Posted by AGORACOM

at 9:38 AM on Wednesday, January 15th, 2020

Affinity Metals Corp. (TSXV: AFF) (“Affinity”) (“the

Corporation”) is pleased to release over-limit assays for samples from

the fall 2019 exploration on the Regal property located in the northern

end of the prolific Kootenay Arc approximately 35 km northeast of

Revelstoke, British Columbia, Canada.

As previously reported, the Corporation received assay results for all 22 rock samples collected from surface outcrops in September 2019 from the Black Jacket and ALLCO areas of the property. Of the 22 grab samples collected, the majority contained bonanza grade silver, zinc, and lead with many samples reaching assay over-limits. The over-limit results for zinc and lead are reported in the table below (italicized) beside the original assay values. Assay values for tin, including high grade samples 11, 14 and 20 which were over-limit in the original assay report, are also presented in the last column of the table.

Sample Number

Sample Type

Silver g/t

Copper %

Zinc %

Lead %

Gold g/t

Tin ppm

ALC19CR01

grab

0

.035

0

0

0

0.4

ALC19CR02

grab

1300

.415

18.20

>20.0 (35.69)

0.70

46.1

ALC19CR03

grab

120

.232

.034

.984

0.02

2.4

ALC19CR04

grab

131

.089

.026

.102

2.66

1.1

ALC10CR05

grab

16.7

.295

.060

.013

0.09

0.4

ALC19CR06

grab

74.9

.144

>30.00 (34.97)

.059

0.28

2.6

ALC19CR07

grab

10.05

.310

.086

.029

0.04

0.5

ALC19CR08

grab

1870

.495

24.5

>20.0 (31.90)

1.85

189.5

ALC19CR09

grab

88.1

.077

>30.00 (39.98)

1.88

0.08

32

ALC19CR10

grab

1545

.178

26.7

>20.0 (28.67)

0.68

373

ALC19CR11

grab

2360

.366

16.80

>20.0 (43.67)

0.11

900

ALC19CR12

grab

3700

.624

1.645

>20.0 (71.14)

3.14

273

ALC19CR13

grab

964

.716

17.30

17.5

0.11

386

ALC19CR14

grab

3530

.350

1.945

>20.0 (59.54)

1.57

1600

ALC19CR15

grab

3670

.026

1.895

>20.0 (77.01)

0.33

205

ALC19CR16

grab

1790

.107

5.28

>20.0 (52.77)

0.37

146.5

ALC19CR17

grab

751

.069

6.45

18.05

0.45

107

ALC19CR18

grab

1065

.718

.178

.514

0.10

7.6

ALC19CR19

grab

2510

.299

5.58

>20.0 (70.63)

0.06

167

ALC19CR20

grab

4410

2.27

26.40

>20.0 (21.56)

5.68

4500

ALC19CR21

grab

47.5

.177

.048

.092

1.78

8.8

ALC19CR22

grab

87.7

.095

.011

.047

4.79

2.9

As

part of the fall 2019 program, a total of 1,846.35 meters of diamond

drilling was completed with 21 holes being drilled. The drilling was

divided over two target areas with 10 holes allocated to testing one of

the phyllite/limestone contacts in the ALLCO area and 11 preliminary

confirmation holes designed to begin testing the historic 1971 resource

(pre NI43-101 and therefore not compliant) reported for the

Regal/Snowflake mines.

The core samples have been submitted to

MSA Laboratories in Langley, BC and assay results are pending and will

be reported once received.

Property History & Background

The

Regal Project hosts several past producing small-scale historic mines

including the Regal Silver. The property also hosts numerous promising

mineral occurrences. From the historic records it appears that most, and

perhaps all, of the known mineralized showings/zones have not been

previously drilled using modern diamond drilling methods.

Snowflake and Regal Silver (Stannex/Woolsey) Mines

The

Snowflake and Regal Silver mines were two former producing mines that

operated intermittently during the period 1936-1953. The last

significant work on the property took place from 1967-1970, when Stannex

Minerals completed 2,450 meters of underground development work and a

feasibility study but did not restart mining operations. In 1982,

reported reserves were 590,703 tonnes grading 71.6 grams per tonne

silver, 2.66 per cent lead, 1.26 per cent zinc, 1.1 per cent copper,

0.13 per cent tin and 0.015 per cent tungsten (Minfile No. 082N 004 –

Prospectus, Gunsteel Resources Inc., April 29, 1986). It should be noted

that the above resource and grades, although believed to be reliable,

were prepared prior to the adoption of NI43-101 and are not compliant

with current standards set out therein for calculating mineral resources

or reserves.

ALLCO Silver Mine

The ALLCO Silver Mine

is situated 6.35 Kilometers northwest of the above described

Snowflake/Regal Mine(s). The ALLCO Silver Mine operated from 1936-1937

and produced 213 tonnes of concentrates containing 11 troy ounces of

gold (1.55 g/t), 11,211 troy ounces of silver (1,637 g/t) and 173,159

lbs of lead (36.9%).

Airborne Geophysics to Guide Future Exploration

An

extensive airborne geophysics survey conducted by Geotech Ltd of

Aurora, Ontario, for Northaven Resources Corp. in 2011, identified four

well defined high potential linear targets correlating with the same

structural orientation as the Allco, Snowflake and Regal Silver mines.

Northaven also reported that the mineralogy and structural orientation

of the Allco, Snowflake and Regal Silver appeared to be similar to that

of Huakan’s J&L gold project located to the north, and on a similar

geophysical trend line. The J&L is reportedly now one of western

Canada’s largest undeveloped gold deposits.

After completing the

airborne survey, Northaven failed in financing their company and

conducting further exploration on the property and subsequently

forfeited the claims without any of the follow up work ever being

completed. Affinity Metals is in the fortunate position of benefitting

from this significant and promising geophysics data and associated

targets.

The aforementioned Northaven airborne geophysical survey

conducted at a cost of $319,458.95 in August of 2011 is described in The

BC Ministry of Energy, Mines and Petroleum Resources Assessment Report

#33054. The results of the survey are competently explained and

illustrated by professionals on You Tube at: https://www.youtube.com/watch?v=GX431eBY_t0

Condor

Consulting, Inc. who compiled the survey data and produced the original

geophysics report was recently retained by Affinity in order to provide

more detailed interpretations and potential drill target locations with

the aim of testing two of the four target areas in the future.

Earth Sciences Services Corp. (ESSCO) has also provided acoustical geophysics data for portions of the Regal property.

The

Corporation is in the process of correlating and interpreting all of

the historic and new geophysical data with the objective of further

advancing exploration plans and associated drill targets.

Affinity

Metals has been granted a 5 Year Multi-Year-Area-Based (MYAB)

exploration permit which includes approval for 51 drill sites.

Qualified Person

The

qualified person for the Regal Project for the purposes of National

Instrument 43-101 is Frank O’Grady, P.Eng. He has read and approved the

scientific and technical information that forms the basis for the

disclosure contained in this news release.

About Affinity Metals

Affinity Metals is focused on the acquisition, exploration and development of strategic metal deposits within North America.

The Corporation’s flagship project and present focus is the Regal.

On behalf of the Board of Directors

Robert Edwards, CEO and Director of Affinity Metals Corp.

Posted by AGORACOM

at 3:57 PM on Tuesday, January 14th, 2020

Sponsor: Affinity Metals (TSX-V: AFF) a Canadian mineral exploration

company building a strong portfolio of mineral projects in North

America. The Corporation’s flagship property is the Drill ready Regal

Property near Revelstoke, BC. Recent sampling encountered bonanza grade

silver, zinc, and lead with many samples reaching assay over-limits.

Further assaying of over-limits has been initiated, results will be

reported once received. Click Here for More Info

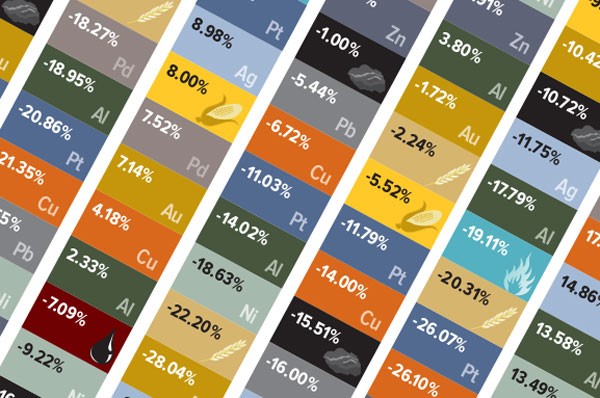

Near

the start of every year, I share our ever-popular Periodic Table of

Commodity Returns, now updated to reflect the final results of 2019. To

view the interactive table and download a copy of your own, click here.

Having

broken above $2,000 an ounce last week, palladium in now forecast by

Citi analysts to hit $2,500 by the middle of this year.

Commodities

as a whole had a mostly positive 2019, returning 16.53 percent as

measured by the S&P GSCI. This far surpasses commodities’ five-year

average return of about negative 11.52 percent, between 2014 and 2018.

Precious

metals were responsible for much of the growth. For the third straight

year, and for the fourth time in six years, palladium was the

top-performing commodity. The metal, used widely in the production of

catalytic converters, increased an incredible 54.21 percent to end 2019

at $1,912 an ounce, a slightly higher price than gold’s all-time high

set in September 2011.

As

was the case in past years, palladium benefited from mounting global

demand to curb emissions from gasoline-burning engines. It’s also among

the world’s scarcest precious metals, mined primarily in Russia and

South Africa, which means supply will potentially remain in deficit for

years to come.

Having

broken above $2,000 an ounce last week, palladium in now forecast by

Citi analysts to hit $2,500 by the middle of this year.

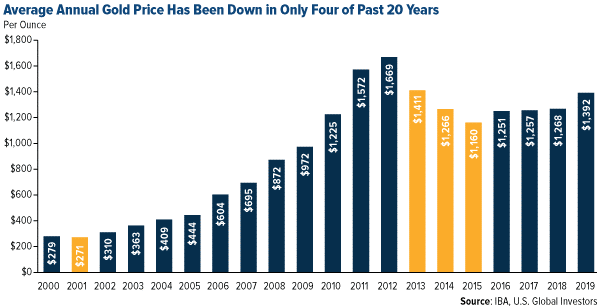

Gold Price Up in Four out of Every Five Years

Gold,

meanwhile, had its best year since 2010, climbing as much as 18.31

percent. The yellow metal’s role as an exceptional store of value shined

brightly in the second half of the year when the pool of negative-yielding debt

around the world began to skyrocket, eventually topping out at around

$17 trillion in August. On the news last week that Iran launched a

counterstrike against U.S.-occupied military bases in Iraq, the safe

haven briefly broke above $1,600 an ounce for the first time since April

2013.

In

the past two decades, gold has helped investors limit market volatility

and portfolio losses. Between 2000 and 2019, the precious metal’s

average annual price was down in only four years. Put another way, gold

was up on average in four out of every five years—a remarkable track

record.

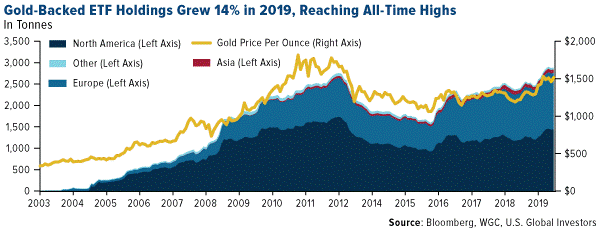

Safe

haven-seeking investors around the world piled into gold-backed ETFs in

2019, making it the best year on record for gold holdings. Assets under

management (AUM) in gold bullion ETFs expanded 37 percent from the

previous year, adding $19.2 billion, or 400 tonnes, according to the World Gold Council (WGC).

During the fourth quarter, total holdings hit a jaw-dropping 2,900

tonnes, the equivalent of 102 million ounces, which is the most on

record.

As

of the end of last week, gold looked slightly overbought on a relative

strength basis, meaning a correction wouldn’t be such a bad thing and in

fact expected.

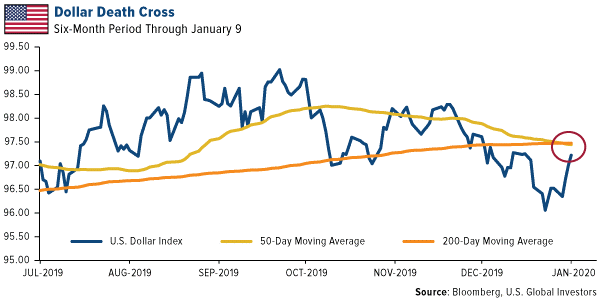

Has the Greenback Peaked?

Short

of escalating tensions in the Middle East or a pullback in stocks, the

catalyst for higher gold prices—and, indeed, commodity prices in

general—may very well be a substantial weakening of the U.S. dollar. On

Tuesday, the U.S. Dollar Index experienced a “death cross,†a bearish

signal that takes places when an asset’s 50-day moving average crosses

below its 200-day moving average. We haven’t seen this from the

greenback since May 2017.

Other

firms and analysts have recently made the case that the dollar is ready

to decline in 2020, which would give gold and other hard assets the

room to gain momentum. Below are just three such forecasts from the past

couple of weeks:

“Our

view is that the dollar is ready to decline in 2020 and will be

encouraged to do so as negative interest rates abroad turn less negative

while the Fed holds pat (or cuts)… In the event of an unlikely

recession in 2020, U.S. fiscal and monetary policy will turn sharply

expansionary, the dollar will decline further, and gold will do well.â€

~Murenbeeld & Co., January 3

“We

expect that U.S. dollar weakness will likely characterize global

financial markets throughout 2020… A weaker dollar is always good news

for commodity prices. We are particularly bullish gold at this point.

Gold is a direct play on a weaker dollar and could also benefit from any

major flare-up in geopolitical tensions.â€

~Alpine Macro, January 6

“Starting

2020, the key setup from a macro perspective is the confirmed top in

the U.S. Dollar Index as well as the U.S. Trade-Weighted Broad Dollar

Index… The U.S. Dollar Index (DXY) has broken below the 97 support to

trigger the bearish implication of the June-December topping pattern

(head-and-shoulders top) and the U.S. Trade-Weighted Broad Dollar Index

has broken below the early-November 2019 low as well as the 200-day

moving average to confirm a similar topping pattern to the DXY.â€

~CLSA, January 7

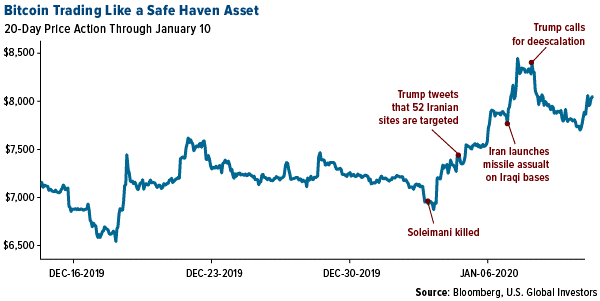

Bitcoin as a Safe Haven Asset

Gold

isn’t the only asset that responded positively to geopolitical

uncertainty involving Iran. The price of bitcoin, the world’s largest

cryptocurrency by market cap, surged on the news that President Donald

Trump had ordered a strike on Iranian general Qasem Soleimani, before

commenting that the U.S. was targeting as many as 52 sites in Iran.

From

January 2, the day before the strike, to January 8, when Trump

announced that Iran appeared to be “standing down,†bitcoin traded up as

much as 21 percent to its highest level in six weeks. In addition,

there were reports that local bitcoin sellers in Iran were charging three times the market rate in response to the threat of war with the U.S.

Google searches for “bitcoin†were also up. Cointelegraph reports that the search term “bitcoin Iran†exploded more than 4,450 percent in the seven days through January 8.

All

of this tells me that bitcoin continues to mature as an asset, and that

investors and savers increasingly trust it as a store of value in times

of uncertainty.

Looking for the inside scoop on mining companies? Click here

to read U.S. Global Investors portfolio manager Ralph Aldis’ interview

with MoneyShow and get his favorite mining picks for 2020!

Posted by AGORACOM

at 7:40 PM on Monday, January 13th, 2020

SPONSOR: American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged of 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits.

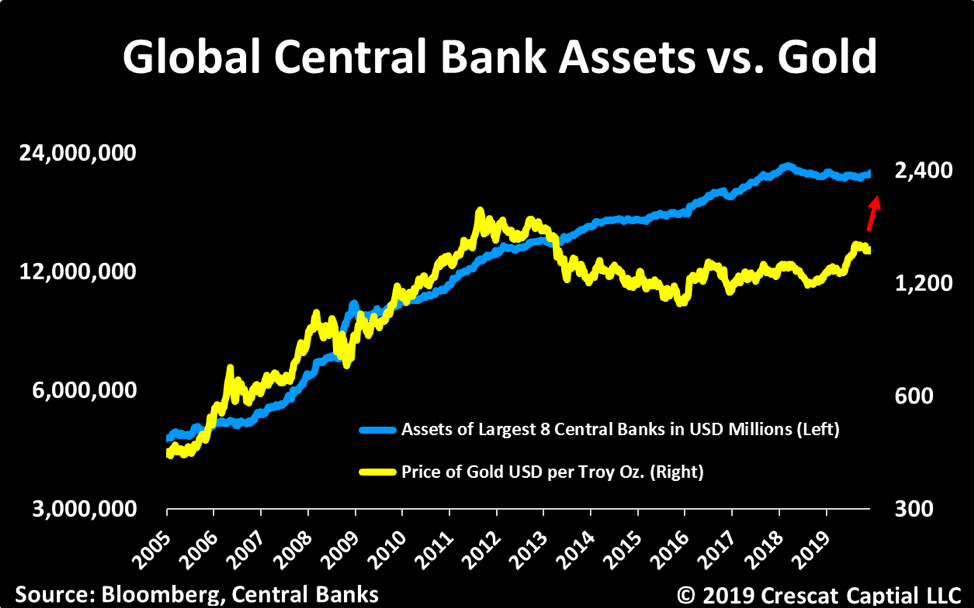

Excerpts from Crescat Capitals November Newsletter:

Precious Metals

Precious metals are poised to benefit from what we consider to be the

best macro set up we’ve seen in our careers. The stars are all

aligning. We believe strongly that this time monetary policy will come

at a cost. Look in the chart below at how the new wave of global money

printing just initiated by the Fed in response to the Treasury market

funding crisis is highly likely to pull depressed gold prices up with

it.

The imbalance between historically depressed commodity prices

relative to record overvalued US stocks remains at the core of our macro

views. On the long side, we believe strongly commodities offer

tremendous upside potential on many fronts. Precious metals remain our

favorite. We view gold as the ultimate haven asset to likely outperform

in an environment of either a downturn in the business cycle, rising

global currency wars, implosion of fiat currencies backed by record

indebted government, or even a full-blown inflationary set up. These

scenarios are all possible. Our base case is that governments and

central banks will keep their pedals to the metal to attempt to fend off

credit implosion or to mop up after one has already occurred until

inflation becomes a persistent problem.

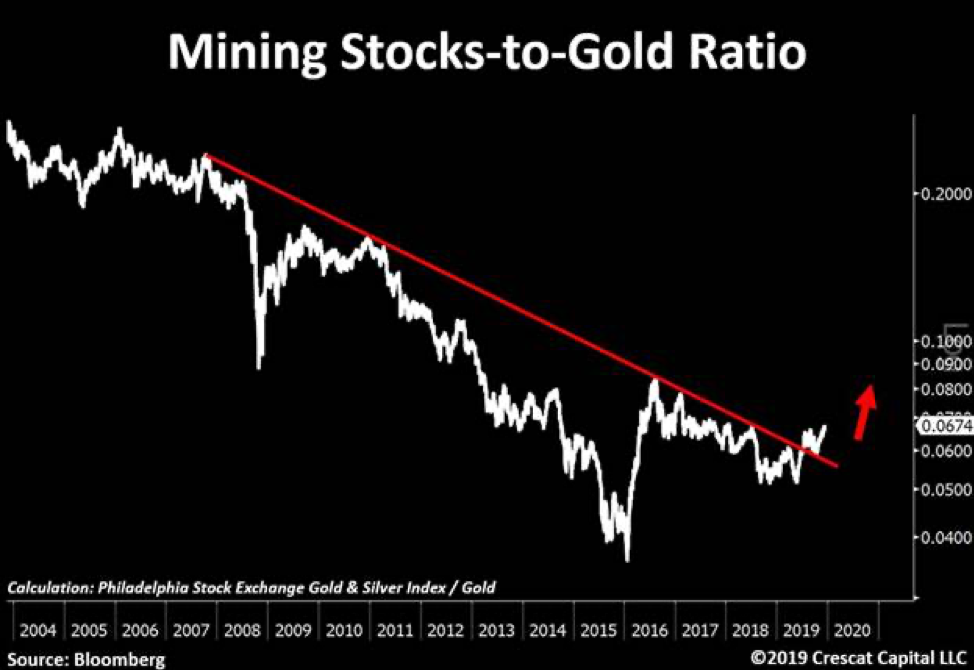

The gold and silver mining industry is precisely where we see one of

the greatest ways to express this investment thesis. These stocks have

been in a severe bear market from 2011 to 2015 and have been formed a

strong base over the last four years. They are offer and incredibly

attractive deep-value opportunity and appear to be just starting to

break out this year. We have done a deep dive in this sector and met

with over 40 different management teams this year. Combining that work

with our proprietary equity models, we are finding some of the greatest

free-cash-flow growth and value opportunities in the market today

unrivaled by any other industry. We have also found undervalued

high-quality exploration assets that will make excellent buyout

candidates.

We recently point out this 12-year breakout in mining stocks relative

to gold now looks as solid as a rock. In our view, this is just the

beginning of a major bull market for this entire industry. We encourage

investors to consider our new Crescat Precious Metals SMA strategy which

is performing extremely well this year.

Zero Discounting for Inflation Risk Today

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, if the global financial markets

cannot absorb the increase in Treasury debt, the Fed will be forced to

monetize it even more. The problem is that the Fed’s panic money

printing at this point in the economic cycle may hasten the unwinding of

the imbalances it is so desperate to maintain because it has perversely

fed the last-gasp melt up of speculation in already record over-valued

and extended equity and corporate credit markets. It is reminiscent of

when the Fed injected emergency cash into the repo market at the peak of

the tech bubble at the end of 1999 to fend off a potential Y2K computer

glitch that led to that market and business cycle top. After 40

years of declining inflation expectations in the US, there is a major

disconnect today between portfolio positioning, valuation, and economic

reality. Too much of the investment world is long the “risk parityâ€

trade to one degree or another, long stocks paired with leveraged long

bonds, a strategy that has back-tested great over the last 40 years, but

one that would be a disaster in a secular rising inflation environment.

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, rising long-term inflation, and

the hidden tax thereon, is the default, bi-partisan plan for the US

government’s future funding regardless of who is in the White House and

Congress after the 2020 elections. The market could start discounting

this sooner rather than later. The Fed’s excessive money printing

may only reinforce the unraveling of financial asset imbalances today as

it leads to rising inflation expectations and thereby a sell-off in

today’s highly over-valued long duration assets including Treasury bonds

and US equities, particularly insanely overvalued growth stocks. We

believe we are in the vicinity of a major US stock market and business

cycle peak.

Posted by AGORACOM

at 4:33 PM on Monday, January 13th, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts `covered by the Hopedale Project. Click Here for More Info

It has been a week of surprises since the last updates were posted.

First, I had not expected Iran to retaliate following the murder of its

top General by a US drone, but it did, despite the risks, as it was

politically necessary to assuage the extreme anger of its population who

demanded revenge. The next surprise was that Israel and the US did not

use this retaliation as an excuse to bomb Iran back to the Stone Age,

which is what they really want to do. As we know, the long-term goal of

Israel and the US is to subjugate Iran, and they will not stop until

they attain this goal, and so it goes on. It appears that there was a

bit of theater involved in Iran’s retaliation, as it clandestinely

signaled its intentions which allowed US forces to get out of harm’s

way. Perhaps US forces did not then launch a blitzkrieg out of

consideration for this courtesy.

Regardless of the muddled and unpredictable fundamental situation,

which included the accidental downing of a passenger plane by Iranian

defensive missile batteries, the charts allowed us to make a reasonably

accurate prediction regarding what was likely to happen to the gold

price. The call for a near-term top in the PM sector made on the site on

Monday looked incorrect the following evening when gold suddenly surged

about $35 on news of the retaliatory Iranian missile strike, but when

it later became apparent that there were, strangely, no US troop

casualties and no further action against Iran, gold and silver reversed

dramatically and dropped quite hard as the tension then looked set to

ease, at least over the short-term. Technically what happened is that

gold pushed quite deep into heavy overhead resistance, becoming very

overbought at a time when COTs were showing extreme readings, and was

thus vulnerable to a sudden reversal. The action around this time

illustrates an important point, which is that when gold rises due to

sudden geopolitical developments, the gains tend not to stick – what

really matters and is the big driver for gold at this time is the insane

monetary expansion that is going on, which is being undertaken in a

desperate attempt to postpone the systemic implosion that is baked in

for as long as possible. As we have already observed in these updates in

recent weeks, gold is already in a raging bullmarket against a wide

variety of currencies, and it won’t be all that long before it’s in a

raging bullmarket against the dollar too, as the Fed sets the stage for

hyperinflation.

There are two big and compelling reasons for the US government to

tank the dollar. One is that it makes US exporters more competitive, and

the other is that it can use the mechanism of inflation to wipe clean

its colossal debts, by paying them off in devalued coin, printing vast

amounts of money to pay them off, in the process legally swindling the

foolish creditors out of their dues. This is precisely what the Weimar

Republic in Germany did in 1923 to eliminate the unfair reparations

imposed by the Treaty of Versailles, which were unfair also because

Germany didn’t start the 1st World War – it was tricked into it by the

allies, because the British Empire was scared of Germany’s rising

industrial and military might and wanted to destroy it, 100 plus years

of propaganda lies about Germany being responsible for the 1st World War

notwithstanding.

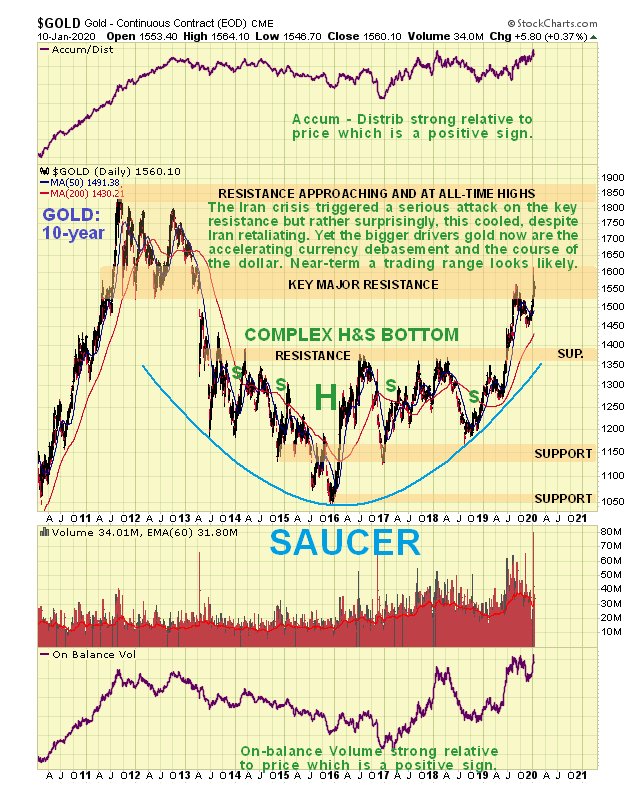

We’ll look at the dollar a little later. First we will review gold’s charts, starting with the 10-year chart.

On the 10-year chart we see that gold is now a bullmarket, even

against the dollar, and is currently challenging the heavy resistance

arising from the 2011 – 2013 top area. The second attack on this

resistance in the space of few months got further because of the Iran

crisis, and if this cools any more short-term, it will probably lead to

gold settling into a trading range before it mounts a more successful

attack on this resistance. A point to note here is that while the

resistance up to the 2011 highs in the $1800 area looks like a major

obstacle, it’s not such a big deal as many think, given the rate at

which the dollar is now being debased.

This week it’s worth also taking a quick look at a 3-year chart

for added perspective. This chart shows us that since the bullmarket

started in mid-Summer, we have seen 3 sharp runups punctuated by 2 bull

Flags. While the 2nd of these Flags targets the $1800 area, we have to

factor in that gold now has much more overhanging supply to contend with

than on the 1st runup, and this, coupled with quite extreme COT

readings, inclines to the view that this will need to be worked off.

Hence the interpretation that it will probably need to consolidate for a

while before it makes significant further progress, although it

obviously won’t if the US starts a serious bombing campaign against

Iran. The Fed’s increasingly manic money printing will eventually drive

it higher, of course

On the 6-month chart we can see the interesting price action

around the Iran crisis over the past week or so. A bearish “shooting

star†appeared on the chart last Monday, which we took as a sign that gold was forming a short-term top,

but then overnight on the 7th to the 8th it surged briefly above $1610

when Iran lobbed missiles at US bases in Iraq, which had many

concluding, not unnaturally that this would trigger a major Israel – US

bombing campaign. When it became apparent that there were no casualties

from the Iranian attack and no US counter strike, tensions quickly

cooled and gold lost ground fast the next day, putting in a big

high-volume reversal candle, approximating to another “shooting starâ€.

Normally such action is followed by a retreat at least for a while, and

some stocks, like silver stock Coeur Mining (CDE), that we ditched a

while ago, got clobbered. This is why gold is expected to settle down

into a trading range for a while before mounting another attack on the

resistance.

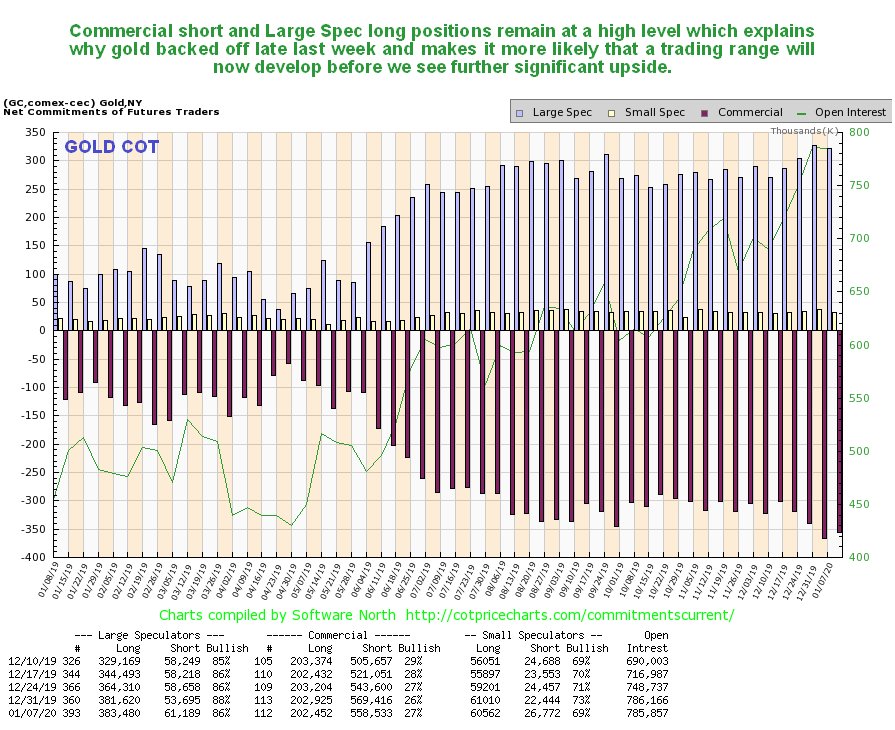

Another factor suggesting that gold will consolidate / react

back for a while is the latest COT, which shows still very high

Commercial short and Large Spec long positions…

Click on chart to popup a larger, clearer version.

What about Precious Metals stocks? The latest 10-year chart for

GDX shows that we still have most everything to look forward to, for

despite the rally from the middle of last year, it still hasn’t broken

out of the giant complex Head-and-Shoulders bottom that has been formed

since way back early in 2013. A breakout above the nearby resistance

should lead to a rapid ascent to the next resistance level at the

underside of a large top pattern, and thereafter it will have to work

its way through continuing resistance up to its highs. The strength of

the volume indicators in the recent past are a sign that it “means

businessâ€.

Now we turn our attention to the dollar, which is looking

increasingly frail as we can see on the latest 6-year chart for the

dollar index. It is rolling over beneath resistance and appears to be

breaking down from the 16-month gentle uptrend shown. This is of course

the main reason that gold, shown at the top of this chart, has been

breaking higher again. If it fails to hold up here it could be targeting

the lower boundary of the bullhorn pattern, which would involve a heavy

drop from the current level that would “light a fire†under the

Precious Metals, and many other commodities, notably copper.

A chart that really gives the game away and calls time on the

dollar is the 6-year chart for dollar proxy UUP. As we can see, unlike

the dollar index itself, this has risen up to the upper boundary of its

giant bullhorn pattern and appears to be on the point of breaking down.

Its Accumulation line has been very weak. This chart suggests that the

dollar could be in for a very rough ride before long, which is hardly

surprising considering the lengths to which the Federal Reserve is going

to destroy it. While other countries and trading blocs, most notably

the EU, are making a valiant attempt to destroy their own currencies,

they will be hard put to keep up with the Fed.

And now, for the benefit of anyone who still doubts that gold is

in a bullmarket, I have pleasure in presenting the following 6-year

chart for gold against the Japanese Yen…

Still think gold might be in bearmarket? – no – didn’t think you would.

Although you can never be 100% sure of anything with these

smaller issues, I am sure that you will agree with me that this chart is

not suggestive of a sector that is going anywhere but up.

Conclusion: although last week’s reversal candle and the current rather extreme COT structure mean that gold may react back more near-term, the overall picture is strongly bullish, which is hardly surprising as the fiat money system is fast approaching its nemesis, with the line of least resistance leading to hyperinflation. Our general approach therefore is not to sell PM sector investments, except on a case by case basis where they become critically overbought, but instead buy or add to positions on dips.

Posted by AGORACOM

at 3:34 PM on Friday, January 10th, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

Excerpts from Crescat Capitals November Newsletter:

Precious Metals

Precious metals are poised to benefit from what we consider to be the

best macro set up we’ve seen in our careers. The stars are all

aligning. We believe strongly that this time monetary policy will come

at a cost. Look in the chart below at how the new wave of global money

printing just initiated by the Fed in response to the Treasury market

funding crisis is highly likely to pull depressed gold prices up with

it.

The imbalance between historically depressed commodity prices

relative to record overvalued US stocks remains at the core of our macro

views. On the long side, we believe strongly commodities offer

tremendous upside potential on many fronts. Precious metals remain our

favorite. We view gold as the ultimate haven asset to likely outperform

in an environment of either a downturn in the business cycle, rising

global currency wars, implosion of fiat currencies backed by record

indebted government, or even a full-blown inflationary set up. These

scenarios are all possible. Our base case is that governments and

central banks will keep their pedals to the metal to attempt to fend off

credit implosion or to mop up after one has already occurred until

inflation becomes a persistent problem.

The gold and silver mining industry is precisely where we see one of

the greatest ways to express this investment thesis. These stocks have

been in a severe bear market from 2011 to 2015 and have been formed a

strong base over the last four years. They are offer and incredibly

attractive deep-value opportunity and appear to be just starting to

break out this year. We have done a deep dive in this sector and met

with over 40 different management teams this year. Combining that work

with our proprietary equity models, we are finding some of the greatest

free-cash-flow growth and value opportunities in the market today

unrivaled by any other industry. We have also found undervalued

high-quality exploration assets that will make excellent buyout

candidates.

We recently point out this 12-year breakout in mining stocks relative

to gold now looks as solid as a rock. In our view, this is just the

beginning of a major bull market for this entire industry. We encourage

investors to consider our new Crescat Precious Metals SMA strategy which

is performing extremely well this year.

Zero Discounting for Inflation Risk Today

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, if the global financial markets

cannot absorb the increase in Treasury debt, the Fed will be forced to

monetize it even more. The problem is that the Fed’s panic money

printing at this point in the economic cycle may hasten the unwinding of

the imbalances it is so desperate to maintain because it has perversely

fed the last-gasp melt up of speculation in already record over-valued

and extended equity and corporate credit markets. It is reminiscent of

when the Fed injected emergency cash into the repo market at the peak of

the tech bubble at the end of 1999 to fend off a potential Y2K computer

glitch that led to that market and business cycle top. After 40

years of declining inflation expectations in the US, there is a major

disconnect today between portfolio positioning, valuation, and economic

reality. Too much of the investment world is long the “risk parityâ€

trade to one degree or another, long stocks paired with leveraged long

bonds, a strategy that has back-tested great over the last 40 years, but

one that would be a disaster in a secular rising inflation environment.

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, rising long-term inflation, and

the hidden tax thereon, is the default, bi-partisan plan for the US

government’s future funding regardless of who is in the White House and

Congress after the 2020 elections. The market could start discounting

this sooner rather than later. The Fed’s excessive money printing

may only reinforce the unraveling of financial asset imbalances today as

it leads to rising inflation expectations and thereby a sell-off in

today’s highly over-valued long duration assets including Treasury bonds

and US equities, particularly insanely overvalued growth stocks. We

believe we are in the vicinity of a major US stock market and business

cycle peak.

Posted by AGORACOM

at 2:20 PM on Friday, January 10th, 2020

This article is an overview of the economic conditions that will

drive the gold price in 2020 and beyond. The turn of the credit cycle,

the effect on government deficits and how they are to be financed are

addressed.

In the absence of foreign demand for new US Treasuries

and of a rise in the savings rate the US budget deficit can only be

financed by monetary inflation. This is bound to lead to higher bond

yields as the dollar’s falling purchasing power accelerates due to the

sheer quantity of new dollars entering circulation. The relationship

between rising bond yields and the gold price is also discussed.

It

may turn out that the recent extraordinary events on Comex, with the

expansion of open interest failing to suppress the gold price, are an

early recognition in some quarters of the US Government’s debt trap.

The strains leading to a crisis for fiat currencies are emerging into plain sight.

Introduction

In 2019, priced in dollars gold rose 18.3% and silver by 15.1%. Or

rather, and this is the more relevant way of putting it, priced in gold

the dollar fell 15.5% and in silver 13%. This is because the story of

2019, as it will be in 2020, was of the re-emergence of fiat currency

debasement. Particularly in the last quarter, the Fed began aggressively

injecting new money into a surprisingly illiquid banking system through

repurchase agreements, whereby banks’ reserves at the Fed are credited

with cash loaned in return for T-bills and coupon-bearing Treasuries as

collateral. Furthermore, the ECB restarted quantitative easing in

November, and the Bank of Japan stands ready to ease policy further “if

the momentum towards its 2% inflation target comes under threat†(Kuroda

– 26 December).

The Bank of Japan is still buying bonds, but at

a pace which is expected to fall beneath redemptions of its existing

holdings. Therefore, we enter 2020 with money supply being expanded by

two, possibly all three of the major western central banks. Besides

liquidity problems, the central bankers’ nightmare is the threat that

the global economy will slide into recession, though no one will confess

it openly because it would be an admission of policy failure. And

policy makers are also terrified that if bankers get wind of a declining

economy, they will withdraw loan facilities from businesses and make

things much worse.

Of the latter concern central banks have good

cause. A combination of the turn of the credit cycle towards its

regular crisis phase and Trump’s tariff war has already hit

international trade badly, with exporting economies such as Germany

already in recession and important trade indicators, such as the Baltic

dry index collapsing. No doubt, President Trump’s most recent

announcement that a trade deal with China is ready for signing is driven

by an understanding in some quarters of the White House that over trade

policy, Trump is turning out to be the turkey who voted for Christmas.

But we have heard this story several times before: a forthcoming

agreement announced only to be scrapped or suspended at the last moment.

The

subject which will begin to dominate monetary policy in 2020 is who

will fund escalating government deficits. At the moment it is on few

investors’ radar, but it is bound to dawn on markets that a growing

budget deficit in America will be financed almost entirely by monetary

inflation, a funding policy equally adopted in other jurisdictions.

Furthermore, Christine Lagarde, the new ECB president, has stated her

desire for the ECB’s quantitative easing to be extended from government

financing to financing environmental projects as well.

2020 is

shaping up to be the year that all pretence of respect for money’s role

as a store of value is abandoned in favour of using it as a means of

government funding without raising taxes. 2020 will then be the year

when currencies begin to be visibly trashed in the hands of their

long-suffering users.

Gold in the context of distorted markets

At the core of current market distortions is a combination of

interest rate suppression and banking regulation. It is unnecessary to

belabour the point about interest rates, because minimal and even

negative rates have demonstrably failed to stimulate anything other than

asset prices into bubble territory. But there is a woeful lack of

appreciation about the general direction of monetary policy and where it

is headed.

The stated intention is the opposite of reality,

which is not to rescue the economy: while important, from a bureaucrat’s

point of view that is not the greatest priority. It is to ensure that

governments are never short of funds. Inflationary financing guarantees

the government will always be able to spend, and government-licenced

banks exist to ensure the government always has access to credit.

Unbeknown

to the public, the government licences the banks to conduct their

business in a way which for an unlicensed organisation is legally

fraudulent. The banks create credit or through their participation in QE

they facilitate the creation of base money out of thin air which is

added to their reserves. It transfers wealth from unsuspecting members

of the public to the government, crony capitalists, financial

speculators and consumers living beyond their means. The government

conspires with its macroeconomists to supress the evidence of rising

prices by manipulating the inflation statistics. So successful has this

scheme of deception been, that by fuelling GDP, monetary debasement is

presented as economic growth, with very few in financial mainstream

understanding the deceit.

The government monopoly of issuing

money, and through their regulators controlling the expansion of credit,

was bound to lead to progressively greater abuse of monetary trust. And

now, in this last credit cycle, the consumer who is also the producer

has had his income and savings so depleted by continuing monetary

debasement that he can no longer generate the taxes to balance his

government’s books later in the credit cycle.

The problem is not

new. America has not had a budget surplus since 2001. The last credit

cycle in the run up to the Lehman crisis did not deliver a budget

surplus, nor has the current cycle. Instead, following the Lehman crisis

we saw a marked acceleration of monetary inflation, and Figure 2 shows

how dollar fiat money has expanded above its long-term trend since then.

In recent years, the Fed’s attempt to return to monetary normality by

reducing its balance sheet has failed miserably. After a brief pause,

the fiat money quantity has begun to grow at a pace not seen since the

immediate aftermath of the Lehman crisis itself and is back in record

territory. Figure 1 is updated to 1 November, since when FMQ will have

increased even more.

In order to communicate effectively the

background for the relationship between gold and fiat currencies in 2020

it is necessary to put the situation as plainly as possible. We enter

the new decade with the highest levels of monetary ignorance imaginable.

It is a systemic issue of not realising the emperor has no clothes.

Consequently, markets have probably become more distorted than we have

ever seen in the recorded history of money and credit, as widespread

negative interest rates and negative-yielding bonds attest. In our

attempt to divine the future, it leaves us with two problems: assessing

when the tension between wishful thinking in financial markets and

market reality will crash the system, and the degree of chaos that will

ensue.

The timing is impossible to predict with certainty

because we cannot know the future. But, if the characteristics of past

credit cycles are a guide, it will be marked with a financial and

systemic crisis in one or more large banks. Liquidity strains suggest

that event is close, even within months and possibly weeks. If so, banks

will be bailed, of that we can be certain. It will require central

banks to create yet more money, additional to that required to finance

escalating government budget deficits. Monetary chaos promises to be

greater than anything seen heretofore, and it will engulf all western

welfare-dependent economies and those that trade with them.

We

have established that between keeping governments financed, bailing out

banks and perhaps investing in renewable green energy, the issuance of

new money in 2020 will in all probability be unprecedented, greater than

anything seen so far. It will lead to a feature of the crisis, which

may have already started, and that is an increase in borrowing costs

forced by markets onto central banks and their governments. The yield on

10-year US Treasuries is already on the rise, as shown in Figure 3.

Assuming no significant increase in the rate of savings and

despite all attempts to suppress the evidence, the acceleration in the

rate of monetary inflation will eventually lead to runaway increases in

the general level of prices measured in dollars. As Milton Friedman put

it, inflation [of prices] is always and everywhere a monetary

phenomenon.

Through QE, central banks believe they can contain

the cost of government funding by setting rates. What they do not seem

to realise is that while to a borrower interest is a cost to set against

income, to a lender it reflects time-preference, which is the

difference between current possession, in this case of cash dollars, and

possession at a future date. Unless and until the Fed realises and

addresses the time preference problem, the dollar will lose purchasing

power. Not only will it be sold in the foreign exchanges, but depositors

will move to minimise their balances and creditors their ownership of

debt.

If, as it appears in Figure 3, dollar bond yields are

beginning a rising trend, the inexorable pull of time preference is

already beginning to apply and further rises in bond yields will imperil

government financing. The Congressional Budget Office assumes the

average interest rate on debt held by the public will be 2.5% for the

next three years, and that net interest in fiscal 2020 will be $390bn,

being about 38% of the projected deficit of $1,008bn. Combining the

additional consequences for government finances of a recession with

higher bond yields than the CBO expects will be disastrous.

Clearly,

in these circumstances the Fed will do everything in its power to stop

markets setting the cost of government borrowing. But we have been here

before. The similarities between the situation for the dollar today and

the deterioration of British government finances in the early to

mid-1970s are remarkable. They resulted in multiple funding crises and

an eventual bail-out from the IMF. Except today there can be no IMF

bail-out for the US and the dollar, because the bailor gets its currency

from the bailee.

Nearly fifty years ago, in the UK gold rose

from under £15 per ounce in 1970 to £80 in December 1974. The peak of

the credit cycle was at the end of 1971, when the 10-year gilt yield to

maturity was 7%. By December 1974, the stock market had crashed, a

banking crisis had followed, price inflation was well into double

figures and the 10-year gilt yield to maturity had risen to over 16%.

History

rhymes, as they say. But for historians the parallels between the

outlook for the dollar and US Treasury funding costs at the beginning of

2020, and what transpired for the British economy following the Barbour

boom of 1970-71 are too close to ignore. It is the same background for

the relationship between gold and fiat currencies for 2020 and the few

years that follow.

Gold and rising interest rates

Received investment wisdom is that rising interest rates are bad for

the gold price, because gold has no yield. Yet experience repeatedly

contradicts it. Anyone who remembers investing in UK gilts at a 7% yield

in December 1971 only to see prices collapse to a yield of over 16%,

while gold rose from under £15 to £80 to the ounce over the three years

following should attest otherwise.

Part of the error is to

believe that gold has no yield. This is only true of gold held as cash

and for non-monetary usage. As money, it is loaned and borrowed, just

like any other form of money. Monetary gold has its own time preference,

as do government currencies. In the absence of state intervention, time

preferences for gold and government currencies are set by their

respective users, bearing in mind the characteristics special to each.

It is not a subject for simple arbitrage, selling gold and buying

government money to gain the interest differential, because the spread

reflects important differences which cannot be ignored. It is like

shorting Swiss francs and buying dollars in the belief there is no

currency risk.

The principal variable between the time

preferences of gold and a government currency is the difference between

an established form of money derived from the collective preferences of

its users, for which there is no issuer risk, and state-issued currency

which becomes an instrument of funding by means of its debasement.

The

time preference of gold will obviously vary depending on lending risk,

which is in addition to an originary rate, but it is considerably more

stable than the time preference of a fiat currency. Gold’s interest rate

stability is illustrated in Figure 4, which covers the period of the

gold standard from the Bank Charter Act of 1844 to before the First

World War, during which time the gold standard was properly implemented.

With the exception of uncontrolled bank credit, sterling operated as a

gold substitute.

Admittedly, due to problems created by the cycle of bank credit,

these year-end values conceal some significant fluctuations, such as at

the time of the Overend Gurney collapse in 1866 when borrowing rates

spiked to 10%. The depression following the Barings crisis of 1890

stalled credit demand which is evident from the chart. However,

wholesale borrowing rates, which were effectively the cost of borrowing

in gold, were otherwise remarkably stable, varying between 2-3½%. Some

of this variation can be ascribed to changing perceptions of general

borrower risk and some to changes in industrial investment demand,

related to the cycle of bank credit.

Compare this with dollar

interest rates since 1971, when the dollar had suspended the remaining

fig-leaf of gold backing, which is shown in Figure 5 for the decade

following.

In February 1972 the Fed Funds rate was 3.29%, rising eventually

to over 19% in January 1981. At the same time gold rose from $46 to a

high of $843 at the morning fix on 21 January 1980. Taking gold’s

originary interest rate as approximately 2% it required a 17% interest

rate penalty to dissuade people from hoarding gold and to hold onto

dollars instead.

In 1971, US Government debt stood at 35% of GDP

and in 1981 it stood at 31%. The US Government ran a budget surplus over

the decade sufficient to absorb the rising interest cost on its T-bill

obligations and any new Treasury funding. America enters 2020 with a

debt to GDP ratio of over 100%. Higher interest rates are therefore not a

policy option and the US Government, and the dollar, are ensnared in a

debt trap from which the dollar is unlikely to recover.

The seeds

of the dollar’s destruction were sown over fifty years ago, when the

London gold pool was formed, whereby central banks committed to help the

US maintain the price at $35, being forced to do so because the US

could no longer supress the gold price on its own. And with good reason:

Figure 6 shows how the last fifty years have eroded the purchasing

power of the four major currencies since the gold pool failed.

Over the last fifty years, the yen has lost over 92%, the

dollar 97.6%, the euro (and its earlier components 98.2% and sterling

the most at 98.7%. And now we are about to embark on the greatest

increase of global monetary inflation ever seen.

The market for physical gold

In recent years, demand for physical gold has been strong. Chinese

and Indian private sector buyers have to date respectively accumulated

an estimated 17,000 tonnes (based on deliveries from Shanghai Gold

Exchange vaults) and about 24,000 tonnes (according to WGC Director

Somasundaram PR quoted in India’s Financial Express last May).

It

is generally thought that higher prices for gold will deter future

demand from these sources, with the vast bulk of it being categorised as

simply jewellery. But this is a western view based on a belief in

objective values for government currencies and subjective prices for

gold. It ignores the fact that for Asians, it is gold that has the

objective value. In Asia gold jewellery is acquired as a store of value

to avoid the depreciation of government currency, hoarded as a central

component of a family’s long-term wealth accumulation.

Therefore,

there is no certainty higher prices will compromise Asian demand.

Indeed, demand has not been undermined in India with the price rising

from R300 to the ounce to over R100,000 today since the London gold pool

failed, and that’s despite all the government disincentives and even

bans from buying gold.

Additionally, since 2008 central banks

have accumulated over 4,400 tonnes to increase their official reserves

to 34,500 tonnes. The central banks most active in the gold market are

Asian, and increasingly the East and Central Europeans.

There

are two threads to this development. First there is a geopolitical

element, with Russia replacing reserve dollars for gold, and China

having deliberately moved to control global physical delivery markets.

And second, there is evidence of concern amongst the Europeans that the

dollar’s role as the reserve currency is either being compromised or no

longer fit for a changed world. Furthermore, the rising power of Asia’s

two hegemons continues to drive over two-thirds of the world’s

population away from the dollar towards gold.

Goldmoney estimates

there are roughly 180,000 tonnes of gold above ground, much of which

cannot be categorised as monetary: monetary not as defined for the

purposes of customs reporting, but in the wider sense to include all

bars, coins and pure gold jewellery accumulated for its long-term wealth

benefits through good and bad times. Annual mine production adds

3,000-3,500 tonnes, giving a stock to flow ratio of over 50 times. Put

another way, the annual increase in the gold quantity is similar to the

growth in the world’s population, imparting great stability as a medium

of exchange.

These qualities stand in contrast to the

increasingly certain acceleration of fiat currency debasement over the

next few years. Anyone prepared to stand back from the financial

coalface can easily see where the relationship between gold and fiat

currencies is going. Most of the world’s population is moving away from

the established fiat regime towards gold as a store of value, their own

fiat currencies lacking sufficient credibility to act as a dollar

alternative. And financial markets immersed in the fiat regime have very

little physical gold in possession. Instead, where it is now perceived

that there is a risk of missing out on a rise in the gold price,

investors have begun accumulating in greater quantities the paper

alternatives to physical gold: ETFs, futures, options, forward contracts

and mining shares.

Paper markets

From the US Government’s point of view, gold as a rival to the dollar

must be quashed, and the primary purpose of futures options and

forwards is to expand artificial supply to keep the price from rising.

In a wider context, the ability to print synthetic commodities out of

thin air is a means of suppressing prices generally and we must not be

distracted by claims that derivatives improve liquidity: they only

improve liquidity at lower prices.

When the dollar price of gold

found a major turning point on 17 December 2015, open interest on Comex

stood at 393,000 contacts. The year-end figure today is nearly double

that at 786,422 contracts, representing an increase of paper supply

equivalent to 1,224 tonnes. But that is not all. Not only are there

other regulated derivative exchanges with gold contracts, but also there

are unregulated over the counter markets. According to the Bank for

International Settlements from end-2015 unregulated OTC contracts

(principally London forward contracts) expanded by the equivalent of

2,450 tonnes by last June, taken at contemporary prices. And we must not

forget the unknown quantity of bank liabilities to customers’

unallocated accounts which probably involve an additional few thousand

tonnes.

In recent months, the paper suppression regime has

stepped up a gear, evidenced by Comex’s open interest rising. This is

illustrated in Figure 7.

There are two notable features in the chart. First, the rising

gold price has seen increasing paper supply, which we would expect from a

market designed to keep a lid on prices. Secondly instead of declining

with the gold price, open interest continued to rise following the price

peak in early September while the gold price declined by about $100.

This tells us that the price suppression scheme has run into trouble,

with large buyers taking the opportunity to increase their positions at

lower prices.

In the past, bullion banks have been able to put a

lid on prices by creating Comex contracts out of thin air. The recent

expansion of open interest has failed to achieve this objective, and it

is worth noting that the quantity of gold in Comex vaults eligible for

delivery and pledged is only 2% of the 2,446-tonne short position. In

London, there are only 3,052 tonnes in LBMA vaults (excluding the Bank

of England), which includes an unknown quantity of ETF and custodial

gold. Physical liquidity for the forward market in London is therefore

likely to be very small relative to forward deliveries. And of course,

the bullion banks in London and elsewhare do not have the metal to cover

their obligations to unallocated account holders, which is an

additional consideration.

Clearly, there is not the gold

available in the system to legitimise derivative paper. It now appears

that paper gold markets could be drifting into systemic difficulties

with bullion banks squeezed by a rising gold price, short positions and

unallocated accounts.

There are mechanisms to counter these

systemic risks, such as the ability to declare force majeure on Comex,

and standard unallocated account contracts which permit a bullion bank

to deliver cash equivalents to bullion obligations. But the triggering

of any such escape from physical gold obligations could exacerbate a

buying panic, driving prices even higher. It leads to the conclusion

that any rescue of the bullion market system is destined to fail.

A two-step future for the gold price

It has been evident for some time that the world of fiat currencies

has been drifting into ever greater difficulties of far greater

magnitude than can be contained by spinning a few thousand tonnes of

gold back and forth on Comex and in London. That appears to be the

lesson to be drawn from the inability of a massive increase in open

interest on Comex to contain a rising gold price.

It will take a

substantial upward shift in the gold price to appraise western financial

markets of this reality. In combination with systemic strains

increasing, a gold price of over $2,000 may do the trick. Professional

investors will have found themselves wrongfooted; underinvested in ETFs,

gold mines and regulated derivatives, in which case their gold demand

is likely to drive one or more bullion houses into considerable

difficulties. We might call this the first step in a two-step monetary

future.

The extent to which gold prices rise could be

substantial, but assuming the immediate crisis itself passes, banks

having been bailed in or out, and QE accelerated in an attempt to put a

lid on government bond yields, then the gold price might be deemed to

have risen too far, and due for a correction. But then there will be the

prospect of an accelerating loss of purchasing power for fiat

currencies as a result of the monetary inflation, and that will drive

the second step as investors realise that what they are seeing is not a

rising gold price but a fiat currency collapse.

The high levels

of government debt today in the three major jurisdictions appear to

almost guarantee this outcome. The amounts involved are so large that

today’s paper gold suppression scheme is likely to be too small in

comparison and cannot stop it happening. The effect on currency

purchasing powers will then be beyond question. Monetary authorities

will be clueless in their response, because they have all bought into a

form of economics that puts what will happen beyond their understanding.

As noted above, the path to a final crisis for fiat currencies

might have already started, with the failure by the establishment to

suppress the gold price through the creation of an extra 100,000 Comex

contracts. If not, then any success by the monetary authorities to

reassert control is likely to be temporary.

Perhaps we are

already beginning to see the fiat currency system beginning to unravel,

in which case those that insist gold is not money will find themselves

impoverished.

Posted by AGORACOM

at 5:48 PM on Thursday, January 9th, 2020

American Creek owns a 20% Carried Interest to Production at the Treaty Creek Project in the Golden Triangle. 2019’s first hole averaged 0.683 g/t Au over 780m in a vertical intercept. The Treaty Creek property is located in the same hydrothermal system as the Pretivm and Seabridge’s KSM deposits.

Low-cost gold-backed ETFs in the US have seen positive flows for 18 of the past 19 months

Global gold-backed exchange-traded funds (ETFs) and similar products

had $19.2 billion or 400 tonnes of net inflows in 2019 after holdings

rebounded in December, the World Gold Council (WGC) reports. In the fourth quarter, ETF holdings reached an all-time high of 2,900 tonnes.

Overall, gold-backed assets under management (AUM) grew by 37% in

dollar terms during the year owing to positive demand and an 18.4%

increase in the gold price.

From a regional perspective, North American funds led the way with

inflows of 206 tonnes ($10.1 billion, 14.4% AUM). SPDR Gold Shares – the

world’s biggest gold ETF—and iShares Gold Trust accounted for nearly

half of last year’s inflows.

Low-cost gold-backed ETFs in the US have seen positive flows for 18

of the past 19 months and increased their collective holdings by 60%,

according to the latest WGC data.

Elsewhere, holdings in European funds increased by 188 tonnes ($8.8

billion, 13.6%), while funds listed in Asia were nearly flat, recording

an outflow of 0.1 tonnes ($12 million, 0.3%). The remaining regions had

combined inflows of 6.3 tonnes ($311 million, 16.3%).

Looking ahead, WGC analysts said that they expect investor demand to remain robust through 2020.

“The strength of gold was mainly the byproduct of a dovish shift in monetary policy. Our research indicates that a shift from a hawkish or neutral stance to a dovish one has historically led gold to outperform,†a WGC analyst said.

About American Creek

American Creek is a Canadian mineral exploration company with a strong portfolio of gold and silver properties in British Columbia. Three of those properties are located in the prolific “Golden Triangleâ€; the Treaty Creek and Electrum joint venture projects with Tudor Gold/Walter Storm as well as the 100% owned past producing Dunwell Mine.

The Corporation also holds the Gold Hill, Austruck-Bonanza, Ample Goldmax, Silver Side, and Glitter King properties located in other prospective areas of the province.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com

Posted by AGORACOM

at 9:52 AM on Thursday, January 9th, 2020

Labrador Gold Corp. (TSX-V: LAB) (“LabGold†or the “Companyâ€) is

pleased to provide a review of its exploration activities completed

during 2019. During 2020, LabGold intends to test the continuity of

recently discovered mineralization at its Hopedale Project with a

drilling program.

Roger Moss, President and CEO stated: “Exploration on both of our

Labrador Projects during 2019 continued to successfully define areas of

gold mineralization. These include the discovery of a new gold showing

with assays from 1.67 to 8.26 g/t gold in grab samples at the Hopedale

Project. This is located 500 metres along strike from the known Thurber

Dog gold showing within a broader three kilometre stretch of anomalous

gold in rock and soil. We look forward to continuing our systematic

exploration, including drilling, of this mineralized system in 2020.â€

2019 Hopedale Project Highlights

Discovered a new gold showing north of the Thurber Dog gold

occurrence, grab samples from which assayed between 1.67 and 8.26 g/t

Au.

The Thurber Dog gold occurrence has assays in grab and channel

samples from below detection up to 7.866 g/t Au, with 5 samples greater

than 1 g/t Au and 16 samples assaying greater than 0.1 g/t Au.

The discovery extends the potential strike length of gold

mineralization by approximately 500 metres along strike to the north.The

new showing occurs within a larger 3km trend of anomalous gold in rock

and soil associated with the contact between mafic/ultramafic volcanic

rocks and felsic volcanic rocks.

2019 Ashuanipi Project Highlights

Discovered a gold enriched zone near a high grade (8,973ppb) soil sample taken in 2018.

The zone is defined by anomalous gold

in both soil (below detection up to 1,746ppb Au and including 12 samples

over 100ppb Au) and grab rock samples (below detection up to 2.35 g/t

Au) that cover an area of 450 metres by 450 metres.A second area of gold

mineralization associated with garnet-bearing gossanous gneiss also

shows potential.

Grab rock samples show values from

below detection to 0.68 g/t Au with 10 samples showing values greater

than 0.1 g/t Au over an area of 200m by 120m within a larger anomalous

area of gold in soil samples.

Note that grab samples are selected samples and are not necessarily representative of mineralization on the properties.

Location of the new showing, Thurber Dog, Thurber North

and Thurber South occurrences within the 3km long mineralized Thurber

trend:

New Showing with rusty zones due to the presence of pyrite and arsenopyrite:

What to expect in 2020

Hopedale Project

Exploration at Hopedale during 2020 will focus on determining the

extent of the Thurber Dog mineralized trend. Such work would aim to fill

in the gaps between showings over the three-kilometre strike length

with sampling and VLF-EM surveys. LabGold also intends to carry out an

initial drill program targeting prospective areas along this trend,

including the new showing.

Ashuanipi Project

LabGold’s priority at Ashuanipi is to reach an agreement with the

Matimekush-Lac John First Nation to enable continued exploration of the

property. The 2019 election of the new Chief and Council has been

challenged in Federal Court in Quebec with a court date scheduled for

the end of February. As such, community engagement and negotiations are

on hold until the court case is settled.

Borden Lake Extension Project

During 2019, Newmont Goldcorp announced the start of commercial

production at their Borden Mine. The Borden Lake Extension project is

located less than five kilometres from the Borden Mine along the

southeast trend of the Borden Gold zone. Note that mineralization hosted

on nearby properties is not necessarily indicative of mineralization

that may be hosted on the Company’s property.

Given the start of mining at Borden, follow up of past results at the

Borden Lake Extension project will be undertaken in 2020. Such work

will likely include additional till sampling and geochemical surveys to

better define the previously outlined anomalous zones as well as a

reinterpretation of VLF-EM data using the latest inversion software. Due

to the glacial cover in the area, overburden drilling, guided by

results of this work, would be the best means to define targets for

follow up diamond drilling.

Location of the BLE property and anomalous gold zones along trend to the southeast of Newmont-Goldcorp’s Borden Gold Zone.

All samples were shipped to the Bureau Veritas laboratory in

Vancouver, BC, where they were crushed and split and a 500g sub sample

pulverized to 200 mesh. Samples of 30g were analyzed for gold by fire

assay with an atomic absorption finish and another 15g sample for 36

elements by ultratrace ICP-MS (inductively coupled plasma-mass

spectrometry) following an aqua regia digestion. Over limit samples

(greater than 10g/t Au) are re-assayed using fire assay with a

gravimetric finish. In addition to the QA-QC conducted by the

laboratory, the Company routinely submits blanks, field duplicates and

certified reference standards with batches of samples to monitor the

quality of the analyses.

Roger Moss, PhD., P.Geo., is the qualified person responsible for all technical information in this release.

The Company gratefully acknowledges the Newfoundland and Labrador

Ministry of Natural Resources’ Junior Exploration Assistance (JEA)

Program for its financial support for exploration of the Ashuanipi

property.

About Labrador Gold:

Labrador Gold is a Canadian based mineral exploration company focused

on the acquisition and exploration of prospective gold projects in the

Americas. In 2017 Labrador Gold signed a Letter of Intent under which

the Company has the option to acquire 100% of the Ashuanipi property in

northwest Labrador and the Hopedale property in eastern Labrador.

The Hopedale property covers much of the Florence Lake greenstone

belt that stretches over 60 km. The belt is typical of greenstone belts

around the world but has been underexplored by comparison. Initial work

by Labrador Gold during 2017 show gold anomalies in soils and lake

sediments over a 3 kilometre section of the northern portion of the

Florence Lake greenstone belt in the vicinity of the known Thurber Dog

gold showing where grab samples assayed up to 7.8g/t gold. In addition,

anomalous gold in soil and lake sediment samples occur over

approximately 40 kilometres along the southern section of the greenstone

belt (see news release dated January 25, 2018 for more details).

The Ashuanipi gold project is located just 35 km from the historical

iron ore mining community of Schefferville, which is linked by rail to

the port of Sept Iles, Quebec in the south. The claim blocks cover large

lake sediment gold anomalies that, with the exception of local

prospecting, have not seen a systematic modern day exploration program.

Results of the 2017 reconnaissance exploration program following up the

lake sediment anomalies show gold anomalies in soils and lake sediments

over a 15 kilometre long by 2 to 6 kilometre wide north-south trend and

over a 14 kilometre long by 2 to 4 kilometre wide east-west trend. The

anomalies appear to be broadly associated with magnetic highs and do not

show any correlation with specific rock types on a regional scale (see

news release dated January 18, 2018). This suggests a possible

structural control on the localization of the gold anomalies. Historical

work 30 km north on the Quebec side led to gold intersections of up to

2.23 grams per tonne (g/t) Au over 19.55 metres (not true width)

(Source: IOS Services Geoscientifiques, 2012, Exploration and geological

reconnaissance work in the Goodwood River Area, Sheffor Project, Summer

Field Season 2011). Gold in both areas appears to be associated with

similar rock types.

The Company has 57,039,022 common shares issued and outstanding and trades on the TSX Venture Exchange under the symbol LAB.

For more information please contact: Roger Moss, President and CEO Tel: 416-704-8291 Or visit our website at: www.labradorgold.com Twitter: @LabGoldCorp

Posted by AGORACOM

at 2:39 PM on Wednesday, January 8th, 2020

Sponsor: Affinity Metals (TSX-V: AFF) a Canadian mineral exploration

company building a strong portfolio of mineral projects in North

America. The Corporation’s flagship property is the Drill ready Regal

Property near Revelstoke, BC. Recent sampling encountered bonanza grade

silver, zinc, and lead with many samples reaching assay over-limits.

Further assaying of over-limits has been initiated, results will be

reported once received. Click Here for More Info

Excerpts from Crescat Capitals November Newsletter:

Precious Metals

Precious metals are poised to benefit from what we consider to be the best macro set up we’ve seen in our careers. The stars are all aligning. We believe strongly that this time monetary policy will come at a cost. Look in the chart below at how the new wave of global money printing just initiated by the Fed in response to the Treasury market funding crisis is highly likely to pull depressed gold prices up with it.

The gold and silver mining industry endured a severe bear market from 2011 to 2015 and have formed a strong base over the last four years.

The imbalance between historically depressed commodity prices

relative to record overvalued US stocks remains at the core of our macro

views. On the long side, we believe strongly commodities offer

tremendous upside potential on many fronts. Precious metals remain our

favorite. We view gold as the ultimate haven asset to likely outperform

in an environment of either a downturn in the business cycle, rising

global currency wars, implosion of fiat currencies backed by record

indebted government, or even a full-blown inflationary set up. These

scenarios are all possible. Our base case is that governments and

central banks will keep their pedals to the metal to attempt to fend off

credit implosion or to mop up after one has already occurred until

inflation becomes a persistent problem.

The gold and silver mining industry is precisely where we see one of

the greatest ways to express this investment thesis. These stocks have

been in a severe bear market from 2011 to 2015 and have been formed a

strong base over the last four years. They are offer and incredibly

attractive deep-value opportunity and appear to be just starting to

break out this year. We have done a deep dive in this sector and met

with over 40 different management teams this year. Combining that work

with our proprietary equity models, we are finding some of the greatest

free-cash-flow growth and value opportunities in the market today

unrivaled by any other industry. We have also found undervalued

high-quality exploration assets that will make excellent buyout

candidates.

We recently point out this 12-year breakout in mining stocks relative

to gold now looks as solid as a rock. In our view, this is just the

beginning of a major bull market for this entire industry. We encourage

investors to consider our new Crescat Precious Metals SMA strategy which

is performing extremely well this year.

“This is just the beginning of a major bull market for this entire industry”

Zero Discounting for Inflation Risk Today

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, if the global financial markets

cannot absorb the increase in Treasury debt, the Fed will be forced to

monetize it even more. The problem is that the Fed’s panic money

printing at this point in the economic cycle may hasten the unwinding of

the imbalances it is so desperate to maintain because it has perversely