent response can be expected from new rounds of

monetary stimulus, rate reductions or central bank balance sheet

expansion. Global debt, public and private, measures 287% vs. global GDP

($244 trillion divided by $85 trillion). The debt burden will most

assuredly grow, a post coronavirus rebound notwithstanding. The world’s

debt structure is already incapable of withstanding even a minute rise

in rates. More debt relative to GDP will only make matters worse. All

that remains is currency destruction.

Gold has been rising for the past eighteen months side by side with a

strong stock market and no inflation. Conventional wisdom said that

wasn’t supposed to happen. As shown in Figure 4, gold has outperformed

equities and bonds since 2000, the dawn of radical monetary

experimentation by central bankers. We think gold has been sensing the

endgame for Keynesian policy prescriptions, mainstream economic thinking

and hyper-leveraged investment practices.

Figure 4. The Modern Era of Gold Gold Bullion vs. Stocks, Bonds, Oil, USD (2000-2020)

For the period from 12/31/1999 to 3/16/2020, gold has provided posted

an average annual return of 8.55%, compared to 5.44% for U.S. bonds,

4.44% for U.S. stocks, 0.57% for oil and -0.19% for the U.S. dollar.

Source: Bloomberg. Period from 12/31/1999 –3/16/2020.4

Gold Miners are Poised to Perform

During the 1930s credit deflation, gold and gold mining stocks

performed well in relative and absolute terms. When credit deflates, and

counterparties cannot be trusted, gold is the ultimate safe asset. In

the 1930s, the metal price rose, costs of producing gold declined and

the miners generated strong earnings and paid handsome dividends. We

believe that this is a sequence that will repeat.

At the moment, mining company valuations appear extraordinarily

cheap. It is one of the few industries that will report solid

year-over-year earnings gains for the remainder of this year and perhaps

into the next.

Buying low is never easy but now is the time to do it.

Posted by AGORACOM

at 10:55 AM on Thursday, March 12th, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged of 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits. Click Here For More Info

Tudor Gold said it had discovered a significant new copper-silver horizon within the Goldstorm system.

The newly discovered copper-rich CS 600 Horizon is a very important feature of the Goldstorm System.

Presence of copper and silver mineralization gives this discovery a true polymetallic nature yet it remains a gold-dominant project.

Tudor Gold Corp. [TUD-TSXV, TUC-Frankfurt] has released the results

of gold-equivalent calculations for all drilling completed at the

company’s Treaty Creek project, which is located in British Columbia’s

Golden Triangle region.

These calculations are posted on the company’s website and include

credit for previously analyzed values for copper and silver. Geological

analysis and reinterpretation of all the drill holes to date exposed a

new copper horizon (CS 600 horizon) as well as significant silver and

copper mineralization through the Goldstorm system, the company said in a

press release, which was issued just after the close of trading on

March 3, 2020.

On Wednesday, Tudor shares eased 4.0% or $0.02 to 48 cents on volume

of 309,585. The shares are currently trading in a 52-week range of 26

cents and $1.08.

Tudor Gold holds a 60% stake in the Treaty Creek joint venture and is

the project operator. The other partners are American Creek Resources

Ltd. [AMK-TSXV] and Teuton Resources Corp. [TUO-TSXV, TUC-Frankfurt],

each of which hold a 20% stake in the project. American Creek and Teuton

are both fully carried to a production notice. At that point, each of

the two is required to contribute their respective 20% share of

development costs.

Until that happens, Tudor is required to fund all exploration and

development costs. The property is also subject to 3% net smelter return

royalties.

The 17,913-hectare Treaty Creek Project borders Seabridge Gold Inc.’s

[SEA-TSX, SA-NYSE] KSM property to the southwest and borders Pretium

Resources Inc.’s [PVG-TSX] Brucejack property to the southeast. The

past-producing Eskay Creek mine lies 12 kilometres to the west.

Exploration of the Treaty Creek area over the past 30 years by

various junior companies has resulted in the discovery of a number of

surface mineral showings, some with very high gold and silver values.

There have been over 150 diamond drill holes completed on the

property from 1987 to date, in eight different mineral zones. However,

it is only recently that drilling revealed the potential for a

large-scale porphyry-style gold deposit at the Copper Belle and

Goldstorm zones, which are located on trend and just five kilometres

northeast of the KSM deposits.

In a press release on December 16, 2019, Tudor Gold said it had

discovered a significant new copper-silver horizon within the Goldstorm

system.

The newly discovered copper-rich CS 600 Horizon is a very important

feature of the Goldstorm System, the company has said. It said presence

of copper and silver mineralization gives this discovery a true

polymetallic nature yet it remains a gold-dominant project.

“We are very encouraged to see that the silver copper mineralization

has made an important impact to the gold equivalent results from our

recent drilling as well as the historical drilling,’’ said Ken Konkin,

vice-president of project development at Tudor Gold.

“The next step is to plan the drill hole program for the 2020

exploration season,†he said. The company’s goal is to design a diamond

drill program that will fast-track the exploration program for 2020 with

the objective to begin mineral resource estimate work as soon as

possible.

Bay Street billionaire Eric Sprott recently increased his stake the company to 14.1% by investing in a non-brokered private placement of 4.2 million shares that raised $2.93 million. The shares are priced at 70 cents each.

About American Creek

American Creek holds a strong portfolio of gold and silver properties

in British Columbia. The portfolio includes three gold/silver

properties in the heart of the Golden Triangle; the Treaty Creek and

Electrum joint ventures with Walter Storm/Tudor, as well as the recently

acquired 100% owned past producing Dunwell Mine. Other properties held

throughout BC include the Gold Hill, Austruck-Bonanza, Ample Goldmax,

Silver Side, and Glitter King.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Company is available on its website at www.americancreek.com

Posted by AGORACOM

at 9:38 AM on Wednesday, March 4th, 2020

P&E Mining Consultants Inc. Provides Drill Hole Spacing Recommendation for the 2020 Drill Plan

Calculations include credit for previously analyzed values for Cu and Ag

Newly discovered NE Extension within the 300 Horizon. The gold-only result of 1.27 gpt Au over a 252 metre (m) interval increased to 1.51 gpt AuEq, an increase of 18.9%.

Cardston, Alberta–(Newsfile Corp. – March 4, 2020) – American Creek Resources Ltd. (TSXV: AMK) (the “Company”)

is pleased to announce the results of gold-equivalent (AuEq)

calculations for all drilling completed at JV partner Tudor Gold’s

(“Tudor”) flagship project Treaty Creek. These calculations include

credit for previously analyzed values for Cu and Ag. Geological analysis

and reinterpretation of all the drill holes to date exposed a new

copper horizon (CS 600 horizon) as well as significant silver and copper

mineralization throughout the Goldstorm system.

The strongest AuEq increase was seen in the newly discovered NE Extension within the 300 Horizon. The

gold-only result of 1.27 gpt Au over a 252 metre (m) interval increased

to 1.51 gpt AuEq (with 13.8 gpt Ag and 504 ppm Cu), an increase of

18.9%.

All drill holes at Goldstorm Zone had

significant increases to the composite results when the AuEq values for

the copper and silver mineralization were included however when the

drill holes intersected the CS-600 Horizon, the copper values within

this mineralized body had the greatest impact to an individual horizon

with up to 79.8% increase to the AuEq value from a gold-only 0.39 gpt Au over 150m to 0.70 gpt AuEq over the same 150m interval.

P&E Mining Consultants Inc. were

retained to assess all Goldstorm drill hole results and historical data

in order to render an opinion as to the consistency of the gold

mineralization as well to ascertain the recommended drill hole spacing

that would be required to potentially derive an Indicated Mineral

Resource and a Measured Mineral Resource. P&E Mining Consultants

Inc. concluded the following:

“Three dimensional continuity analyses

of the Treaty Creek drill hole assay results were carried out for the

Goldstorm Zone. The regional geological trend was used to guide the

selection of horizontal, across-strike, and dip-plane directions during

variogram fan analysis. Variogram fans were generated separately for Ag,

Au, Cu, Pb, and Zn uncapped composite samples in each zone.

All modeled semi-variograms display a

very low nugget effect, and display long range continuity down the

plunge of the mineralization and along the regional strike of the

deposits.

For the Goldstorm Zone, a drill spacing

of 200 m is recommended for Indicated Mineral Resources, and 100 m for

Measured Mineral Resources.”

Tudor’s goal is to design a diamond drill

hole program that will fast-track the exploration program for 2020 with

the objective to begin the Mineral Resource Estimate work as soon as

possible.

Vice President of Project Development Ken Konkin P.Geo. comments:

“We are very encouraged to see that the silver and copper

mineralization has made an important impact to the AuEq results from our

recent drilling as well as the historical drilling. The next step is to

plan the drill hole program for the 2020 exploration season. We

continue to work with our Mineral Resource Estimate geologists and

engineers from P&E Mining Consultants to plan the drill hole program

in order to optimize the drilling and to attempt to fast-track the

exploration program for this coming drill season

Table l provides gold equivalent composites from the 2019 drilling

and all historical drilling within the Goldstorm Zone. Table ll contains

the drill data including collar location, depth of drill holes as well

as the dip and azimuth for all drill hole.

TABLE l: Au Eq COMPOSITES GOLDSTORM ZONE

Section

HOLE ID

From

To

Interval (m)

AuEq g/t

Au g/t

Ag g/t

Cu ppm

% increase

Horizon

107+00 NE

CB-17-29

1.20

575.00

573.80

0.321

0.278

0.9

224

15.5%

300

107+00 NE

CB-17-29

60.50

333.50

273.00

0.435

0.392

1.1

197

11.0%

300

107+00 NE

CB-17-29

60.50

176.00

115.50

0.728

0.685

1.9

142

6.3%

300

107+00 NE

CB-18-32

196.50

783.50

587.00

0.542

0.497

1.6

177

9.1%

300 + CS600

107+00 NE

CB-18-32

196.50

316.50

120.00

1.082

1.045

1.7

106

3.5%

300

107+00 NE

CB-18-34

419.00

711.50

292.50

0.499

0.461

2.4

63

8.2%

300

107+00 NE

CB-18-34

831.50

897.50

66.00

0.290

0.221

1.3

361

31.2%

CS600

108+00 NE

CB-17-09

41.00

545.00

504.00

0.549

0.488

2.3

225

12.5%

300

108+00 NE

CB-17-09

41.00

200.00

159.00

0.782

0.708

2.9

261

10.5%

300

108+00 NE

CB-17-12

3.00

243.50

240.50

0.848

0.797

2.6

139

6.4%

300

108+00 NE

CB-17-12

33.00

224.00

191.00

0.979

0.923

3.0

134

6.1%

300

108+00 NE

CB-17-24

3.50

563.00

559.50

0.618

0.576

2.0

121

7.3%

300

108+00 NE

CB-17-24

62.00

275.00

213.00

1.018

0.945

3.9

180

7.7%

300

108+00 NE

CB-17-24

3.50

686.00

682.50

0.563

0.498

1.8

288

13.1%

300

108+00 NE

CB-18-36

659.50

772.00

112.50

0.487

0.454

1.8

74

7.3%

300

108+00 NE

CB-18-36

659.50

704.50

45.00

0.733

0.688

2.7

88

6.5%

300

108+00 NE

CB-18-36

682.00

703.00

21.00

1.101

1.035

4.6

79

6.4%

300

108+00 NE

CB-18-38

20.50

638.00

617.50

0.465

0.429

1.3

137

8.4%

300

108+00 NE

CB-18-38

248.50

353.00

104.50

0.733

0.639

3.4

360

14.7%

300

108+00 NE

CB-18-38

468.50

638.00

169.50

0.683

0.659

1.1

76

3.6%

300

108+00 NE

GS-19-40

23.00

350.00

327.00

0.501

0.443

1.72

251

13.1%

300

108+00 NE

GS-19-40

81.50

127.00

45.50

1.060

0.907

4.92

634

16.9%

300

108+00 NE

GS-19-41

27.50

353.00

325.50

0.724

0.589

5.25

480

22.9%

300

108+00 NE

GS-19-41

47.00

146.00

99.00

1.252

1.015

9.83

800

23.3%

300

109+00 NE

CB-16-03

88.00

708.00

620.00

0.582

0.534

1.5

202

9.0%

300

109+00 NE

CB-16-03

112.00

426.00

314.00

0.792

0.733

2.2

220

8.0%

300

109+00 NE

CB-17-04

152.10

327.00

174.90

0.827

0.803

1.0

76

3.0%

300

109+00 NE

CB-17-27

12.50

536.00

523.50

0.688

0.640

1.6

197

7.5%

300

109+00 NE

CB-17-27

12.50

350.00

337.50

0.807

0.758

2.0

169

6.5%

300

109+00 NE

CB-18-31

404.00

680.50

276.50

0.526

0.494

1.4

100

6.5%

300

109+00 NE

CB-18-31

481.00

597.00

116.00

0.773

0.732

1.8

124

5.6%

300

109+00 NE

CB-18-33B

599.00

623.00

24.00

0.435

0.367

5.4

22

18.5%

300

109+00 NE

GS-19-43

68.00

561.50

493.50

0.608

0.566

1.36

174

7.4%

300 + CS600

109+00 NE

GS-19-43

141.50

197.00

55.50

1.068

1.005

2.62

211

6.3%

300

109+00 NE

GS-19-43

405.50

561.50

156.00

0.785

0.718

1.50

325

9.3%

CS600

109+00 NE

GS-19-44

101.00

368.00

267.00

0.867

0.807

3.30

134

7.4%

300

109+00 NE

GS-19-44

125.00

275.00

150.00

1.143

1.065

4.62

151

7.3%

300

109+00 NE

GS-19-45

44.00

369.50

325.50

0.765

0.719

1.91

154

6.4%

300

109+00 NE

GS-19-45

62.00

278.00

216.00

0.947

0.901

2.27

122

5.1%

300

109+00 NE

GS-19-45

105.00

278.00

173.00

1.054

1.000

2.63

144

5.4%

300

109+00 NE

GS-19-46

34.50

628.50

594.00

0.550

0.510

1.31

165

7.8%

300 + CS600

109+00 NE

GS-19-46

175.50

337.50

162.00

0.778

0.734

1.93

135

6.0%

300

109+00 NE

GS-19-46

564.00

600.00

36.00

1.425

1.328

1.12

560

7.3%

CS600

110+00 NE

CB-17-06

182.50

589.50

407.00

0.767

0.675

3.1

369

13.6%

300

110+00 NE

CB-17-06

222.00

393.50

171.50

0.914

0.814

3.7

379

12.3%

300

110+00 NE

CB-17-07

99.50

530.00

430.50

0.697

0.625

2.4

293

11.5%

300

110+00 NE

CB-17-07

162.50

309.50

147.00

1.155

1.028

4.9

457

12.4%

300

110+00 NE

CB-18-37B

125.00

819.50

694.50

0.502

0.459

1.2

196

9.4%

300

110+00 NE

CB-18-37B

300.50

423.50

123.00

1.002

0.944

2.0

234

6.1%

300

110+00 NE

CB-18-37B

125.00

912.00

787.00

0.473

0.427

1.2

212

10.8%

300 + CS600

110+00 NE

GS-19-50

148.00

725.50

577.50

0.681

0.602

1.99

372

13.1%

300 + CS600

110+00 NE

GS-19-50

160.00

427.00

267.00

0.878

0.811

2.67

300

8.3%

300

110+00 NE

GS-19-50

652.00

736.00

84.00

0.816

0.571

2.53

1444

42.9%

CS600

110+00 NE

GS-19-51

119.00

365.00

246.00

0.777

0.722

2.31

187

7.6%

300

110+00 NE

GS-19-51

578.00

618.50

40.50

1.304

1.019

2.94

1693

28.0%

CS600

110+00 NE

GS-19-53

108.00

255.00

147.00

1.036

0.984

3.07

98

5.3%

300

111+00 NE

CB-18-39

141.50

705.30

563.80

1.086

0.981

4.4

352

10.7%

300

111+00 NE

CB-18-39

141.50

422.00

280.50

1.274

1.141

5.5

449

11.7%

300

111+00 NE

CB-18-39

539.00

695.00

156.00

1.247

1.154

4.6

257

8.1%

300

111+00 NE

GS-19-48

97.50

1024.50

927.00

0.793

0.677

3.00

543

17.1%

300 + CS600

111+00 NE

GS-19-48

97.50

426.00

328.50

1.152

1.048

4.30

354

9.9%

300

111+00 NE

GS-19-48

871.50

940.50

69.00

1.483

0.937

3.90

3364

58.3%

CS600

111+00 NE

GS-19-49

81.00

907.50

826.50

0.800

0.696

3.40

429

14.9%

300 + CS600

111+00 NE

GS-19-49

81.00

330.00

249.00

1.080

0.998

5.10

137

8.2%

300

111+00 NE

GS-19-49

483.00

606.00

123.00

1.042

0.941

1.80

538

10.7%

300

111+00 NE

GS-19-49

747.00

832.50

85.50

1.494

1.067

10.50

2035

40.0%

CS600

111+00 NE

GS-19-52

62.00

663.50

601.50

0.783

0.668

3.25

513

17.2%

300 + CS600

111+00 NE

GS-19-52

62.00

398.00

336.00

1.062

1.004

2.65

182

5.8%

300

111+00 NE

GS-19-52

513.50

663.50

150.00

0.703

0.391

6.49

1583

79.8%

CS600

112+50 NE

GS-19-42

63.50

843.50

780.00

0.849

0.683

5.80

650

24.3%

300 + CS600

112+50 NE

GS-19-42

63.50

434.00

370.50

1.275

1.097

10.00

393

16.2%

300

112+50 NE

GS-19-42

63.50

315.50

252.00

1.508

1.268

13.80

504

18.9%

300

112+50 NE

GS-19-42

717.70

843.50

125.80

0.902

0.522

3.80

2253

72.8%

CS600

114+00 NE

GS-19-47

117.50

1199.00

1081.50

0.697

0.589

3.40

450

18.3%

300 + CS600 + DS

114+00 NE

GS-19-47

200.00

501.50

301.50

0.867

0.828

2.10

96

4.7%

300

114+00 NE

GS-19-47

665.00

816.50

151.50

1.009

0.572

8.90

2228

76.4%

CS600

114+00 NE

GS-19-47

933.50

1176.50

243.00

0.996

0.908

4.80

207

9.7%

DS

* All assay grades are uncut and intervals reflect drilled intercept

lengths. True widths have not been determined as the mineralized body

remains open in all directions. Further drilling is required to

determine the mineralized body orientation and true widths.

HQ and NQ2 diameter core samples were sawn in half and typically sampled at standard 1.5m intervals.

**Metal prices used to calculate the AuEq metal content are: Gold

$1322/oz, Ag: $15.91/oz, Cu: $2.86/lb. All metals are reported in USD

and calculations do not consider metal recoveries

The goal is to design a diamond drill hole program for the 2020

exploration program with the objective to begin the Mineral Resource

Estimate work at the end of the 2020 field season. Tudor hopes to

accomplish as much drilling needed to bring a Measured and Indicated

Mineral Resource Estimate forward as quickly as possible.

Walter Storm, President and CEO, stated: “These

new gold equivalents are extremely encouraging as our technical team

continues to take positive steps advancing Tudor Gold’s flagship Treaty

Creek Au-Ag-Cu project. Furthermore we received good news from P&E

Mining Consultants Inc. that the drill hole spacing required to derive a

Measured Resource is 100 meters due to the homogenous nature of the

AuEq composites obtained to-date. During the new few weeks, our

geologist and engineers will continue to work with the geological model

and begin to prepare the diamond drill hole proposal for 2020.”

The Treaty Creek Project is a Joint Venture with Tudor Gold owning

3/5th and acting as operator. American Creek and Teuton Resources each

have a 1/5th interest in the project. American Creek and Teuton are both

fully carried until such time as a Production Notice is issued, at

which time they are required to contribute their respective 20% share of

development costs. Until such time, Tudor is required to fund all

exploration and development costs while both American Creek and Teuton

have “free rides”.

QA/QC

Drill core samples were prepared at MSA Labs’ Preparation Laboratory

in Terrace, BC and assayed at MSA Labs’ Geochemical Laboratory in

Langley, BC. Analytical accuracy and precision are monitored by the

submission of blanks, certified standards and duplicate samples inserted

at regular intervals into the sample stream by Tudor Gold personnel.

MSA Laboratories quality system complies with the requirements for the

International Standards ISO 17025 and ISO 9001. MSA Labs is independent

of the Company.

Qualified Person

The Qualified Person for this news release for the purposes of

National Instrument 43-101 is the Company’s Vice President of Project

Development, Ken Konkin, P.Geo. He has read and approved the scientific

and technical information that forms the basis for the disclosure

contained in this news release.

About American Creek

American Creek holds a strong portfolio of gold and silver properties

in British Columbia. The portfolio includes three gold/silver

properties in the heart of the Golden Triangle; the Treaty Creek and

Electrum joint ventures with Walter Storm/Tudor, as well as the recently

acquired 100% owned past producing Dunwell Mine. Other properties held

throughout BC include the Gold Hill, Austruck-Bonanza, Ample Goldmax,

Silver Side, and Glitter King.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Company is available on its website at www.americancreek.com

Posted by AGORACOM-JC

at 4:32 PM on Friday, February 28th, 2020

AGORACOM Clients Attending PDAC 2020

THEREGAL PROJECT

B.C.’s Next Premier

Silver, Lead, Zinc, Copper Deposit?

Affinity Metals holds under option, a 100% interest in the Project, located within the northern end of the prolific Kootenay Arc, a highly prospective mineralized trend.

Treaty Creeks’ GOLDSTORM zone hosts a conceptual volume of ONE BILLION TONNES rock grading close to one gram per tonne gold and is open to the north, east, and at depth. Â

A major drill program is being planned for spring to develop a resource calculation. The focus has been on the gold enriched Goldstorm Zone which is on trend with, and part of, the same geological system as Seabridge Gold’s neighboring KSM deposits.

American Creek been selected to do a formal presentation at the conference. The presentation will be held on Tuesday, March 5 at 2:00PM in room #802

HPQ Silicon Resources designs, develops, manufactures and commercializes plasma base processes

The innovative PUREVAP “Quartz Reduction Reactors†(QRR), will permit the One Step transformation of Quartz (SiO2) into High Purity Silicon (Si) at prices that will promote considerable renewable energy potential.

Lomiko hosts high-grade graphite at its La Loutre Property in Quebec. The company is working toward a Pre-Economic Assessment (PEA) that will increase its current indicated resource of 4.1 Mt of 6.5% Cg to over 10 Mt of 10%+ Cg in order to supply and develop graphite materials for the green economy.

Posted by AGORACOM

at 9:21 AM on Thursday, February 27th, 2020

Cardston, Alberta–(February 27, 2020) – American Creek Resources

Ltd. (TSXV: AMK) (“the Corporation”) is pleased to report the assays

from phase 1 drilling from the 2019 fall drill program that was

conducted at the company’s 100% owned Dunwell Mine property located in

the Golden Triangle of British Columbia.

The Dunwell Mine is a high-grade past producing polymetallic mine

located just 8km by road from the shipping town of Stewart. This

property boasts exceptional logistics and a rich mining history with

significant potential for future development. A significant geological

feature running through the property is the Portland Canal Fissure Zone.

With the recent acquisition of the Glacier Creek claims American Creek

now controls 5km of the 6.5km Portland Canal Fissure Zone which contains

numerous high-grade polymetallic mineral occurrences including two past

producing mines (the Dunwell and Portland Canal). Very little modern

exploration has been done on the property. While there is huge potential

exploring along the extended reaches of the fissure zone, the initial

drill program was designed to test areas near the workings of the

Dunwell mine itself.

The initial objective for the drill program was to test the down dip

extension of the Dunwell main vein below sub-level 4. The second

objective was to test geophysical anomalies from an Induced Polarization

(IP) survey conducted later in the fall of 2019. Both of these

objectives were successfully accomplished with this drill program.

A total of 20 holes totaling 3,245.9m were completed on the property.

The first 14 holes were based on geological and historical data and

were successful in encountering veins of high-grade polymetallic

mineralization including 20.3 g/t AuEq over 2.7m, 18.4 g/t AuEq over 1.5m, 28.6 g/t AuEq over 0.5m and 24.4 g/t AuEq over 0.5m.

Holes DW19-04 to DW19-08 were drilled to test the down dip of the Dunwell zone below sub-level 4.

Results show high-grade hits, including 13.2 g/t AuEq,

in this series of holes that traversed from the east southeast to the

east. The holes consistently hit two zones, both at the base of dikes at

22 – 26 meters and 83 – 87 meters. These two zones, seen in the five

holes, run sub-parallel to the fault the drill pad was located on and

trend for some distance to the north.

Hole DW19-09 was drilled to test the north extension of the main zone

below level 4. The first breccia below the dike shows up in this hole

with a 28.5 g/t AuEq assay and the second with a 18.4 g/t AuEq assay.

HOLE

FROM (m)

TO (m)

INTERVAL (m)

AU g/t

AG g/t

CU %

PB %

ZN %

AuEq g/t

DW19-09

27.60

28.05

0.45

13.870

258.0

0.438

15.530

11.040

28.509

DW19-09

143.02

144.52

1.50

7.898

84.9

0.359

0.791

20.250

18.440

Hole DW19-10 was drilled to test below sub-level 4 but further to the southeast from hole DW19-04.

HOLE

FROM (m)

TO (m)

INTERVAL (m)

AU g/t

AG g/t

CU %

PB %

ZN %

AuEq g/t

DW19-10

29.00

29.57

0.57

2.785

42.5

0.055

0.713

3.020

4.956

DW19-10

88.71

89.61

0.90

3.535

43.2

0.060

1.480

2.860

5.959

DW19-10

99.13

99.79

0.66

1.707

33.7

0.031

0.285

0.529

2.491

The two breccias below the dikes, seen in holes 7 and 8 are present.

Holes 11 to 13 were drilled to follow up on the results from hole 9.

The holes were drilled in a fan where holes 11 and 12 were drilled at a

steeper angle to test below hole 9 and hole 13 was drilled at a flatter

angle to test above hole 9. Hole 14 was drilled at a 5° rotation to the

north of hole 9 to test the width of the structure.

HOLE

FROM (m)

TO (m)

INTERVAL (m)

AU g/t

AG g/t

CU %

PB %

ZN %

AuEq g/t

DW19-11

26.82

27.82

1.00

5.601

66.0

0.213

1.700

7.850

10.729

DW19-11

95.63

96.27

0.64

4.408

34.5

0.026

0.363

0.757

5.326

DW19-11

138.45

138.95

0.50

4.026

66.0

0.166

1.070

6.220

8.139

DW19-11

142.24

144.93

2.69

11.346

142.5

0.220

3.197

13.069

20.269

DW19-12

22.17

23.47

1.30

2.851

60.8

0.147

1.844

4.946

6.638

DW19-12

27.05

27.81

0.76

1.562

30.4

0.104

0.647

2.660

3.461

DW19-12

97.49

99.15

1.66

1.546

54.4

0.041

1.060

5.356

4.998

DW19-13

27.55

28.15

0.60

8.110

113.0

0.171

4.630

8.270

15.116

DW19-13

142.87

143.57

0.70

4.486

66.6

0.068

0.710

1.009

6.087

DW19-14

27.43

28.23

0.80

8.924

161.0

0.309

5.120

6.800

16.222

DW19-14

98.32

99.86

1.54

7.692

32.8

0.009

0.207

0.111

8.227

DW19-14

142.75

144.70

1.95

3.720

43.2

0.103

0.755

9.240

8.673

DW19-14

146.88

147.38

0.50

9.403

264.0

0.528

5.210

20.900

24.347

All the holes intersected the breccia below the dike at about 27

meters. Holes 11, 13 and 14 appear to intersect a similar structure to

that seen in hole 9. Multiple high-grade intercepts assayed as high as 24.3 g/t AuEq, 20.3 g/t AuEq, 16.3 AuEq, and 15.1 g/t AuEq while the remaining intercepts were still strong.

No modern exploration techniques or technologies have been used on

the Dunwell until a cutting edge Induced Polarization (IP) survey took

place in late fall of 2019. Only two of the dozens of geophysical

anomalies identified in the survey in close proximity to the Dunwell

Mine were drill tested in this first phase of drilling.

The last 6 holes (DW19-15 to DW19-19) were drilled to test the extent

of a large IP anomaly and were successful in encountering veins of

high-grade polymetallic mineralization including 19.4 g/t AuEq over 3.6m, 38.1 g/t AuEq over 0.5m and 28.4 AuEq over 0.4m with the remaining intercepts also containing significant mineralization.

Hole 15 was drilled south into the anomaly and Hole 16 was drilled

west into the anomaly with both intersecting a massive sulphide zone.

Holes 17 – 19 were drilled in a fan to follow up hole 16. Hole 18 also

hit a massive sulphide zone.

HOLE

FROM (m)

TO (m)

INTERVAL (m)

AU g/t

AG g/t

CU %

PB %

ZN %

AuEq g/t

DW19-15

100.90

102.08

1.18

8.445

869.0

0.034

0.186

1.265

19.536

DW19-15

152.09

152.59

0.50

32.230

472.0

0.008

0.134

0.372

38.119

DW19-16

45.11

45.81

0.70

11.260

144.0

0.208

6.550

6.010

18.471

DW19-16

75.07

78.68

3.61

8.850

88.8

0.221

1.768

19.514

19.354

DW19-17

no significant results

DW19-18

38.79

39.22

0.43

15.300

185.0

2.874

2.870

14.470

28.243

DW19-19

34.87

36.04

1.17

3.332

27.9

0.048

0.986

2.580

5.239

DW19-19

75.71

77.13

1.42

5.255

225.9

0.159

9.298

3.315

13.328

Hole 16 hit a massive sulphide interval at 75 – 78 meters. Hole 20

was drilled to test an IP anomaly along the access road below the second

drill pad. One small breccia was intercepted.

HOLE

FROM (m)

TO (m)

INTERVAL (m)

AU g/t

AG g/t

CU %

PB %

ZN %

AuEq g/t

DW19-20

121.01

121.45

0.44

1.669

27.5

0.007

0.034

0.082

2.056

CEO and President, Darren Blaney stated: “Our very

first drill program has intersected a significant number of high-grade

veins in the vicinity of the mine workings confirming our belief in the

potential of this project.

The Dunwell is an incredibly prospective property located in the

heart of the Golden Triangle. It has everything going for it from

amazing logistics to past high-grade production, with all indications

being that there is substantive additional ore yet to be mined.

With the recent acquisition of the Glacier Creek Crown Grants we now

cover 5km of the heavily mineralized Portland Canal Fissure Zone which

runs for 6.5km and is associated with over a dozen high-grade gold and

silver showings including two past producing mines. The potential of the

property extends far beyond the old workings of the Dunwell Mine.

Future exploration will be using the latest technologies to aid us in

unlocking that potential.”

Through a series of strategic acquisitions American Creek was able to

purchase the past-producing Dunwell Mine as well as several adjoining

very prospective properties, combining them into one large land package

that encompasses the best gold and silver mineral occurrences and

historic workings in the Bear River valley. The amalgamated property

spans 2,222 hectares covering the majority of the Portland Canal Fissure

Zone, an area first prospected in the late 1800’s and hosting some of

the earliest producing gold and silver mines in the Stewart area.

The Dunwell project is located 8km northeast of Stewart and is road

accessible with the Dunwell Mine adit itself located only 2km from

Highway 37A and a major power line. Stewart hosts a deep sea port

including ore loading and shipping facilities. Unlike the majority of

mineral properties located near Stewart, the Dunwell is located in low

mountainous terrain (700 m and lower elevation) with moderate relief.

These features allow for year-round work which typically isn’t the case

for exploration programs conducted in the Stewart region where projects

are typically at higher altitude, are accessible only by helicopter, and

lack critical infrastructure such as roads and power. The Dunwell

project may just have the best logistics of any project in the Golden

Triangle.

The Dunwell Mine is the most significant mineral occurrence within

the Portland Canal Fissure Zone. Production at the Dunwell occurred

between 1926 and 1937. From historic reports, it appears that a total of

45,657 tonnes averaging 6.63 g/t gold, 223.91 g/t silver, 1.83% lead,

2.43% zinc and 0.056% copper were produced.

In addition to the Dunwell mine itself, the property package also

contains over a dozen other high-grade gold and silver occurrences and

historic small-scale gold/silver high-grading operations along a

north/south trend that correlates to the fissure zone and major

faulting. Some examples of the nine areas that actually produced ore

are:

Ben Ali: 4,500 tons at 21.6 g/t gold

Lakeview 60 tons at 4.7 g/t gold, 2,734 g/t silver, and 11.5% lead

Victoria 11 tons at 20.15 g/t gold, 775 g/t silver, 25% lead

Tyee 8.2 tons at 124.4 g/t gold and 4,478.8 g/t silver

George E 12 tons at 13 g/t gold and 3,250 g/t silver, 23.3% lead

Each of these areas were producing during the 1930’s when exploration

techniques and technology was very primitive. American Creek has

already started to use the latest in exploration technology on the

property and will continue to do so to unlock the great potential that

exists here.

The Qualified Person for the Dunwell results in this new release is

James A. McCrea, P. Geo., for the purposes of National Instrument

43-101. He has read and approved the scientific and technical

information that forms the basis for the disclosure contained in this

news release.

About American Creek

American Creek holds a strong portfolio of gold and silver properties

in British Columbia. The portfolio includes three Golden Triangle

gold/silver properties; the Treaty Creek and Electrum joint ventures

with Walter Storm/Tudor as well as the 100% owned past-producing Dunwell

Mine. Other properties held throughout BC include the Gold Hill,

Austruck-Bonanza, Ample Goldmax, Silver Side, and Glitter King.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com

Posted by AGORACOM

at 1:13 PM on Wednesday, February 26th, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged of 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits. Click Here For More Info

Exchange-traded fund holdings expand for 25 days to most ever

Moody’s Analytics says recession possible if pandemic occurs

Global investors are stashing more and more assets into gold as the

coronavirus outbreak spreads and appetite for risk takes a hit.

The global tally of bullion in exchange-traded funds swelled by the

most in more than a month on Tuesday as equities sank. That was the 25th

consecutive day of inflows, a record. At 2,624.7 tons, the holdings are

the largest ever.

After surging 18% last year, gold has extended its rally in 2020,

with prices hitting the highest since 2013. The haven has been favored

as the virus outbreak has spread beyond China, threatening a pandemic

and slower growth.

Goldman Sachs Group Inc. has said that should the disruption from the disease stretch into the second quarter, prices may rally toward $1,850 an ounce. Spot bullion was last at $1,644.67, up 0.6%. It touched $1,689.31 on Monday.

A global recession

is likely if the coronavirus becomes a pandemic, according to Moody’s

Analytics Chief Economist Mark Zandi. The odds of that outcome now stand

at 40%, up from 20%, he said in a note.

The threat of a prolonged downturn in growth due to the impact of the virus may keep gold elevated, according to Morgan Stanley. Further ETF inflows are likely as long as real interest rates remain negative, it said in a note.

Posted by AGORACOM

at 2:03 PM on Thursday, February 6th, 2020

American Creek Resources Ltd. (TSXV: AMK) is positioned to take full

advantage of the precious metals bull run that many experts believe we

are only in the early stages of.

Image of the Goldstorm Zone found along the base of this hill at Treaty Creek.

With approximately one billion tonnes of gold enriched rock identified (potential for a resource calculation in 2020), the Goldstorm has potential to become a world class gold deposit.

The 2020 drilling is designed to significantly expand the deposit as the system is open to the north, the east and at depth.

The company raised over $3.3 million to strengthen existing

alliances and create a number of new strategic relationships, bringing

strength, credibility and future increased exposure.

Eric Sprott made two separate investments of $1,000,000 into

American Creek. Mr. Sprott is the largest external investor in Treaty

Creek. He recently stated that he is “very excited about the opportunity there as the project has a great shot at having 20 million ounces.”

If you have not yet read the 2019 REPORT ON TREATY CREEK (potential world-class deposit in B.C.’s GOLDEN TRIANGE) click on the image for the fullreport.

The Treaty Creek Project is a joint venture with Tudor Gold owning

3/5th and acting as project operator. American Creek and Teuton

Resources each have a 1/5th interest in the project. American Creek and

Teuton are both fully carried until such time as a Production Notice is

issued, at which time they are required to contribute their respective

20% share of development costs. Until such time, Tudor is required to

fund all exploration and development costs while both American Creek and

Teuton have “free rides”.

About American Creek

American Creek is a Canadian mineral exploration company with a

strong portfolio of gold and silver properties in British Columbia.

Three of those properties are located in the prolific “Golden Triangle”;

the Treaty Creek and Electrum joint venture projects with Tudor

Gold/Walter Storm as well as the 100% owned past producing Dunwell Mine.

The Corporation also holds the Gold Hill, Austruck-Bonanza, Ample

Goldmax, Silver Side, and Glitter King properties located in other

prospective areas of the province.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com

Posted by AGORACOM

at 2:10 PM on Monday, February 3rd, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged of 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits. Click Here For More Info

Gold is reporting its biggest monthly gain since August 2019.

January’s price rise has confirmed a resumption of the rally from lows seen in May 2019.

Safe haven flows and dovish Fed expectations could continue to push the yellow metal higher.

Gold has printed its biggest monthly gain in five months,

signaling a resumption of the rally from lows near $1,266 seen in May

2019.

The yellow metal is currently trading at a 4.00% gain from the

opening price of $1,517.70 observed on Jan. 2. That is the biggest

monthly price rise since August 2019. Back then, gold had rallied by

7.65%.

Haven flows

The US-Iran tensions escalated on Jan. 3, putting a strong

haven bid under gold. The yellow metal rose from $1,550 to a six-year

high of $1,611 in the five days to Jan. 8.

The break above $1,600 seen during the Asian trading hours on

Jan. 8 was short-lived, as tensions quickly eased after media outlets reported zero US casualties in Iran’s retaliatory attack on US bases in Iraq.

Gold fell back sharply to $1,550 on the same day and extended

losses to $1,536 by Jan. 14, before regaining poise on coronavirus

scare.

The mysterious Wuhan coronavirus spread quickly within China

during the second half of the month. Cases were also registered in Japan

and other Asian currencies and in the US and Europe. As a result, fear

gripped markets that China is struggling to contain the virus and it

could turn into a pandemic, derailing the global growth story.

Risk assets, therefore, took a beating and safe havens like gold, US treasuries, and yen found love.

Additionally, markets ramped up expectations for a Federal

Reserve rate cut by December and the central bank reinforced the dovish

expectations by reiterating its commitment to high inflation.

As a result, gold moved higher to $1,589 earlier Friday and is about to end the week with nearly 1 percent gain.

Looking forward, the coronavirus fears and the dovish Fed expectations could continue to push the yellow metal higher.

Many observers have revised lower their forecast for China’s first-quarter GDP

growth. For instance, Citigroup on Friday said it expects China’s GDP

growth to slow to 4.8% this quarter from 6.0% in the fourth quarter. It

cut its full-year forecast for 2020 to 5.5% from 5.8, according to

Bloomberg.

Further, analysts think the slowdown will force the Chinese

government and the People’s Bank of China to take action. Yields on

government bonds and currency usually drop with monetary easing, making the zero-yielding yellow metal look attractive.

As for next week, the focus will be on Caixin PMIs for China

and key US data releases – ISM Manufacturing and Non-Manufacturing data,

ADP report and the monthly Nonfarm Payrolls report.

Fed

rate cut expectations would strengthen, possibly yielding a stronger

rally in gold if the payrolls and wage growth figures disappoint

expectations.

Technical outlook

The metal traded in a sideways manner for four months, starting

from September to December. The range play has ended with a bullish

breakout with January’s 4% gain.

The range breakout indicates the rally from the low of $1,266 seen in May 2019 has resumed.

The next major resistance as per the monthly chart is $1,733. That level marks the 78.6% Fibonacci retracement of the sell-off from $1,920.94 to $1,046.54.

The daily chart is also biased bullish. Notably, the RSI is again looking north, having established support at 62.00.

The odds appear stacked in favor of a re-test of the high of $1,611 registered on Jan. 8.

The outlook would turn bearish if and when the daily chart RSI violates the support at 62.

Posted by AGORACOM

at 2:07 PM on Tuesday, January 28th, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged of 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits. Click Here For More Info

Excerpts from Crescat Capital November Newsletter:

Precious Metals

Precious metals are poised to benefit from what we consider to be the

best macro set up we’ve seen in our careers. The stars are all

aligning. We believe strongly that this time monetary policy will come

at a cost. Look in the chart below at how the new wave of global money

printing just initiated by the Fed in response to the Treasury market

funding crisis is highly likely to pull depressed gold prices up with

it.

The imbalance between historically depressed commodity prices

relative to record overvalued US stocks remains at the core of our macro

views. On the long side, we believe strongly commodities offer

tremendous upside potential on many fronts. Precious metals remain our

favorite. We view gold as the ultimate haven asset to likely outperform

in an environment of either a downturn in the business cycle, rising

global currency wars, implosion of fiat currencies backed by record

indebted government, or even a full-blown inflationary set up. These

scenarios are all possible. Our base case is that governments and

central banks will keep their pedals to the metal to attempt to fend off

credit implosion or to mop up after one has already occurred until

inflation becomes a persistent problem.

The gold and silver mining industry is precisely where we see one of

the greatest ways to express this investment thesis. These stocks have

been in a severe bear market from 2011 to 2015 and have been formed a

strong base over the last four years. They are offer and incredibly

attractive deep-value opportunity and appear to be just starting to

break out this year. We have done a deep dive in this sector and met

with over 40 different management teams this year. Combining that work

with our proprietary equity models, we are finding some of the greatest

free-cash-flow growth and value opportunities in the market today

unrivaled by any other industry. We have also found undervalued

high-quality exploration assets that will make excellent buyout

candidates.

We recently point out this 12-year breakout in mining stocks relative

to gold now looks as solid as a rock. In our view, this is just the

beginning of a major bull market for this entire industry. We encourage

investors to consider our new Crescat Precious Metals SMA strategy which

is performing extremely well this year.

Zero Discounting for Inflation Risk Today

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, if the global financial markets

cannot absorb the increase in Treasury debt, the Fed will be forced to

monetize it even more. The problem is that the Fed’s panic money

printing at this point in the economic cycle may hasten the unwinding of

the imbalances it is so desperate to maintain because it has perversely

fed the last-gasp melt up of speculation in already record over-valued

and extended equity and corporate credit markets. It is reminiscent of

when the Fed injected emergency cash into the repo market at the peak of

the tech bubble at the end of 1999 to fend off a potential Y2K computer

glitch that led to that market and business cycle top. After 40

years of declining inflation expectations in the US, there is a major

disconnect today between portfolio positioning, valuation, and economic

reality. Too much of the investment world is long the “risk parityâ€

trade to one degree or another, long stocks paired with leveraged long

bonds, a strategy that has back-tested great over the last 40 years, but

one that would be a disaster in a secular rising inflation environment.

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, rising long-term inflation, and

the hidden tax thereon, is the default, bi-partisan plan for the US

government’s future funding regardless of who is in the White House and

Congress after the 2020 elections. The market could start discounting

this sooner rather than later. The Fed’s excessive money printing

may only reinforce the unraveling of financial asset imbalances today as

it leads to rising inflation expectations and thereby a sell-off in

today’s highly over-valued long duration assets including Treasury bonds

and US equities, particularly insanely overvalued growth stocks. We

believe we are in the vicinity of a major US stock market and business

cycle peak.

-637160977007144981.png)

-637160977627630029.png)