Posted by AGORACOM

at 11:49 AM on Friday, March 20th, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged of 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits. Click Here For More Info

Credit Deflation and Gold

Gold and precious metals mining shares are casualties of panic

selling across all financial markets. The scenario is similar to what

happened in 2008 during the global financial crisis (GFC). When the

general selling exhausted itself in late 2008, gold and mining shares

delivered superior absolute and relative performance for the following

three years. We believe that this pattern is likely to repeat following

this sell-off.

While COVID-19 outbreak is grabbing the headlines, the far bigger

story is the deflation of financial assets that it has triggered and the

resulting loss of investment confidence. Markets that had been priced

for perfection must now reckon with a likely recession, soaring fiscal

deficits and the very real possibility of a sustained bear market.

In our opinion, even though the economy will recover from the

downturn and the health scare will prove to be temporary, financial

asset valuations are unlikely to return to pre-crash manic levels. In

mid-February, the Wilshire 5000 Stock Index1 traded at approximately

145% to gross domestic product (GDP),2 its second highest level since

1950, and only slightly below the 2000 peak (see Figure 1). At this

writing, the ratio has fallen to 114% (as of 3/17/2020), which is still

very expensive by historical standards. Valuations are driven by

investor psychology, leverage and the liquidity necessary to support

leverage. All three may have been critically impaired for the near to

intermediate term.

Figure 1. Total U.S. Corporate Equities and U.S. GDP (1950-2020)

If financial assets struggle, interest in gold is very likely to

widen. Gold may have been caught up in the recent stampede for

liquidity, but it has delivered good relative performance on a

year-to-date basis; gold bullion is up 0.73% as of March 17, compared to

-25.17% for the S&P 500 Index.3 The 12-month figures (as of

3/17/2020) are even more impressive: gold has returned 17.19% vs. -8.54%

for the S&P 500.

On a peak-to-trough basis for the last few weeks, gold has declined

roughly 12%. Other safe haven assets have experienced the same pressure.

For example, the yield on 30-year U.S. Treasury bond rose from less

than 1.0% to 1.5% in only a few days, a drawdown of more than 30%. What

this shows is that quality assets will be sold by portfolio managers

desperate to reduce leverage. Low-grade assets cannot be sold quickly

enough to meet margin calls.

It was leverage that inflated valuations, not fundamental economic

growth and strong year-over-year earnings. In fact, corporate pre-tax

profits have been declining since Q3 2014. Figure 2 shows pretax profits

on a quarterly basis since 2014.

Figure 2. U.S. Corporate Pre-Tax Profits Have Been Declining ($Billions)

The illusion of earnings growth that has captivated investor

psychology was achieved through share buybacks and increased leverage.

Growth of earnings per share, not the same as profit growth, has been

juiced by financial engineering. The same can be said for returns on

financial assets. The amount and location of leverage within the economy

and financial markets is opaque but may well have reached high tide for

many years. A post-recession economic recovery will not necessarily,

and does not have to, translate into strong returns from investing in

financial assets.

Global Debt Has Increased +100% Since 2007

In popular thinking, the current U.S. administration, or the one that

follows it, will pull every trick out of the bag to stimulate the

economy. This belief will likely excite investors from time to time in

anticipation of a rebound. Unfortunately, the financial markets are

experiencing a deflationary bust that could spread to general economic

activity. Public policy has all but exhausted the potential benefits of

resorting to traditional monetary and fiscal solutions. The marginal

benefit to economic growth from heaping on new layers of debt is capped

by the law of diminishing returns, as shown by Figure 4 from Rosenberg

Economics. Since 2007, global debt increased 110% vs. 46% for global

GDP:

Figure 3. Global Debt vs. Global GDP ($ Trillions)

Source: Rosenberg Economics. Data as of 12/31/2019.

Central banks have few conventional tools remaining to combat credit

deflation. An impotent response can be expected from new rounds of

monetary stimulus, rate reductions or central bank balance sheet

expansion. Global debt, public and private, measures 287% vs. global GDP

($244 trillion divided by $85 trillion). The debt burden will most

assuredly grow, a post coronavirus rebound notwithstanding. The world’s

debt structure is already incapable of withstanding even a minute rise

in rates. More debt relative to GDP will only make matters worse. All

that remains is currency destruction.

Gold has been rising for the past eighteen months side by side with a

strong stock market and no inflation. Conventional wisdom said that

wasn’t supposed to happen. As shown in Figure 4, gold has outperformed

equities and bonds since 2000, the dawn of radical monetary

experimentation by central bankers. We think gold has been sensing the

endgame for Keynesian policy prescriptions, mainstream economic thinking

and hyper-leveraged investment practices.

Figure 4. The Modern Era of Gold Gold Bullion vs. Stocks, Bonds, Oil, USD (2000-2020)

For the period from 12/31/1999 to 3/16/2020, gold has provided posted

an average annual return of 8.55%, compared to 5.44% for U.S. bonds,

4.44% for U.S. stocks, 0.57% for oil and -0.19% for the U.S. dollar.

Source: Bloomberg. Period from 12/31/1999 –3/16/2020.4

Gold Miners are Poised to Perform

During the 1930s credit deflation, gold and gold mining stocks

performed well in relative and absolute terms. When credit deflates, and

counterparties cannot be trusted, gold is the ultimate safe asset. In

the 1930s, the metal price rose, costs of producing gold declined and

the miners generated strong earnings and paid handsome dividends. We

believe that this is a sequence that will repeat.

At the moment, mining company valuations appear extraordinarily

cheap. It is one of the few industries that will report solid

year-over-year earnings gains for the remainder of this year and perhaps

into the next.

Buying low is never easy but now is the time to do it.

Posted by AGORACOM

at 9:38 AM on Wednesday, March 4th, 2020

P&E Mining Consultants Inc. Provides Drill Hole Spacing Recommendation for the 2020 Drill Plan

Calculations include credit for previously analyzed values for Cu and Ag

Newly discovered NE Extension within the 300 Horizon. The gold-only result of 1.27 gpt Au over a 252 metre (m) interval increased to 1.51 gpt AuEq, an increase of 18.9%.

Cardston, Alberta–(Newsfile Corp. – March 4, 2020) – American Creek Resources Ltd. (TSXV: AMK) (the “Company”)

is pleased to announce the results of gold-equivalent (AuEq)

calculations for all drilling completed at JV partner Tudor Gold’s

(“Tudor”) flagship project Treaty Creek. These calculations include

credit for previously analyzed values for Cu and Ag. Geological analysis

and reinterpretation of all the drill holes to date exposed a new

copper horizon (CS 600 horizon) as well as significant silver and copper

mineralization throughout the Goldstorm system.

The strongest AuEq increase was seen in the newly discovered NE Extension within the 300 Horizon. The

gold-only result of 1.27 gpt Au over a 252 metre (m) interval increased

to 1.51 gpt AuEq (with 13.8 gpt Ag and 504 ppm Cu), an increase of

18.9%.

All drill holes at Goldstorm Zone had

significant increases to the composite results when the AuEq values for

the copper and silver mineralization were included however when the

drill holes intersected the CS-600 Horizon, the copper values within

this mineralized body had the greatest impact to an individual horizon

with up to 79.8% increase to the AuEq value from a gold-only 0.39 gpt Au over 150m to 0.70 gpt AuEq over the same 150m interval.

P&E Mining Consultants Inc. were

retained to assess all Goldstorm drill hole results and historical data

in order to render an opinion as to the consistency of the gold

mineralization as well to ascertain the recommended drill hole spacing

that would be required to potentially derive an Indicated Mineral

Resource and a Measured Mineral Resource. P&E Mining Consultants

Inc. concluded the following:

“Three dimensional continuity analyses

of the Treaty Creek drill hole assay results were carried out for the

Goldstorm Zone. The regional geological trend was used to guide the

selection of horizontal, across-strike, and dip-plane directions during

variogram fan analysis. Variogram fans were generated separately for Ag,

Au, Cu, Pb, and Zn uncapped composite samples in each zone.

All modeled semi-variograms display a

very low nugget effect, and display long range continuity down the

plunge of the mineralization and along the regional strike of the

deposits.

For the Goldstorm Zone, a drill spacing

of 200 m is recommended for Indicated Mineral Resources, and 100 m for

Measured Mineral Resources.”

Tudor’s goal is to design a diamond drill

hole program that will fast-track the exploration program for 2020 with

the objective to begin the Mineral Resource Estimate work as soon as

possible.

Vice President of Project Development Ken Konkin P.Geo. comments:

“We are very encouraged to see that the silver and copper

mineralization has made an important impact to the AuEq results from our

recent drilling as well as the historical drilling. The next step is to

plan the drill hole program for the 2020 exploration season. We

continue to work with our Mineral Resource Estimate geologists and

engineers from P&E Mining Consultants to plan the drill hole program

in order to optimize the drilling and to attempt to fast-track the

exploration program for this coming drill season

Table l provides gold equivalent composites from the 2019 drilling

and all historical drilling within the Goldstorm Zone. Table ll contains

the drill data including collar location, depth of drill holes as well

as the dip and azimuth for all drill hole.

TABLE l: Au Eq COMPOSITES GOLDSTORM ZONE

Section

HOLE ID

From

To

Interval (m)

AuEq g/t

Au g/t

Ag g/t

Cu ppm

% increase

Horizon

107+00 NE

CB-17-29

1.20

575.00

573.80

0.321

0.278

0.9

224

15.5%

300

107+00 NE

CB-17-29

60.50

333.50

273.00

0.435

0.392

1.1

197

11.0%

300

107+00 NE

CB-17-29

60.50

176.00

115.50

0.728

0.685

1.9

142

6.3%

300

107+00 NE

CB-18-32

196.50

783.50

587.00

0.542

0.497

1.6

177

9.1%

300 + CS600

107+00 NE

CB-18-32

196.50

316.50

120.00

1.082

1.045

1.7

106

3.5%

300

107+00 NE

CB-18-34

419.00

711.50

292.50

0.499

0.461

2.4

63

8.2%

300

107+00 NE

CB-18-34

831.50

897.50

66.00

0.290

0.221

1.3

361

31.2%

CS600

108+00 NE

CB-17-09

41.00

545.00

504.00

0.549

0.488

2.3

225

12.5%

300

108+00 NE

CB-17-09

41.00

200.00

159.00

0.782

0.708

2.9

261

10.5%

300

108+00 NE

CB-17-12

3.00

243.50

240.50

0.848

0.797

2.6

139

6.4%

300

108+00 NE

CB-17-12

33.00

224.00

191.00

0.979

0.923

3.0

134

6.1%

300

108+00 NE

CB-17-24

3.50

563.00

559.50

0.618

0.576

2.0

121

7.3%

300

108+00 NE

CB-17-24

62.00

275.00

213.00

1.018

0.945

3.9

180

7.7%

300

108+00 NE

CB-17-24

3.50

686.00

682.50

0.563

0.498

1.8

288

13.1%

300

108+00 NE

CB-18-36

659.50

772.00

112.50

0.487

0.454

1.8

74

7.3%

300

108+00 NE

CB-18-36

659.50

704.50

45.00

0.733

0.688

2.7

88

6.5%

300

108+00 NE

CB-18-36

682.00

703.00

21.00

1.101

1.035

4.6

79

6.4%

300

108+00 NE

CB-18-38

20.50

638.00

617.50

0.465

0.429

1.3

137

8.4%

300

108+00 NE

CB-18-38

248.50

353.00

104.50

0.733

0.639

3.4

360

14.7%

300

108+00 NE

CB-18-38

468.50

638.00

169.50

0.683

0.659

1.1

76

3.6%

300

108+00 NE

GS-19-40

23.00

350.00

327.00

0.501

0.443

1.72

251

13.1%

300

108+00 NE

GS-19-40

81.50

127.00

45.50

1.060

0.907

4.92

634

16.9%

300

108+00 NE

GS-19-41

27.50

353.00

325.50

0.724

0.589

5.25

480

22.9%

300

108+00 NE

GS-19-41

47.00

146.00

99.00

1.252

1.015

9.83

800

23.3%

300

109+00 NE

CB-16-03

88.00

708.00

620.00

0.582

0.534

1.5

202

9.0%

300

109+00 NE

CB-16-03

112.00

426.00

314.00

0.792

0.733

2.2

220

8.0%

300

109+00 NE

CB-17-04

152.10

327.00

174.90

0.827

0.803

1.0

76

3.0%

300

109+00 NE

CB-17-27

12.50

536.00

523.50

0.688

0.640

1.6

197

7.5%

300

109+00 NE

CB-17-27

12.50

350.00

337.50

0.807

0.758

2.0

169

6.5%

300

109+00 NE

CB-18-31

404.00

680.50

276.50

0.526

0.494

1.4

100

6.5%

300

109+00 NE

CB-18-31

481.00

597.00

116.00

0.773

0.732

1.8

124

5.6%

300

109+00 NE

CB-18-33B

599.00

623.00

24.00

0.435

0.367

5.4

22

18.5%

300

109+00 NE

GS-19-43

68.00

561.50

493.50

0.608

0.566

1.36

174

7.4%

300 + CS600

109+00 NE

GS-19-43

141.50

197.00

55.50

1.068

1.005

2.62

211

6.3%

300

109+00 NE

GS-19-43

405.50

561.50

156.00

0.785

0.718

1.50

325

9.3%

CS600

109+00 NE

GS-19-44

101.00

368.00

267.00

0.867

0.807

3.30

134

7.4%

300

109+00 NE

GS-19-44

125.00

275.00

150.00

1.143

1.065

4.62

151

7.3%

300

109+00 NE

GS-19-45

44.00

369.50

325.50

0.765

0.719

1.91

154

6.4%

300

109+00 NE

GS-19-45

62.00

278.00

216.00

0.947

0.901

2.27

122

5.1%

300

109+00 NE

GS-19-45

105.00

278.00

173.00

1.054

1.000

2.63

144

5.4%

300

109+00 NE

GS-19-46

34.50

628.50

594.00

0.550

0.510

1.31

165

7.8%

300 + CS600

109+00 NE

GS-19-46

175.50

337.50

162.00

0.778

0.734

1.93

135

6.0%

300

109+00 NE

GS-19-46

564.00

600.00

36.00

1.425

1.328

1.12

560

7.3%

CS600

110+00 NE

CB-17-06

182.50

589.50

407.00

0.767

0.675

3.1

369

13.6%

300

110+00 NE

CB-17-06

222.00

393.50

171.50

0.914

0.814

3.7

379

12.3%

300

110+00 NE

CB-17-07

99.50

530.00

430.50

0.697

0.625

2.4

293

11.5%

300

110+00 NE

CB-17-07

162.50

309.50

147.00

1.155

1.028

4.9

457

12.4%

300

110+00 NE

CB-18-37B

125.00

819.50

694.50

0.502

0.459

1.2

196

9.4%

300

110+00 NE

CB-18-37B

300.50

423.50

123.00

1.002

0.944

2.0

234

6.1%

300

110+00 NE

CB-18-37B

125.00

912.00

787.00

0.473

0.427

1.2

212

10.8%

300 + CS600

110+00 NE

GS-19-50

148.00

725.50

577.50

0.681

0.602

1.99

372

13.1%

300 + CS600

110+00 NE

GS-19-50

160.00

427.00

267.00

0.878

0.811

2.67

300

8.3%

300

110+00 NE

GS-19-50

652.00

736.00

84.00

0.816

0.571

2.53

1444

42.9%

CS600

110+00 NE

GS-19-51

119.00

365.00

246.00

0.777

0.722

2.31

187

7.6%

300

110+00 NE

GS-19-51

578.00

618.50

40.50

1.304

1.019

2.94

1693

28.0%

CS600

110+00 NE

GS-19-53

108.00

255.00

147.00

1.036

0.984

3.07

98

5.3%

300

111+00 NE

CB-18-39

141.50

705.30

563.80

1.086

0.981

4.4

352

10.7%

300

111+00 NE

CB-18-39

141.50

422.00

280.50

1.274

1.141

5.5

449

11.7%

300

111+00 NE

CB-18-39

539.00

695.00

156.00

1.247

1.154

4.6

257

8.1%

300

111+00 NE

GS-19-48

97.50

1024.50

927.00

0.793

0.677

3.00

543

17.1%

300 + CS600

111+00 NE

GS-19-48

97.50

426.00

328.50

1.152

1.048

4.30

354

9.9%

300

111+00 NE

GS-19-48

871.50

940.50

69.00

1.483

0.937

3.90

3364

58.3%

CS600

111+00 NE

GS-19-49

81.00

907.50

826.50

0.800

0.696

3.40

429

14.9%

300 + CS600

111+00 NE

GS-19-49

81.00

330.00

249.00

1.080

0.998

5.10

137

8.2%

300

111+00 NE

GS-19-49

483.00

606.00

123.00

1.042

0.941

1.80

538

10.7%

300

111+00 NE

GS-19-49

747.00

832.50

85.50

1.494

1.067

10.50

2035

40.0%

CS600

111+00 NE

GS-19-52

62.00

663.50

601.50

0.783

0.668

3.25

513

17.2%

300 + CS600

111+00 NE

GS-19-52

62.00

398.00

336.00

1.062

1.004

2.65

182

5.8%

300

111+00 NE

GS-19-52

513.50

663.50

150.00

0.703

0.391

6.49

1583

79.8%

CS600

112+50 NE

GS-19-42

63.50

843.50

780.00

0.849

0.683

5.80

650

24.3%

300 + CS600

112+50 NE

GS-19-42

63.50

434.00

370.50

1.275

1.097

10.00

393

16.2%

300

112+50 NE

GS-19-42

63.50

315.50

252.00

1.508

1.268

13.80

504

18.9%

300

112+50 NE

GS-19-42

717.70

843.50

125.80

0.902

0.522

3.80

2253

72.8%

CS600

114+00 NE

GS-19-47

117.50

1199.00

1081.50

0.697

0.589

3.40

450

18.3%

300 + CS600 + DS

114+00 NE

GS-19-47

200.00

501.50

301.50

0.867

0.828

2.10

96

4.7%

300

114+00 NE

GS-19-47

665.00

816.50

151.50

1.009

0.572

8.90

2228

76.4%

CS600

114+00 NE

GS-19-47

933.50

1176.50

243.00

0.996

0.908

4.80

207

9.7%

DS

* All assay grades are uncut and intervals reflect drilled intercept

lengths. True widths have not been determined as the mineralized body

remains open in all directions. Further drilling is required to

determine the mineralized body orientation and true widths.

HQ and NQ2 diameter core samples were sawn in half and typically sampled at standard 1.5m intervals.

**Metal prices used to calculate the AuEq metal content are: Gold

$1322/oz, Ag: $15.91/oz, Cu: $2.86/lb. All metals are reported in USD

and calculations do not consider metal recoveries

The goal is to design a diamond drill hole program for the 2020

exploration program with the objective to begin the Mineral Resource

Estimate work at the end of the 2020 field season. Tudor hopes to

accomplish as much drilling needed to bring a Measured and Indicated

Mineral Resource Estimate forward as quickly as possible.

Walter Storm, President and CEO, stated: “These

new gold equivalents are extremely encouraging as our technical team

continues to take positive steps advancing Tudor Gold’s flagship Treaty

Creek Au-Ag-Cu project. Furthermore we received good news from P&E

Mining Consultants Inc. that the drill hole spacing required to derive a

Measured Resource is 100 meters due to the homogenous nature of the

AuEq composites obtained to-date. During the new few weeks, our

geologist and engineers will continue to work with the geological model

and begin to prepare the diamond drill hole proposal for 2020.”

The Treaty Creek Project is a Joint Venture with Tudor Gold owning

3/5th and acting as operator. American Creek and Teuton Resources each

have a 1/5th interest in the project. American Creek and Teuton are both

fully carried until such time as a Production Notice is issued, at

which time they are required to contribute their respective 20% share of

development costs. Until such time, Tudor is required to fund all

exploration and development costs while both American Creek and Teuton

have “free rides”.

QA/QC

Drill core samples were prepared at MSA Labs’ Preparation Laboratory

in Terrace, BC and assayed at MSA Labs’ Geochemical Laboratory in

Langley, BC. Analytical accuracy and precision are monitored by the

submission of blanks, certified standards and duplicate samples inserted

at regular intervals into the sample stream by Tudor Gold personnel.

MSA Laboratories quality system complies with the requirements for the

International Standards ISO 17025 and ISO 9001. MSA Labs is independent

of the Company.

Qualified Person

The Qualified Person for this news release for the purposes of

National Instrument 43-101 is the Company’s Vice President of Project

Development, Ken Konkin, P.Geo. He has read and approved the scientific

and technical information that forms the basis for the disclosure

contained in this news release.

About American Creek

American Creek holds a strong portfolio of gold and silver properties

in British Columbia. The portfolio includes three gold/silver

properties in the heart of the Golden Triangle; the Treaty Creek and

Electrum joint ventures with Walter Storm/Tudor, as well as the recently

acquired 100% owned past producing Dunwell Mine. Other properties held

throughout BC include the Gold Hill, Austruck-Bonanza, Ample Goldmax,

Silver Side, and Glitter King.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Company is available on its website at www.americancreek.com

Posted by AGORACOM

at 3:47 PM on Thursday, February 13th, 2020

Gold will outperform the S&P 500 Index in 2020. That’s one of several projections made by CLSA in its just-released “Global Surprises 2020†report.

The Hong Kong investment firm has an impressive track record when it comes to making market predictions—last year it had a 70 percent hit rate—so it may be prudent to take this one seriously.

CLSA’s

head of research Shaun Cochran: “If investors are concerned about the

role of liquidity in recent equity market strength… gold provides a

hedge that could perform across multiple scenarios.â€

Indeed, gold is one of the most liquid assets in the world with an average daily trading volume of more than $112 billion,

according to the World Gold Council (WGC). That far exceeds the Dow

Jones Industrial Average’s daily volume of approximately $23 billion.

The

yellow metal, Cochran adds, can be particularly useful in an era of

perpetually loose monetary policy: “[I]n the event that growth

disappoints the market’s expectations, gold is positively leveraged to

the inevitable policy response of lower rates and larger central bank

balance sheets.â€

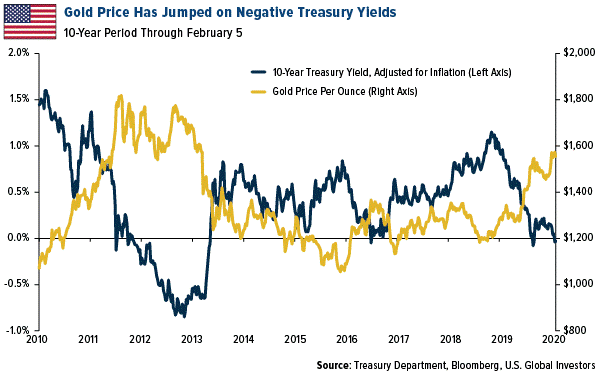

As

I’ve pointed out many times before, gold has traded inversely with

government bond yields. The recent gold rally has largely been driven by

the growing pool of negative-yielding government debt around the world,

now standing at $13 trillion. Here in the U.S., the nominal yield on

the 10-year Treasury has remained positive, but when adjusted for

inflation, it’s recently turned negative, despite a strengthening

economy. What’s more, the Federal Reserve’s balance sheet has begun to

increase again. It now holds about 30 percent of outstanding Treasury

debt, up from about 10 percent prior to the financial crisis.

I

can’t say whether gold will beat the S&P this year or next, but

what I do know is that the yellow metal has been a wise long-term

investment. For the 20-year period through the end of 2019, gold crushed

the market two-to-one, returning 451.8 percent compared to the

S&P’s 223.6 percent. That comes out to a compound annual growth rate

(CAGR) of 8.78 percent for gold, 4.03 percent for the S&P.

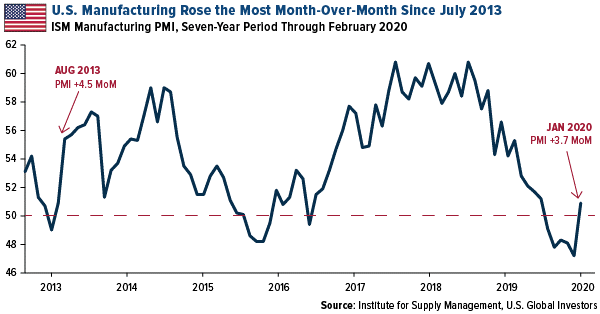

Manufacturing Turnaround Has Begun

U.S.

manufacturers started 2020 on stronger footing, a welcome turnaround

after contracting for five straight months. January’s ISM manufacturing

purchasing manager’s index (PMI) clocked in at 50.9, indicating slight

growth. Up from 47.2 in December, this represents the biggest

month-over-month jump since August 2013, when the PMI increased to 55.4

from 50.9 in July.

This

may also mark the end of the recent manufacturing bear market, prompted

by the trade war between the U.S. and China. Although relations between

the world’s two biggest superpowers remain strained, to say the least,

we’ve seen improvements lately that hint at better days. Both sides

signed a “Phase One†agreement in mid-January, and last week, China

announced it would be cutting tariffs in half on as much as $75 billion

of U.S.-imported products.

The

coronavirus is a new development that has disrupted global trade, but

there’s reason to be optimistic, as the PMI makes clear.

To read my full comments on the coronavirus, and its impact on Chinese and Hong Kong stocks, click here!

The

Dow Jones Industrial Average is a price-weighted average of 30 blue

chip stocks that are generally leaders in their industry. The S&P

500 Stock Index is a widely recognized capitalization-weighted index of

500 common stock prices in U.S. companies. The Purchasing Manager’s

Index is an indicator of the economic health of the manufacturing

sector. The PMI index is based on five major indicators: new orders,

inventory levels, production, supplier deliveries and the employment

environment. Compound annual growth rate (CAGR) is a business and

investing specific term for the geometric progression ratio that

provides a constant rate of return over the time period.

All

opinions expressed and data provided are subject to change without

notice. Some of these opinions may not be appropriate to every investor.

Some links above may be directed to third-party websites. U.S. Global

Investors does not endorse all information supplied by these websites

and is not responsible for their content.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC. This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Posted by AGORACOM

at 1:16 PM on Friday, February 7th, 2020

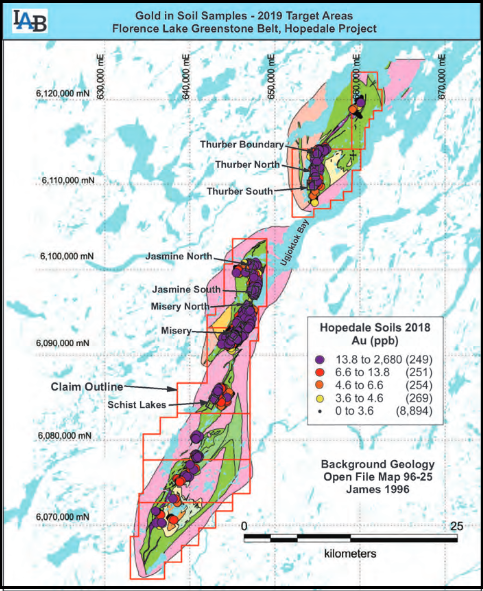

SPONSOR: Labrador Gold – Two successful gold

explorers lead the way in the Labrador gold rush targeting the

under-explored gold potential of the province. Exploration has already

outlined district scale gold on two projects, including a 40km strike

length of the Florence Lake greenstone belt, one of two greenstone belts

covered by the Hopedale Project. Click Here for More Info

Labrador Gold: District Scale Discovery Potential

First stage drilling on selected targets in 2020 at Hopedale

Large under-explored properties, including the major portion of two greenstone belts

Potential for discovery of new gold district(s)

Experienced exploration success in finding gold deposits (>17 million oz)

First mover advantage

Results of aggressive initial exploration programs already indicate district scale gold targets

Hopedale Project Highlights:

Discovered a new gold showing north of the Thurber Dog gold

occurrence, grab samples from which assayed between 1.67 and 8.26 g/t

Au.

The Thurber Dog gold occurrence has assays in grab and channel

samples from below detection up to 7.866 g/t Au, with 5 samples greater

than 1 g/t Au and 16 samples assaying greater than 0.1 g/t Au.

The discovery extends the potential strike length of gold mineralization by approximately 500 metres along strike to the north.

The new showing occurs within a larger 3km trend of anomalous gold

in rock and soil associated with the contact between mafic/ultramafic

volcanic rocks and felsic volcanic rocks.

Exploration at Hopedale during 2020 will focus on determining the

extent of the Thurber Dog mineralized trend. Such work would aim to fill

in the gaps between showings over the three-kilometre strike length

with sampling and VLF-EM surveys. LabGold also intends to carry out an

initial drill program targeting prospective areas along this trend,

including the new showing.

The Hopedale property covers much of the Hunt River and Florence

Lake greenstone belts that stretch over 80 km. The belts are typical of

greenstone belts around the world but have been underexplored by

comparison. Initial work by Labrador Gold during 2017 show gold

anomalies in soils and lake sediments over a 3 kilometre section of the

northern portion of the Florence Lake greenstone belt in the vicinity of

the known Thurber Dog gold showing where grab samples assayed up to

7.8g/t gold. In addition, anomalous gold in soil and lake sediment

samples occur over approximately 40 kilometres along the southern

section of the greenstone belt (see news release dated January 25th 2018

for more details). Labrador Gold now controls approximately 57km strike

length of the Florence Lake Greenstone Belt.

FULL DISCLOSURE: Labrador Gold is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM

at 5:42 PM on Friday, January 31st, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

We believe that there is a strong case to expect gold mining shares to outperform the metal in the years ahead…

On September 17, 2019, overnight repo rates spiked 121 basis points,

climbing from 2.19% to 3.40%, providing yet another crucial buttress for

the bullish rationale for gold. The spike signaled that the U.S.

Federal Reserve (“Fedâ€) had lost control of the price of money. Without

subsequent massive injections of liquidity by the Fed into the repo

market, out of control, short-term interest rates would have undermined

the leverage that underpins record financial asset valuations. Going

forward, unless the Fed continues to expand its balance sheet, it risks a

meltdown in equity and bond prices that could exceed the damage of the

2008 global financial crisis. Despite consensus expectations, there

appears no escape from this treadmill.

The Fed must monetize deficits because non-U.S. investors are no

longer absorbing the growing supply of U.S. debt. Ultra-low, short-term

interest rates do not compensate foreign investors for the cost of

hedging potential foreign currency (FX) losses (see Figure 1). The U.S.

fiscal deficit is too high and the issuance of new U.S. treasuries is

too great for the market to absorb at such low interest rates. In a free

market, interest rates would rise, the economy would stall and

financial asset valuations would decline sharply.

Figure 1. Treasury Issuance Goes Up, Foreign Purchases Go Down (2010-2019)

Source: Bloomberg. Data as of 12/31/2019.

The predicament facing monetary policy explains why central banks are

buying gold in record quantities, as shown in Figure 2. It also

explains the fourth quarter “melt-up†in the equity market, even with Q4

earnings that are likely to be flat to down versus a year ago (marking

the second quarter in a row for lackluster results) and the weakest

macroeconomic landscape since 2009 (as shown by Figure 3).

Figure 2. Central Banks Purchases of Gold are 12% Higher than Last Year

Source: World Gold Council; Metals Focus; Refinitiv GFMS. Data as of 9/30/2019.

Figure 3. The U.S. ISM PMI Index Indicates Economic Contraction

The U.S. ISM Manufacturing Purchasing Managers Index (PMI)1 ended the

year at 47.2, indicating that the U.S. economy is in contraction

territory (a reading above 50 indicates expansion, while a reading below

50 indicates contraction).

Source: Bloomberg. Data as of 12/31/2019.

Liquidity injections will result in more debt, both public and private sector, but not necessarily enhanced economic growth:

“As these forms of easing (i.e., interest

rate cuts and QE [quantitative easing]) cease to work well and the

problem of there being too much debt and non-debt liabilities (e.g.,

pension and healthcare liabilities) remains, the other forms of easing

(most obviously currency depreciations and fiscal deficits that are

monetized) will become increasingly likely …. [this] will reduce the

value of money and real returns for creditors and will test how far

creditors will let central banks go in providing negative real returns

before moving into other assets [including gold].â€

– Ray Dalio, Paradigm Shifts, Bridgewater Daily Observations, 7/15/2019

Gold Bullion and Miners Shine in 2019

Though overshadowed by the rip-roaring equity market, precious metals

and related mining equities also had significant gains in 2019 (up

43.49%)2. Gold’s 18.31% rise last year was its strongest performance

since 2016. More significantly, after two more years of range-bound

trading, the metal closed out 2019 at its highest level since mid-2013,

and within striking distance of $1,900/oz, the all-time high it reached

in 2011.

The investment world has taken little notice. Despite gold’s strong

performance, GDX3, the best ETF (exchange-traded fund) proxy for

precious metals mining stocks, saw significant outflows over the year as

shares outstanding declined from 502 million to 441 million (or 12%)

over the twelve months, despite posting a 39.73% gain, well ahead of the

31.49% total return for the S&P 500 Total Return Index.4

We believe that there is a strong case to expect gold mining shares to outperform the metal in the years ahead…

It has been our long-held view that until mainstream investment

strategies run aground, interest in precious metals will continue to

simmer on low, notwithstanding the likelihood that 2020 may be another

very good year for the precious metals complex. The many reasons why

mainstream investment strategies could unravel are not difficult to

imagine. They include the emergence of meaningful inflation, further

slippage of the U.S. dollar’s nearly exclusive reserve currency status,

and market-driven interest rate increases or a recession. Any or all of

these could disrupt the continued expansion of the Fed’s balance sheet,

triggering a rapid reversal in financial asset valuations. Each

possibility deserves a more complete discussion than space here allows,

but evidence strongly suggests that none can be ruled out. While timing

the zenith in complacency is risky, we feel confident that a reversal of

fortune for high financial asset valuations awaits unsuspecting

investors sooner than they expect.

We are even more confident that a bear market will generate far

broader investment interest in gold. Considering that institutional

exposure to gold and related mining stocks hovers near multi-decade

lows, the slightest uptick could easily drive the metal and related

precious metals mining shares to historic highs. Today, the aggregate

market capitalization of precious metals equity shares is $400 billion,

an insignificant speck on the current market landscape.

Investors outflows from precious metals mining stocks in 2019, even

as gold rose 18.31%, suggests skepticism that the current rally is

sustainable — perhaps hardened by the wounds of years of middling

performance. Contrarian analysis would regard such bearishness as

grounds to be very bullish. In our opinion, investors have overlooked

that the 2019 rise in gold prices has restored financial health to

sector balance sheets, earnings and cash flow. Gold stocks offer both

relative and absolute fundamental value and growth potential that

compares very favorably to conventional investment strategies

We believe that there is a strong case to expect gold mining shares

to outperform the metal in the years ahead by a substantially wider

margin than they outperformed in 2019. With continued advances in

precious metals prices, the return potential from these still unloved

orphans and pariahs of the investment universe should prove to be very

compelling.

Posted by AGORACOM

at 11:58 AM on Wednesday, January 22nd, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

At first glance gold looks like it may be about to advance out of a

bull Flag, but there are a number of factors in play that we will

examine which suggest that any near-term advance won’t get far before it

turns and drops again, and that a longer period of consolidation and

perhaps reaction is necessary before it makes significant further

progress.

On the 6-month chart we can see how gold stabbed into a zone of

strong resistance on the Iran crisis around the time Iran’s General was

murdered, but after a couple of bearish looking candles with high upper

shadows formed, it backed off into what many are taking to be a bull

Flag.

The 10-year chart makes it plain why gold is vulnerable here to

reacting back over the short to medium-term, because it has advanced

deep into “enemy territory†– the broad band of heavy resistance

approaching the 2011 highs, with a zone of particularly strong

resistance right where it is now. It would be healthier and increase

gold’s chances of breaking out to new highs if it now backed off into a

trading range for a while to moderate what now looks like excessive

bullishness.

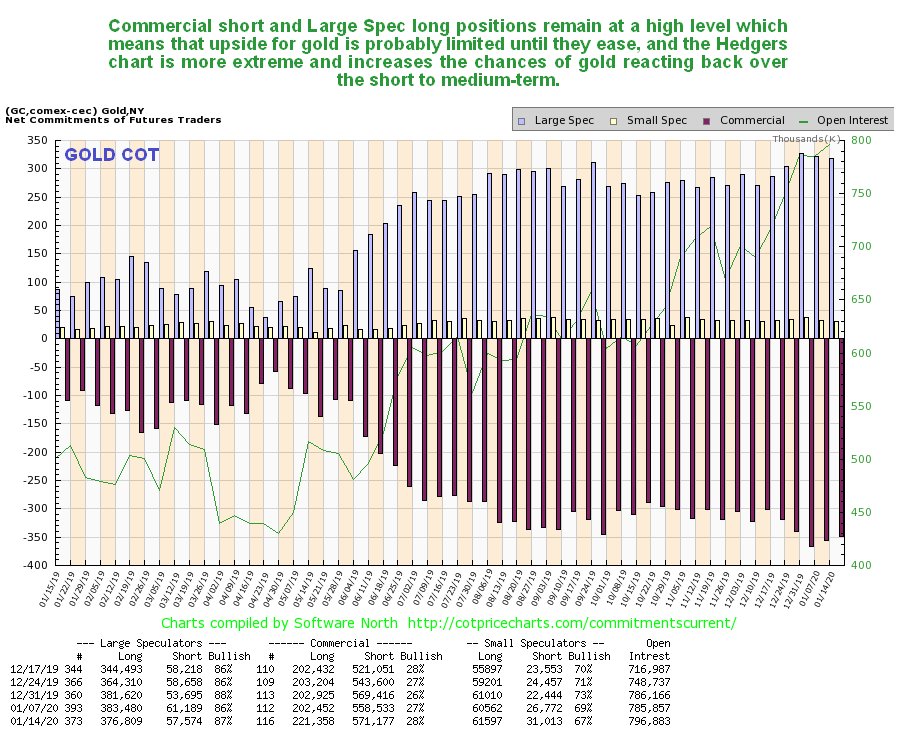

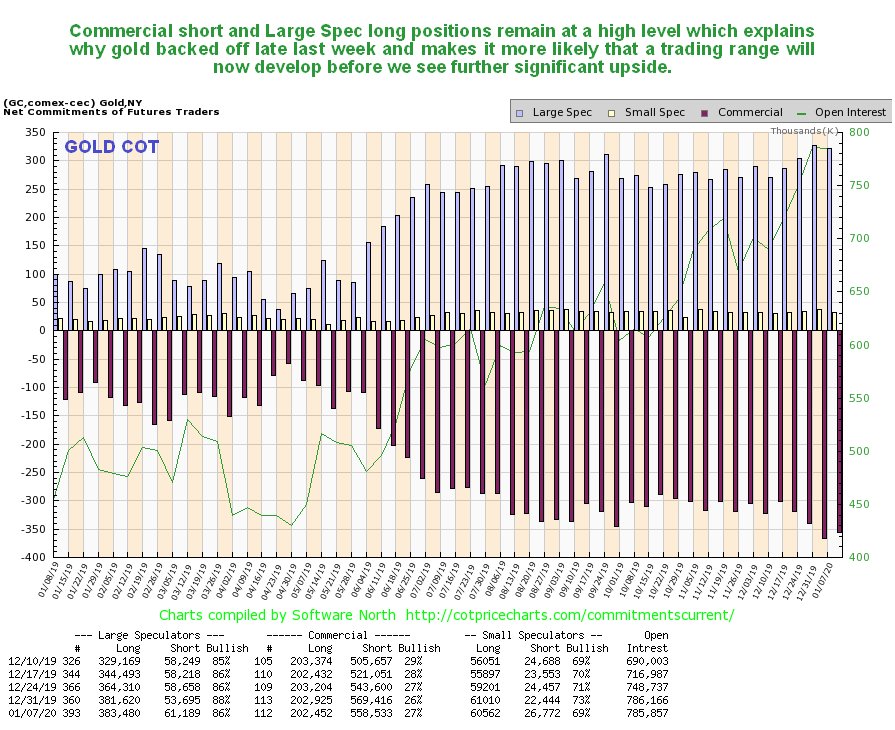

Thus it remains a cause for concern (or it should be for gold

bulls) to see gold’s latest COTs continuing to show high Commercial

short and Large Spec long positions. Is it “going to be different this

time� – the latest Hedgers charts that we are now going to look at

suggest not.

Click on chart to popup a larger, clearer version.

The COT chart only goes back a year. The Hedgers charts shown

below, which are a form of COT chart, go back many years, and frankly,

they look pretty scary.

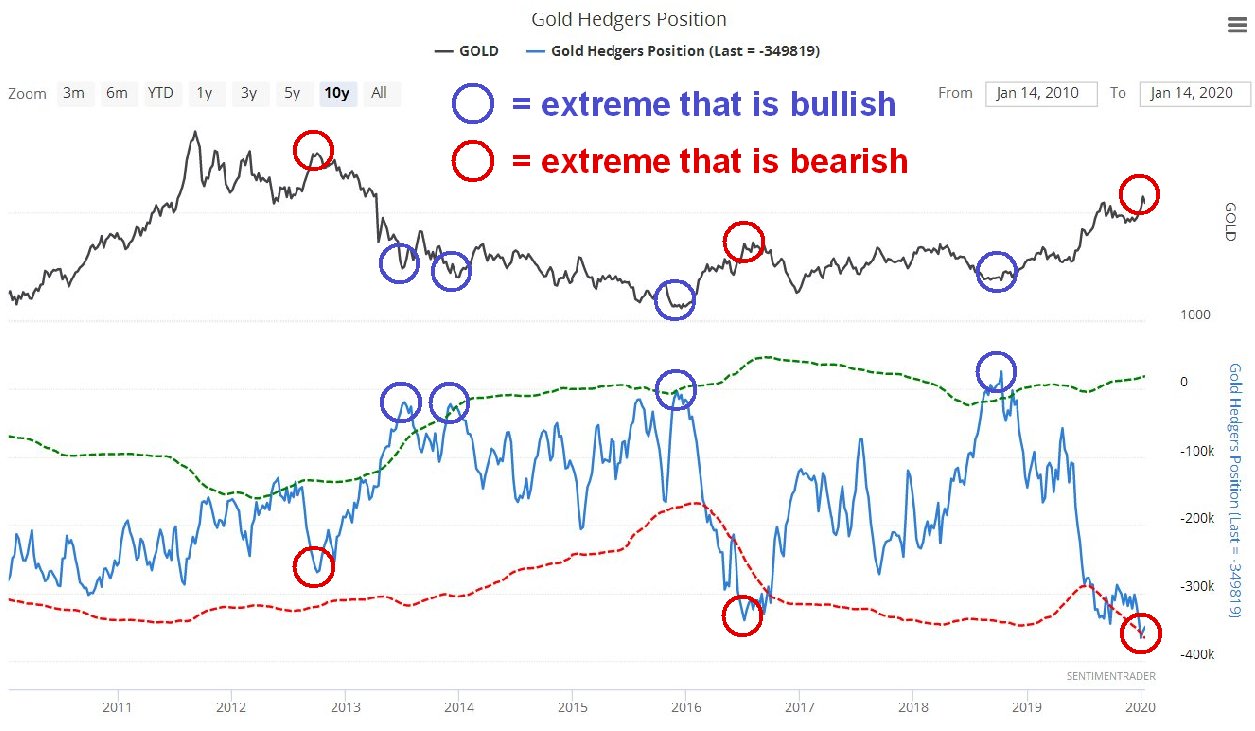

We’ll start by looking at the Hedger’s chart that goes back to before

the 2011 sector peak. On it we see that current Hedgers positions are

at extremes that way exceed even those at the peak of the 2012 sucker

rally, which was followed by the bulk of the decline in the bearmarket

that followed. Does this mean that we are going to see another

bearmarket like that – no it doesn’t, but it does mean that these

positions will probably need to moderate before we see significant

further gains.

Click on chart to popup a larger, clearer version.

Chart courtesy of sentimentrader.com

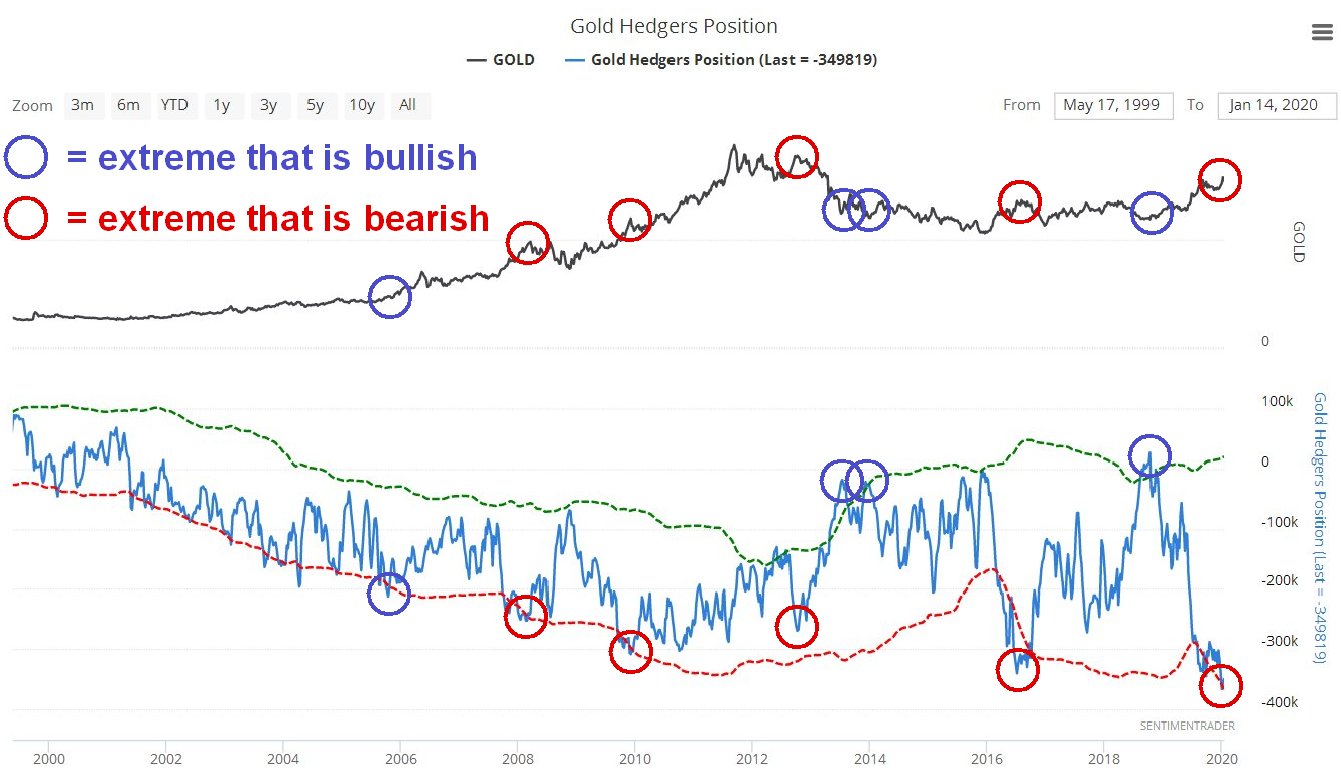

Looking at the Hedgers chart going way back to before the year

2000, we see that the current readings are record readings by a

significant margin and obviously increase the risks of a sizeable

reaction. We can speculate about what the reasons for a decline might

be, one possibility being the sector getting dragged down by a

stockmarket crash after its blowoff top, which may be imminent, as

happened in 2008, since it remains to be seen whether investors will

rush into the sector as a safe haven in the event of a market crash.

Click on chart to popup a larger, clearer version.

Chart courtesy of sentimentrader.com

Turning now to Precious Metals stocks, we see on its latest

10-year chart that GDX still looks like it is completing a giant

Head-and-Shoulders bottom pattern. However, it is currently dithering

just beneath resistance at the top of this base pattern, which means

that it is vulnerable to backing off.

So, how then does gold stock sentiment look right now? As we can

see on the 5-year chart for the Gold Miners’ Bullish Percent Index,

bullishness towards the sector is now at a very high level, 84.6%, which

makes it more likely that stocks will drop soon rather than rally, and

what they could do of course is rally some to increase this level of

bullishness still further, and then drop.

Does all this mean that investors in the sector should suddenly

rush for the exits? No, it doesn’t, especially as the charts for many

individual stocks across the sector look very bullish, and it may be

that all that is needed is a cooling period of consolidation. However it

does make sense to use Hedges at extremes, such as leveraged inverse

ETFs and better still options as insurance, which have the advantage of

providing protection for a very small capital outlay, a fine example

being GLD Puts which are liquid with narrow spreads. We did this just ahead of the recent peak

when Iran lobbed a volley of missiles at Iraq. We will not be selling

our strongest gold and silver stocks, but instead look to buy more on

dips.

Posted by AGORACOM

at 4:36 PM on Friday, January 17th, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

From the HRA Journal: Issue 314

The fun doesn’t stop. Waves of liquidity continue to wash traders

cares away. Even assassinations and war mongering generate little more

than half day dips on Wall St. It seems nothing can get in the way of

the bull rally that’s carrying all risk assets higher.

It feels like it could go on for a while, though I think the

liquidity will have to keep coming to sustain it. By most readings,

bullishness on Wall St is at levels that are rarely sustained for more

than a few weeks. Some sort of correction on Wall St seems highly

likely, and soon. Whether its substantial or just another blip on the

way higher remains to be seen.

The resource sector, especially gold and silver stocks, have had

their own rally. Our Santa Claus market was as good or better than Wall

St’s for a change. And I don’t think its over yet. I think we’re in for

the best Q1 we’ve seen for a few years. And we could be in for something

better than that even. I increasingly see signs of a major rally

developing in the gold space. It’s already been pretty good but I think a

multi-quarter, or longer, move may be starting to take shape.

I usually spend time on all the metals in the first issue of the

year. But, because the makings of this gold rally are complex and long

in coming I decided to detail my reasoning. That ended up taking several

pages so I’ll save talk on base metals and other markets for the next

issue.

No, I’m not writing about Louis IV, though there might be some

appropriateness to the analogy, now that I think about it. The quote is

famous, even though there’s no agreement on what it was supposed to

mean. Most figure Louis was referring to the biblical flood, that all

would be chaos once his reign ended.

The deluge I’m referring to isn’t water. It’s the flood of money the

US Fed, and other central banks, continue to unleash to keep markets

stable. Markets, especially stock markets, love liquidity. You can see

the impact of the latest deluge, particularly the US Fed’s in the chart

below that traces both the SPX index value and the level of a “Global

Liquidity Proxy†(“GLPâ€) measuring fiscal/monetary tightness and

weakness.

You can see the GLP moved lower in late 2018 as the Fed tightened and

the impact that had on Wall St. Conversely, you can see the SPX running

higher in the past couple of months as the US backed off rate

increases, increased fiscal deficit expansion, and grew the Fed balance

sheet through, mainly, repo market operations.

Wall St, and most other bourses, are loving these money flows. The

Santa Claus rally discussed in the last issue continued to strengthen

all the way to and through year end. As it turned out, the Fed either

provided enough backstop in advance or the yearend repo issues were

overstated. The repo market itself was calm going through year end and a

lot of the short-term money offered by the Fed during that week wasn’t

taken down.

Everything may have changed in the past couple of days with the

dramatic increase in US-Iran tensions. I don’t know how big an issue

that will be, since no one knows what form Iran’s retaliation will be or

how much things will escalate. I DO think it’s potentially a big deal

with very negative connotations, but it may take time to unfold. Someone

at the Fed thought so too, as the past couple of days saw a return to

large scale Fed lending in the repo market.

I’ve no doubt Iran will try and take revenge for the assassination of

its most famous military commander by the US. But I don’t know what

form it will take and if this means the US has drawn itself into the

Mideast quagmire even more. I fear it has though. The US is already

talking about adding 3,000 troops to its Mideast presence and they’re

just warming up. Even larger scale attacks, if they happen, may not

derail Wall St, but they’re certainly not a positive development at any

level.

We know how stretched both market valuations and sentiment were

before the Suleimani drone strike. The chart below shows a three-year

trace of the “fear/greed indexâ€. You can see that its hardly a stable

reading. It flip flops often and extreme readings rarely hold for long.

At last check, the reading was 94% bullish.

Sentiment almost never gets that bullish and, when it does, nothing

good comes of it for bulls. A reading that close to 100% tells you we’re

just about out of buyers. Whatever happens in and around Iran, I think a

near term correction is inevitable. The only question is whether it’s a

large one or not.

A rapid escalation in US-Iran tensions could certainly make a near

term correction larger. If the flood of liquidity continues though, a

correction could just be another waystation on the road to higher highs.

There are a couple of other dangers Wall St still faces that I’ll touch

on briefly at the end of this article. First however, lets move on to

the main event for us-the gold market.

It wasn’t just the SPX enjoying a Santa rally this year. Gold

experienced the rally we were hoping for that gold miner stocks seemed

to be foretelling early last month. Gold’s been doing well since it

bottomed at $1275 in June, but it didn’t feel that way during the long

hiatus between the early September high and the current move. The gold

price currently sits above September’s multi-year high, after breaching

that high in the wake of the Baghdad drone strike. And the first

retaliatory strike by Iran. Volatility will be very high for a while

going forward.

I think we’ll see more multi-year highs going forward. I hate that

the latest move higher is driven by geopolitics. Scary geopolitics and

military confrontations mean people are dying. We don’t want to profit

from misery. And we won’t anyway, if things get ugly enough in the

Mideast to scare traders out of the market.

Geopolitical price moves almost always unwind quickly. I’d much

prefer to see gold moving higher for macro reasons, not as a political

safety trade. I expect more political/military inspired moves. As the

Iran conflict unfolds. Make no mistake, Iran is NOT Iraq. Its army is

far larger, better trained and better equipped than Iraq. This could get

ugly.

The balance of this piece will deal with my macro argument for higher

gold prices over an extended period. The geopolitical stuff will be

layered on top of that for the next while and could strengthen both gold

prices and the $US in risk-off trading. It should be viewed as a

separate event from the argument laid out below.

What else is driving gold higher? In part, it was gold’s inverse

relationship with the US Dollar. As you already know, I’m not a believer

that “its all about the USD, all the time†when it comes to the gold

market. That’s an over-simplification of a more complex relationship. It

also discounts the idea of gold as its own asset class that trades for

its own reasons.

If you look at the gold chart above, and the USD chart below it, its

immediately apparent that there isn’t a constant negative correlation at

play. Gold rallied during the summer at the same time the USD did and

for the same reason; the world-wide explosion of negative real yields.

Gold weakened a bit when yields reversed to the upside and the USD got a

bit of traction, but things changed again at the start of December.

The USD turned lower and lost two percent during December. US bond

yields were generally rising during the month and the market (right or

wrong) was assuming economic growth was accelerating. So, neither of

those items explains the USD weakness.

If gold was a “risk off†trade, you sure couldn’t see it in the way

any other market was trading. So, is there another explanation for

recent strength in the gold price, and what does it tell us about 2020

and, perhaps, beyond?

Well, I’ve got a theory. If I’m right, it could mean a bull run for gold has a long way to go.

Some of this theory will be no surprise to you because it does

partially hinge on further USD weakness. There are long term structural

reasons why the US currency should weaken. But there are also

fluctuating sources of demand for USDs, particularly from offshore

buyers and borrowers that transact in US currency. That can create

enough demand to strengthen the US over long periods. We just went

though one such period, but it looks like that may have come to an end,

with more bearish forces to the USD reasserting themselves.

How did we get here? Let’s start with the big picture, displayed on

the top chart on the next page. It gives a long-term view of US Federal

deficits and the unemployment rate. Normally, these travel in tandem.

Higher unemployment means more social spending and higher deficits.

Government spending expands during recessions and contracts-or should-

(as a percentage of GDP) during expansions. Classic Keynesian stuff.

You rarely see these two measures diverge. The two times they did

significantly before, on the left side of the chart, was due to “wartime

deficits†which acted (along with conscription) to stimulate the

economy and drive down unemployment.

You can see the Korean and Vietnam war periods pointed out on the chart.

The current period stands out for the extreme size of the divergence.

US unemployment rates are at multi decade lows and yet the fiscal

deficit as a percentage of GDP keeps rising. There has never been a

divergence this large and its due to get larger.

We know why this is. Big tax cuts combined with a budget that is

mostly non-discretionary. And the US is 10 years into an economic

expansion, however weak. Just think what this graph will look like the

next time the US goes into recession.

We can assume US government deficits aren’t going to shrink any time

soon (and I think we can, pun intended, take that to the bank). That

leaves trade in goods to act as a counterbalance to the funding demand

created by fiscal deficits.

The chart above makes it clear the US won’t get much help from

international trade. The US trade balance has been getting increasingly

negative for decades. It’s better recently, but unlikely to turn

positive soon, and maybe not ever.

To be clear, this is not a bad thing in itself, notwithstanding the

view from the White House. The relative strength of the US economy and

the US Dollar and cheaper offshore production costs have driven the

trade balance. It’s grown because Americans found they got more value

buying abroad and the world was happy to help finance it. It’s not a bad

thing, but not a US Dollar support either.

The more complete picture of currency/investment flows is given by

changes in the Current Account. In simplified terms, the Current Account

measures the difference between what a country produces and what it

consumes. For example, if a country’s trade deficit increases, so does

its current account deficit. If there are funds flowing in from overseas

investments on the other hand, this decrease the Current Account

deficit or increase the surplus.

The graph below summarizes quarterly changes in the US current

account. You can see how the balance got increasingly negative in the

mid 2000’s as both imports and foreign investment by US companies

increased.

Not coincidentally, this same period leading up to the Financial

Crisis included a sustained downtrend in the US Dollar Index. The USD

index chart on the bottom of the next page shows the scale of that

decline, from an index value of 120 at the start of 2002 all the way

down to 73 in early 2008.

The current account deficit (and value of the USD) improved markedly

up to the end of the Financial Crisis as money poured into the US as a

safe haven and consumers cut back on imports. The current account

deficit bas been relatively stable since then, running at about

$100bn/quarter until it dipped a bit again last year.

Trade, funds flows and changes in money supply have the largest

long-term impacts on currency values. When the US Fed ended QE and

started tightening monetary conditions in 2014, the USD enjoyed a strong

rally. The USD Index was back to 100 by early 2015 and stayed there

until loosening monetary conditions-and lots of jawboning from

Washington-led to pullback. Things reversed again and the USD maintained

a mild uptrend from early 2018 until now.

There are still plenty of US Dollar bulls around, and their arguments

have short-term merit. Yes, the US has higher real interest rates and

somewhat higher growth. Both are important to relative currency

valuations as I’ve said in the past. Longer term however, the “twin

deficits†-fiscal and current account-should underpin the fundamental

value of the currency.

Movements don’t happen overnight, especially when you’re talking

about the worlds reserve currency that has the deepest and largest

market supporting it. Changing the overall trend for the USD is like

turning a supertanker. I think it’s happening though, and it has big

potential implications for commodities, especially gold.

Dollar bulls will tell you the USD is the “cleanest shirt in the

laundry hamperâ€, referring to the relative strength of the growth rate

and interest rates compared to other major currencies. That’s true if we

just look at those measures but definitely not true when we look at the

longer term-fiscal and current account deficits.

In fact, the US has about the worst combined fiscal/current account deficit in the G7. The chart at the bottom of this page, from lynalden.com

shows the 2018 values for Current Account and Trade balances for a

number of major economies, as a percentage of their GDP. It’s not a

handsome group.

Both the trade and current account deficits are negative for most of

them. In terms of G7 economies, the US has the worst combined

Current/Trade deficit at 6% of GDP annually. You may be surprised to

note that the Current/Trade balance for the Euro zone is much better

than the US, thanks to a large Trade surplus. Much of that is generated

by Germany. Indeed, this chart explains Germanys defense of the Euro.

It’s combined Trade/Current Account surplus is so large it’s currency

would be skyrocketing if it still used the Deutschmark.

Because the current account deficit is cumulative, the overall

international investment position of the US has continued to worsen. The

US has gone from being an international creditor to an international

debtor, and the scale if its debt keeps increasing. That means it’s

getting harder every year to reverse the current account position as the

US borrows ever more abroad to cover its trade and fiscal deficits.

Interest outflows keep growing and investment inflows shrinking.

Something has to give.

The US has to borrow overseas, as private domestic demand for

Treasury bonds isn’t high enough to fund the twin deficits. In the past,

whenever the US Dollar got too high, offshore demand for US government

debt diminished. It’s not clear why. Maybe the higher dollar made

raising enough foreign funds difficult, or perhaps buyers started

worrying about the USD dropping after they bought when it got too

expensive. Whatever the reason, foreign holdings of US Treasuries have

been declining, forcing the US to find new, domestic, buyers.

Last year, the US Fed stopped its quantitative tightening program,

due to concerns about Dollar liquidity. Then came the repo market. Since

September, the Fed’s balance sheet has expanded by over $400 billion,

mainly due to repo market transactions.

The Fed maintains this “isn’t QE†because these are very short duration transactions but, cumulatively, the total Fed balance sheet keeps expanding. The “QE/no QE†debate is just semantics.

What do these transactions look like? Mostly, its Primary Dealers,

banks that also take part in Treasury auctions, in the repo market. The

Fed buys bonds, usually Treasuries, from these banks and pays for them

in newly printed Dollars. That injects money into the system, helps hold

down interest rates in the repo market and, not coincidentally,

effectively helps fund the US fiscal deficit. To put the series of

transactions in their simplest form, the US is effectively monetizing its deficit with a lot of these transactions.

The chart below illustrates the problem for the Primary Dealer US

banks. They’ve got to buy Treasuries when they’re auctioned-that is

their commitment as Primary Dealers. They also need to hold minimum cash

balances as a percentage of assets under Basel II bank regulations.

Cash balances fell to the minimum mandated level by late 2019- the

horizontal black line on the chart. That’s when the trouble started.

These banks are so stuffed with Treasuries that they didn’t have

excess cash reserves to lend into the repo market. Hence the blow up

back in September and the need for the Fed to inject cash by buying

Treasuries. The point, however, is that this isn’t really a “repo market

issueâ€, that’s just where it reared its head. It’s a “too many

Treasuries and not enough buyers†problem.

It will be tough for the Treasury to attract more offshore buyers

unless the USD weakens, or interest rates rise enough to make them

irresistible. Or a big drop in the federal deficit reduces the supply of

Treasuries itself.

I doubt we’ll see interest rates move up significantly. I don’t think

the economy could handle it and it would be self-defeating anyway, as

the government deficit would explode because of interest expenses. And

that’s not even taking into account the fact that President Trump would

be freaking out daily.

Based on recent history and political expediency, I’d say the odds of

significant budget deficit reductions are slim and none. That’s

especially true going into an election year. There’s just no way we’re

going to see spending restraint or tax increases in the next couple of

years. Indeed, the supply of Treasuries will keep growing even if the US

economy grows too. If there is any sort of significant slowdown or

recession the Federal deficit will explode and so will the new supply of

Treasures. Not an easy fix.

Barring new haven demand for US Treasuries, odds are the Fed will

have to keep sopping up excess supply. That means expanding its balance

sheet and, in so doing, effectively increasing the US money supply.

That brings us (finally!) to the “money shot†chart that appears

above. It compares changes in the size of the Fed balance sheet and the

US Dollar Index. To make it readable and allow me to match the scales, I

generated a chart that tracks annual percentage changes.

The chart shows a strong inverse correlation between changes in the

size of the Fed balance sheet and the value of the USD. This is

unsurprising as most transactions that expand the Fed balance sheet also

expand the money supply.

It’s impossible to tell how long the repo market transactions will

continue but, after three months, they aren’t feeling very “temporaryâ€.

To me, it increasingly looks like these market operations are “debt

monetization in dragâ€.

I don’t know if that’s the Fed’s real intent or just a side effect.

It doesn’t really matter if the funding and money printing continues at

scale. Even if the repo market calms completely, the odds are good we

see some sort of “new QE†start up. Whatever official reason is given

for it; I think it will happen mainly to soak up the excess supply of

Treasuries fiscal deficits are creating.

I don’t blame the FOMC if they’re being disingenuous about it. That’s

their job after all. If you’re a central banker, the LAST thing you’re

going to say is “our government is having trouble finding buyers for its

debtâ€, especially if its true.

With no prospect of lower deficits and apparent continued reduction

in offshore Treasury holdings, this could develop into long-term

sustained trend. I don’t expect it to move in a straight line, markets

never do. A severe escalation in Mideast tensions or the start of a

serious recession could both generate safe-haven Treasury buying. Money

flows from that would take the pressure off the Fed and would be US

Dollar supportive too.

That said, it seems the US has reached the point where a substantial

increase in its central bank’s balance sheet is inevitable. Both Japan

and the Eurozone have gotten there before the Fed, but it looks like it

won’t be immune.

The Eurozone at least has a “Twin surplus†to help cushion things.

And Japan, considered a basket case economically, had an extremely deep

pool of domestic savings (far deeper than the US) to draw on. Until very

recently, Japan also ran massive Current Account surpluses thanks to

decades of heavy investments overseas by Japanese entities. Those

advantages allowed the ECB and especially the BoJ to massively expand

their balance sheets without generating a huge run up in interest rates

or currency collapse.

I don’t know how far the US Fed can expand its balance sheet before

bond yields start getting away from it. I think pretty far though.

Having the world’s reserve currency is a massive advantage. There is

huge built in demand for US Dollars and US denominated debt. That gives

the Fed some runway if it must keep buying US Treasuries.

Assuming a run on yields doesn’t spoil the party, continued balance

sheet and money supply expansion should put increasing downward pressure

on the US Dollar. I don’t know if we’ll see a move as large as the

mid-2000s but a move down to the low 80s for the USD Index over the

course of two or three years wouldn’t be surprising.

It won’t be a straight-line move. A recession could derail things,

though the bear market on Wall St that would generate would support

bullion. Currency markets tend to be self-correcting over extended

periods. If the USD Index falls enough and there is a bump in US real

interest rates offshore demand for Treasuries should increase again.

The bottom line is that this is, and will continue to be, a very

dynamic system. Even so, I think we’ve reached a major inflection point

for the US currency. The 2000s were pretty good for the gold market and

gold stocks. We started from a much lower base of $300/oz on the gold

price. Starting at a $1200-1300 base this time, I think a price above

$2000/oz is a real possibility over the next year or two.

It’s not hard to extrapolate prices higher than that, but I’m not

looking or hoping for those. I prefer to see a longer, steadier move

that brings traders along rather than freaking them out.

This prediction isn’t a sure thing. Predictions never are. But I

think the probabilities now favor an extended bull run in the gold

price. Assuming stock markets don’t blow up (though I still expect that

correction), gold stocks should put in a leveraged performance much more

impressive than the bullion price itself.

There will be consolidations and corrections along the way, but I

think there will be many gold explorers and developers that rack up

share price gains in the hundreds of percent. That doesn’t mean buying

blindly and never trading. We still need to adjust when a stock gets

overweight and manage risk around major exploration campaigns. The last

few weeks has been a lot more fun in the resource space. I don’t think

the fun’s over yet. Enjoy the ride.

Like any good contrarian, a 10-year bull market makes me alert of

signs of potential trouble. As noted at the start of this editorial, I’m

expecting continues floods of liquidity. That may simply overwhelm

everything else for a while and allow Wall St to keep rallying, come

what may.

That said, a couple of data points recently got my attention. One is

more of a sentiment indicator, seen in the chart below. More than one

wag has joked that the Fed need only worry about Wall St, since the

stock market is the economy now. Turns out there is more than a bit of

truth to that.

The chart shows the US Leading Indicator reading with the level of

the stock market (which is a component of the official Leading

Indicator) removed. As you can see, without Wall St, the indicator

implies zero growth going forward. I’m mainly showing it as evidence of

just how surreal things have become.

The chart above is something to keep an eye on going forward. It

shows weekly State unemployment claims for several major sectors of the

economy. What’s interesting about this chart is that claims have been

climbing rapidly over the past few weeks. Doubly interesting is that the

increase in claims is broad, both within and across several sectors of

the economy.

I take the monthly Non-Farm Payroll number less seriously than most,

because it’s a backward-looking indicator. This move in unemployment

claims looks increasingly like a trend though. It’s now at its highest

level since the Financial Crisis.

It’s not in the danger zone-yet. But its climbing fast. We may need

to start paying more attention to those payroll numbers. If the chart

below isn’t a statistical fluke, we may start seeing negative surprises

in the NFP soon. That won’t hurt the gold price either.

Source and Thanks: https://www.hraadvisory.com/golds-big-picture

Posted by AGORACOM

at 4:33 PM on Monday, January 13th, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts `covered by the Hopedale Project. Click Here for More Info

It has been a week of surprises since the last updates were posted.

First, I had not expected Iran to retaliate following the murder of its

top General by a US drone, but it did, despite the risks, as it was

politically necessary to assuage the extreme anger of its population who

demanded revenge. The next surprise was that Israel and the US did not

use this retaliation as an excuse to bomb Iran back to the Stone Age,

which is what they really want to do. As we know, the long-term goal of

Israel and the US is to subjugate Iran, and they will not stop until

they attain this goal, and so it goes on. It appears that there was a

bit of theater involved in Iran’s retaliation, as it clandestinely

signaled its intentions which allowed US forces to get out of harm’s

way. Perhaps US forces did not then launch a blitzkrieg out of

consideration for this courtesy.

Regardless of the muddled and unpredictable fundamental situation,

which included the accidental downing of a passenger plane by Iranian

defensive missile batteries, the charts allowed us to make a reasonably

accurate prediction regarding what was likely to happen to the gold

price. The call for a near-term top in the PM sector made on the site on

Monday looked incorrect the following evening when gold suddenly surged

about $35 on news of the retaliatory Iranian missile strike, but when

it later became apparent that there were, strangely, no US troop

casualties and no further action against Iran, gold and silver reversed

dramatically and dropped quite hard as the tension then looked set to

ease, at least over the short-term. Technically what happened is that

gold pushed quite deep into heavy overhead resistance, becoming very

overbought at a time when COTs were showing extreme readings, and was

thus vulnerable to a sudden reversal. The action around this time

illustrates an important point, which is that when gold rises due to

sudden geopolitical developments, the gains tend not to stick – what

really matters and is the big driver for gold at this time is the insane

monetary expansion that is going on, which is being undertaken in a

desperate attempt to postpone the systemic implosion that is baked in

for as long as possible. As we have already observed in these updates in

recent weeks, gold is already in a raging bullmarket against a wide

variety of currencies, and it won’t be all that long before it’s in a

raging bullmarket against the dollar too, as the Fed sets the stage for

hyperinflation.

There are two big and compelling reasons for the US government to

tank the dollar. One is that it makes US exporters more competitive, and

the other is that it can use the mechanism of inflation to wipe clean

its colossal debts, by paying them off in devalued coin, printing vast

amounts of money to pay them off, in the process legally swindling the

foolish creditors out of their dues. This is precisely what the Weimar

Republic in Germany did in 1923 to eliminate the unfair reparations

imposed by the Treaty of Versailles, which were unfair also because

Germany didn’t start the 1st World War – it was tricked into it by the

allies, because the British Empire was scared of Germany’s rising

industrial and military might and wanted to destroy it, 100 plus years

of propaganda lies about Germany being responsible for the 1st World War

notwithstanding.

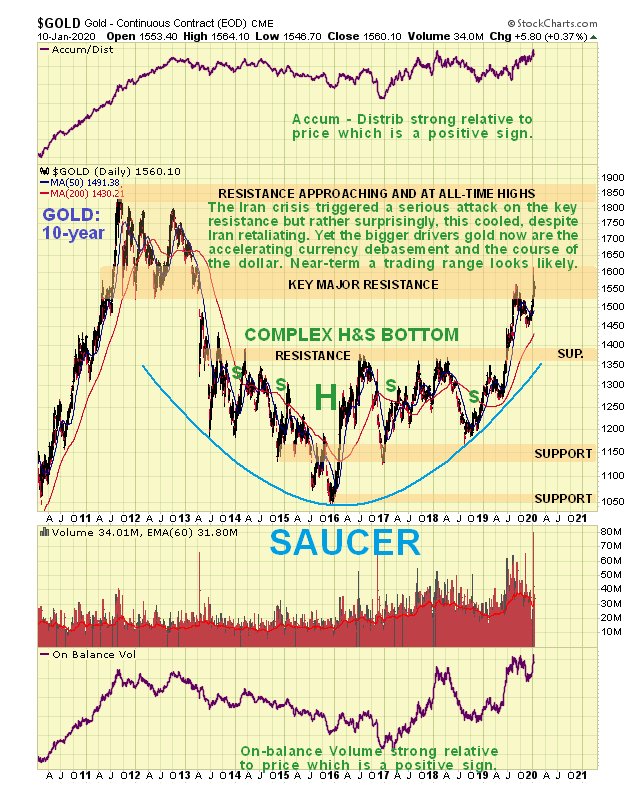

We’ll look at the dollar a little later. First we will review gold’s charts, starting with the 10-year chart.

On the 10-year chart we see that gold is now a bullmarket, even

against the dollar, and is currently challenging the heavy resistance

arising from the 2011 – 2013 top area. The second attack on this

resistance in the space of few months got further because of the Iran

crisis, and if this cools any more short-term, it will probably lead to

gold settling into a trading range before it mounts a more successful