ThreeD Capital Announces Its Artificial Intelligence Investment, GoldSpot Discoveries, Reports Major Milestone At Sprott Mining Majority Owned Jerritt Canyon Project

If You Are Looking For A Small Cap Artificial Intelligence Investment, Consider ThreeD Capital, Led By Sheldon Inwentash. JERRITT CANYON PROJECT – USING ARTIFICIAL INTELLIGENCE TO IDENTIFY THE MOST PROSPECTIVE TARGETS

Took 5 months to accomplish what would have taken years by a team of geologists WATCH EXCLUSIVE AGORACOM VIDEO – BEYOND THE PRESS RELEASE |

Agoracom Blog Home

Archive for the ‘Small-Cap Investor Revolts’ Category

BREAKING – Sprott Mining $SII.ca And Sheldon Inwentash $IDK.ca Bring Artificial Intelligence To #Gold Exploration – MUST WATCH!

Posted by

at 12:18 PM on Friday, September 8th, 2017

BREAKING: SEC Says “YES” To Social Media. AGORACOM Online IR Platform For Investor Relations & Disclosure

Posted by

at 7:09 AM on Wednesday, April 3rd, 2013

This is simply big – and long overdue – Â news out of the SEC last night. Â In 2008, the SEC allowed companies to use their websites to conduct investor relations and make disclosure. Â As of today, companies can now use social media sites to conduct investor relations, including the release of material news, data and information.

WHY IS THIS SO IMPORTANT FOR US SMALL CAP COMPANIES?

1.  Freedom To Communicate And Create Real Conversations With Investors – Until yesterday, small-cap CEO’s couldn’t say a thing about their businesses without consulting lawyers, their board and anybody else in the compliance process.  This made it extremely difficult – actually impossible – for small-cap companies to release any new information via anything but a press release, especially those small but important tidbits of information that didn’t warrant the expense of a press release.

For example, this specific decision arose from an incident that occurred last summer when NetFlix CEO, Reed Hastings, posted to Facebook that NetFlix had exceeded 1 billion hours in a month for the first time. Â It was an important milestone that Hastings wanted investors to know about – but not necessarily something that warranted a press release or SEC filing.

The SEC took exception and opened an investigation in whether or not this violated selective disclosure rules.

However, as a result of this decision, the SEC now agrees that release of such information via social media sites is sufficient. Â The only requirement is that all companies must make it clear to investors that they plan to use a particular social media site (i.e. AGORACOM).

In the case of AGORACOM, all clients issue press releases announcing the launch of their online IR community. Â Until yesterday, those IR communities were used to post press releases and then answer questions from shareholders. NOW, small-cap executives can make a major leap forward by actually posting helpful information and data to help investors better understand their company and progress.

For example, a small-cap executive at a trade show can now go back to their hotel room and post an overview of the day including the number of visitors to their booth, product feedback, etc. Moreover, small cap companies can now provide regular updates on previously announced or brand new initiatives. Â The possibilities are endless. Â The most important thing is such disclosure can now lead to real conversations with investors that extend well beyond big material news.

This is critical for small-cap companies that typically don’t have or can’t afford a plethora of press releases and want to fill the information gaps with shareholders.

2. Â Significant Savings – In the sentence above, I touched on the fact that most small-cap companies simply can’t afford a plethora of press releases. Â As such, they are forced to release only the biggest, most important news, which significantly limited their frequency of communication with investors. Â The only option was to issue more press releases and spend more $$. Â With this new SEC decision, this is no longer an issue.

Moreover, small cap companies were often forced to issue “kitchen sink” press releases because they would piggyback smaller tidbits of information and updates with material press releases. Â I don’t have to tell you how that causes expenses to skyrocket when you are being charged by the word.

3. Â Size Doesn’t Matter – It doesn’t matter if your online shareholder audience is 200,000 or 200. Â As long as you’ve clearly told investors where to look for your information, you’re good to go.

4.  Social Media vs Your Website – Investors simply don’t have time to navigate to every website of companies they’re either invested in, or interested in.  They overwhelmingly prefer financial communities such as AGORACOM, or even non-financial communities such as Twitter where all information is available under one roof.  Thanks to this decision, small-cap companies can now meet investors where they exist, rather than forcing them to visit stand alone websites that rarely change with the exception of new press releases.

CONCLUSION

This is a great day for small-cap companies and investors that want to truly engage in meaningful discussions without having to worry about disclosure rules and expenses. Â To be clear, you are still going to issue important, material press releases by press release.

However, much like the NetFlix example above, it is all those valuable morsels and tidbits of information that can now finally be set free to open the lines of communications with current and prospective investors.

“Great day” is actually an understatement. Â It is more accurate to say this day is monumental, even epic for small-cap investor relations.

To discuss this post and your next investor relations steps, contact me right now.

Regards,

George Tsiolis, Founder

AGOARCOM

Dacha Strategic Metals Says Tye Burt Isn’t Qualified After Losing $2.49 Billion For Kinross Shareholders – AGORACOM Agrees

Posted by

at 10:40 AM on Monday, November 5th, 2012

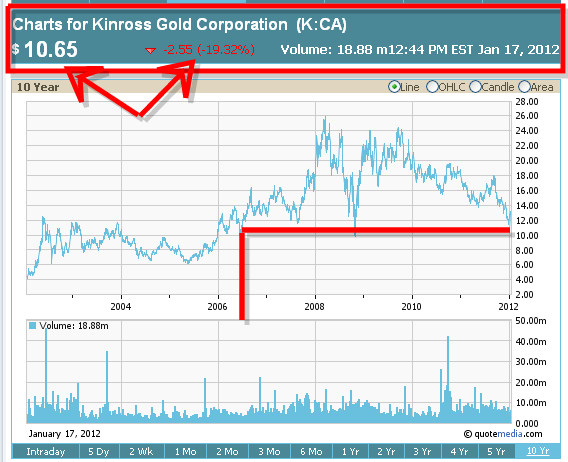

It seems like Tye Burt can’t build a company on his own. Â Rather he prefers to act as an opportunist, as was well documented in our very heated and public battle over the Kinross “take over” of Aurelian Resources. Â Despite the unanimous “approval” of an Aurelian Board that happened to stock up on millions of options just before the Kinross “offer”, the AGORACOM community fought and battled Kinross into renewing their offer several times before obtaining the requisite number of shares … an industry first.

Tye was so confident, that he gave Aurelian investors a warrant to purchase Kinross shares at $32 … when it was trading around $18 … and attached a value to that warrant that made up a good portion of the ridiculous consideration Aurelian shareholders received.  So how did that work out? It never got over $24 and expired worthless:

Now, had Tye taken Aurelian and built an even better company for the benefit of all, you could argue the move was the right one. Â Unfortunately, Tye was such a bad CEO that Kinross tossed him after – and I quote the Dacha press release below:

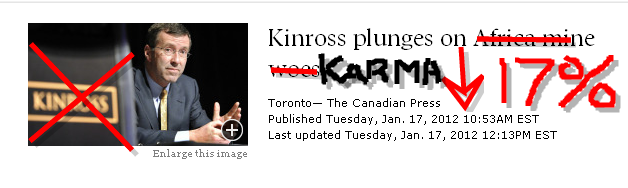

“Mr. Tye W. Burt was terminated as Chief Executive Officer of Kinross Gold Corp. after presiding over a reported US$2.49 billion loss related to the acquisition of Red Back Mining, the largest single loss in the company’s history.”

Here’s a little more imagery to help drive the Dacha point home:

Now, if you didn’t know these facts, you’d have to consider the possibility that Dacha management are simply saying whatever they can to keep their jobs … but now you know better when you read the following Dacha statements below:

Now, if you didn’t know these facts, you’d have to consider the possibility that Dacha management are simply saying whatever they can to keep their jobs … but now you know better when you read the following Dacha statements below:

- DISSIDENT NOMINEES CANNOT BE TRUSTED TO RUN YOUR COMPANY

- DISSIDENT NOMINEES ARE NOT QUALIFIED TO CREATE YOUR SHAREHOLDER VALUE

- DISSIDENT NOMINEES ARE NOT QUALIFIED TO CREATE YOUR SHAREHOLDER VALUE

The most troubling part of the press release below is that the dissident group which proposed him as a board member secretly acquired shares, despite good faith negotiations by Dacha management to agree to a compromise without a battle for the board. Â This comes as no surprise to me.

Dacha shareholders be forewarned, if Tye gets his hands on Dacha by squeezing out this board, you stand to be the next ones to be squeezed out.

Last Friday we were notified that a group of four shareholders is trying to take control of your company and the value of your investment. The group, which includes funds managed by Goodwood Inc. (“Goodwoodâ€) and Salida Capital L.P. (“Salidaâ€), seeks to replace the entire Dacha board with eight connected nominees at the annual and special meeting of Dacha shareholders, to be held on November 28, 2012. In addition to Goodwood and Salida, the group also includes Takota Asset Management Inc. and Longford Energy Inc. Their actions have launched a costly and distracting proxy contest to advance their own agenda rather than the best interests of the majority of Dacha’s shareholders or Dacha.

Your board opposes this initiative for the reasons detailed in this Circular. Join us in voting the BLUE Proxy to stop Goodwood and Salida. We believe Goodwood and Salida are attempting a coercive takeover of Dacha and its valuable assets, without paying shareholders the premium they are owed.

DISSIDENT NOMINEES CANNOT BE TRUSTED TO RUN YOUR COMPANY

The rare earth element (REE) business is a highly specialized and complex international market, with no open and transparent exchange supporting REE transactions. The market relies on trusted relationships with professionals who understand the sophisticated chemistry associated with these metals as counterparties contract directly with one another to purchase rare earth elements primarily from specific plants and suppliers who have met stringent pre-qualification. Additionally, the market has high regulatory barriers to entry, with most of its trade being conducted primarily via Chinese state owned enterprises that hold a limited number of export quotas to remove rare earths from the country. Sourcing rare earths in China for inventory is very difficult and requires a combination of chemical expertise, relationships, knowledge and experience that Goodwood, Salida and their director nominees clearly lack.

Your board and management team understands the intricacies of this highly specialized international marketplace and has the proven expertise and experience to maximize shareholder value through investment in REE. Very few individuals in the world can do this type of work and that is the competitive advantage of Dacha’s current management team. Goodwood, Salida and their nominees do not have the experience, expertise or relationships to manage or grow the assets that have been diligently built by Dacha’s highly-experienced management team.

DISSIDENT NOMINEES ARE NOT QUALIFIED TO CREATE YOUR SHAREHOLDER VALUE

Members of the dissident slate have in the past demonstrated self-serving activism, value destruction, and strategic miscues. Unsuccessful investment strategies have left Goodwood and Salida with a limited ability to raise investor funds and with a motivation to instead raid cash rich public companies. We fear that Goodwood, Salida and the other members of the dissident group intend to do the same with Dacha, and seize the value that rightly belongs to our shareholders without paying anything. To advance this goal, Mr. Puccetti, Goodwood’s founder, Chairman and Chief Investment Officer, with the support of Salida, has put forward a slate of connected nominees with no track record in the REE industry, with demonstrated underperformance and who are not necessarily motivated to act in the best interests of the shareholders of Dacha as a whole.

Notably:

Mr. Tye W. Burt was terminated as Chief Executive Officer of Kinross Gold Corp. after presiding over a reported US$2.49 billion loss related to the acquisition of Red Back Mining, the largest single loss in the company’s history.

Mr. Ian W. Delaney has several connections with Goodwood and is reportedly currently barred from entering the United States because of dealings with a dictatorship.

Mr. Peter H. Puccetti is the founder, Chairman and Chief Investment Officer of Goodwood Inc., a Toronto-based hedge fund whose Goodwood Fund A, B, Capital and 2.0 each have negative returns for the three and five year period, underperforming the S&P/TSX composite TRI, which has yielded positive returns for those periods.

Mr. Timothy E. Thorsteinson presided over 97.2% stock price decline as CEO of Enablence Technologies, a former Goodwood portfolio investment.

We do not believe that the members of the dissidents’ slate possess the expertise to lead Dacha into the future and enhance total shareholder value within the dynamic nature of the REE industry.

DISSIDENTS HAVE ACQUIRED SHARES WITHOUT DISCLOSURE

Following a good faith settlement with Goodwood and certain dissident nominees over Longford, Forbes & Manhattan Inc. (“Forbes & Manhattanâ€) was prepared to work constructively with Goodwood for the benefit of all shareholders. Unfortunately, Goodwood put up a false front of cooperation while simultaneously and secretly, along with Salida, acquiring shares of Dacha. Apparently, the dissident group rapidly accumulated a stake of 31.5% without any disclosure of its purchase.

DACHA AND FORBES & MANHATTAN – A TRACK RECORD OF CREATING VALUE

Dacha, a Forbes & Manhattan company, has a history of creating value for shareholders in a volatile market. Dacha has posted a 93% return on sales transactions and a 135% return on investment capital since January 2010, and has done so while aggressively managing SG&A to levels that are comparable with its peers.

Together with Forbes & Manhattan, whose investment model combines industry leading expertise, exceptional capital markets access and the strongest deal flow for resource assets to produce consistently strong returns, Dacha is focused on building on this record to generate incremental value for all shareholders.

Forbes & Manhattan’s active management approach, which mitigates risk through hands-on involvement competitively positions its partner companies through more efficient approaches to general and administrative expenses. Forbes & Manhattan’s strategies significantly decrease costs, such that G&A of those companies are in line with, if not better than, their competitors. The track record shows that by bringing deep, hands-on expertise in geology and mining engineering, capital markets expertise, and by providing portfolio companies with economies of scale, Forbes & Manhattan enables the development of assets that might not have been developed as stand-alone companies with traditional management structures.

YOUR HIGHLY QUALIFIED AND EXPERIENCED MANAGEMENT NOMINEES

Dacha’s highly qualified incumbent director nominees have the necessary skills and knowledge to maximize the rare earth assets that the company currently holds, grow net asset value and drive share price appreciation. In addition, management has nominated for election as a director of Dacha, Mr. Jim Rogers, a commodities investment expert, author and a financial commentator who has been a successful international investor since 1980. Mr. Rogers will be appointed non-executive Chairman following the meeting, replacing Mr. Stan Bharti who will not stand for re-election.

Mr. Rogers has frequently been featured in Time, The Washington Post, The New York Times, Barron’s, Forbes, Fortune, The Wall Street Journal and The Financial Times among others. He has been a regular columnist at WORTH Magazine since 1995, and a regular commentator on CNBC since 1998. Mr. Rogers has written four books on investment, including ‘Investment Biker: On the Road with Jim Rogers’ (1994), ‘Adventure Capitalist: The Ultimate Road Trip’ (2003), ‘Hot Commodities: How Anyone Can Invest Profitably in the World’s Best Market’ (2005) and ‘A Gift to My Children: A Father’s Lessons for Life and Investing’ (2009). Mr. Rogers holds a B.A. in History from Yale University and a B.A. and M.A. in Politics, Economics and Philosophy from Oxford University.

Dacha also plans to nominate Hon. J. Trevor Eyton, David S. Warner and Ken Taylor. The incumbent management nominees are G. Scott Moore, President and Chief Executive Officer; Alastair Neill P.Eng, MBA, Executive Vice President and Director; and General (Ret) Ron Hite, Director.

Dacha encourages shareholders to carefully review its proxy circular and other materials and vote only their BLUE Proxy by no later than Monday, November 26, 2012 at 10:00 a.m. (Toronto time) in advance of the proxy voting deadline. If you have any questions and/or need assistance in voting your shares, please call Kingsdale Shareholder Services at 1-866-229-8263 toll-free in North America, or 1-416-867-2272 outside of North America (collect calls accepted).

Do not let Goodwood and Salida’s representatives take the value that belongs to you! The highly-qualified and experienced Dacha board of directors is completely dedicated to maximizing shareholder value and strengthening the company. We encourage you to vote for management’s nominees and look forward to your support.

“G. Scott Mooreâ€

G. Scott Moore

President and CEO

Dacha Strategic Metals Inc.

About Dacha

Dacha Strategic Metals Inc. is an investment company focused on the acquisition, storage and trading of strategic metals with a primary focus on Rare Earth Elements. Dacha is in the unique position of holding a commercial stockpile of Physical Rare Earth Elements. Its shares are listed on the TSX Venture Exchange under the symbol “DSM” and on the OTCQX exchange under the symbol “DCHAF”.

Except for statements of historical fact relating to the Company, certain information contained herein constitutes “forward-looking information†under Canadian securities legislation. Forward-looking information includes, but is not limited to, statements with respect to the Company’s ability to trade in rare earth elements, the realization value of Dacha’s physical inventory portfolio, proposed investment strategy of the Company, and general investment and market trends. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plansâ€, “expects†or “does not expectâ€, “is expectedâ€, “budgetâ€, “scheduledâ€, “estimatesâ€, “forecastsâ€, “intendsâ€, “anticipates†or “does not anticipateâ€, or “believesâ€, or variations of such words and phrases or statements that certain actions, events or results “mayâ€, “couldâ€, “wouldâ€, “might†or “will be takenâ€, “occur†or “be achievedâ€. Forward-looking statements are based on the opinions and estimates of management as of the date such statements are made. Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Dacha to be materially different from those expressed or implied by such forward-looking information. Although management of Dacha has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking information. Dacha does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

NEITHER THE TSX VENTURE EXCHANGE NOR ITS REGULATION SERVICES PROVIDER (AS THAT TERM IS DEFINED IN THE POLICIES OF THE TSX VENTURE EXCHANGE) ACCEPTS RESPONSIBILITY FOR THE ADEQUACY OR ACCURACY OF THIS RELEASE

The Rise Of Social Media Investor Relations “Experts” a.k.a. Pretenders – Part 2

Posted by

at 4:04 PM on Wednesday, August 3rd, 2011

Back In October of 2010, I posted the story The Rise of Social Media IR “Experts†a.k.a. Pretenders and I used the image below.  It was humorous poke at a very serious subject – Pretenders that are fleecing small-cap companies by promising they can tap into 700 Gazillion people on Facebook, Twitter and every where else (see full story at the end).

Courtesy of Briansolis.com

I used the concept for my keynote speech at IR Conference 2011 where I presented 500 Million Reasons Why Facebook IR Will Kill You (Watch Webcast) to small-cap resource companies – to their great satisfaction.

Well, it seems my good friends (and our fantastic web developers) at The Working Group are running into a similar problem in their industry and have also used humour to convey their caution to customers … so I just had to add it on to this post to drive the point home even further.

Courtesy Of The Working Group

As you all know, I simply love online investor relations. I believe it is the ultimate equalizer for small-cap companies that need affordable and efficient ways to both communicate with current shareholders and find new prospective investors.

I’m proud to say that AGORACOM pioneered online investor relations for small-cap companies by creating a platform that ties both communications and marketing together into one great package. More than just lip service, AGORACOM ranked #57 in the Profit 100 of Canada’s fastest growing companies in 2009. This isn’t meant to show off our success but, rather, to demonstrate how big online investor relations has become – and how big it is going to be.

GREAT ONLINE IR COLLEAGUES

I’m also happy to say that we don’t own the online investor relations space. Otherwise how valuable could the services be if others didn’t find it worthy to participate in? For example, Q4 Websystems, Meet The Street and IR Web Report have done some great things in the space, keep me on my toes and teach me new tactics along the way.

I respect my colleagues for the work they do and for making the space better for everyone.

GREAT ONLINE IR PRETENDERS – A Twitter/Facebook/YouTube Account Is Not An Online IR Program

Unfortunately, we are now starting to see the rise of Online IR Pretenders. They claim to be “leaders” in social media and will set up a Twitter/Facebook/YouTube account to prove it.

If it were only that easy.

Setting up some social media accounts mean nothing unless they come with traffic and visibility. Any 16-year old kid can create flashy looking social media accounts for you in under an hour and bolt on some basic advertising to it.  This is why social media pretenders are so cheap. Unfortunately, social media pages do not make an online investor relations program, no matter how cheap the pitch.

Said another way, you’re better off saving the $10,000 you’d spend on a Yugo and putting it towards a $40,000 Maxima.

Without a real vehicle, all you have is a puttering online IR program.

A REAL AUDIENCE VS. A PRETENDERS AUDIENCE

Social Media IR Pretenders don’t have an audience – they simply talk about the blue sky audience. Hell, if a traditional IR firm pitched you by saying “there are 6 Billion people on this planet”, would you get excited and hire them? Think about it.

Here Is What A Pretender Audience Looks Like

- Facebook Has 500 Million Members

- Twitter Has 165 Million Users

- YouTube Has 1 Zillion people watching 10 Zillion videos every day

- Everybody in the world has a mobile phone

- …. etc., etc.

This may all be true – but it doesn’t mean any of them are going to run to your social media pages. Getting their attention is hard. Very hard. It takes time … years even …. to build credibility and content that drives a small fraction of these people to you.

Here Is What A Real Audience Looks Like:

- 1.1 Million Investors Hit AGORACOM Annually (Average 2008 – 2010)

- They Visit 7.4 Million Times Annually (Average 2008 – 2010)

- The Read 75 Million Pages Of Small Cap Information (Average 2008 – 2010)

- AGORACOM Reports 17,792 Investors From 77 Countries Participated In Online Gold and Commodities Conference

- Mobile Devices Drive 16,000 Small-Cap Visits To AGORACOM In August

- AGORACOM Videos Viewed Over 250,000 Times

- …. you get the idea

CONCLUSION

Next time a Social Media IR “Expert” comes knocking on your door – ask them how much traffic they’re actually pulling into their sites. If they start talking about blue sky, show them the door.

Century Mining Members Commence 3rd Small-Cap Shareholder Revolt Via AGORACOM

Posted by

at 9:15 AM on Tuesday, April 19th, 2011

I am very proud to announce that members of AGORACOM have once again used the power of the web to launch yet another small-cap shareholder revolt against an unfair acquisition of their company. The Century Mining Corporation Concerned Shareholders issued this press release yesterday to officially “Question The Business Combination With White Tiger Gold Ltd.”

This is a well written, well reasoned press release that provides the market with succinct facts behind the revolt. I highly recommend reading it. Moreover, if you are a small-cap resource investor, you need to support this campaign and send a clear signal that predatory takeovers of your companies is a thing of the past.

SMALL CAP SHAREHOLDERS WON’T BE PUSHED AROUND ANYMORE

On September 7th 2007, I posted a story on this blog titled “The Empowerment Of Online Investors – It’s Here For Good”. In that story, I stated the following:

“What does this mean for small-cap and micro-cap CEO’s?

Online investors have almost as much power as you do when it comes to the future

of your company. Unhappy investors are no longer relegated to the vacuum of “harsh”

e-mail and letters to express their discontent. Today, investors can rally in short order

via video, blogs and online forums to challenge you at your next AGM, oust you from

your position or even elect their own slate of directors.In fact, not only is this possible, I’ll go as far as predict it will actually happen in the

next 12-24 months as investors make Web 2.0 a part of their daily investing lives.

I’m the biggest proponent of great small-cap and micro-companies but we all know

there are still many companies out there deserving of being the first target of an online

shareholder revolt – and I’ll be the first to applaud it.”

Within months we saw shareholders of Aurelian Resources and then Noront Resources rise up and fight against an unfair “friendly takeover” / predatory proposed changes to control of its board respectively. They went 1-for-2 but man did they make a lot of noise … see Aurelian Resources … see Noront Resources

APPLAUDING SHAREHOLDERS OF CENTURY MINING

I said I would be the first to applaud it, so bravo to all of you for your efforts. I want to congratulate the “Century Mining Corporation Concerned Shareholders” group for its activism efforts. By amalgamating all shareholders for the purpose of educating, communicating, sharing and analyzing all aspects of this potential acquisition, you have given yourself the opportunity to generate greater shareholder value through:

* Rejection of this offer

* Sweetening of the current offer

* Attracting a better offer

This ordeal is long from over, so don’t give up. Continue to push for a better deal if the majority of you truly believe the White Tiger offer is insufficient ….and let AGORACOM know if there is anything further we can do to help the cause.

Best Regards,

George and the AGORACOM Team