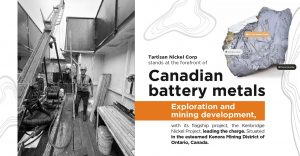

Introduction

With the global energy transition fueling an insatiable demand for battery materials, Tartisan Nickel Corp. is primed to capitalize on this seismic market shift. Nickel, vital for electric vehicle (EV) batteries, is experiencing exponential growth in demand. Positioned strategically, Tartisan Nickel’s advanced projects and ESG-driven operations make it a promising player in the critical minerals sector.

Industry Trends and Market Potential

The adoption of EVs is transforming the nickel market, with battery-grade nickel demand forecasted to grow by 27% annually. By 2030, nickel-based chemistries will dominate global battery markets outside China, claiming over 85% of market share. As supply chains reconfigure to prioritize Western sources, Tartisan Nickel emerges as a critical player, addressing the growing demand for localized, sustainable resources.

Tartisan Nickel’s FLASH Highlights

- Kenbridge Nickel Project: Situated in Ontario, the project holds 7.47 million tonnes of measured and indicated resources, containing 74 million pounds of nickel and 39.1 million pounds of copper, alongside inferred resources of 32.7 million pounds of nickel and 14.9 million pounds of copper.

- Life of Mine Revenues: Projected at $837 million, underscoring robust economic viability.

- Development Milestones: Progressing through feasibility and permitting stages to align with surging market demand.

- Sustainability Commitment: ESG principles guide operations, fostering long-term investor confidence and environmental stewardship.

Strategic Impact and Real-World Relevance

Nickel is to EV batteries what oil was to traditional engines—a cornerstone material driving innovation and adoption. Tartisan’s Kenbridge Project offers a domestic, reliable supply of nickel, reducing dependency on geopolitical uncertainties and paving the way for a stable EV ecosystem.

The Road Ahead

Tartisan Nickel’s forward-thinking approach and market-aligned strategies position it to capture the immense opportunities of the clean energy revolution. As the world accelerates toward a sustainable future, Tartisan’s focus on critical minerals solidifies its role as a leader in the battery-grade nickel market.

Conclusion

The surging demand for nickel presents unparalleled opportunities for innovative companies like Tartisan Nickel. With its advanced projects, sustainable operations, and alignment with market trends, Tartisan is well-positioned to thrive in the energy transition, delivering value to stakeholders and contributing to a cleaner, greener future.

Source: https://carboncredits.com/nickel-demand-to-triple-by-2030-can-the-market-keep-up/

YOUR NEXT STEPS

Visit $TN HUB On AGORACOM: https://agoracom.com/ir/TartisanNickel

Visit $TN 5 Minute Research Profile On AGORACOM: https://agoracom.com/ir/TartisanNickel/profile

Visit $TN Official Verified Discussion Forum On AGORACOM: https://agoracom.com/ir/TartisanNickel/forums/discussion

DISCLAIMER AND DISCLOSURE

This record is published on behalf of the featured company or companies mentioned (Collectively “Clients”), which are paid clients of Agora Internet Relations Corp or AGORACOM Investor Relations Corp. (Collectively “AGORACOM”)

AGORACOM.com is a platform. AGORACOM is an online marketing agency that is compensated by public companies to provide online marketing, branding and awareness through Advertising in the form of content on AGORACOM.com, its related websites (smallcapepicenter.com; smallcappodcast.com; smallcapagora.com) and all of their social media sites (Collectively “AGORACOM Network”) . As such please assume any of the companies mentioned above have paid for the creation, publication and dissemination of this article / post.

You understand that AGORACOM receives either monetary or securities compensation for our services, including creating, publishing and distributing content on behalf of Clients, which includes but is not limited to articles, press releases, videos, interview transcripts, industry bulletins, reports, GIFs, JPEGs, (Collectively “Records”) and other records by or on behalf of clients. Although AGORACOM compensation is not tied to the sale or appreciation of any securities, we stand to benefit from any volume or stock appreciation of our Clients. In exchange for publishing services rendered by AGORACOM on behalf of Clients, AGORACOM receives annual cash and/or securities compensation of typically up to $125,000.

Facts relied upon by AGORACOM are generally provided by clients or gathered by AGORACOM from other public sources including press releases, SEDAR and/or EDGAR filings, website, powerpoint presentations. These facts may be in error and if so, Records created by AGORACOM may be materially different. In our video interviews or video content, opinions are those of our guests or interviewees and do not necessarily reflect the opinion of AGORACOM.

From time to time, reference may be made in our marketing materials to prior Records we have published. These references may be selective, may reference only a portion of an article or recommendation, and are likely not to be current. As markets change continuously, previously published information and data may not be current and should not be relied upon.

NO INVESTMENT ADVICE

This record, and any record we publish by or on behalf of our clients, should not be construed as an offer or solicitation to buy or sell products or securities.

You understand and agree that no content in this record or published by AGORACOM constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable or advisable for any specific person and that no such content is tailored to any specific person’s needs. We will never advise you personally concerning the nature, potential, advisability, value or suitability of any particular security, portfolio of securities, transaction, investment strategy, or other matter.

Neither the writer of this record nor AGORACOM is an investment advisor. Both are neither licensed to provide nor are making any buy or sell recommendations. For more information about this or any other company, please review their public documents to conduct your own due diligence.

If you have any questions, please direct them to [email protected]

For our full website disclaimer, please visit https://agoracom.com/terms-and-conditions