Sponsor: Loncor is a Canadian gold exploration company focused on two projects in the DRC – the Ngayu and North Kivu projects, both have historic gold production. Exploration at the Ngayu project is currently being undertaken by Loncor’s joint venture partner Barrick Gold. The Ngayu project is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

From the HRA Journal: Issue 314

The fun doesn’t stop. Waves of liquidity continue to wash traders cares away. Even assassinations and war mongering generate little more than half day dips on Wall St. It seems nothing can get in the way of the bull rally that’s carrying all risk assets higher.

It feels like it could go on for a while, though I think the liquidity will have to keep coming to sustain it. By most readings, bullishness on Wall St is at levels that are rarely sustained for more than a few weeks. Some sort of correction on Wall St seems highly likely, and soon. Whether its substantial or just another blip on the way higher remains to be seen.

The resource sector, especially gold and silver stocks, have had their own rally. Our Santa Claus market was as good or better than Wall St’s for a change. And I don’t think its over yet. I think we’re in for the best Q1 we’ve seen for a few years. And we could be in for something better than that even. I increasingly see signs of a major rally developing in the gold space. It’s already been pretty good but I think a multi-quarter, or longer, move may be starting to take shape.

I usually spend time on all the metals in the first issue of the year. But, because the makings of this gold rally are complex and long in coming I decided to detail my reasoning. That ended up taking several pages so I’ll save talk on base metals and other markets for the next issue.

Eric Coffin

January 7, 2020

Gold’s Big Picture

“Après moi, le déluge“

No, I’m not writing about Louis IV, though there might be some appropriateness to the analogy, now that I think about it. The quote is famous, even though there’s no agreement on what it was supposed to mean. Most figure Louis was referring to the biblical flood, that all would be chaos once his reign ended.

The deluge I’m referring to isn’t water. It’s the flood of money the US Fed, and other central banks, continue to unleash to keep markets stable. Markets, especially stock markets, love liquidity. You can see the impact of the latest deluge, particularly the US Fed’s in the chart below that traces both the SPX index value and the level of a “Global Liquidity Proxy” (“GLP”) measuring fiscal/monetary tightness and weakness.

You can see the GLP moved lower in late 2018 as the Fed tightened and the impact that had on Wall St. Conversely, you can see the SPX running higher in the past couple of months as the US backed off rate increases, increased fiscal deficit expansion, and grew the Fed balance sheet through, mainly, repo market operations.

Wall St, and most other bourses, are loving these money flows. The Santa Claus rally discussed in the last issue continued to strengthen all the way to and through year end. As it turned out, the Fed either provided enough backstop in advance or the yearend repo issues were overstated. The repo market itself was calm going through year end and a lot of the short-term money offered by the Fed during that week wasn’t taken down.

Everything may have changed in the past couple of days with the dramatic increase in US-Iran tensions. I don’t know how big an issue that will be, since no one knows what form Iran’s retaliation will be or how much things will escalate. I DO think it’s potentially a big deal with very negative connotations, but it may take time to unfold. Someone at the Fed thought so too, as the past couple of days saw a return to large scale Fed lending in the repo market.

I’ve no doubt Iran will try and take revenge for the assassination of its most famous military commander by the US. But I don’t know what form it will take and if this means the US has drawn itself into the Mideast quagmire even more. I fear it has though. The US is already talking about adding 3,000 troops to its Mideast presence and they’re just warming up. Even larger scale attacks, if they happen, may not derail Wall St, but they’re certainly not a positive development at any level.

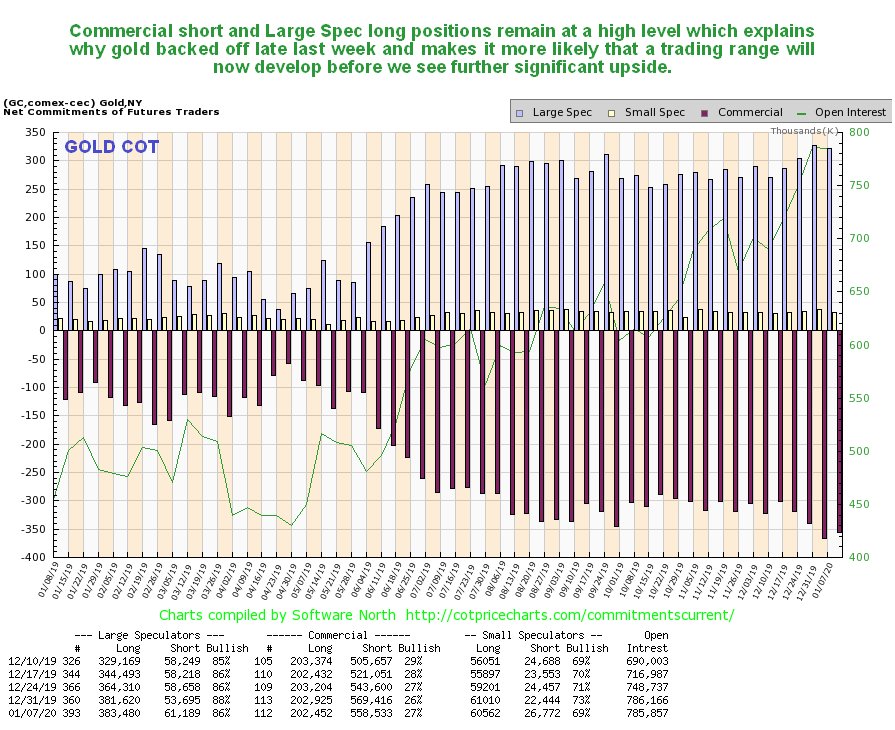

We know how stretched both market valuations and sentiment were before the Suleimani drone strike. The chart below shows a three-year trace of the “fear/greed index”. You can see that its hardly a stable reading. It flip flops often and extreme readings rarely hold for long. At last check, the reading was 94% bullish.

Sentiment almost never gets that bullish and, when it does, nothing good comes of it for bulls. A reading that close to 100% tells you we’re just about out of buyers. Whatever happens in and around Iran, I think a near term correction is inevitable. The only question is whether it’s a large one or not.

A rapid escalation in US-Iran tensions could certainly make a near term correction larger. If the flood of liquidity continues though, a correction could just be another waystation on the road to higher highs. There are a couple of other dangers Wall St still faces that I’ll touch on briefly at the end of this article. First however, lets move on to the main event for us-the gold market.

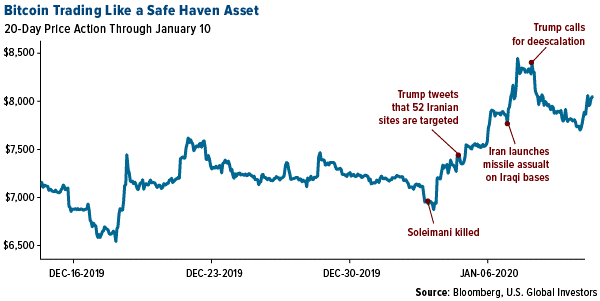

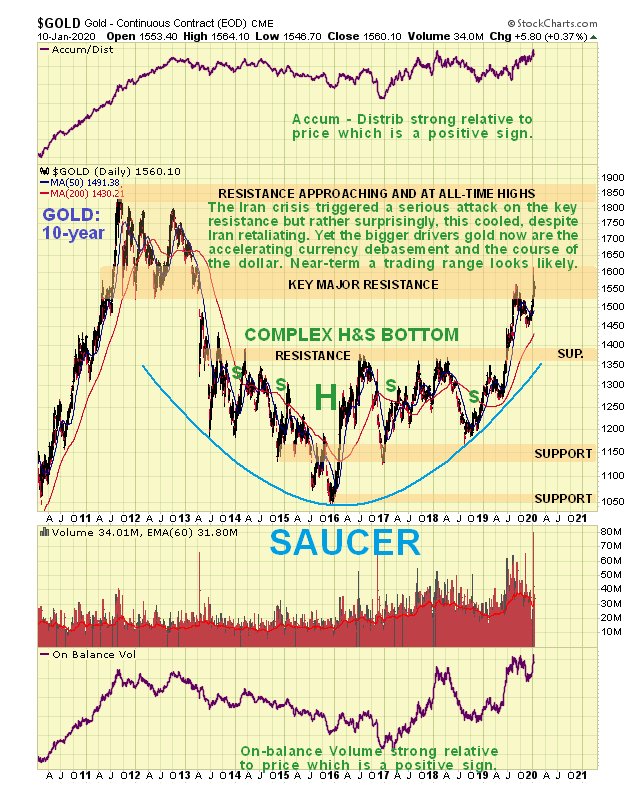

It wasn’t just the SPX enjoying a Santa rally this year. Gold experienced the rally we were hoping for that gold miner stocks seemed to be foretelling early last month. Gold’s been doing well since it bottomed at $1275 in June, but it didn’t feel that way during the long hiatus between the early September high and the current move. The gold price currently sits above September’s multi-year high, after breaching that high in the wake of the Baghdad drone strike. And the first retaliatory strike by Iran. Volatility will be very high for a while going forward.

I think we’ll see more multi-year highs going forward. I hate that the latest move higher is driven by geopolitics. Scary geopolitics and military confrontations mean people are dying. We don’t want to profit from misery. And we won’t anyway, if things get ugly enough in the Mideast to scare traders out of the market.

Geopolitical price moves almost always unwind quickly. I’d much prefer to see gold moving higher for macro reasons, not as a political safety trade. I expect more political/military inspired moves. As the Iran conflict unfolds. Make no mistake, Iran is NOT Iraq. Its army is far larger, better trained and better equipped than Iraq. This could get ugly.

The balance of this piece will deal with my macro argument for higher gold prices over an extended period. The geopolitical stuff will be layered on top of that for the next while and could strengthen both gold prices and the $US in risk-off trading. It should be viewed as a separate event from the argument laid out below.

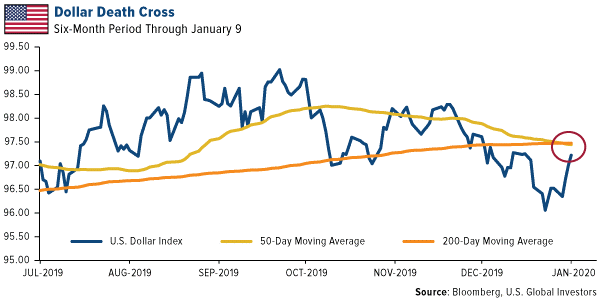

What else is driving gold higher? In part, it was gold’s inverse relationship with the US Dollar. As you already know, I’m not a believer that “its all about the USD, all the time” when it comes to the gold market. That’s an over-simplification of a more complex relationship. It also discounts the idea of gold as its own asset class that trades for its own reasons.

If you look at the gold chart above, and the USD chart below it, its immediately apparent that there isn’t a constant negative correlation at play. Gold rallied during the summer at the same time the USD did and for the same reason; the world-wide explosion of negative real yields. Gold weakened a bit when yields reversed to the upside and the USD got a bit of traction, but things changed again at the start of December.

The USD turned lower and lost two percent during December. US bond yields were generally rising during the month and the market (right or wrong) was assuming economic growth was accelerating. So, neither of those items explains the USD weakness.

If gold was a “risk off” trade, you sure couldn’t see it in the way any other market was trading. So, is there another explanation for recent strength in the gold price, and what does it tell us about 2020 and, perhaps, beyond?

Well, I’ve got a theory. If I’m right, it could mean a bull run for gold has a long way to go.

Some of this theory will be no surprise to you because it does partially hinge on further USD weakness. There are long term structural reasons why the US currency should weaken. But there are also fluctuating sources of demand for USDs, particularly from offshore buyers and borrowers that transact in US currency. That can create enough demand to strengthen the US over long periods. We just went though one such period, but it looks like that may have come to an end, with more bearish forces to the USD reasserting themselves.

How did we get here? Let’s start with the big picture, displayed on the top chart on the next page. It gives a long-term view of US Federal deficits and the unemployment rate. Normally, these travel in tandem. Higher unemployment means more social spending and higher deficits. Government spending expands during recessions and contracts-or should- (as a percentage of GDP) during expansions. Classic Keynesian stuff.

You rarely see these two measures diverge. The two times they did significantly before, on the left side of the chart, was due to “wartime deficits” which acted (along with conscription) to stimulate the economy and drive down unemployment.

You can see the Korean and Vietnam war periods pointed out on the chart.

The current period stands out for the extreme size of the divergence. US unemployment rates are at multi decade lows and yet the fiscal deficit as a percentage of GDP keeps rising. There has never been a divergence this large and its due to get larger.

We know why this is. Big tax cuts combined with a budget that is mostly non-discretionary. And the US is 10 years into an economic expansion, however weak. Just think what this graph will look like the next time the US goes into recession.

We can assume US government deficits aren’t going to shrink any time soon (and I think we can, pun intended, take that to the bank). That leaves trade in goods to act as a counterbalance to the funding demand created by fiscal deficits.

The chart above makes it clear the US won’t get much help from international trade. The US trade balance has been getting increasingly negative for decades. It’s better recently, but unlikely to turn positive soon, and maybe not ever.

To be clear, this is not a bad thing in itself, notwithstanding the view from the White House. The relative strength of the US economy and the US Dollar and cheaper offshore production costs have driven the trade balance. It’s grown because Americans found they got more value buying abroad and the world was happy to help finance it. It’s not a bad thing, but not a US Dollar support either.

The more complete picture of currency/investment flows is given by changes in the Current Account. In simplified terms, the Current Account measures the difference between what a country produces and what it consumes. For example, if a country’s trade deficit increases, so does its current account deficit. If there are funds flowing in from overseas investments on the other hand, this decrease the Current Account deficit or increase the surplus.

The graph below summarizes quarterly changes in the US current account. You can see how the balance got increasingly negative in the mid 2000’s as both imports and foreign investment by US companies increased.

Not coincidentally, this same period leading up to the Financial Crisis included a sustained downtrend in the US Dollar Index. The USD index chart on the bottom of the next page shows the scale of that decline, from an index value of 120 at the start of 2002 all the way down to 73 in early 2008.

The current account deficit (and value of the USD) improved markedly up to the end of the Financial Crisis as money poured into the US as a safe haven and consumers cut back on imports. The current account deficit bas been relatively stable since then, running at about $100bn/quarter until it dipped a bit again last year.

Trade, funds flows and changes in money supply have the largest long-term impacts on currency values. When the US Fed ended QE and started tightening monetary conditions in 2014, the USD enjoyed a strong rally. The USD Index was back to 100 by early 2015 and stayed there until loosening monetary conditions-and lots of jawboning from Washington-led to pullback. Things reversed again and the USD maintained a mild uptrend from early 2018 until now.

There are still plenty of US Dollar bulls around, and their arguments have short-term merit. Yes, the US has higher real interest rates and somewhat higher growth. Both are important to relative currency valuations as I’ve said in the past. Longer term however, the “twin deficits” -fiscal and current account-should underpin the fundamental value of the currency.

Movements don’t happen overnight, especially when you’re talking about the worlds reserve currency that has the deepest and largest market supporting it. Changing the overall trend for the USD is like turning a supertanker. I think it’s happening though, and it has big potential implications for commodities, especially gold.

Dollar bulls will tell you the USD is the “cleanest shirt in the laundry hamper”, referring to the relative strength of the growth rate and interest rates compared to other major currencies. That’s true if we just look at those measures but definitely not true when we look at the longer term-fiscal and current account deficits.

In fact, the US has about the worst combined fiscal/current account deficit in the G7. The chart at the bottom of this page, from lynalden.com shows the 2018 values for Current Account and Trade balances for a number of major economies, as a percentage of their GDP. It’s not a handsome group.

Both the trade and current account deficits are negative for most of them. In terms of G7 economies, the US has the worst combined Current/Trade deficit at 6% of GDP annually. You may be surprised to note that the Current/Trade balance for the Euro zone is much better than the US, thanks to a large Trade surplus. Much of that is generated by Germany. Indeed, this chart explains Germanys defense of the Euro. It’s combined Trade/Current Account surplus is so large it’s currency would be skyrocketing if it still used the Deutschmark.

Because the current account deficit is cumulative, the overall international investment position of the US has continued to worsen. The US has gone from being an international creditor to an international debtor, and the scale if its debt keeps increasing. That means it’s getting harder every year to reverse the current account position as the US borrows ever more abroad to cover its trade and fiscal deficits. Interest outflows keep growing and investment inflows shrinking. Something has to give.

The US has to borrow overseas, as private domestic demand for Treasury bonds isn’t high enough to fund the twin deficits. In the past, whenever the US Dollar got too high, offshore demand for US government debt diminished. It’s not clear why. Maybe the higher dollar made raising enough foreign funds difficult, or perhaps buyers started worrying about the USD dropping after they bought when it got too expensive. Whatever the reason, foreign holdings of US Treasuries have been declining, forcing the US to find new, domestic, buyers.

Last year, the US Fed stopped its quantitative tightening program, due to concerns about Dollar liquidity. Then came the repo market. Since September, the Fed’s balance sheet has expanded by over $400 billion, mainly due to repo market transactions.

The Fed maintains this “isn’t QE” because these are very short duration transactions but, cumulatively, the total Fed balance sheet keeps expanding. The “QE/no QE” debate is just semantics.

What do these transactions look like? Mostly, its Primary Dealers, banks that also take part in Treasury auctions, in the repo market. The Fed buys bonds, usually Treasuries, from these banks and pays for them in newly printed Dollars. That injects money into the system, helps hold down interest rates in the repo market and, not coincidentally, effectively helps fund the US fiscal deficit. To put the series of transactions in their simplest form, the US is effectively monetizing its deficit with a lot of these transactions.

The chart below illustrates the problem for the Primary Dealer US banks. They’ve got to buy Treasuries when they’re auctioned-that is their commitment as Primary Dealers. They also need to hold minimum cash balances as a percentage of assets under Basel II bank regulations. Cash balances fell to the minimum mandated level by late 2019- the horizontal black line on the chart. That’s when the trouble started.

These banks are so stuffed with Treasuries that they didn’t have excess cash reserves to lend into the repo market. Hence the blow up back in September and the need for the Fed to inject cash by buying Treasuries. The point, however, is that this isn’t really a “repo market issue”, that’s just where it reared its head. It’s a “too many Treasuries and not enough buyers” problem.

It will be tough for the Treasury to attract more offshore buyers unless the USD weakens, or interest rates rise enough to make them irresistible. Or a big drop in the federal deficit reduces the supply of Treasuries itself.

I doubt we’ll see interest rates move up significantly. I don’t think the economy could handle it and it would be self-defeating anyway, as the government deficit would explode because of interest expenses. And that’s not even taking into account the fact that President Trump would be freaking out daily.

Based on recent history and political expediency, I’d say the odds of significant budget deficit reductions are slim and none. That’s especially true going into an election year. There’s just no way we’re going to see spending restraint or tax increases in the next couple of years. Indeed, the supply of Treasuries will keep growing even if the US economy grows too. If there is any sort of significant slowdown or recession the Federal deficit will explode and so will the new supply of Treasures. Not an easy fix.

Barring new haven demand for US Treasuries, odds are the Fed will have to keep sopping up excess supply. That means expanding its balance sheet and, in so doing, effectively increasing the US money supply.

That brings us (finally!) to the “money shot” chart that appears above. It compares changes in the size of the Fed balance sheet and the US Dollar Index. To make it readable and allow me to match the scales, I generated a chart that tracks annual percentage changes.

The chart shows a strong inverse correlation between changes in the size of the Fed balance sheet and the value of the USD. This is unsurprising as most transactions that expand the Fed balance sheet also expand the money supply.

It’s impossible to tell how long the repo market transactions will continue but, after three months, they aren’t feeling very “temporary”. To me, it increasingly looks like these market operations are “debt monetization in drag”.

I don’t know if that’s the Fed’s real intent or just a side effect. It doesn’t really matter if the funding and money printing continues at scale. Even if the repo market calms completely, the odds are good we see some sort of “new QE” start up. Whatever official reason is given for it; I think it will happen mainly to soak up the excess supply of Treasuries fiscal deficits are creating.

I don’t blame the FOMC if they’re being disingenuous about it. That’s their job after all. If you’re a central banker, the LAST thing you’re going to say is “our government is having trouble finding buyers for its debt”, especially if its true.

With no prospect of lower deficits and apparent continued reduction in offshore Treasury holdings, this could develop into long-term sustained trend. I don’t expect it to move in a straight line, markets never do. A severe escalation in Mideast tensions or the start of a serious recession could both generate safe-haven Treasury buying. Money flows from that would take the pressure off the Fed and would be US Dollar supportive too.

That said, it seems the US has reached the point where a substantial increase in its central bank’s balance sheet is inevitable. Both Japan and the Eurozone have gotten there before the Fed, but it looks like it won’t be immune.

The Eurozone at least has a “Twin surplus” to help cushion things. And Japan, considered a basket case economically, had an extremely deep pool of domestic savings (far deeper than the US) to draw on. Until very recently, Japan also ran massive Current Account surpluses thanks to decades of heavy investments overseas by Japanese entities. Those advantages allowed the ECB and especially the BoJ to massively expand their balance sheets without generating a huge run up in interest rates or currency collapse.

I don’t know how far the US Fed can expand its balance sheet before bond yields start getting away from it. I think pretty far though. Having the world’s reserve currency is a massive advantage. There is huge built in demand for US Dollars and US denominated debt. That gives the Fed some runway if it must keep buying US Treasuries.

Assuming a run on yields doesn’t spoil the party, continued balance sheet and money supply expansion should put increasing downward pressure on the US Dollar. I don’t know if we’ll see a move as large as the mid-2000s but a move down to the low 80s for the USD Index over the course of two or three years wouldn’t be surprising.

It won’t be a straight-line move. A recession could derail things, though the bear market on Wall St that would generate would support bullion. Currency markets tend to be self-correcting over extended periods. If the USD Index falls enough and there is a bump in US real interest rates offshore demand for Treasuries should increase again.

The bottom line is that this is, and will continue to be, a very dynamic system. Even so, I think we’ve reached a major inflection point for the US currency. The 2000s were pretty good for the gold market and gold stocks. We started from a much lower base of $300/oz on the gold price. Starting at a $1200-1300 base this time, I think a price above $2000/oz is a real possibility over the next year or two.

It’s not hard to extrapolate prices higher than that, but I’m not looking or hoping for those. I prefer to see a longer, steadier move that brings traders along rather than freaking them out.

This prediction isn’t a sure thing. Predictions never are. But I think the probabilities now favor an extended bull run in the gold price. Assuming stock markets don’t blow up (though I still expect that correction), gold stocks should put in a leveraged performance much more impressive than the bullion price itself.

There will be consolidations and corrections along the way, but I think there will be many gold explorers and developers that rack up share price gains in the hundreds of percent. That doesn’t mean buying blindly and never trading. We still need to adjust when a stock gets overweight and manage risk around major exploration campaigns. The last few weeks has been a lot more fun in the resource space. I don’t think the fun’s over yet. Enjoy the ride.

Like any good contrarian, a 10-year bull market makes me alert of signs of potential trouble. As noted at the start of this editorial, I’m expecting continues floods of liquidity. That may simply overwhelm everything else for a while and allow Wall St to keep rallying, come what may.

That said, a couple of data points recently got my attention. One is more of a sentiment indicator, seen in the chart below. More than one wag has joked that the Fed need only worry about Wall St, since the stock market is the economy now. Turns out there is more than a bit of truth to that.

The chart shows the US Leading Indicator reading with the level of the stock market (which is a component of the official Leading Indicator) removed. As you can see, without Wall St, the indicator implies zero growth going forward. I’m mainly showing it as evidence of just how surreal things have become.

The chart above is something to keep an eye on going forward. It shows weekly State unemployment claims for several major sectors of the economy. What’s interesting about this chart is that claims have been climbing rapidly over the past few weeks. Doubly interesting is that the increase in claims is broad, both within and across several sectors of the economy.

I take the monthly Non-Farm Payroll number less seriously than most, because it’s a backward-looking indicator. This move in unemployment claims looks increasingly like a trend though. It’s now at its highest level since the Financial Crisis.

It’s not in the danger zone-yet. But its climbing fast. We may need to start paying more attention to those payroll numbers. If the chart below isn’t a statistical fluke, we may start seeing negative surprises in the NFP soon. That won’t hurt the gold price either.

Source and Thanks: https://www.hraadvisory.com/golds-big-picture