Posted by AGORACOM

at 9:38 AM on Wednesday, January 15th, 2020

Affinity Metals Corp. (TSXV: AFF) (“Affinity”) (“the

Corporation”) is pleased to release over-limit assays for samples from

the fall 2019 exploration on the Regal property located in the northern

end of the prolific Kootenay Arc approximately 35 km northeast of

Revelstoke, British Columbia, Canada.

As previously reported, the Corporation received assay results for all 22 rock samples collected from surface outcrops in September 2019 from the Black Jacket and ALLCO areas of the property. Of the 22 grab samples collected, the majority contained bonanza grade silver, zinc, and lead with many samples reaching assay over-limits. The over-limit results for zinc and lead are reported in the table below (italicized) beside the original assay values. Assay values for tin, including high grade samples 11, 14 and 20 which were over-limit in the original assay report, are also presented in the last column of the table.

Sample Number

Sample Type

Silver g/t

Copper %

Zinc %

Lead %

Gold g/t

Tin ppm

ALC19CR01

grab

0

.035

0

0

0

0.4

ALC19CR02

grab

1300

.415

18.20

>20.0 (35.69)

0.70

46.1

ALC19CR03

grab

120

.232

.034

.984

0.02

2.4

ALC19CR04

grab

131

.089

.026

.102

2.66

1.1

ALC10CR05

grab

16.7

.295

.060

.013

0.09

0.4

ALC19CR06

grab

74.9

.144

>30.00 (34.97)

.059

0.28

2.6

ALC19CR07

grab

10.05

.310

.086

.029

0.04

0.5

ALC19CR08

grab

1870

.495

24.5

>20.0 (31.90)

1.85

189.5

ALC19CR09

grab

88.1

.077

>30.00 (39.98)

1.88

0.08

32

ALC19CR10

grab

1545

.178

26.7

>20.0 (28.67)

0.68

373

ALC19CR11

grab

2360

.366

16.80

>20.0 (43.67)

0.11

900

ALC19CR12

grab

3700

.624

1.645

>20.0 (71.14)

3.14

273

ALC19CR13

grab

964

.716

17.30

17.5

0.11

386

ALC19CR14

grab

3530

.350

1.945

>20.0 (59.54)

1.57

1600

ALC19CR15

grab

3670

.026

1.895

>20.0 (77.01)

0.33

205

ALC19CR16

grab

1790

.107

5.28

>20.0 (52.77)

0.37

146.5

ALC19CR17

grab

751

.069

6.45

18.05

0.45

107

ALC19CR18

grab

1065

.718

.178

.514

0.10

7.6

ALC19CR19

grab

2510

.299

5.58

>20.0 (70.63)

0.06

167

ALC19CR20

grab

4410

2.27

26.40

>20.0 (21.56)

5.68

4500

ALC19CR21

grab

47.5

.177

.048

.092

1.78

8.8

ALC19CR22

grab

87.7

.095

.011

.047

4.79

2.9

As

part of the fall 2019 program, a total of 1,846.35 meters of diamond

drilling was completed with 21 holes being drilled. The drilling was

divided over two target areas with 10 holes allocated to testing one of

the phyllite/limestone contacts in the ALLCO area and 11 preliminary

confirmation holes designed to begin testing the historic 1971 resource

(pre NI43-101 and therefore not compliant) reported for the

Regal/Snowflake mines.

The core samples have been submitted to

MSA Laboratories in Langley, BC and assay results are pending and will

be reported once received.

Property History & Background

The

Regal Project hosts several past producing small-scale historic mines

including the Regal Silver. The property also hosts numerous promising

mineral occurrences. From the historic records it appears that most, and

perhaps all, of the known mineralized showings/zones have not been

previously drilled using modern diamond drilling methods.

Snowflake and Regal Silver (Stannex/Woolsey) Mines

The

Snowflake and Regal Silver mines were two former producing mines that

operated intermittently during the period 1936-1953. The last

significant work on the property took place from 1967-1970, when Stannex

Minerals completed 2,450 meters of underground development work and a

feasibility study but did not restart mining operations. In 1982,

reported reserves were 590,703 tonnes grading 71.6 grams per tonne

silver, 2.66 per cent lead, 1.26 per cent zinc, 1.1 per cent copper,

0.13 per cent tin and 0.015 per cent tungsten (Minfile No. 082N 004 –

Prospectus, Gunsteel Resources Inc., April 29, 1986). It should be noted

that the above resource and grades, although believed to be reliable,

were prepared prior to the adoption of NI43-101 and are not compliant

with current standards set out therein for calculating mineral resources

or reserves.

ALLCO Silver Mine

The ALLCO Silver Mine

is situated 6.35 Kilometers northwest of the above described

Snowflake/Regal Mine(s). The ALLCO Silver Mine operated from 1936-1937

and produced 213 tonnes of concentrates containing 11 troy ounces of

gold (1.55 g/t), 11,211 troy ounces of silver (1,637 g/t) and 173,159

lbs of lead (36.9%).

Airborne Geophysics to Guide Future Exploration

An

extensive airborne geophysics survey conducted by Geotech Ltd of

Aurora, Ontario, for Northaven Resources Corp. in 2011, identified four

well defined high potential linear targets correlating with the same

structural orientation as the Allco, Snowflake and Regal Silver mines.

Northaven also reported that the mineralogy and structural orientation

of the Allco, Snowflake and Regal Silver appeared to be similar to that

of Huakan’s J&L gold project located to the north, and on a similar

geophysical trend line. The J&L is reportedly now one of western

Canada’s largest undeveloped gold deposits.

After completing the

airborne survey, Northaven failed in financing their company and

conducting further exploration on the property and subsequently

forfeited the claims without any of the follow up work ever being

completed. Affinity Metals is in the fortunate position of benefitting

from this significant and promising geophysics data and associated

targets.

The aforementioned Northaven airborne geophysical survey

conducted at a cost of $319,458.95 in August of 2011 is described in The

BC Ministry of Energy, Mines and Petroleum Resources Assessment Report

#33054. The results of the survey are competently explained and

illustrated by professionals on You Tube at: https://www.youtube.com/watch?v=GX431eBY_t0

Condor

Consulting, Inc. who compiled the survey data and produced the original

geophysics report was recently retained by Affinity in order to provide

more detailed interpretations and potential drill target locations with

the aim of testing two of the four target areas in the future.

Earth Sciences Services Corp. (ESSCO) has also provided acoustical geophysics data for portions of the Regal property.

The

Corporation is in the process of correlating and interpreting all of

the historic and new geophysical data with the objective of further

advancing exploration plans and associated drill targets.

Affinity

Metals has been granted a 5 Year Multi-Year-Area-Based (MYAB)

exploration permit which includes approval for 51 drill sites.

Qualified Person

The

qualified person for the Regal Project for the purposes of National

Instrument 43-101 is Frank O’Grady, P.Eng. He has read and approved the

scientific and technical information that forms the basis for the

disclosure contained in this news release.

About Affinity Metals

Affinity Metals is focused on the acquisition, exploration and development of strategic metal deposits within North America.

The Corporation’s flagship project and present focus is the Regal.

On behalf of the Board of Directors

Robert Edwards, CEO and Director of Affinity Metals Corp.

Posted by AGORACOM

at 3:57 PM on Tuesday, January 14th, 2020

Sponsor: Affinity Metals (TSX-V: AFF) a Canadian mineral exploration

company building a strong portfolio of mineral projects in North

America. The Corporation’s flagship property is the Drill ready Regal

Property near Revelstoke, BC. Recent sampling encountered bonanza grade

silver, zinc, and lead with many samples reaching assay over-limits.

Further assaying of over-limits has been initiated, results will be

reported once received. Click Here for More Info

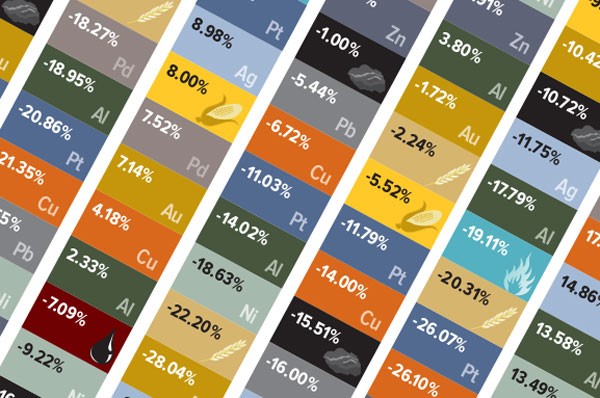

Near

the start of every year, I share our ever-popular Periodic Table of

Commodity Returns, now updated to reflect the final results of 2019. To

view the interactive table and download a copy of your own, click here.

Having

broken above $2,000 an ounce last week, palladium in now forecast by

Citi analysts to hit $2,500 by the middle of this year.

Commodities

as a whole had a mostly positive 2019, returning 16.53 percent as

measured by the S&P GSCI. This far surpasses commodities’ five-year

average return of about negative 11.52 percent, between 2014 and 2018.

Precious

metals were responsible for much of the growth. For the third straight

year, and for the fourth time in six years, palladium was the

top-performing commodity. The metal, used widely in the production of

catalytic converters, increased an incredible 54.21 percent to end 2019

at $1,912 an ounce, a slightly higher price than gold’s all-time high

set in September 2011.

As

was the case in past years, palladium benefited from mounting global

demand to curb emissions from gasoline-burning engines. It’s also among

the world’s scarcest precious metals, mined primarily in Russia and

South Africa, which means supply will potentially remain in deficit for

years to come.

Having

broken above $2,000 an ounce last week, palladium in now forecast by

Citi analysts to hit $2,500 by the middle of this year.

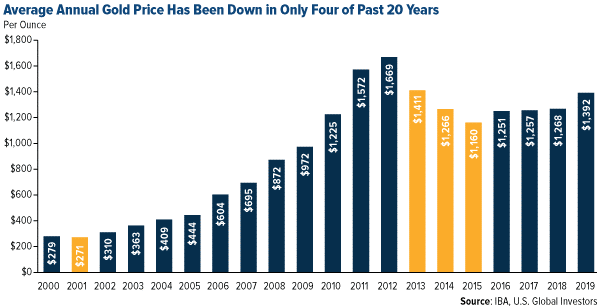

Gold Price Up in Four out of Every Five Years

Gold,

meanwhile, had its best year since 2010, climbing as much as 18.31

percent. The yellow metal’s role as an exceptional store of value shined

brightly in the second half of the year when the pool of negative-yielding debt

around the world began to skyrocket, eventually topping out at around

$17 trillion in August. On the news last week that Iran launched a

counterstrike against U.S.-occupied military bases in Iraq, the safe

haven briefly broke above $1,600 an ounce for the first time since April

2013.

In

the past two decades, gold has helped investors limit market volatility

and portfolio losses. Between 2000 and 2019, the precious metal’s

average annual price was down in only four years. Put another way, gold

was up on average in four out of every five years—a remarkable track

record.

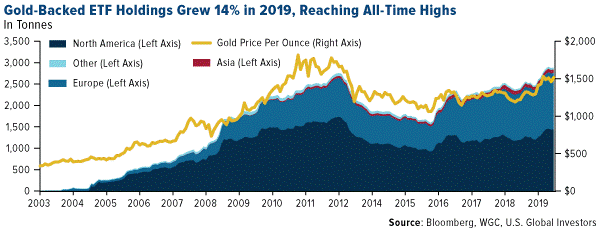

Safe

haven-seeking investors around the world piled into gold-backed ETFs in

2019, making it the best year on record for gold holdings. Assets under

management (AUM) in gold bullion ETFs expanded 37 percent from the

previous year, adding $19.2 billion, or 400 tonnes, according to the World Gold Council (WGC).

During the fourth quarter, total holdings hit a jaw-dropping 2,900

tonnes, the equivalent of 102 million ounces, which is the most on

record.

As

of the end of last week, gold looked slightly overbought on a relative

strength basis, meaning a correction wouldn’t be such a bad thing and in

fact expected.

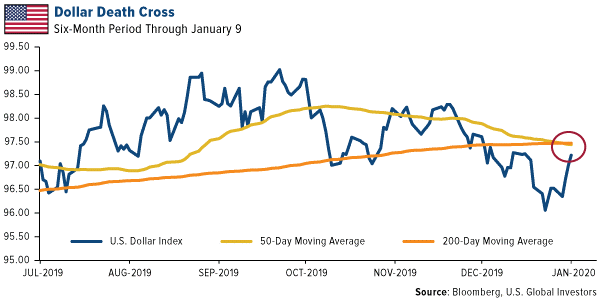

Has the Greenback Peaked?

Short

of escalating tensions in the Middle East or a pullback in stocks, the

catalyst for higher gold prices—and, indeed, commodity prices in

general—may very well be a substantial weakening of the U.S. dollar. On

Tuesday, the U.S. Dollar Index experienced a “death cross,†a bearish

signal that takes places when an asset’s 50-day moving average crosses

below its 200-day moving average. We haven’t seen this from the

greenback since May 2017.

Other

firms and analysts have recently made the case that the dollar is ready

to decline in 2020, which would give gold and other hard assets the

room to gain momentum. Below are just three such forecasts from the past

couple of weeks:

“Our

view is that the dollar is ready to decline in 2020 and will be

encouraged to do so as negative interest rates abroad turn less negative

while the Fed holds pat (or cuts)… In the event of an unlikely

recession in 2020, U.S. fiscal and monetary policy will turn sharply

expansionary, the dollar will decline further, and gold will do well.â€

~Murenbeeld & Co., January 3

“We

expect that U.S. dollar weakness will likely characterize global

financial markets throughout 2020… A weaker dollar is always good news

for commodity prices. We are particularly bullish gold at this point.

Gold is a direct play on a weaker dollar and could also benefit from any

major flare-up in geopolitical tensions.â€

~Alpine Macro, January 6

“Starting

2020, the key setup from a macro perspective is the confirmed top in

the U.S. Dollar Index as well as the U.S. Trade-Weighted Broad Dollar

Index… The U.S. Dollar Index (DXY) has broken below the 97 support to

trigger the bearish implication of the June-December topping pattern

(head-and-shoulders top) and the U.S. Trade-Weighted Broad Dollar Index

has broken below the early-November 2019 low as well as the 200-day

moving average to confirm a similar topping pattern to the DXY.â€

~CLSA, January 7

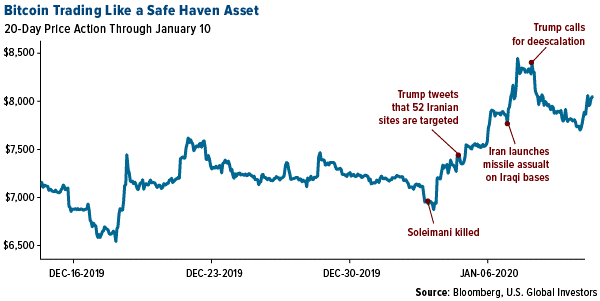

Bitcoin as a Safe Haven Asset

Gold

isn’t the only asset that responded positively to geopolitical

uncertainty involving Iran. The price of bitcoin, the world’s largest

cryptocurrency by market cap, surged on the news that President Donald

Trump had ordered a strike on Iranian general Qasem Soleimani, before

commenting that the U.S. was targeting as many as 52 sites in Iran.

From

January 2, the day before the strike, to January 8, when Trump

announced that Iran appeared to be “standing down,†bitcoin traded up as

much as 21 percent to its highest level in six weeks. In addition,

there were reports that local bitcoin sellers in Iran were charging three times the market rate in response to the threat of war with the U.S.

Google searches for “bitcoin†were also up. Cointelegraph reports that the search term “bitcoin Iran†exploded more than 4,450 percent in the seven days through January 8.

All

of this tells me that bitcoin continues to mature as an asset, and that

investors and savers increasingly trust it as a store of value in times

of uncertainty.

Looking for the inside scoop on mining companies? Click here

to read U.S. Global Investors portfolio manager Ralph Aldis’ interview

with MoneyShow and get his favorite mining picks for 2020!

Posted by AGORACOM

at 1:55 PM on Thursday, January 9th, 2020

Sponsor: Loncor is a Canadian gold exploration company focused on two projects in the DRC – the Ngayu and North Kivu projects, both have historic gold production. Exploration at the Ngayu project is currently being undertaken by Loncor’s joint venture partner Barrick Gold. The Ngayu project is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

Another year of covering commodities and select junior mining stocks is all but done and dusted.

We’ve seen palladiumprices

more than double those of platinum, its sister metal, on tight supply

and high demand for catalytic converters in gas-powered vehicles, as

smog-belching diesel cars and trucks get phased out to meet tighter air

emissions standards particularly in Europe and China.

Indonesia advanced a 2022 deadline for banning the export of mineral ores, including nickel,

prompting a massive surge in the price of the stainless steel and

electric-vehicle battery ingredient. In September, nickel powered past

$8 a pound, before slipping back to around $6/lb after the resumption of

Indonesian ore exports and weaker demand from the stainless

steel industry.

Palladium and nickel are both in-demand metals for the foreseeable

future, nickel for its use in batteries and stainless steel, and

palladium as an important ingredient of catalytic converters found in

gas-powered/ hybrid vehicles.

Zinc inventories

in February fell to the point where there were less than two days worth

of global consumption locked in London Metal Exchange (LME) warehouses.

The paucity of the metal used to prevent rusting caused prices to spike

to the highest since June 2018.

Gold started off the year around $1,300/oz,

and didn’t do much for the first half on account of higher interest

rates holding prices down. In July though, gold started to run when the

US Federal Reserve reversed course and began cutting interest rates

instead of raising them. The ECB and a number of other central banks

followed suit, wanting to keep interest rates low to try and boost

flagging economic growth.

The yellow metal advanced

to $1,550 in early September due to a combination of factors including

negative real interest rates (always good for gold), a sluggish dollar,

and safe haven demand owing to US tensions with Iran, impeachment,

Brexit fears, etc.

Copper had an off year in 2018 over fears of slowing

Chinese growth and the US-China trade war, but as we at AOTH have

always maintained, the market fundamentals are solid. Over

200 copper mines currently in operation will reach the end of their

productive life before 2035. Most of the low-hanging copper “fruit†has

been picked. New copper mines will be lower-grade and farther afield,

meaning higher capex and production costs.

Although copper prices suffered in the second and third quarter,

things are looking up for the essential base metal needed for plumbing

and wiring, power generation, communications, 5G networks, and electric

vehicles, which use around four times as much copper as a conventional

car or truck.

Energized by a rip-roaring fourth quarter, copper bulls are back on

board. From its 52-week low in August of $2.51/lb, the red metal gained

an impressive 11%, reaching a pinnacle of $2.83/lb Dec. 12, on

expectations of a trade war resolution between the world’s number one

and two economies, and the improved economic growth prospects that would

entail. Copper has risen 7% in December alone.

We pinned our thesis on three key points: 1/ Commodities are

cyclical, and the timing is right to get in now; 2/ The US dollar

is falling, and will likely continue to fall or be range-bound going

forward. A resolution to the trade war between the US and China, and a

looser monetary policy by the Federal Reserve (both of which are likely)

will weigh on the dollar and be good for commodities; 3/ The need for

infrastructure spending is not going to let up.

Close to a year later, our commodities hypothesis rings true. The dollar’s upward march in 2018 (DXY moved from 89 to 97) did stop

in 2019, helping commodities priced in US dollars. The US-China trade

war escalated but as we predicted, there was a resolution – not a

complete trade deal – but enough hope for one, to send copper, the most

important base metal, soaring in recent weeks.

At the beginning of the year, as stock markets bounced back from

their awful fourth-quarter 2018, everyone thought that the US economy

was roaring. We weren’t so sure, and presented evidence of a less

sanguine picture including negative fallout from the trade war with

China and a yield curve inversion which is a very accurate indicator of a

coming recession.

The US Federal Reserve appeared to agree. Worried about low growth,

globally and in the US, the Fed slammed the brakes on the interest rate

hikes it started in 2015, and began lowering them in July, 2019. That

immediately juiced gold and silver. Investors piled into precious metals as an alternative to near-zero or negative-yielding sovereign bonds. Looser monetary policy, check.

In later articles we showed the bullish cases for zinc, nickel and palladium.

The palladium price tripled from the start of 2016 to spring of 2019,

beating gold just under a year ago for the first time in 16 years.

Palladium has been in deficit for eight straight years, because of low

mined output and smoking-hot demand from the auto sector. So far in 2019

it has gained 47%.

Battery companies have been developing nickel-rich batteries in

two of the dominant chemistries for EVs, the nickel-manganese-cobalt

(NMC) battery used in the Chevy Bolt (also the Nissan Leaf and BMW i3)

and the nickel-cobalt-aluminum (NCA) battery manufactured by

Panasonic/Tesla. Added to Indonesia’s on and off export ban, a demand

boost from nickel’s growing use in electric-vehicle batteries, and

dwindling global stockpiles, have helped support nickel prices.

According to the USGS, despite new zinc mines opening in Australia

and Cuba, supply failed to keep up with consumption. Some very large

zinc mines have been depleted and shut down in recent years, with not

enough new mine supply to take their place. As a result, the zinc market

was in deficit in 2018.

Tighter environmental restrictions in China are lessening the amount

smelters can produce. National production of refined zinc in 2018 fell

to just 4.53 million tonnes, the sharpest downturn since 2013. The

result has been a record amount of refined zinc imported by the world’s

largest metals consumer, 715,355t in 2018. The high demand in China has

also pulled a lot of zinc out of LME warehouses.

In October zinc prices hit a four-month high due to falling zinc

stocks – inventories in London Metal Exchange-registered warehouses

plunged to 57,775 tonnes – a smidgen higher than the 50,425t in April,

the lowest since the 1990s, Reuters said.

Tough market for explorers

It’s good to see we were right about so many metal markets.

Regrettably however, the valuations of mineral exploration companies

have yet to follow the prices of the metals they are hunting.

Indeed the junior mining sector has been in a funk since around 2012.

The juniors’ place in the mining food chain is to provide projects to

be turned into mines for larger mining companies whose reserves are

running low. This is becoming a growing problem as all the low-hanging, high-grade deposit fruit has been picked. Such is the case for gold, silver, copper, palladium,

zinc and nickel, all of which are encountering, or will shortly

encounter, supply deficits, amid booming demand for battery metals and

precious metals.

Finding the kind of grades at amounts that will make a mine

profitable usually requires going farther afield or deeper – greatly

adding to costs per ounce or tonne.

Here’s the problem juniors have been facing: At the same time as

investment capital has been pulled out of the mining majors and

mid-tiers – by investors tired of seeing falling or stagnant stock

prices/ red ink balance sheets – there’s been a dearth of speculative

capital flowing into exploration companies.

The ascendance of index funds has also made it harder for juniors to

attract money, because they are too small to be in the funds that these

vehicle track.

According to a 2019 report by PDAC –

the association that puts on the annual mining show in Toronto –

and Oreninc, a junior financing tracker, equity financing in 2018 was

35% less than in 2017 – a decade-low $4.1 billion.

A good chunk of that cash went to marijuana stocks, as dozens of

companies emerged to take advantage of the pot legalization bill passed

by the Canadian federal government. Whereas weed stock IPOs attracted

$491.1 million in investment dollars in 2018, mining IPOs only accounted for $51.6 million, a startling drop from the $830 million in 2017.

That’s a lot of speculative capital pulled out of resource stocks.

However it’s not all gloom and doom, according to TD Securities mining

investment bankers, who say “current market conditions and historical

precedents make them optimistic generalist investors will return in

greater numbers to mining stocks,†Bloomberg reported:

“The current market is reminiscent of the late 90’s and early 2000’s,

[TD Securities’ Deputy Chairman Rick] McCreary says. At the time,

investors had low interest in mining, and companies found it hard to

raise capital. That was followed by waves of consolidation and a mining

bull run. A similar trend may be building as this ‘period of

consolidation’ rolls on.â€

Gold M&A

As far as that goes, mining companies, especially in the gold space,

have realized since the vicious 2012-16 bear market, they have cut as

much as they can and the next step is to bring assets and companies

together. On top of that, the top gold miners are running out of

reserves, and are looking to replace them with high-margin projects that

have the right combination of grade, size and infrastructure.

This explains Barrick combining with South Africa’s Randgold, the Barrick-Newmont joint venture in Nevada,

the fusing of Newmont and Goldcorp, a $1-billion deal for Lundin Mining

to acquire a Brazilian copper-gold mine from Yamana Gold, Newcrest’s

70% purchase of Imperial Metals’ Red Chris mine in British Columbia, and

other recent examples of gold mining M&A.

Among December’s gold deals are Zijin Mining’s cash purchase of

Continental Gold’s Buriticá project in Colombia, for CAD$1.3 billion;

and a $770 million merger between two mid-tier gold miners, Equinox Gold

and Leagold Mining. The latter arrangement will keep the Equinox name

and create a company valued at $1.75 billion with six mines spread

across Brazil, Mexico and the United States.

Junior resource M&A?

The goal of every junior resource investor is for the company(ies)

they are invested in to get bought out, resulting in a 5, 10, even

20-bagger.

The question is, will the current round of mergers and acquisitions

at the major and mid-tier level trickle down to the juniors? PwC appears

hopeful. In its 2019 report ‘Shifting Ground’ the mining consultancy states,

The heightened level of deal activities, most of which have been

in the gold sector, may well spark further moves among intermediate

players seeking to grow into multi-project companies. A new phase of

industry consolidation could pave the way for more exploration and mine

development and boost investor interest and activity.

Another optimistic opinion comes from Tom Palmer, chief operating officer at Newmont, who told the Wall Street Journal that smaller

players are waiting to see what the bigger miners sell once they have

completed their mergers before they start their own M&A.

“Fast forward two or three years, there will be countless more†mergers, he said.

In fact we are already starting to see this happening. Nevada has

witnessed the return of junior gold explorers, and majors, after a lull

in activity between 2012 and 2016. According to an industry report,

exploration in Nevada increased by 15% in 2017, with 19,040 new claims.

The tide has continued to turn in mining’s favor, with 198,337 active

claims as of January, 2019 – 7% more than in 2018.

In 2018 Idaho-based Hecla Mining snapped up Klondex Mines for US$462

million, delivering three more Nevada properties – Fire Creek, Midas and

Hollister – to Hecla’s stable of mines and adding 162,000

gold-equivalent ounces to its annual production.

Also in Nevada, last year Alio Gold paid Rye Patch Gold $128 million

for the Vancouver-based company and its past-producing Florida Canyon

mine.

The 2019 creation of Nevada Gold Mines (the Barrick-Newmont JV) has

piqued the interest of other companies looking to discover and develop

new ounces in the golden state. Major miners with new projects include

AngloGold Ashanti, Coeur Mining and Kinross Gold. For the details read Getchell’s Gold

And for an inspiring story of junior mining success in Canada, look

no further than Great Bear Resources. Working the historic Red Lake gold

camp in Ontario, Great Bear’s drills discovered the “LP Fault Zoneâ€

this past May. That eureka moment, the realization that most of the gold

on its property is structurally controlled, prompted a massive 90,000m

drill program aimed at identifying the parameters. The discovery of

three new gold zones with high-grade intercepts, along with the earlier

nearby Hinge-Dixie Limb discoveries, caught the market’s attention;

within 18 months, Great Bear’s stock catapulted 2,000%.

Conclusion

I firmly believe that 2019 has been a pivotal year for junior mining.

Coming out of 2018’s slump in several commodities, due mostly to the

uncertainty associated with the US-China trade war, this year we saw

very strong performances from gold, silver, copper, palladium, nickel

and zinc – having correctly predicted price corrections for each.

While it’s disappointing not to see a rising tide of junior miner

stock prices to accompany these bullish calls, we continue to believe.

After all, we want to own the cheapest most in demand metals we can

find to reap the maximum coming rewards. That means buying it while it’s

still in the ground.

The fact is junior resource companies – the owners of the world’s

future mines – are on sale. If you like their management teams, their

projects and their plans for 2020, perhaps now is the time to be

acquiring a position.

Posted by AGORACOM

at 2:39 PM on Wednesday, January 8th, 2020

Sponsor: Affinity Metals (TSX-V: AFF) a Canadian mineral exploration

company building a strong portfolio of mineral projects in North

America. The Corporation’s flagship property is the Drill ready Regal

Property near Revelstoke, BC. Recent sampling encountered bonanza grade

silver, zinc, and lead with many samples reaching assay over-limits.

Further assaying of over-limits has been initiated, results will be

reported once received. Click Here for More Info

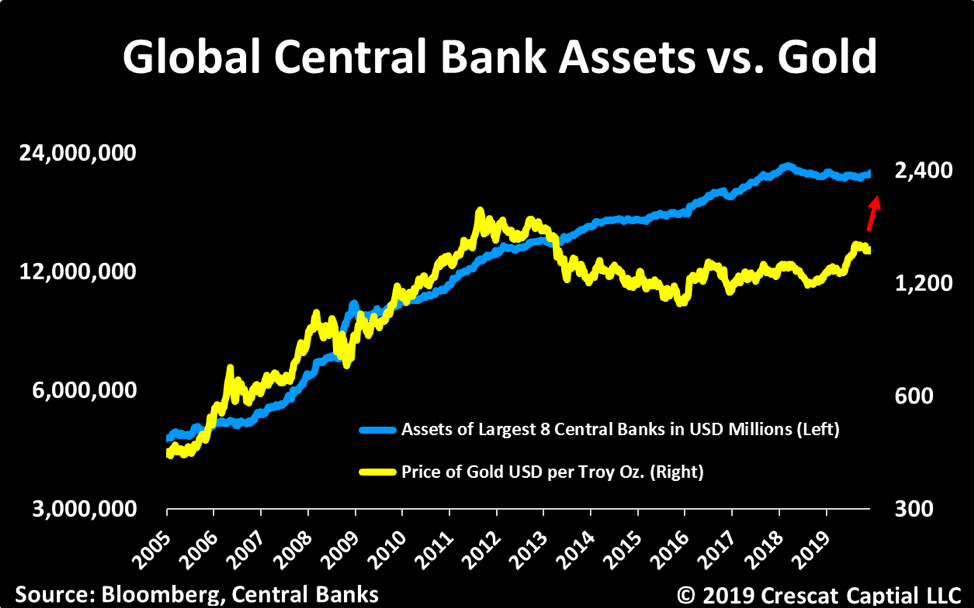

Excerpts from Crescat Capitals November Newsletter:

Precious Metals

Precious metals are poised to benefit from what we consider to be the best macro set up we’ve seen in our careers. The stars are all aligning. We believe strongly that this time monetary policy will come at a cost. Look in the chart below at how the new wave of global money printing just initiated by the Fed in response to the Treasury market funding crisis is highly likely to pull depressed gold prices up with it.

The gold and silver mining industry endured a severe bear market from 2011 to 2015 and have formed a strong base over the last four years.

The imbalance between historically depressed commodity prices

relative to record overvalued US stocks remains at the core of our macro

views. On the long side, we believe strongly commodities offer

tremendous upside potential on many fronts. Precious metals remain our

favorite. We view gold as the ultimate haven asset to likely outperform

in an environment of either a downturn in the business cycle, rising

global currency wars, implosion of fiat currencies backed by record

indebted government, or even a full-blown inflationary set up. These

scenarios are all possible. Our base case is that governments and

central banks will keep their pedals to the metal to attempt to fend off

credit implosion or to mop up after one has already occurred until

inflation becomes a persistent problem.

The gold and silver mining industry is precisely where we see one of

the greatest ways to express this investment thesis. These stocks have

been in a severe bear market from 2011 to 2015 and have been formed a

strong base over the last four years. They are offer and incredibly

attractive deep-value opportunity and appear to be just starting to

break out this year. We have done a deep dive in this sector and met

with over 40 different management teams this year. Combining that work

with our proprietary equity models, we are finding some of the greatest

free-cash-flow growth and value opportunities in the market today

unrivaled by any other industry. We have also found undervalued

high-quality exploration assets that will make excellent buyout

candidates.

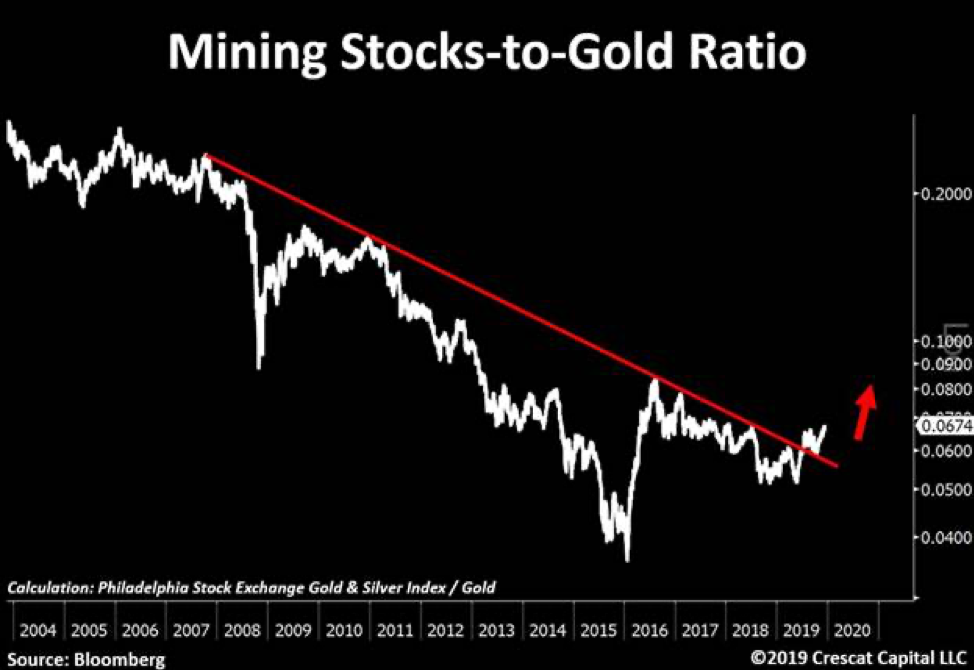

We recently point out this 12-year breakout in mining stocks relative

to gold now looks as solid as a rock. In our view, this is just the

beginning of a major bull market for this entire industry. We encourage

investors to consider our new Crescat Precious Metals SMA strategy which

is performing extremely well this year.

“This is just the beginning of a major bull market for this entire industry”

Zero Discounting for Inflation Risk Today

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, if the global financial markets

cannot absorb the increase in Treasury debt, the Fed will be forced to

monetize it even more. The problem is that the Fed’s panic money

printing at this point in the economic cycle may hasten the unwinding of

the imbalances it is so desperate to maintain because it has perversely

fed the last-gasp melt up of speculation in already record over-valued

and extended equity and corporate credit markets. It is reminiscent of

when the Fed injected emergency cash into the repo market at the peak of

the tech bubble at the end of 1999 to fend off a potential Y2K computer

glitch that led to that market and business cycle top. After 40

years of declining inflation expectations in the US, there is a major

disconnect today between portfolio positioning, valuation, and economic

reality. Too much of the investment world is long the “risk parityâ€

trade to one degree or another, long stocks paired with leveraged long

bonds, a strategy that has back-tested great over the last 40 years, but

one that would be a disaster in a secular rising inflation environment.

With historic Federal debt relative to GDP and large deficits into

the future as far as the eye can see, rising long-term inflation, and

the hidden tax thereon, is the default, bi-partisan plan for the US

government’s future funding regardless of who is in the White House and

Congress after the 2020 elections. The market could start discounting

this sooner rather than later. The Fed’s excessive money printing

may only reinforce the unraveling of financial asset imbalances today as

it leads to rising inflation expectations and thereby a sell-off in

today’s highly over-valued long duration assets including Treasury bonds

and US equities, particularly insanely overvalued growth stocks. We

believe we are in the vicinity of a major US stock market and business

cycle peak.

Source:”Running Hot”

Courtesy of Crescat Capital: https://www.crescat.net/running-hot/

Posted by AGORACOM

at 11:54 AM on Monday, January 6th, 2020

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

In this update I am not going to repeat the points made in the last

fairly comprehensive update, instead we are going to focus on the

importance of the resistance level just above where the price is now,

and impact of the killing of the Iranian General and its potential

implications for the gold price.

On the latest 10-year chart we can see that gold is making a 2nd

attack on the key major resistance level in the $1530 – $1560 zone,

which is hardly surprising considering what happened last week.

The reason that this resistance level is of such major

importance is made abundantly clear by the following chart made by a

subscriber and kindly forwarded to me, which I reproduce with his

permission. As we can see gold made no less than 5 significant lows at

this level between 2011 and 2013, before it finally crashed this support

and plunged 15% in 2 days, so it is clearly of huge significance and is

the biggest hurdle by far on the way up. Therefore, even given the

latest mayhem in the Mid-East, we should not be surprised if it now

stalls out here and possibly backs off for a while to form a trading

range, which is also made likely by its now being critically overbought

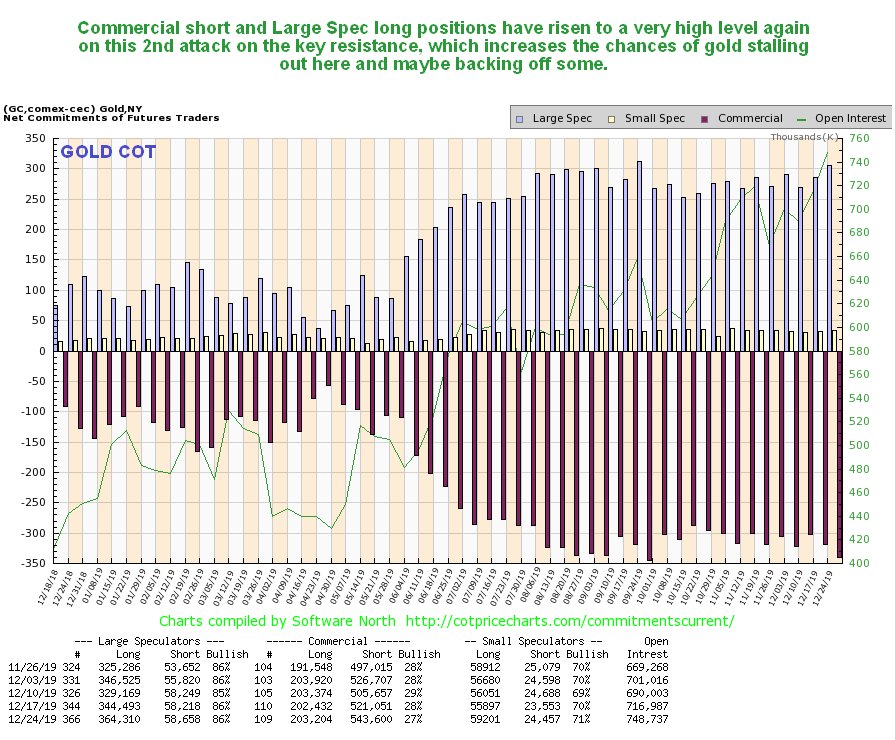

on its RSI indicator and by the latest COTs, which we will look at lower

down the page, coming in with really extreme readings again. This makes

sense given that we now at a time of maximum tension.

From a subscriber – highlighting gold’s key support at the $1530 – $1560 level, which is now of course strong resistance…

Detail showing the plunge that was triggered the failure of this support…

On the 6-month chart we can see how, after breaking out of the

corrective downtrend in force from early September, gold has risen

steeply, without one down day so far to become critically

overbought on its RSI indicator as it drives into the zone of strong

resistance with volume becoming heavy on Friday. This of course

increases the chances of its reacting back the moment tension over the

Mid-East situation eases, even if only slightly.

As for the COTs, they are showing extreme readings once more

(chart is for 24th December), which suggest that, especially if tension

over the Iran situation eases short-term, gold will probably back off

some into a consolidation pattern that will enable it to charge up

sufficiently to take out the key resistance in due course.

Click on chart to popup a larger, clearer version.

Now we come to the possible impact of the US killing of the top

Iranian General. In order to figure out the real motivation for this

act, we simply have to ask the usual question “Who stands to gain?†The

first interest group that stands to gain is the US military, which

receives about $700 billion of taxpayers’ money every year, and probably

about $500 billion of this is in excess of what it needs to defend the

Homeland. So in order to justify this bloated budget it creates enemies

and conflicts around the world. The next interest group is Israel, which

controls the US and uses the US military as a sledgehammer to achieve

its objectives which include dominance of the Mid-East. Iran is the big

prize. Finally the Republicans and Trump himself stand to gain at the

polls later this year as the population will predictably “rally round

the flag†as a result of conflict with Iran. Knowing all this, we can

quickly deduce that the killing of the Iranian General was an act of

extreme provocation designed to trigger some kind of counter attack by

Iran that can then be used as an excuse to launch a bombing campaign

against it. Even if Iran exercises maximum restraint and does nothing

beyond making empty threats to assuage its angry populace, it may still

fall victim to an onslaught after a calculated false flag attack which

is blamed on it. So whatever it does, it loses – it’s been put in a

classic “zugzwang†situation.

For all the bluster, Iran’s military is no match for that of the US

of course, which spends more than the rest of the world put together on

arms. The best way for Iran and Islam in general to “get even†with the

West for all its many decades of Colonial interference in the Mid-East,

exploitation and massive destruction inflicted on places like Iraq and

Libya and the Palestinians therefore (looked at from their point of

view) is to conduct “asymmetrical warfareâ€, invade Western countries and

attack their churches

and institutions etc, and then take them over gradually by outbreeding

them. Western societies are now too corrupt, decadent, morally bankrupt

and weak to stop this happening, and it is happening right now in

Europe, and the only reason it isn’t happening to the same extent in the

US is that it is a lot harder to pilot a rubber dingy across the

Atlantic Ocean than the Mediterranean Sea, although as we know the

Democrats and the Left appear to trying to take up the slack by

destroying the country from within in places like Portland, L.A. and San

Francisco, and this rot will spread unless right minded people take a

vigorous stand.

All this is mentioned because it is clear that the killing of the

Iranian General is the prelude to a military strike against Iran, which

will probably take the form of an extensive and intensive bombing

campaign that both Israel and the US have been looking forward to for

years, because a ground invasion is out of the question due to the

geography and logistics. The goal as usual will be to destroy its

military capability and wreck its infrastructure with the eventual aim

of installing a puppet government and opening up the country to Western

exploitation, and the wild card in all this will be whether Russia and

China will do anything to prevent it, or just stand and watch. It is

thought that they don’t have the nerve to intervene. In any event, if

such a campaign is launched, we can expect the world to be gripped by an

acute sense of crisis and gold will spike. Iran may have the ability to

disrupt the flow of oil out of the Persian Gulf, albeit temporarily,

which would trigger an oil price spike and a stockmarket crash.

Last week’s updates concluded with a look at the highly bullish

charts for gold measured against the Australian dollar and the Japanese

Yen, and this week we will look at gold against the Canadian dollar and

the Swiss Franc.

While many investors are still agonizing about whether gold is in a

bullmarket or not, that is because they are fixated on the charts for

gold in US dollars. When you look at gold in other currencies you

realize that it is already very much in a bullmarket, and recently made

new highs against many currencies, like the Canadian dollar shown below…

Even against the Swiss Franc, which amongst currencies enjoys

some safe haven status, gold is performing better than it is against the

dollar…

…and we should remember that the dollar may not remain as “king

of the hill†forever, especially as a number of major powers in the Asia

especially are preparing to ditch it.

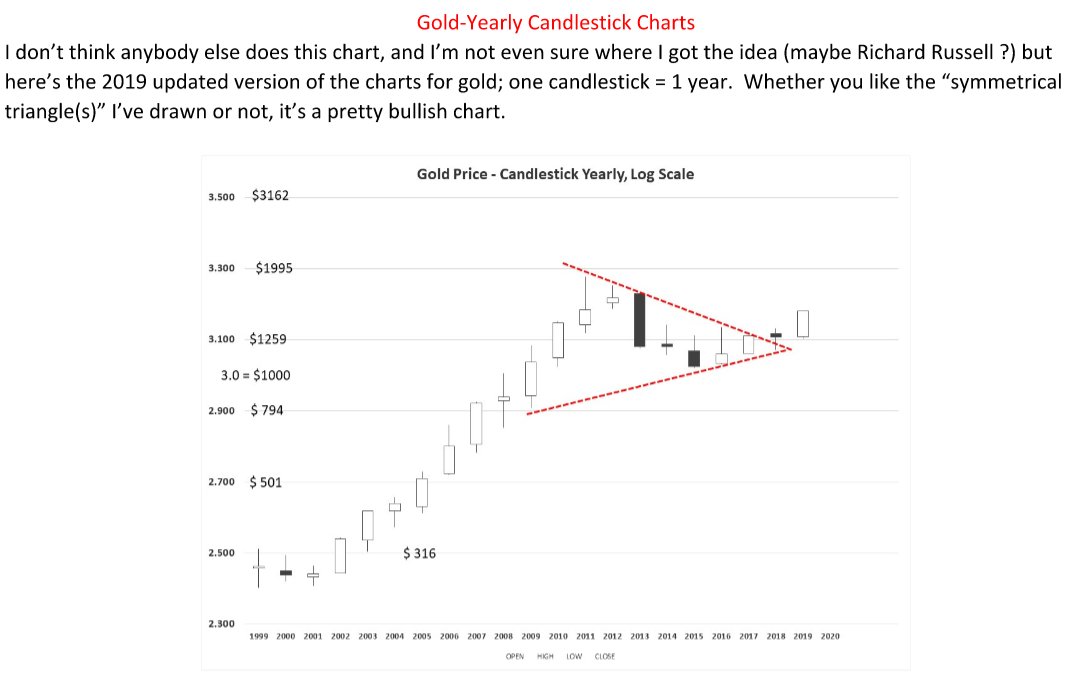

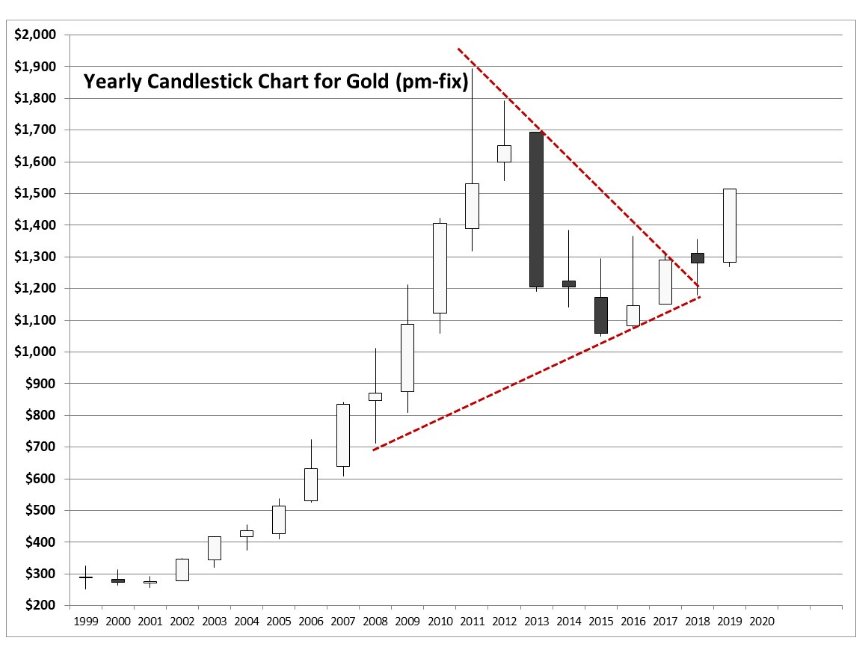

Finally, we are going to take a quick look at an unusual chart for

gold submitted by the same subscriber as some of the charts above. It is

unusual because it is a yearly candlestick chart, meaning that each

candle on it is for an entire year. Its supreme advantage is that it

keeps things simple. The Triangle shown on it is his interpretation, not

mine. It certainly looks positive here with a big white candle for

2019, with the arithmetic version shown looking even more bullish. This

type of chart also has a potential advantage for the writer, as if only

this chart were used, I would only have to write these updates once a

year.

Courtesy of Clive Maund: https://www.clivemaund.com/gmu.php?art_id=68&date=2020-01-05

Posted by AGORACOM

at 1:21 PM on Friday, January 3rd, 2020

Sponsor: Affinity Metals (TSX-V: AFF) a Canadian mineral exploration company building a strong portfolio of mineral projects in North America. The Corporation’s flagship property is the Drill ready Regal Property near Revelstoke, BC. Recent sampling encountered bonanza grade silver, zinc, and lead with many samples reaching assay over-limits. Further assaying of over-limits has been initiated, results will be reported once received. Click Here for More Info

With an impressive start to the year this new heightened geopolitical development could be the catalyst to break out gold to multi year highs. The U.S. strike that killed a key Iranian general could have a ripple effect on the signing of the trade agreement on the 15th as China and Iran have recently worked together on joint military operations along with Russia. Any set back in the trade agreement would severely impact the direction of U.S. equities and the expectations for interest rate decisions globally. Price Analysis and Outlook The daily gold chart shows that momentum indicator slow stochastics are rising steadily and reaching overbought territory giving longer term indication that we have pushed into a Bull Market. While ADX, which measures strength of the trend, has turned up over 40 showing that the driving force behind the recent upward move is very strong. The 2 key levels of support to watch are the November 1st high of $1525.2 and the December 30th high of $1519.1. This should act as a consolidation level while a likely upside target completing this trend would be an objective of $1572

Posted by AGORACOM

at 3:03 PM on Wednesday, December 18th, 2019

Sprott is eager to believe junior gold miners are on the verge of striking the motherlode, but skeptical of nearly everything else related to the industry

One week before Halloween, Canada’s biggest gold enthusiast,

the septuagenarian billionaire Eric Sprott, wearing a neatly pressed tuxedo,

bounded onto a stage in a downtown Toronto ballroom and accepted his induction

into Canada’s Investment Industry Hall of Fame.

He declared himself both humbled and honoured, and then

rollicked into the wee hours of the night at his home in a nearby tower with

expansive views of the city’s sparkling skyline. The next morning, though 75

and technically retired, he showed up at his office, grumbling about a lack of

sleep, but dressed in a magenta-coloured, paisley button-up, ready for a 9 a.m.

meeting with a penny stock exploration company.

“I keep reading that people are never making (gold)

discoveries, the rate of discoveries is going down,†he said, occasionally

rubbing his temples and closing his eyes. “The funny thing, well, I guess I’m

the sucker then because I keep buying guys who say they’re making discoveries.â€

Just as the price of gold often moves in the opposite

direction of the stock market, Sprott has a strong contrarian streak that means

he also often moves in the opposite direction of the market. For example, this

past spring, after years of middling precious metal prices and declining

discoveries had led most investors to abandon Canada’s gold and silver

explorers, he decided to go all-in.

Sprott launched an investment blitz, the likes of which the

junior mining precious metals sector had seldom seen, doling out somewhere

between $200 and $300 million in a matter of just a few months to acquire large

stakes in about two dozen companies, most of which have never earned a dollar

of revenue

His investments between May and July accounted for about one

in every four dollars raised by junior miners, according to Vancouver-based

market research firm Oreninc. During that time, gold prices started to rise,

breaking through US$1,400 in June for the first time in six years, bringing

some investors back to the major miners — exactly where Sprott doesn’t want to

be.

“They’re the worst place to put money, okay?†he said.

Putting his money where his mouth is, he has been selling his position in Kirkland Lake Gold Ltd., one of, if

not the lowest-cost gold producers and one of the best-performing stocks on the

S&P/TSX Composite Index since 2016.

Sprott was an early investor in Kirkland Lake, was appointed

chairman in 2015, and one year later helped engineer its merger with Newmarket

Gold Inc., a small gold producer in Australia. Not long after, the newly merged

company discovered high-grade veins at two mines, which propelled its stock

upwards to $63 per share.

Many investors pride themselves on not selling when a stock

hits a bump, but Sprott said it is equally important to not sell when the stock

rises, at least not until it’s gone up five or even 10 times, a so-called

tenbagger.

“I’ve had lots of tenbaggers and the important thing is to

stay in it,†he said.

But when his stake in Kirkland Lake reached about $1.3

billion earlier this year, and it looked like gold prices would keep rising,

Sprott said he decided it was time to sell.

“Here’s what I say to the management of Kirkland Lake: you

will not be the No. 1 performing stock this year,†he said during an interview

in October. “You will not be, because companies like Eldorado (Gold Corp.) and

Detour (Gold Corp.) are going to kick your butt.â€

And yet, Sprott — who found out about the deal on a day he

was meeting with a junior mining company seeking investment — elected to

support the deal, and waxes enthusiastic about Detour.

It’s one of the reasons why Sprott doesn’t much care about Canada’s major gold miners.

The

best-run companies might provide 20- or 30-per-cent returns, or maybe

100 per cent in a few cases, but Sprott would rather invest in a company

that might strike gold and give him a 500-per-cent return, or even a

coveted 1,000-per-cent return.

In

July, Sprott had bought about 10 million shares at $3.10, meaning he

made about $25 million or a 75-per-cent return in just a few months. But

he was nonplussed, saying the buyout may have come a little early.

“You’ve got to have the dream, right?†he said. “You’ve got to have the dream you’re going to find something.â€

Therein

lies Sprott’s biggest paradox: he’s eager to believe that junior gold

miners are on the verge of striking the motherlode, but skeptical of

nearly everything else related to the gold industry.

You’ve got to have the dream, right? You’ve got to have the dream you’re going to find somethingEric Sprott

After a five-decade career in the financial

services industry, during which he worked as an investment banker and

founded an eponymous empire that includes fund and asset management

firms, a brokerage firm, bullion storage and more businesses, he is

skeptical of commercial banks, major precious metals miners, central

banks, the stated rate of annual inflation and, perhaps above all, gold

and silver prices.

“One of the things about the media, they never

talk about the gold conspiracy,†he said. “Look at the guys who are

paying fines for spoofing the precious metals markets. Every two weeks

some guy’s paying a fine.â€

Case in point, U.S. prosecutors in

September filed criminal charges against three JPMorgan Chase & Co.

bankers for allegedly spoofing the precious metals market, which means

placing fake orders and then quickly cancelling them to manipulate the

price. The indictment alleged a decade-long conspiracy.

Sprott

believes the futures market — where investors can buy options that

essentially allow them to place bets on the price of gold or silver

without actually having to own any of the metals — allows commercial

banks to exert way too much influence on the market for physical metals.

Stacked gold bars in Germany.

Michaela Handrek-Rehle/Bloomberg files

As someone who stockpiles bullion, and often gives it out as

a gift, he watches the prices of silver and gold so closely it often

colours his mood.

This fall, Sprott was out fishing for grouper on

a staffed boat somewhere warm on a Friday when he normally records his

podcast. In spite of his idyllic circumstances, he sounded distinctly

downtrodden when he called in to the podcast.

“I’ve had better days, you know, it’s a bit of a tough one,†he said.

As

the podcast progressed, it soon became clear that gold and silver

prices were both down, about four and six per cent, respectively, and

options market manipulation appeared to be the reason to him.

Juan

Carlos Artega, director of investment research at the World Gold

Council, is skeptical that banks are having a significant effect on gold

or silver prices through the futures market, but believes options do

have an impact on short-term prices.

As

someone who stockpiles bullion, and often gives it out as a gift, he

watches the prices of silver and gold so closely it often colours his

mood

“What you find is that the gold price is

responding to demand-and-supply dynamics including those on the

(options) market, but it’s only one component,†he said.

Artega

said central bank and consumer buying, production numbers, recycling,

investment in gold-backed exchange-traded funds and a host of other

factors play a role in determining long-term prices.

Sprott would

hear none of it, and said he’s long disagreed with the World Gold

Council about many things. His skepticism of the futures market ties in

to his skepticism of the financial market writ large.

“We have a weird financial system; it doesn’t make any sense to a rational thinker,†he said.

Gene

McBurney, co-founder of GMP Securities LP, once a competitor of Sprott

Inc. in the investment business and now a friend, said part of the key

to understanding Sprott is that he enjoys entertaining other people with

provocative comments.

Fine gold coins at a bullion dealer in London.

Chris Ratcliffe/Bloomberg files

“He’s told people there’s no gold in Fort Knox; that kicks off an interesting conversation,†he said.

But

McBurney added that he believes Sprott is extremely well versed in the

companies in which he invests, and he has even given some of his

personal money to Sprott to manage.

Peter Grosskopf, chief

executive of Sprott Inc., the asset management firm Sprott founded and a

mentee, said Sprott is always covered as being this “unbelievable gold

bug,†but there’s a lot more to it than that.

“I mean, he’s a savant at what he does,†said Grosskopf, who added that it’s not easy to explain how Sprott does what he does.

That’s

mainly because Sprott is investing in companies that have no revenue,

which means standard investment metrics, such as internal rate of

return, aren’t necessarily useful, never mind that he said they’re not

something he would use.

He’s a savant at what he doesPeter Grosskopf, chief executive of Sprott Inc.

Instead, he attempts to value companies based on whether they are likely to discover a deposit of precious metals.

Of

course, even if a company discovers a deposit, it would still need to

figure out whether it makes economic sense to extract the deposit,

including how much it would cost to build and operate a mine, which

requires further calculations about energy costs, transportation,

processing and refining, and so on.

Sprott said he focuses solely

on the deposit and how big it could be. Though he has no education in

geology, he said he has devised his own valuation method, which involves

looking at a few variables to determine the potential size of a

deposit.

“I want to turn it into numbers, like, okay, what could

this thing earn?†he said. “You know, you multiply the strike by the

depth by the width by 2.7 specific gravity times the ounces — it’s just

four or five things you’ve got to multiply, five things.â€

People

close to him said he studies junior mining companies and can recall the

details of his investments better than most fund managers.

“The

guy gets up at ungodly hours, he might get up at 2 a.m. studying,†said

Conor O’Brien, a former capital markets manager who joined Sprott in May

to help with the investment blitz. “Neither one of us are geologists,

we’re just financial people that can do mathematics, as opposed to the

geology. We more kind of conceptualize, and dream and kind of multiply.â€

Putting

his latest investment spree of more than $200 million in perspective,

the TSX Venture Exchange’s junior mining sector through August was on

course to raise $2 billion for all of 2019, about 27 per cent less than

it did in 2009.

Sprott takes a birdshot approach to investment

that spreads his money far and wide, so that his portfolio contains

companies exploring for high-grade and low-grade mines, potential

open-pit and potential underground mines, and so on.

“Most of them won’t make it,†he said. “But what about the ones that do? If I’m in early and I stay the ground, I press the bet. It’s like being at a table with a winning run, you keep doubling down.â€

Grosskopf said Sprott calls it “stealing value,†not because he’s

conning anyone, but because he’s investing in assets the market has

mispriced. He said the billionaire is an expert trader, adept at sizing

up an opportunity and timing his entrance and exit.

And because of

his outsized profile, recently juiced by his epic returns while

chairman of Kirkland Lake, there are hordes of investors who will follow

his lead, Grosskopf said.

Not all of Sprott’s bets work out, of course. In 2017, Sprott said he invested in Garibaldi Resources Corp., a nickel explorer, based on comments he read on an online chat board.

Its

stock surged 1,731 per cent that year, and Sprott has continued to

invest even though two years later, its stock has declined from a peak

above $4 in late 2017 to 87 cents today.

“They’re for sure

drilling, we know that, and they’ve announced some holes, and they’ve

got more to go,†Sprott said. “They haven’t found the motherlode they’re

looking for. Even I’ll say that.â€

Sprott’s vast ownership may

also have a downside: It’s not easy to liquidate his positions in

companies without attracting attention. But his vast wealth also means

he’s relatively insulated from a lot of threats, such as dilutive

financings or litigation, that smaller investors can’t afford to

participate in.

He also owns a private gold mining company in

Nevada called Jerritt Canyon Gold LLC, which he said made its first

profit in the third quarter.

Kevin Small, vice-president of

operations at that mine, said Sprott likes to be generous. In April, he

said Sprott showed up at the site and handed out silver coins to several

hundred people who work there.

“He said when you guys make lots of money, I’ll give you each a gold coin, but he hasn’t been back yet,†Small said.

Eric Sprott at his induction into Canada’s Investment Industry Hall of Fame in October.

Peter J. Thompson/National Post

But he added that Sprott has been investing heavily in the

operation, which has a capacity to produce 280,000 ounces of gold per

year, and predicted the company would soon be well known.

Colleagues

also add that he can be unrelenting when judging a company’s financial

performance. Case in point, one of his biggest gripes with Kirkland Lake

is that he wants it to increase its dividend, an issue he once again

raised in October after the miner posted solid quarterly results.

Kirkland

Lake pays a quarterly dividend of four cents, and chief executive Tony

Makuch said he may consider raising it, but the company still needs to

spend money on exploration so it can improve its reserves of gold.

“We’re

not an industry people should be buying for dividends,†Makuch said.

“You should be buying bank stocks or something else. If you look at our

share price, that comes from investing in new projects.â€

It’s a sentiment that Sprott would likely agree with.

“I still have a lot of money in Kirkland and it’s a great company, but it’s not a tenbagger from here,†he said. “And I like tenbaggers as opposed to 100 per cent. It’s just my nature.â€

Posted by AGORACOM

at 11:45 AM on Wednesday, December 18th, 2019

Sponsor: Affinity Metals (TSX-V: AFF) a Canadian mineral exploration company building a strong portfolio of mineral projects in North America. The Corporation’s flagship property is the Drill ready Regal Property near Revelstoke, BC. Recent sampling encountered bonanza grade silver, zinc, and lead with many samples reaching assay over-limits. Further assaying of over-limits has been initiated, results will be reported once received. Click Here for More Info

Central bankers have been voracious buyers of gold during the last two years, and analysts look for that trend to continue in 2020.

Through the end of October, net official-sector purchases this year

totaled 562 metric tons, reported Alistair Hewitt, director of market

intelligence with the World Gold Council. That 56.2-tons-a-month average

puts sales on pace to roughly match the 656 tons bought in 2018, which

were the most central-bank purchases since 1967, according to WGC data.

“This year has been exceptionally strong. We think that next year,

net buying will continue at a high level, even if it’s not as high as

this year,†said Philip Newman, director of the London-based consultancy

Metals Focus.

Goldman Sachs looks for global central banks to collectively acquire

around 650 tons in 2020, while Standard Chartered is projecting

central-bank purchases will total 525 tons.

“It’s still elevated,†said Suki Cooper, precious-metals analyst with

Standard Chartered. “That is still firmly on the buy side.â€

‘Safe, liquid and generates returns’

Hewitt commented that central banks are looking at three main

criteria when deciding to expand the amount of gold they hold within

their foreign-exchange reserves.

“For a central bank, gold is a fantastic asset because it’s safe, liquid and generates returns over the long term,†Hewitt said.

He also listed two more factors why the central-bank buying has suddenly jumped in recent years.

“One issue is we are seeing heightened geopolitical tensions,†Hewitt

said, with these involving major gold-buying countries and economies.

“Central banks are looking toward gold to balance some of that risk.

“We’ve also got negative rates and yields for a large number of sovereign bonds.â€

Newman added that many central banks are “trying to get away†from

the U.S. dollar. This is especially the case with Russia due to U.S.

sanctions, he added.

As recently as 2017, most of the official-sector buying came from a

handful of central banks, including Russia, Turkey and Kazakhstan. But

in 2018 and 2019, there have been a slew, including some that had not

been in the market for years.

“You’ve got a whole range of buyers,†Newman said.

The largest buyers during the first 10 months of the year were Turkey

with 144.8 tons; Russia, 139; Poland, 100; and China, 95.8.

Others include Kazakhstan, 26.9 tons; India, 17.7; Qatar, 11; Ecuador, 10.6; Serbia and the U.K., 9.9; Argentina, 7; Colombia, 6.1; Kyrgyz Republic, 3.2; Mongolia, 2.3; Belarus, 1.9; Guinea, 0.9; Egypt and Mauritania, 0.7; Albania and Malta, 0.6; and Ukraine and Greece, 0.3.

Goldman Sachs projected that central-bank purchases could amount to as much as 22% of global supplies during 2019.

Central banks ‘buy for an extended period’

Hewitt looks for official-sector buying momentum to continue.

Central banks tend to put a lot of thought into decisions to buy –

with a long, rigorous policy-making process — and purchase the metal

for strategic reasons, rather than simply reacting to day-to-day moves

in the price, Hewitt said.

“Once these people start buying, they continue to buy for an extended

period of time,†Hewitt said. For instance, he pointed out that

Kazakhstan has been a regular gold buyer since 2010.

“Both trade tensions and negative yields are still here,†Hewitt

said. “They may rear their ugly heads again and become more pronounced,

or they may fade away and become less pronounced. But those underlying

forces will remain ever present in the market. Certainly in the next

year or so, those two factors should continue to support and underpin

central-bank demand for gold.â€

Observers pointed out that not only have central-bank gold purchases

been strong, but sales have been light. Back in 1999, when European

central banks were selling the metal, they began following central-bank

sales agreements to try to limit how much was sold in any one year and

thereby keep this from being a destabilizing force in the gold market.

These agreements have been discontinued, Hewitt noted. Commerzbank

analysts pointed out they were no longer necessary since hardly any

European central banks are selling anyway. Germany’s central bank sells a

modest amount each year only for its coin-minting program, Hewitt said.

“The market was not bothered by the central-bank gold agreement

coming to an end, partly because the gold market is very different from

what it was in 1999,†Hewitt said, adding that there “dramatic sellingâ€

back then.

“The gold market today is just more diverse, more resilient and more

liquid. That’s why the market just shrugged its shoulder when the

central-bank gold agreement came to an end.â€

Further, analysts at Commerzbank, in their 2020 outlook, commented

that one or more Western European central banks might even enter the

market as a gold buyer.

“One possible candidate is the Dutch central bank (DNB), which in

October published a remarkable statement about the role of gold on its

website,†Commerzbank said. “In it, it described gold as an anchor of

trust for the financial system. According to the DNB, gold reserves

could serve as the basis for a new beginning in the event of a system

collapse.

“If one or more Western central banks indeed started to actively buy

gold, this would attract considerable attention and spark market

reactions.â€

Posted by AGORACOM

at 4:19 PM on Thursday, December 12th, 2019

SPONSOR: Labrador Gold – Two successful gold explorers lead the way in the Labrador gold rush targeting the under-explored gold potential of the province. Exploration has already outlined district scale gold on two projects, including a 40km strike length of the Florence Lake greenstone belt, one of two greenstone belts covered by the Hopedale Project. Click Here for More Info

Completed gold acquisitions have reached about $33 billion so far in 2019, the highest since 2011

A torrent of deal-making among gold producers that’s pushed M&A in the sector to an eight-year high is seen spilling over into the wider mining industry — if there’s a rally in global growth.

Pending and completed gold acquisitions have reached about

$33 billion so far in 2019, the highest since 2011, according to data complied

by Bloomberg. That’s as deals among all mining companies have declined about

29% from last year to $60-billion, the data show.

A revival in the economic outlook, with higher interest

rates and inflation, would prompt other metals producers to rethink their

current strategy of cutting debt and lifting shareholder returns — and focus

again on pursuing growth, according to Christopher LaFemina, a New

York-based analyst at Jefferies.

“Until now, the market has rewarded companies for austerityâ€

amid a chase for yield, LaFemina said in a phone interview. “We will see a

significant acceleration of M&A activity when global growth recovers.â€

In recent times, the biggest miners, including Rio Tinto and

BHP, have made only some small investments in undeveloped projects and

authorized new spending on expansions at existing operations.

Larger-scale M&A could be an option for Rio next year,

UBS Group analysts, including Glyn Lawcock, said in a report this month.

“Will 2020 see the shackles come off? Growth in the portfolio is limited,†they

said.

Rio has a “watching brief for attractive M&A

opportunities,†though intends to remain “absolutely disciplined,†CEO Jean-Sebastien

Jacques told investors at an October seminar. The company has said its

ventures team is evaluating opportunities in battery materials, including in

nickel. There would be “plenty of logic†for Rio in adding copper producer

First Quantum Minerals, according to Barclays.

BHP is also seeking to add oil, copper and nickel, and could

consider deals that offer an early entry into high-quality resource bases,

particularly before the value of a project is fully understood, CFO Peter

Beaven said in May.

Still, large companies and their investors continue to be

chastened by past failed deals, according to Paul Mitchell, EY’s global mining

and metals leader, and they remain cautious after a multi-year effort to repair

balance sheets in the wake of the 2015 price collapse.

Sectors such as base metals have fewer opportunities for

consolidation than precious metals, and a price downturn hasn’t yet forced

companies into distress, according to David Harquail, chief executive officer

at Franco-Nevada Corp., a mine streaming and royalty company.

Since January’s $10-billion gold mega-merger between then

Newmont Mining and Goldcorp, companies in the sector including Newcrest Mining

have added individual mines, while Kirkland Lake Gold and Zijin Mining Group

acquired smaller rivals. Barrick Gold and a partner on Tuesday agreed to a $430

million deal to sell a 90% stake in a project in Senegal to with Teranga Gold.

Gold’s rally means there’s been “a slightly improved

environment to be able to finally do transactions,†Harquail said. There’s a

prospect of further activity among gold producers into next year, with

investors ready to back proposals that reduce overheads and combine assets, he

said.

“I want to see smart consolidation, not the same thing that

we’ve seen in the past†among gold producers, said Joe Foster, a New York-based

portfolio manager at Van Eck. “There’s value to be created by consolidating

some of these single-asset companies.â€

Posted by AGORACOM

at 3:06 PM on Thursday, December 12th, 2019

Ken Konkin Discusses the Goldstorm Deposit at Treaty Creek (including recent outstanding drill results like 0.725 g/t over 838.5m), it’s Potential, and 2020 Development Plans

American

Creek is a Canadian junior mineral exploration company with a strong

portfolio of gold and silver properties in British Columbia.

Three

of those properties are located in the prolific “Golden Triangleâ€; the

Treaty Creek and Electrum joint venture projects with Tudor Gold/Walter

Storm as well as the 100% owned past producing Dunwell Mine.

The

Treaty Creek Project is a Joint Venture with Tudor Gold owning 60% and

acting as operator. American Creek and Teuton Resources each have 20%

interests in the project. American Creek and Teuton are both fully

carried until such time as a Production Notice is issued, at which time

they are required to contribute their respective 20% share of

development costs. Until such time, Tudor is required to fund all

exploration and development costs while both American Creek and Teuton

have “free ridesâ€.

The Corporation also holds the Gold Hill, Austruck-Bonanza, Ample Goldmax, Silver Side, and Glitter King properties located in other prospective areas of the province.

For further information please contact Kelvin Burton at: Phone: 403 752-4040 or Email: [email protected]. Information relating to the Corporation is available on its website at www.americancreek.com.

Hub on Agoracom FULL DISCLOSURE: American Creek is an advertising client of AGORA Internet Relations Corp.