Posted by AGORACOM

at 9:24 AM on Thursday, August 6th, 2020

TORONTO, Aug. 06, 2020 (GLOBE NEWSWIRE) — Labrador Gold Corp. (TSX-V: LAB | OTCQB: NKOSF) (“LabGold” or the “Company”) is pleased to announce that its field crew has arrived in Gander and started the 2020 exploration program on the Kingsway Property.

LabGold’s work program will initially focus on following up known gold anomalies identified from previous work on the three licenses. Soil sampling has begun on a high priority target that covers a 3km long anomaly of gold in heavy mineral concentrates with values from <5ppb to 89ppm (89g/t Au) that runs along the interpreted trace of the Appleton fault zone. Geological mapping and prospecting of anomalous areas and known showings is also underway.

Up to 10,000 soil samples and 250 km of ground magnetics/VLF-EM are planned for the property and are expected to take about six weeks to complete. We intend to hit the priority areas with known gold anomalies first so that the results of these surveys, together with the results of the geological mapping and prospecting can be used to plan a first phase fall drilling program.

Concurrently with the field work, we are working on a structural compilation of the district. This compilation will allow us to more efficiently target areas for detailed mapping and prospecting based on a better understanding of the role of primary and secondary structures on the localization of gold mineralization.

“It feels good to get boots on the ground at Kingsway which we believe to be the most strategically located property in the Gander gold district relative to New Found Gold’s recent discovery,” said Roger Moss, President and CEO. “Our focus on soil geochemistry and mag/VLF to define structures and potential alteration zones is consistent with what has worked well in the past and we expect to generate numerous targets along the major structures for drill testing.”

“It’s good to see the Kingsway Project moving along. Our limited 2019 deeper soil program over anomalous gold in till and vegetation samples proved successful in outlining new gold targets that will be followed up during this season’s work,” said Shawn Ryan, Technical Advisor to LabGold. “Based on last year’s success, the proposed larger 10,000 sample soil program covering existing gold in till and vegetation samples should produce some nice new gold anomalies leading to new drill targets.”

Roger Moss, PhD., P.Geo., is the qualified person responsible for all technical information in this release.

The Company gratefully acknowledges the Newfoundland and Labrador Ministry of Natural Resources’ Junior Exploration Assistance (JEA) Program for its financial support for exploration of the Kingsway property.

About Labrador Gold:

Labrador Gold is a Canadian based mineral exploration company focused on the acquisition and exploration of prospective gold projects in Eastern Canada.

In early March 2020, Labrador Gold acquired the option to earn a 100% interest in the Kingsway project in the Gander area of Newfoundland. The property is along strike to the northeast of New Found Gold’s discovery of 92.86 g/t Au over 19.0 metres on their Queensway property. (Note that mineralization hosted on adjacent or nearby properties is not necessarily indicative of mineralization hosted on the Company’s property). In early July 2020, the Company signed an option agreement to acquire a third license to add to the property package which now covers approximately 77 km2. The three licenses comprising the Kingsway project cover approximately 16km of the Appleton fault zone which is associated with gold occurrences in the region, including the New Found Gold discovery. Historical work over the area covered by the Kingsway licenses shows evidence of gold in till, vegetation, soil, stream sediments, lake sediments and float. Infrastructure in the area is excellent located just 18km from the town of Gander with road access to the project, nearby electricity and abundant local water.

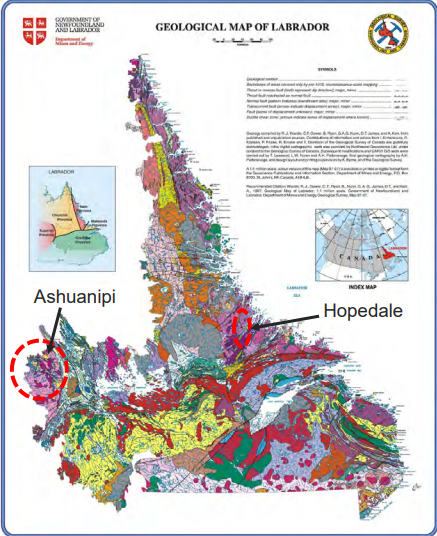

The Hopedale property covers much of the Hunt River and Florence Lake greenstone belts that stretch over 80 km. The belts are typical of greenstone belts around the world but have been underexplored by comparison. Initial work by Labrador Gold during 2017 show gold anomalies in soils and lake sediments over a 3 kilometre section of the northern portion of the Florence Lake greenstone belt in the vicinity of the known Thurber Dog gold showing where grab samples assayed up to 7.8g/t gold. In addition, anomalous gold in soil and lake sediment samples occur over approximately 40 kilometres along the southern section of the greenstone belt (see news release dated January 25th 2018 for more details). Labrador Gold now controls approximately 57km strike length of the Florence Lake Greenstone Belt.

The Ashuanipi gold project is located just 35 km from the historical iron ore mining community of Schefferville, which is linked by rail to the port of Sept Iles, Quebec in the south. The claim blocks cover large lake sediment gold anomalies that, with the exception of local prospecting, have not seen a systematic modern day exploration program. Results of the 2017 reconnaissance exploration program following up the lake sediment anomalies show gold anomalies in soils and lake sediments over a 15 kilometre long by 2 to 6 kilometre wide north-south trend and over a 14 kilometre long by 2 to 4 kilometre wide east-west trend. The anomalies appear to be broadly associated with magnetic highs and do not show any correlation with specific rock types on a regional scale (see news release dated January 18th 2018). This suggests a possible structural control on the localization of the gold anomalies. Historical work 30 km north on the Quebec side led to gold intersections of up to 2.23 grams per tonne (g/t) Au over 19.55 metres (not true width) (Source: IOS Services Geoscientifiques, 2012, Exploration and geological reconnaissance work in the Goodwood River Area, Sheffor Project, Summer Field Season 2011). Gold in both areas appears to be associated with similar rock types.

The Company has 91,584,175 common shares issued and outstanding and trades on the TSX Venture Exchange under the symbol LAB.

Posted by AGORACOM

at 11:01 AM on Monday, July 27th, 2020

Labrador Gold Corp. (TSX-V: LAB) (“LabGold” or the “Company”) is pleased to announce that it has received approval for mineral exploration on the Kingsway Property from the Department of Natural Resources, Newfoundland and Labrador. Receipt of the approval, which is good through July 22, 2021, means that the Company can now begin mobilizing field crews to Gander to kickstart its summer exploration program.

LabGold has planned a systematic exploration program that leverages its significant geochemical database to rapidly follow up known anomalies and generate drill targets. This will be done by a combination of soil sampling and magnetic/VLF-EM geophysical surveys on detailed grids over known anomalous areas. These include a 3km long anomaly of gold in heavy mineral concentrates with values from <5ppb to 89ppm (89g/t Au) within which a quartz vein boulder containing visible gold and assaying 168g/t Au was found. This anomaly runs along the interpreted trace of the Appleton fault zone and represents a high priority target.

Up to 10,000 soil samples and 250 km of magnetics/VLF-EM will be carried out on the property. The results of the surveys, together with detailed geological mapping will be used to plan a first phase drill program currently scheduled for the fall.

“We are excited to get the go ahead to carry out our proposed program at Kingsway,” said Roger Moss, President and CEO. “Due to our database and our research over the last four months we have a very good idea of where to focus our efforts to maximum effect to aggressively advance the Kingsway property to the drill stage. We anticipate an exciting field season exploring for Fosterville style gold mineralization in the Gander gold district.”

Exploration to date in the Gander district has shown the effectiveness of soil sampling to detect gold mineralization. Most of the known gold occurrences were discovered by following up gold in soil anomalies. It is also clear that mineralization in the district is structurally controlled as shown by the location of many of the known gold occurrences along the Appleton fault zone, a major crustal structure, and the secondary structures associated with it. The magnetic and VLF-EM survey will help define such cross-cutting structures that are often the focus of concentrated gold mineralization.

The Company also announces the grant of 3,150,000 options to the Company’s directors, officers and consultants. The options are exercisable at a price of $0.45 for a period of five years.

Roger Moss, PhD., P.Geo., is the qualified person responsible for all technical information in this release.

The Company gratefully acknowledges the Newfoundland and Labrador Ministry of Natural Resources’ Junior Exploration Assistance (JEA) Program for its financial support for exploration of the Kingsway property.

About Labrador Gold:

Labrador Gold is a Canadian based mineral exploration company focused on the acquisition and exploration of prospective gold projects in Eastern Canada.

In early March 2020, Labrador Gold acquired the option to earn a 100% interest in the Kingsway project in the Gander area of Newfoundland. The property is along strike to the northeast of New Found Gold’s discovery of 92.86 g/t Au over 19.0 metres on their Queensway property. (Note that mineralization hosted on adjacent or nearby properties is not necessarily indicative of mineralization hosted on the Company’s property). In early July 2020, the Company signed an option agreement to acquire a third license to add to the property package which now covers approximately 77 km2. The three licenses comprising the Kingsway project cover approximately 16km of the Appleton fault zone which is associated with gold occurrences in the region, including the New Found Gold discovery. Historical work over the area covered by the Kingsway licenses shows evidence of gold in till, vegetation, soil, stream sediments, lake sediments and float. Infrastructure in the area is excellent located just 18km from the town of Gander with road access to the project, nearby electricity and abundant local water.

The Hopedale property covers much of the Hunt River and Florence Lake greenstone belts that stretch over 80 km. The belts are typical of greenstone belts around the world but have been underexplored by comparison. Initial work by Labrador Gold during 2017 show gold anomalies in soils and lake sediments over a 3 kilometre section of the northern portion of the Florence Lake greenstone belt in the vicinity of the known Thurber Dog gold showing where grab samples assayed up to 7.8g/t gold. In addition, anomalous gold in soil and lake sediment samples occur over approximately 40 kilometres along the southern section of the greenstone belt (see news release dated January 25th 2018 for more details). Labrador Gold now controls approximately 57km strike length of the Florence Lake Greenstone Belt.

The Ashuanipi gold project is located just 35 km from the historical iron ore mining community of Schefferville, which is linked by rail to the port of Sept Iles, Quebec in the south. The claim blocks cover large lake sediment gold anomalies that, with the exception of local prospecting, have not seen a systematic modern day exploration program. Results of the 2017 reconnaissance exploration program following up the lake sediment anomalies show gold anomalies in soils and lake sediments over a 15 kilometre long by 2 to 6 kilometre wide north-south trend and over a 14 kilometre long by 2 to 4 kilometre wide east-west trend. The anomalies appear to be broadly associated with magnetic highs and do not show any correlation with specific rock types on a regional scale (see news release dated January 18th 2018). This suggests a possible structural control on the localization of the gold anomalies. Historical work 30 km north on the Quebec side led to gold intersections of up to 2.23 grams per tonne (g/t) Au over 19.55 metres (not true width) (Source: IOS Services Geoscientifiques, 2012, Exploration and geological reconnaissance work in the Goodwood River Area, Sheffor Project, Summer Field Season 2011). Gold in both areas appears to be associated with similar rock types.

The Company has 85,610,451 common shares issued and outstanding and trades on the TSX Venture Exchange under the symbol LAB.

Posted by AGORACOM

at 10:29 AM on Thursday, July 2nd, 2020

Plethora now owns 13.92% of LabGold

Stichting Depositary Plethora Precious Metals Fund (“Plethoraâ€) announces that on June 26, 2020 it acquired 1,100,000 Units (hereinafter defined) of Labrador Gold Corp. (the “Companyâ€) at $0.175 per Unit pursuant to a private placement for gross proceeds of $192,500 (the “Acquisitionâ€). Each “Unit†acquired consists of one common share in the Company (a “Shareâ€) and one common share purchase warrant in the Company (a “Warrantâ€). Each Warrant entitles the holder thereof to acquire one Share for $0.30 until June 25, 2022.

Prior to this Acquisition, Plethora owned or controlled 8,579,000 Shares and 1,500,000 common share purchase warrants representing 16.12% of the Company’s issued and outstanding Shares on a partially diluted basis. On an undiluted basis, Plethora’s ownership before the Acquisition represented 14.05% of the Company’s issued and outstanding Shares. Following the Acquisition, Plethora now owns or controls an aggregate 9,679,000 Shares, and 2,600,000 common share purchase warrants, representing 13.92% of the issued and outstanding Shares on a partially diluted basis. On an undiluted basis, Plethora’s ownership after the Acquisition represents 11.31% of the Company’s issued and outstanding Shares.

In satisfaction of the requirements of National Instrument 62-104 – Take-Over Bids and Issuer Bids and National Instrument 62-103 – The Early Warning System and Related Take-Over Bid and Insider Reporting Issues, an early warning report respecting the acquisition of securities by Plethora will be filed under the Company’s SEDAR Profile at www.sedar.com.

Plethora acquired the Units for investment purposes only, and depending on market and other conditions, Plethora may from time to time in the future increase or decrease their ownership, control or direction over securities of the Company, through market transactions, private agreements, or otherwise.

Plethora is incorporated under the laws of the Netherlands and its head office is located at Prins Hendriklaan 26, 1075HD, Amsterdam, Netherlands. The principal business of Plethora is a Management Fund.

For information, please contact:

Douwe van Hees- Fund Manager Prins Hendriklaan 26 1075HD, Amsterdam Netherlands Phone: +3 16 14 51 46 92

About Labrador Gold:

Labrador Gold is a Canadian based mineral exploration company focused on the acquisition and exploration of prospective gold projects in the Americas.

In early March 2020, Labrador Gold acquired the option to earn a 100% interest in the Kingsway project in the Gander area of Newfoundland. The property is along strike to the northeast of New Found Gold’s discovery of 92.86 g/t Au over 19.0 metres on their Queensway property. (Note that mineralization hosted on adjacent or nearby properties is not necessarily indicative of mineralization hosted on the Company’s property). The two licenses comprising the Kingsway project cover approximately 16km of the Appleton fault zone which is associated with gold occurrences in the region, including the New Found Gold discovery. Historical work over the area covered by the Kingsway licenses shows evidence of gold in till, vegetation, soil, stream sediments, lake sediments and float. Infrastructure in the area is excellent located just 18km from the town of Gander with road access to the project, nearby electricity and abundant local water.

The Hopedale property covers much of the Florence Lake greenstone belt that stretches over 60 km. The belt is typical of greenstone belts around the world but has been underexplored by comparison. Initial work by Labrador Gold during 2017 show gold anomalies in soils and lake sediments over a 3 kilometre section of the northern portion of the Florence Lake greenstone belt in the vicinity of the known Thurber Dog gold showing where grab samples assayed up to 7.8g/t gold. In addition, anomalous gold in soil and lake sediment samples occur over approximately 40 kilometres along the southern section of the greenstone belt (see news release dated January 25th 2018 for more details).

The Ashuanipi gold project is located just 35 km from the historical iron ore mining community of Schefferville, which is linked by rail to the port of Sept Iles, Quebec in the south. The claim blocks cover large lake sediment gold anomalies that, with the exception of local prospecting, have not seen a systematic modern day exploration program. Results of the 2017 reconnaissance exploration program following up the lake sediment anomalies show gold anomalies in soils and lake sediments over a 15 kilometre long by 2 to 6 kilometre wide north-south trend and over a 14 kilometre long by 2 to 4 kilometre wide east-west trend. The anomalies appear to be broadly associated with magnetic highs and do not show any correlation with specific rock types on a regional scale (see news release dated January 18th 2018). This suggests a possible structural control on the localization of the gold anomalies. Historical work 30 km north on the Quebec side led to gold intersections of up to 2.23 grams per tonne (g/t) Au over 19.55 metres (not true width) (Source: IOS Services Geoscientifiques, 2012, Exploration and geological reconnaissance work in the Goodwood River Area, Sheffor Project, Summer Field Season 2011). Gold in both areas appears to be associated with similar rock types.

Posted by AGORACOM-JC

at 1:08 PM on Tuesday, March 3rd, 2020

Highlights:

Option to acquire 100% of two licenses from Shawn Ryan in an area of excellent infrastructure.

Licenses cover over 14km of the potential extension of the

Appleton fault zone associated with many of the gold showings, including

the new discovery, on New Found Gold’s Queensway project to the south.

The two licenses represent the most prospective areas for

gold of a 45km by 15km regional till and vegetation sampling program

conducted over 3 years.

VANCOUVER, British Columbia, March 03, 2020 – Labrador Gold Corp. (TSX-V: LAB) (“LabGold†or the “Companyâ€) is pleased to announce the acquisition of two licenses near Gander, Newfoundland from Shawn Ryan. The licenses are along strike to the northeast of the recently announced gold discovery of New Found Gold of 92.86g/t Au over 19 metres in Hole NFGC-01 on their Queensway Project. The licenses, Gander South and Gander North, consist of 264 claims covering an area of 6,600 hectares (66 square kilometres). Note that gold values in adjacent properties in similar rocks are not indicative of mineralization on the Gander licenses.

The company has the option to acquire a 100% interest in the two licenses subject to TSX Venture Exchange approval as follows:

Payment of $1,250,000 cash and issue 2 million shares as follows: $250,000 cash and 400,000 shares following TSX venture exchange approval $150,000 cash and 250,000 shares on the first anniversary of the option agreement; $150,000 cash and 300,000 shares on the second anniversary of the option agreement; $200,000 cash and 350,000 shares on the third anniversary of the option agreement; $250,000 cash and 400,000 shares on the fourth anniversary of the option agreement and $250,000 cash and 300,000 shares on the fifth anniversary of the option agreement.

Additional payments based on exploration expenditures will be made as follows: $750,000 on $10 million expenditure on one of the licenses $750,000 on $20 million expenditure on one of the licenses $750,000 on $30 million expenditure on one of the licenses

The Company will also grant a 1% net smelter return royalty (NSR) to

the Vendor plus $1 per ounce of gold in a measured and indicated

resource. An advance royalty of $50,000 per annum for each property will

be payable starting in 2026.

The Company also undertakes to spend $750,000 on each license over the first four years.

“I am very happy to see this district is getting the attention it

deserves,†said Shawn Ryan, Technical Advisor to LabGold. “I started

with 2,200 claims in 2016, and with over 1700 till samples and 3,700

vegetation samples taken over an area of 45km by 15km in 3 years have

whittled it down to the most prospective 264 claims. I am looking

forward to continuing my relationship with LabGold to aggressively

explore these licenses.â€

The two licenses cover over 14 kilometres of strike length of the

potential Appleton fault zone extension. The Appleton fault zone is

associated with many of the gold showings, including the new discovery,

on New Found Gold’s Queensway project to the south. Exploration over the

past four years including till, vegetation and soil sampling has

demonstrated the prospectivity of the licences, particularly along the

extension of the crustal scale Appleton fault zone.

Roger Moss, President and CEO, stated: “We are very happy to continue

our relationship with Shawn and work together to discover more gold

along the same structural trend that hosts the recent New Found Gold

Discovery. We believe this area has great potential for the discovery of

orogenic gold deposits associated with deep seated structures. Work

already completed on the licenses to date indicates significant gold

anomalies in till, vegetation and soil samples along the extension of

the Appleton fault zone. We intend to systematically explore this very

prospective trend during 2020 to delineate drill targets.â€

The licenses occur in an area of excellent infrastructure, situated

just 16km northwest of the town of Gander with good road access, nearby

electricity and abundant water.

Roger Moss, PhD., P.Geo., is the qualified person responsible for all technical information in this release.

About Labrador Gold:

Labrador Gold is a Canadian based mineral exploration company focused

on the acquisition and exploration of prospective gold projects in the

Americas. In 2017 Labrador Gold signed a Letter of Intent under which

the Company has the option to acquire 100% of the Ashuanipi property in

northwest Labrador and the Hopedale property in eastern Labrador.

The Hopedale property covers much of the Florence Lake greenstone

belt that stretches over 60 km. The belt is typical of greenstone belts

around the world but has been underexplored by comparison. Initial work

by Labrador Gold during 2017 show gold anomalies in soils and lake

sediments over a 3 kilometre section of the northern portion of the

Florence Lake greenstone belt in the vicinity of the known Thurber Dog

gold showing where grab samples assayed up to 7.8g/t gold. In addition,

anomalous gold in soil and lake sediment samples occur over

approximately 40 kilometres along the southern section of the greenstone

belt (see news release dated January 25th, 2018 for more details).

The Ashuanipi gold project is located just 35 km from the historical

iron ore mining community of Schefferville, which is linked by rail to

the port of Sept Iles, Quebec in the south. The claim blocks cover large

lake sediment gold anomalies that, with the exception of local

prospecting, have not seen a systematic modern day exploration program.

Results of the 2017 reconnaissance exploration program following up the

lake sediment anomalies show gold anomalies in soils and lake sediments

over a 15 kilometre long by 2 to 6 kilometre wide north-south trend and

over a 14 kilometre long by 2 to 4 kilometre wide east-west trend. The

anomalies appear to be broadly associated with magnetic highs and do not

show any correlation with specific rock types on a regional scale (see

news release dated January 18th, 2018). This suggests a possible

structural control on the localization of the gold anomalies. Historical

work 30 km north on the Quebec side led to gold intersections of up to

2.23 grams per tonne (g/t) Au over 19.55 metres (not true width)

(Source: IOS Services Geoscientifiques, 2012, Exploration and geological

reconnaissance work in the Goodwood River Area, Sheffor Project, Summer

Field Season 2011). Gold in both areas appears to be associated with

similar rock types.

The Company has 57,039,022 common shares issued and outstanding and trades on the TSX Venture Exchange under the symbol LAB.

Neither TSX Venture Exchange nor its Regulation Services

Provider (as that term is defined in policies of the TSX Venture

Exchange) accepts responsibility for the adequacy or accuracy of this

release.

Posted by AGORACOM

at 2:47 PM on Friday, February 21st, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

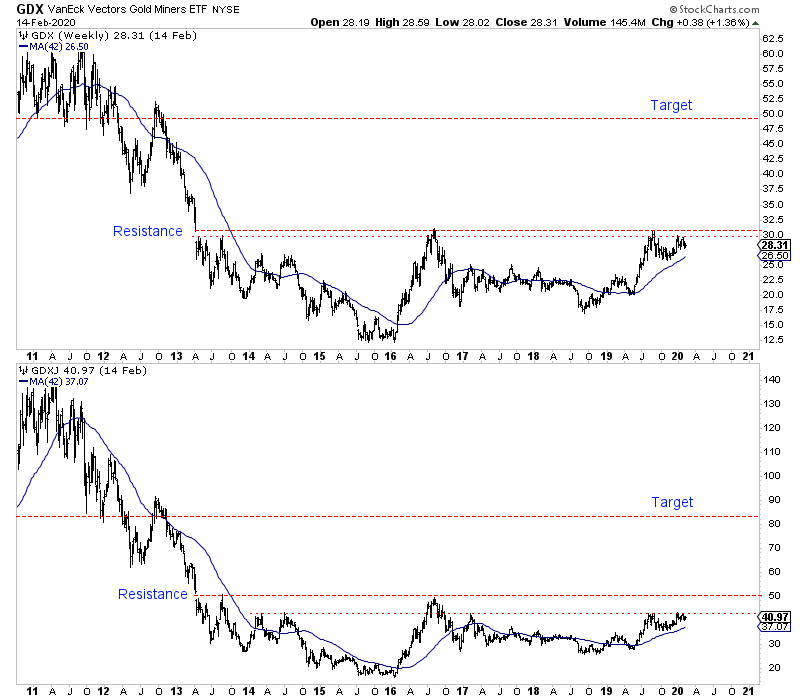

GDX and GDXJ are consolidating bullishly within a now seven-year-long base

Last week, I covered the historical trajectory of the gold stocks and how today compares to the early 1960s.

The late 2015 to early 2016 period marked one of the three best

buying opportunities of the past 100 years (from a secular standpoint),

and gold stocks are in position for sensational performance over the

next 20 years.

That sounds great, but what matters most is the here and now. We do

not want to get caught in a cyclical downturn (which could occur more

than once during this super bull).

Fortunately, the outlook over the next 12 to 18 months is bullish.

The macro-fundamentals are supportive and improving, and the gold stocks

now have a beautiful technical setup that could lead to massive gains.

GDX and GDXJ are consolidating bullishly within a now seven-year-long

base. They are digesting recent gains while holding well above key

support levels and are in position for an eventual explosive breakout.

GDX & GDXJ Weekly Bars

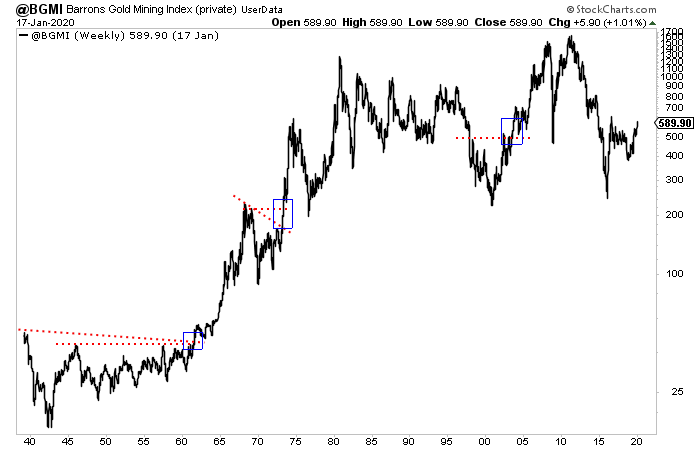

Historically, there have not been many multi-year breakouts with the

potential magnitude of this next one. In using the Barron’s Gold Mining

Index, I only find three.

The breakout in 1964 was a historic, multi-decade breakout that

ushered in an enormous bull market in gold stocks. It was the most

significant inflection point ever for gold stocks.

Later during that bull market, the gold stocks broke a 5-year downtrend and 5-year resistance in 1973, exploding higher.

Barron’s Gold Mining Index

The 2005 breakout compares best with the potential next one.

Like the one in 2005, this next one is setting up several years after

a secular low, following one of the worst bear markets of the past 90

years.

Also, this next breakout could occur following a +7 year-long base,

which is not too far from the +9 year base that was broken in late

2005.

Furthermore, the May 2005 low is similar to September 2018 in that

both followed a mini-bear market that lasted at least 18 months.

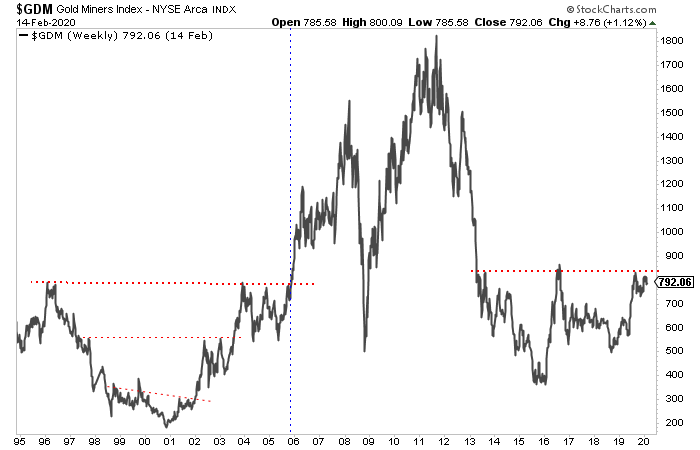

We plot the NYSE Arca Gold Miners Index, which is the parent index of GDX.

GDM Weekly Line

Since there are similarities in the setup, perhaps the upside

potential from a new breakout could be similar to that which followed

the 2005 breakout.

I want to focus on GDXJ because we invest in juniors and not seniors. The history of GDXJ back to January 2004 is available on this website.

From its May 2005 low to its peak in November 2007, GDXJ advanced

nearly 4-fold. Once GDXJ surpassed its January 2004 peak, it gained 138%

into that 2007 peak.

GDXJ closed last week just below $41. The measured upside target from

a break past $50 is $83. If GDXJ today duplicated its performance

before and after the 2005 breakout, then it would peak at $100 or $115.

If we get the breakout, then $83 becomes the minimum upside target. In that case, $100 or $115 is hardly a stretch.

Posted by AGORACOM

at 3:47 PM on Thursday, February 13th, 2020

Gold will outperform the S&P 500 Index in 2020. That’s one of several projections made by CLSA in its just-released “Global Surprises 2020†report.

The Hong Kong investment firm has an impressive track record when it comes to making market predictions—last year it had a 70 percent hit rate—so it may be prudent to take this one seriously.

CLSA’s

head of research Shaun Cochran: “If investors are concerned about the

role of liquidity in recent equity market strength… gold provides a

hedge that could perform across multiple scenarios.â€

Indeed, gold is one of the most liquid assets in the world with an average daily trading volume of more than $112 billion,

according to the World Gold Council (WGC). That far exceeds the Dow

Jones Industrial Average’s daily volume of approximately $23 billion.

The

yellow metal, Cochran adds, can be particularly useful in an era of

perpetually loose monetary policy: “[I]n the event that growth

disappoints the market’s expectations, gold is positively leveraged to

the inevitable policy response of lower rates and larger central bank

balance sheets.â€

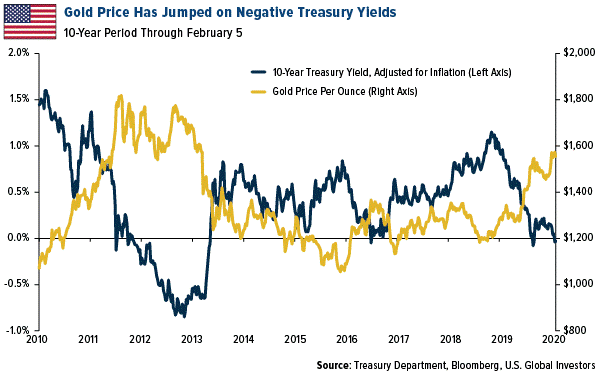

As

I’ve pointed out many times before, gold has traded inversely with

government bond yields. The recent gold rally has largely been driven by

the growing pool of negative-yielding government debt around the world,

now standing at $13 trillion. Here in the U.S., the nominal yield on

the 10-year Treasury has remained positive, but when adjusted for

inflation, it’s recently turned negative, despite a strengthening

economy. What’s more, the Federal Reserve’s balance sheet has begun to

increase again. It now holds about 30 percent of outstanding Treasury

debt, up from about 10 percent prior to the financial crisis.

I

can’t say whether gold will beat the S&P this year or next, but

what I do know is that the yellow metal has been a wise long-term

investment. For the 20-year period through the end of 2019, gold crushed

the market two-to-one, returning 451.8 percent compared to the

S&P’s 223.6 percent. That comes out to a compound annual growth rate

(CAGR) of 8.78 percent for gold, 4.03 percent for the S&P.

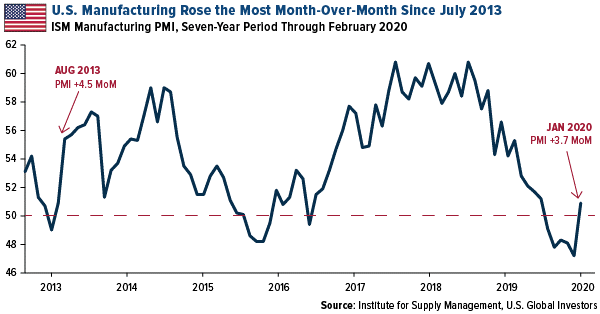

Manufacturing Turnaround Has Begun

U.S.

manufacturers started 2020 on stronger footing, a welcome turnaround

after contracting for five straight months. January’s ISM manufacturing

purchasing manager’s index (PMI) clocked in at 50.9, indicating slight

growth. Up from 47.2 in December, this represents the biggest

month-over-month jump since August 2013, when the PMI increased to 55.4

from 50.9 in July.

This

may also mark the end of the recent manufacturing bear market, prompted

by the trade war between the U.S. and China. Although relations between

the world’s two biggest superpowers remain strained, to say the least,

we’ve seen improvements lately that hint at better days. Both sides

signed a “Phase One†agreement in mid-January, and last week, China

announced it would be cutting tariffs in half on as much as $75 billion

of U.S.-imported products.

The

coronavirus is a new development that has disrupted global trade, but

there’s reason to be optimistic, as the PMI makes clear.

To read my full comments on the coronavirus, and its impact on Chinese and Hong Kong stocks, click here!

The

Dow Jones Industrial Average is a price-weighted average of 30 blue

chip stocks that are generally leaders in their industry. The S&P

500 Stock Index is a widely recognized capitalization-weighted index of

500 common stock prices in U.S. companies. The Purchasing Manager’s

Index is an indicator of the economic health of the manufacturing

sector. The PMI index is based on five major indicators: new orders,

inventory levels, production, supplier deliveries and the employment

environment. Compound annual growth rate (CAGR) is a business and

investing specific term for the geometric progression ratio that

provides a constant rate of return over the time period.

All

opinions expressed and data provided are subject to change without

notice. Some of these opinions may not be appropriate to every investor.

Some links above may be directed to third-party websites. U.S. Global

Investors does not endorse all information supplied by these websites

and is not responsible for their content.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC. This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Posted by AGORACOM

at 1:16 PM on Friday, February 7th, 2020

SPONSOR: Labrador Gold – Two successful gold

explorers lead the way in the Labrador gold rush targeting the

under-explored gold potential of the province. Exploration has already

outlined district scale gold on two projects, including a 40km strike

length of the Florence Lake greenstone belt, one of two greenstone belts

covered by the Hopedale Project. Click Here for More Info

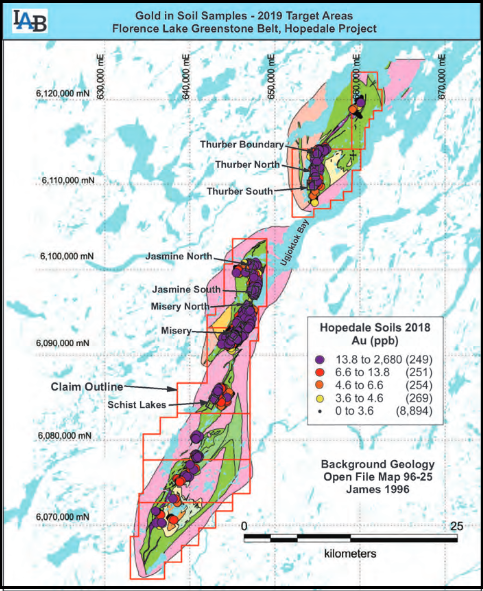

Labrador Gold: District Scale Discovery Potential

First stage drilling on selected targets in 2020 at Hopedale

Large under-explored properties, including the major portion of two greenstone belts

Potential for discovery of new gold district(s)

Experienced exploration success in finding gold deposits (>17 million oz)

First mover advantage

Results of aggressive initial exploration programs already indicate district scale gold targets

Hopedale Project Highlights:

Discovered a new gold showing north of the Thurber Dog gold

occurrence, grab samples from which assayed between 1.67 and 8.26 g/t

Au.

The Thurber Dog gold occurrence has assays in grab and channel

samples from below detection up to 7.866 g/t Au, with 5 samples greater

than 1 g/t Au and 16 samples assaying greater than 0.1 g/t Au.

The discovery extends the potential strike length of gold mineralization by approximately 500 metres along strike to the north.

The new showing occurs within a larger 3km trend of anomalous gold

in rock and soil associated with the contact between mafic/ultramafic

volcanic rocks and felsic volcanic rocks.

Exploration at Hopedale during 2020 will focus on determining the

extent of the Thurber Dog mineralized trend. Such work would aim to fill

in the gaps between showings over the three-kilometre strike length

with sampling and VLF-EM surveys. LabGold also intends to carry out an

initial drill program targeting prospective areas along this trend,

including the new showing.

The Hopedale property covers much of the Hunt River and Florence

Lake greenstone belts that stretch over 80 km. The belts are typical of

greenstone belts around the world but have been underexplored by

comparison. Initial work by Labrador Gold during 2017 show gold

anomalies in soils and lake sediments over a 3 kilometre section of the

northern portion of the Florence Lake greenstone belt in the vicinity of

the known Thurber Dog gold showing where grab samples assayed up to

7.8g/t gold. In addition, anomalous gold in soil and lake sediment

samples occur over approximately 40 kilometres along the southern

section of the greenstone belt (see news release dated January 25th 2018

for more details). Labrador Gold now controls approximately 57km strike

length of the Florence Lake Greenstone Belt.

FULL DISCLOSURE: Labrador Gold is an advertising client of AGORA Internet Relations Corp.

Posted by AGORACOM

at 5:42 PM on Friday, January 31st, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

We believe that there is a strong case to expect gold mining shares to outperform the metal in the years ahead…

On September 17, 2019, overnight repo rates spiked 121 basis points,

climbing from 2.19% to 3.40%, providing yet another crucial buttress for

the bullish rationale for gold. The spike signaled that the U.S.

Federal Reserve (“Fedâ€) had lost control of the price of money. Without

subsequent massive injections of liquidity by the Fed into the repo

market, out of control, short-term interest rates would have undermined

the leverage that underpins record financial asset valuations. Going

forward, unless the Fed continues to expand its balance sheet, it risks a

meltdown in equity and bond prices that could exceed the damage of the

2008 global financial crisis. Despite consensus expectations, there

appears no escape from this treadmill.

The Fed must monetize deficits because non-U.S. investors are no

longer absorbing the growing supply of U.S. debt. Ultra-low, short-term

interest rates do not compensate foreign investors for the cost of

hedging potential foreign currency (FX) losses (see Figure 1). The U.S.

fiscal deficit is too high and the issuance of new U.S. treasuries is

too great for the market to absorb at such low interest rates. In a free

market, interest rates would rise, the economy would stall and

financial asset valuations would decline sharply.

Figure 1. Treasury Issuance Goes Up, Foreign Purchases Go Down (2010-2019)

Source: Bloomberg. Data as of 12/31/2019.

The predicament facing monetary policy explains why central banks are

buying gold in record quantities, as shown in Figure 2. It also

explains the fourth quarter “melt-up†in the equity market, even with Q4

earnings that are likely to be flat to down versus a year ago (marking

the second quarter in a row for lackluster results) and the weakest

macroeconomic landscape since 2009 (as shown by Figure 3).

Figure 2. Central Banks Purchases of Gold are 12% Higher than Last Year

Source: World Gold Council; Metals Focus; Refinitiv GFMS. Data as of 9/30/2019.

Figure 3. The U.S. ISM PMI Index Indicates Economic Contraction

The U.S. ISM Manufacturing Purchasing Managers Index (PMI)1 ended the

year at 47.2, indicating that the U.S. economy is in contraction

territory (a reading above 50 indicates expansion, while a reading below

50 indicates contraction).

Source: Bloomberg. Data as of 12/31/2019.

Liquidity injections will result in more debt, both public and private sector, but not necessarily enhanced economic growth:

“As these forms of easing (i.e., interest

rate cuts and QE [quantitative easing]) cease to work well and the

problem of there being too much debt and non-debt liabilities (e.g.,

pension and healthcare liabilities) remains, the other forms of easing

(most obviously currency depreciations and fiscal deficits that are

monetized) will become increasingly likely …. [this] will reduce the

value of money and real returns for creditors and will test how far

creditors will let central banks go in providing negative real returns

before moving into other assets [including gold].â€

– Ray Dalio, Paradigm Shifts, Bridgewater Daily Observations, 7/15/2019

Gold Bullion and Miners Shine in 2019

Though overshadowed by the rip-roaring equity market, precious metals

and related mining equities also had significant gains in 2019 (up

43.49%)2. Gold’s 18.31% rise last year was its strongest performance

since 2016. More significantly, after two more years of range-bound

trading, the metal closed out 2019 at its highest level since mid-2013,

and within striking distance of $1,900/oz, the all-time high it reached

in 2011.

The investment world has taken little notice. Despite gold’s strong

performance, GDX3, the best ETF (exchange-traded fund) proxy for

precious metals mining stocks, saw significant outflows over the year as

shares outstanding declined from 502 million to 441 million (or 12%)

over the twelve months, despite posting a 39.73% gain, well ahead of the

31.49% total return for the S&P 500 Total Return Index.4

We believe that there is a strong case to expect gold mining shares to outperform the metal in the years ahead…

It has been our long-held view that until mainstream investment

strategies run aground, interest in precious metals will continue to

simmer on low, notwithstanding the likelihood that 2020 may be another

very good year for the precious metals complex. The many reasons why

mainstream investment strategies could unravel are not difficult to

imagine. They include the emergence of meaningful inflation, further

slippage of the U.S. dollar’s nearly exclusive reserve currency status,

and market-driven interest rate increases or a recession. Any or all of

these could disrupt the continued expansion of the Fed’s balance sheet,

triggering a rapid reversal in financial asset valuations. Each

possibility deserves a more complete discussion than space here allows,

but evidence strongly suggests that none can be ruled out. While timing

the zenith in complacency is risky, we feel confident that a reversal of

fortune for high financial asset valuations awaits unsuspecting

investors sooner than they expect.

We are even more confident that a bear market will generate far

broader investment interest in gold. Considering that institutional

exposure to gold and related mining stocks hovers near multi-decade

lows, the slightest uptick could easily drive the metal and related

precious metals mining shares to historic highs. Today, the aggregate

market capitalization of precious metals equity shares is $400 billion,

an insignificant speck on the current market landscape.

Investors outflows from precious metals mining stocks in 2019, even

as gold rose 18.31%, suggests skepticism that the current rally is

sustainable — perhaps hardened by the wounds of years of middling

performance. Contrarian analysis would regard such bearishness as

grounds to be very bullish. In our opinion, investors have overlooked

that the 2019 rise in gold prices has restored financial health to

sector balance sheets, earnings and cash flow. Gold stocks offer both

relative and absolute fundamental value and growth potential that

compares very favorably to conventional investment strategies

We believe that there is a strong case to expect gold mining shares

to outperform the metal in the years ahead by a substantially wider

margin than they outperformed in 2019. With continued advances in

precious metals prices, the return potential from these still unloved

orphans and pariahs of the investment universe should prove to be very

compelling.

Posted by AGORACOM

at 11:58 AM on Wednesday, January 22nd, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

At first glance gold looks like it may be about to advance out of a

bull Flag, but there are a number of factors in play that we will

examine which suggest that any near-term advance won’t get far before it

turns and drops again, and that a longer period of consolidation and

perhaps reaction is necessary before it makes significant further

progress.

On the 6-month chart we can see how gold stabbed into a zone of

strong resistance on the Iran crisis around the time Iran’s General was

murdered, but after a couple of bearish looking candles with high upper

shadows formed, it backed off into what many are taking to be a bull

Flag.

The 10-year chart makes it plain why gold is vulnerable here to

reacting back over the short to medium-term, because it has advanced

deep into “enemy territory†– the broad band of heavy resistance

approaching the 2011 highs, with a zone of particularly strong

resistance right where it is now. It would be healthier and increase

gold’s chances of breaking out to new highs if it now backed off into a

trading range for a while to moderate what now looks like excessive

bullishness.

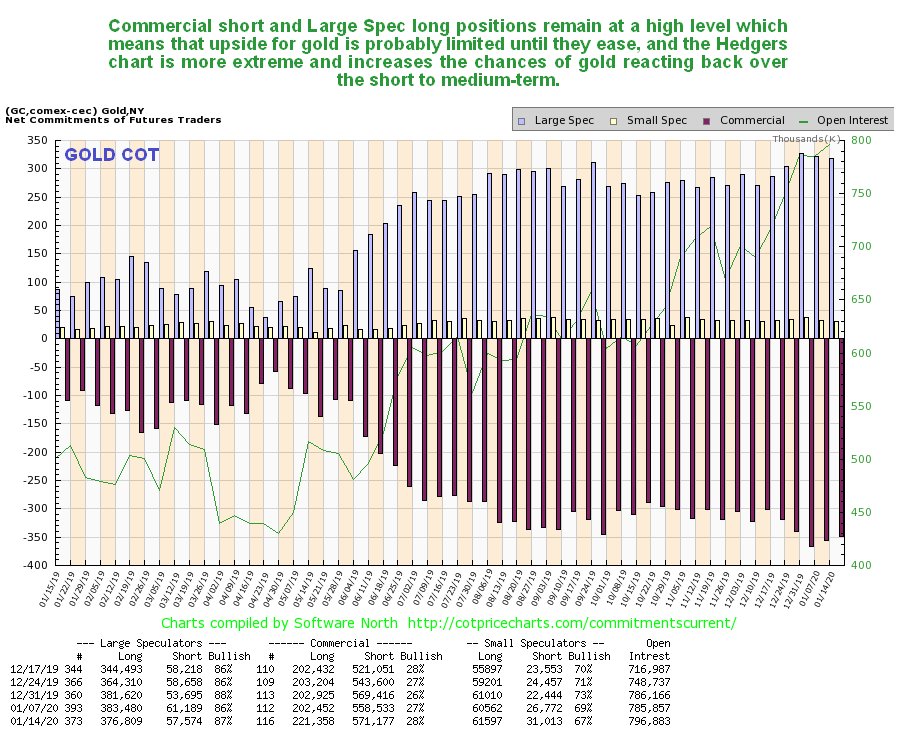

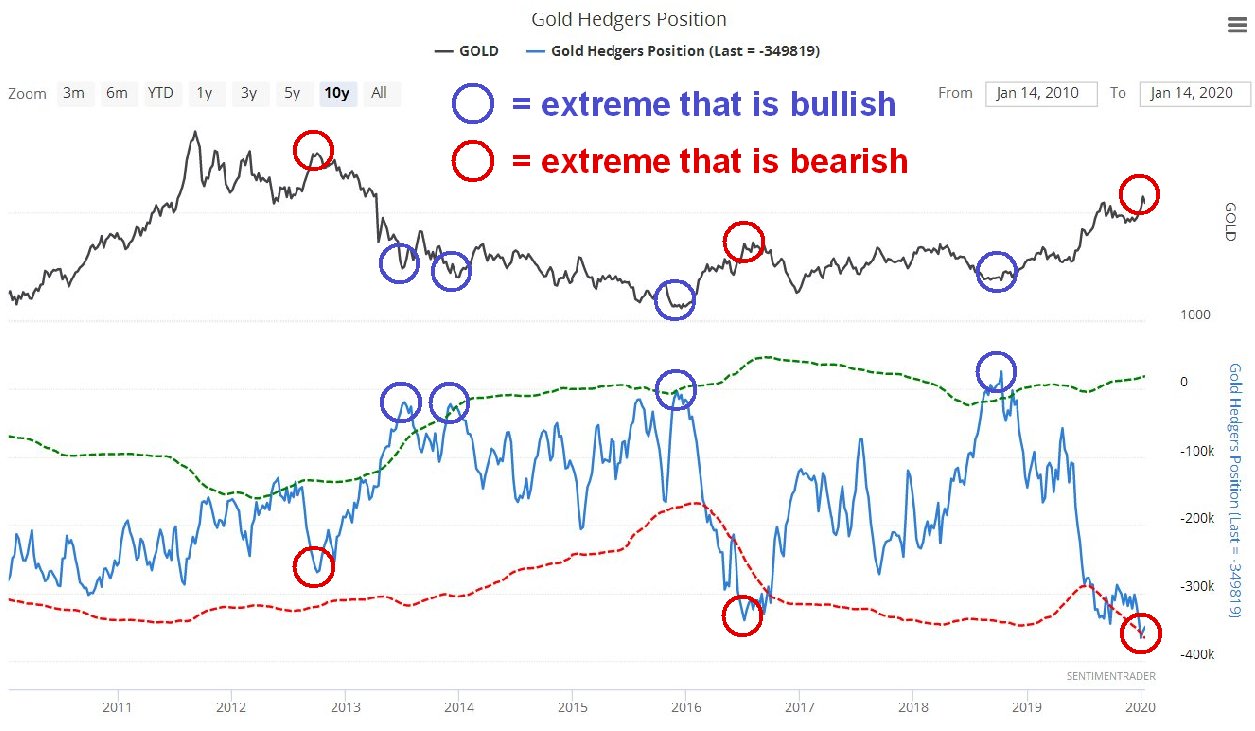

Thus it remains a cause for concern (or it should be for gold

bulls) to see gold’s latest COTs continuing to show high Commercial

short and Large Spec long positions. Is it “going to be different this

time� – the latest Hedgers charts that we are now going to look at

suggest not.

Click on chart to popup a larger, clearer version.

The COT chart only goes back a year. The Hedgers charts shown

below, which are a form of COT chart, go back many years, and frankly,

they look pretty scary.

We’ll start by looking at the Hedger’s chart that goes back to before

the 2011 sector peak. On it we see that current Hedgers positions are

at extremes that way exceed even those at the peak of the 2012 sucker

rally, which was followed by the bulk of the decline in the bearmarket

that followed. Does this mean that we are going to see another

bearmarket like that – no it doesn’t, but it does mean that these

positions will probably need to moderate before we see significant

further gains.

Click on chart to popup a larger, clearer version.

Chart courtesy of sentimentrader.com

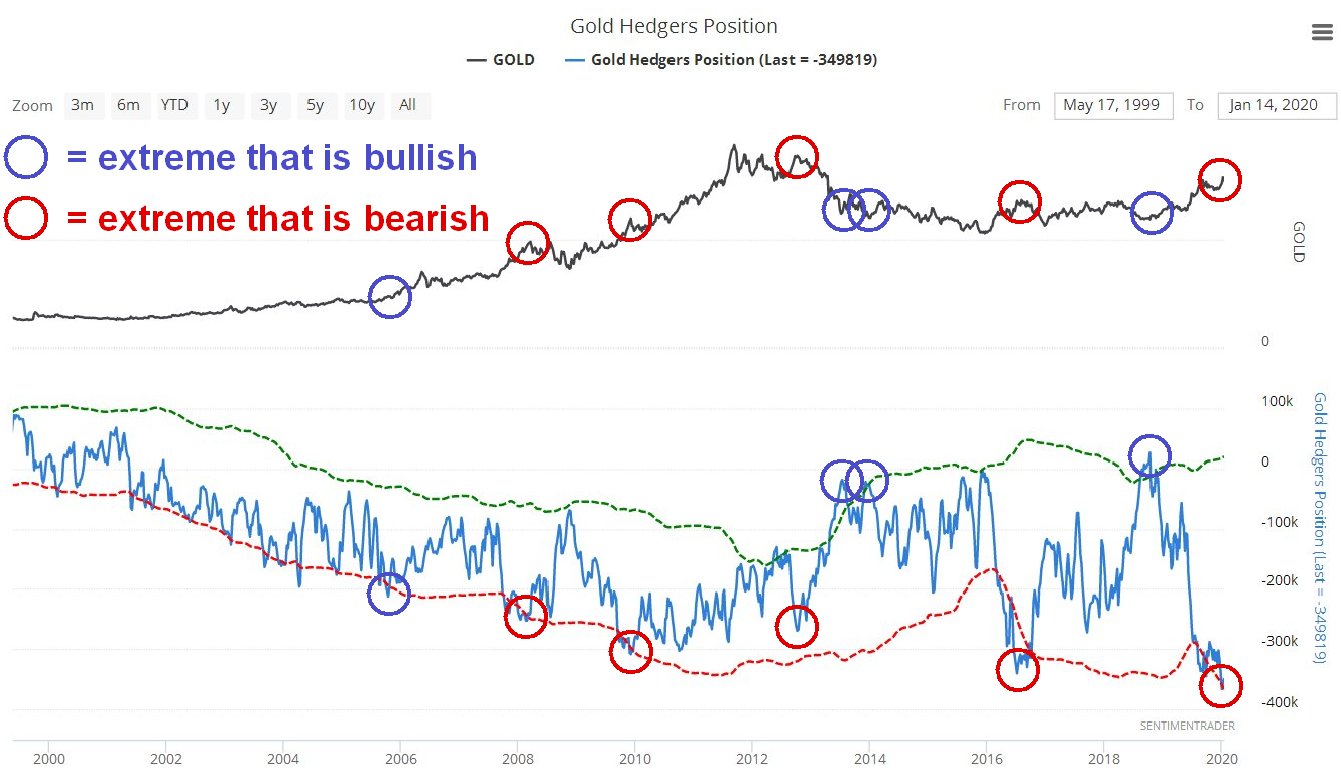

Looking at the Hedgers chart going way back to before the year

2000, we see that the current readings are record readings by a

significant margin and obviously increase the risks of a sizeable

reaction. We can speculate about what the reasons for a decline might

be, one possibility being the sector getting dragged down by a

stockmarket crash after its blowoff top, which may be imminent, as

happened in 2008, since it remains to be seen whether investors will

rush into the sector as a safe haven in the event of a market crash.

Click on chart to popup a larger, clearer version.

Chart courtesy of sentimentrader.com

Turning now to Precious Metals stocks, we see on its latest

10-year chart that GDX still looks like it is completing a giant

Head-and-Shoulders bottom pattern. However, it is currently dithering

just beneath resistance at the top of this base pattern, which means

that it is vulnerable to backing off.

So, how then does gold stock sentiment look right now? As we can

see on the 5-year chart for the Gold Miners’ Bullish Percent Index,

bullishness towards the sector is now at a very high level, 84.6%, which

makes it more likely that stocks will drop soon rather than rally, and

what they could do of course is rally some to increase this level of

bullishness still further, and then drop.

Does all this mean that investors in the sector should suddenly

rush for the exits? No, it doesn’t, especially as the charts for many

individual stocks across the sector look very bullish, and it may be

that all that is needed is a cooling period of consolidation. However it

does make sense to use Hedges at extremes, such as leveraged inverse

ETFs and better still options as insurance, which have the advantage of

providing protection for a very small capital outlay, a fine example

being GLD Puts which are liquid with narrow spreads. We did this just ahead of the recent peak

when Iran lobbed a volley of missiles at Iraq. We will not be selling

our strongest gold and silver stocks, but instead look to buy more on

dips.

Posted by AGORACOM

at 4:36 PM on Friday, January 17th, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

From the HRA Journal: Issue 314

The fun doesn’t stop. Waves of liquidity continue to wash traders

cares away. Even assassinations and war mongering generate little more

than half day dips on Wall St. It seems nothing can get in the way of

the bull rally that’s carrying all risk assets higher.

It feels like it could go on for a while, though I think the

liquidity will have to keep coming to sustain it. By most readings,

bullishness on Wall St is at levels that are rarely sustained for more

than a few weeks. Some sort of correction on Wall St seems highly

likely, and soon. Whether its substantial or just another blip on the

way higher remains to be seen.

The resource sector, especially gold and silver stocks, have had

their own rally. Our Santa Claus market was as good or better than Wall

St’s for a change. And I don’t think its over yet. I think we’re in for

the best Q1 we’ve seen for a few years. And we could be in for something

better than that even. I increasingly see signs of a major rally

developing in the gold space. It’s already been pretty good but I think a

multi-quarter, or longer, move may be starting to take shape.

I usually spend time on all the metals in the first issue of the

year. But, because the makings of this gold rally are complex and long

in coming I decided to detail my reasoning. That ended up taking several

pages so I’ll save talk on base metals and other markets for the next

issue.

No, I’m not writing about Louis IV, though there might be some

appropriateness to the analogy, now that I think about it. The quote is

famous, even though there’s no agreement on what it was supposed to

mean. Most figure Louis was referring to the biblical flood, that all

would be chaos once his reign ended.

The deluge I’m referring to isn’t water. It’s the flood of money the

US Fed, and other central banks, continue to unleash to keep markets

stable. Markets, especially stock markets, love liquidity. You can see

the impact of the latest deluge, particularly the US Fed’s in the chart

below that traces both the SPX index value and the level of a “Global

Liquidity Proxy†(“GLPâ€) measuring fiscal/monetary tightness and

weakness.

You can see the GLP moved lower in late 2018 as the Fed tightened and

the impact that had on Wall St. Conversely, you can see the SPX running

higher in the past couple of months as the US backed off rate

increases, increased fiscal deficit expansion, and grew the Fed balance

sheet through, mainly, repo market operations.

Wall St, and most other bourses, are loving these money flows. The

Santa Claus rally discussed in the last issue continued to strengthen

all the way to and through year end. As it turned out, the Fed either

provided enough backstop in advance or the yearend repo issues were

overstated. The repo market itself was calm going through year end and a

lot of the short-term money offered by the Fed during that week wasn’t

taken down.

Everything may have changed in the past couple of days with the

dramatic increase in US-Iran tensions. I don’t know how big an issue

that will be, since no one knows what form Iran’s retaliation will be or

how much things will escalate. I DO think it’s potentially a big deal

with very negative connotations, but it may take time to unfold. Someone

at the Fed thought so too, as the past couple of days saw a return to

large scale Fed lending in the repo market.

I’ve no doubt Iran will try and take revenge for the assassination of

its most famous military commander by the US. But I don’t know what

form it will take and if this means the US has drawn itself into the

Mideast quagmire even more. I fear it has though. The US is already

talking about adding 3,000 troops to its Mideast presence and they’re

just warming up. Even larger scale attacks, if they happen, may not

derail Wall St, but they’re certainly not a positive development at any

level.

We know how stretched both market valuations and sentiment were

before the Suleimani drone strike. The chart below shows a three-year

trace of the “fear/greed indexâ€. You can see that its hardly a stable

reading. It flip flops often and extreme readings rarely hold for long.

At last check, the reading was 94% bullish.

Sentiment almost never gets that bullish and, when it does, nothing

good comes of it for bulls. A reading that close to 100% tells you we’re

just about out of buyers. Whatever happens in and around Iran, I think a

near term correction is inevitable. The only question is whether it’s a

large one or not.

A rapid escalation in US-Iran tensions could certainly make a near

term correction larger. If the flood of liquidity continues though, a

correction could just be another waystation on the road to higher highs.

There are a couple of other dangers Wall St still faces that I’ll touch

on briefly at the end of this article. First however, lets move on to

the main event for us-the gold market.

It wasn’t just the SPX enjoying a Santa rally this year. Gold

experienced the rally we were hoping for that gold miner stocks seemed

to be foretelling early last month. Gold’s been doing well since it

bottomed at $1275 in June, but it didn’t feel that way during the long

hiatus between the early September high and the current move. The gold

price currently sits above September’s multi-year high, after breaching

that high in the wake of the Baghdad drone strike. And the first

retaliatory strike by Iran. Volatility will be very high for a while

going forward.

I think we’ll see more multi-year highs going forward. I hate that

the latest move higher is driven by geopolitics. Scary geopolitics and

military confrontations mean people are dying. We don’t want to profit

from misery. And we won’t anyway, if things get ugly enough in the

Mideast to scare traders out of the market.

Geopolitical price moves almost always unwind quickly. I’d much

prefer to see gold moving higher for macro reasons, not as a political

safety trade. I expect more political/military inspired moves. As the

Iran conflict unfolds. Make no mistake, Iran is NOT Iraq. Its army is

far larger, better trained and better equipped than Iraq. This could get

ugly.

The balance of this piece will deal with my macro argument for higher

gold prices over an extended period. The geopolitical stuff will be

layered on top of that for the next while and could strengthen both gold

prices and the $US in risk-off trading. It should be viewed as a

separate event from the argument laid out below.

What else is driving gold higher? In part, it was gold’s inverse

relationship with the US Dollar. As you already know, I’m not a believer

that “its all about the USD, all the time†when it comes to the gold

market. That’s an over-simplification of a more complex relationship. It

also discounts the idea of gold as its own asset class that trades for

its own reasons.

If you look at the gold chart above, and the USD chart below it, its

immediately apparent that there isn’t a constant negative correlation at

play. Gold rallied during the summer at the same time the USD did and

for the same reason; the world-wide explosion of negative real yields.

Gold weakened a bit when yields reversed to the upside and the USD got a

bit of traction, but things changed again at the start of December.

The USD turned lower and lost two percent during December. US bond

yields were generally rising during the month and the market (right or

wrong) was assuming economic growth was accelerating. So, neither of

those items explains the USD weakness.

If gold was a “risk off†trade, you sure couldn’t see it in the way

any other market was trading. So, is there another explanation for

recent strength in the gold price, and what does it tell us about 2020

and, perhaps, beyond?

Well, I’ve got a theory. If I’m right, it could mean a bull run for gold has a long way to go.

Some of this theory will be no surprise to you because it does

partially hinge on further USD weakness. There are long term structural

reasons why the US currency should weaken. But there are also

fluctuating sources of demand for USDs, particularly from offshore

buyers and borrowers that transact in US currency. That can create

enough demand to strengthen the US over long periods. We just went

though one such period, but it looks like that may have come to an end,

with more bearish forces to the USD reasserting themselves.

How did we get here? Let’s start with the big picture, displayed on

the top chart on the next page. It gives a long-term view of US Federal

deficits and the unemployment rate. Normally, these travel in tandem.

Higher unemployment means more social spending and higher deficits.

Government spending expands during recessions and contracts-or should-

(as a percentage of GDP) during expansions. Classic Keynesian stuff.

You rarely see these two measures diverge. The two times they did

significantly before, on the left side of the chart, was due to “wartime

deficits†which acted (along with conscription) to stimulate the

economy and drive down unemployment.

You can see the Korean and Vietnam war periods pointed out on the chart.

The current period stands out for the extreme size of the divergence.

US unemployment rates are at multi decade lows and yet the fiscal

deficit as a percentage of GDP keeps rising. There has never been a

divergence this large and its due to get larger.

We know why this is. Big tax cuts combined with a budget that is

mostly non-discretionary. And the US is 10 years into an economic

expansion, however weak. Just think what this graph will look like the

next time the US goes into recession.

We can assume US government deficits aren’t going to shrink any time

soon (and I think we can, pun intended, take that to the bank). That

leaves trade in goods to act as a counterbalance to the funding demand

created by fiscal deficits.

The chart above makes it clear the US won’t get much help from

international trade. The US trade balance has been getting increasingly

negative for decades. It’s better recently, but unlikely to turn

positive soon, and maybe not ever.

To be clear, this is not a bad thing in itself, notwithstanding the

view from the White House. The relative strength of the US economy and

the US Dollar and cheaper offshore production costs have driven the

trade balance. It’s grown because Americans found they got more value

buying abroad and the world was happy to help finance it. It’s not a bad

thing, but not a US Dollar support either.

The more complete picture of currency/investment flows is given by

changes in the Current Account. In simplified terms, the Current Account

measures the difference between what a country produces and what it

consumes. For example, if a country’s trade deficit increases, so does

its current account deficit. If there are funds flowing in from overseas

investments on the other hand, this decrease the Current Account

deficit or increase the surplus.

The graph below summarizes quarterly changes in the US current

account. You can see how the balance got increasingly negative in the

mid 2000’s as both imports and foreign investment by US companies

increased.

Not coincidentally, this same period leading up to the Financial

Crisis included a sustained downtrend in the US Dollar Index. The USD

index chart on the bottom of the next page shows the scale of that

decline, from an index value of 120 at the start of 2002 all the way

down to 73 in early 2008.

The current account deficit (and value of the USD) improved markedly

up to the end of the Financial Crisis as money poured into the US as a

safe haven and consumers cut back on imports. The current account

deficit bas been relatively stable since then, running at about

$100bn/quarter until it dipped a bit again last year.

Trade, funds flows and changes in money supply have the largest

long-term impacts on currency values. When the US Fed ended QE and

started tightening monetary conditions in 2014, the USD enjoyed a strong

rally. The USD Index was back to 100 by early 2015 and stayed there

until loosening monetary conditions-and lots of jawboning from

Washington-led to pullback. Things reversed again and the USD maintained

a mild uptrend from early 2018 until now.

There are still plenty of US Dollar bulls around, and their arguments

have short-term merit. Yes, the US has higher real interest rates and

somewhat higher growth. Both are important to relative currency

valuations as I’ve said in the past. Longer term however, the “twin

deficits†-fiscal and current account-should underpin the fundamental

value of the currency.

Movements don’t happen overnight, especially when you’re talking

about the worlds reserve currency that has the deepest and largest

market supporting it. Changing the overall trend for the USD is like

turning a supertanker. I think it’s happening though, and it has big

potential implications for commodities, especially gold.

Dollar bulls will tell you the USD is the “cleanest shirt in the

laundry hamperâ€, referring to the relative strength of the growth rate

and interest rates compared to other major currencies. That’s true if we

just look at those measures but definitely not true when we look at the

longer term-fiscal and current account deficits.

In fact, the US has about the worst combined fiscal/current account deficit in the G7. The chart at the bottom of this page, from lynalden.com

shows the 2018 values for Current Account and Trade balances for a

number of major economies, as a percentage of their GDP. It’s not a

handsome group.

Both the trade and current account deficits are negative for most of

them. In terms of G7 economies, the US has the worst combined

Current/Trade deficit at 6% of GDP annually. You may be surprised to

note that the Current/Trade balance for the Euro zone is much better

than the US, thanks to a large Trade surplus. Much of that is generated

by Germany. Indeed, this chart explains Germanys defense of the Euro.

It’s combined Trade/Current Account surplus is so large it’s currency

would be skyrocketing if it still used the Deutschmark.

Because the current account deficit is cumulative, the overall

international investment position of the US has continued to worsen. The

US has gone from being an international creditor to an international

debtor, and the scale if its debt keeps increasing. That means it’s

getting harder every year to reverse the current account position as the

US borrows ever more abroad to cover its trade and fiscal deficits.

Interest outflows keep growing and investment inflows shrinking.

Something has to give.

The US has to borrow overseas, as private domestic demand for

Treasury bonds isn’t high enough to fund the twin deficits. In the past,

whenever the US Dollar got too high, offshore demand for US government

debt diminished. It’s not clear why. Maybe the higher dollar made

raising enough foreign funds difficult, or perhaps buyers started

worrying about the USD dropping after they bought when it got too

expensive. Whatever the reason, foreign holdings of US Treasuries have

been declining, forcing the US to find new, domestic, buyers.

Last year, the US Fed stopped its quantitative tightening program,

due to concerns about Dollar liquidity. Then came the repo market. Since

September, the Fed’s balance sheet has expanded by over $400 billion,

mainly due to repo market transactions.

The Fed maintains this “isn’t QE†because these are very short duration transactions but, cumulatively, the total Fed balance sheet keeps expanding. The “QE/no QE†debate is just semantics.

What do these transactions look like? Mostly, its Primary Dealers,

banks that also take part in Treasury auctions, in the repo market. The

Fed buys bonds, usually Treasuries, from these banks and pays for them

in newly printed Dollars. That injects money into the system, helps hold

down interest rates in the repo market and, not coincidentally,

effectively helps fund the US fiscal deficit. To put the series of

transactions in their simplest form, the US is effectively monetizing its deficit with a lot of these transactions.

The chart below illustrates the problem for the Primary Dealer US

banks. They’ve got to buy Treasuries when they’re auctioned-that is

their commitment as Primary Dealers. They also need to hold minimum cash

balances as a percentage of assets under Basel II bank regulations.

Cash balances fell to the minimum mandated level by late 2019- the

horizontal black line on the chart. That’s when the trouble started.

These banks are so stuffed with Treasuries that they didn’t have

excess cash reserves to lend into the repo market. Hence the blow up

back in September and the need for the Fed to inject cash by buying

Treasuries. The point, however, is that this isn’t really a “repo market

issueâ€, that’s just where it reared its head. It’s a “too many

Treasuries and not enough buyers†problem.

It will be tough for the Treasury to attract more offshore buyers

unless the USD weakens, or interest rates rise enough to make them

irresistible. Or a big drop in the federal deficit reduces the supply of

Treasuries itself.

I doubt we’ll see interest rates move up significantly. I don’t think

the economy could handle it and it would be self-defeating anyway, as

the government deficit would explode because of interest expenses. And

that’s not even taking into account the fact that President Trump would

be freaking out daily.

Based on recent history and political expediency, I’d say the odds of

significant budget deficit reductions are slim and none. That’s

especially true going into an election year. There’s just no way we’re

going to see spending restraint or tax increases in the next couple of

years. Indeed, the supply of Treasuries will keep growing even if the US

economy grows too. If there is any sort of significant slowdown or

recession the Federal deficit will explode and so will the new supply of

Treasures. Not an easy fix.

Barring new haven demand for US Treasuries, odds are the Fed will

have to keep sopping up excess supply. That means expanding its balance

sheet and, in so doing, effectively increasing the US money supply.

That brings us (finally!) to the “money shot†chart that appears

above. It compares changes in the size of the Fed balance sheet and the

US Dollar Index. To make it readable and allow me to match the scales, I

generated a chart that tracks annual percentage changes.

The chart shows a strong inverse correlation between changes in the

size of the Fed balance sheet and the value of the USD. This is

unsurprising as most transactions that expand the Fed balance sheet also

expand the money supply.

It’s impossible to tell how long the repo market transactions will

continue but, after three months, they aren’t feeling very “temporaryâ€.

To me, it increasingly looks like these market operations are “debt

monetization in dragâ€.

I don’t know if that’s the Fed’s real intent or just a side effect.

It doesn’t really matter if the funding and money printing continues at

scale. Even if the repo market calms completely, the odds are good we

see some sort of “new QE†start up. Whatever official reason is given

for it; I think it will happen mainly to soak up the excess supply of

Treasuries fiscal deficits are creating.

I don’t blame the FOMC if they’re being disingenuous about it. That’s

their job after all. If you’re a central banker, the LAST thing you’re

going to say is “our government is having trouble finding buyers for its

debtâ€, especially if its true.

With no prospect of lower deficits and apparent continued reduction

in offshore Treasury holdings, this could develop into long-term

sustained trend. I don’t expect it to move in a straight line, markets

never do. A severe escalation in Mideast tensions or the start of a

serious recession could both generate safe-haven Treasury buying. Money

flows from that would take the pressure off the Fed and would be US

Dollar supportive too.

That said, it seems the US has reached the point where a substantial

increase in its central bank’s balance sheet is inevitable. Both Japan

and the Eurozone have gotten there before the Fed, but it looks like it

won’t be immune.

The Eurozone at least has a “Twin surplus†to help cushion things.

And Japan, considered a basket case economically, had an extremely deep

pool of domestic savings (far deeper than the US) to draw on. Until very

recently, Japan also ran massive Current Account surpluses thanks to

decades of heavy investments overseas by Japanese entities. Those

advantages allowed the ECB and especially the BoJ to massively expand

their balance sheets without generating a huge run up in interest rates

or currency collapse.

I don’t know how far the US Fed can expand its balance sheet before

bond yields start getting away from it. I think pretty far though.

Having the world’s reserve currency is a massive advantage. There is

huge built in demand for US Dollars and US denominated debt. That gives

the Fed some runway if it must keep buying US Treasuries.

Assuming a run on yields doesn’t spoil the party, continued balance

sheet and money supply expansion should put increasing downward pressure

on the US Dollar. I don’t know if we’ll see a move as large as the

mid-2000s but a move down to the low 80s for the USD Index over the

course of two or three years wouldn’t be surprising.

It won’t be a straight-line move. A recession could derail things,

though the bear market on Wall St that would generate would support

bullion. Currency markets tend to be self-correcting over extended

periods. If the USD Index falls enough and there is a bump in US real

interest rates offshore demand for Treasuries should increase again.

The bottom line is that this is, and will continue to be, a very

dynamic system. Even so, I think we’ve reached a major inflection point

for the US currency. The 2000s were pretty good for the gold market and

gold stocks. We started from a much lower base of $300/oz on the gold

price. Starting at a $1200-1300 base this time, I think a price above

$2000/oz is a real possibility over the next year or two.

It’s not hard to extrapolate prices higher than that, but I’m not

looking or hoping for those. I prefer to see a longer, steadier move

that brings traders along rather than freaking them out.

This prediction isn’t a sure thing. Predictions never are. But I

think the probabilities now favor an extended bull run in the gold

price. Assuming stock markets don’t blow up (though I still expect that

correction), gold stocks should put in a leveraged performance much more

impressive than the bullion price itself.

There will be consolidations and corrections along the way, but I

think there will be many gold explorers and developers that rack up

share price gains in the hundreds of percent. That doesn’t mean buying

blindly and never trading. We still need to adjust when a stock gets

overweight and manage risk around major exploration campaigns. The last

few weeks has been a lot more fun in the resource space. I don’t think

the fun’s over yet. Enjoy the ride.

Like any good contrarian, a 10-year bull market makes me alert of

signs of potential trouble. As noted at the start of this editorial, I’m

expecting continues floods of liquidity. That may simply overwhelm

everything else for a while and allow Wall St to keep rallying, come

what may.

That said, a couple of data points recently got my attention. One is

more of a sentiment indicator, seen in the chart below. More than one

wag has joked that the Fed need only worry about Wall St, since the

stock market is the economy now. Turns out there is more than a bit of

truth to that.

The chart shows the US Leading Indicator reading with the level of

the stock market (which is a component of the official Leading

Indicator) removed. As you can see, without Wall St, the indicator

implies zero growth going forward. I’m mainly showing it as evidence of

just how surreal things have become.

The chart above is something to keep an eye on going forward. It

shows weekly State unemployment claims for several major sectors of the

economy. What’s interesting about this chart is that claims have been

climbing rapidly over the past few weeks. Doubly interesting is that the

increase in claims is broad, both within and across several sectors of

the economy.

I take the monthly Non-Farm Payroll number less seriously than most,

because it’s a backward-looking indicator. This move in unemployment

claims looks increasingly like a trend though. It’s now at its highest

level since the Financial Crisis.

It’s not in the danger zone-yet. But its climbing fast. We may need

to start paying more attention to those payroll numbers. If the chart

below isn’t a statistical fluke, we may start seeing negative surprises

in the NFP soon. That won’t hurt the gold price either.

Source and Thanks: https://www.hraadvisory.com/golds-big-picture