Posted by AGORACOM

at 1:25 PM on Monday, May 11th, 2020

SPONSOR: Lomiko Metals is focused on the exploration and development of minerals for the new green economy such as lithium and graphite. Lomiko owns 80% of the high-grade La Loutre graphite Property, Lac Des Iles Graphite Property and the 100% owned Quatre Milles Graphite Property. Lomiko is uniquely poised to supply the growing EV battery market. Click Here For More Information

Electric vehicles (EVs) in their current form are not practical for long distance travel due to the need for multiple or lengthy stops at charging stations. But what if they could—like planes being refueled in the air from another aircraft—get a charge-on-the-go?

The idea sounds like science fiction, but there are already technologies in use that would help facilitate specialized vehicles for charging.

For instance, Tesla cars use radar to detect the speed of other cars around them, which controls the speed of the car in relation to traffic—a feature that would make “docking†possible.

With rural electric charging stations almost non-existent, Swarup Bhunia and engineers at the University of Florida, Gainesville, are postulating that “peer-to-peer charging†and “mobile charging stations†could likely solve this problem faster than the current proliferation of charging points or battery advancements

Along with the mobile charging stations idea, Bhunia believes that if more and more people buy electric cars, it would be super-efficient if all cars on the road could share charge with one another.

The idea is bold and definitely something out of Blade Runner or Ex Machina, but Bhunia explains that, incredibly, it’s the easiest way to solve the two largest hang-ups that prevent consumers from selecting an EV—battery range, and charging time.

Cloud Technology for Traffic

“A set of cloud-based schedulers decides charge providers and receivers,†begins the hypothesis written by Bhunia et al. in a journal called arxiv that allows non peer-reviewed material to be discussed.

What Bhunia and his team are describing is a cloud system that examines all of the EV drivers on the road, where they are going, and how much charge each vehicle has. The cloud then determines, for example, that EV-A has 89% battery, but requires only 4% to reach its destination, while EV-B has 22% battery, yet requires 31% to reach its destination.

If the rerouting isn’t intrusive, the system would instruct the two EVs to carry out the charge transfer. The system would then link the provider with the receiver, and a credit system would ensure that everyone is paying for the charge they use.

Inside the given traffic network, every vehicle’s charge could be examined against each vehicle’s demand, and “mobile charging stations,†which would be large automated trucks with onboard charging equipment to fill in the demand gaps.

“We envision a safe, insulated, and firm telescopic arm carrying the charging cable,†reads the paper, describing how to get one charge into another car while barreling down the freeway, much like two aircraft during mid-air refueling. “After two EVs lock speed and are in range for charge sharing, they will extend their charging arms.â€

They admit this would be just one possible way to tackle this problem. One extremely exciting thing that the team has also imagined would be wireless charging in the future, as we can already do with our phones. Imagine realizing you need a bit of a charge up, and so you simply pull your car alongside an 18 wheeler, set the cruise control, and charge up wirelessly before continuing on your way.

Volkswagen has already unveiled a conceptual design for a little robot that will tug around a trailer of batteries while charging all the cars inside a given parking garage, and if the technology could be adopted onto a mobile charging station like a truck, car, semi-trailer, or even drone, as some have imagined, Bhunia’s dream of a cloud-sharing peer-to-peer charging network is already halfway real.

Posted by AGORACOM

at 12:50 PM on Monday, May 11th, 2020

Sponsor: Affinity Metals Corp. (TSX-V: AFF) is a Canadian mineral exploration company building a strong portfolio of mineral projects in North America. The Corporation’s flagship property is the drill ready Regal Property near Revelstoke, BC where Affinity Metals is making preparations for a spring drill program to test two large Z-TEM anomalies. Click Here for More Info

COVID-19: The Pin that Punctured the Credit Balloon

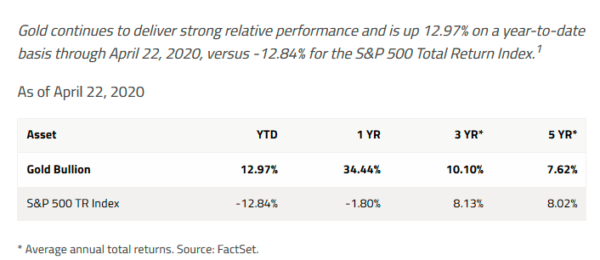

Gold is on the cusp of breaking out to all-time highs in U.S. dollars and has already done so in virtually every other currency. Gold mining stocks continue to lag the metal and, in our opinion, represent a compelling investment opportunity at this moment. The COVID-19 pandemic panic was merely the black swan that punctured a financial market asset bubble that took almost a decade to inflate.

Think of the pandemic as the pin that punctured the credit balloon. In a few months, the pandemic will ease (hopefully) with the formulation of a COVID-19 vaccine, widespread testing and other responses that will surely come from the healthcare industry. However, the fiscal and monetary policy damage committed by all governments to save the world has created a debt hangover that will linger for years. Economic growth will rebound but only to subpar levels once extreme health-related restrictions are lifted and “stimulus†kicks in.

The requisites for robust economic growth most likely to misfire are investment confidence and bank lending. Both have been severely compromised. Whether this landscape evolves into a long stretch of deflation or combusts into untamed inflation remains to be seen. What seems quite apparent is that traditional Keynesian stimulus measures are in their endgame. They will most likely deliver only steadily diminishing returns. Starkly opposite economic outcomes are possible from this policy morass; both would be positive for gold but negative for real returns on fixed income or equities.

Q1 Marks a Pivotal Turning Point for All Asset Classes

As of this writing, gold is trading about 10% less than its all-time high of US$1,900 attained nine years ago (September 2011). In effect, it has gone nowhere for a decade despite a tectonic shift in the investment and economic outlook. A lengthy correction lasting until 2016 and subsequent churning resulted in the establishment of a powerful multi-year basing structure. From this base and with strong macroeconomic tailwinds, we believe new highs well above $1,900 can be achieved over the next four years.

Despite enthusiastic advocacy and much chatter from investment luminaries, including Ray Dalio, Jeff Gundlach, Seth Klarman and others, gold remains severely and inappropriately underrepresented in the portfolios of fiduciaries, endowments and family offices. Flows into channels such as gold-backed exchange traded funds (“ETFsâ€) have been strong relative to previous low levels, but must still be considered a trickle in terms of what could still come.

Figure 1. Gold-Backed ETFs Reach Record Levels Global gold-backed ETFs added 298 tonnes and net inflows of US$23 billion in Q1 2020 — the highest quarterly amount ever in absolute U.S. dollar terms and the largest tonnage additions since 2016. Source: World Gold Council. Data as of 3/31/2020.

In our opinion, the first quarter of 2020 will mark a pivotal, secular turning point for all major asset classes including equities, bonds, gold and currencies. A return to the pre-2020 financial market normalcy and investment complacency is unlikely. In our view, consensus hopes remain high that the credit smash is only a temporary repercussion of the health scare. We disagree and suggest the effects will be long lasting.

Despite the solid price gains achieved by gold in the past two years, there is much more upside to come as investors gradually give up on repeated equity market bottom fishing and the hope of a return to financial market normalcy. A full reversal to the previous complacency cannot take place following a brief crash. The mood change will more likely become pervasive after grueling stretches of disappointing returns from previously successful investment strategies.

Unprecedented Central Bank Monetary Expansion

In our view, the decade preceding 2020 was characterized by the systematic stifling of price discovery for interest rates and the appropriate dependent valuations for financial assets. Such distortion was made possible only by unprecedented central bank balance sheet expansion that encouraged, abetted and rewarded risk taking in the form of ever greater leverage.

The prolonged somnolence of gold was among the most egregious price distortions of the previous decade and this suppressed interest in the metal as a risk mitigator and portfolio diversifier. Disinterest was fed in large part by the nearly universal expectation that the past would always be prologue and that highly leveraged financial and economic structures would perpetually result in outsized returns. In our view, the greatest change stemming from the credit bust will be a mood shift or paradigm change in the opposite direction.

At gold’s previous peak in 2011, the combined balance sheets of the U.S. Federal Reserve (“U.S. Fedâ€) and the European Central Bank (“ECBâ€) totaled approximately US$5.5 trillion. Today, that number is more than $11.4 trillion and rapidly moving higher. The USD gold price is still lower than nine years ago. In our view, gold price is still well below where it should be and will likely trade higher in the new macro landscape.

Figure 2. Pandemic Policy Response Pushes Global Balance Sheets to Record Levels Source: Bloomberg. Data as of 3/31/2020.

Gold Mining Stocks are Inexpensive

If gold is not correctly priced for what has transpired and what lies ahead, gold mining stocks are even more inappropriately priced. Based on current metal prices, most companies are generating positive earnings and cash flow and in many cases, free cash flow that can be applied to higher dividend payouts. Compared to other sectors of the economy, the gold mining industry stands almost alone in looking forward to strong 2020 earnings and a positive outlook for 2021.

2020 free cash flow yields for large-cap producers range from 3%-7% and 6%-25% for intermediate producers based on conventional sell-side research. The stats are similar or better for 2021 based on spot gold prices. As Figure 3. shows, mining stocks are inexpensive in absolute terms and have never been so cheap relative to the gold price.

Figure 3. Gold Equities Are Undervalued Relative to Bullion Ratio of XAU Index to Spot Gold (12/23/1983-3/31/2020)

Since 2008, the relative valuation of gold equities to gold bullion has fallen 75% from the prior 25-year average. The ratio of the XAU Index to spot gold averaged 0.2497x for a quarter century through 2008. As of 3/31/2020, the ratio was 0.0501x.

It is undoubtedly true that the industry will suffer health-related mine shutdowns and other shortfalls this year. Much of the disruption potential has already been broadcast and priced into the market. Some downside news may still have yet to surface. However, most miners are not financially levered and should be able to survive a few quarters of lower or no production. Unlike the airline, leisure, retail and manufacturing sectors, gold not produced today should grow in value and be produced at higher prices and lower costs next year and those beyond. It is not the same story for many other sectors of the economy. Based on fundamentals, gold stocks are inexpensive. By contrast, several other sectors of the economy could face long stretches of poor earnings, bad news flow and financial woes.

The gold mining sector registered a decline of approximately 20% in Q1 (as measured by GDX2) as shares did get battered by indiscriminate liquidations during March. However, as of this writing, two weeks after the close of the quarter, most shares trade near to where they stood at the beginning of the year, and have certainly registered outstanding performance in relative terms. It is remarkable that the largest sector ETF, GDX, suffered outflows of $381 million3 during the quarter at what could be the threshold of an upside breakout. In a favorable cycle for the gold price, mining stocks have historically delivered outperformance 3 to 5 times that of the metal itself.

Gold mining shares continue to be viewed by investors with deep skepticism as reflected by valuation and flows. When we scan Figure 4, it appears to us that the sector is on the verge of an upside breakout from a multi-year base should our assessment of the macroeconomic environment prove correct.

Figure 4. NYSE Arca Gold BUGS Index (HUI4)

Monetary and Fiscal Policy Going Ballistic

There is no need to belabor the obvious. However, the consequences of these actions have yet to be priced into the financial markets or gold. The risk parity trade has fallen short, partly because bonds were caught up in the indiscriminate liquidations of Q1. Looking forward, bonds may no longer be able to play the safe haven role they traditionally filled to balance equity risk. The vacuum could be filled in part by increased gold exposure for all classes of investors. Sovereign credit liquidity injections are likely to remain significant and permanent. The bond market has become socialized. Owning Treasury bonds of any duration could become akin to parking Treasury bills, with little upside and considerable risk of impairment through inflation. Gold is the antidote to the fixed-income investor’s dilemma.

Gold is extremely under-owned, under-represented, and poorly thought of in the circles of conventional investment thinking. It is still considered to be a fringe asset. Just ask Goldman Sachs which recently advised its clients:

“We concluded then (2010) that gold does not have a role as a strategic asset class in clients’ already well-diversified portfolios. We have updated the research and the evidence is even more compelling today than it was then.” (4/5/2020; Goldman Sachs Investment Strategy Group)

We remind the reader that Goldman is the same firm that in December 2019 declared the U.S. economy to be “recession proof†and then in March 2020 cautioned that stocks had substantial further downside:

“Overall, the changes underlying the Great Moderation appear intact, and we see the economy as structurally less recession prone today.†(12/31/2019; Goldman economists Jan Hatzius and David Mericle)

“Goldman Sachs on Friday dramatically cut its U.S. economic forecast, saying it now expects GDP to decline by 25% in the second quarter of 2020 because of the coronavirus panic.†(3/20/2020; Business Insider)

“What is your estimate for the S&P 500 by yearend 2020? David Kostin, “3400.†(1/2020; GS Podcast, David Kostin Goldman, U.S. chief equity strategist and Jake Siewert)

“Kostin thinks the market goes lower. ‘In the near term, we expect the S&P 500 will fall towards a low of 2000.’†(3/22/2020; Yahoo Finance)

Goldman’s commentary is, in our opinion, a reasonable proxy for conventional wisdom. One could easily find other embarrassing examples of mainstream thinking ignorant of the best-performing asset class (by far) versus equities and bonds since 2000.

Contrarians and value investors, take note! The secular gold bull that began in 2000 and corrected for a few years has returned to life with renewed vigor. Pullbacks — price declines during this uptrend — should be bought. The setup for gold and gold mining shares ticks every box for highly rewarding investment returns.

Figure 5. Gold Has Outperformed Stocks, Bonds and USD over the Past 20 Years Returns for Period from 12/31/1999-4/13/2020 Source: Bloomberg. Period from 12/31/1999-4/20/2020. Gold is measured by GOLDS Comdty; US Agg Bond Index is measured by the Bloomberg Barclays US Agg Total Return Value Unhedged USD (LBUSTRUU Index); S&P 500 TR is measured by the SPX; and the U.S. Dollar is measured by DXY Curncy. Past performance is no guarantee of future results.

Figure 6. Gold Provides Portfolio Diversification Gold provides diversification in a portfolio, and has low correlation with other asset classes. The period measured is April 1, 2015 to April 1, 2020.

* Source: World Gold Council. Period from April 1, 2015 to April 1, 2020, based on monthly returns. Gold is measured by the LBMA Gold Price; stocks by the S&P 500 Index; commodities by the Bloomberg Commodity Index;Â Bonds by the BarCap Treasuries and Corporates.

1

The S&P 500 or Standard & Poor’s 500 Index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. You cannot invest directly in an index. TR, “Total Return”, represents the index with dividend income reinvested.

2

VanEck Vectors Gold Miners ETF (GDX) seeks to replicate the NYSE Arca Gold Miners Index (GDMNTR), which is intended to track the overall performance of companies involved in the gold mining industry.

3

Source: ETFtrends.com.

4

The NYSE Arca Gold BUGS Index (HUI) is a modified equal dollar weighted index of companies involved in gold mining.

Posted by AGORACOM

at 11:05 AM on Monday, May 11th, 2020

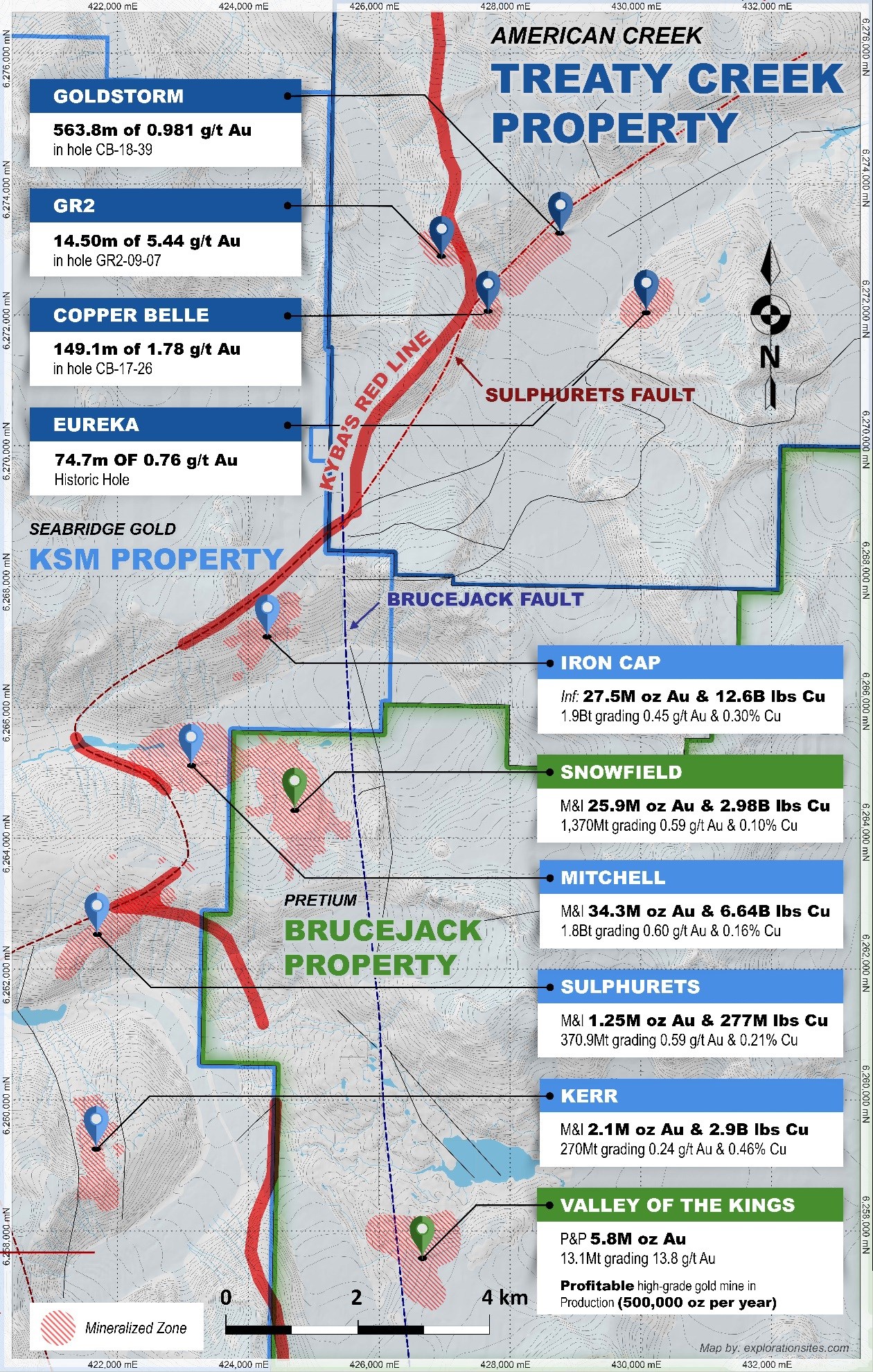

The length of the northeast axis of the Goldstorm System is over 850 meters

The Southeast axis is at least 600m

The system remains open in both dimensions, as well as to depth.

The strongest mineralization encountered to date is from two consecutive 150m step-out holes at the northeast end of the drill grid: GS-19-42 yielded0.849 g/t Au Eq over 780 m with the 300 Horizon averaging 1.275 g/t Au Eq over 370.5m and GS-19-47 yielded 0.697 g/t Au Eq over 1,081.5m with the 300 Horizon averaging 0.867 g/t Au Eq over 301.5m.

Program focused on expanding the mineralized area from these two very encouraging step-out holes.

Furthermore, we plan to continue advancing along the NE axis with yet another 150 meter step out hole. The best results from the southeast dimension came from GS-19-52 which yielded 0.783 g/t Au Eq over 601.5m with 1.062 g/t Au Eq over 336.0m within the 300 Horizon.“

Cardston, Alberta–(Newsfile Corp. – May 11, 2020) – American Creek Resources Ltd. (TSXV: AMK) (“the Corporation”) is pleased to report that its JV partner Tudor Gold Corp has begun this season’s diamond drill hole program at its flagship property, Treaty Creek, located in the heart of the Golden Triangle of Northwestern British Columbia. Diamond drilling has begun with two drill rigs on the Goldstorm Zone which is on-trend from Seabridges’ KMS Project located just five kilometers to the southwest. These first two drills have begun drilling the initial holes of the 20,000 meter exploration program.

Tudor Gold’s Vice President of Project Development, Ken Konkin, P.Geo., states: “We are very proud of the hard work and dedication that our crews exhibited during the weeks prior to the start of drilling. Due to their diligence in preparing the camp we have been able to start our drill program a month earlier than last year’s program. The priority is to continue to expand the Goldstorm System to the southeast and to the northeast.”

“The current known length of the northeast axis of the Goldstorm System is over 850 meters, and the southeast axis is at least 600 m; the system remains open in both dimensions, as well as to depth. The strongest mineralization encountered to date is from two consecutive 150m step-out holes at the northeast end of the drill grid: GS-19-42 yielded0.849 g/t Au Eq over 780 m with the 300 Horizon averaging 1.275 g/t Au Eq over 370.5m and GS-19-47 yielded 0.697 g/t Au Eq over 1,081.5m with the 300 Horizon averaging 0.867 g/t Au Eq over 301.5m. Our program will be focused on expanding the mineralized area from these two very encouraging step-out holes. Furthermore, we plan to continue advancing along the NE axis with yet another 150 meter step out hole. The best results from the southeast dimension came from GS-19-52 which yielded 0.783 g/t Au Eq over 601.5m with 1.062 g/t Au Eq over 336.0m within the 300 Horizon.“

(The above results were from Tudors news release dated March 3rd, 2020,, in which the following metal prices were used to calculate the Au Eq metal content: Gold $1322/oz, Ag: $15.91/oz, Cu: $2.86/lb. Calculations used the formula Au Eq g/t = (Au g/t) + (Ag g/t x 0.012) + (Cu% x 1.4835). All metals are reported in USD and calculations do not consider metal recoveries. True widths have not been determined as the mineralized body remains open in all directions. Further drilling is required to determine the mineralized body orientation and true widths.)

Tudor Gold and its associated service companies have taken extreme measures to maintain the highest professional standards while working under COVID-19 health and safety protocols. Only essential personnel are permitted to enter the camp and staging areas. An on-site certified paramedic conducts strict daily monitoring of temperatures and general health conditions of personnel and service providers who are working at the project site and the staging area.

Walter Storm, Tudor President and CEO, stated: “I am very pleased with the safe start-up of the 2020 exploration program thanks to the hard work and dedication of our crews. The Company’s intent is to advance the Treaty Creek Project with full recognition and confidence in the recommended COVID-19 safety protocols. The goal for this year is to complete enough drilling that we can begin to delineate a first resource estimation at Treaty Creek.”

Darren Blaney, American Creek President and CEO stated: “2019 was a very successful year at Treaty Creek and this year looks to be far better with an extension of the drilling season and a drill program that is over twice as big as last years. With the recent announcement of working towards a resource calculation along with baseline studies and metallurgical work for an initial economic assessment, Mr Storm was right in calling this a transformational year at Treaty Creek.”

Qualified Person

The Qualified Person for this news release for the purposes of National Instrument 43-101 is the Company‘s Vice President of Project Development, Ken Konkin, P.Geo. He has read and approved the scientific and technical information that forms the basis for the disclosure contained in this news release.

Treaty Creek JV Partnership

The Treaty Creek Project is a Joint Venture with Tudor Gold owning 3/5th and acting as operator. American Creek and Teuton Resources each have a 1/5th interest in the project creating a 3:1 ownership relationship between Tudor Gold and American Creek. American Creek and Teuton are both fully carried until such time as a Production Notice is issued, at which time they are required to contribute their respective 20% share of development costs. Until such time, Tudor is required to fund all exploration and development costs while both American Creek and Teuton have “free rides”.

Treaty Creek Background

The Treaty Creek Project lies in the same hydrothermal system as Pretium’s Brucejack mine and Seabridge’s KSM deposits with far better logistics.

American Creek is a Canadian junior mineral exploration company with a strong portfolio of gold and silver properties in British Columbia. Three of those properties are located in the prolific “Golden Triangle”; the Treaty Creek and Electrum joint venture projects with Tudor Gold/Walter Storm as well as the 100% owned past producing Dunwell Mine.

The Corporation also holds the Gold Hill, Austruck-Bonanza, Ample Goldmax, Silver Side, and Glitter King properties located in other prospective areas of the province.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com

Posted by AGORACOM-JC

at 9:42 AM on Monday, May 11th, 2020

Secured non-exclusive rights to COVID-19 test kits with Health Canada approval,

Kingdom of Saudi Arabia, Saudi Food & Drug Authority approval, and

CE marking certification for European Economic Area countries, which covers the 27 member states of the EU, the 4 members of EFTA, plus Turkey and the United Kingdom under Brexit.

latest, and fourth kit to be added by Datametrex to distribute is the 1copy™ COVID-19 qPCR Multi Kit

Datametrex anticipates that it will have little or no upfront costs associated with importing and selling these test kits.

TORONTO, May 11, 2020 — Datametrex AI Limited (the “Company†or “Datametrexâ€) (TSXV: DM, FSE: D4G, OTC: DTMXF) is pleased to announce that it has secured non-exclusive rights to COVID-19 test kits with Health Canada (“HCâ€) approval, Kingdom of Saudi Arabia, Saudi Food & Drug Authority (“SFDAâ€) approval, and CE marking certification (“CEâ€) for European Economic Area (“EEAâ€) countries, which covers the 27 member states of the EU, the 4 members of EFTA, plus Turkey and the United Kingdom under Brexit.Â

The latest, and fourth kit to be added by Datametrex to distribute is the 1copy™ COVID-19 qPCR Multi Kit (“qPCR kitâ€), which is Health Canada approved with Authorization Reference Number 312777, Device ID 1020660 and Model No. M22MD100. It is a nucleic test kit providing results in less than two hours that verifies the RdRp gene for SARS-CoV-2 with real-time qPCR kit via a nasopharyngeal swab and oropharyngeal swab, specifically targeting the E gene sequences of COVID-19. The kits are made by 1drop Inc. (“1dropâ€) in South Korea, and are immediately ready for sales orders in Canada.

1drop is located in South Korea and is a medical technology spin-off from Samsung Electronic’s C-Lab program. The C-Lab is an internal incubation program within Samsung that first started in 2012 to help inspire a more creative company culture. 1drop already has more than five products approved in Europe in the past 18 month under the CE marking certification. “CBC News reported that Canada lost almost two million jobs during the month of April as the impact of COVID-19 according to Stats Canada’s release on May 8, 2020. The team has been working around the clock to identify and source high quality test kits from South Korea for Canada. We are thrilled to have secured the rights to sell kits from 1drop, Health Canada approved manufacturer. We will be able to start filling orders immediately and are looking forward to help flatten the curve and get Canadians back to work safely,†says Marshall Gunter, CEO of the Company.

The Company’s ability to fulfill any purchase order for COVID-19 test kits is subject to the availability of inventory at the time of order. Due to the extraordinarily high demand for COVID-19 tests, there is volatility in the supply chain, and available supply may fluctuate on a daily basis.

Datametrex anticipates that it will have little or no upfront costs associated with importing and selling these test kits. Assuming these test kits are purchased by the Canadian Government, the manufacturer will ship the test kits directly to the Canadian government or hospitals, and Datametrex will not be involved in the shipping, warehousing, or distribution process.

The Company did not pay consideration to the manufacturer to obtain sales rights.

The Company granted 16,500,000 incentive stock options to its directors, officers, employees and consultants in accordance with the Company’s Stock Option Plan. These stock options have an exercise price of $0.17 and expire on June 30, 2022. All options will be subject to a vesting schedule, with 25% immediately vesting and 25% vesting on the three, six and nine month anniversaries of the grant date.

About CE Marking

CE marking is a certification mark that indicates conformity with health, safety, and environmental protection standards for products sold within the European Economic Area (EEA). The CE marking is also found on products sold outside the EEA that have been manufactured to EEA standards. This makes the CE marking recognizable worldwide even to people who are not familiar with the European Economic Area (the 27 member states of the EU, the 4 members of European Free Trade Association (“EFTAâ€), plus Turkey and United Kingdom). CE marking also supports fair competition by holding all companies accountable to the same rules. For more information please consult the European Commission website at: CE marking

About Kingdom of Saudi Arabia, Saudi Food & Drug Authority (“SFDAâ€)

The Saudi Food & Drug Authority (SFDA) is the government agency that regulates drugs and medical devices in Saudi Arabia. It is also in charge of biological and chemical substances, as well as electronic products. The agency was established under the Council of Ministers and functions under the Council of Ministers as an independent body that reports to the President of Council of Ministers.

SFDA is in charge of overseeing the safety, security and effectiveness of medical devices, ensuring their accuracy, and controlling and supervising manufacturing facilities, as well as overseeing the importation and registration of these products.

A list of regulations can be found here on SFDA website.

About 1drop Inc.

1drop is located in Jungwon-gu, South Korea, and was incorporated in 2017 following a technology spin-off from Samsung Electronic’s C-Lab program. Samsung Electronic’s C-Lab, located in South Korea is an internal incubation program that first started in 2012 to help inspire a more creative company culture. 1drop already had more than five products approved in Europe in the past 18 month under CE marking is a certification.

For more information please consult the website at: 1drop

About Datametrex

Datametrex AI Limited is a technology focused company with exposure to Artificial Intelligence and Machine Learning through its wholly owned subsidiary, Nexalogy (www.nexalogy.com). Additional information on Datametrex is available at www.datametrex.com

For further information, please contact:

Marshall Gunter – CEO Phone: (514) 295-2300 Email: [email protected]

Neither the TSX Venture Exchange nor it’s Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) accepts responsibility for the adequacy or accuracy of this release.

Forward-Looking Statements

This news release contains “forward-looking information†within the meaning of applicable securities laws. All statements contained herein that are not clearly historical in nature may constitute forward-looking information. In some cases, forward-looking information can be identified by words or phrases such as “mayâ€, “willâ€, “expectâ€, “likelyâ€, “shouldâ€, “wouldâ€, “planâ€, “anticipateâ€, “intendâ€, “potentialâ€, “proposedâ€, “estimateâ€, “believe†or the negative of these terms, or other similar words, expressions and grammatical variations thereof, or statements that certain events or conditions “may†or “will†happen, or by discussions of strategy.

Readers are cautioned to consider these and other factors, uncertainties and potential events carefully and not to put undue reliance on forward-looking information. The forward-looking information contained herein is made as of the date of this press release and is based on the beliefs, estimates, expectations and opinions of management on the date such forward-looking information is made. The Company undertakes no obligation to update or revise any forward-looking information, whether as a result of new information, estimates or opinions, future events or results or otherwise or to explain any material difference between subsequent actual events and such forward-looking information, except as required by applicable law.

Posted by AGORACOM

at 7:37 AM on Monday, May 11th, 2020

VANCOUVER, BC / ACCESSWIRE / May 11, 2020 / Mota Ventures Corp. (CSE:MOTA)(FSE:1WZ:GR)(OTC PINK:PEMTF) (the “Company“) subsidiary, Nature’s Exclusive, an ecommerce provider of CBD products to consumers in the United States and Europe, is pleased to announce record revenues for the month of April totaling Cdn$3,818,000, representing an increase of 39% compared to April 2019. Expenses totaled Cdn$3,609,000, representing a Gross Profit of Cdn$209,000 for the month.

DOMINANT ONLINE CUSTOMER ACQUISITION STRATEGY

The Company credits this success to its’ online customer acquisition strategy, which is capitalizing on the strong consumer demand for natural health solutions, resulting in an interim record number of customer acquisitions for the Nature’s Exclusive brand, as well as, new customers for the immune support category introduced in March 2020.

The Company’s strong ability to continue capturing customers, for both existing and new products, bodes well for the Company’s CBD based hand sanitizer launch this month.

Ryan Hoggan, CEO of the Company stated, “I am very pleased to report another successful month with increased sales over 2019. Our investment in customer acquisition in March 2020, which yielded additional subscribers, has been a significant driver to our increased profitability. Despite the worldwide pandemic, we continue to move forward towards our full year goals for 2020, including expansion into the European market. I look forward to reporting on new customer acquisitions in the coming weeks”.

NATURE’S EXCLUSIVE CBD BRAND LEADING THE WAY

The Company’s Nature’s Exclusive brand offers a CBD hemp-oil formulation intended to provide users with the therapeutic benefits that hemp may offer. The hemp oil used in the products is derived from hemp grown and cultivated in the United States. The extraction process is designed to maintain all the beneficial qualities that hemp may offer. Nature’s Exclusive offers a range of products, which include CBD oil drops, CBD gummies, CBD pain relief cream, CBD skin serum, CBD hand sanitizer and CBD coffee.

We encourage readers to visit www.motaventuresco.com to view our brands and sign up to our newsletter.

We encourage shareholders and prospective investors to visit the Company’s AGORACOM Discussion Forum, a moderated social media platform that enables civilized discussion and Q&A between Management and Shareholders.

The Company cautions that figures for revenue, expenses and margin generated from the sale of Nature’s Exclusive products have not been audited, and are based on calculations prepared by management. Actual results may differ from those reported in this release once these figures have been audited. These figures were translated from US dollars into Canadian dollars using the Bank of Canada monthly average exchange rate of US$1.00:Cdn$1.4058 for April 2020 and US$1.00:Cdn$1.3378 for April 2019.

About Mota Ventures Corp.

Mota is an established ecommerce, direct to consumer provider of a wide range of CBD products in the United States and Europe. In the United States, the company sells a CBD hemp-oil formulation derived from hemp grown and formulated in the US through its Nature’s Exclusive brand. Within Europe, its Sativida brand of award winning 100% organic CBD oils and cosmetics are sold throughout Spain, Portugal, Austria, Germany, France, and the United Kingdom. Mota Ventures is also seeking to acquire additional revenue producing CBD brands and operations in both Europe and North America, with the goal of establishing an international distribution network for CBD products. Low cost production, coupled with international, direct to customer, sales channels will provide the foundation for the success of Mota Ventures.

ON BEHALF OF THE BOARD OF DIRECTORS

MOTA VENTURES CORP.

Ryan Hoggan

Chief Executive Officer

For further information, readers are encouraged to contact Joel Shacker, President at +604.423.4733 or by email at [email protected] or www.motaventuresco.com

Posted by AGORACOM-JC

at 9:45 PM on Sunday, May 10th, 2020

SPONSOR: Hollister Biosciences Inc. (HOLL:CSE) A vertically integrated cannabis company with products in 220 California dispensaries and joint ventures, licensing agreement & partnerships with global brands. The company recently closed $20 MILLION deal with Venom Extracts adding $CDN 16.4 million in revenue and $CDN 2.48 million in EBITDA. Learn More

How The Cannabis Industry Is Coping In 2020

Canada and most U.S. states with legalized cannabis industries declared dispensaries as essential services, allowing sales to continue throughout the COVID-19 crisis, enabling robust demand to be met

Even with strong sales momentum, cannabis stocks broadly suffered during the quarter amid heightened market volatility

Early-stage cannabis companies rely heavily on external capital to fuel their growth ambitions, but investors are stepping back from financing riskier industries in the current environment

Despite these near-term challenges, we remain optimistic on the longer-term prospects for cannabis as its acceptance grows

Amid widespread COVID-19-related retail store closures, many cannabis dispensaries received “essential business” designations. This allowed cannabis consumers to stock up on medicinal and recreational cannabis, fueling strong sales figures despite a tumultuous Q1 2020. Yet, even with strong sales momentum, cannabis stocks broadly suffered during the quarter amid heightened market volatility. Early-stage cannabis companies rely heavily on external capital to fuel their growth ambitions, but investors are stepping back from financing riskier industries in the current environment. Some cannabis companies are now running low on cash, forcing them to sell stakes at undesirable valuations or scale back operations or staffing.

Despite these near-term challenges, we remain optimistic on the longer-term prospects for cannabis as its acceptance grows. New store openings and the sale of edibles are helping to fuel greater legal consumption. In addition, COVID-19’s economic impact is broadly hurting tax revenues at the local, state, and federal level, potentially providing greater impetus to legalize and tax cannabis. With only about 10% of cannabis sales occurring through legal channels, we believe there is substantial opportunity for continued growth across regulated channels.

Is Cannabis A Consumer Staple?

The COVID-19 crisis is plunging the global economy into recession, yet its impact will not be felt equally across industries. During recessions, consumers may forgo discretionary items like jewelry or electronics, but staples such as essential food and beverages tend to see robust sales. Historically, alcohol and tobacco exhibit staples-like characteristics, demonstrating strong sales despite economic weakness. During the global financial crisis, for example, alcohol consumption increased 7.2% in 2008-09 from 2006-07 levels, while total sales in the consumer discretionary sector fell by -9.35% over that time frame.1,2

Legalized cannabis did not exist during the Great Recession, but recent figures suggest cannabis sales share similar characteristics with alcohol and tobacco. Canada and most U.S. states with legalized cannabis industries declared dispensaries as essential services, allowing sales to continue throughout the COVID-19 crisis, enabling robust demand to be met.

Online cannabis purchases in Ontario have surged from 5,000 orders in mid-March to 9,000 orders by mid-April.3

Oregon’s cannabis sales increased 37% year over year in March, its highest single-month increase.4

Between March 16th and March 22nd, year-over-year sales of recreational cannabis across key US markets, including California, Colorado, Oregon and Alaska, were up 50%.5

One of Nevada’s largest cannabis delivery businesses reported a 400% increase in cannabis retail deliveries since March 20th.6

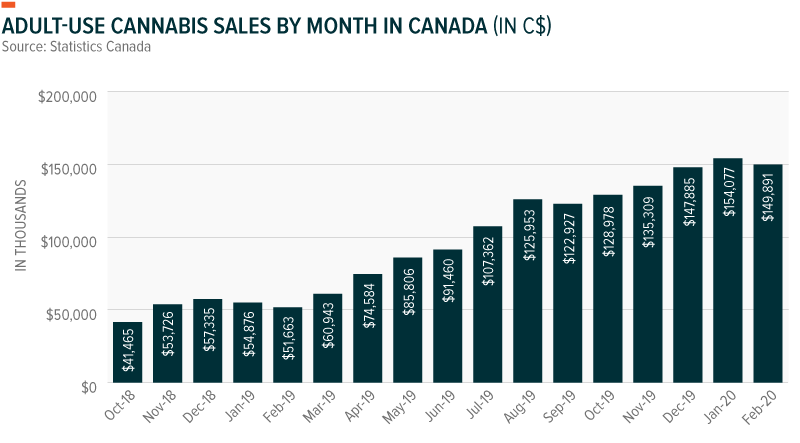

While lockdown may have accelerated cannabis demand, cannabis sales were already on an accelerating path. January and February sales numbers in Canada increased 181% year-over-year to C$154 million and 190% to C$150 million.7 Estimates from Cannabis Benchmarks for March sales show a spike to C$216 million, more than three times March 2019’s sales of C$59 million.8

The shift towards greater cannabis acceptance has spurred much of this growth. Cannabis consumers among the legal adult population in Canada grew to 63% at the end of 2019 from 54% in 2018.9

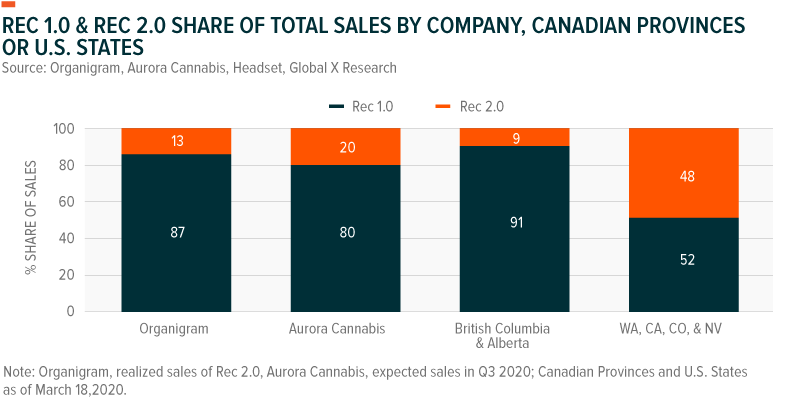

Canada’s new recreational cannabis market, dubbed Rec 2.0, is also fueling growth. Rec 2.0 officially launched at the end of 2019, almost a year after legalization in Canada. Before Rec 2.0, only dried flower and oil were products sold, but now the sale of cannabis beverages, edibles and vapes, among other forms, is permitted. Derivative formats like these account for almost half of sales in mature and developed markets such as Colorado, showing how Rec 2.0 could play a major role in accelerating cannabis sales in Canada. Aurora Cannabis (ACB), for example, recently mentioned that approximately 20% of total sales could come from Rec 2.0 products.10 OrganiGram Holdings (OGI) also reported new Rec 2.0 products to account for 13% of total revenue in its most recent quarter.11

New Store Openings Grow Legal Cannabis’s Market Share

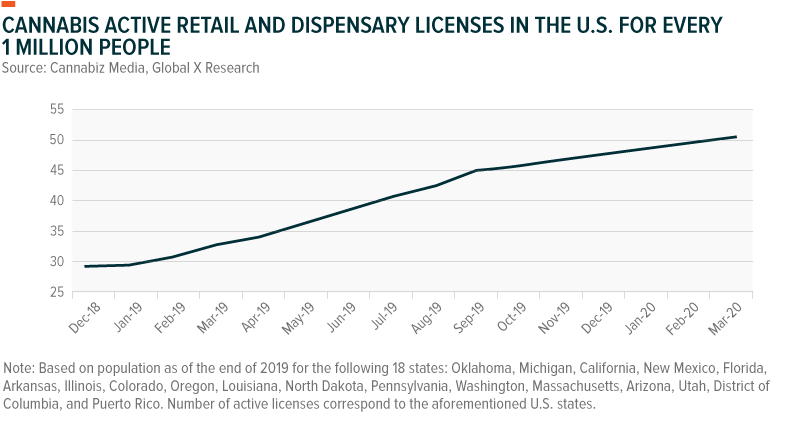

Curbing illicit cannabis sales is on the agenda for many governments around the world. Globally, legal cannabis sales reached $15 billion at the end of 2019, which is less than 10% of the estimated total market of $160 billion.12 Such low penetration both demonstrates the growth opportunity ahead as well as highlights some of the challenges for the legal market. In Canada, for instance, limited dispensary licenses plays a major factor, as recreational cannabis sales per capita are highly correlated to the number of stores.

In Q1 2020, Canada opened 191 new stores, bringing its total to 806.13 Ontario, Canada’s most populous province, now has 52 stores, versus just 27 at the end of 2019. But the few dozen stores represent just four per 1 million people. For comparison, Colorado has 180 stores for every 1 million people.14 The store comparison between the two countries is notable, as further licenses should help meet consumer demand and promote greater legal sales.

Within the U.S., active dispensary licenses are up 5.5% year-to-date, with 385 new stores opening around the country.15 Yet, given that the US has nine times more dispensary licenses than Canada, more stores is a less critical factor than wider legalization across populous states or at the broader federal level.

Cannabis Industry Leveraging E-commerce To Further Grow Sales

Oftentimes, crises breed both new problems and new solutions. During this social distancing era, Colorado legalized online sales of recreational cannabis, fulfilling a longstanding request from cannabis companies.16 Cannabis consumers can now order, pay online and pick up at-store. A few other states – Massachusetts, Illinois, Michigan and Oregon – already allow cannabis e-commerce.

In Canada, the Alcohol and Gaming Commission of Ontario (AGCO) authorized cannabis retail stores to offer e-commerce solutions, starting April 7th.17 E-commerce authorization resulted from an emergency order by the Government of Ontario to deter illegal cannabis sales amid physical distance mandates. For now, the measure is temporary, but it includes the possibility of extension.

Financing Cannabis’s Growth

Early-stage industries tend to rely on the capital markets to fund growth. The phenomenon describes a healthy dynamic between those with capital to invest and those seeking capital for growth. The cannabis industry is particularly dependent on capital, as growing, harvesting, packaging and distribution require property, equipment and employees. With high growth expectations, cannabis companies tend to plow their freshly raised capital into various parts of the ecosystem, leaving little cash available to weather a storm. The constant need for new financing can expose weaker companies that may need to raise capital at undesirable terms, or worse, cannot raise additional capital at all.

HEXO Corp. (HEXO), for example, a leading cannabis grower in Canada, recently closed a C$46 million public offering but was forced to sell its equity 20% below its last traded price.18 Other larger players have followed suit, like Tilray (TLRY), which raised C$90 also at a 20% discount.19

There are companies, however, with strong cash positions that may be able to weather this challenging financing environment better than others. Canopy Growth Corp. (CGC) and Cronos Group (CRON) both have over $1 billion in cash & equivalents on their balance sheets. GW Pharmaceuticals (GWPH) holds over $500 million in cash & equivalents. Balance sheet strength allows these companies to potentially wait longer before needing to raise additional outside capital.

COVID-19 Could Expedite Cannabis Legalization

In our article “Themes for Defensive Positioning,” we highlighted that economic downturns can accelerate efforts to find new sources of economic stimulus and tax revenue. Legalizing (and taxing) recreational cannabis is one such avenue states could pursue given its track record of generating economic growth and taxes. Estimates hold that nationwide legalization in the U.S. could generate $132 billion in aggregate tax revenue and more than a million new jobs across the country by 2025.20 Such growth comes not from an unproven, speculative market, but from the conversion of a largely illicit market to a legal, regulated one. Such taxes and economic growth could be particularly welcome given stalling economic growth and swelling debt caused by COVID-19.

This year, several states could legalize recreational use. Virginia recently decriminalized cannabis, joining 27 other states that have taken such actions.21 The bill doesn’t legalize cannabis sales yet, but Virginia’s Governor is also clearing the path for easier access for medicinal uses.22 In New Jersey, lawmakers voted to add legalization to November’s ballot. Should the bill pass, it could add additional pressure to neighboring New York and Connecticut.

Illinois, where legalized cannabis went into effect in January, is the most recent model other states could follow. Illinois has the second-highest tax regime on cannabis sales in the country, where taxes vary from 10% to 25%.23 In Q1, Illinois cannabis stores sold $110 million, generating at least $11 million in tax revenues. Another benchmark is Colorado, which legalized cannabis in 2014. In Q1 2020, Colorado generated $79 million in tax revenue from cannabis-related sales.24 In 2019 alone, the state collected over $300 million in tax revenue, which was earmarked for cannabis regulation, research and schools.25

With a global recession looming, the economic benefits of legalized cannabis could be too enticing for states, provinces and countries to ignore.

Conclusion

The recent increase in cannabis sales in the U.S. and Canada since COVID-19 reflects the non-cyclical nature of cannabis sales. While some cannabis companies may struggle from lack of access to capital during this volatile period, the stronger ones could continue to see substantial growth as they meet robust consumer demand. Trends in new dispensary openings, a shift to e-commerce, and the introduction of new consumable forms of cannabis should further fuel growth across North America. Longer term, the potential for further legalization efforts amid the COVID-19 crisis should provide a tailwind to the industry.

Related ETFs

POTX: The Global X Cannabis ETF seeks to invest in companies across the cannabis industry. This includes companies involved in the legal production, growth and distribution of cannabis and industrial hemp, as well as those involved in providing financial services to the cannabis industry, pharmaceutical applications of cannabis, cannabidiol (i.e., CBD), or other related uses including but not limited to extracts, derivatives or synthetic versions.

Please click on the fund name for current holdings.

Footnotes

1. Jacob Bor, et al. “Alcohol Use During the Great Recession of 2008-2009,” January 29, 2013.

2. U.S. Census Bureau. Discretionary sales including retail sales of Motor Vehicles & Parts, Furnitures, Electronics & Appliances, Clothing, Sporting Goods, General Merchandise, and Miscellaneous Stores. Accessed on April 2020.

3. Cannabis Benchmarks, “Canada Cannabis Spot Index (CCSI)”, April 17, 2020.

4. Willamette Week, “Oregon Cannabis Sales in March Were the Highest Ever for a Single Month,” April 6, 2020.

5. New York Post, “Cannabis sales hit new highs in US and Canada,” March 24, 2020

6. Reno Gazette Journal, “Nevada marijuana deliveries are skyrocketing. Is this the new normal for the pot industry?,” March 30, 2020.

7. Statistics Canada, “Cannabis Stores Sales,” Accessed on April 2020.

8. Cannabis Benchmarks, (n3).

9. BDS Analytics, “How Will “Cannabis 2.0″ Affect the Legal Canadian Market?,” February 18, 2020.

16. The Colorado Sun, “Coronavirus fuels marijuana industry’s push for online sales, delivery in Colorado,” April 13, 2020.

17. Alcohol and Gaming Commission of Ontario, “Ontario Allows Cannabis Delivery and Curbside Pick-up from Authorized Retail Stores During COVID-19,” April 7, 2020.

18. Hexo Corp, “HEXO Corp. Closes $46 Million Underwritten Public Offering,” April 13, 2020.

19. Tilray, “Tilray, Inc. Announces Pricing of its $90.4 Million Registered Offering,” March 13, 2020.

20. The Washington Post, “Study: Legal marijuana could generate more than $132 billion in federal tax revenue and 1 million jobs,” January 10, 2018.

21. Leafly, “Virginia just decriminalized marijuana. Here’s what that means,” April 13, 2020.

22. Marijuana Moment, “Virginia Governor Urges Medical Marijuana Expansion As Amendment To Recently Approved Bill,” April 15, 2020.

23. Illinois Policy, “What you need to know about marijuana legalization in Illinois?,” January 1, 2020.

24. Colorado Department of Revenue, “Marijuana Tax Data,” April 2020.

25. Ibis.

Investing involves risk, including the possible loss of principal. The investable universe of companies in which POTX may invest may be limited. The Fund invests in securities of companies engaged in Healthcare and Pharmaceutical sectors. These sectors can be affected by government regulations, expiring patents, rapid product obsolescence, and intense industry competition. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from social, economic or political instability in other nations. POTX is non-diversified.

POTX’s investments are concentrated in the cannabis industry, and the Fund may be susceptible to loss due to adverse occurrences affecting this industry. The cannabis industry is a very young, fast evolving industry with increased exposure to the risks associated with changes in applicable laws (including increased regulation, other rule changes, and related federal and state enforcement activities), as well as market developments, which may cause businesses to contract or close suddenly and negatively impact the value of securities held by the Fund. Cannabis Companies are subject to various laws and regulations that may differ at the state/local, federal and international level. These laws and regulations may significantly affect a Cannabis Company’s ability to secure financing and traditional banking services, impact the market for cannabis business sales and services, and set limitations on cannabis use, production, transportation, export and storage. The possession, use and importation of marijuana remains illegal under U.S. federal law. Federal law criminalizing the use of marijuana remains enforceable notwithstanding state laws that legalize its use for medicinal and recreational purposes. This conflict creates volatility and risk for all Cannabis Companies, and any stepped-up enforcement of marijuana laws by the federal government could adversely affect the value of the Fund’s investments. Given the uncertain nature of the regulation of the cannabis industry in the United States, the Fund’s investment in certain entities could, under unique circumstances, raise issues under one or more of those laws, and any investigation or prosecution related to those investments could result in expense and losses to the Fund.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions will reduce returns. Global X NAVs are calculated using prices as of 4:00 PM Eastern Time. The closing price is the Mid-Point between the Bid and Ask price as of the close of exchange. Closing price returns do not represent the returns you would receive if you traded shares at other times. Indices are unmanaged and do not include the effect of fees, expenses or sales charges. One cannot invest directly in an index.

Since the Fund’s shares did not trade in the secondary market until several days after the Fund’s inception, for the period from inception to the first day of secondary market trading in Shares, the NAV of the Fund is used to calculate market returns.

Global X Management Company LLC serves as an advisor to Global X Funds. The Funds are distributed by SEI Investments Distribution Co. (SIDCO), which is not affiliated with Global X Management Company LLC or Mirae Asset Global Investments. Global X Funds are not sponsored, endorsed, issued, sold or promoted by Solactive AG, nor does Solactive AG make any representations regarding the advisability of investing in the Global X Funds. Neither SIDCO, Global X nor Mirae Asset Global Investments are affiliated with Solactive AG.

Tags: Cannabis, CBD, CSE, Hemp, small cap, tsx, tsx-v, weed Posted in Hollister Biosciences | Comments Off on How The #Cannabis Industry Is Coping In 2020 – SPONSOR: Hollister Biosciences $HOLL.ca $WEED.ca $CGC $ACB $APH $CRON.ca $OGI.ca $FAF.ca

Posted by AGORACOM-JC

at 9:30 PM on Sunday, May 10th, 2020

SPONSOR: Esports Entertainment Group(GMBL:NASDAQ) – Millions of people from around the world tune in to watch teams of video game players compete with each other. In first quarter 2020, YouTube reported 1.1 billion hours watched, an increase of 13% when compared to fourth quarter 2019. Wagering on Esports is projected to hit $23 BILLION this year although that number will likely be eclipsed due to the recent pandemic. Esports Entertainment Group is the next generation online gambling company designed for the purpose of facilitating as much of this wagering as possible. LEARN MORE.

CSGO has a million active players, is CSGO the best esports for tournaments?

With over a million active players playing CSGO it’s a huge game and with over 450 million esports fans worldwide. Of these 450 million fans 201 million are active players from League of Legends, Dota 2 and CSGO.

CSGO only recently hit the 1 million milestone. Previously at 950,000 and jumped to 1 million active users. In areas like China, CSGO is unpopular but the game is still clearly the most popular.

Looking at CSGO with Asiabet.org, sites like these offer a wide range of games and reviews that show how much esports fans love esports betting.

Big tournaments in the CSGO Esport universe provide the ability to inspire and improve your style by seeing the incredible talents of athletes representing your favourite team.

Please enjoy this list of the next CSGO 2020 tournaments if you share our enthusiasm. Don’t forget – the list is in progress, and when it is publicly released, we will include updates on other contests according to the CSGO tournament schedule.

Many tournaments have different formats, however, esports platforms have data on each match and data on all teams.

Most pro players do not only use different skins to customise their characters but also to personalise csgo settings.

List of the most-watched CSGO tournaments:

ESL One Cologne (506,000 viewers)

IEM Katowice (1,200,000)

StarLadder Berlin (838,000)

These tournaments see millions of views following the tournament due to esports fans not being able to watch the tournament live.

What is CSGO?

CSGO or lengthened to Counter-Strike: Global Offensive is the Valve and Secret Path Entertainment squad focused the first-person shooter, published in 2012. The name itself was a standalone game developed in 1999 and eventually adapted into a Valve game series.

Players play the role of a terrorist or counter-terrorist with each side having a particular task to achieve before they are eliminated by the opposing team, or according to the full timeline, such as, for example, planting and protecting a bomb on a specific location, while counter-terrorist agents must destroy the terrorists before they can be planted or re-armed

Esports fills the gap while sports declines

In recent years, global recognition on a different stage has been influenced by esports clubs, competitions and matches. The result was that the marketers were looking more and more at the sporting industry in the same way as they consider conventional American sport like basketball and football.

Earlier in this year, we saw leading brands like Nike, BT, and Kia Motors all partner with sports teams at Louis Vuitton’s then planned 2020 League of Legends World Championships.

With the advent of the pandemic of coronavirus, athletics have now another feature where the sporting industry maintains: widespread suspension of live activities and all the resulting destruction.

But one distinction with esports is that it is fairly well placed to change to the pandemic environment, given its increasing popularity for filling stages and arenas around the world. Live sporting competitions can be moved online very quickly, unlike conventional sporting. Even though IEM Katowice is absent from his usual live crowd, the annual Counter-Strike: Global Offensive (CSGO) game event set a new crowd record in early March, making it one of the most highly watched major tournaments ever.

It can only be the solution for the millions of fans whose regular activities are now held. Announcers are informed. So why are companies only just coming on board if they should have had an edge in the first mover?

Posted by AGORACOM-JC

at 9:00 PM on Sunday, May 10th, 2020

SPONSOR: New Age Metals Inc. The company owns one of North America’s largest primary platinum group metals deposits in Sudbury, Canada. The company has an updated NI 43-101 Mineral Resource Estimate of 2,867,000 PdEq Measured and Indicated Ounces, with an additional 1,059,000 PdEq Ounces Inferred. Learn More.

BAML sees platinum, palladium deficit this year as South Africa production losses bite

There is likely to be a deficit of platinum and palladium this year after a COVID-19 lockdown in South Africa, the world’s biggest platinum producer, forced mines to shut, analysts at Bank of America Merrill Lynch predicted on Friday

While demand for platinum group metals, which are mainly used in cars and jewellery, has also plummeted due to the global pandemic, the analysts said they expect demand to rebound, while mine production will take months to build back up.

By Helen Reid; Editing by Mark Potter

In South Africa, which produces 78% of the world’s platinum and 36% of palladium according to BAML, a strict lockdown to stop the spread of COVID-19 forced most mines to shut from March 27.

Though the government allowed mines to restart at up to 50% capacity from April 16, BAML analysts predict it will take six months for production to ramp back up to pre-pandemic levels.

“Our base line assumption is that output runs at 50% in May and June, before rising to capacity by December,” they wrote in a note dated May 7 but distributed to media on May 8.

“Putting it all together, we anticipate that both platinum and palladium will be in deficit this year. As such, we remain bullish the white metals into year-end.”

South Africa’s biggest platinum miners have cut production guidance for 2020 and announced production losses due to the lockdown.

Anglo American Platinum said quarterly production decreased by 7%, while Impala Platinum reported a 6% drop.

Analysts are split on how the demand-supply dynamics will play out: Citi on Wednesday predicted platinum group metals prices could fall 15-20% due to a “rising surplus”.

Platinum prices are down 20% since the start of the year, while palladium prices have fallen 3.6%.

Tags: CSE, palladium, PGM, PGM Demand, tsx Posted in New Age Metals | Comments Off on BAML sees #platinum, #palladium deficit this year as South Africa production losses bite – SPONSOR: New Age Metals $NAM.ca $WG.ca $XTM.ca $WM.ca $PDL.ca $GLEN #PGM

Posted by AGORACOM-JC

at 8:43 PM on Sunday, May 10th, 2020

Loncor Resources ( LN:TSX ) is the preeminent gold exploration company to own. Armed with a Barrick JV on their 200km NGAYU Greenstone property anticipates a maiden drill program on multiple targets in 2020. Loncor controls 3.6 million ounces of high grade gold outside of this relationship.

If the JV and Ounces aren’t enough to grab your attention, then look at ownership; African Majors own impressive pieces of Loncor:

Resolute Mining owns 27% and has a 30% ROFR on any Loncor financing,Â

Source: Bloomberg. Data as of 3/31/2020.

Source: Bloomberg. Data as of 3/31/2020.

{kind=link}