Posted by Brittany McNabb

at 9:12 AM on Wednesday, December 6th, 2023

Introduction:

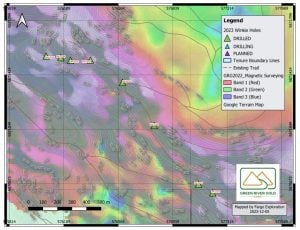

In the heart of British Columbia’s Cariboo Mining District, Green River Gold Corp. (CSE: CCR) (OTC Pink: CCRRF) is making waves with a groundbreaking announcement that positions the company as a key player in the mining industry. The recently received assay results from the Quesnel Nickel Project mark a significant milestone in Green River’s pursuit of mineral wealth.

Background and Context:

Green River Gold’s journey is rooted in over 50 drill holes, covering almost 10 kilometers along the Deep Purple magnetic anomaly. These holes consistently reveal nickel, magnesium, cobalt, and chromium starting from the surface of the bedrock. The company’s commitment to exploration and resource development has laid a robust foundation for success in the Cariboo Mining District.

Key Highlights and Advantages:

The assay results from drill holes WK-23-06, WK-23-07, and WK-23-08 showcase an average nickel grade of 0.18% and an impressive magnesium grade exceeding 21%. What sets Green River Gold apart is the consistency in results, mirroring those from previous years. The upcoming 6,000-meter NQ drill program and the ongoing exploration signify a strategic push toward development, affirming the company’s commitment to unlocking the potential of the Quesnel Nickel Project.

Potential Impact and Significance:

The Quesnel Nickel Project’s immense upside potential is highlighted by Kyle Townsend, Mine Manager for Green River. The continuous mineralization across all 50 consecutive drill holes underscores the project’s promising prospects. As Green River Gold embarks on a new phase of drilling, the potential impact on the company, the industry, and the broader market is a testament to the strategic importance of this discovery.

Expert Opinions and Analysis:

Experts echo the sentiment of optimism surrounding Green River Gold. Perry Little, President and CEO, emphasizes the significance of Craig Brekkas joining the Board, bringing over 30 years of experience in agriculture markets. His expertise adds a new perspective as the company looks beyond exploration towards development, including the extraction of nickel, talc, and other minerals.

Challenges and Considerations:

While Green River Gold enjoys a wave of success, challenges such as awaiting permits for the 6,000-meter NQ drill program exist. The company’s transparency in addressing challenges and outlining strategies to overcome them reflects a balanced and proactive approach.

Conclusion:

Green River Gold’s assay results reveal more than minerals; they unveil a company poised for prosperity in the mining industry. The consistency in findings, the strategic addition to the Board, and the ambitious drilling program all contribute to a narrative of growth and potential. As Green River Gold continues to carve its path in the Cariboo Mining District, investors and the business community are invited to witness and engage in a journey marked by discovery, innovation, and success.

Posted by Brittany McNabb

at 3:47 PM on Wednesday, November 29th, 2023

As the electric vehicle (EV) market gears up for exponential growth, recent projections from RBC Capital Markets indicate a promising trajectory. This surge in demand for EVs, driven by factors like price stability and charging infrastructure expansion, sets the stage for robust growth. Against this backdrop, Green River Gold emerges as a key player, strategically positioned to capitalize on the evolving dynamics of the mining industry.

Industry Outlook and Green River Gold’s Trajectory:

The electric vehicle (EV) market is poised for unprecedented growth, with RBC Capital Markets predicting a surge in demand for battery electric vehicles (BEVs). This aligns seamlessly with Green River Gold’s strategic trajectory, positioning the company as a key player in the evolving landscape of the mining industry. As the demand for BEVs rises, so does the significance of Green River Gold’s role in supplying essential minerals for their production.

Voices of Authority:

Industry leaders echo the optimism surrounding the electric vehicle market’s future. According to RBC Capital Markets, the consensus is that the market share for battery electric vehicles (BEVs) could reach 75% by 2050. Green River Gold’s executives align with this sentiment, underlining the company’s commitment to advancing mineral projects crucial for the electric vehicle revolution. Perry Little, President and CEO of Green River, affirms, “Our strategic focus positions us to play a vital role in the industry’s transformative journey.”

Green River Gold’s Highlights:

Green River Gold’s remarkable achievements, as outlined in the milestones, underscore the company’s commitment to industry leadership. The successful drilling campaign at the Quesnel Nickel Project, spanning 50 consecutive breakthroughs, aligns seamlessly with the industry’s trajectory. The strategic focus on nickel, magnesium, cobalt, and chromium positions Green River Gold as a key contributor to the imminent demand surge for minerals essential in electric vehicle production.

Real-world Relevance:

Green River Gold’s contributions extend beyond the mining industry, making a real-world impact on the electric vehicle revolution. As the demand for EVs rises, Green River Gold’s exploration efforts translate into a stable supply of essential minerals. This stability ensures the seamless production of electric vehicles, contributing to the global shift towards sustainable transportation. Investors can view Green River Gold not just as a mining company but as a driving force behind a greener, more sustainable future.

Looking Ahead with Green River Gold:

Looking ahead, Green River Gold stands at the forefront of the mining industry’s transformative journey. The company’s forward-looking goals align seamlessly with the optimistic industry forecast presented by RBC Capital Markets. Green River Gold’s strategic presence, coupled with its commitment to sustainable exploration, positions the company as a key player in shaping the future of mining. As the industry anticipates robust growth, investors have a unique opportunity to be part of Green River Gold’s promising journey towards a greener, more sustainable mining landscape.

Conclusion:

In conclusion, Green River Gold stands as a beacon of opportunity amid the surging tide of the electric vehicle revolution. As the industry gears up for substantial growth, Green River Gold’s strategic focus on exploration and commitment to advancing mineral projects places it at the forefront of this transformative wave. Investors keen on aligning with a company poised to navigate the currents of prosperity in a booming mining industry should delve deeper into Green River Gold’s promising journey.

This record is published on behalf of the featured company or companies mentioned (Collectively “Clients”), which are paid clients of Agora Internet Relations Corp or AGORACOM Investor Relations Corp. (Collectively “AGORACOM”)

AGORACOM.com is a platform. AGORACOM is an online marketing agency that is compensated by public companies to provide online marketing, branding and awareness through Advertising in the form of content on AGORACOM.com, its related websites (smallcapepicenter.com; smallcappodcast.com; smallcapagora.com) and all of their social media sites (Collectively “AGORACOM Network”) . As such please assume any of the companies mentioned above have paid for the creation, publication and dissemination of this article / post.

You understand that AGORACOM receives either monetary or securities compensation for our services, including creating, publishing and distributing content on behalf of Clients, which includes but is not limited to articles, press releases, videos, interview transcripts, industry bulletins, reports, GIFs, JPEGs, (Collectively “Records”) and other records by or on behalf of clients. Although AGORACOM compensation is not tied to the sale or appreciation of any securities, we stand to benefit from any volume or stock appreciation of our Clients. In exchange for publishing services rendered by AGORACOM on behalf of Clients, AGORACOM receives annual cash and/or securities compensation of typically up to $125,000.

Facts relied upon by AGORACOM are generally provided by clients or gathered by AGORACOM from other public sources including press releases, SEDAR and/or EDGAR filings, website, powerpoint presentations. These facts may be in error and if so, Records created by AGORACOM may be materially different. In our video interviews or video content, opinions are those of our guests or interviewees and do not necessarily reflect the opinion of AGORACOM.

Posted by Brittany McNabb

at 2:39 PM on Tuesday, November 28th, 2023

Introduction:

In a revolutionary shift, U.S. consumers are propelling electric vehicles (EVs) to the forefront of the automotive market, constituting a remarkable 9% of new car sales in 2023. As this surge continues, Infinity Stone Ventures stands poised to harness the momentum, strategically positioning itself in the rapidly evolving landscape of clean energy. Did you know in the U.S., there were roughly 136,000 EVs sold in September — a 67% year-over-year increase?

Industry Outlook and Infinity Stone Ventures’ Trajectory:

Against the backdrop of EVs claiming 9% of U.S. new car sales, Infinity Stone Ventures navigates the landscape with strategic prowess. The company’s trajectory aligns seamlessly with the burgeoning trends, ensuring it remains at the vanguard of the industry’s electrifying advancements. According to EIA, sales of hybrids, plug-in hybrids, and battery electric vehicles account for 15.8% of all new light-duty vehicle sales in the United States so far this year, compared with 12.3% in 2022 and 8.5% in 2021. While hybrids are more efficient in their use of gasoline, they do not offer the same benefits as all-electric vehicles.

Voices of Authority:

Industry leaders echo the sentiment that the EV sector’s ascent is undeniable, with a substantial 5 million new car sales dedicated to electric vehicles. These voices of authority resonate with Infinity Stone Ventures’ strategic direction, validating the company’s commitment to spearheading clean energy technologies.

Infinity Stone Ventures Highlights:

Framed against the backdrop of EVs claiming 9% of U.S. new car sales, their milestones underscore Infinity Stone Ventures’ pivotal role. The company’s innovative projects, strategic partnerships, and commitment to sustainability align seamlessly with the evolving market dynamics. Their partnership with R&D Innovations to use their patent-pending & proprietary air classification technology to mill graphite material into a fine graphite concentrate shows their potential for use as anode material in lithium-ion batteries.

Real-world Relevance:

With EVs becoming the new norm and an anticipated 5 million new sales, Infinity Stone Ventures plays a crucial role in the production of batteries, essential for the long-range electric cars dominating the market. Having refined graphite from its Rockstone Graphite Project to 99.73% Cg shows great significance for EV batteries.

Looking Ahead with Infinity Stone Ventures:

Positioned at the forefront of the green revolution, the company’s future goals mirror the optimistic trajectory of the EV industry, offering investors a compelling opportunity.

Conclusion:

In a landscape where electric mobility claims a substantial 9% share of U.S. new car sales, Infinity Stone Ventures stands as a key player, ready to shape the future of sustainable energy. This Industry Bulletin extends an invitation for potential investors to explore the unique opportunities within Infinity Stone Ventures, a company perfectly aligned with the accelerating surge in clean energy demand.

This record is published on behalf of the featured company or companies mentioned (Collectively “Clients”), which are paid clients of Agora Internet Relations Corp or AGORACOM Investor Relations Corp. (Collectively “AGORACOM”)

AGORACOM.com is a platform. AGORACOM is an online marketing agency that is compensated by public companies to provide online marketing, branding and awareness through Advertising in the form of content on AGORACOM.com, its related websites (smallcapepicenter.com; smallcappodcast.com; smallcapagora.com) and all of their social media sites (Collectively “AGORACOM Network”) . As such please assume any of the companies mentioned above have paid for the creation, publication and dissemination of this article / post.

You understand that AGORACOM receives either monetary or securities compensation for our services, including creating, publishing and distributing content on behalf of Clients, which includes but is not limited to articles, press releases, videos, interview transcripts, industry bulletins, reports, GIFs, JPEGs, (Collectively “Records”) and other records by or on behalf of clients. Although AGORACOM compensation is not tied to the sale or appreciation of any securities, we stand to benefit from any volume or stock appreciation of our Clients. In exchange for publishing services rendered by AGORACOM on behalf of Clients, AGORACOM receives annual cash and/or securities compensation of typically up to $125,000.

Facts relied upon by AGORACOM are generally provided by clients or gathered by AGORACOM from other public sources including press releases, SEDAR and/or EDGAR filings, website, powerpoint presentations. These facts may be in error and if so, Records created by AGORACOM may be materially different. In our video interviews or video content, opinions are those of our guests or interviewees and do not necessarily reflect the opinion of AGORACOM.

From time to time, reference may be made in our marketing materials to prior Records we have published. These references may be selective, may reference only a portion of an article or recommendation, and are likely not to be current. As markets change continuously, previously published information and data may not be current and should not be relied upon.

NO INVESTMENT ADVICE

This record, and any record we publish by or on behalf of our clients, should not be construed as an offer or solicitation to buy or sell products or securities.

You understand and agree that no content in this record or published by AGORACOM constitutes a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable or advisable for any specific person and that no such content is tailored to any specific person’s needs. We will never advise you personally concerning the nature, potential, advisability, value or suitability of any particular security, portfolio of securities, transaction, investment strategy, or other matter.

Neither the writer of this record nor AGORACOM is an investment advisor. Both are neither licensed to provide nor are making any buy or sell recommendations. For more information about this or any other company, please review their public documents to conduct your own due diligence.

Posted by Brittany McNabb

at 10:20 AM on Tuesday, November 28th, 2023

In the dynamic landscape of copper exploration, Fabled Copper Corp. emerges as a transformative force, breaking new ground on the Muskwa Copper Project. Today, the company proudly announces the reception of its Mines Act Permit, a pivotal milestone unlocking a two-year drilling endeavor across the Neil, Toro, and Bronson properties in northern British Columbia.

Background and Context:

Founded on a commitment to excellence, Fabled Copper Corp. has a rich history woven with successful explorations and unwavering dedication to responsible mining practices. The Muskwa Copper Project, comprising the Neil, Toro, and Bronson properties, has been granted the drilling permit, with the Davis Keays Eagle Vein area taking precedence. This marks the dawn of a groundbreaking chapter in the company’s legacy.

Key Highlights and Advantages:

First-ever Surface Drilling on Eagle Vein:

Fabled Copper Corp. embarks on an unprecedented journey with a helicopter-supported diamond drill program spanning 3,000 to 5,000 meters on the Davis Keays Eagle Vein. The magnitude of this endeavor is underscored by its historic nature, representing the inaugural surface drilling in the Eagle Vein area.

Precision Redefining Exploration:

Fabled Copper Corp.’s approach is not just about reaching the Eagle Vein; it’s about reshaping the understanding of the ore body. With cutting-edge technology ensuring a target accuracy of 3 cms, the company anticipates not just intercepting the Eagle Vein but unraveling a network of copper-bearing veins, potentially reshaping the future of the project.

Extending Reserves and Exploring Depths:

Building upon the legacy of the 1990 Feasibility Report, Fabled Copper Corp. aims to extend the known reserves below the 5,800-foot level. The potential of parallel veins, discovered during the 2022 work program, adds a layer of excitement to the prospect of uncovering new copper-rich domains.

Potential Impact and Significance:

The issuance of the Mines Act Permit is more than a regulatory approval; it’s a catalyst for potential game-changing discoveries. As Fabled Copper Corp. envisions the intersections of multiple copper-bearing veins, the reverberations extend beyond the company, influencing the industry’s outlook and investor sentiment.

Expert Opinions and Analysis:

Peter Hawley, President, CEO of Fabled Copper Corp., expresses the company’s enthusiasm, stating, “We are very excited to finally receive our long-awaited drill permit.” Industry analysts echo this sentiment, recognizing the strategic importance of the Muskwa Copper Project in an era where copper’s value is paramount.

Challenges and Considerations:

While the prospects are exhilarating, challenges and considerations are inherent. Fabled Copper Corp. acknowledges the need for funding to materialize this ambitious drill program. The company’s transparent approach to addressing challenges reflects a commitment to prudent financial management.

Conclusion:

In the heart of the Muskwa Copper Project, Fabled Copper Corp. is not merely exploring; it is pioneering a new era of copper exploration. The Mines Act Permit opens doors to possibilities that transcend conventional boundaries. As the company ventures into uncharted territories, investors are invited to witness the unfolding narrative of discovery and innovation. Fabled Copper Corp.’s commitment to responsible stewardship and its relentless pursuit of excellence make it a beacon in the evolving story of copper exploration.

Posted by AGORACOM

at 1:56 PM on Monday, January 27th, 2020

Sponsor: Loncor is a Canadian gold exploration company that controls over 2,400,000 high grade ounces outside of a Barrick JV.. The Ngayu JV property is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

Barrick Gold’s Kibali mine beat its 2019 production guidance of 750,000 ounces by delivering 814,027 ounces

Kibali is 200km to the southwest of Loncor’s JV with Barrick in search for further Tier Once mining assets

KINSHASA, Democratic Republic of Congo, Jan. 27, 2020 (GLOBE NEWSWIRE) — Barrick Gold Corporation (NYSE:GOLD) (TSX:ABX) - Barrick Gold Corporation’s Kibali mine beat its 2019 production guidance of 750,000 ounces of gold by a substantial margin, delivering 814,027 ounces in another record year.

Barrick president and chief executive Mark Bristow told a media briefing here that Kibali’s continuing stellar performance was a demonstration of how a modern, Tier One gold mine could be developed and operated successfully in what is one of the world’s most remote and infrastructurally under-endowed regions.  He also noted that in line with Barrick’s policy of employing, training and advancing locals, the mine was managed by a majority Congolese team, supported by a corps of majority Congolese supervisors and personnel.

Already one of the world’s most highly automated underground gold

mines, Kibali continues its technological advance with the introduction

of truck and drill training simulators and the integration of systems

for personnel safety tracking and ventilation demand control. The

simulators will also be used to train operators from Barrick’s Tanzanian

mines.

“The completion of the Kalimva Ikamva prefeasibility study has

delivered another viable opencast project which will help balance

Kibali’s opencast/underground ore ratio and enhance the flexibility of

the mine plan. Down-plunge extension drilling at Gorumbwa has

highlighted future underground potential and ongoing conversion drilling

at KCD is delivering reserve replenishment. All in all, Kibali is well

on track not only to meet its 10-year production targets but to extend

them beyond this horizon,†Bristow said.

“We’re maintaining a strong focus on energy efficiency through

the development of our grid stabilizer project, scheduled for

commissioning in the second quarter of 2020. This uses new battery

technology to offset the need for running diesel generators as a

spinning reserve and ensures we maximize the use of renewable hydro

power. The installation of three new elution diesel heaters will also

help improve efficiencies and control power costs. It’s worth noting

that our clean energy strategy not only achieves cost and efficiency

benefits but also once again reduces Kibali’s environmental footprint.â€

Bristow said despite the pace of production and the size and complexity of the mine, Kibali was maintaining its solid safety and environmental records, certified by ISO 45001 and ISO 14001 accreditations. Â It also remained committed to community upliftment and local economic development. Â In 2019, it spent $158 million with Congolese contractors and suppliers and in December, it started work on a trial section for a new concrete road between Durba and the Watsa bridge.

Posted by AGORACOM

at 11:37 AM on Tuesday, January 21st, 2020

Sponsor: Loncor is a Canadian gold exploration company that controls over 2,400,000 high grade ounces outside of a Barrick JV. Exploration is currently being conducted by Barrick. The Ngayu property is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

Gold is a hedge against inflation that is being used more and more

Goldex CEO pointed to a recent Goldman Sachs report that pointed to gold as being a better hedge than oil.

This view is the new consensus that will increase demand for gold.

(Kitco News) What can take the

gold market from $1,550 to $1,600 and higher? Goldex CEO and founder

Sylvia Carrasco told Kitco News that she is not ruling out the $1,900 an

ounce level this year if geopolitical and trade tensions escalate in

the current economic climate.

There are a number of strong drivers supporting gold prices this

year, including geopolitical and trade tensions, global debt, dovish

central banks, weakening U.S. dollar as well as the political situation

in the U.S., Carrasco said on Thursday.

“Last year, I said that the perfect storm was forming and I think I

would use this phrase again. The perfect storm is now happening,”

Carrasco noted. “Gold should be around $1,600 if nothing else crazy

happens. At this moment in time, I can see gold between the $1,500 and

the $2,000 mark during 2020.”

If the market sees a further increase in geopolitical tensions or

additional trade concerns this year, gold will surge towards $1,900,

Goldex CEO pointed out. And if things do calm down, Carrasco does not

see gold falling much below $1,500 an ounce.

“It is going to be another record year,” she said, referring to gold

hitting record-highs in many currencies last year. “And it will be

mainly due to geopolitical tensions raising prices higher.”

“With the current economic climate, gold should be between $1,500 and

$1,600. If on top of that bare minimum, you add very strong

geopolitical tensions or commercial trade issues, then you take it from

$1,600 up to $1,900,” she added.

At the time of writing, the spot gold price was trading at $1,560.40,

up 0.24% on the day and up 2.8% since the start of the year.

Gold is a hedge against inflation that is being used more and more by

investors who are realizing the benefits of the yellow metal, Carrasco

said.

“Gold is the hedge that people should be using. I wouldn’t build my

personal wealth portfolio just on gold. But gold is more and more

clearly overtaking oil and any other hedging mechanisms … Gold will be a

good trade whether for speculative reasons or for trading,” she noted.

Goldex CEO pointed to a recent Goldman Sachs report

that pointed to gold as being a better hedge than oil. Carrasco added

that this view is the new consensus that will increase demand for gold.

Gold began the year with a bang as U.S.-Iran tensions flared up and surprised the markets in the first two weeks of January.

“The rally we’ve seen is based on geopolitical tensions between the

U.S. and Iran. We need to see also the reasons behind Trump’s approach

when it comes to Iran … In September, the U.S. ended up a positive net

exporter of oil for the first time in history. That gives you a reason

why Trump thinks he is not affected by the tensions even though the rest

of the world is affected,” Carrasco described.

Also, U.S. President Donald Trump was driven by the goal to distract

the market from the impeachment proceedings against him, she added.

Going forward, gold prices are likely to rise further, especially

considering that most of the major central banks around the world are

not planning to start raising rates any time soon.

“Central banks using unconventional ways … Is there going to be an

increase in interest rates in Europe or in the U.S.? The answer is no.

And if interest rates are not going to increase, gold is the first one

that is affected,” Carrasco said.

On top of that, the central banks will remain significant gold buyers

in 2020. “That’s another reason why gold prices will increase this

year,” she said.

Growing debt also supports higher gold prices this year, the CEO

added. “We’ve been talking about debt for years — how corporate debt and

government debt continues to increase. More debt effectively means a

potentially weaker U.S. dollar. The moment the U.S. dollar is weak,

where do you go? The only safe place is gold. And I think we are going

to be seeing a weakening dollar as the year continues,” Carrasco

described.

Posted by AGORACOM

at 12:32 PM on Friday, January 17th, 2020

Sponsor: Loncor is a Canadian gold exploration company focused on two projects in the DRC – the Ngayu and North Kivu projects, both have historic gold production. Exploration at the Ngayu project is currently being undertaken by Loncor’s joint venture partner Barrick Gold. The Ngayu project is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

From the HRA Journal: Issue 314

The fun doesn’t stop. Waves of liquidity continue to wash traders

cares away. Even assassinations and war mongering generate little more

than half day dips on Wall St. It seems nothing can get in the way of

the bull rally that’s carrying all risk assets higher.

It feels like it could go on for a while, though I think the

liquidity will have to keep coming to sustain it. By most readings,

bullishness on Wall St is at levels that are rarely sustained for more

than a few weeks. Some sort of correction on Wall St seems highly

likely, and soon. Whether its substantial or just another blip on the

way higher remains to be seen.

The resource sector, especially gold and silver stocks, have had

their own rally. Our Santa Claus market was as good or better than Wall

St’s for a change. And I don’t think its over yet. I think we’re in for

the best Q1 we’ve seen for a few years. And we could be in for something

better than that even. I increasingly see signs of a major rally

developing in the gold space. It’s already been pretty good but I think a

multi-quarter, or longer, move may be starting to take shape.

I usually spend time on all the metals in the first issue of the

year. But, because the makings of this gold rally are complex and long

in coming I decided to detail my reasoning. That ended up taking several

pages so I’ll save talk on base metals and other markets for the next

issue.

No, I’m not writing about Louis IV, though there might be some

appropriateness to the analogy, now that I think about it. The quote is

famous, even though there’s no agreement on what it was supposed to

mean. Most figure Louis was referring to the biblical flood, that all

would be chaos once his reign ended.

The deluge I’m referring to isn’t water. It’s the flood of money the

US Fed, and other central banks, continue to unleash to keep markets

stable. Markets, especially stock markets, love liquidity. You can see

the impact of the latest deluge, particularly the US Fed’s in the chart

below that traces both the SPX index value and the level of a “Global

Liquidity Proxy” (“GLP”) measuring fiscal/monetary tightness and

weakness.

You can see the GLP moved lower in late 2018 as the Fed tightened and

the impact that had on Wall St. Conversely, you can see the SPX running

higher in the past couple of months as the US backed off rate

increases, increased fiscal deficit expansion, and grew the Fed balance

sheet through, mainly, repo market operations.

Wall St, and most other bourses, are loving these money flows. The

Santa Claus rally discussed in the last issue continued to strengthen

all the way to and through year end. As it turned out, the Fed either

provided enough backstop in advance or the yearend repo issues were

overstated. The repo market itself was calm going through year end and a

lot of the short-term money offered by the Fed during that week wasn’t

taken down.

Everything may have changed in the past couple of days with the

dramatic increase in US-Iran tensions. I don’t know how big an issue

that will be, since no one knows what form Iran’s retaliation will be or

how much things will escalate. I DO think it’s potentially a big deal

with very negative connotations, but it may take time to unfold. Someone

at the Fed thought so too, as the past couple of days saw a return to

large scale Fed lending in the repo market.

I’ve no doubt Iran will try and take revenge for the assassination of

its most famous military commander by the US. But I don’t know what

form it will take and if this means the US has drawn itself into the

Mideast quagmire even more. I fear it has though. The US is already

talking about adding 3,000 troops to its Mideast presence and they’re

just warming up. Even larger scale attacks, if they happen, may not

derail Wall St, but they’re certainly not a positive development at any

level.

We know how stretched both market valuations and sentiment were

before the Suleimani drone strike. The chart below shows a three-year

trace of the “fear/greed index”. You can see that its hardly a stable

reading. It flip flops often and extreme readings rarely hold for long.

At last check, the reading was 94% bullish.

Sentiment almost never gets that bullish and, when it does, nothing

good comes of it for bulls. A reading that close to 100% tells you we’re

just about out of buyers. Whatever happens in and around Iran, I think a

near term correction is inevitable. The only question is whether it’s a

large one or not.

A rapid escalation in US-Iran tensions could certainly make a near

term correction larger. If the flood of liquidity continues though, a

correction could just be another waystation on the road to higher highs.

There are a couple of other dangers Wall St still faces that I’ll touch

on briefly at the end of this article. First however, lets move on to

the main event for us-the gold market.

It wasn’t just the SPX enjoying a Santa rally this year. Gold

experienced the rally we were hoping for that gold miner stocks seemed

to be foretelling early last month. Gold’s been doing well since it

bottomed at $1275 in June, but it didn’t feel that way during the long

hiatus between the early September high and the current move. The gold

price currently sits above September’s multi-year high, after breaching

that high in the wake of the Baghdad drone strike. And the first

retaliatory strike by Iran. Volatility will be very high for a while

going forward.

I think we’ll see more multi-year highs going forward. I hate that

the latest move higher is driven by geopolitics. Scary geopolitics and

military confrontations mean people are dying. We don’t want to profit

from misery. And we won’t anyway, if things get ugly enough in the

Mideast to scare traders out of the market.

Geopolitical price moves almost always unwind quickly. I’d much

prefer to see gold moving higher for macro reasons, not as a political

safety trade. I expect more political/military inspired moves. As the

Iran conflict unfolds. Make no mistake, Iran is NOT Iraq. Its army is

far larger, better trained and better equipped than Iraq. This could get

ugly.

The balance of this piece will deal with my macro argument for higher

gold prices over an extended period. The geopolitical stuff will be

layered on top of that for the next while and could strengthen both gold

prices and the $US in risk-off trading. It should be viewed as a

separate event from the argument laid out below.

What else is driving gold higher? In part, it was gold’s inverse

relationship with the US Dollar. As you already know, I’m not a believer

that “its all about the USD, all the time” when it comes to the gold

market. That’s an over-simplification of a more complex relationship. It

also discounts the idea of gold as its own asset class that trades for

its own reasons.

If you look at the gold chart above, and the USD chart below it, its

immediately apparent that there isn’t a constant negative correlation at

play. Gold rallied during the summer at the same time the USD did and

for the same reason; the world-wide explosion of negative real yields.

Gold weakened a bit when yields reversed to the upside and the USD got a

bit of traction, but things changed again at the start of December.

The USD turned lower and lost two percent during December. US bond

yields were generally rising during the month and the market (right or

wrong) was assuming economic growth was accelerating. So, neither of

those items explains the USD weakness.

If gold was a “risk off” trade, you sure couldn’t see it in the way

any other market was trading. So, is there another explanation for

recent strength in the gold price, and what does it tell us about 2020

and, perhaps, beyond?

Well, I’ve got a theory. If I’m right, it could mean a bull run for gold has a long way to go.

Some of this theory will be no surprise to you because it does

partially hinge on further USD weakness. There are long term structural

reasons why the US currency should weaken. But there are also

fluctuating sources of demand for USDs, particularly from offshore

buyers and borrowers that transact in US currency. That can create

enough demand to strengthen the US over long periods. We just went

though one such period, but it looks like that may have come to an end,

with more bearish forces to the USD reasserting themselves.

How did we get here? Let’s start with the big picture, displayed on

the top chart on the next page. It gives a long-term view of US Federal

deficits and the unemployment rate. Normally, these travel in tandem.

Higher unemployment means more social spending and higher deficits.

Government spending expands during recessions and contracts-or should-

(as a percentage of GDP) during expansions. Classic Keynesian stuff.

You rarely see these two measures diverge. The two times they did

significantly before, on the left side of the chart, was due to “wartime

deficits” which acted (along with conscription) to stimulate the

economy and drive down unemployment.

You can see the Korean and Vietnam war periods pointed out on the chart.

The current period stands out for the extreme size of the divergence.

US unemployment rates are at multi decade lows and yet the fiscal

deficit as a percentage of GDP keeps rising. There has never been a

divergence this large and its due to get larger.

We know why this is. Big tax cuts combined with a budget that is

mostly non-discretionary. And the US is 10 years into an economic

expansion, however weak. Just think what this graph will look like the

next time the US goes into recession.

We can assume US government deficits aren’t going to shrink any time

soon (and I think we can, pun intended, take that to the bank). That

leaves trade in goods to act as a counterbalance to the funding demand

created by fiscal deficits.

The chart above makes it clear the US won’t get much help from

international trade. The US trade balance has been getting increasingly

negative for decades. It’s better recently, but unlikely to turn

positive soon, and maybe not ever.

To be clear, this is not a bad thing in itself, notwithstanding the

view from the White House. The relative strength of the US economy and

the US Dollar and cheaper offshore production costs have driven the

trade balance. It’s grown because Americans found they got more value

buying abroad and the world was happy to help finance it. It’s not a bad

thing, but not a US Dollar support either.

The more complete picture of currency/investment flows is given by

changes in the Current Account. In simplified terms, the Current Account

measures the difference between what a country produces and what it

consumes. For example, if a country’s trade deficit increases, so does

its current account deficit. If there are funds flowing in from overseas

investments on the other hand, this decrease the Current Account

deficit or increase the surplus.

The graph below summarizes quarterly changes in the US current

account. You can see how the balance got increasingly negative in the

mid 2000’s as both imports and foreign investment by US companies

increased.

Not coincidentally, this same period leading up to the Financial

Crisis included a sustained downtrend in the US Dollar Index. The USD

index chart on the bottom of the next page shows the scale of that

decline, from an index value of 120 at the start of 2002 all the way

down to 73 in early 2008.

The current account deficit (and value of the USD) improved markedly

up to the end of the Financial Crisis as money poured into the US as a

safe haven and consumers cut back on imports. The current account

deficit bas been relatively stable since then, running at about

$100bn/quarter until it dipped a bit again last year.

Trade, funds flows and changes in money supply have the largest

long-term impacts on currency values. When the US Fed ended QE and

started tightening monetary conditions in 2014, the USD enjoyed a strong

rally. The USD Index was back to 100 by early 2015 and stayed there

until loosening monetary conditions-and lots of jawboning from

Washington-led to pullback. Things reversed again and the USD maintained

a mild uptrend from early 2018 until now.

There are still plenty of US Dollar bulls around, and their arguments

have short-term merit. Yes, the US has higher real interest rates and

somewhat higher growth. Both are important to relative currency

valuations as I’ve said in the past. Longer term however, the “twin

deficits” -fiscal and current account-should underpin the fundamental

value of the currency.

Movements don’t happen overnight, especially when you’re talking

about the worlds reserve currency that has the deepest and largest

market supporting it. Changing the overall trend for the USD is like

turning a supertanker. I think it’s happening though, and it has big

potential implications for commodities, especially gold.

Dollar bulls will tell you the USD is the “cleanest shirt in the

laundry hamper”, referring to the relative strength of the growth rate

and interest rates compared to other major currencies. That’s true if we

just look at those measures but definitely not true when we look at the

longer term-fiscal and current account deficits.

In fact, the US has about the worst combined fiscal/current account deficit in the G7. The chart at the bottom of this page, from lynalden.com

shows the 2018 values for Current Account and Trade balances for a

number of major economies, as a percentage of their GDP. It’s not a

handsome group.

Both the trade and current account deficits are negative for most of

them. In terms of G7 economies, the US has the worst combined

Current/Trade deficit at 6% of GDP annually. You may be surprised to

note that the Current/Trade balance for the Euro zone is much better

than the US, thanks to a large Trade surplus. Much of that is generated

by Germany. Indeed, this chart explains Germanys defense of the Euro.

It’s combined Trade/Current Account surplus is so large it’s currency

would be skyrocketing if it still used the Deutschmark.

Because the current account deficit is cumulative, the overall

international investment position of the US has continued to worsen. The

US has gone from being an international creditor to an international

debtor, and the scale if its debt keeps increasing. That means it’s

getting harder every year to reverse the current account position as the

US borrows ever more abroad to cover its trade and fiscal deficits.

Interest outflows keep growing and investment inflows shrinking.

Something has to give.

The US has to borrow overseas, as private domestic demand for

Treasury bonds isn’t high enough to fund the twin deficits. In the past,

whenever the US Dollar got too high, offshore demand for US government

debt diminished. It’s not clear why. Maybe the higher dollar made

raising enough foreign funds difficult, or perhaps buyers started

worrying about the USD dropping after they bought when it got too

expensive. Whatever the reason, foreign holdings of US Treasuries have

been declining, forcing the US to find new, domestic, buyers.

Last year, the US Fed stopped its quantitative tightening program,

due to concerns about Dollar liquidity. Then came the repo market. Since

September, the Fed’s balance sheet has expanded by over $400 billion,

mainly due to repo market transactions.

The Fed maintains this “isn’t QE” because these are very short duration transactions but, cumulatively, the total Fed balance sheet keeps expanding. The “QE/no QE” debate is just semantics.

What do these transactions look like? Mostly, its Primary Dealers,

banks that also take part in Treasury auctions, in the repo market. The

Fed buys bonds, usually Treasuries, from these banks and pays for them

in newly printed Dollars. That injects money into the system, helps hold

down interest rates in the repo market and, not coincidentally,

effectively helps fund the US fiscal deficit. To put the series of

transactions in their simplest form, the US is effectively monetizing its deficit with a lot of these transactions.

The chart below illustrates the problem for the Primary Dealer US

banks. They’ve got to buy Treasuries when they’re auctioned-that is

their commitment as Primary Dealers. They also need to hold minimum cash

balances as a percentage of assets under Basel II bank regulations.

Cash balances fell to the minimum mandated level by late 2019- the

horizontal black line on the chart. That’s when the trouble started.

These banks are so stuffed with Treasuries that they didn’t have

excess cash reserves to lend into the repo market. Hence the blow up

back in September and the need for the Fed to inject cash by buying

Treasuries. The point, however, is that this isn’t really a “repo market

issue”, that’s just where it reared its head. It’s a “too many

Treasuries and not enough buyers” problem.

It will be tough for the Treasury to attract more offshore buyers

unless the USD weakens, or interest rates rise enough to make them

irresistible. Or a big drop in the federal deficit reduces the supply of

Treasuries itself.

I doubt we’ll see interest rates move up significantly. I don’t think

the economy could handle it and it would be self-defeating anyway, as

the government deficit would explode because of interest expenses. And

that’s not even taking into account the fact that President Trump would

be freaking out daily.

Based on recent history and political expediency, I’d say the odds of

significant budget deficit reductions are slim and none. That’s

especially true going into an election year. There’s just no way we’re

going to see spending restraint or tax increases in the next couple of

years. Indeed, the supply of Treasuries will keep growing even if the US

economy grows too. If there is any sort of significant slowdown or

recession the Federal deficit will explode and so will the new supply of

Treasures. Not an easy fix.

Barring new haven demand for US Treasuries, odds are the Fed will

have to keep sopping up excess supply. That means expanding its balance

sheet and, in so doing, effectively increasing the US money supply.

That brings us (finally!) to the “money shot” chart that appears

above. It compares changes in the size of the Fed balance sheet and the

US Dollar Index. To make it readable and allow me to match the scales, I

generated a chart that tracks annual percentage changes.

The chart shows a strong inverse correlation between changes in the

size of the Fed balance sheet and the value of the USD. This is

unsurprising as most transactions that expand the Fed balance sheet also

expand the money supply.

It’s impossible to tell how long the repo market transactions will

continue but, after three months, they aren’t feeling very “temporary”.

To me, it increasingly looks like these market operations are “debt

monetization in drag”.

I don’t know if that’s the Fed’s real intent or just a side effect.

It doesn’t really matter if the funding and money printing continues at

scale. Even if the repo market calms completely, the odds are good we

see some sort of “new QE” start up. Whatever official reason is given

for it; I think it will happen mainly to soak up the excess supply of

Treasuries fiscal deficits are creating.

I don’t blame the FOMC if they’re being disingenuous about it. That’s

their job after all. If you’re a central banker, the LAST thing you’re

going to say is “our government is having trouble finding buyers for its

debt”, especially if its true.

With no prospect of lower deficits and apparent continued reduction

in offshore Treasury holdings, this could develop into long-term

sustained trend. I don’t expect it to move in a straight line, markets

never do. A severe escalation in Mideast tensions or the start of a

serious recession could both generate safe-haven Treasury buying. Money

flows from that would take the pressure off the Fed and would be US

Dollar supportive too.

That said, it seems the US has reached the point where a substantial

increase in its central bank’s balance sheet is inevitable. Both Japan

and the Eurozone have gotten there before the Fed, but it looks like it

won’t be immune.

The Eurozone at least has a “Twin surplus” to help cushion things.

And Japan, considered a basket case economically, had an extremely deep

pool of domestic savings (far deeper than the US) to draw on. Until very

recently, Japan also ran massive Current Account surpluses thanks to

decades of heavy investments overseas by Japanese entities. Those

advantages allowed the ECB and especially the BoJ to massively expand

their balance sheets without generating a huge run up in interest rates

or currency collapse.

I don’t know how far the US Fed can expand its balance sheet before

bond yields start getting away from it. I think pretty far though.

Having the world’s reserve currency is a massive advantage. There is

huge built in demand for US Dollars and US denominated debt. That gives

the Fed some runway if it must keep buying US Treasuries.

Assuming a run on yields doesn’t spoil the party, continued balance

sheet and money supply expansion should put increasing downward pressure

on the US Dollar. I don’t know if we’ll see a move as large as the

mid-2000s but a move down to the low 80s for the USD Index over the

course of two or three years wouldn’t be surprising.

It won’t be a straight-line move. A recession could derail things,

though the bear market on Wall St that would generate would support

bullion. Currency markets tend to be self-correcting over extended

periods. If the USD Index falls enough and there is a bump in US real

interest rates offshore demand for Treasuries should increase again.

The bottom line is that this is, and will continue to be, a very

dynamic system. Even so, I think we’ve reached a major inflection point

for the US currency. The 2000s were pretty good for the gold market and

gold stocks. We started from a much lower base of $300/oz on the gold

price. Starting at a $1200-1300 base this time, I think a price above

$2000/oz is a real possibility over the next year or two.

It’s not hard to extrapolate prices higher than that, but I’m not

looking or hoping for those. I prefer to see a longer, steadier move

that brings traders along rather than freaking them out.

This prediction isn’t a sure thing. Predictions never are. But I

think the probabilities now favor an extended bull run in the gold

price. Assuming stock markets don’t blow up (though I still expect that

correction), gold stocks should put in a leveraged performance much more

impressive than the bullion price itself.

There will be consolidations and corrections along the way, but I

think there will be many gold explorers and developers that rack up

share price gains in the hundreds of percent. That doesn’t mean buying

blindly and never trading. We still need to adjust when a stock gets

overweight and manage risk around major exploration campaigns. The last

few weeks has been a lot more fun in the resource space. I don’t think

the fun’s over yet. Enjoy the ride.

Like any good contrarian, a 10-year bull market makes me alert of

signs of potential trouble. As noted at the start of this editorial, I’m

expecting continues floods of liquidity. That may simply overwhelm

everything else for a while and allow Wall St to keep rallying, come

what may.

That said, a couple of data points recently got my attention. One is

more of a sentiment indicator, seen in the chart below. More than one

wag has joked that the Fed need only worry about Wall St, since the

stock market is the economy now. Turns out there is more than a bit of

truth to that.

The chart shows the US Leading Indicator reading with the level of

the stock market (which is a component of the official Leading

Indicator) removed. As you can see, without Wall St, the indicator

implies zero growth going forward. I’m mainly showing it as evidence of

just how surreal things have become.

The chart above is something to keep an eye on going forward. It

shows weekly State unemployment claims for several major sectors of the

economy. What’s interesting about this chart is that claims have been

climbing rapidly over the past few weeks. Doubly interesting is that the

increase in claims is broad, both within and across several sectors of

the economy.

I take the monthly Non-Farm Payroll number less seriously than most,

because it’s a backward-looking indicator. This move in unemployment

claims looks increasingly like a trend though. It’s now at its highest

level since the Financial Crisis.

It’s not in the danger zone-yet. But its climbing fast. We may need

to start paying more attention to those payroll numbers. If the chart

below isn’t a statistical fluke, we may start seeing negative surprises

in the NFP soon. That won’t hurt the gold price either.

Source and Thanks: https://www.hraadvisory.com/golds-big-picture

Posted by AGORACOM

at 1:55 PM on Thursday, January 9th, 2020

Sponsor: Loncor is a Canadian gold exploration company focused on two projects in the DRC – the Ngayu and North Kivu projects, both have historic gold production. Exploration at the Ngayu project is currently being undertaken by Loncor’s joint venture partner Barrick Gold. The Ngayu project is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

Another year of covering commodities and select junior mining stocks is all but done and dusted.

We’ve seen palladiumprices

more than double those of platinum, its sister metal, on tight supply

and high demand for catalytic converters in gas-powered vehicles, as

smog-belching diesel cars and trucks get phased out to meet tighter air

emissions standards particularly in Europe and China.

Indonesia advanced a 2022 deadline for banning the export of mineral ores, including nickel,

prompting a massive surge in the price of the stainless steel and

electric-vehicle battery ingredient. In September, nickel powered past

$8 a pound, before slipping back to around $6/lb after the resumption of

Indonesian ore exports and weaker demand from the stainless

steel industry.

Palladium and nickel are both in-demand metals for the foreseeable

future, nickel for its use in batteries and stainless steel, and

palladium as an important ingredient of catalytic converters found in

gas-powered/ hybrid vehicles.

Zinc inventories

in February fell to the point where there were less than two days worth

of global consumption locked in London Metal Exchange (LME) warehouses.

The paucity of the metal used to prevent rusting caused prices to spike

to the highest since June 2018.

Gold started off the year around $1,300/oz,

and didn’t do much for the first half on account of higher interest

rates holding prices down. In July though, gold started to run when the

US Federal Reserve reversed course and began cutting interest rates

instead of raising them. The ECB and a number of other central banks

followed suit, wanting to keep interest rates low to try and boost

flagging economic growth.

The yellow metal advanced

to $1,550 in early September due to a combination of factors including

negative real interest rates (always good for gold), a sluggish dollar,

and safe haven demand owing to US tensions with Iran, impeachment,

Brexit fears, etc.

Copper had an off year in 2018 over fears of slowing

Chinese growth and the US-China trade war, but as we at AOTH have

always maintained, the market fundamentals are solid. Over

200 copper mines currently in operation will reach the end of their

productive life before 2035. Most of the low-hanging copper “fruit†has

been picked. New copper mines will be lower-grade and farther afield,

meaning higher capex and production costs.

Although copper prices suffered in the second and third quarter,

things are looking up for the essential base metal needed for plumbing

and wiring, power generation, communications, 5G networks, and electric

vehicles, which use around four times as much copper as a conventional

car or truck.

Energized by a rip-roaring fourth quarter, copper bulls are back on

board. From its 52-week low in August of $2.51/lb, the red metal gained

an impressive 11%, reaching a pinnacle of $2.83/lb Dec. 12, on

expectations of a trade war resolution between the world’s number one

and two economies, and the improved economic growth prospects that would

entail. Copper has risen 7% in December alone.

We pinned our thesis on three key points: 1/ Commodities are

cyclical, and the timing is right to get in now; 2/ The US dollar

is falling, and will likely continue to fall or be range-bound going

forward. A resolution to the trade war between the US and China, and a

looser monetary policy by the Federal Reserve (both of which are likely)

will weigh on the dollar and be good for commodities; 3/ The need for

infrastructure spending is not going to let up.

Close to a year later, our commodities hypothesis rings true. The dollar’s upward march in 2018 (DXY moved from 89 to 97) did stop

in 2019, helping commodities priced in US dollars. The US-China trade

war escalated but as we predicted, there was a resolution – not a

complete trade deal – but enough hope for one, to send copper, the most

important base metal, soaring in recent weeks.

At the beginning of the year, as stock markets bounced back from

their awful fourth-quarter 2018, everyone thought that the US economy

was roaring. We weren’t so sure, and presented evidence of a less

sanguine picture including negative fallout from the trade war with

China and a yield curve inversion which is a very accurate indicator of a

coming recession.

The US Federal Reserve appeared to agree. Worried about low growth,

globally and in the US, the Fed slammed the brakes on the interest rate

hikes it started in 2015, and began lowering them in July, 2019. That

immediately juiced gold and silver. Investors piled into precious metals as an alternative to near-zero or negative-yielding sovereign bonds. Looser monetary policy, check.

In later articles we showed the bullish cases for zinc, nickel and palladium.

The palladium price tripled from the start of 2016 to spring of 2019,

beating gold just under a year ago for the first time in 16 years.

Palladium has been in deficit for eight straight years, because of low

mined output and smoking-hot demand from the auto sector. So far in 2019

it has gained 47%.

Battery companies have been developing nickel-rich batteries in

two of the dominant chemistries for EVs, the nickel-manganese-cobalt

(NMC) battery used in the Chevy Bolt (also the Nissan Leaf and BMW i3)

and the nickel-cobalt-aluminum (NCA) battery manufactured by

Panasonic/Tesla. Added to Indonesia’s on and off export ban, a demand

boost from nickel’s growing use in electric-vehicle batteries, and

dwindling global stockpiles, have helped support nickel prices.

According to the USGS, despite new zinc mines opening in Australia

and Cuba, supply failed to keep up with consumption. Some very large

zinc mines have been depleted and shut down in recent years, with not

enough new mine supply to take their place. As a result, the zinc market

was in deficit in 2018.

Tighter environmental restrictions in China are lessening the amount

smelters can produce. National production of refined zinc in 2018 fell

to just 4.53 million tonnes, the sharpest downturn since 2013. The

result has been a record amount of refined zinc imported by the world’s

largest metals consumer, 715,355t in 2018. The high demand in China has

also pulled a lot of zinc out of LME warehouses.

In October zinc prices hit a four-month high due to falling zinc

stocks – inventories in London Metal Exchange-registered warehouses

plunged to 57,775 tonnes – a smidgen higher than the 50,425t in April,

the lowest since the 1990s, Reuters said.

Tough market for explorers

It’s good to see we were right about so many metal markets.

Regrettably however, the valuations of mineral exploration companies

have yet to follow the prices of the metals they are hunting.

Indeed the junior mining sector has been in a funk since around 2012.

The juniors’ place in the mining food chain is to provide projects to

be turned into mines for larger mining companies whose reserves are

running low. This is becoming a growing problem as all the low-hanging, high-grade deposit fruit has been picked. Such is the case for gold, silver, copper, palladium,

zinc and nickel, all of which are encountering, or will shortly

encounter, supply deficits, amid booming demand for battery metals and

precious metals.

Finding the kind of grades at amounts that will make a mine

profitable usually requires going farther afield or deeper – greatly

adding to costs per ounce or tonne.

Here’s the problem juniors have been facing: At the same time as

investment capital has been pulled out of the mining majors and

mid-tiers – by investors tired of seeing falling or stagnant stock

prices/ red ink balance sheets – there’s been a dearth of speculative

capital flowing into exploration companies.

The ascendance of index funds has also made it harder for juniors to

attract money, because they are too small to be in the funds that these

vehicle track.

According to a 2019 report by PDAC –

the association that puts on the annual mining show in Toronto –

and Oreninc, a junior financing tracker, equity financing in 2018 was

35% less than in 2017 – a decade-low $4.1 billion.

A good chunk of that cash went to marijuana stocks, as dozens of

companies emerged to take advantage of the pot legalization bill passed

by the Canadian federal government. Whereas weed stock IPOs attracted

$491.1 million in investment dollars in 2018, mining IPOs only accounted for $51.6 million, a startling drop from the $830 million in 2017.

That’s a lot of speculative capital pulled out of resource stocks.

However it’s not all gloom and doom, according to TD Securities mining

investment bankers, who say “current market conditions and historical

precedents make them optimistic generalist investors will return in

greater numbers to mining stocks,†Bloomberg reported:

“The current market is reminiscent of the late 90’s and early 2000’s,

[TD Securities’ Deputy Chairman Rick] McCreary says. At the time,

investors had low interest in mining, and companies found it hard to

raise capital. That was followed by waves of consolidation and a mining

bull run. A similar trend may be building as this ‘period of

consolidation’ rolls on.â€

Gold M&A

As far as that goes, mining companies, especially in the gold space,

have realized since the vicious 2012-16 bear market, they have cut as

much as they can and the next step is to bring assets and companies

together. On top of that, the top gold miners are running out of

reserves, and are looking to replace them with high-margin projects that

have the right combination of grade, size and infrastructure.

This explains Barrick combining with South Africa’s Randgold, the Barrick-Newmont joint venture in Nevada,

the fusing of Newmont and Goldcorp, a $1-billion deal for Lundin Mining

to acquire a Brazilian copper-gold mine from Yamana Gold, Newcrest’s

70% purchase of Imperial Metals’ Red Chris mine in British Columbia, and

other recent examples of gold mining M&A.

Among December’s gold deals are Zijin Mining’s cash purchase of

Continental Gold’s Buriticá project in Colombia, for CAD$1.3 billion;

and a $770 million merger between two mid-tier gold miners, Equinox Gold

and Leagold Mining. The latter arrangement will keep the Equinox name

and create a company valued at $1.75 billion with six mines spread

across Brazil, Mexico and the United States.

Junior resource M&A?

The goal of every junior resource investor is for the company(ies)

they are invested in to get bought out, resulting in a 5, 10, even

20-bagger.

The question is, will the current round of mergers and acquisitions

at the major and mid-tier level trickle down to the juniors? PwC appears

hopeful. In its 2019 report ‘Shifting Ground’ the mining consultancy states,

The heightened level of deal activities, most of which have been

in the gold sector, may well spark further moves among intermediate

players seeking to grow into multi-project companies. A new phase of

industry consolidation could pave the way for more exploration and mine

development and boost investor interest and activity.

Another optimistic opinion comes from Tom Palmer, chief operating officer at Newmont, who told the Wall Street Journal that smaller

players are waiting to see what the bigger miners sell once they have

completed their mergers before they start their own M&A.

“Fast forward two or three years, there will be countless more†mergers, he said.

In fact we are already starting to see this happening. Nevada has

witnessed the return of junior gold explorers, and majors, after a lull

in activity between 2012 and 2016. According to an industry report,

exploration in Nevada increased by 15% in 2017, with 19,040 new claims.

The tide has continued to turn in mining’s favor, with 198,337 active

claims as of January, 2019 – 7% more than in 2018.

In 2018 Idaho-based Hecla Mining snapped up Klondex Mines for US$462

million, delivering three more Nevada properties – Fire Creek, Midas and

Hollister – to Hecla’s stable of mines and adding 162,000

gold-equivalent ounces to its annual production.

Also in Nevada, last year Alio Gold paid Rye Patch Gold $128 million

for the Vancouver-based company and its past-producing Florida Canyon

mine.

The 2019 creation of Nevada Gold Mines (the Barrick-Newmont JV) has

piqued the interest of other companies looking to discover and develop

new ounces in the golden state. Major miners with new projects include

AngloGold Ashanti, Coeur Mining and Kinross Gold. For the details read Getchell’s Gold

And for an inspiring story of junior mining success in Canada, look

no further than Great Bear Resources. Working the historic Red Lake gold

camp in Ontario, Great Bear’s drills discovered the “LP Fault Zoneâ€

this past May. That eureka moment, the realization that most of the gold

on its property is structurally controlled, prompted a massive 90,000m

drill program aimed at identifying the parameters. The discovery of

three new gold zones with high-grade intercepts, along with the earlier

nearby Hinge-Dixie Limb discoveries, caught the market’s attention;

within 18 months, Great Bear’s stock catapulted 2,000%.

Conclusion

I firmly believe that 2019 has been a pivotal year for junior mining.

Coming out of 2018’s slump in several commodities, due mostly to the

uncertainty associated with the US-China trade war, this year we saw

very strong performances from gold, silver, copper, palladium, nickel

and zinc – having correctly predicted price corrections for each.

While it’s disappointing not to see a rising tide of junior miner

stock prices to accompany these bullish calls, we continue to believe.

After all, we want to own the cheapest most in demand metals we can

find to reap the maximum coming rewards. That means buying it while it’s

still in the ground.

The fact is junior resource companies – the owners of the world’s

future mines – are on sale. If you like their management teams, their

projects and their plans for 2020, perhaps now is the time to be

acquiring a position.

Posted by AGORACOM

at 10:22 AM on Tuesday, January 7th, 2020

Sponsor: Loncor is a Canadian gold exploration company focused on two projects in the DRC – the Ngayu and North Kivu projects, both have historic gold production. Exploration at the Ngayu project is currently being undertaken by Loncor’s joint venture partner Barrick Gold. The Ngayu project is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

Recent strong price gains are a bullish upside technical ‘breakout’ from recent trading levels, to suggest still more price gains are very likely in the coming weeks and months, or longer

Bullion’s price has benefited from heightened political tensions but also has enjoyed softness in the dollar,

Gold futures on Monday marked their highest settlement since April of 2013, as the killing last week of a top Iranian military commander, Qassem Soleimani, reverberated through financial markets, momentarily upending appetite for assets considered risky and boosting traditional haven assets like gold.

February gold GCG20, +0.23%

on Comex added $16.40, a gain of 1.1%, to settle at $1,568.80 an

ounce, after it briefly touched $1,590.90 in intraday action. The most

active contract saw its highest settlement since April 9, 2013,

according to FactSet data. Gold also rose for a ninth consecutive

session, its longest period of straight gains since an 11-day streak

that ran from December 2018 to January 2019.

March silver SIH20, +0.28%

edged up by 2.8 cents, or 0.2%, to finish at $18.179 an ounce, pulling

back from a high of $18.55, which was the highest intraday level since

late September.

Last week, the most-active gold contract gained 2.3%, its second week

of gains, while silver prices added 1.1%, also landing it higher for

two consecutive weeks.

“History shows that a big spike up in prices amid higher volatility

tends to produce near-term market tops sooner rather than later, after

that initial spike up,†said Jim Wyckoff, senior analyst at Kitco.com.

“That means in the coming days the gold market could put in a

‘near-term’ top that will last for a moderate period of time.â€

“However, for the longer-term investors in gold, it’s important to

note that the recent strong price gains are a bullish upside technical

‘breakout’ from recent trading levels, to suggest still more price gains

are very likely in the coming weeks and months, or longer,†he said in

daily commentary.

On Sunday, the Iraqi parliament passed a nonbinding resolution to

expel American troops in the wake of the U.S. drone strike that killed

Soleimani, leader of the foreign wing of Iran’s Islamic Revolutionary

Guard Corps, on Iraqi soil.

That act has intensified tensions in the Middle East, boosting the

appeal of assets considered safe during global political conflicts.

Trump has threatened harsh sanctions against

Iraq if it expels U.S. troops, and doubled down on earlier comments

threatening to target Iranian cultural sites if Iran strikes back. Iran has said it would no longer honor the 2015 nuclear deal with a group of world powers, which the U.S. backed out of in 2018.

Meanwhile, the benchmark 10-year Treasury yield TMUBMUSD10Y, +0.24% was up at 1.7917%, after tapping a four-week low on Friday after the Iranian military leader’s killing.

Bullion’s price has benefited from heightened political tensions but

also has enjoyed softness in the dollar, which has occurred as investors

shift to Swiss franc USDCHF, +0.3719% and Japanese yen USDJPY, +0.09% amid the potential for political turmoil.

The U.S. ICE Dollar Index DXY, +0.33%,

a measure of the buck against a half-dozen currencies, was down 0.2% at

96.661 and has posted weekly declines in the last two weeks.

A weaker buck can make gold more attractive to buyers using other

currencies, and lower bond yields can also help boost the comparative

appeal of gold against government debt.

“Gold continues its breakout higher as it is now at the highest level

since April 2013,†wrote Peter Boockvar, chief investment officer at

Bleakley Advisory Group, in a Monday research report.

“I remain bullish but caution not to buy it on geopolitical concerns

because as stated they are usually temporary. Buy it instead because the

dollar continues to weaken and real yields continue to fall,†he said.

Among other metals, March copper HGH20, -0.11% added 0.1% to $2.79 a pound. April PLJ20, -0.34% shed 2.4% to $966.20 an ounce, but March palladium PAH20, +0.87%

added 1.7% to $1,989.60 an ounce. Palladium futures notched a record

high, as they’ve done each day so far this year and many times

throughout 2019.

The platinum group markets are “not concerned that recent geopolitical events could derail the global economy and therefore demand for auto catalysts,†analysts at Zaner Metals, wrote in daily note. “Instead, it is apparent that platinum and palladium are being considered as safe haven instruments, with classic physical market fundamentals being pushed to the sidelines.”

Posted by AGORACOM

at 3:32 PM on Monday, December 9th, 2019

Sponsor: Loncor is a Canadian gold exploration company focused on two projects in the DRC – the Ngayu and North Kivu projects. Both projects have historic gold production. Exploration at the Ngayu project is currently being undertaken by Loncor’s joint venture partner Barrick Gold. The Ngayu project is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting the investment criteria of Barrick. Click Here for More Info

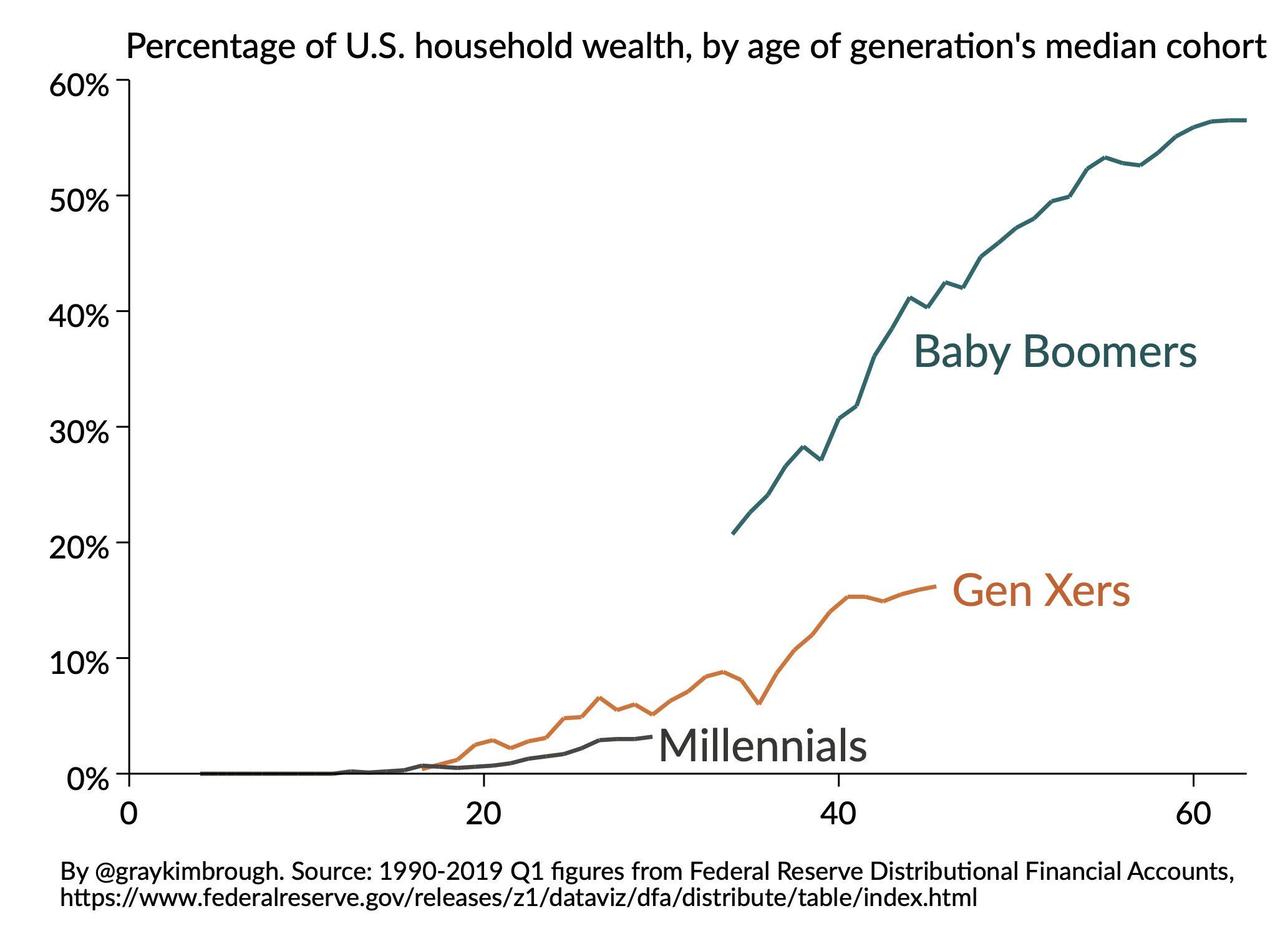

Millennials’ willingness to accept ever-increasing central-planning means gold is the go-to asset to preserve wealth over long-term horizons

Goldman keeps its 3,6 and 12m forecasts at $1,600toz.

“Drop Gold” – the ever-present tagline of Grayscale’s Bitcoin Trust TV commercial – appears to be working its magic on a certain cohort of society.

https://youtu.be/x6B6cj1CIMk

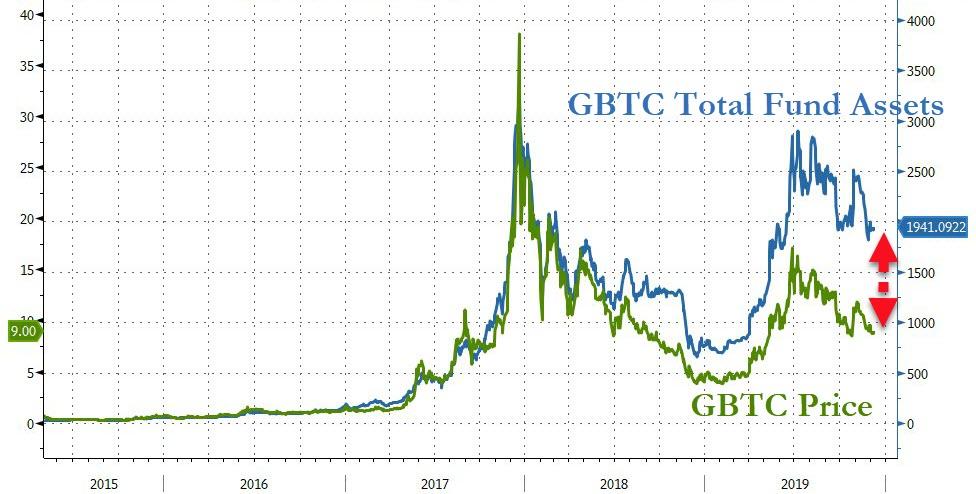

2019 has seen assets under management in GBTC soar…

Source: Bloomberg

And for Millennials, according to the latest data from Charles Schwab, the

Grayscale Bitcoin Trusts is the 5th largest holding in retirement

accounts (including 401(k)s) with almost 2% of their assets tied to the success (or failure) of the largest cryptocurrency.

For now this remains a relatively small number…

But, given the increasing acceptance of socialist policies, and the

historically-ignorant promise of MMT (and don’t forget UBI), Goldman

Sachs suggests that Millennials’ willingness to accept ever-increasing

central-planning means gold is the go-to asset to preserve wealth over

long-term horizons.

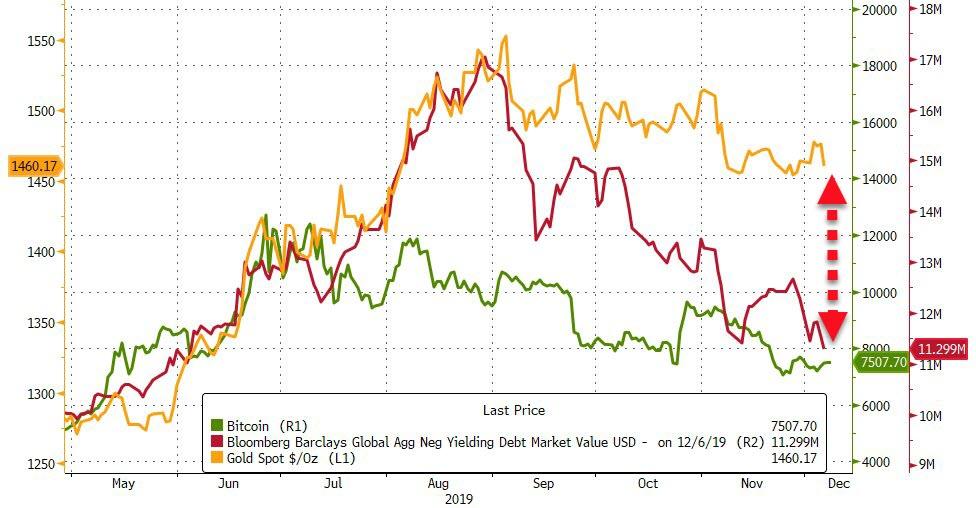

And, at least in the short-term, gold has held its value (relative to

Bitcoin) as the world’s volume of negative-yielding assets has shrunk

on the latest round of optimism that ‘this time is different’…

Source: Bloomberg

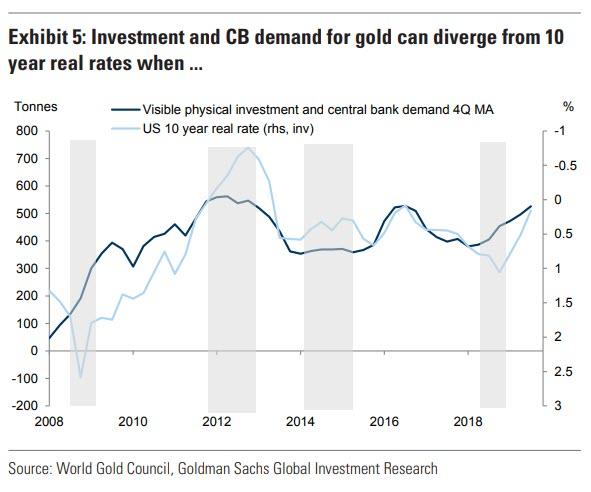

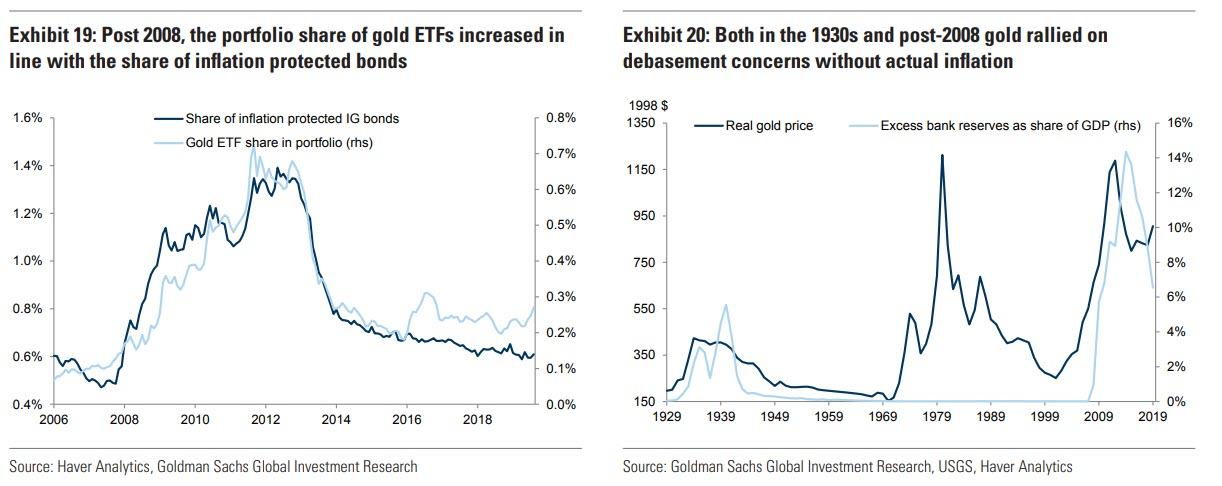

Indeed, Goldman notes that gold looks attractive particularly relative to DM bonds. Both

bonds and gold are defensive assets which go up in value when fear

spikes. Exhibit 5 shows that investment and central bank demand for gold

has been highly correlated with US 10 year real rates.

During the next recession gold may offer better

diversification value to bonds because the latter may be capped by the

lower bound in rates limiting their ability to appreciate materially.

This is particularly relevant for Europe where rates are already close

to the lower bound. This means that during the next recession when fear

spikes, gold may decouple from rates and outperform them.