Posted by AGORACOM

at 5:56 PM on Monday, October 28th, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

BENGALURU — Fragile global growth and the prospect of interest rates

staying lower for longer, boosting gold’s appeal for nervous investors,

are behind upward revisions to price forecasts for the yellow metal, a

Reuters survey showed.

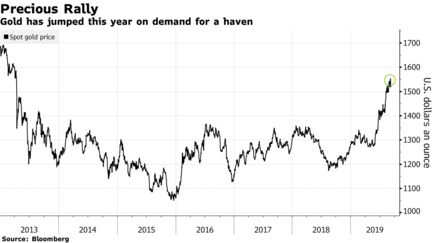

Spot gold will average $1,402 an ounce in

2019 and $1,537 an ounce next year, according to the median forecasts

returned by the poll of 40 analysts and traders in mid-October.

Those

numbers are sharply higher than predictions of $1,351 for 2019 and

$1,433 for 2020 returned by a similar poll conducted three months ago.

Gold has averaged around $1,375 an ounce so far this year.

Gold –

traditionally seen as a safe place to invest in uncertain times – hit a

more than six-year high of $1,557 in September and with gains of about

17% so far is set for its biggest yearly gain since 2010.

“Rate

cuts by major central banks, a deteriorating global economic outlook and

elevated geopolitical tensions are the key tailwinds for gold prices,â€

ANZ analyst Daniel Hynes said.

A U.S.-China trade war has sent a shiver through the global economy.

The U.S. Federal Reserve has meanwhile cut interest rates twice this

year to stimulate growth, and other major central banks have followed

suit.

Lower rates reduce the opportunity cost of holding non-yielding bullion, making it more attractive to investors.

Central

banks have also steadily increased their gold reserves and private cash

has flooded into gold-backed exchange traded funds (ETFs), boosting

physical demand.

“If central banks and exchange-traded funds keep

on buying and the Fed continues with lowering interest rates, we will

talk about prices of $1,600 in the near future,†said LBBW analyst Frank

Schallenberger.

For silver, poll respondents forecast average

prices of $16.24 an ounce this year and $18.13 in 2020, up from

predictions of $15.50 and $16.85 three months ago. In the year to date

it has averaged $15.97 an ounce.

Silver will remain cheap

relative to gold, with the gold/silver ratio averaging 86 in 2019 and 85

in 2020, not far from a more than two-decade high just above 93 reached

in July.

Silver in September breached the $19 mark for the first

time since 2016. It tends to move with gold, but around half of

consumption comes from industry, and weaker economic growth would drag

on demand and, potentially, prices.

Gold and silver prices have

dipped in recent weeks as signs of progress in trade talks revived

appetite for riskier assets. If reached, a trade deal could boost

economic growth and hurt gold and silver, said ETF Securities analyst

Nitesh Shah.

Speculative bets on price rises for gold on the COMEX

exchange have eased slightly from record highs in September, while

those for silver have also dipped from a near two-year peak in July. .

High prices have also dampened demand in Asia, the biggest gold-consuming region.

“The

main negative factors (for gold) are the speculative overhang in the

futures market and the lackluster demand from physical buyers in India,

to some extent in China and amongst Western coin and bar purchasers,â€

said Ross Norman, an independent analyst.

“Gold is due a period of consolidation and perhaps even a temporary correction,†he said.

Posted by AGORACOM

at 4:48 PM on Tuesday, October 22nd, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

Fears of a Trans-Atlantic trade war have increased gold’s safety bid.

U.S. economic data also continues to attract safety seekers to gold.

All signs point to a continuation of the metal’s bull market in Q4.

After a brief respite last month, fear and uncertainty have returned

with a vengeance in October. Recent world events have given investors

plenty of reasons to fear an expansion of the global trade war.

Meanwhile on the domestic front, investors are becoming increasingly

alarmed by soft economic data which some interpret as a harbinger of

recession. Gold’s “fear factor†has thus been resuscitated, bringing

with it the promise of stronger prices in the months ahead. Here we’ll

discuss the growing number of variables which suggest gold is

consolidating its recent gains ahead of the next stage of its long-term

bull market.

One sign of a market controlled by the bulls is the steadfast refusal

of prices, following a correction, to stay down for long. Bull markets

have a tendency to consolidate gains achieved during extended rallies in

the form of a lateral trading range, or sideways drift. That appears to

be the form of gold’s most recent correction in September following a

productive three-month rally.

Although gold prices briefly violated a key short-term trend line

earlier this week, the bulls fought back fiercely and pushed prices back

above the widely, followed 50-day moving average within two days of the

violation. It may take several more days for gold to regain enough

strength and build the support necessary to stay above the 50-day MA.

But the signs are plainly evident that the bulls are clawing their way

back to controlling gold’s immediate-term (1-4 week) trend.

And while gold prices haven’t kept pace with its nearest competitor

in the rush to safety – namely U.S. Treasury bonds – it’s instructive

that gold has so far responded favorably to most of the latest negative

economic and political news. For instance, gold jumped nearly 1.5% on

Oct. 2 after the release of the latest ADP National Employment Report.

The report showed that private payroll growth by U.S. employers slowed

in September and wasn’t as strong in August as previously estimated,

according to a Reuters article. Reuters reporter Lucia Mutikani, capturing the sentiment which has overtaken many gold investors, observed:

The longest economic expansion on record, now in its 11th year, is

losing ground with the blame largely put on a 15-month trade war between

the United States and China, which has eroded business confidence.â€

It’s further believed by many investors that the growing signs of a

slowing U.S. economy could influence the Federal Reserve to further

lower its benchmark interest rate this fall. Lower rates are widely

regarded as bullish for gold since it reduces the competition vs.

interest-bearing assets for the non-yielding metal.

Elsewhere on the U.S. economic front, the recent disappointments in

the Purchasing Managers’ Index (PMI) is another reason for the revival

of gold’s fear factor. The PMI has now fallen for seven consecutive

months and is below 50.0, which indicates contraction in the manufacturing sector.

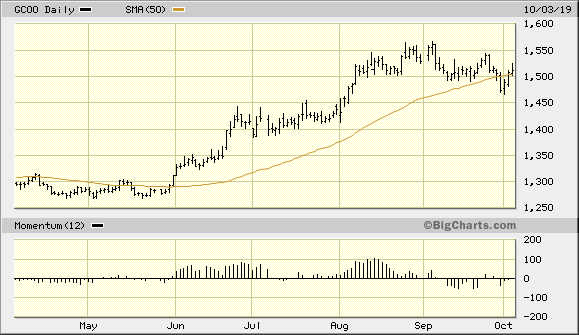

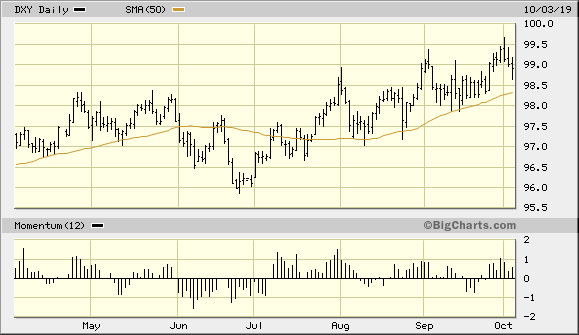

The latest disappointing PMI readings also have weighed heavily on

the U.S. dollar index (DXY) of late. The dollar fell to one-week lows

against the euro and yen on Oct. 3. However, the dollar index is still

close to a multi-year high, which means that gold doesn’t yet enjoy

support from its currency component (see chart below). Nonetheless, gold

has proven to be stalwart enough this year under the influence of the

fear factor alone and in spite of a strong dollar. Thus, a weaker dollar

isn’t necessarily a prerequisite for a Q4 gold rally.

Aside from a weakening manufacturing sector, the U.S. service sector

also is showing signs of slowing. The latest ISM survey released on Oct.

3 showed service-sector activity for September fell to its lowest level

in three years. Some analysts blamed the U.S.-China trade dispute for

the slowdown. The latest ISM Non-Manufacturing Index fell to 52.6 last

month as new orders fell more than expected. This disappointed

economists’ expectations of 55.3. This increased gold’s allure as a safe

haven in the eyes of many investors and should provide some underlying

support for the metal going forward.

In yet another development which bolsters gold’s safety bid, the U.S.

won approval on Oct. 2 from the World Trade Organization to levy

tariffs on $7.5 billion worth of European goods. The WTO’s decision

relates to illegal subsided given to Airbus (EASDF) and Boeing (NYSE:BA). Consequently, many investors fear the outbreak of yet another front in the ongoing global trade war.

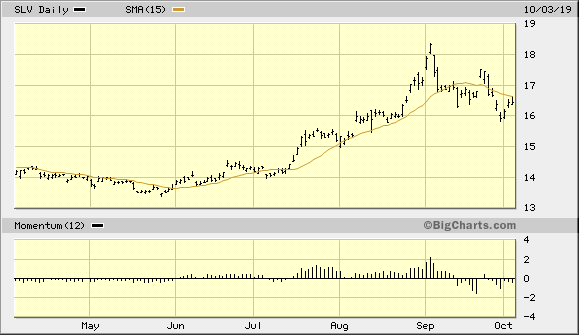

In view of the above-mentioned factors, gold’s intermediate-term (3-6

month) upward trend looks secure. The only thing standing in the way of

a renewed immediate-term gold buy signal, however, is confirming

strength in gold’s sister metal. Silver remains below its 15-day moving

average, as can be seen in the iShares Silver Trust (ETF) below. As I

mentioned in a previous report, we need to see silver confirm gold’s

returning strength before we get a confirmed re-entry signal. A lack of

confirmation from silver normally means that gold’s rally will fail due

to the lack of institutional demand. Historically, when market-moving

institutional investors are bullish enough to buy gold, they usually buy

silver as an adjunct.

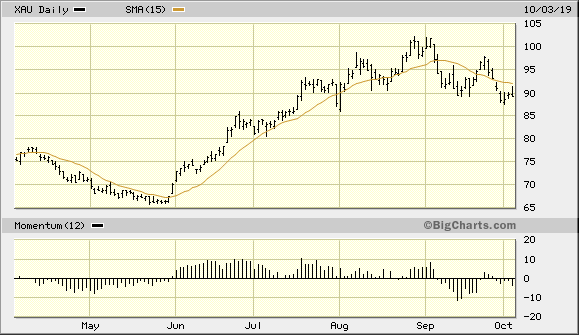

Another sign that should accompany gold’s next confirmed breakout is a

return to strength in the actively traded U.S. mining shares. Shown

below is the PHLX Gold/Silver Index (XAU), which remains below its

15-day moving average as of Oct. 3. To get a renewed buy signal for gold

stocks in the aggregate, we should see a two-day higher close above the

15-day in the XAU. Moreover, a gold stock rally tends to accompany a

rally in bullion prices due to the leverage factor of the miners, which

attracts precious metals investors.

In summary, a growing number of worries on the U.S. economic and

global trade fronts has provided gold with a renewed safety bid. The

evidence reviewed here suggests that gold prices are consolidating ahead

of another breakout attempt this fall. Confirming strength in the

silver price would increase gold’s bullish prospects in Q4, as would a

breakout in the leading gold mining stocks. With trade war threats on

the rise, however, gold is poised to benefit from safe-haven demand and

keep its bull market intact. Investors are therefore justified in

maintaining longer-term investment positions in the yellow metal.

On a strategic note, I’m waiting for both the gold price and the gold

mining stocks to confirm a breakout before initiating a new trading

position in the VanEck Vectors Gold Miners ETF (GDX), my preferred trading vehicle for the mining stocks. I’m currently in a cash position in my short-term trading portfolio

Posted by AGORACOM

at 2:55 PM on Thursday, October 17th, 2019

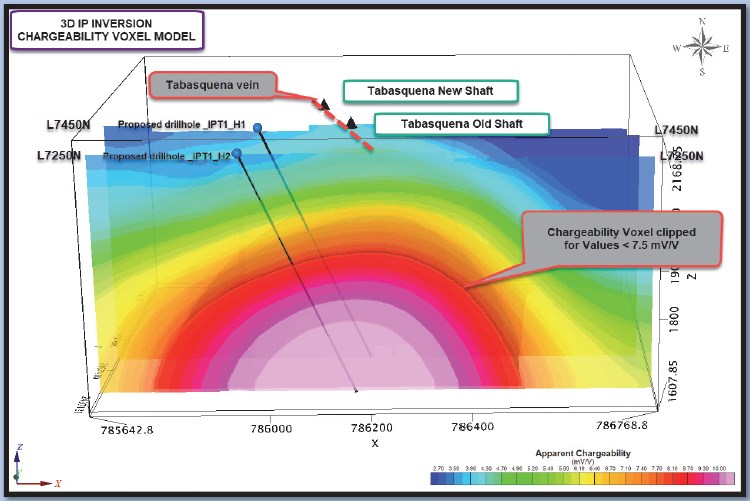

A 3D Induced Polarization (IP) geophysical survey on its Tabasquena project in Zacatecas, Mexico has outlined a significant continuous chargeability anomaly.

This anomaly has an east-west width of approximately 250 metres and an apparent strike length of over 800 metres.

2nd planned IP surgery to extend the grid approximately 1000 metres to the south where due to the elevation change the anomaly is closest to surface.

The anomaly remains open to the north and to the south and at depth.

Drilling to commence once the IP survey has been completed.

The chargeability anomaly is approximately 250 metres below historical mining and was designed for 500 to 550 metres of vertical depth investigation.

The IP data also clearly shows that the large polarisable body/target is apparently quickly deepening northward and getting closer to surface southward. The IP anomaly starts at around 100 metres below the past drill hole intersections that contained widespread gold and silver mineralization in epithermal veins.

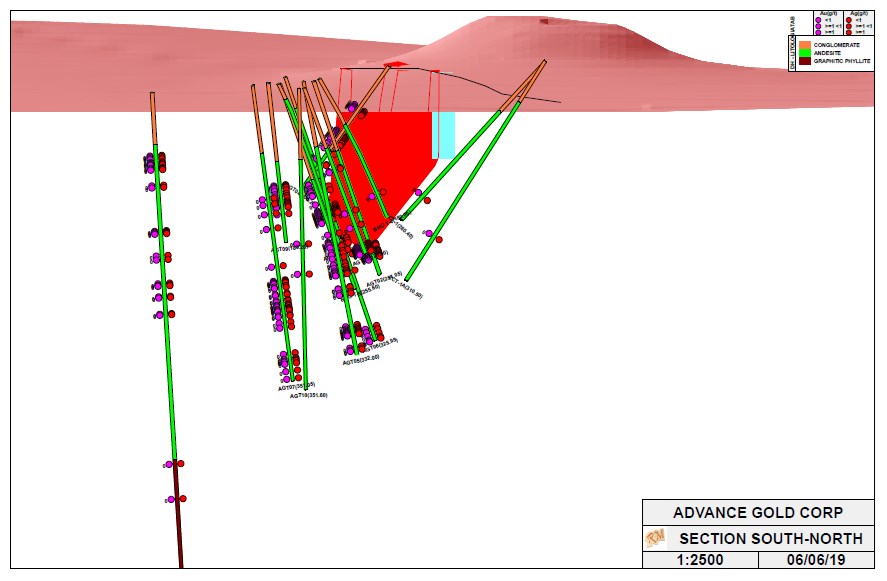

Tabasquena

Previous drilling found a network of veins with widespread gold and silver mineralization.

The first phase geophysical survey revealed a large chargeability anomaly right below these veins and is getting nearer to the surface as it trends south.

Geophysical advisor described the anomaly as ‘quite remarkable in its size and continuity.

Advance is in a region with very large mines, including the El Coronel open pit, 12 miles to the south of Tabasquena.

Posted by AGORACOM

at 1:52 PM on Thursday, October 3rd, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

Recession fears are once again gripping financial markets and

pushing gold prices higher as sentiment within the U.S. service sector

fell more than expected, according to the latest data from the

Institute for Supply Management (ISM).

Thursday, the ISM said its nonmanufacturing index showed a reading

of 52.6% for September, down from August’s reading of 56.4%. The data

was much weaker than expected as consensus forecasts were calling for a

reading of 55.1%.

According to reports this is the lowest reading in three years.

Readings above 50% in such diffusion indexes are seen as a sign of

economic growth, and vice-versa. The farther an indicator is above or

below 50%, the greater or smaller the rate of change.

Ahead of the report, the gold market was holding its own above

$1,500 an ounce, recovering from a 2% selloff at the start of the week.

The latest economic data has added to gold’s gains. December gold

futures last traded at $1,518.80 an ounce, up 0.72% on the day.

Economists and analysts warned that disappointing service sector

data could boost recession fears as this is the largest component of

the U.S. economy.

The nonmanufacturing data comes just two days after the ISM said

that its manufacturing index fell even further into contraction

territory, also missing economist expectations.

“The non-manufacturing sector pulled back after reflecting strong

growth in August. The respondents are mostly concerned about tariffs,

labor resources and the direction of the economy,†said Anthony Nieves,

chair of the ISM Non-Manufacturing Business Survey Committee.

Looking at the components of the report, the Business Activity Index

dropped to a reading of 55.2%, down from August’s level of 61.5%.

The labor market also lost some momentum in September, with the

Employment Index falling to 50.4%, down from August’s level of 53.1%.

This indicator is closely watched by economists as it is used as a

predictor for Friday’s nonfarm employment report.

Some economists have noted that the miss in the ISM employment data points to downside risk to Friday’s employment report.

Posted by AGORACOM

at 9:19 AM on Wednesday, September 18th, 2019

Kamloops, British Columbia–(Newsfile Corp. – September 18, 2019) –

Advance Gold Corp. (TSXV: AAX) (“Advance Gold” or “the Company”) is

pleased to provide an exploration update on its Tabasquena gold and

silver project in Zacatecas, Mexico. To date, 10 drill holes have been

completed hitting widespread gold and silver mineralization in near

surface epithermal veins. Recently, a 3D induced polarization (IP)

survey was completed that identified a significant continuous

chargeability anomaly, with an east-west width of approximately 250

metres and an apparent strike length of over 800 metres. This anomaly is

located directly below the Tabasquena vein. The anomaly remains open

to the north and to the south and at depth. A second phase 3D IP

geophysical survey is scheduled to begin in the first week of October to

extend the grid to the south.

The purpose of the extended grid to

the south will be threefold, firstly it will establish the continuity

of the anomaly to the south, secondly whether or not the target anomaly

becomes shallower and lastly it will assist in positioning the upcoming

drill hole locations. It is planned to commence drilling once the IP

survey has been completed.

Images shown below are a 3D model of

the epithermal veins hit in previous drilling and a voxel inversion

model showing the extent of the large chargeability anomaly for lines

L7450N and L7250N. These two diagrams are an excellent representation of

the emerging targets at Tabasquena.

The black line at the surface

of the 3D model of drill holes is the surface projection of the

Tabasquena vein. The red shaded area is the historical mining done by

Penoles. The chargeability anomaly is approximately 250 metres below the

historical mining, and it follows the strike direction of the

Tabasquena vein. The epithermal veins, with highlighted widespread gold

and silver mineralization, are above and slightly to the west of the

deeper chargeability anomaly.

Allan Barry Laboucan, President and CEO of Advance Gold Corp., commented: “Our

exploration efforts at Tabasquena are coming together nicely with the

past drilling and the recent IP geophysical survey. It is important to

point out, the IP survey is meant to reveal sulphides through

chargeability. The epithermal veins are low sulphidation and relatively

small and don’t show up well in the IP survey, however right below these

veins is the large continuous chargeability anomaly of over 800 metres

from north to south and approximately 250 metres from east to west.

Before starting our next round of drilling, we wanted to extend the IP

grid to the south, where the anomaly is closer to surface. There is a

significant elevation change of approximately 300 metres from the

northernmost line of the geophysical survey to the most southerly one.

We have approximately 1500 metres to the southern limits of our claims.

The chargeability anomaly is open to the north, but due to the higher

elevation and more cover it exceeds the depth limits of the IP survey.

We are very excited to extend the grid to the south as that is the

direction of the highest intensity of the chargeability and where it

becomes closest to surface. The combination of the quality of Tabasquena

and our various projects, our low share count and a tight share

structure, with substantial insider ownership and tiny valuation, puts

us in a unique position relative to our exploration focused peers as the

market for gold and silver are gaining strength.”

Julio Pinto

Linares is a QP, Doctor in Geological Sciences with specialty in

Economic Geology and Qualified Professional No. 01365 by MMSA., and QP

for Advance Gold and is the qualified person as defined by National

Instrument 43-101 and he has read and approved the accuracy of technical

information contained in this news release.

About Advance Gold Corp. (AAX.V)

Advance

Gold is a TSX-V listed junior exploration company focused on acquiring

and exploring mineral properties containing precious metals. The Company

acquired a 100% interest in the Tabasquena Silver Mine in Zacatecas,

Mexico in 2017, and the Venaditas project, also in Zacatecas state, in

April, 2018.

The Tabasquena project is located near the Milagros

silver mine near the city of Ojocaliente, Mexico. Benefits at Tabasquena

include road access to the claims, power to the claims, a 100-metre

underground shaft and underground workings, plus it is a fully permitted

mine.

Venaditas is well located adjacent to Teck’s San Nicolas

mine, a VMS deposit, and it is approximately 11km to the east of the

Tabasquena project, along a paved road.

In addition, Advance Gold

holds a 13.23% interest on strategic claims in the Liranda Corridor in

Kenya, East Africa. The remaining 86.77% of the Kakamega project is held

by Barrick Gold Corporation.

Posted by AGORACOM

at 2:11 PM on Thursday, September 12th, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

Diversify Well To Protect Oneself Against The Coming ‘Paradigm Shift’

The most important forces that now exist are:

1) The End of the Long-Term Debt Cycle (When Central Banks Are No Longer Effective) +

2) The Large Wealth Gap and Political Polarity +

3) A Rising World Power Challenging an Existing World Power = The Bond Blow-Off, Rising Gold Prices, and the Late 1930s Analogue

In other words now 1) central banks have limited ability to stimulate, 2) there is large wealth and political polarity and 3) there is a conflict between China as a rising power and the US as an existing world power.

If/when

there is an economic downturn, that will produce serious problems in

ways that are analogous to the ways that the confluence of those three

influences produced serious problems in the late 1930s.

Before I get into the meat of what I hope to convey, I will repeat my

simple timeless and universal template for understanding and

anticipating what is happening in the economy and markets.

My Template

There are four important influences that drive economies and markets:

Productivity

The short-term debt/business cycle

The long-term debt cycle

Politics (within countries and between countries).

There are three equilibriums:

Debt growth is in line with the income growth required to service the debt,

The economy’s operating rate is neither too high (because that will

produce unacceptable inflation and inefficiencies) nor too low (because

economically depressed levels of activity will produce unacceptable pain

and political changes), and

The projected returns of cash are below the projected returns of

bonds, which are below the projected returns of equities and the

projected returns of other “risky assets.â€

And there are two levers that the government has to try to bring things into equilibrium:

Monetary policy

Fiscal policy

The equilibriums move around in relation to each other to produce

changes in each like a perpetual motion machine, simultaneously trying

to find their equilibrium level. When there are big deviations from one

or more of the equilibriums, the forces and policy levers react in ways

that one can pretty much expect in order to move them toward their

equilibriums.

For example, when growth and inflation fall to lower than the desired

equilibrium levels, central banks will ease monetary policies which

lowers the short-term interest rate relative to expected bond returns,

expected returns on equities, and expected inflation. Expected bond

returns, equity returns, and inflation themselves change in response to

changes in expected conditions (e.g. if expected growth is falling, bond

yields will fall and stock prices will fall).

These price changes happen until debt and spending growth pick up to

shift growth and inflation back toward inflation. And of course all this

affects politics (because political changes will happen if the

equilibriums get too far out of line), which affects fiscal and monetary

policy. More simply and most importantly said, the central bank has the

stimulant which can be injected or withdrawn and cause these things to

change most quickly.

Fiscal policy, which changes taxes and spending in politically

motivated ways, can also be changed to be more stimulative or less

stimulative in response to what is needed but that happens in lagging

and highly inefficient ways.

For a simpler explanation of this template see my 30-minute animated video “How the Economic Machine Works†and for a more comprehensive explanation see my book Understanding the Principles of Big Debt Crises, which is available free as a PDF here or in print on Amazon. Also, to learn more about our extensive debt cycle research, please visit our debt crises research library on Bridgewater.com.

Looking at What Is Happening Now in the Context of That Template

Regarding the above template and where we are now, in my opinion, the most important things that are happening (which last happened in the late 1930s) are

a) we are approaching the ends of both the short-term and long-term

debt cycles in the world’s three major reserve currencies, while

b) the debt and non-debt obligations (e.g. healthcare and

pensions) that are coming at us are larger than the incomes that are

required to fund them,

c) large wealth and political gaps are producing political conflicts

within countries that are characterized by larger and more extreme

levels of internal conflicts between the rich and the poor and between

capitalists and socialists,

d) external politics is driven by the rising of an emerging power

(China) to challenge the existing world power (the US), which is leading

to a more extreme external conflict and will eventually lead to a

change in the world order, and [Ian Bremmer calls this the return of a

bi-polar world but with significant differences in the goals of the

powers—JM]

e) the excess expected returns of bonds is compressing relative to the returns on the cash rates central banks are providing.

As for monetary policy and fiscal policy responses, it seems to me that we

are classically in the late stages of the long-term debt cycle when

central banks’ power to ease in order to reverse an economic downturn is

coming to an end because:

Monetary Policy 1 (i.e. the ability to lower interest rates) doesn’t

work effectively because interest rates get so low that lowering them

enough to stimulate growth doesn’t work well,

Monetary Policy 2 (i.e. printing money and buying financial assets)

doesn’t work well because that doesn’t produce adequate credit in the

real economy (as distinct from credit growth to leverage up investment

assets), so there is “pushing on a string.†That creates the need for…

Monetary Policy 3 (large budget deficits and monetizing of them)

which is problematic especially in this highly politicized and

undisciplined environment.

More specifically, central bank policies will push short-term

and long-term real and nominal interest rates very low and print money

to buy financial assets because they will need to set

short-term interest rates as low as possible due to the large debt and

other obligations (e.g. pensions and healthcare obligations) that are

coming due and because of weakness in the economy and low inflation.

Their hope will be that doing so will drive the expected returns of cash

below the expected returns of bonds, but that won’t work well because:

a) these rates are too close to their floors,

b) there is a weakening in growth and inflation expectations which is also lowering the expected returns of equities,

c) real rates need to go very low because of the large debt and other obligations coming due, and

d) the purchases of financial assets by central banks stays in the

hands of investors rather than trickles down to most of the economy

(which worsens the wealth gap and the populist political responses).

This has happened at a time when investors have become increasingly leveraged long due to the low interest rates and their increased liquidity. As a result we see the market driving down short-term rates while central

banks are also turning more toward long-term interest rate and yield

curve controls, just as they did from the late 1930s through most of the

1940s.

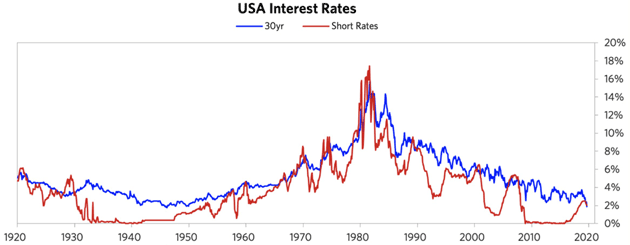

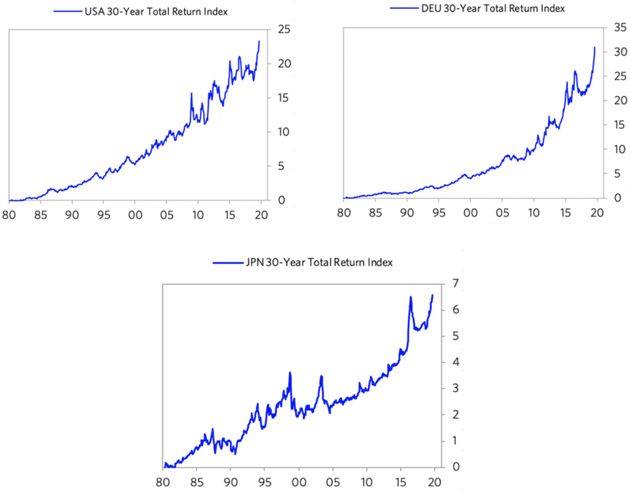

To put this interest rate situation in perspective, see the long-term

debt/interest rate wave in the following chart. As shown below, there

was a big inflationary blow-off that drove interest rates into a

blow-off in 1980–82. During that period, Paul Volcker raised real and

nominal interest rates to what were called the highest levels “since the

birth of Jesus Christ,†which caused the reversal.

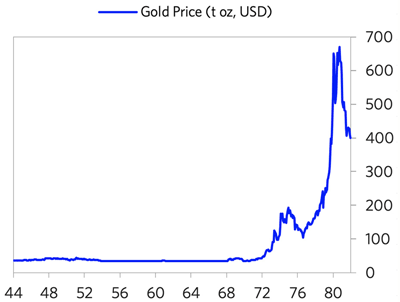

During the period leading into the 1980–82 peak, we saw the blow-off

in gold. The below chart shows the gold price from 1944 (near the end of

the war and the beginning of the Bretton Woods monetary system) into

the 1980–82 period (the end of the inflationary blow-off). Note that the

bull move in gold began in 1971, when the Bretton Woods monetary system

that linked the dollar to gold broke down and was replaced by the

current fiat monetary system. The de-linking of the dollar from gold set

off that big move. During the resulting inflationary/gold

blow-off, there was the big bear move in bonds that reversed with the

extremely tight monetary policies of 1979–82.

Since then, we have had a mirror-like symmetrical reversal (a dis/deflationary blow-off). Look

at the current inflation rates at the current cyclical peaks (i.e. not

much inflation despite the world economy and financial markets being

near a peak and despite all the central banks’ money printing) and

imagine what they will be at the next cyclical lows. That is because there

are strong deflationary forces at work as productive capacity has

increased greatly. These forces are creating the need for extremely

loose monetary policies that are forcing central banks to drive interest

rates to such low levels and will lead to enormous deficits that are

monetized, which is creating the blow-off in bonds that is the

reciprocal of the 1980–82 blow-off in gold. The charts below show the 30-year T-bond returns from that 1980–82 period until now, which highlight the blow-off in bonds.

To understand the current period, I recommend that you understand the

workings of the 1935–45 period closely, which is the last time similar

forces were at work to produce a similar dynamic.

Please understand that I’m not saying that the past is

prologue in an identical way. What I am saying that the basic

cause/effect relationships are analogous:

a) approaching the ends of the short-term and long-term debt cycles, while

b) the internal politics is driven by large wealth and political

gaps, which are producing large internal conflicts between the rich and

the poor and between capitalists and socialists, and

c) the external political conflict that is driven by the rising of an

emerging power to challenge the existing world power, leading to

significant external conflict that eventually leads to a change in the

world order.

As a result, there is a lot to be learned by understanding the mechanics of what happened then (and in other analogous times before then) in order to understand the mechanics of what is happening now.

It is also worth understanding how paradigm shifts work and how to diversify well to protect oneself against them.

by Ray Dalio, Bridgewater Associates, August 28, 2019

Posted by AGORACOM

at 9:45 PM on Tuesday, September 10th, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

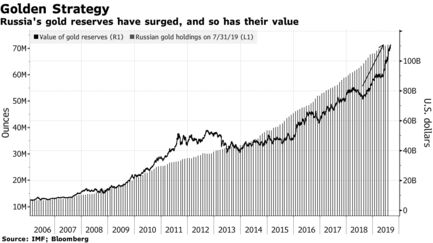

Value of Russia’s gold reserves climbed 42% in the past year

Russia is diversifying from U.S. assets and gold has rallied

Russia’s long-running bet on gold is looking better every month.

The

country quadrupled gold reserves in the past decade as it diversified

away from U.S. assets, a move that has paid off recently as haven demand

sent prices to a six-year high. In the past year, the value of the

nation’s gold jumped 42% to $109.5 billion and the metal now makes up the biggest share of Russia’s total reserves since 2000.

Russia’s central bank has been the largest buyer of gold in

the past few years as President Vladimir Putin seeks to break reliance

on the U.S. dollar as relations between the countries remain strained.

If Russia did need to tap its gold holding, it would fetch a hefty price

— the metal is heading for the best year since 2010 as the U.S.-China

trade war hurts global growth and central banks ease monetary policy.

“Russia

prefers to cushion its macroeconomic stability through politically

neutral tools,†said Vladimir Miklashevsky, a strategist at Danske Bank

A/S in Helsinki. “There is a massive substitution of U.S. dollar assets

by gold — a strategy which has earned billions of dollars for the Bank

of Russia just within several months.â€

More on Russia’s reserves

Russia’s

gold reserves total more than 2,200 tons, the fifth-biggest hoard by

country, and gold now accounts for 20.7% of overall reserves.The value of Russia’s currency reserves are up 9.5% in the past year, lagging the gains seen in bullion.The

central bank bought about 106 tons so far this year, the latest data

show. That’s down 19% from the same period in 2018 but still more than

any other nation.Last year, Russia’s gold buying exceeded its mine supply for the first time.

Russia

isn’t alone in hoarding gold. China, Kazakhstan and Poland have been

among the biggest buyers in the past couple of years, and global

holdings are expected to increase for a while yet.

Not all of Russia’s moves are paying off. Last year, the central bank shifted

about $100 billion of U.S. holdings into euros, yuan and the yen, and

since then the Chinese currency has dropped. Russia also missed out on

the rally in U.S. Treasuries.

Russia may keep buying gold to compensate for those other

losses in its reserves, said Kirill Tremasov, a former Economics

Ministry official and now director of analysis at Loko-Invest in Moscow.

So far it’s working, with gold up 18% this year to $1,513 an ounce.

For

Russia at least, it’s more about diversification than benefiting from

the price. The central bank started buying gold more than a decade ago

as it rallied toward 2011‘s record, and kept adding when prices dropped

in the following few years.

“The central bank is unlikely to have

pursued the goal of earning in the process of managing gold reserves,â€

Dmitry Dolgin, an economist at ING Bank, said by email. “The buying was

rather about diversification of assets

Posted by AGORACOM

at 1:41 PM on Thursday, September 5th, 2019

Kamloops, British Columbia–(Newsfile Corp. – September 5, 2019) –

Advance Gold Corp. (TSXV: AAX) (“Advance Gold” or “the Company”) is

pleased to announce that the recently completed 3D Induced Polarization

(IP) geophysical survey on its Tabasquena project in Zacatecas, Mexico

has outlined a significant continuous chargeability anomaly. This

anomaly has an east-west width of approximately 250 metres and an

apparent strike length of over 800 metres. The anomaly remains open to

the north and to the south and at depth.

The complete geophysical report on this work is available on the

company’s web site. Image below are cross sections representing a key

portion of the overall anomaly.

Allan Barry Laboucan, President and CEO of Advance Gold Corp. commented: “Based

on the size and number of vein intersections in the near surface

drilling in the andesites, our exploration team has felt that we have

found a very large system. The IP survey has now identified such a

possible system. Where the IP anomaly starts is approximately 100 metres

below the past drilling and almost directly under the main Tabasquena

vein. This depth is very important because it is approximately where the

graphitic phyllite horizon begins. The major mines nearby, operated by

Fresnillo Plc., and MAG Silver’s Juanicipio mine currently under

construction, are epithermal veins systems focused on zones within the

graphitic phyllites. We have now established the existence of a large IP

anomaly, below the widespread gold and silver mineralized veins, in the

graphitic phyllite horizon. We are currently making plans to extend the

IP grid to the north and south, and to commence our next drilling

campaign. To put the size of the anomaly into perspective, while taking

into consideration the widespread gold and silver mineralization above

it, it is safe to say that this is the size that all major gold and

silver mining companies would be interested in. It is clear to see that

our small gold and silver exploration company is sitting on a very large

target at a time when the industry is dramatically in need of new gold

and silver discoveries.”

Details of Geophysical Survey

The 3D Induced Polarization survey was carried out by GEOFISICA TMC

SA de CV, between August 3rd and August 14th, 2019. Approximately 9.6

kms of IP data was collected over the central portion of the company’s

claims. The IP grid consisted of nine, east-west lines, 100 metres

apart. Lines were approximately 1 km long. An off-set pole dipole array

was used.

Data processing and inversion of the data was carried out using

RES3DINV software. The inversion model was extended to approximately 550

meters below surface. 3D Voxel images together with a series of depth

slices were generated (all available on the company’s website).

The main purpose of the IP survey was to map, laterally and at depth

the evolution of the known silver veins and to identify new mineralised

structures. The survey was designed in such a way to allow approximately

500 to 550 metres of vertical depth investigation.

The IP survey area encompassed the historic and new shafts that are

located to the east of the Tabasquena and Nina veins that define a

mineralised system that outcrops at surface for 2.0 km. From past

exploration work, the Tabasquena vein was recognized over approximately

70 m along strike near the shaft but only at shallow depth (< 100 m).

The nine (9) vertical sections that were extracted from the 3D IP

inversion voxels suggest the presence of (4) four main stratigraphic

horizons (lithological units) mainly characterized by their resistivity

signatures.

The IP data also clearly shows that the large polarisable body/target

is apparently quickly deepening northward and getting closer to surface

southward. The IP anomaly starts at around 100 metres below the past

drill hole intersections that contained widespread gold and silver

mineralization in epithermal veins.

Chargeability and resistivity anomalies are indicated on the IP

sections (see report on company’s website) and are graded as per their

relative strength. Those chargeability anomalies that are deemed to be

caused by the same anomalous target are grouped together in what is

called a polarisable axis. Only one main axis was delineated following

the review of the IP data, which was labeled IPT-1 (Map C351-3 &

Figure 11, report on company website). This axis is a single large

amplitude continuous anomaly running north-south, coincident with the

two shafts at Tabasquena and the surface projection of the mineralised

veins. This anomaly has been categorized as having a high chargeability

and is conductive. The anomaly has an average depth of approximately 250

to 300 meters. The most southerly line (L7150N) clearly shows that this

anomaly is becoming shallower as one moves to the south. It should also

be mentioned that this anomaly is visible on every line, albeit less

intense on the most northerly line, as the target is becoming deeper to

the north.

In conclusion

This geophysical work has identified a large consistent chargeability

anomaly that can be seen on all lines, implying a strike extent of at

least 800 meters and an apparent width of 250 meters. This observed IP

anomaly could define a much wider mineralised system at depth.

The main recommendation of the geophysical report is to extend the 3D

IP survey to the southeast for at least 1 km in the direction of the

Tesorito shaft, which will determine the southerly extension of the main

anomaly and establish whether this main target is becoming shallower.

Following this a number of proposed boreholes are planned to intersect

this anomaly.

Julio Pinto Linares is a QP, Doctor in Geological Sciences with

specialty in Economic Geology and Qualified Professional No. 01365 by

MMSA., and QP for Advance Gold and is the qualified person as defined by

National Instrument 43-101 and he has read and approved the accuracy of

technical information contained in this news release.

About Advance Gold Corp. (AAX.V)

Advance Gold is a TSX-V listed junior exploration company focused on

acquiring and exploring mineral properties containing precious metals.

The Company acquired a 100% interest in the Tabasquena Silver Mine in

Zacatecas, Mexico in 2017, and the Venaditas project, also in Zacatecas

state, in April, 2018.

The Tabasquena project is located near the Milagros silver mine near

the city of Ojocaliente, Mexico. Benefits at Tabasquena include road

access to the claims, power to the claims, a 100-metre underground shaft

and underground workings, plus it is a fully permitted mine.

Venaditas is well located adjacent to Teck’s San Nicolas mine, a VMS

deposit, and it is approximately 11km to the east of the Tabasquena

project, along a paved road.

In addition, Advance Gold holds a 14.63% interest on strategic claims

in the Liranda Corridor in Kenya, East Africa. The remaining 85.37% of

the Kakamega project is held by Acacia Mining (63% owned by Barrick Gold

Corporation).

Posted by AGORACOM

at 2:38 PM on Tuesday, September 3rd, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

Uncertainties surrounding U.S.-China trade relations and Britain’s departure from the European Union influencing gold price

The dollar climbed to a more than two-year high against other major currencies, making dollar-denominated gold costlier for investors holding other currencies.

Gold prices held steady on Tuesday as

uncertainties surrounding U.S.-China trade relations and Britain’s

departure from the European Union offset pressure from a stronger

dollar.

Spot gold was up 0.1% at $1,532.48 per ounce but still not far off its more than six-year high of $1,554.56. U.S. gold futures were up 0.8% at $1,541.40.

“We are having a battle right now against multiple layers of

uncertainties in the market and a strong dollar,†Saxo Bank commodity

strategist Ole Hansen said.

“The trade talks between U.S. and

China are going nowhere. The political debacle in the UK with Brexit,

where we are potentially facing another vote before the day is over, is

adding enough underlying support to gold to offset the strength in

dollar.â€

The dollar climbed to a more than two-year high against

other major currencies, making dollar-denominated gold costlier for

investors holding other currencies.

On the trade front, China has

lodged a complaint at the World Trade Organization over U.S. import

duties, trashing the latest tariff actions as violating the consensus

reached by leaders of both countries at a meeting in Osaka.

In

Britain, lawmakers will decide on Tuesday whether to move towards a snap

election when they vote on the first stage of their plan to block Prime

Minister Boris Johnson from pursuing a no-deal Brexit.

But

analysts said that fears of a deceleration in global economic growth,

negative yielding debts around the world and hopes for interest rate

cuts by global central banks also provided support for gold.

“Given this week’s economic calendar is jam-packed with crucial economic

releases that will shape monetary policy expectations for the September

18 Federal Open Market Committee meeting, gold traders are trading very

delicately waiting for more convincing U.S. economic signals,†VM

Markets Managing Partner Stephen Innes said in a note.

Investors

are awaiting the U.S. manufacturing survey by the Institute for Supply

Management (ISM), due at 1400 GMT, for some forward guidance on U.S.

economic conditions.

Federal fund futures implied traders saw a 91% chance of a 25 basis point rate cut by the U.S. Federal Reserve this month.

“Rate cut will happen almost no matter what kind of economic data we’re

going to be presented with from now on until the Fed meeting but any

acceleration to the weaker side could increase the expectations of how

big the cut would be,†Saxo Bank’s Hansen said.

Silver rose 0.2% to $18.48 per ounce. Platinum was up 0.9% at $938.34 per ounce, while palladium gained 0.3% to $1,535.79.

Posted by AGORACOM

at 1:19 PM on Monday, August 12th, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining

In Canada, Gold is $100 higher than its (previous) all-time highs.

Gold and Silver Ratio also close to previous highs

{kind=link}

{kind=link}