Posted by AGORACOM-JC

at 7:23 PM on Sunday, June 14th, 2020

ThreeD Capital Inc. (CSE:IDK) is a venture capital firm focused on opportunistic investments in companies in the Junior Resources, Artificial Intelligence and Blockchain sectors. ThreeD seeks to invest in early stage, promising companies and ICOs where it may be the lead investor and can additionally provide investees with advisory services, mentoring and access to the Company’s ecosystem.

Posted by AGORACOM

at 10:31 AM on Tuesday, April 21st, 2020

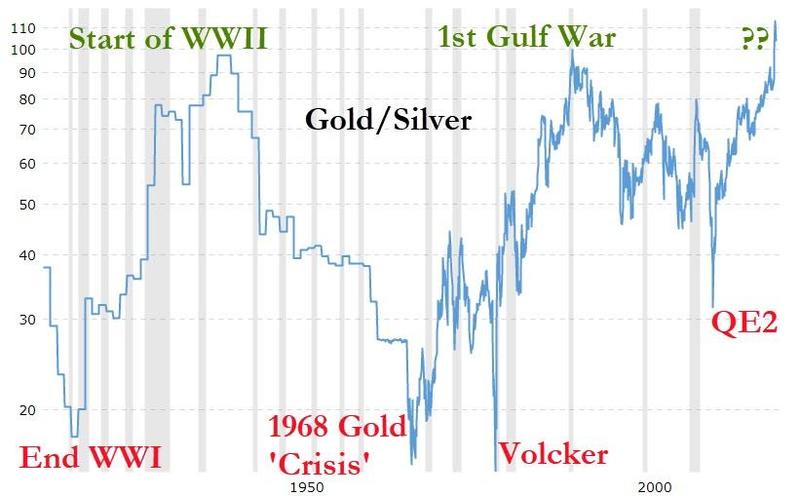

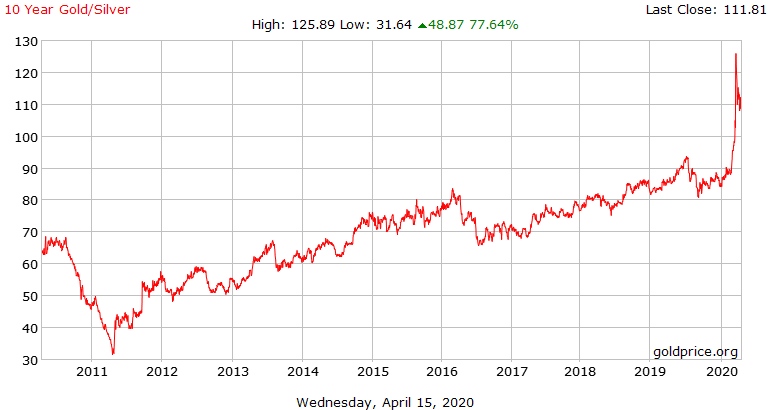

The gold silver ratio has been rising for nine years.

There are many commentators suggesting that the gold silver ratio is nearing a top at present. Here and here are good examples. I am not of that opinion and consider that it will keep climbing for the next 10 years at least. Below is a chart of the gold silver ratio (Source)

As you can see, the chart shows that the gold silver ratio hit a high of 125.89 on the 18th March 2020 and has since declined back to 111.81 (16/4/20). It is likely over time to retest and break the recent highs and then keep on climbing.

The analysis

To understand why the ratio is going to keep on climbing, we need to look at how gold and silver are used.

Silver

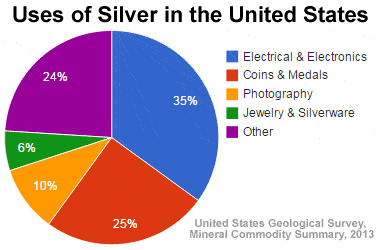

Below is the breakdown of the percentage usage of silver in the US:

As you can see, 45% is used in photography and electrics. The other category (24%) is a mix of energy use, brazing and soldering, chemical production, mirror production and medicine (see link above). In total therefore 69% is used in industry. Only 31% is used in jewelry and coins (silver kept in circulation).

Gold

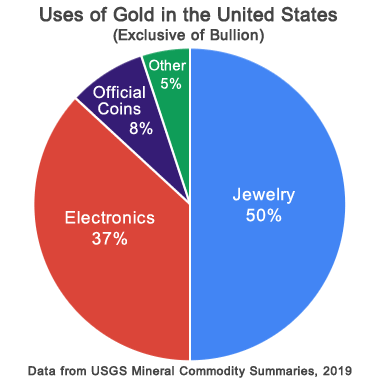

Below is a breakdown of the percentage uses of gold in the US:

Industrial use of gold is only 37%, but 58% is used in coins and jewelry (gold kept in circulation).

Conclusion

As silver is 69% used in industry and gold only 35%, silver is much more sensitive to the strength of the economy than gold is. The last economic cycle in the US was the weakest in modern economic history. Real potential GDP was 1.6% from 2008 to 2018 (Source). This is the lowest 10-year rate since before the Second World War. The gold silver ratio is therefore doing exactly what you would expect it to do in a weak economic backdrop. It is steadily rising. If the economy remains weak after the present recession, I would expect that the gold silver ratio will continue to rise. So will it remain weak?

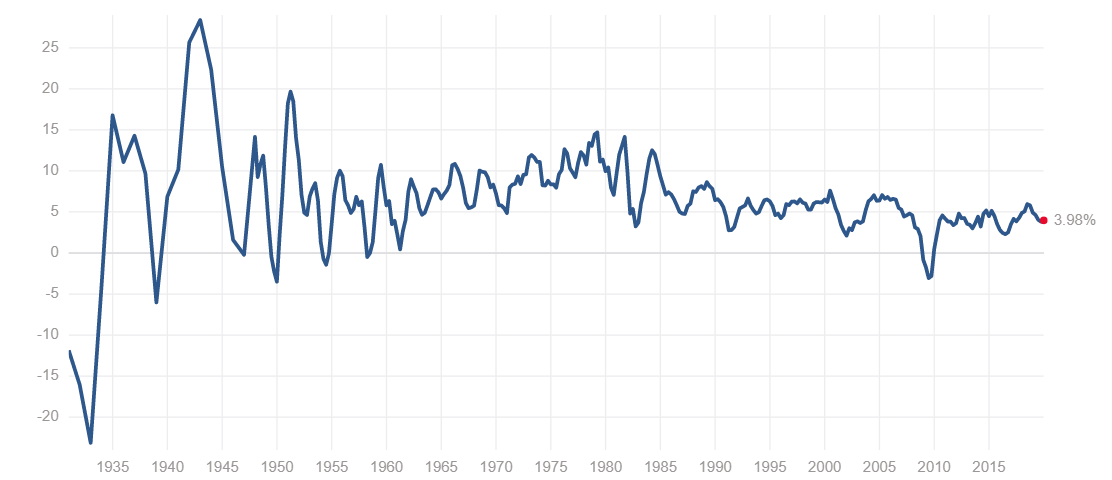

Here is a link to the latest Hoisington Investment Management March report. Their conclusion is that growth and inflation will remain weak, despite the massive money printing and stimulus presently being rolled out by the US government and Federal Reserve. I heartily agree with this analysis. Below is a long-term chart of US GDP:

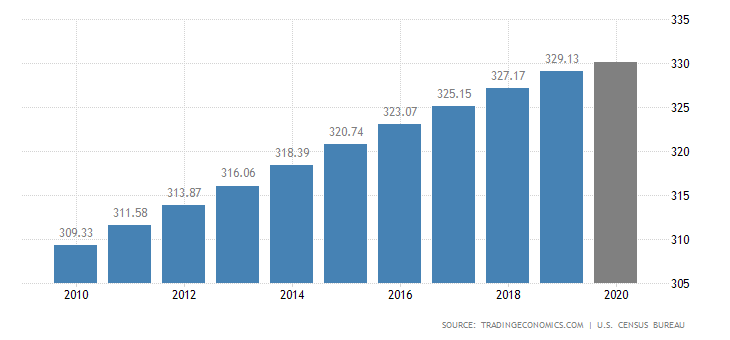

Growth peaked during the second world war and has been steadily falling since then. Since the war, average growth is falling at .7 of a percent every 10 years. As the US government and Federal Reserve are insistent on bailing out all industries and companies, productivity will remain low. This is because the weak companies will not be eliminated, allowing a re-allocation of the capital from the weak to the strong. Below is the population growth of the US economy for the last decade:

The 2019 growth rate was .6 of 1%. With slow population growth and slow productivity growth, the growth rate of the US economy must remain weak. GDP growth is the product of the change in population growth and the change in productivity growth. If both are weak, GDP must remain weak.

Implications

For investment (not trading) purposes, it is clear that if the gold silver ratio keeps climbing, gold will outperform silver on a long-term basis. If you like precious metals to diversify your portfolio, you should buy gold and not silver. It may well be that the gold silver ratio trades lower in the short term and is a good trade, but it is not the way to go if you are an investor. It is also clear that gold miners will outperform silver miners. I presently have no exposure to any silver mining stocks (although some of my gold miners produce silver as a byproduct). Don’t be fooled into thinking that just because the gold silver ratio has hit a high and is now falling that it will mean revert. We are in a low growth environment for the foreseeable future and the ratio will behave accordingly!

Posted by AGORACOM

at 9:16 AM on Thursday, April 16th, 2020

Affinity Metals Corp. (TSXV: AFF) (“Affinity”) (“the Corporation”) is pleased to release assay results from the late fall drill program conducted on the Regal property encompassing 8,800 hectares of the northern end of the prolific Kootenay Arc approximately 25 km northeast of Revelstoke, British Columbia, Canada.

Along with numerous high grade intercepts in multiple holes, a significant new silver discovery was made in the ALLCO area with drill hole #10 intersecting 11.10 meters of 143.29 g/t silver including 0.55 meters of 2612.0 g/t silver. This intersection also carried high grade zinc and lead with some copper.

A total of 1,846.35 meters of diamond drilling was completed with 21 holes being drilled.

The drilling was divided over two separate target areas with 10 holes from two separate drill pads allocated to testing two areas within a graphitic argillite/limestone contact in the ALLCO area. Mineralized intersections encountered within the ALLCO area drill core consisted mostly of argentiferous galena, sphalerite and tetrahedrite hosted within quartz veins and breccias along a northwest-southeast fault that separates the limestones from the argillites.

A further 11 preliminary confirmation holes were drilled from a single drill pad designed to begin testing the underground structure associated with the historic 1971 resource (pre NI43-101 and therefore not compliant) reported for the past producing Regal/Snowflake mines. The Regal mine is located within moderately to gently, westerly dipping, graphitic phyllites/argillites of the lower Index Formation. Mineralization, hosted in quartz veins concordant with host rocks, consists of pyrite, galena, sphalerite, and locally with scheelite (lower levels), stannite (upper levels), and trace chalcopyrite/tetrahedrite throughout. Sulphides occur either as disseminations in the quartz, or as massive pods or bands parallel with slatey partings.

Robert Edwards, CEO of Affinity stated: “We are extremely encouraged to see such positive assay results from the 2019 drilling, our first drill program on the property. Our expectations were that the assays would show strong mineralization given what we have seen from our prior surface sampling program and the historical production grades, but to find this new 11 meter silver zone is truly exciting! These results set the backdrop for our 2020 exploration program which will target not only this new silver discovery but even more importantly, the two very large anomalies identified by the geophysics that may be the core deposits associated with all this surrounding mineralization. 2020 should be a very exciting year for Affinity.”

Significant intervals from the drill program are presented below:

ALLCO

Hole No.

From (m)

To (m)

Interval (m)

Ag g/t

Cu %

Pb %

Zn %

RP-19-01

28.67

29.09

0.42

106.00

0.06

0.33

0.01

RP-19-01

105.00

106.00

1.00

28.72

0.10

0.05

0.09

RP-19-03

48.70

48.77

0.07

171.00

0.05

1.24

0.46

RP-19-04

38.64

41.00

2.36

214.13

0.14

2.60

2.67

including

38.64

40.32

1.68

62.55

0.08

0.25

0.16

and

40.32

41.00

0.68

588.63

0.30

8.41

8.87

RP-19-05

40.25

43.00

2.75

29.74

0.02

0.02

0.01

RP-19-05

44.75

45.51

0.76

50.80

0.02

0.25

1.64

RP-19-05

56.33

56.78

0.45

26.16

0.00

0.89

0.91

RP-19-06

39.26

43.29

4.03

29.53

0.08

0.13

7.38

including

42.00

42.62

0.62

17.90

0.04

0.02

4.12

and

42.62

43.29

0.67

130.00

0.40

0.41

40.14

RP-19-06

49.72

50.57

0.85

129.02

0.03

0.04

0.32

RP-19-07

38.37

39.27

0.90

182.00

0.13

0.30

0.32

RP-19-07

43.70

46.51

2.81

49.21

0.02

0.34

0.78

including

45.10

46.25

1.15

91.92

0.02

0.71

1.68

RP-19-07

56.61

57.42

0.81

98.60

0.01

2.42

2.45

RP-19-08

45.44

45.94

0.50

20.64

0.00

0.46

0.01

RP-19-08

47.84

52.27

4.43

111.96

0.09

0.23

0.29

including

49.24

51.12

1.88

238.20

0.19

0.51

0.50

RP-19-08

57.51

58.52

1.01

45.70

0.00

0.05

0.03

RP-19-08

67.86

68.05

0.19

85.24

0.02

1.21

0.11

RP-19-08

82.46

82.66

0.20

11.39

0.00

0.32

0.01

RP-19-08

84.82

85.02

0.20

568.00

0.55

0.08

0.18

RP-19-09

44.41

46.62

2.21

28.70

0.02

0.15

0.13

RP-19-09

46.62

48.70

2.08

31.70

0.02

0.47

1.12

RP-19-09

48.70

49.76

1.06

6.88

0.00

0.14

0.32

RP-19-10

61.00

72.10

11.10

143.29

0.04

0.62

0.50

including

61.00

67.81

6.81

230.84

0.07

0.94

0.66

including

61.00

61.31

0.31

122.00

0.03

4.18

5.04

and

62.72

63.27

0.55

2612.00

0.66

6.00

2.89

REGAL

Hole No.

From (m)

To (m)

Interval (m)

Ag g/t

Cu %

Pb %

Zn %

RP-19-11

9.14

9.38

0.24

13.24

0.00

0.73

0.03

RP-19-11

11.14

15.79

4.65

12.23

0.00

0.32

0.36

including

15.35

15.79

0.44

52.47

0.00

1.20

2.89

RP-19-11

58.44

59.85

1.41

24.85

0.01

0.77

0.25

RP-19-12

7.32

7.62

0.30

40.02

0.00

0.69

0.02

RP-19-12

11.20

11.80

0.60

39.64

0.00

0.95

0.25

RP-19-12

11.93

13.02

1.09

35.90

0.01

0.89

0.79

RP-19-12

13.80

17.77

3.97

26.00

0.00

0.59

0.25

including

13.8

16.17

2.37

39.78

0.00

0.90

0.30

RP-19-12

60.18

60.70

0.52

12.28

0.00

0.07

0.96

RP-19-13

13.76

17.41

3.65

25.38

0.00

0.58

0.48

including

16.91

17.41

0.50

102.21

0.00

1.87

0.28

RP-19-13

18.57

19.05

0.48

15.44

0.01

0.71

0.22

RP-19-14

10.89

11.18

0.29

60.81

0.02

1.24

1.64

RP-19-14

12.28

12.84

0.56

19.83

0.00

0.25

0.21

RP-19-14

12.99

13.34

0.35

13.28

0.03

0.54

0.47

RP-19-14

13.49

13.82

0.33

20.02

0.00

0.35

0.96

RP-19-14

13.93

14.22

0.29

33.00

0.00

1.32

0.53

RP-19-14

16.04

16.31

0.27

43.86

0.00

1.65

1.01

RP-19-15

14.88

15.38

0.50

12.37

0.00

0.38

0.68

RP-19-16

11.30

11.88

0.58

31.23

0.01

0.91

0.55

RP-19-16

13.07

13.80

0.73

41.88

0.00

0.92

0.46

RP-19-16

14.48

15.32

0.84

23.84

0.00

0.62

0.44

RP-19-16

16.88

17.80

0.92

32.15

0.00

1.40

0.56

RP-19-16

28.13

28.29

0.16

4.99

0.02

0.02

2.21

RP-19-17

7.01

7.16

0.15

1360.00

0.01

19.67

0.21

RP-19-17

10.94

11.69

0.75

62.32

0.00

2.78

0.19

RP-19-17

14.64

15.47

0.83

19.82

0.00

0.52

0.36

RP-19-18

12.12

13.41

1.29

48.31

0.00

2.66

0.53

including

12.12

12.94

0.82

70.50

0.00

4.02

0.53

RP-19-18

15.97

18.53

2.56

13.02

0.00

0.33

1.43

including

15.97

17.41

1.44

12.81

0.01

0.37

2.52

RP-19-18

19.92

20.52

0.60

27.27

0.04

1.15

0.76

RP-19-19

6.00

7.00

1.00

68.42

0.00

2.38

0.22

including

6.00

6.30

0.30

134.00

0.01

7.13

0.13

RP-19-19

12.13

17.68

5.55

13.35

0.00

0.46

0.39

including

15.82

17.68

1.86

30.83

0.00

1.17

0.78

RP-19-19

29.91

30.42

0.51

22.88

0.02

1.22

0.89

RP-19-20

6.15

6.65

0.50

46.47

0.01

1.75

0.13

RP-19-20

7.60

8.32

0.72

33.37

0.00

0.50

0.19

RP-19-20

12.01

12.68

0.67

21.51

0.01

0.67

0.49

RP-19-20

15.27

16.36

1.09

18.63

0.00

0.48

0.43

RP-19-20

17.29

18.68

1.39

10.52

0.00

0.34

0.62

RP-19-20

28.08

31.17

3.09

58.78

0.00

0.35

0.33

including

29.52

30.22

0.70

214.00

0.00

0.34

0.19

RP-19-21

9.05

9.56

0.51

37.45

0.00

0.58

0.02

RP-19-21

12.98

13.82

0.84

17.29

0.01

0.47

0.79

RP-19-21

15.89

17.27

1.38

39.77

0.00

1.55

0.70

including

15.89

16.57

0.68

76.50

0.00

3.07

0.31

and

17.00

17.27

0.27

1.84

0.00

0.06

2.27

RP-19-21

30.40

30.54

0.14

46.83

0.00

0.31

0.16

RP-19-21

31.82

32.82

1.00

61.10

0.01

3.39

1.49

RP-19-21

72.01

72.26

0.25

77.11

0.00

0.62

0.02

Note: True widths are presently unknown.

Additional assay work is presently being conducted regarding Tin results in the drill core. Those results will be released once received and interpreted.

Photo description: Photos of 11.10 meter silver discovery intersection in Hole #10. Host rock is a limestone dissolution breccia/dolomitization breccia with weak to moderate silicification overprinting. Flooding this is milky quartz which hosts wispy veinlets of galena and blebby sphalerite at intersections of these or other veinlets.

As previously reported, the Corporation received assay results for 22 rock samples collected from surface outcrops in September 2019 from the Black Jacket and ALLCO areas of the property. Of the 22 grab samples collected, the majority contained bonanza grade silver, zinc, and lead with many samples reaching assay over-limits. The over-limit results for zinc and lead are reported in the table below (italicized) beside the original assay values. Assay values for tin, including high grade samples 11, 14 and 20 which were over-limit in the original assay report, are also presented in the last column of the table.

Sample Number

Sample Type

Silver g/t

Copper %

Zinc %

Lead %

Gold g/t

Tin ppm

ALC19CR01

grab

0

.035

0

0

0

0.4

ALC19CR02

grab

1300

.415

18.20

>20.0 (35.69)

0.70

46.1

ALC19CR03

grab

120

.232

.034

.984

0.02

2.4

ALC19CR04

grab

131

.089

.026

.102

2.66

1.1

ALC10CR05

grab

16.7

.295

.060

.013

0.09

0.4

ALC19CR06

grab

74.9

.144

>30.00 (34.97)

.059

0.28

2.6

ALC19CR07

grab

10.05

.310

.086

.029

0.04

0.5

ALC19CR08

grab

1870

.495

24.5

>20.0 (31.90)

1.85

189.5

ALC19CR09

grab

88.1

.077

>30.00 (39.98)

1.88

0.08

32

ALC19CR10

grab

1545

.178

26.7

>20.0 (28.67)

0.68

373

ALC19CR11

grab

2360

.366

16.80

>20.0 (43.67)

0.11

900

ALC19CR12

grab

3700

.624

1.645

>20.0 (71.14)

3.14

273

ALC19CR13

grab

964

.716

17.30

17.5

0.11

386

ALC19CR14

grab

3530

.350

1.945

>20.0 (59.54)

1.57

1600

ALC19CR15

grab

3670

.026

1.895

>20.0 (77.01)

0.33

205

ALC19CR16

grab

1790

.107

5.28

>20.0 (52.77)

0.37

146.5

ALC19CR17

grab

751

.069

6.45

18.05

0.45

107

ALC19CR18

grab

1065

.718

.178

.514

0.10

7.6

ALC19CR19

grab

2510

.299

5.58

>20.0 (70.63)

0.06

167

ALC19CR20

grab

4410

2.27

26.40

>20.0 (21.56)

5.68

4500

ALC19CR21

grab

47.5

.177

.048

.092

1.78

8.8

ALC19CR22

grab

87.7

.095

.011

.047

4.79

2.9

Property History & Background

The Regal Project hosts several past producing small-scale historic mines including the Regal Silver.

The property also hosts numerous promising mineral occurrences. From the historic records it appears that most, and perhaps all, of the known mineralized showings/zones have not been previously drilled using modern diamond drilling methods.

The geology of the Regal property generally consists of the Badshot and Lade Peak limestones, and argillites and phyllites of the Index Formation.

Snowflake and Regal Silver (Stannex/Woolsey) Mines

The Snowflake and Regal Silver mines were two former producing mines that operated intermittently during the period 1936-1953. The last significant work on the property took place from 1967-1970, when Stannex Minerals completed 2,450 meters of underground development work and a feasibility study, but did not restart mining operations. In 1982, reported reserves were 590,703 tonnes grading 71.6 grams per tonne silver, 2.66 per cent lead, 1.26 per cent zinc, 1.1 per cent copper, 0.13 per cent tin and 0.015 per cent tungsten (Minfile No. 082N 004 – Prospectus, Gunsteel Resources Inc., April 29, 1986). It should be noted that the above resource and grades, although believed to be reliable, were prepared prior to the adoption of NI43-101 and are not compliant with current standards set out therein for calculating mineral resources or reserves.

ALLCO Silver Mine

The ALLCO Silver Mine is situated 6.35 Kilometers northwest of the above described Snowflake/Regal Mine(s). The ALLCO Silver Mine operated from 1936-1937 and produced 213 tonnes of concentrates containing 11 troy ounces of gold (1.55 g/t), 11,211 troy ounces of silver (1,637 g/t) and 173,159 lbs of lead (36.9%).

Airborne Geophysics to Guide Future Exploration

An extensive airborne geophysics survey conducted by Geotech Ltd of Aurora, Ontario, for Northaven Resources Corp. in 2011, on the Regal Project identified four well defined high potential linear targets correlating with the same structural orientation as the Allco, Snowflake and Regal Silver mines. Northaven also reported that the mineralogy and structural orientation of the Allco, Snowflake and Regal Silver appeared to be similar to that of Huakan’s J&L gold project located to the north, and on a similar geophysical trend line. The J&L is reportedly now one of western Canada’s largest undeveloped gold deposits. Rokmaster Resources Corp. recently optioned the J&L property in a $44.2M deal and has renamed it the Revel Ridge Project. Rokmaster is presently working on expanding the current resource.

After completing the airborne survey, Northaven failed in financing their company and conducting further follow up exploration on the property and subsequently forfeited the claims without any of the follow up work ever being completed. Affinity Metals is in the fortunate position of benefitting from this significant and promising geophysics data and the associated targets.

The aforementioned Northaven airborne geophysical survey conducted at a cost of $319,458.95 in August of 2011 is described in The BC Ministry of Energy, Mines and Petroleum Resources Assessment Report #33054. The results of the survey are competently explained and illustrated by professionals on You Tube at: https://www.youtube.com/watch?v=GX431eBY_t0

Condor Consulting, Inc. who compiled the survey data and produced the original geophysics report was recently retained by Affinity in order to provide more detailed interpretations and potential drill target locations with the aim of testing two of the four main target areas in the future.

Earth Sciences Services Corp. (ESSCO) has also recently provided acoustical geophysics data for portions of the Regal property. This data is also being interpreted and analyzed with respect to future drill targets.

The Corporation is presently in the process of correlating and interpreting all of the historic and new geophysical and geochemical data as well as the 2019 drill results with the objective of further defining 2020 drill targets.

Affinity Metals has been granted a 5 Year Multi-Year-Area-Based (MYAB) exploration permit which includes approval for 51 drill sites.

Assay Procedure, Quality Assurance and Quality Control Procedures

All drill core samples were sent to MSA Laboratories in Langley, British Columbia for assay. Samples were analyzed by the following methods, as appropriate, to determine grades: ICP-130 35 element two acid digestion with ICP-AES finish, IMS-130 51 element two acid digestion with ICP-AES/MS finish, FAS-418 Ag 30g fire assay with gravimetric finish, determination of Ag, Cd, Pb, W, and Zn with four acid digestion and ICP-AES finish, determination of Pb and Zn by titration, and determination of Sn by Sodium Peroxide fusion with ICP-OES finish.

The Company employed a QA/QC program that was managed by a Qualified Person during the entire drill program. Blanks, duplicates (both pulp splits and 1/4 core), and two certified standard reference materials were used. These QA/QC samples were inserted at a rate of 1 every 10 to 15 samples.

Qualified Person

The Qualified Person for the Regal Project for the purposes of National Instrument 43-101 is Frank O’Grady, P.Eng. He has read and approved the scientific and technical information that forms the basis for the disclosure contained in this news release.

About Affinity Metals

Affinity Metals is focused on the acquisition, exploration and development of strategic metal deposits within North America.

The Corporation’s flagship project and present focus is the Regal.

On behalf of the Board of Directors

Robert Edwards, CEO and Director of Affinity Metals Corp.

Posted by AGORACOM

at 8:59 AM on Tuesday, April 14th, 2020

Sponsor: Affinity Metals Corp. (TSX-V: AFF) is a Canadian mineral exploration company building a strong portfolio of mineral projects in North America. The Corporation’s flagship property is the drill ready Regal Property near Revelstoke, BC where Affinity Metals is making preparations for a spring drill program to test two large Z-TEM anomalies. Click Here for More Info

By the mid-6th century BC, Darius the Great was ‘King of Kings’, ruling over the vast Achaemenid Empire.

By that time, gold and silver had already been in use by earlier civilizations for thousands of years.

There are cuneiform tablets that are nearly 4,000 years old from ancient Sumeria which record commercial transactions made in gold and silver.And subsequent civilizations – the Babylonians, Egyptians, Lydians, etc. all used gold or silver in commerce.But Darius had a unique idea. He borrowed the idea of minting gold and silver coins from the Lydians… but then established a fixed exchange rate between the two metals.

Darius decreed that one gold “daric†was worth 13.5 silver coins– one of the first examples in history of a fixed, bimetallic standard.

His idea caught on. And for thousands of years afterward, later civilizations established a fixed gold/silver ratio.

In ancient Greece during the age of Pericles, gold was valued at 14x silver. In ancient Rome, Julius Caesar valued gold at 12x silver.

It remained this way for centuries.

Even in the earliest days of the United States, eighteen centuries after Caesar, The Coinage Act of 1792 established a ratio of 15:1.

(According to the law, one US dollar is supposed to be 24.1 grams of silver, or 1.6 grams of gold. So those pieces of paper in your wallet are not dollars– they are technically “Federal Reserve Notesâ€.)

In modern times there is no longer a fixed ratio between gold and silver, though its long-term average over the last several decades has been between 50:1 and 80:1.

This is a lot higher than in ancient times… but the circumstances are obviously different.

Today, gold is still widely used as a reserve by central banks and governments around the world. And investors still buy gold as a hedge against inflation and uncertainty.

Silver, on the other hand, has countless industrial applications; it’s a critical component in everything from mobile phones to automobiles to solar panels.

Like gold, silver is also a hedge against inflation and uncertainty.

But silver’s demand fundamentals are more heavily influenced by overall economic health. If the economy is in recession, silver prices can fall because there’s less demand from industry.

Gold, on the other hand, doesn’t follow that pattern. In 5 out of the last 6 recessions, in fact, gold has increased in price.

That’s why recessions, and extreme turmoil, can lead to a massive spike in the gold/silver ratio. Gold goes up, and silver stays flat (or falls).

Just prior to World War II as Hitler launched his invasion of Poland, the ratio spiked to 98:1.

In 1991 as the first Gulf War began, the ratio again reached 100:1.

Today we’re back again in that territory; as of this morning, the ratio is 110:1, and it’s been as high as 120 or more in recent weeks

Now, there are very few things about this pandemic that we can be certain about.

Things that were unthinkable even a month ago are now part of our daily lives. And so as I’ve written over and over again, EVERY possible scenario is on the table right now.

But one thing that does seem very clear is that central banks around the world are going to print an extraordinary amount of money.

Many of them already have.

The Federal Reserve in the US, for example, has already expanded its balance sheet to SIX TRILLION DOLLARS.

That’s a nearly 50% increase from last month. And they’re just getting started.

Why does something so mundane as a central bank balance sheet even matter?

Because a rising balance sheet means they’re conjuring trillions of dollars out of thin air to bail everyone out.

This is the way they solve problems: they print money and debase the currency, something that policymakers have been doing for thousands of years.

But you can only get away with doing that a limited number of times before the currency starts to lose value.

We don’t know how long it will last, how much destruction it will cause, or what the world will look like once this is over.

But we can be pretty sure that central banks are going to print a ridiculous amount of money, and that governments will go into a ridiculous amount of debt.

They’ve told us this much. And they’ve already started to do it. So this seems pretty obvious.

The price of gold is up significantly over the last several months, and since the start of this crisis.

But the price of silver has declined… leading to a record-high gold/silver ratio.

This ratio may stay elevated for a while, or even go higher.

But in the past, the ratio has always returned to more traditional levels. Always. Even when the world was facing Adolf Hitler or the Great Depression.

So it stands to reason that, if they keep printing money (which they already are), and the ratio eventually returns to its historical range, the price of silver could really skyrocket.

We’ll spend some time this week talking about some interesting ways to take advantage of this.

Posted by AGORACOM

at 4:04 PM on Monday, April 13th, 2020

Sponsor: Affinity Metals Corp. (TSX-V: AFF) is a Canadian mineral exploration company building a strong portfolio of mineral projects in North America. The Corporation’s flagship property is the drill ready Regal Property near Revelstoke, BC where Affinity Metals is making preparations for a spring drill program to test two large Z-TEM anomalies. Click Here for More Info

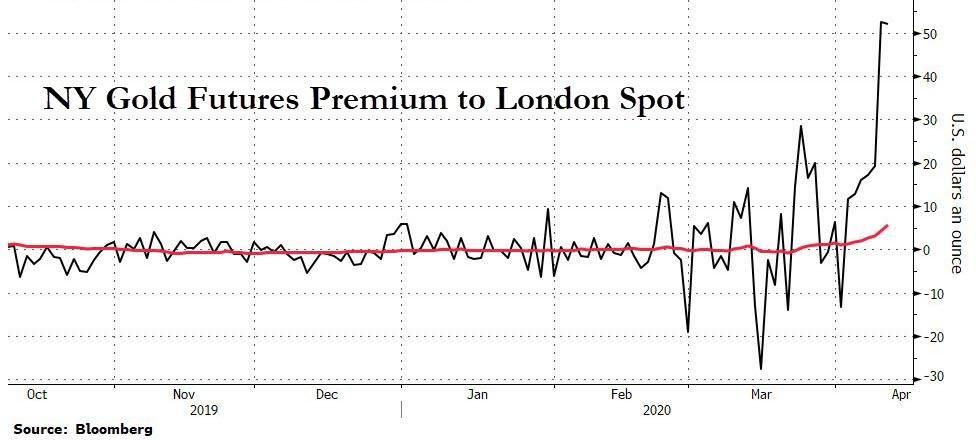

The gaping price differential between spot gold and gold futures that has been plaguing the paper gold markets in London and New York for the last three weeks shows no signs of abating and is continuing to flare up.

In essence, the contango phenomenon we are seeing is one of gold futures prices trading far above spot gold prices, a sign of liquidity problems in the London gold market and a signal that something is completely broken between the world‘s two predominant “gold price discovery” trading venues – which both, by the way, trade paper gold. As a reminder, London LBMA trades unallocated gold over the counter (OTC), a form of synthetic fractional gold derivative. The vast quantities of unallocated gold which are traded in London are then netted and cleared in an electronic clearing engine called Aurum by 5 LBMA bullion banks that comprices London Precious Metals Clearing Limited (LPMCL), namely JP Morgan, HSBC, UBS, Scotia, and ICBC Standard Bank). Allocation of physical gold is a totally separate process beyond clearing in Aurum

COMEX trades predominantly cash-settled gold futures contracts on exchange and facilitates the trading of these contracts bilaterally. COMEX futures are 99.9% cash-settled and even those that result in delivery really result in warehouse warrants changing hands but the gold staying in the New York vaults of JP Morgan, HSBC and Scotia.

That the wide-open spread continues to persist is even more remarkable, despite the best efforts of the London Bullion Market Association (LBMA), CME Group (operator of COMEX) and the powerful London-New York bullion bank syndicate to throw all they have at the problem.

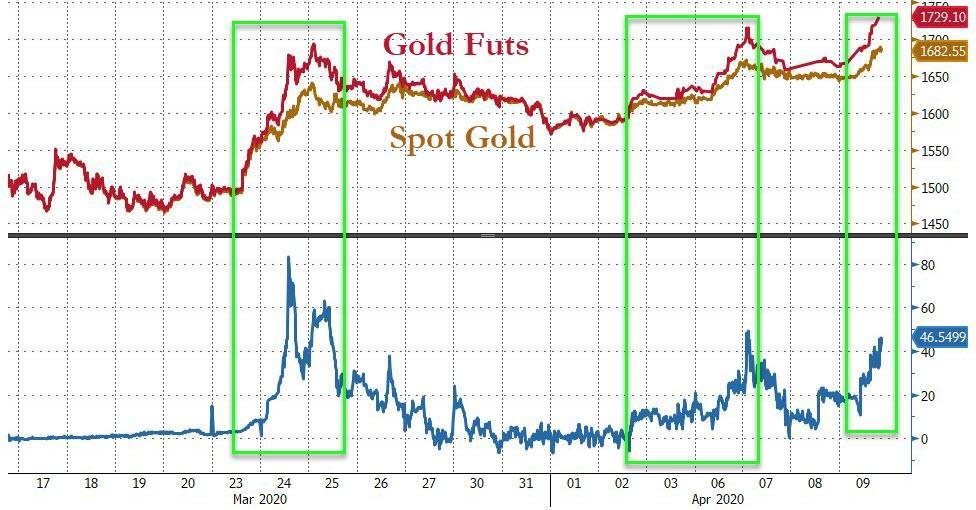

At the time of writing, spot gold was trading at US$ 1696 against US$ 1753 for the front-month (most actively traded) COMEX gold futures contract, a $36 spread with futures over 3.44% over spot. The spread we‘re referring to can be seen in the below 3-day chart, which plots June 2020 gold futures (red and green line) against spot XAUUSD (blue line) from 6 April to 8 April. Notice that over this time the futures price has stayed far above spot, and more importantly, it has persistently done so.

3 day chart of COMEX gold futures price (June 2020) versus LBMA spot gold price, 6 – 9 April 2020. Source:Â www.barchart.com

The spot-futures spread blow out that has been running into its third week now can vividly be seen by zooming out and looking at a similar chart but this time from 24 March until 9 April, the first day that the price spread between London and New York gaped open. Notice the big gaps between futures and spot over 24-25 March, the persistence of the gap over the remainder of the week, and the subsequent re-explosion of the divergence since early April, particularly over the last few days.

Its instructive to review a short timeline of some of the events which have contributed to this ongoing saga over the last three weeks, because it shows that no matter what the LBMA and CME do, the spread between London and COMEX continues to stay out there.

Week 1

23 March – COMEX gold futures (April contract) begin trading noticeably above LBMA bullion bank spot gold prices.

24 March – Spreads between COMEX futures and London spot blew out to $100 at one point during the day, while bid – ask spreads within London spot widened substantially.

24 March – Rumors in the gold market suggested that bullion banks that were required to deliver physical gold for COMEX Exchange for Physical (EFP) transactions failed to do so, suffered losses and exited the market, and that this caused the Spread between COMEX and London to widen substantially.

The bullion bank controlled LBMA releases its first control statement, deflecting attention away from London, saying it will help (essentially collude with) the CME-COMEX in the gold market – The official language is that the LBMA “is working closely with COMEX and other key stakeholders to ensure the efficient running of the global gold market.”

Note – Who are these other key stakeholders, what do they mean by efficient running, and what gives them the right to think they can “run“ the global gold market?

24 March – LBMA and its bullion banks pressure CME to launch a gold futures contract with a deliverable clause in London 400 oz gold bars.

24 March – At end of day, CME announces the launch of a new gold futures contract that can theoretically deliver 400 oz bars, 100 oz bars and kg bars but that uses a fractional paper concept called Accumulated Certificates of Exchange (ACEs) to divide 400 oz deliverable bars into 100 oz bars, and that critically includes all refiner brands on the LBMA Good Delivery List (current and former Good Delivery refiners). This contract will be called 4GC (See here and here).

30 March – CME published its daily gold vault stocks report (for Friday 27 March) with a new category for “400 oz AND eligible brands”, but with all vaults showing zero stocks of 400 oz gold bars. And notably, that the JP Morgan vault in New York had zero holdings.

30 March – When Bullionstar draws attention to this new CME vault report, in “COMEX can’t find a 400 oz bar for its new 400 oz gold futures contract“, the CME then deletes the new report from its website on the morning of 31 March, and replaces it intra-day with a report which reverted to the original version.

1 April – LBMA and CME publish an unprecedented second control statement titled “LBMA and CME group comment on healthy gold stocks in New York and Londonâ€, saying that “CME Group and LBMA..will continue to coordinate efforts as market circumstances evolveâ€. See “LBMA and COMEX try to Reassure the Market – Twice in One Week“ for background.

Note – If LBMA and CME are trading gold bars, why would they need to coordinate efforts, and more importantly, coordinate efforts to what end?

LBMA disingenuously refers to 8326 tonnes of gold in London, a figure that is from 3 months ago, and nearly all of this total tonnage is central bank gold, gold held in ETFs, and allocated gold held by other investors. The real float of physical gold in the london LBMA gold vaults controlled by the LBMA bullion banks is less than 1000 tonnes and some estimates from sources in the bullion banks say it could be between 300 and 500 tonnes.

In the same statement, CME refers to 9.2 million ozs ( 287 tonnes) of gold held in its approved vaults, with irrelevant claims that 5.6 million ozs of this is eligible gold. Eligible gold is gold which just happens to be in the form that satisfies the deliverable unit of the contracts (1 kg bars or 100 oz bars). The rest of this figure is registered gold, which already has warehouse warrants attached.

2 April – The spread between COMEX gold futures prices and London spot gold prices starts to gap up strongly again.

Rest of week – CME Group releases publicly a PowerPoint slide presentation titled “Precious Metals Physical Delivery Processâ€, which includes the new 4GC contract and explains how to get an electronic warrant if standing for delivery of COMEX gold futures contracts, but that explains nothing about withdrawing gold from the COMEX vaults.

The COMEX presentation also features a slide discussing the COMEX New York approved vaults but unbelievably instead of showing photos of one of its approved New York vaults, this slide contains photos of a HSBC gold vault in London showing gold bars belonging to the exchange traded fund, the SPDR Gold Trust (GLD). This GLD gold has nothing to do with COMEX gold vaults in New York (or does it?).

COMEX presentation slide uses photos of a HSBC gold vault in London featuring SPDR Gold Trust gold bars

6 April – The spread between the COMEX June gold futures contract and the LBMA spot gold price blows out again very widely to over $80 at one point in the day.

6 April – CME adds back the category “Enhanced Delivery (400 oz AND eligible brands)” to its New York daily vault report. Of the 9 vaults on the report, 5 have 0 holdings in this 400 oz category, 2 (Brinks & Loomis) have a combined 2 tonnes, HSBC claims 21.5 tonnes, JP Morgan appears for the second time, claiming 126.8 tonnes. The first time being 30 January when JP Morgan was listed as having zero tonnes of 400 oz bars.

Note – “400 oz AND Eligible Brands” will be the subject of another article soon, but for now it means as follows. For the new 4GC contract, CME added all LBMA Good Delivery gold bar Brands (Current and Former) as Eligible brands. That’s 68 brands from the existing GC100 contract + 71 brands from the LBMA current Good Delivery List + another 113 LBMA former Good Delivery List As another aside, where did the JP Morgan New York vault suddenly get 126.8 tonnes of gold suddenly to add to Eligible category for the COMEX 4 GC contract? Was this 126.8 tonnes of gold suddenly shipped in to the JP Morgan vault from London? Hardly. Were 126.8 of London Good Delivery gold bars already sitting in its New York vault. Probably not as its London and not New York which is the center of 400 oz gold bar storage. Was there some type of gold swap involved between London and New York. Possibly.

Another intriguing possibility is that now that former LBMA Good Delivery List gold bars are eligible for the new 400 oz contract, that JP Morgan borrowed Old US Assay Office gold bars from the New York Fed (their two gold vaults are beside each other), and then added these to the Eligible category for the new 4GC gold contract.

Root Cause of Spot vs Futures Gold Price Discrepancy

So what is the cause of this dislocation in pricing between the lower ‘spot’ price and the higher ‘futures’ price, i.e. between the London LBMA gold spot market and the New York COMEX gold futures market? The answer in general is that the problem is with the spot price. And where is the spot price? London.

Ironically, the LBMA bullion banks are trying to shift the attention away from London, when London is exactly where the problem is. The spot price problem appears to be due to liquidity problems of the LBMA market makers in London where they are suspicious of trading with each other. This is despite the fact that these LBMA market makers are obliged to constantly make a market and offer two way price quotations to each other. These market makers are BNP Paribas, Citibank, Goldman Sachs, HSBC, ICBC Standard, JP Morgan Chase, Merrill Lynch, Morgan Stanley, Standard Chartered, Bank of Nova Scotia, Toronto-Dominion and UBS.

The spot price problem has nothing to do with air travel cancellations or shipments of 100 oz gold bars from London to New York. These market makers do not make markets in physical gold. The unit of trading in London is not real gold anyway, its unallocated gold or gold credit which is issued by a bullion bank and which has counterparty risk.

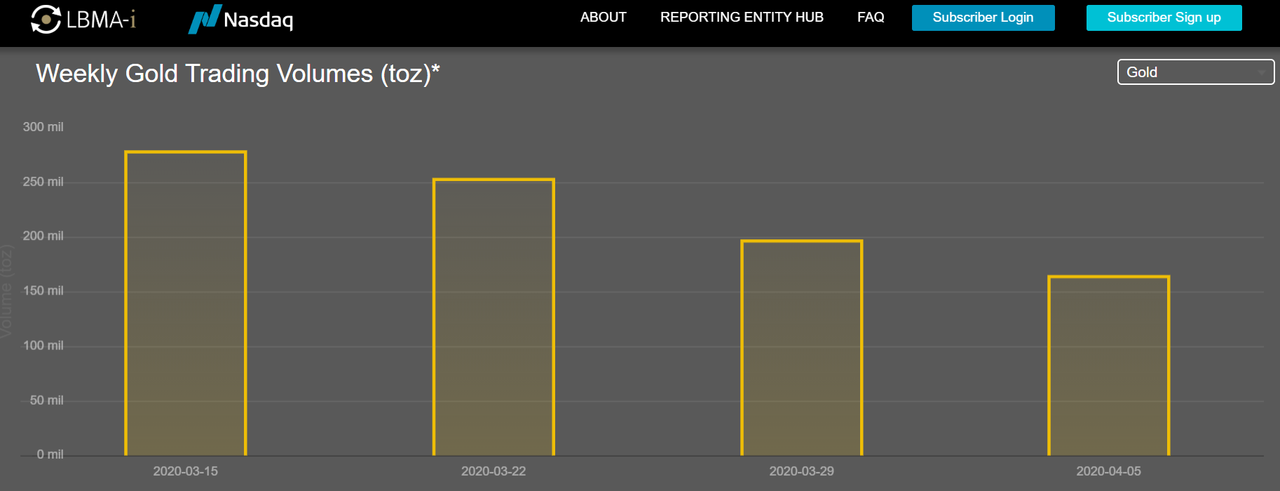

Something has spooked these market makers and caused a drop in liquidity in the London market. These banks, which normally trade with each other, now do not want to trade with each other due to heightened counterparty risk. Unallocated trading volumes in the London gold market have fallen over the last three weeks. See chart below.LBMA – Unallocated gold trading volumes, week-to-week, last 4 weeks to 5th April. Source: www.lbma-i.com

Likewise, according to Bloomberg, COMEX gold futures trading volume last week was 80.6 million ounces, a 72% drop compared to the end of February. From the same Bloomberg article, there is an intriguing and obviously dramatic quote from commodities broker Marex Spectron, saying:

“You have a bunch of shell-shocked market makers who are literally hiding under their desks and do not and possibly can not make markets in any size, shape or form,†said David Govett, head of precious metals trading at Marex Spectron. “Hence we have the lack of liquidity, the small volumes and the wide spreads.â€

Marex is a broker for EFPs, so maybe the LBMA market makers are not answering calls. Then they are failing in their duty and obligations as market makers. But why would market makers not want to trade and how does this relate to EFP spreads? If banks suffered EFP problems and then the EFP spread between London and New York blew up, and then they use the excuse that the EFP spread is too large for them to make a market in spot because they don’t want to take on risk, then that’s just circular logic and a pathetic excuse. But what causes LBMA market makers to become shell shocked and literally hide under their desks?

Could it be that the gold trading activities of some of these LBMA bullion banks have blown up and they have ceased their market making activities, but have not publicly stated this, and covered it up? Stranger things have happened. All the while, as trading volumes continue to fall in the paper gold markets of London and New York, the opposite is the case in physical gold markets, where BullionStar and other bullion dealers – those that continue to have inventory – see unprecedented demand and increasing trading volumes.

Posted by AGORACOM

at 8:26 AM on Wednesday, March 25th, 2020

Loncor has acquired an additional 5.04% interest in its subsidiary Adumbi Mining

Adumbi holds six exploitation licences in the Ngayu Greenstone Belt including the Imbo exploitation licence, where an Inferred Mineral Resource of 1.675 million ounces of gold (20.78 million tonnes grading 2.5 g/t Au

TORONTO, March 25, 2020 (GLOBE NEWSWIRE) — Loncor Resources Inc. (“Loncor” or the “Company“) (TSX: “LN”; OTCQB: “LONCF”) announces that it has acquired an additional 5.04% interest in its subsidiary Adumbi Mining SARL (“Adumbi Holdcoâ€) pursuant to a private transaction with one of the former minority shareholders of Adumbi Holdco.  This acquisition increases Loncor’s interest in Adumbi Holdco from 71.25% to 76.29%. “Loncor continues to consolidate its dominant position in the Ngayu Goldbelt. Over the next twelve months we intend to drill the Adumbi gold deposit and several other highly prospective areas of the Imbo license,†said Founder and CEO, Arnold Kondrat.

Adumbi

Holdco, which recently changed its name from KGL Somituri SARL, holds

six exploitation licences in the Ngayu Greenstone Belt including the

Imbo exploitation licence, where an Inferred Mineral Resource of 1.675

million ounces of gold (20.78 million tonnes grading 2.5 g/t Au,) was

outlined in January 2014 by independent consultants Roscoe Postle

Associates Inc on three separate deposits, Adumbi, Kitenge and Manzako.

76.29% of this gold resource is now attributable to Loncor.

About Loncor Resources Inc. Loncor

is a Canadian gold exploration company focussed on the Ngayu Greenstone

Belt in the Democratic Republic of the Congo (the “DRCâ€).

The Loncor team has over two decades of experience of operating in the

DRC. Ngayu has numerous positive indicators based on the geology,

artisanal activity, encouraging drill results and an existing gold

resource base. The area is 200 kilometres southwest of the Kibali gold

mine, which is operated by Barrick Gold (Congo) SARL (“Barrickâ€).

In 2019, Kibali produced record gold production of 814,000 ounces at

“all-in sustaining costs†of US$693/oz. Barrick has highlighted the

Ngayu Greenstone Belt as an area of particular exploration interest and

is moving towards earning 65% of any discovery in 1,894 km2 of Loncor

ground that they are exploring. As per the joint venture agreement

signed in January 2016, Barrick manages and funds exploration on the

said ground at the Ngayu project until the completion of a

pre-feasibility study on any gold discovery meeting the investment

criteria of Barrick. In a recent announcement Barrick highlighted six

prospective drill targets and are moving towards confirmation drilling

in 2020. Subject to the DRC’s free carried interest requirements,

Barrick would earn 65% of any discovery with Loncor holding the balance

of 35%. Loncor will be required, from that point forward, to fund its

pro-rata share in respect of the discovery in order to maintain its 35%

interest or be diluted.

In

addition to the Barrick JV, certain parcels of land within the Ngayu

project surrounding and including the Makapela and Adumbi deposits have

been retained by Loncor and do not form part of the joint venture with

Barrick. Barrick has certain pre-emptive rights over the Makapela

deposit. Loncor’s Makapela deposit (which is 100%-owned by Loncor) has

an Indicated Mineral Resource of 614,200 ounces of gold (2.20 million

tonnes grading 8.66 g/t Au) and an Inferred Mineral Resource of 549,600

ounces of gold (3.22 million tonnes grading 5.30 g/t Au). Adumbi and

two neighbouring deposits hold an Inferred Mineral Resource of 1.675

million ounces of gold (20.78 million tonnes grading 2.5 g/t Au), with

76.29% of this resource being attributable to Loncor via its 76.29%

interest.

Resolute

Mining Limited (ASX/LSE: “RSG”) owns 25% of the outstanding shares of

Loncor and holds a pre-emptive right to maintain its pro rata equity

ownership interest in Loncor following the completion by Loncor of any

proposed equity offering.

Additional information with respect to Loncor and its projects can be found on Loncor’s website at www.loncor.com.

Qualified Person Peter

N. Cowley, who is President of Loncor and a “qualified person” as such

term is defined in National Instrument 43-101, has reviewed and approved

the technical information in this press release.

Technical Reports Certain

additional information with respect to the Company’s Ngayu project is

contained in the technical report of Venmyn Rand (Pty) Ltd dated May 29,

2012 and entitled “Updated National Instrument 43-101 Independent

Technical Report on the Ngayu Gold Project, Orientale Province,

Democratic Republic of the Congo”. A copy of the said report can be

obtained from SEDAR at www.sedar.com and EDGAR at www.sec.gov.

Posted by AGORACOM

at 3:02 PM on Wednesday, March 11th, 2020

Sponsor: Loncor, a Canadian gold explorer controlling over 2,400,000 high grade ounces outside of a Barrick JV. The Ngayu JV property is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting their Tier One investment criteria. Newmont $NGT$NEM owns 7.8%, Resolute $RSG owns 27% Click Here for More Info

Maurice Jackson of Proven and Probable speaks to Bob Moriarty of

321gold about his thoughts on the current financial markets and

investment opportunity

Excerpt:

Maurice Jackson:……Staying in the Southern Hemisphere, let’s visit the Congo, where you just introduced Loncor Resources (TSX:LN). Sir, who is Loncor Resources, and what is the opportunity they present to the market?

Bob Moriarty: Here’s what’s absolutely amazing, I’m

glad you brought that up. Loncor Resources approached me, I had never

even heard a whisper of the name, I had no clue as to who they were. I

went looking into it, they have an incredibly massive land position, in

the Democratic Republic of Congo, the DRC.

Barrick Gold has several gold mines there, in the Greenstone Belt,

and across the border in Tanzania. Barrick Gold has some of their other

really giant mines. Loncor has, in their wholly owned properties,

resources of about 2.4 million ounces. They’ve got joint venture with

Barrack, on a big piece of their property, like 3000 square kilometers,

which is a really big project. Barrick is funding it to feasibility,

they’re paying everything. Barrick runs the project, and Barrick spends

the money. There are no particular limits on what Barrick can spend,

they can spend anything they want to. They’ve got a drill program that’s

literally starting right now.

If you look at any stock, you want to figure out what the basement

is, what is the lowest price the stock can go to? If you ignored the JV

with Barrick, which would be a foolish thing to do, but if you ignored

it, you’re buying ounces of gold, in the ground, for $19 an ounce, U.S.

So, I don’t think there’s any downside to it. Approximately 70% of

shares are in the top three or four shareholders. I think Loncor

Resources is a great stock, because if you like gold, and I think after

all of the things that I’ve said over the last 15 years, anybody who

doesn’t like gold right now is economically illiterate.

Maurice Jackson: You know, you said that lightly, $19 an ounce.

Bob Moriarty: Yeah, yeah. How can you go wrong? At the stage they’re operating, they should be getting $50 or $60 bucks an ounce.

Now, one of the things that we haven’t gotten into, and we need to

get into is, one, the T-bond, and, two, what I see happening to gold and

gold shares. The T-bond Daily Sentiment Index (DSI), on Friday, hit 98.

That is the highest rating I’ve seen, on the Daily Sentiment Indicator

for any commodity, ever. Therefore, the T-bond’s going to crash, it’s

probably going to take gold with it. Gold had a DSI of 96 a couple of

weeks ago.

Everybody hates it. They act like, “Oh my God, you say that gold’s

going down. My God, I hate you!” The corrections are perfectly normal,

and we’re going to have a correction in gold, and we’re going to have a

correction in palladium, and we’re going to have a correction in

rhodium. We’re going to go into the biggest financial crash in world

history, and most asset classes are going to get sold off. That’s not a

bad thing, that creates opportunity, but you’ve got to be flexible, and

hopefully liquid.

Now, I am not saying, “Go out and sell everything you’ve got.” Every

time I say we’re going to have a correction, “Oh my God, you told me to

sell everything.” Well, that’s not what I said, not at all. I said we’re

going to have a correction. At the end of the correction, gold and

silver and platinum are going to be a lot more valuable. We’re going to

do exactly what we did in 2008. A lot of stocks were down 70% or 80%.

Most of the big ones, the ones that I like, Lion One Metals, Novo Resources, Irving Resources, Barksdale Capital, these stocks are down 30 or 40% since the first of the year, when I said, “Beware of the stock market.”

I’m not saying something’s going to change on Monday with gold shares, gold shares have been going down for two months.

Maurice Jackson: You referenced Jake Bernstein’s work on the Daily Sentiment Index. What are the parameters that you referenced regarding buy and sell indicators?

Bob Moriarty: The DSI measures sentiment. Most

investor look at fundamentals, technicals, worry about the interest

rates, worry about the Fed. That’s all bull. People buy stocks because

of emotions, and they sell stocks because of emotions. If you can

measure those emotions accurately, you’d make a lot of money.

When 98 out of 100 people say something is going to go up, and it

doesn’t make any difference what it is, or what the fundamentals are, or

what the Fed does, or what the economy does, or what interest rates do,

when 98 out of 100 people say something is going to go up, the next

move is down. That is the highest number I’ve ever seen. Anything above

90 says the top is near, and anything below 10 says the bottom is near.

98 is such an extreme measure, that I’m perfectly comfortable saying

that, you and I are talking on Saturday, and on Monday, T-bonds are

going to go down.

Maurice Jackson: Mark the words, there. Which metals have your attention, and why?

Bob Moriarty: Silver and platinum, strange enough, you sent me some information (click here).

There was a fire, an explosion at a platinum processing place in South

Africa, and the real story is the price of platinum is so far below the

cost of production, they’ve got to shut production.

Nobody wants to admit this, everybody’s got their own pet theory, but

the fact is supply and demand does work. You cannot have the price of

any commodity below the cost of production for very long, or things are

going to happen. People are going to shut down production whether it’s

wheat, whether it’s gold, or anything else. The silver gold ratio got

above 100 to 1, that’s the highest it’s ever been. I think it got up to

102, intraday, a week ago. Silver was very cheap, relative to gold, but

that doesn’t mean silver couldn’t correct. I own a lot of silver, and I

own a lot of platinum, and a little bit of gold.

Posted by AGORACOM

at 11:09 AM on Thursday, March 5th, 2020

Sponsor: Loncor, a Canadian gold explorer controlling over 2,400,000 high grade ounces outside of a Barrick JV. The Ngayu JV property is 200km southwest of the Kibali gold mine, operated by Barrick, which produced 800,000 ounces of gold in 2018. Barrick manages and funds exploration at the Ngayu project until the completion of a pre-feasibility study on any gold discovery meeting their Tier One investment criteria. Newmont $NGT$NEM owns 7.8%, Resolute $RSG owns 27% Click Here for More Info

What if you gave a party and no one came? The Fed found themselves in that embarrassing position on Tuesday as they dumped a .5% drop in the Fed Funds rate onto a startled market. The market wasn’t startled at the interest rate decline, the market was startled because when the Fed spiked the punch one more time no one would drink the Kool Aid.

I’ve said for months the Fed would stick another Band-Aid on a

fatally wounded financial system yet they would fail. I felt that way

because I spent almost two years fighting a useless and pointless war.

You see we are all raised to believe that governments are all

powerful. But if you watch a squadron of 27 B-52s each loaded with 117

bombs carpet sweep an area and your enemy armed only with a bolt action

rifle gets up and shoots back at you, you begin to understand that

government only think they are all powerful. There is always a limit to

power. The Fed just reached it.

The Fed found that out on March 3rd. And it wasn’t even a tiny virus

from a laboratory in Wuhan that defeated the Fed. It was a totally

dysfunctional financial system where outright frauds such as Tesla can

double in a week.

I’ll say it again. The Everything Bubble just burst, some because of

the virus, some because of an out of balance useless financial system

and a lot because of a now broken Just in Time manufacturing system

totally dependent on China.

The metals are going to be included for a period as the margin clerks

man their phones and whisper sweet words of doom to their clients.

Everything is going to get sold. We are going into a massive period of

deflation. At the end all those million dollar MacMansions will be going

for pennies on the dollar. Gold might be $500 an ounce but will buy ten

times what it does today. We have sailed off the edge of the known

world.

I cannot predict the price of gold; many believe in error that they

can. I can just say that after many trials and tribulations the world

will realize that an honest monetary system is the only cure to what

ails us. It will include a jubilee and a metals based currency.

So it would behoove investors to be looking around for production or near production stories.

Someone came to me a week ago with a compelling story of a company

effectively off the radar screens of investors. Part of the reason is

that the founder of Loncor Resources (LN-T) Arnold Kondrat owns 29% of

the shares. Resolute Mining owns another 27% and Newmont 7.6%. With 64%

of the shares in the strongest of strong hands, there hasn’t been all

that much inclination to tell their story.

Loncor operates in the DRC, the Democratic Republic of the Congo. The

company has such a massive land position that it’s fairly hard to

understand why they have been so far off the radar of investors.

Loncor has 43-101 gold ounces of over 2.4 million. To use USD

figures, at today’s stock price Loncor is worth $19 per ounce in the

ground of gold. That no doubt will tend to set a floor under the price.

At their stage of development they should be getting more like $50-$60

USD an ounce.

It’s pretty hard to fathom the incredible size of Loncor’s land

position in the DRC. They hold 3,534 square km in the Ngayu greenstone

belt with similar endowment and geology with the greenstone belt to

their east in Tanzania home to several big gold mines. Within their

Ngayu land position they have a joint venture with Barrick on 1,894

square km of the total property. Barrick has an active trenching and

ground sampling program and is preparing to drill some of the six drill

ready targets already identified. Drilling begins this month.

The JV with Barrick is interesting. First of all, Barrick knows the

greenstone belt with big mines both in the DRC and in Tanzania. Barrick

wants at least four million ounces and would prefer high grade. Barrick

funds and runs the exploration program across the 1,894 square km all

the way to completion of a pre-feasibility study.

The DRC has a 10% carried interest and Barrick will have 65% of the

remainder with Loncor getting the remaining 35% of what is left after

the DRC gets their cut. At that point Loncor pays their own way on their

piece of the pie.

In Loncor’s fact sheet

they mention something interesting. Loncor’s Ngayu Greenstone belt is

home to a 130 km BIF. (Banded Iron Formation) Readers with a really good

memory may recall me writing about BIF

before when I was talking about where the gold showed up in the Western

Australia Pilbara Basin, also near the giant iron projects of WA.

Basically the iron was dissolved in seawater. When single cell

cyanobacteria began to produce oxygen some 3 billion years or so ago, as

the chemistry of the water changed, the iron precipitated out of

solution. Quinton Hennigh came up with the theory years ago that that is

how the world’s biggest gold properties got their gold. Gold and BIF

are similar in age and where you find one, you almost always find the

other.

Loncor is cheap. Yes, they may get cheaper but I find them attractive

enough that I bought some shares in the open market. Investors are

probably going to find it difficult to pick up a large position. The

shares pretty much trade by appointment. With a Barrick JV and with gold

in the ground at $19 an ounce in USD I don’t expect them to remain

cheap for long.

Loncor is an advertiser. I own shares. That makes me biased. I don’t

share in your gains or losses so take some responsibility for your own

trading decisions. It’s your money after all.

Posted by AGORACOM-JC

at 4:32 PM on Friday, February 28th, 2020

AGORACOM Clients Attending PDAC 2020

THEREGAL PROJECT

B.C.’s Next Premier

Silver, Lead, Zinc, Copper Deposit?

Affinity Metals holds under option, a 100% interest in the Project, located within the northern end of the prolific Kootenay Arc, a highly prospective mineralized trend.

Treaty Creeks’ GOLDSTORM zone hosts a conceptual volume of ONE BILLION TONNES rock grading close to one gram per tonne gold and is open to the north, east, and at depth. Â

A major drill program is being planned for spring to develop a resource calculation. The focus has been on the gold enriched Goldstorm Zone which is on trend with, and part of, the same geological system as Seabridge Gold’s neighboring KSM deposits.

American Creek been selected to do a formal presentation at the conference. The presentation will be held on Tuesday, March 5 at 2:00PM in room #802

HPQ Silicon Resources designs, develops, manufactures and commercializes plasma base processes

The innovative PUREVAP “Quartz Reduction Reactors†(QRR), will permit the One Step transformation of Quartz (SiO2) into High Purity Silicon (Si) at prices that will promote considerable renewable energy potential.

Lomiko hosts high-grade graphite at its La Loutre Property in Quebec. The company is working toward a Pre-Economic Assessment (PEA) that will increase its current indicated resource of 4.1 Mt of 6.5% Cg to over 10 Mt of 10%+ Cg in order to supply and develop graphite materials for the green economy.

Posted by AGORACOM

at 3:47 PM on Thursday, February 13th, 2020

Gold will outperform the S&P 500 Index in 2020. That’s one of several projections made by CLSA in its just-released “Global Surprises 2020†report.

The Hong Kong investment firm has an impressive track record when it comes to making market predictions—last year it had a 70 percent hit rate—so it may be prudent to take this one seriously.

CLSA’s

head of research Shaun Cochran: “If investors are concerned about the

role of liquidity in recent equity market strength… gold provides a

hedge that could perform across multiple scenarios.â€

Indeed, gold is one of the most liquid assets in the world with an average daily trading volume of more than $112 billion,

according to the World Gold Council (WGC). That far exceeds the Dow

Jones Industrial Average’s daily volume of approximately $23 billion.

The

yellow metal, Cochran adds, can be particularly useful in an era of

perpetually loose monetary policy: “[I]n the event that growth

disappoints the market’s expectations, gold is positively leveraged to

the inevitable policy response of lower rates and larger central bank

balance sheets.â€

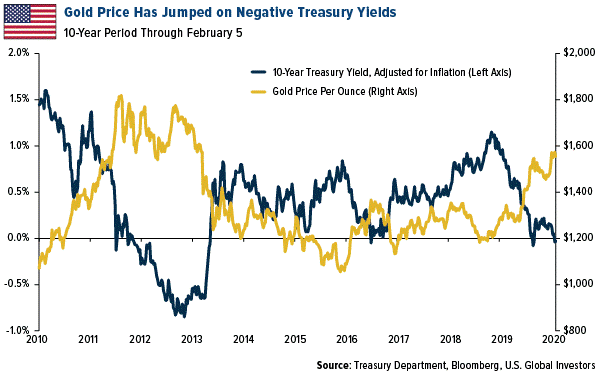

As

I’ve pointed out many times before, gold has traded inversely with

government bond yields. The recent gold rally has largely been driven by

the growing pool of negative-yielding government debt around the world,

now standing at $13 trillion. Here in the U.S., the nominal yield on

the 10-year Treasury has remained positive, but when adjusted for

inflation, it’s recently turned negative, despite a strengthening

economy. What’s more, the Federal Reserve’s balance sheet has begun to

increase again. It now holds about 30 percent of outstanding Treasury

debt, up from about 10 percent prior to the financial crisis.

I

can’t say whether gold will beat the S&P this year or next, but

what I do know is that the yellow metal has been a wise long-term

investment. For the 20-year period through the end of 2019, gold crushed

the market two-to-one, returning 451.8 percent compared to the

S&P’s 223.6 percent. That comes out to a compound annual growth rate

(CAGR) of 8.78 percent for gold, 4.03 percent for the S&P.

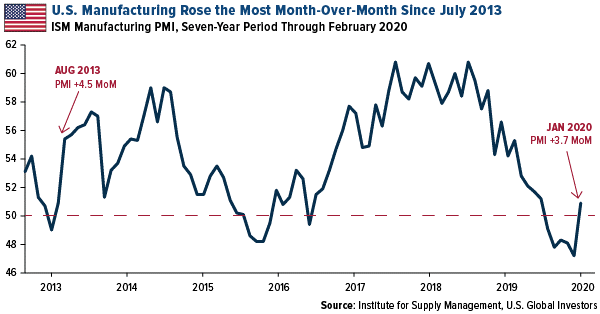

Manufacturing Turnaround Has Begun

U.S.

manufacturers started 2020 on stronger footing, a welcome turnaround

after contracting for five straight months. January’s ISM manufacturing

purchasing manager’s index (PMI) clocked in at 50.9, indicating slight

growth. Up from 47.2 in December, this represents the biggest

month-over-month jump since August 2013, when the PMI increased to 55.4

from 50.9 in July.

This

may also mark the end of the recent manufacturing bear market, prompted

by the trade war between the U.S. and China. Although relations between

the world’s two biggest superpowers remain strained, to say the least,

we’ve seen improvements lately that hint at better days. Both sides

signed a “Phase One†agreement in mid-January, and last week, China

announced it would be cutting tariffs in half on as much as $75 billion

of U.S.-imported products.

The

coronavirus is a new development that has disrupted global trade, but

there’s reason to be optimistic, as the PMI makes clear.

To read my full comments on the coronavirus, and its impact on Chinese and Hong Kong stocks, click here!

The

Dow Jones Industrial Average is a price-weighted average of 30 blue

chip stocks that are generally leaders in their industry. The S&P

500 Stock Index is a widely recognized capitalization-weighted index of

500 common stock prices in U.S. companies. The Purchasing Manager’s

Index is an indicator of the economic health of the manufacturing

sector. The PMI index is based on five major indicators: new orders,

inventory levels, production, supplier deliveries and the employment

environment. Compound annual growth rate (CAGR) is a business and

investing specific term for the geometric progression ratio that

provides a constant rate of return over the time period.

All

opinions expressed and data provided are subject to change without

notice. Some of these opinions may not be appropriate to every investor.

Some links above may be directed to third-party websites. U.S. Global

Investors does not endorse all information supplied by these websites

and is not responsible for their content.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC. This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}