Posted by AGORACOM

at 11:48 AM on Tuesday, August 4th, 2020

SPONSOR: Candente Gold is creating a growth strategy encompassing its Mexican assets to build a cash flowing business. Recent acquisition of the SDA Plant and the El Dorado Historic Mines is the first step. Their growth strategy is to build a cash flowing business platform and gain access to properties with near surface exploration potential while maintaining El Oro as its flagship asset, and an integral part of the overall growth strategy. El Oro is a district scale gold project encompassing a well-known prolific high-grade gold-silver epithermal vein system in Mexico that has several undeveloped veins and has tremendous exploration potential. Click Here for More Info

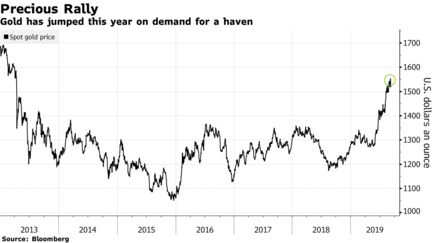

LONDON (Reuters) – Gold’s rally has halted just below $2,000 an ounce partly due to fierce technical resistance, but an eventual break above that level is likely, freeing prices for more record highs, technical analysts said.

The gold price XAU= has surged 30% this year to an all-time peak around $1,975 an ounce and is one of 2020’s best-performing assets.

The rally was driven by a belief that gold will hold its value better than other assets as fallout from COVID-19 ripples through the global economy.

Central bank stimulus has pushed inflation-adjusted U.S. bond yields to record lows, making non-yielding gold more attractive, and the dollar has weakened sharply, making bullion cheaper for buyers with other currencies.

The never-before-reached $2,000-an-ounce mark is a major psychological resistance level, with gold’s 49-year trend channel resting just below it at $1,983, said Commerzbank technical analyst Karen Jones.

Only an end-of-month or, better yet, end-of-quarter close above these levels will signal a break from the channel, she said.

“Tighten your stops … unless the top of my range is taken out in a convincing manner … upside from here is marginal.”

Technical analysts seek patterns and signals in price charts which allow them to predict and interpret moves. Traders and automated trading systems also take prompts from technical signals.

Because gold’s rally has been so fast, a downward correction is likely and could be brutal, analysts said, before the market attempts another stab higher.

Early support is coming in around its 20-day moving average, at $1,875, and the bottom of its 4-month uptrend, around $1,830.

Below that is more powerful support at the 20-week moving average, currently at $1,755, said Tom Pelc, an independent technical analyst formerly at Nomura and RBS.

Such a fall wouldn’t necessarily doom the longer-term uptrend.

“We continue to see this improving volatility backdrop, so there’s no sign that the long-term trend is changing,” said Richard Adcock, a former UBS and now independent technical analyst.

“The market can carry on higher than people expect,” he said.

If resistance is broken, Fibonacci extensions offer short-term targets. These are based on the idea that a rally will extend in predictable proportions extrapolated from a previous rally. One is at $2,067, said Pelc, another comes in at $2,286.

That could only be the beginning of a multi-year move. Lucas ratios — a tool using a sequence of numbers similar to Fibonacci’s — suggest gold could rise to $3,598.80 an ounce in 4-5 years, said Pelc.

Reporting by Peter Hobson; Editing by Veronica Brown and Emelia Sithole-Matarise

Posted by AGORACOM

at 1:25 PM on Friday, June 12th, 2020

SPONSOR: Lomiko Metals is focused on the exploration and development of minerals for the new green economy such as lithium and graphite. Lomiko has an option for 100% of the high-grade La Loutre graphite Property, Lac Des Iles Graphite Property and the 100% owned Quatre Milles Graphite Property. Lomiko is uniquely poised to supply the growing EV battery market. Click Here For More Information

These trials will help steer business investment decisions in future years

The benefits from trials so far include:

Health and safety improvements for employees underground: EVs are much quieter than diesel vehicles and produce less heat and zero exhaust emissions. “From an operator comfort perspective, EVs are certainly an improvement,â€

Cost savings: EVs can reduce underground ventilation demands and the associated operating and capital expenditure

Environmental benefits: EVs contribute to the reduction of greenhouse gas emissions.

By the end of 2020, Vale hopes to have upward of 20 battery-powered vehicles operating within its North Atlantic operations, according to Alex Mulloy, Mining Engineer within Vale’s Base Metals Technology and Innovation division.

The plan is for the electric vehicles (EVs) to be operating on a trial basis at its Creighton, Coleman, Copper Cliff, Garson and Thompson mines by the end of the year, with the company having already made significant headway on achieving this goal.

Mulloy said the green vehicles are going to be evaluated with feedback from operations, as well as operating data, to help Vale understand how they perform in terms of reliability, functionality and the benefits they can offer our people and the business.

The benefits from trials so far include:

Health and safety improvements for our employees underground: EVs are much quieter than diesel vehicles and produce less heat and zero exhaust emissions. “From an operator comfort perspective, EVs are certainly an improvement,†Mulloy said;

Cost savings: EVs can reduce underground ventilation demands and the associated operating and capital expenditure; and

Environmental benefits: EVs contribute to the reduction of greenhouse gas emissions.

“EVs certainly complement the efforts of the business in terms of greenhouse gas and carbon reduction,†Mulloy said. “It’s a great technology. Not only does it enable operational benefit and improvement, it also contributes to our greater goals of reducing our emissions and the impact on the environment.â€

Natalie Kari, Principal Engineer, Strategic Electric Vehicle Implementation, said: “Exhaust emissions from diesel engines are one of the larger contributors to environmental pollution. EVs are an opportunity to increase safety by improving operating conditions and creating a safe work environment. Reducing noise, vibrations, heat, greenhouse gas emissions, and diesel particulate matter, while improving air quality, contributes to creating an attractive work environment for top talent.

“With increased challenging mine conditions at depth, EVs also provide an opportunity to sustain productivity by enabling mines to produce in areas that otherwise may not be feasible without these benefits, contributing towards mining for years to come.â€

These trials will help steer business investment decisions in future years, according to Mulloy.

“Over the coming months, a number of large prime mover vehicles will be delivered,†he said. “When those vehicles arrive, it will be an exciting step in the journey because most of the question marks around the performance of EVs relate to the large vehicles, so that’ll be a chance for us to really put this technology to the test.â€

Kari added: “Our company’s next major steps include collaborating with internal and external industry stakeholders towards safe implementation, comprehensive trial data collection and validation of a robust model towards a final approved five-year implementation strategy. With any new technology, investment in our people will be a priority to ensure they are equipped with the tools necessary for successful operation and maintenance.

“It is thrilling to be a part of leading this effort in a time of increased innovation and environmental awareness,†she continued. “The movement from traditional diesel to electric vehicle brings a feeling of social pride in creating a healthier workplace.â€

Posted by AGORACOM-JC

at 4:32 PM on Friday, February 28th, 2020

AGORACOM Clients Attending PDAC 2020

THEREGAL PROJECT

B.C.’s Next Premier

Silver, Lead, Zinc, Copper Deposit?

Affinity Metals holds under option, a 100% interest in the Project, located within the northern end of the prolific Kootenay Arc, a highly prospective mineralized trend.

Treaty Creeks’ GOLDSTORM zone hosts a conceptual volume of ONE BILLION TONNES rock grading close to one gram per tonne gold and is open to the north, east, and at depth. Â

A major drill program is being planned for spring to develop a resource calculation. The focus has been on the gold enriched Goldstorm Zone which is on trend with, and part of, the same geological system as Seabridge Gold’s neighboring KSM deposits.

American Creek been selected to do a formal presentation at the conference. The presentation will be held on Tuesday, March 5 at 2:00PM in room #802

HPQ Silicon Resources designs, develops, manufactures and commercializes plasma base processes

The innovative PUREVAP “Quartz Reduction Reactors†(QRR), will permit the One Step transformation of Quartz (SiO2) into High Purity Silicon (Si) at prices that will promote considerable renewable energy potential.

Lomiko hosts high-grade graphite at its La Loutre Property in Quebec. The company is working toward a Pre-Economic Assessment (PEA) that will increase its current indicated resource of 4.1 Mt of 6.5% Cg to over 10 Mt of 10%+ Cg in order to supply and develop graphite materials for the green economy.

Posted by AGORACOM-JC

at 9:36 AM on Wednesday, October 23rd, 2019

When the Wall Street Journal calls your Gold Report “The Gold Standard Of Gold Research”, it is safe to say you are a global influencer and expert in all things gold.

This is Ronnie Stoeferle, whose “In Gold We Trust” report has also been downloaded 1.8 million times in English, German and Mandarin in case anyone had any doubt as to his expertise.

Today, Ronnie became the founding member of the Affinity Metals (AFF:TSXV) Advisory Board, which implies that we can expect others to be appointed as well. Why would Ronnie join a company with a market cap under $5,000,000? You’ll have to watch the interview to find out … but here are a couple of hints:

1. Affinity Metals flagship project, the Regal, has reported HISTORICAL reserves of 590,703 tonnes grading 71.6 grams per tonne silver, 2.66 per cent lead, 1.26 per cent zinc, 1.1 per cent copper, 0.13 per cent tin and 0.015 per cent tungsten. These were prepated prior to 43-101 standards and should not be relied upon until they are brought into compliance with 43-101 standards.

2. A Technical Report, which was prepared in 1971 using a silver price of $1.75 per troy ounce, makes a positive recommendation for production, including the establishment of a 500 ton per day concentrator with a 400 ton per day silver, lead and zinc circuit and a 100 ton per day tin, tungsten and copper circuit.

These are just 2 factors that led Ronnie to declare that Affnity Metals is “one of the largest investments in my private portfolio”.

Grab your favourite beverage, kick back and watch this great interview with both Ronnie and Affinity CEO, Rob Edwards.

Posted by AGORACOM

at 10:10 AM on Thursday, October 10th, 2019

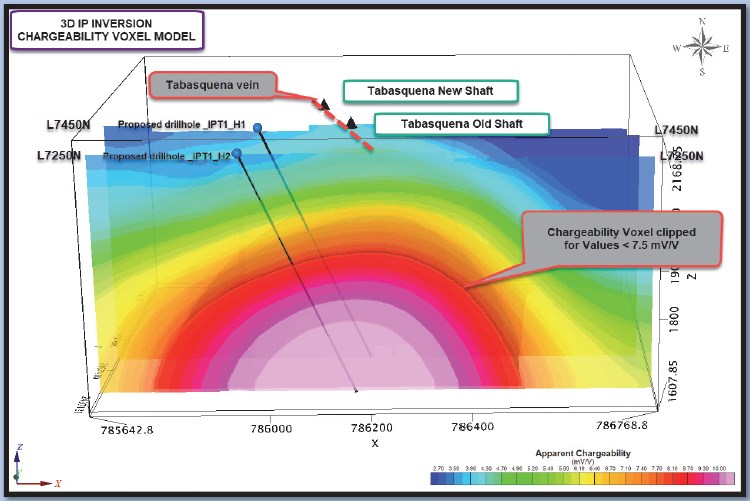

Previous drilling found a network of veins with widespread gold and silver mineralization.

The first phase geophysical survey revealed a large chargeability anomaly right below these veins.

The anomaly is quite large, allowing AAX to expand the grid to the south with fewer lines so we expect to complete this survey within 2 weeks and then begin drilling

12 miles to the west is the San Nicolas VMS mine owned by Teck Corporation and 12 miles to the south is the El Coronel open pit gold mine located in the same geological environment as the Tabasquena project.

Kamloops, British Columbia–(Newsfile Corp. – October 10, 2019) – Advance Gold Corp. (TSXV: AAX) (“Advance Gold” or “the Company”) is

pleased to announce that the second phase of geophysics is underway on

the Company’s Tabasquena project in Zacatecas, Mexico. The goal of this

second 3D induced polarization (IP) survey is to expand the grid

completed in the first phase to the south where the anomaly comes

closest to surface.

The

first phase survey identified a large continuous chargeability anomaly

just below an area of widespread gold and silver mineralization in

epithermal veins. The anomaly is approximately 250 metres wide and 800

metres long from north to south. The second phase IP survey will extend

the grid approximately 1000 metres to the south where due to the

elevation change the anomaly is closest to surface. The chargeability

anomaly remains open to the north, south and at depth.

An

IP survey is a geophysical imaging technique used to identify the

electrical chargeability of subsurface materials such as ore. The

technique involves the measurement of the slow decay of voltage in the

ground following the cessation of an excitation current. The method

makes use of the capacitive action of the subsurface to locate zones

where chargeable minerals are present. Disseminated sulphides and other

chargeable minerals have distinct IP signatures.

It is important to note that approximately 12 miles to the west is the San Nicolas VMS mine owned by Teck Corporation and 12 miles to the south is the El Coronel open pit gold mine located in the same geological environment as the Tabasquena project.

Allan Barry Laboucan, President and CEO of Advance Gold Corp. commented: “It’s

a very exciting time for Advance Gold, previous drilling found a

network of veins with widespread gold and silver mineralization.

Following this the first phase geophysical survey revealed a large

chargeability anomaly right below these veins. Another impressive aspect

of the first IP survey is that as we move to the south there is a

decrease in the depth to the IP anomaly that would indicate that the

anomaly is getting nearer to the surface as we move to the south. A

possible reason for this is that the elevation decreases as we go

southward, so it is important for us to extend the IP grid to the south

before we drill test the IP anomaly. In our recent news release

announcing the addition of our geophysical advisor, he described the

anomaly as ‘quite remarkable in its size and continuity.’ As the anomaly

is quite large, we are able to expand the grid to the south with fewer

lines so we expect to complete this survey within 2 weeks and then begin

drilling. We are in a region with very large mines, including El

Coronel which is an open pit mine in production since 2008 which is 12

miles to the south of Tabasquena. Our team looks forward to further

advancing the Tabasquena project with the second phase of geophysics and

upcoming drilling.”

Julio

Pinto Linares is a QP, Doctor in Geological Sciences with specialty in

Economic Geology and Qualified Professional No. 01365 by MMSA., and QP

for Advance Gold and is the qualified person as defined by National

Instrument 43-101 and he has read and approved the accuracy of technical

information contained in this news release.

About Advance Gold Corp. (AAX.V)

Advance

Gold is a TSX-V listed junior exploration company focused on acquiring

and exploring mineral properties containing precious metals. The Company

acquired a 100% interest in the Tabasquena Silver Mine in Zacatecas,

Mexico in 2017, and the Venaditas project, also in Zacatecas state, in

April 2018.

The

Tabasquena project is located near the Milagros silver mine near the

city of Ojocaliente, Mexico. Benefits at Tabasquena include road access

to the claims, power to the claims, a 100-metre underground shaft and

underground workings, plus it is a fully permitted mine.

Venaditas

is well located adjacent to Teck’s San Nicolas mine, a VMS deposit, and

it is approximately 11km to the east of the Tabasquena project, along a

paved road.

In

addition, Advance Gold holds a 13.23% interest on strategic claims in

the Liranda Corridor in Kenya, East Africa. The remaining 86.77% of the

Kakamega project is held by Barrick Gold Corporation.

For further information, please contact:

Allan Barry Laboucan, President and CEO Phone (604) 505-4753 www.advancegold.ca

Posted by AGORACOM

at 1:52 PM on Thursday, October 3rd, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

Recession fears are once again gripping financial markets and

pushing gold prices higher as sentiment within the U.S. service sector

fell more than expected, according to the latest data from the

Institute for Supply Management (ISM).

Thursday, the ISM said its nonmanufacturing index showed a reading

of 52.6% for September, down from August’s reading of 56.4%. The data

was much weaker than expected as consensus forecasts were calling for a

reading of 55.1%.

According to reports this is the lowest reading in three years.

Readings above 50% in such diffusion indexes are seen as a sign of

economic growth, and vice-versa. The farther an indicator is above or

below 50%, the greater or smaller the rate of change.

Ahead of the report, the gold market was holding its own above

$1,500 an ounce, recovering from a 2% selloff at the start of the week.

The latest economic data has added to gold’s gains. December gold

futures last traded at $1,518.80 an ounce, up 0.72% on the day.

Economists and analysts warned that disappointing service sector

data could boost recession fears as this is the largest component of

the U.S. economy.

The nonmanufacturing data comes just two days after the ISM said

that its manufacturing index fell even further into contraction

territory, also missing economist expectations.

“The non-manufacturing sector pulled back after reflecting strong

growth in August. The respondents are mostly concerned about tariffs,

labor resources and the direction of the economy,†said Anthony Nieves,

chair of the ISM Non-Manufacturing Business Survey Committee.

Looking at the components of the report, the Business Activity Index

dropped to a reading of 55.2%, down from August’s level of 61.5%.

The labor market also lost some momentum in September, with the

Employment Index falling to 50.4%, down from August’s level of 53.1%.

This indicator is closely watched by economists as it is used as a

predictor for Friday’s nonfarm employment report.

Some economists have noted that the miss in the ISM employment data points to downside risk to Friday’s employment report.

Posted by AGORACOM

at 9:19 AM on Wednesday, September 18th, 2019

Kamloops, British Columbia–(Newsfile Corp. – September 18, 2019) –

Advance Gold Corp. (TSXV: AAX) (“Advance Gold” or “the Company”) is

pleased to provide an exploration update on its Tabasquena gold and

silver project in Zacatecas, Mexico. To date, 10 drill holes have been

completed hitting widespread gold and silver mineralization in near

surface epithermal veins. Recently, a 3D induced polarization (IP)

survey was completed that identified a significant continuous

chargeability anomaly, with an east-west width of approximately 250

metres and an apparent strike length of over 800 metres. This anomaly is

located directly below the Tabasquena vein. The anomaly remains open

to the north and to the south and at depth. A second phase 3D IP

geophysical survey is scheduled to begin in the first week of October to

extend the grid to the south.

The purpose of the extended grid to

the south will be threefold, firstly it will establish the continuity

of the anomaly to the south, secondly whether or not the target anomaly

becomes shallower and lastly it will assist in positioning the upcoming

drill hole locations. It is planned to commence drilling once the IP

survey has been completed.

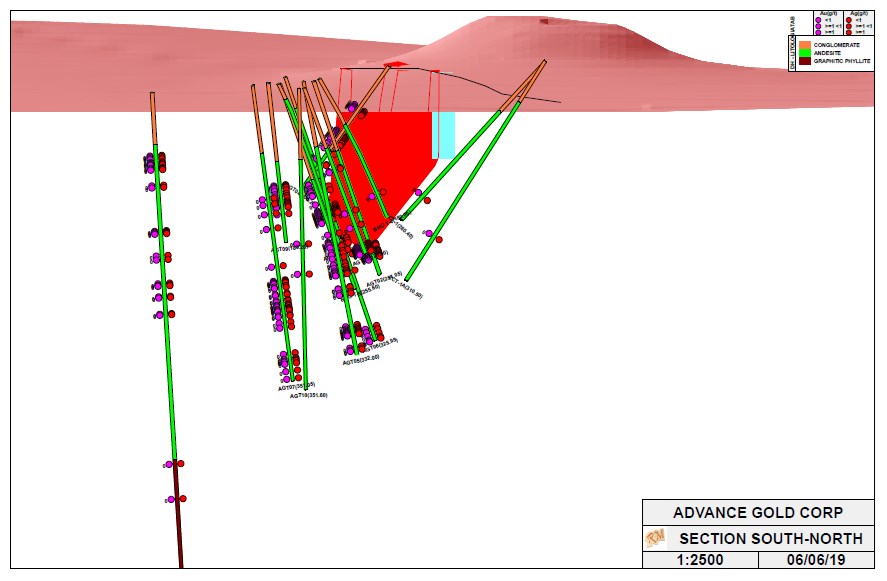

Images shown below are a 3D model of

the epithermal veins hit in previous drilling and a voxel inversion

model showing the extent of the large chargeability anomaly for lines

L7450N and L7250N. These two diagrams are an excellent representation of

the emerging targets at Tabasquena.

The black line at the surface

of the 3D model of drill holes is the surface projection of the

Tabasquena vein. The red shaded area is the historical mining done by

Penoles. The chargeability anomaly is approximately 250 metres below the

historical mining, and it follows the strike direction of the

Tabasquena vein. The epithermal veins, with highlighted widespread gold

and silver mineralization, are above and slightly to the west of the

deeper chargeability anomaly.

Allan Barry Laboucan, President and CEO of Advance Gold Corp., commented: “Our

exploration efforts at Tabasquena are coming together nicely with the

past drilling and the recent IP geophysical survey. It is important to

point out, the IP survey is meant to reveal sulphides through

chargeability. The epithermal veins are low sulphidation and relatively

small and don’t show up well in the IP survey, however right below these

veins is the large continuous chargeability anomaly of over 800 metres

from north to south and approximately 250 metres from east to west.

Before starting our next round of drilling, we wanted to extend the IP

grid to the south, where the anomaly is closer to surface. There is a

significant elevation change of approximately 300 metres from the

northernmost line of the geophysical survey to the most southerly one.

We have approximately 1500 metres to the southern limits of our claims.

The chargeability anomaly is open to the north, but due to the higher

elevation and more cover it exceeds the depth limits of the IP survey.

We are very excited to extend the grid to the south as that is the

direction of the highest intensity of the chargeability and where it

becomes closest to surface. The combination of the quality of Tabasquena

and our various projects, our low share count and a tight share

structure, with substantial insider ownership and tiny valuation, puts

us in a unique position relative to our exploration focused peers as the

market for gold and silver are gaining strength.”

Julio Pinto

Linares is a QP, Doctor in Geological Sciences with specialty in

Economic Geology and Qualified Professional No. 01365 by MMSA., and QP

for Advance Gold and is the qualified person as defined by National

Instrument 43-101 and he has read and approved the accuracy of technical

information contained in this news release.

About Advance Gold Corp. (AAX.V)

Advance

Gold is a TSX-V listed junior exploration company focused on acquiring

and exploring mineral properties containing precious metals. The Company

acquired a 100% interest in the Tabasquena Silver Mine in Zacatecas,

Mexico in 2017, and the Venaditas project, also in Zacatecas state, in

April, 2018.

The Tabasquena project is located near the Milagros

silver mine near the city of Ojocaliente, Mexico. Benefits at Tabasquena

include road access to the claims, power to the claims, a 100-metre

underground shaft and underground workings, plus it is a fully permitted

mine.

Venaditas is well located adjacent to Teck’s San Nicolas

mine, a VMS deposit, and it is approximately 11km to the east of the

Tabasquena project, along a paved road.

In addition, Advance Gold

holds a 13.23% interest on strategic claims in the Liranda Corridor in

Kenya, East Africa. The remaining 86.77% of the Kakamega project is held

by Barrick Gold Corporation.

Posted by AGORACOM

at 2:11 PM on Thursday, September 12th, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

Diversify Well To Protect Oneself Against The Coming ‘Paradigm Shift’

The most important forces that now exist are:

1) The End of the Long-Term Debt Cycle (When Central Banks Are No Longer Effective) +

2) The Large Wealth Gap and Political Polarity +

3) A Rising World Power Challenging an Existing World Power = The Bond Blow-Off, Rising Gold Prices, and the Late 1930s Analogue

In other words now 1) central banks have limited ability to stimulate, 2) there is large wealth and political polarity and 3) there is a conflict between China as a rising power and the US as an existing world power.

If/when

there is an economic downturn, that will produce serious problems in

ways that are analogous to the ways that the confluence of those three

influences produced serious problems in the late 1930s.

Before I get into the meat of what I hope to convey, I will repeat my

simple timeless and universal template for understanding and

anticipating what is happening in the economy and markets.

My Template

There are four important influences that drive economies and markets:

Productivity

The short-term debt/business cycle

The long-term debt cycle

Politics (within countries and between countries).

There are three equilibriums:

Debt growth is in line with the income growth required to service the debt,

The economy’s operating rate is neither too high (because that will

produce unacceptable inflation and inefficiencies) nor too low (because

economically depressed levels of activity will produce unacceptable pain

and political changes), and

The projected returns of cash are below the projected returns of

bonds, which are below the projected returns of equities and the

projected returns of other “risky assets.â€

And there are two levers that the government has to try to bring things into equilibrium:

Monetary policy

Fiscal policy

The equilibriums move around in relation to each other to produce

changes in each like a perpetual motion machine, simultaneously trying

to find their equilibrium level. When there are big deviations from one

or more of the equilibriums, the forces and policy levers react in ways

that one can pretty much expect in order to move them toward their

equilibriums.

For example, when growth and inflation fall to lower than the desired

equilibrium levels, central banks will ease monetary policies which

lowers the short-term interest rate relative to expected bond returns,

expected returns on equities, and expected inflation. Expected bond

returns, equity returns, and inflation themselves change in response to

changes in expected conditions (e.g. if expected growth is falling, bond

yields will fall and stock prices will fall).

These price changes happen until debt and spending growth pick up to

shift growth and inflation back toward inflation. And of course all this

affects politics (because political changes will happen if the

equilibriums get too far out of line), which affects fiscal and monetary

policy. More simply and most importantly said, the central bank has the

stimulant which can be injected or withdrawn and cause these things to

change most quickly.

Fiscal policy, which changes taxes and spending in politically

motivated ways, can also be changed to be more stimulative or less

stimulative in response to what is needed but that happens in lagging

and highly inefficient ways.

For a simpler explanation of this template see my 30-minute animated video “How the Economic Machine Works†and for a more comprehensive explanation see my book Understanding the Principles of Big Debt Crises, which is available free as a PDF here or in print on Amazon. Also, to learn more about our extensive debt cycle research, please visit our debt crises research library on Bridgewater.com.

Looking at What Is Happening Now in the Context of That Template

Regarding the above template and where we are now, in my opinion, the most important things that are happening (which last happened in the late 1930s) are

a) we are approaching the ends of both the short-term and long-term

debt cycles in the world’s three major reserve currencies, while

b) the debt and non-debt obligations (e.g. healthcare and

pensions) that are coming at us are larger than the incomes that are

required to fund them,

c) large wealth and political gaps are producing political conflicts

within countries that are characterized by larger and more extreme

levels of internal conflicts between the rich and the poor and between

capitalists and socialists,

d) external politics is driven by the rising of an emerging power

(China) to challenge the existing world power (the US), which is leading

to a more extreme external conflict and will eventually lead to a

change in the world order, and [Ian Bremmer calls this the return of a

bi-polar world but with significant differences in the goals of the

powers—JM]

e) the excess expected returns of bonds is compressing relative to the returns on the cash rates central banks are providing.

As for monetary policy and fiscal policy responses, it seems to me that we

are classically in the late stages of the long-term debt cycle when

central banks’ power to ease in order to reverse an economic downturn is

coming to an end because:

Monetary Policy 1 (i.e. the ability to lower interest rates) doesn’t

work effectively because interest rates get so low that lowering them

enough to stimulate growth doesn’t work well,

Monetary Policy 2 (i.e. printing money and buying financial assets)

doesn’t work well because that doesn’t produce adequate credit in the

real economy (as distinct from credit growth to leverage up investment

assets), so there is “pushing on a string.†That creates the need for…

Monetary Policy 3 (large budget deficits and monetizing of them)

which is problematic especially in this highly politicized and

undisciplined environment.

More specifically, central bank policies will push short-term

and long-term real and nominal interest rates very low and print money

to buy financial assets because they will need to set

short-term interest rates as low as possible due to the large debt and

other obligations (e.g. pensions and healthcare obligations) that are

coming due and because of weakness in the economy and low inflation.

Their hope will be that doing so will drive the expected returns of cash

below the expected returns of bonds, but that won’t work well because:

a) these rates are too close to their floors,

b) there is a weakening in growth and inflation expectations which is also lowering the expected returns of equities,

c) real rates need to go very low because of the large debt and other obligations coming due, and

d) the purchases of financial assets by central banks stays in the

hands of investors rather than trickles down to most of the economy

(which worsens the wealth gap and the populist political responses).

This has happened at a time when investors have become increasingly leveraged long due to the low interest rates and their increased liquidity. As a result we see the market driving down short-term rates while central

banks are also turning more toward long-term interest rate and yield

curve controls, just as they did from the late 1930s through most of the

1940s.

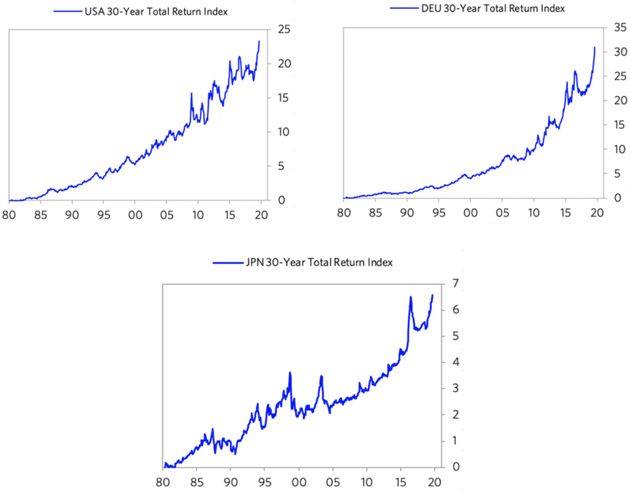

To put this interest rate situation in perspective, see the long-term

debt/interest rate wave in the following chart. As shown below, there

was a big inflationary blow-off that drove interest rates into a

blow-off in 1980–82. During that period, Paul Volcker raised real and

nominal interest rates to what were called the highest levels “since the

birth of Jesus Christ,†which caused the reversal.

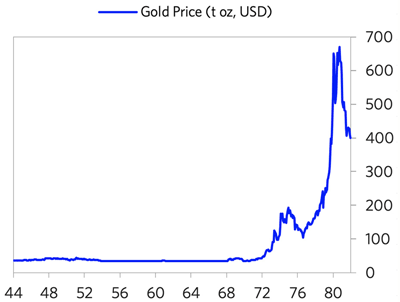

During the period leading into the 1980–82 peak, we saw the blow-off

in gold. The below chart shows the gold price from 1944 (near the end of

the war and the beginning of the Bretton Woods monetary system) into

the 1980–82 period (the end of the inflationary blow-off). Note that the

bull move in gold began in 1971, when the Bretton Woods monetary system

that linked the dollar to gold broke down and was replaced by the

current fiat monetary system. The de-linking of the dollar from gold set

off that big move. During the resulting inflationary/gold

blow-off, there was the big bear move in bonds that reversed with the

extremely tight monetary policies of 1979–82.

Since then, we have had a mirror-like symmetrical reversal (a dis/deflationary blow-off). Look

at the current inflation rates at the current cyclical peaks (i.e. not

much inflation despite the world economy and financial markets being

near a peak and despite all the central banks’ money printing) and

imagine what they will be at the next cyclical lows. That is because there

are strong deflationary forces at work as productive capacity has

increased greatly. These forces are creating the need for extremely

loose monetary policies that are forcing central banks to drive interest

rates to such low levels and will lead to enormous deficits that are

monetized, which is creating the blow-off in bonds that is the

reciprocal of the 1980–82 blow-off in gold. The charts below show the 30-year T-bond returns from that 1980–82 period until now, which highlight the blow-off in bonds.

To understand the current period, I recommend that you understand the

workings of the 1935–45 period closely, which is the last time similar

forces were at work to produce a similar dynamic.

Please understand that I’m not saying that the past is

prologue in an identical way. What I am saying that the basic

cause/effect relationships are analogous:

a) approaching the ends of the short-term and long-term debt cycles, while

b) the internal politics is driven by large wealth and political

gaps, which are producing large internal conflicts between the rich and

the poor and between capitalists and socialists, and

c) the external political conflict that is driven by the rising of an

emerging power to challenge the existing world power, leading to

significant external conflict that eventually leads to a change in the

world order.

As a result, there is a lot to be learned by understanding the mechanics of what happened then (and in other analogous times before then) in order to understand the mechanics of what is happening now.

It is also worth understanding how paradigm shifts work and how to diversify well to protect oneself against them.

by Ray Dalio, Bridgewater Associates, August 28, 2019

Posted by AGORACOM

at 9:45 PM on Tuesday, September 10th, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

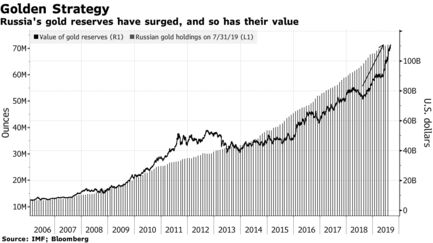

Value of Russia’s gold reserves climbed 42% in the past year

Russia is diversifying from U.S. assets and gold has rallied

Russia’s long-running bet on gold is looking better every month.

The

country quadrupled gold reserves in the past decade as it diversified

away from U.S. assets, a move that has paid off recently as haven demand

sent prices to a six-year high. In the past year, the value of the

nation’s gold jumped 42% to $109.5 billion and the metal now makes up the biggest share of Russia’s total reserves since 2000.

Russia’s central bank has been the largest buyer of gold in

the past few years as President Vladimir Putin seeks to break reliance

on the U.S. dollar as relations between the countries remain strained.

If Russia did need to tap its gold holding, it would fetch a hefty price

— the metal is heading for the best year since 2010 as the U.S.-China

trade war hurts global growth and central banks ease monetary policy.

“Russia

prefers to cushion its macroeconomic stability through politically

neutral tools,†said Vladimir Miklashevsky, a strategist at Danske Bank

A/S in Helsinki. “There is a massive substitution of U.S. dollar assets

by gold — a strategy which has earned billions of dollars for the Bank

of Russia just within several months.â€

More on Russia’s reserves

Russia’s

gold reserves total more than 2,200 tons, the fifth-biggest hoard by

country, and gold now accounts for 20.7% of overall reserves.The value of Russia’s currency reserves are up 9.5% in the past year, lagging the gains seen in bullion.The

central bank bought about 106 tons so far this year, the latest data

show. That’s down 19% from the same period in 2018 but still more than

any other nation.Last year, Russia’s gold buying exceeded its mine supply for the first time.

Russia

isn’t alone in hoarding gold. China, Kazakhstan and Poland have been

among the biggest buyers in the past couple of years, and global

holdings are expected to increase for a while yet.

Not all of Russia’s moves are paying off. Last year, the central bank shifted

about $100 billion of U.S. holdings into euros, yuan and the yen, and

since then the Chinese currency has dropped. Russia also missed out on

the rally in U.S. Treasuries.

Russia may keep buying gold to compensate for those other

losses in its reserves, said Kirill Tremasov, a former Economics

Ministry official and now director of analysis at Loko-Invest in Moscow.

So far it’s working, with gold up 18% this year to $1,513 an ounce.

For

Russia at least, it’s more about diversification than benefiting from

the price. The central bank started buying gold more than a decade ago

as it rallied toward 2011‘s record, and kept adding when prices dropped

in the following few years.

“The central bank is unlikely to have

pursued the goal of earning in the process of managing gold reserves,â€

Dmitry Dolgin, an economist at ING Bank, said by email. “The buying was

rather about diversification of assets

Posted by AGORACOM

at 9:50 AM on Monday, September 9th, 2019

SPONSOR: Advance Gold AAX.v – Advance Gold controls 100% interest in the Tabasquena Silver Mine in Zacatecas, Mexico. A cluster of 30 Epithermal veins have been discovered, with recent emphasis on exploring a large anomaly to drill. Advance also owns 15% of the Kakamega JV attached to Barrick Takeover Offer for Acacia Mining. Click Here For More Info

China has added almost 100 tons of gold to its reserves since it resumed buying in December

People’s Bank of China raised bullion holdings to 62.45 million ounces in August from 62.26 million a month earlier

Terms of Trade is a daily newsletter that untangles a world embroiled in trade wars. Sign up here.Â

China

has added almost 100 tons of gold to its reserves since it resumed

buying in December, with the consistent run of accumulation coming amid a

rally in prices and the drag of the trade war with Washington.

The

People’s Bank of China raised bullion holdings to 62.45 million ounces

in August from 62.26 million a month earlier, according to data on its

website at the weekend. In tonnage terms, August’s inflow was 5.91 tons,

following the addition of about 94 tons in the previous eight months.

Bullion

is near a six-year high as central banks including the Federal Reserve

cut interest rates as signs of a slowdown mount amid the U.S.-China

trade war. Central-bank purchases have been another key support for

prices as authorities from China to Russia accumulate significant

quantities of bullion to help diversify their reserves. That buying

spree likely to persist in the coming years, according to Australia

& New Zealand Banking Group Ltd.

Trade

war restrictions, in the case of China, or sanctions, as with Russia,

give “an incentive for these central banks to diversify,†John Sharma,

an economist at National Australia Bank Ltd., said in an email. “Also,

with increasing political and economic uncertainty prevailing, gold

provides an ideal hedge, and will therefore be sought after by central

banks globally.â€

China

has previously gone long periods without revealing increases in gold

holdings. When the central bank announced a 57% jump in reserves to 53.3

million ounces in mid-2015, it was the first update in six years.

Spot

gold rose 0.2% to $1,510.27 an ounce on Monday. Prices, which capped a

fourth straight monthly gains in August, have risen 18% this year.

Goldman Sachs Group Inc. and BNP Paribas SA are among banks that expect

the metal to challenge $1,600 an ounce within the coming months.

{kind=link}

{kind=link}

{kind=link}

{kind=link}